Analyzing the Banking Business: Relevance of Service Value for the Satisfaction and Loyalty of Consumers

, ,

, ,

Abstract

:1. Introduction

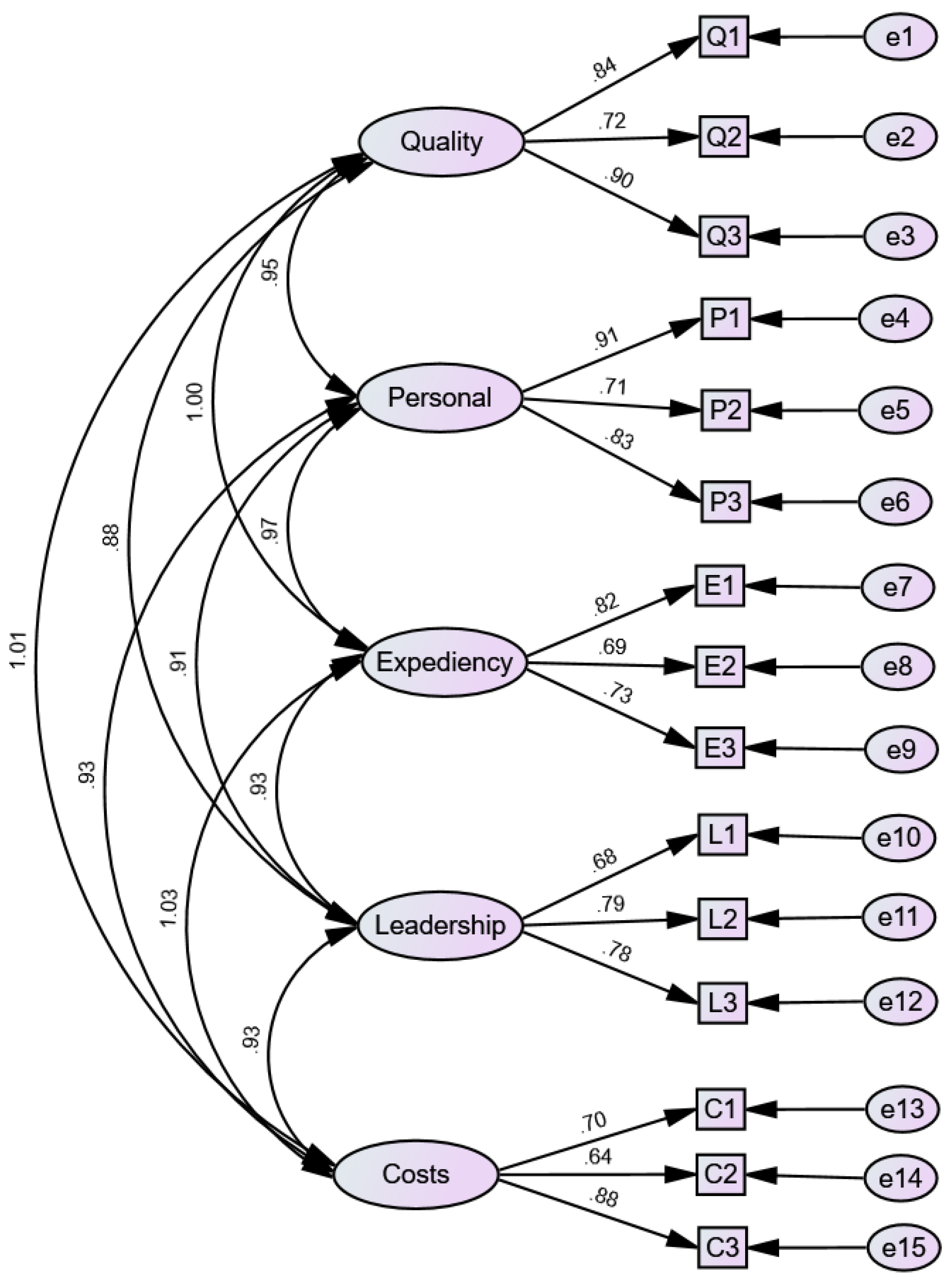

2. Materials and Methods

2.1. Quality of Banking Services

2.2. Personal Relation in Banking Services

2.3. Expediency of Banking Services

2.4. Bank Leadership

2.5. Perceived Costs of Banking Services

2.6. Satisfaction with Banking Services

2.7. Loyalty of Banking Service Users

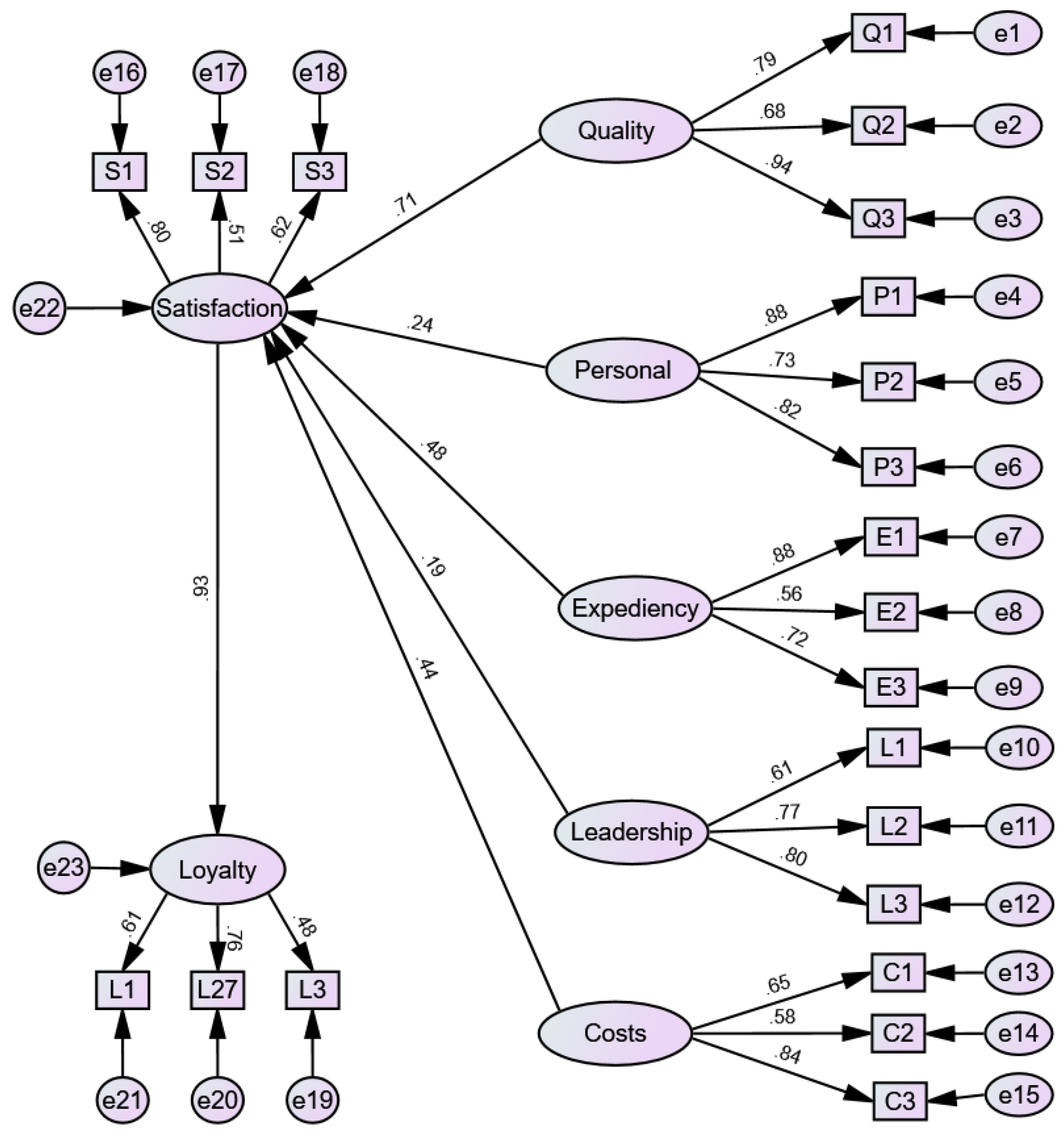

3. Results

4. Concluding Remarks and Discussion

Author Contributions

Funding

Conflicts of Interest

References

- Gallarza, M.G.; Gil-Saura, I.; Holbrook, M.B. The value of value: Further excursions on the meaning and role of customer value. J. Consum. Behav. 2011, 10, 179–191. [Google Scholar] [CrossRef]

- Garanti, Z.; Kissi, P.S. The effects of social media brand personality on brand loyalty in the Latvian banking industry. Int. J. Bank Mark. 2019, 37, 1480–1503. [Google Scholar] [CrossRef]

- Akhgari, M.; Bruning, E.R.; Finlay, J.; Bruning, N.S. Image, performance, attitudes, trust, and loyalty in financial services. Int. J. Bank Mark. 2017, 36, 744–763. [Google Scholar] [CrossRef]

