The Optimal Consumption, Investment and Life Insurance for Wage Earners under Inside Information and Inflation

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Abstract

:1. Introduction

- (i)

- Solving the asset-allocation strategies for a wage earner under inside information, and analyzing the impact of inside information on asset-allocation strategies.

- (ii)

- Taking multidimensional life insurance in the insurance market into consideration.

- (iii)

- Solving the optimal inflation-indexed bond strategy. By addressing these key aspects, we aim to shed light on the intricate dynamics of consumption, investment and life-insurance decisions when individuals have access to inside information and are navigating the complexities associated with inflation.

2. Model

2.1. The Financial Market

2.2. The Income and the Insurance Market

2.3. Inside Information

2.4. The Stochastic Optimal Control Problem

- (i)

- The life-insurance purchase is -measurable and satisfies

- (ii)

- The consumption is -measurable and satisfies

- (iii)

- The investment strategies and are -measurable processes and comply with

3. Solution to the Stochastic Optimal Control Problem

- (i)

- Note that when there is no inflation in consideration, the wealth process under inside information can be expressed asThe optimal value function V under strategy satisfies the following HJB equationwhere infinitesimal generator

- (ii)

- On the other hand, when there is no inside information, the real wealth process under can be obtained asThe HJB equation corresponding to problem (4) under filtration iswhere and infinitesimal generator

4. Numerical Illustrations

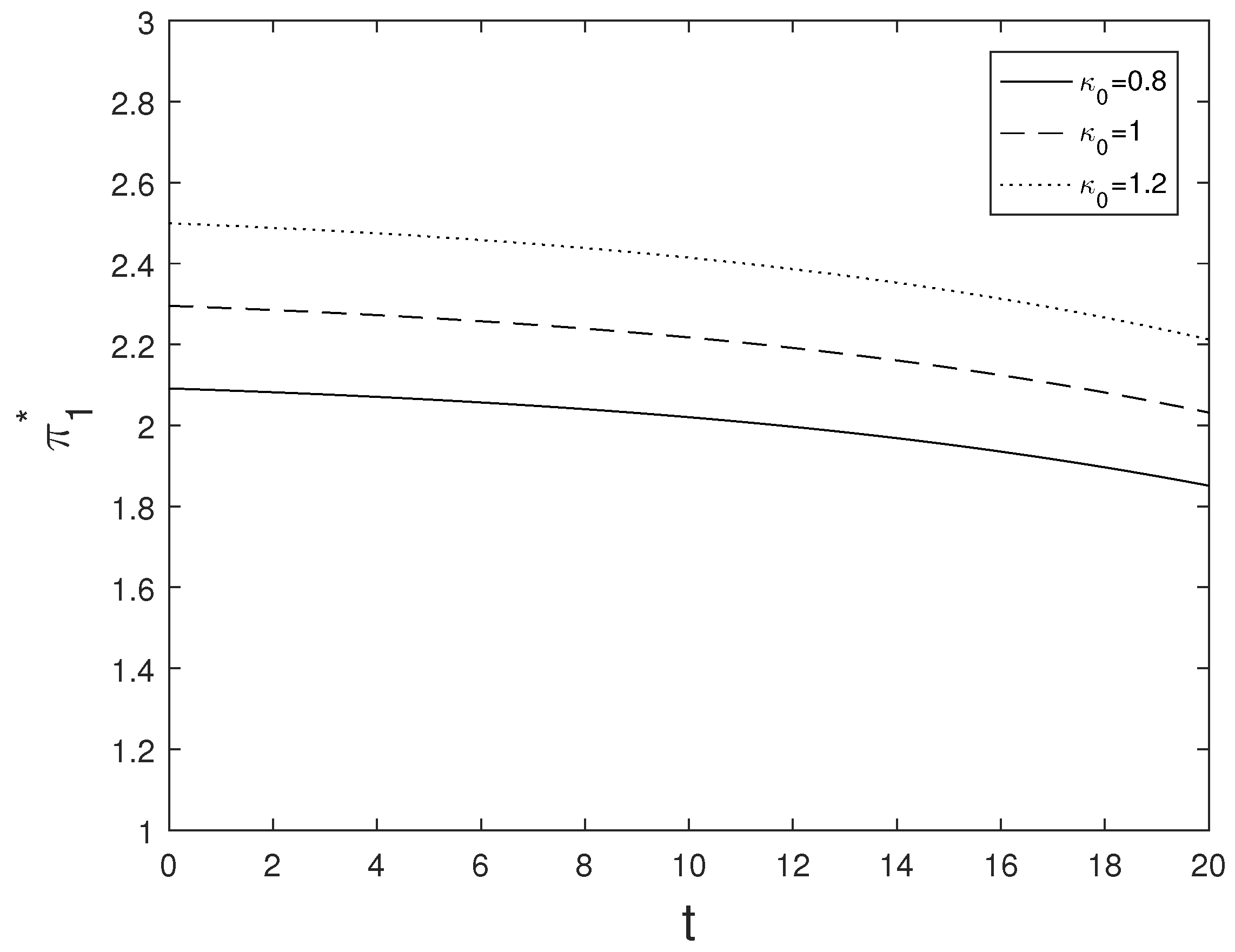

4.1. Optimal Investment Strategy

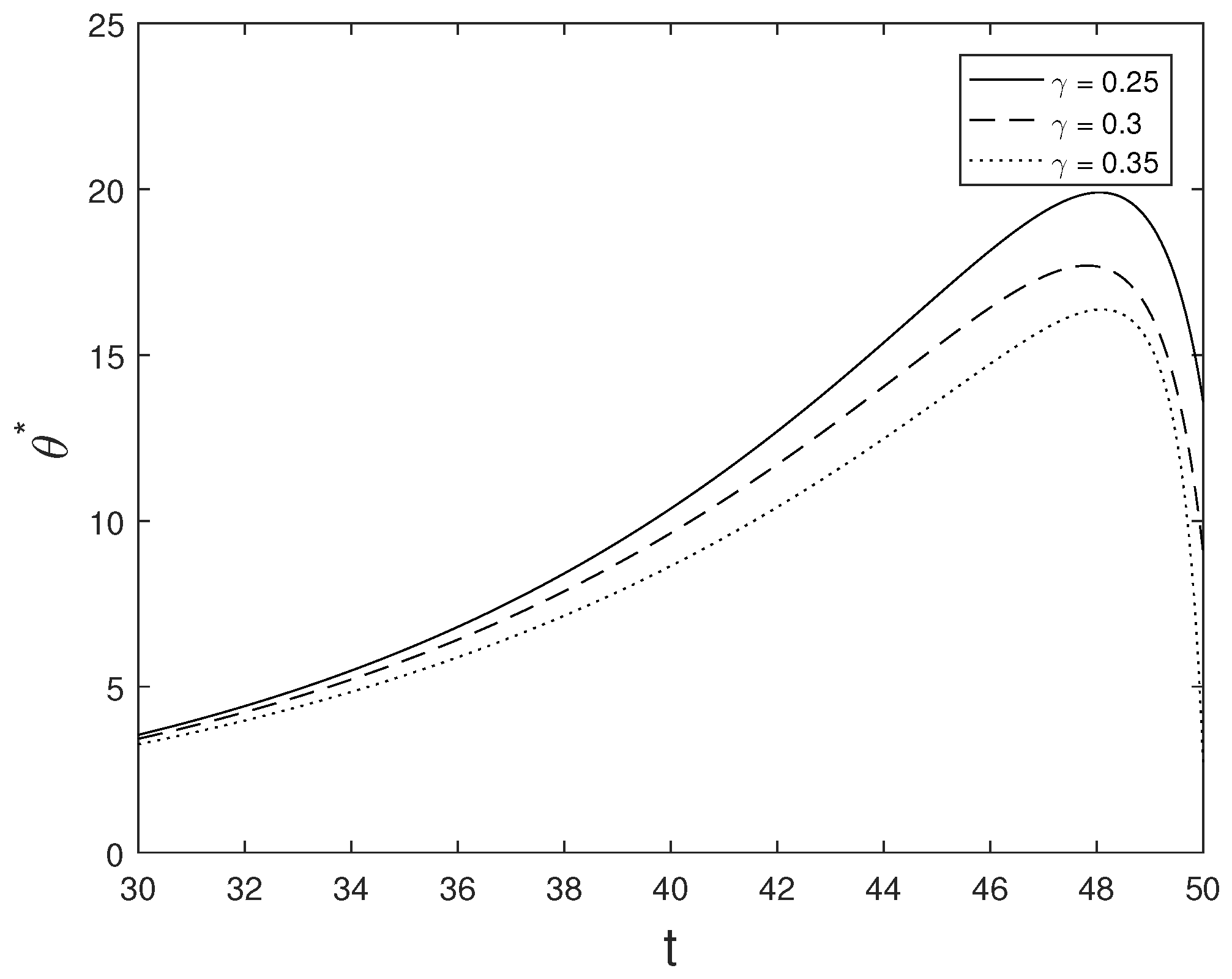

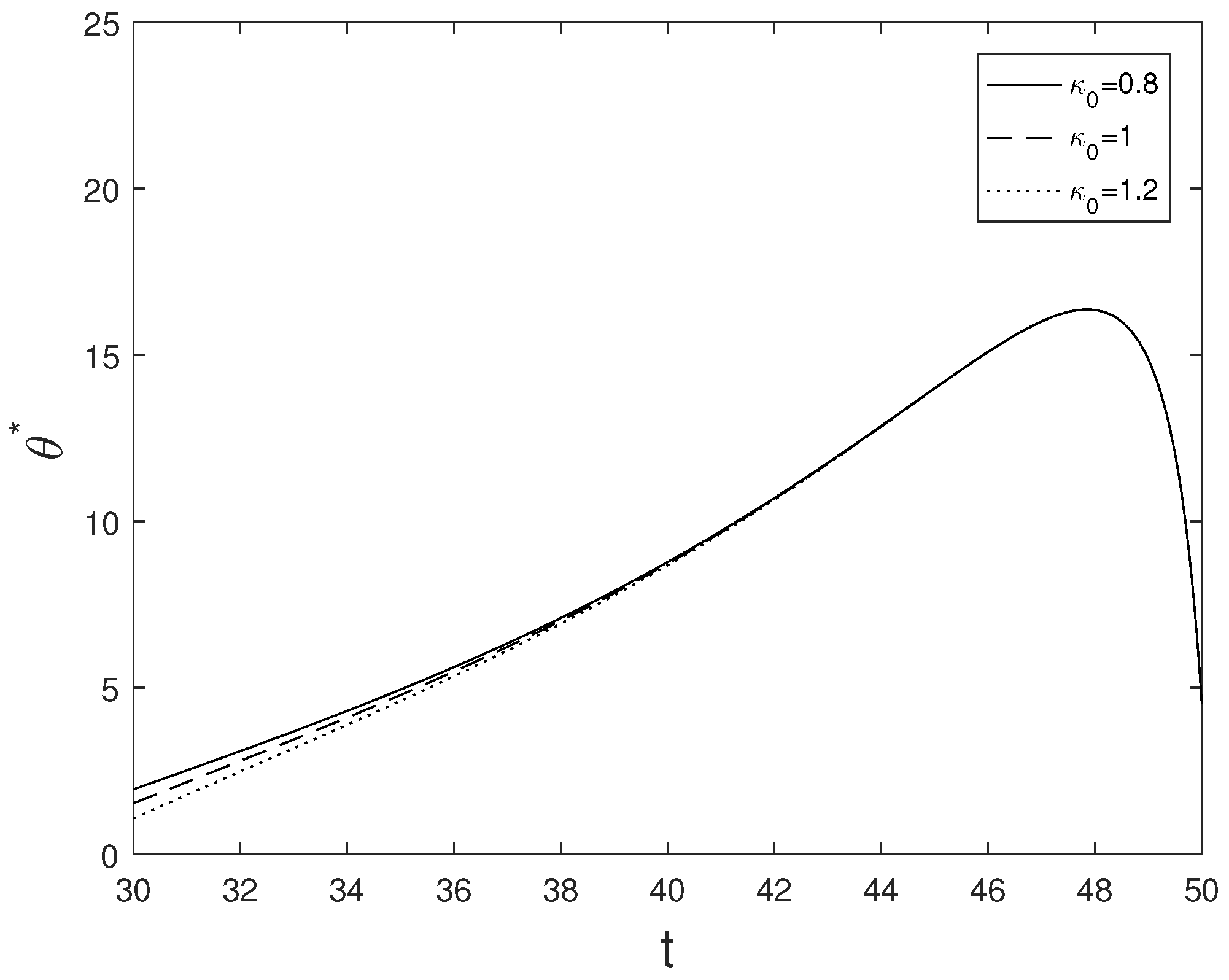

4.2. Optimal Life Insurance Strategy

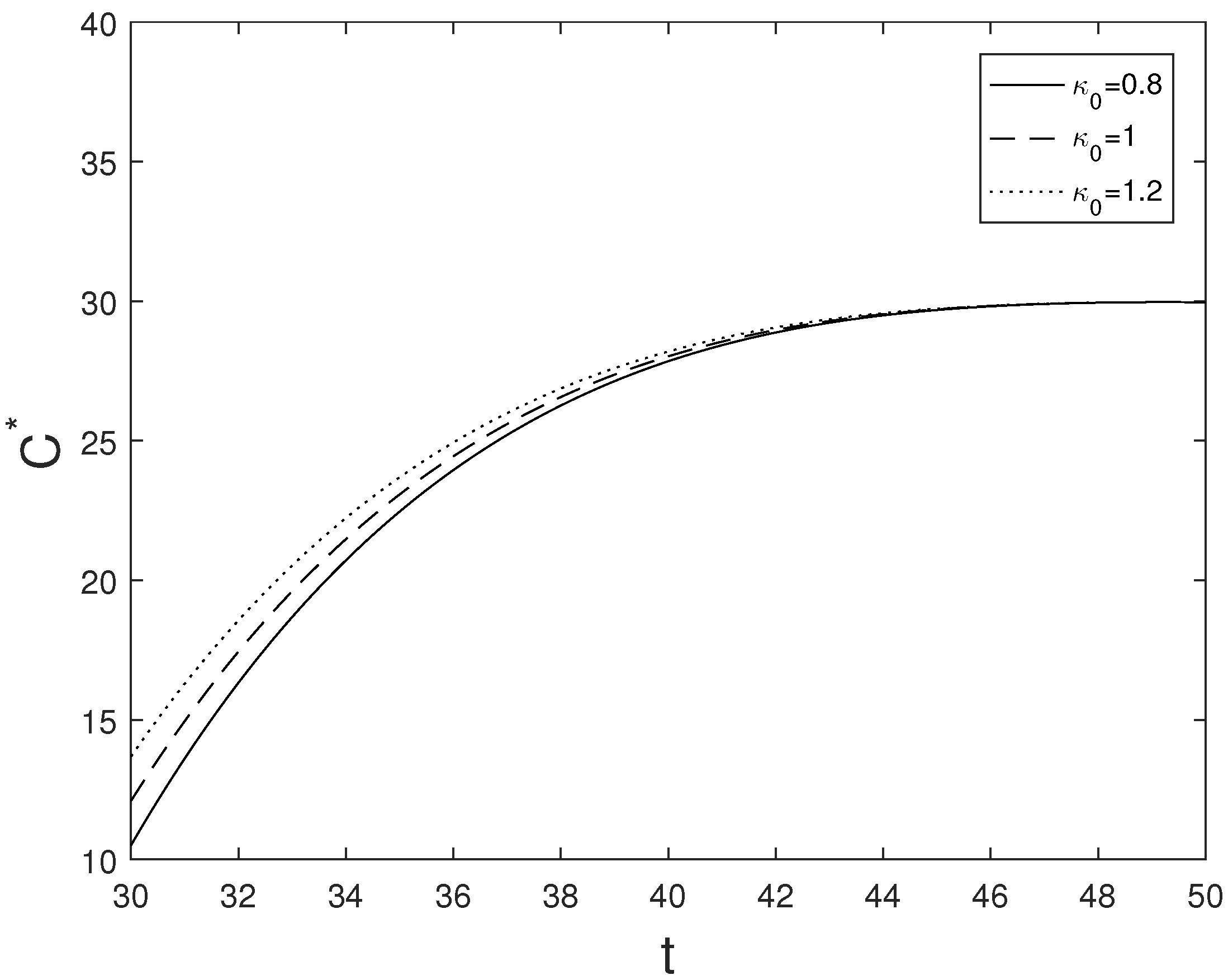

4.3. Optimal Consumption Strategy

5. Conclusions

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

References

- Merton, R.C. Lifetime Portfolio Selection under Uncertainty: The Continuous-Time Case. Rev. Econ. Stat. 1969, 51, 247–257. [Google Scholar] [CrossRef] [Green Version]

- Karatzas, I.; Lehoczky, J.P.; Sethi, S.P.; Shreve, S.E. Explicit solution of a general consumption/investment problem. Math. Oper. Res. 1986, 11, 261–294. [Google Scholar] [CrossRef]