- Boonlertvanich, K. Service quality, satisfaction, trust, and loyalty: The moderating role of main-bank and wealth status. Int. J. Bank Mark. 2018, 37, 278–302. [Google Scholar] [CrossRef]

- Tseng, L.M. How customer orientation leads to customer satisfaction. Int. J. Bank Mark. 2018, 37, 210–225. [Google Scholar] [CrossRef]

- Ponnam, A.; Paul, R. Relative importance of service value by customer relationship stages—Evidence from the Indian retail banking. Int. J. Bank Mark. 2016, 35, 319–334. [Google Scholar] [CrossRef]

- Vera, J.; Trujillo, A. Service quality dimensions and superior customer perceived value in retail banks: An empirical study on Mexican consumers. J. Retail. Consum. Serv. 2013, 20, 579–586. [Google Scholar] [CrossRef]

- Yilmaz, V.; Ari, E.; Gurbuz, H. Investigating the relationship between service quality dimensions, customer satisfaction and loyalty in Turkish banking sector—An application of structural equation model. Int. J. Bank Mark. 2017, 36, 423–440. [Google Scholar] [CrossRef]

- Popović Šević, N.; Slijepčević, M.; Šević, A. Strengthening E-services as a New Identity Paradigm in Serbian Retail Banking During COVID-19. LIMES+ 2021, 1, 97–122. [Google Scholar]