- Fleming, W.H.; Pang, T. An application of stochastic control theory to financial economics. Siam J. Control Optim. 2004, 43, 502–531. [Google Scholar] [CrossRef] [Green Version]

- Chang, H.; Chang, K. Optimal consumption-investment strategy under the Vasicek model: HARA utility and Legendre transform. Insur. Math. Econ. 2017, 72, 215–227. [Google Scholar] [CrossRef]

- Campbell, R.A. The Demand for Life Insurance: An Application of the Economics of Uncertainty. J. Financ. 1980, 35, 1155–1172. [Google Scholar] [CrossRef]

- Richard, S.F. Optimal consumption, portfolio and life insurance rules for an uncertain lived individual in a continuous time model. J. Financ. Econ. 1975, 2, 187–203. [Google Scholar] [CrossRef]

- Pliska, S.R.; Ye, J. Optimal life-insurance purchase and consumption/investment under uncertain lifetime. J. Bank. Financ. 2007, 31, 1307–1319. [Google Scholar] [CrossRef]

- Huang, H.; Milevsky, M.A. Portfolio choice and mortality-contingent claims: The general HARA case. J. Bank. Financ. 2008, 32, 2444–2452. [Google Scholar] [CrossRef]

- Pirvu, T.A.; Zhang, H. Optimal investment, consumption and life insurance under mean-reverting returns: The complete market solution. Insur. Math. Econ. 2012, 51, 303–309. [Google Scholar] [CrossRef]

- Zeng, X.; Carsonb, J.M.; Chen, Q.; Wang, Y. Optimal life insurance with noborrowing constraints: Duality approach and example. Scand. Actuar. J. 2015, 9, 793–816. [Google Scholar]

- Wei, J.; Cheng, X.; Jin, Z.; Wang, H. Optimal consumption–investment and life-insurance purchase strategy for couples with correlated lifetimes. Insur. Math. Econ. 2020, 91, 244–256. [Google Scholar] [CrossRef]

- Wang, N.; Jin, Z.; Siu, T.K.; Qiu, M. Household consumption-investment-insurance decisions with uncertain income and market ambiguity. Scand. Actuar. J. 2021, 10, 832–865. [Google Scholar] [CrossRef]

- Mousa, A.S.; Pinheiro, D.; Pinto, A.A. Optimal life-insurance selection and purchase within a market of several life-insurance providers. Insur. Math. Econ. 2016, 67, 133–141. [Google Scholar] [CrossRef] [Green Version]

- Hoshiea, M.; Mousa, A.S.; Pinto, A.A. Optimal social welfare policy within financial and life insurance markets. Optimization 2022. [Google Scholar] [CrossRef]