- Slijepčević, M.; Popović Šević, N.; Radojević, I.; Šević, A. Relative Importance of Neuromarketing in Support of Banking Service Users. Marketing 2022, 53, 131–143. [Google Scholar]

- Slijepčević, M.; Popović Šević, N.; Popović Pantić, S.; Šević, A. Investigating the Relationship between Quality, Loyalty, and Personal Relationship in the Banking Sector: An Analysis of Micro, Small and Medium-Sized Enterprises in Serbia. Ekon. Preduz. 2022, 70, 215–230. [Google Scholar] [CrossRef]

- Satar, M.; Safie, N.; Yusnorizam, M. Customer Value Proposition for E-Commerce: A Case Study Approach International. J. Adv. Comput. Sci. Appl. 2019, 10, 454–458. [Google Scholar] [CrossRef]

- Matarazzo, M.; Penco, L.; Profumo, G.; Quaglia, R. Digital transformation and customer value creation in Made in Italy SMEs: A dynamic capabilities perspective. J. Bus. Res. 2021, 123, 642–656. [Google Scholar] [CrossRef]

- Bucea-Manea-Țoniş, R.; Šević, A.; Ilić, M.P.; Bucea-Manea-Țoniş, R.; Popović Šević, N.; Mihoreanu, L. Untapped Aspects of Innovation and Competition within a European Resilient Circular Economy. A Dual Comparative Study. Sustainability 2021, 13, 8290. [Google Scholar] [CrossRef]

- Carranza, R.; Díaz, E.; Sánchez-Camacho, C.; Martín-Consuegra, D. E-Banking Adoption: An Opportunity for Customer Value Co-Creation. Front. Psychol. 2021, 11, 621248. [Google Scholar] [CrossRef]

- Haro-de-Rosario, A.; Saraite, L.; Saez-Martin, A. The impact of social media on customer engagement with US banks. In Social Media Marketing: Breakthroughs in Research and Practice; Kardes, M., Clark, S., Eds.; IGI Global: Hershey, PA, USA, 2018; Volume 2, pp. 774–788. [Google Scholar]

- Wang, G.; Miao, C.F. Effects of sales force market orientation on creativity, innovation implementation, and sales performance. J. Bus. Res. 2015, 68, 2374–2382. [Google Scholar] [CrossRef]

- Severović, K.; Žajdala, N.; Cvetković Šoštarić, B. Conceptual model as a tool for managing the quality of banking services. Econ. Gaz. 2009, 22, 147–160. [Google Scholar]

- Marinković, V.; Senić, V. Analysis of the elements of service quality in corporate banking. Ekon. Horiz. 2012, 14, 13–22. [Google Scholar]

- Babić-Hodović, V.; Mehić, E. Influence of Buyers’ Expectations towards Perceived Quality of Services—Example of Banking Services in Bosnia and Herzegovina. In Proceedings of the 4th Research/Expert Conference with International Participation, Fojnica, Zenica, Bosnia and Herzegovina, 9–12 November 2005; Faculty of Mechanical Engineering: Zenica, Bosnia and Herzegovina, 2005; pp. 179–187. [Google Scholar]

- Dang, T.T.; Pham, A.D. What make banks’ front-line staff more customer oriented? The role of interactional justice. Int. J. Bank Mark. 2020, 38, 777–798. [Google Scholar] [CrossRef]

- Kamarudin, A.A.; Kassim, S. An analysis of customer satisfaction on employee professionalism: A comparison between Islamic and conventional banks in Malaysia. J. Islam. Mark. 2020, 12, 1854–1871. [Google Scholar] [CrossRef]

- Demerouti, E.; Xanthopoulou, D.; Bakker, A.B. How do cynical employees serve their customers? A multi-method study. Eur. J. Work Organ. Psychol. 2018, 27, 16–27. [Google Scholar] [CrossRef] [Green Version]

- Japutra, A.; Molinillo, S. Responsible and active brand personality: On the relationships with brand experience and key relationship constructs. J. Bus. Res. 2017, 99, 464–471. [Google Scholar] [CrossRef]

- Gordon, R.; Zainuddin, N.; Magee, C. Unlocking the potential of branding in social marketing services: Utilising brand personality and brand personality appeal. J. Serv. Mark. 2016, 3, 48–62. [Google Scholar] [CrossRef]

- Edwards, A.; Edwards, C.; Wahl, S.T.; Myers, S.A. The Communication Age: Connecting and Engaging; Sage Publications: Thousand Oaks, CA, USA, 2019. [Google Scholar]

- Van Tonder, E.; Petzer, D.J.; van Vuuren, N.; de Beer, L. Perceived value, relationship quality and positive WOM intention in banking. Int. J. Bank Mark. 2018, 36, 1347–1366. [Google Scholar] [CrossRef]

- Paul, J.; Mittal, A.; Srivastav, G. Impact of service quality on customer satisfaction in private and public sector banks. Int. J. Bank Mark. 2016, 34, 606–622. [Google Scholar] [CrossRef]

- Terho, H.; Eggert, A.; Haas, A.; Ulaga, W. How sales strategy translates into performance: The role of salesperson customer orientation and value-based selling. Ind. Mark. Manag. 2015, 45, 12–21. [Google Scholar] [CrossRef]

- Frambach, R.T.; Fiss, P.C.; Ingenbleek, P.T. How important is customer orientation for firm performance? A fuzzy set analysis of orientations, strategies, and environments. J. Bus. Res. 2016, 69, 1428–1436. [Google Scholar] [CrossRef]