- Mousa, A.S.; Pinheiro, D.; Pinheiro, S.; Pinto, A.A. Optimal consumption, investment and life-insurance purchase under a stochastically fluctuating economy. Optimization 2022, 2022, 1–41. [Google Scholar] [CrossRef]

- Kwak, M.; Lim, B.H. Optimal portfolio selection with life insurance under inflation risk. J. Bank. Financ. 2014, 46, 59–71. [Google Scholar] [CrossRef]

- Han, N.W.; Hung, M.W. Optimal consumption, portfolio and life insurance policies under interest rate and inflation risks. Insur. Math. Econ. 2017, 73, 54–67. [Google Scholar] [CrossRef]

- Liang, Z.; Zhao, X. Optimal mean-variance efficiency of a family with life insurance under inflation risk. Insur. Math. Econ. 2016, 71, 164–178. [Google Scholar] [CrossRef]

- Shi, A.; Li, X.; Li, Z. Optimal investment, consumption and life insurance choices with habit formation and inflation risk. Complexity 2022, 2022, e3440037. [Google Scholar] [CrossRef]

- Kyle, A. Continuous Auctions and Insider Trading. Econometrica 1985, 53, 1315–1335. [Google Scholar] [CrossRef] [Green Version]

- Pikovsky, I.; Karatzas, I. Anticipative portfolio optimization. Adv. Appl. Probab. 1996, 28, 1095–1122. [Google Scholar] [CrossRef]

- Imkeller, P.; Pontier, M.; Weisz, F. Free lunch and arbitrage possibilities in a financial market with an insider. Stoch. Process. Their Appl. 2001, 92, 103–130. [Google Scholar] [CrossRef] [Green Version]

- Baltas, I.D.; Frangos, N.E.; Yannacopoulos, A.N. Optimal investment and reinsurance policies in insurance markets under the effect of inside information. Appl. Stoch. Model. Bus. Ind. 2012, 8, 506–528. [Google Scholar] [CrossRef]

- Cao, J.; Peng, X.; Hu, Y. Optimal time-consistent investment and reinsurance strategy for mean-variance insurers under the inside information. Acta Math. Appl. Sin. 2016, 32, 1087–1100. [Google Scholar] [CrossRef]

- Peng, X.; Wang, W. Optimal investment and risk control for an insurer under inside information. Insur. Math. Econ. 2016, 69, 104–116. [Google Scholar] [CrossRef]

- Peng, X.; Chen, F.; Wang, W. Robust optimal investment and reinsurance for an insurer with inside information. Insur. Math. Econ. 2021, 96, 15–30. [Google Scholar] [CrossRef]

- Peng, X.; Chen, F. Mean-variance asset-liability management with inside information. Commun. Stat.—Theory Methods 2022, 51, 2281–2302. [Google Scholar] [CrossRef]

- Fleming, W.H.; Soner, H.M. Controlled Markov Processes and Viscosity Solutions, 2nd ed.; Springer: New York, NY, USA, 2006. [Google Scholar]

- Ye, J. Optimal Life Insurance Purchase, Consumption and Portfolio under an Uncertain Life. Ph.D. Thesis, University of Illinois at Chicago, Chicago, IL, USA, 2006. [Google Scholar]

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Jiao, R.; Liu, W.; Hu, Y. The Optimal Consumption, Investment and Life Insurance for Wage Earners under Inside Information and Inflation. Mathematics 2023, 11, 3415. https://doi.org/10.3390/math11153415

Jiao R, Liu W, Hu Y. The Optimal Consumption, Investment and Life Insurance for Wage Earners under Inside Information and Inflation. Mathematics. 2023; 11(15):3415. https://doi.org/10.3390/math11153415

Chicago/Turabian StyleJiao, Rui, Wei Liu, and Yijun Hu. 2023. "The Optimal Consumption, Investment and Life Insurance for Wage Earners under Inside Information and Inflation" Mathematics 11, no. 15: 3415. https://doi.org/10.3390/math11153415