- Eriksson, K.; Hermansson, C. How relationship attributes affect bank customers’ saving. Int. J. Bank Mark. 2018, 37, 156–170. [Google Scholar] [CrossRef]

- Marinović Matović, I.; Pavlović, M.; Vemić Đurković, J. Effect of short-term incentives on manager s motivation: A case study of Serbian banking sector. EMC Rev. 2021, 11, 336–347. [Google Scholar] [CrossRef]

- Neacşu, N.A. The customer-oriented strategy—A tool for increasing customer satisfaction on the Romanian banking market. Bull. Transilv. Univ. Brasov Ser. V Econ. Sci. 2020, 13, 49–56. [Google Scholar] [CrossRef]

- Zietsman, M.L.; Mostert, P.; Svensson, G. Perceived price and service quality as mediators between price fairness and perceived value in business banking relationships—A micro-enterprise perspective. Int. J. Bank Mark. 2019, 37, 2–19. [Google Scholar] [CrossRef] [Green Version]

- Kaura, V.; Prasad, C.S.D.; Sharma, S. Impact of service quality, service convenience and perceived price fairness on customer satisfaction in Indian retail banking sector. Manag. Labour Stud. 2014, 39, 127–139. [Google Scholar] [CrossRef]

- Kim, S.H.; Kim, M.; Holland, S. How customer personality trait influence brand loyalty in the coffee shop industry: The moderating role of business types. Int. J. Hosp. Tour. Adm. 2018, 19, 311–335. [Google Scholar] [CrossRef]

- Ojeme, M.; Robson, A.; Coates, N. Investigating the Nigerian small and medium enterprises (SMEs)—Banking long-term relationship building. Int. J. Bank Mark. 2018, 36, 89–110. [Google Scholar] [CrossRef]

- Djikanovic, Z.; Drakic-Grgur, M. Globalizacija i digitalizacija bankarskih usluga. In Globalizacija i Izolacionizam; Vukotić, V.Š., Ed.; Centar za Ekonomska Istraživanja Instituta Društvenih Nauka: Belgrade, Serbia, 2017; pp. 107–115. [Google Scholar]

- Aksoy, L. Linking satisfaction to share of deposits: An application of the Wallet Allocation Rule. Int. J. Bank Mark. 2014, 32, 28–42. [Google Scholar] [CrossRef]

- Atorough, P.; Salem, H. A framework for understanding the evolution of relationship quality and the customer relationship development process. J. Financ. Serv. Mark. 2016, 21, 267–283. [Google Scholar] [CrossRef] [Green Version]

- De Leon, M.; Atienza, R.P.; Susilo, D. Influence of self-service technology (SST) service quality dimensions as a second-order factor on perceived value and customer satisfaction in a mobile banking application. Cogent Bus. Manag. 2020, 1, 1794241. [Google Scholar] [CrossRef]

- Khatoon, S.; Zhengliang, X.; Hussain, H. The Mediating Effect of Customer Satisfaction on the Relationship between Electronic Banking Service Quality and Customer Purchase Intention: Evidence from the Qatar Banking Sector. SAGE Open 2020, 10, 21582440209. [Google Scholar] [CrossRef]

- Salimon, M.; Yusoff, R.; Mokhtar, S. The mediating role of hedonic motivation on the relationship between adoption of e-banking and its determinants. Int. J. Bank Mark. 2017, 35, 558–582. [Google Scholar] [CrossRef]

- Raza, S.A.; Umer, A.; Qureshi, M.A.; Dahri, A.S. Internet banking service quality, e-customer satisfaction and loyalty: The modified e-SERVQUAL model. TQM J. 2020, 32, 1443–1466. [Google Scholar] [CrossRef]

- Waheed Siyal, A.; Donghong, D.; Ali Umrani, W.; Siyal, S.; Bhand, S. Predicting Mobile Banking Acceptance and Loyalty in Chinese Bank Customers. SAGE Open 2019, 9, 2158244019844084. [Google Scholar]

- Roblek, V.; Meško, M.; Krapež, A. A Complex View of Industry 4.0. SAGE Open 2016, 6, 2158244016653987. [Google Scholar] [CrossRef] [Green Version]

- Monferrer, D.; Moliner, M.A.; Estrada, M. Increasing customer loyalty through customer engagement in the retail banking industry. Span. J. Mark. ESIC 2019, 23, 461–484. [Google Scholar] [CrossRef]

- Ong, K.S.; Nguyen, B.; Syed Alwi, S.F. Consumer-based virtual brand personality (CBVBP), customer satisfaction and brand loyalty in the online banking industry. Int. J. Bank Mark. 2017, 35, 370–390. [Google Scholar] [CrossRef]

- Khadim, R.A.; Hanan, M.A.; Arshad, A.; Saleem, N. Revisiting antecedents of brand loyalty: Impact of perceived social media communication with brand trust and brand equity as mediators. Acad. Strateg. Manag. J. 2018, 17, 1–15. [Google Scholar]

- Foroudi, P.; Jin, Z.; Gupta, S.; Foroudi, M.M. Perceptional components of brand equity: Configuring the symmetrical and asymmetrical paths to brand loyalty and brand purchase intention. J. Bus. Res. 2018, 89, 462–474. [Google Scholar] [CrossRef]

- Wahyuni, S.; Fitriani, N. Brand religiosity aura and brand loyalty in Indonesia Islamic Banking. J. Islam. Mark. 2017, 8, 361–372. [Google Scholar] [CrossRef]

- Nikhashemi, S.R.; Valaei, N. The chain of effects from brand personality and functional congruity to stages of brand loyalty: The moderating role of gender. Asia Pac. J. Mark. Logist. 2018, 30, 84–105. [Google Scholar] [CrossRef]

- Hair, F.J.; Sarstedt, M.; Hopkins, L.; Kuppelwies, R. Partial least squares structural equation modelling (PLS-SEM): An emerging tool in business research. Eur. Bus. Rev. 2014, 26, 106–121. [Google Scholar] [CrossRef]

- Schermelleh-Engel, K.; Mossbrugger, H.; Muller, H. Evaluating the fit of structural equation models: Test of significance and descriptive goodness of fit measures. Methods Psychol. Res. Online 2003, 8, 23–74. [Google Scholar]

- Makanyeza, C.; Chikazhe, L. Mediators of the Relationship between Service Quality and Customer Loyalty: Evidence from the Banking Sector in Zimbabwe. Int. J. Bank Mark. 2017, 35, 540–556. [Google Scholar] [CrossRef]

- Urikova, O.; Ivanochko, I.; Kryvinska, N.; Strauss, C.; Zinterhof, P. Consideration of Aspects Affecting the Evolvement of Collaborative eBusiness in Service Organizations. Int. J. Serv. Econ. Manag. 2013, 5, 72–92. [Google Scholar]

- Fauska, P.; Kryvinska, N.; Strauss, C. The role of e-commerce in B2B markets of goods and services. Int. J. Serv. Econ. Manag. 2013, 5, 41–71. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Sample Data Gender | Male | 76 | 27% |

| Female | 205 | 73% | |

| Education | Postgraduate | 58 | 21% |

| Graduate | 176 | 63% | |

| High School | 43 | 15% | |

| Other | 4 | 1% | |

| Firm size | Micro | 152 | 54% |

| Small | 87 | 31% | |

| Mid-size | 31 | 11% | |

| Large | 11 | 4% | |

| Firm location | Belgrade | 191 | 68% |

| Inner Serbia | 53 | 19% | |

| Vojvodina | 37 | 13% |

| Factor | Items | Mean | St. Dev. | Item-Total Correlation | Cronbach’s Alpha | AVE | CR |

|---|---|---|---|---|---|---|---|

| Quality | The selected bank is responsible, secure and consistent in providing its services. | 3.886 | 1.150 | 0.707 | 0.841 | 0.760 | 0.905 |

| The chosen bank provides me with a superior service. | 3.598 | 1.195 | 0.631 | ||||

| The overall quality provided to me by the chosen bank is excellent. | 3.701 | 1.258 | 0.788 | ||||

| Personal Relationship | The chosen bank always offers me products and services that best suit my needs. | 3.498 | 1.296 | 0.765 | 0.847 | 0.766 | 0.908 |

| I have certain benefits when using the services of the chosen bank, which many users do not get. | 2.982 | 1.475 | 0.661 | ||||

| In a problematic situation, the chosen bank always shows sincere interest and helps to find a solution. | 3.505 | 1.312 | 0.711 | ||||

| Expediency | Selected bank always fulfills its promises. | 3.505 | 1.301 | 0.687 | 0.757 | 0.675 | 0.861 |

| The selected bank performs all its transactions safely and in a short time. | 4.110 | 1.101 | 0.501 | ||||

| The efficient behaviour of the employees in the chosen bank gives me additional confidence. | 3.587 | 1.285 | 0.596 | ||||

| Leadership Role | The selected bank uses the most modern technology to provide its services. | 3.782 | 1.035 | 0.534 | 0.768 | 0.684 | 0.866 |

| The chosen bank always informs me about new banking products and services. | 3.897 | 1.342 | 0.642 | ||||

| The selected bank regularly informs me about its products and services that are in line with my income and property status. | 3.352 | 1.336 | 0.645 | ||||

| Perceived costs | The selected bank charges the correct service costs for its services. | 3.260 | 1.279 | 0.554 | 0.734 | 0.654 | 0.850 |

| The selected bank regularly informs me about price changes of all its services. | 4.036 | 1.267 | 0.510 | ||||

| The service I receive from the chosen bank is of an extremely high standard | 3.708 | 1.242 | 0.610 | ||||

| Satisfaction | I am satisfied with all the services that the selected bank provides. | 3.744 | 1.241 | 0.794 | 0.851 | 0.771 | 0.910 |

| The services of the chosen bank, as well as the services rendered by bank clerks, exceed all my expectations. | 3.217 | 1.262 | 0.650 | ||||

| The selected bank never disappointed me. | 3.317 | 1.430 | 0.719 | ||||

| Loyalty | I think it is a wise decision to have a bank account with the chosen bank, although I am aware that not all banks have the same terms of cooperation. | 3.737 | 1.172 | 0.689 | 0.831 | 0.748 | 0.899 |

| I will always recommend my chosen bank. | 3.722 | 1.263 | 0.751 | ||||

| When selecting banks, I will always give priority to the selected bank. | 3.794 | 1.201 | 0.635 |

| Hypothesis | Coefficient | p-Value | |

|---|---|---|---|

| H1: Quality→Satisfaction | 0.712 | 0.040 | Supported |

| H2: Personal Relations→Satisfaction | 0.237 | 0.023 | Supported |

| H3: Expediency→Satisfaction | 0.476 | 0.028 | Supported |

| H4: Leadership→Satisfaction | 0.189 | 0.045 | Supported |

| H5: Costs→Satisfaction | 0.438 | 0.043 | Supported |

| H6: Satisfaction→Loyalty | 0.928 | 0.092 | Weakly Supported |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Šević, A.; Zečar, J.; Nešić Tomašević, A.; Popović Šević, N.; Slijepčević, M.; Dudić, B. Analyzing the Banking Business: Relevance of Service Value for the Satisfaction and Loyalty of Consumers. Mathematics 2022, 10, 4645. https://doi.org/10.3390/math10244645

Šević A, Zečar J, Nešić Tomašević A, Popović Šević N, Slijepčević M, Dudić B. Analyzing the Banking Business: Relevance of Service Value for the Satisfaction and Loyalty of Consumers. Mathematics. 2022; 10(24):4645. https://doi.org/10.3390/math10244645

Chicago/Turabian StyleŠević, Aleksandar, Jelena Zečar, Ana Nešić Tomašević, Nevenka Popović Šević, Milica Slijepčević, and Branislav Dudić. 2022. "Analyzing the Banking Business: Relevance of Service Value for the Satisfaction and Loyalty of Consumers" Mathematics 10, no. 24: 4645. https://doi.org/10.3390/math10244645