Market Reaction to Corporate Releases and News Articles: Evidence from Thailand’s Stock Market

Abstract

:1. Introduction

2. Literature Review

3. The Stock Exchange of Thailand

- Information that could have a significant impact on a company’s securities and their market price.

- Information that may impact investment decisions regarding the company’s securities.

- Information that may affect the interests of shareholders.

4. The Data Set

5. Empirical Tests

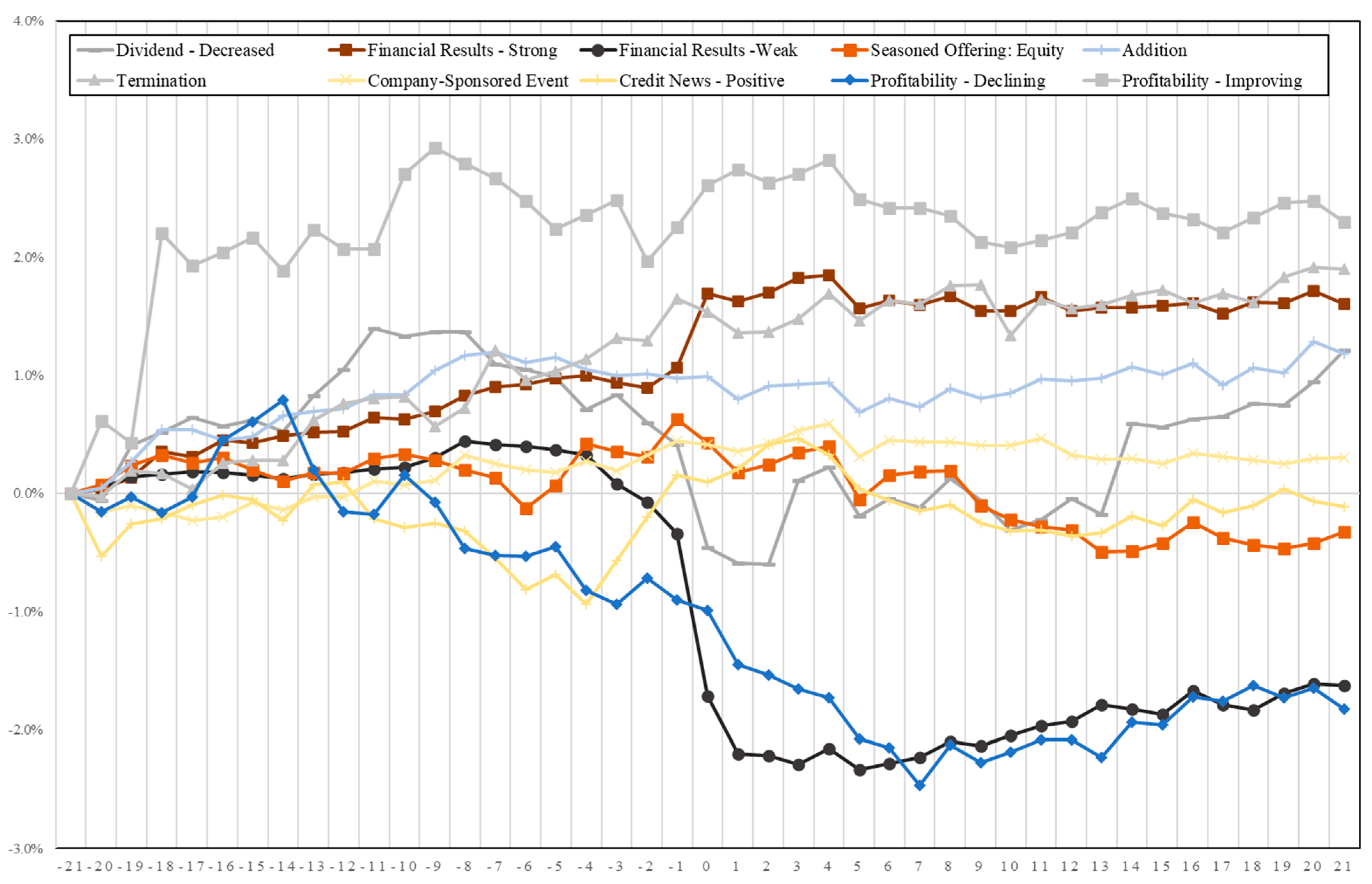

6. Event Study Results

6.1. Empirical Results

- (a)

- Dividend and Financial News

- (b)

- Strategy and performance

- (c)

- Other news categories

6.2. Longer Event Window

6.2.1. Corporate Press Releases

6.2.2. News Articles

7. Conclusions

Author Contributions

Funding

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

| 1 | CG Watch 2020, published by the Asian Corporate Governance Association. |

| 2 | The Global Competitiveness Report 2017–2018, published by the World Economic Forum. |

References

- Ahern, Kenneth R., and Denis Sosyura. 2014. Who writes the news? Corporate press releases during merger negotiations. The Journal of Finance 69: 241–91. [Google Scholar] [CrossRef]

- Ahmad, Khurshid, JingGuang Han, Elaine Hutson, Colm Kearney, and Sha Liu. 2016. Media-expressed negative tone and firm-level stock returns. Journal of Corporate Finance 37: 152–72. [Google Scholar] [CrossRef]

- Akerlof, George A. 1978. The market for “lemons”: Quality uncertainty and the market mechanism. In Uncertainty in Economics. Cambridge: Academic Press, pp. 235–51. [Google Scholar]

- Akerlof, George A., and Robert J. Shiller. 2010. Animal Spirits: How Human Psychology Drives the Economy, and Why It Matters for Global Capitalism. Princeton: Princeton University Press. [Google Scholar]

- Antweiler, Werner, and Murray Z. Frank. 2006. Do US Stock Markets Typically Overreact to Corporate News Stories? Available online: https://ssrn.com/abstract=878091 (accessed on 17 August 2023).

- Asquith, Paul, and David W. Mullins Jr. 1986. Signalling with Dividends, Stock Repurchases, and Equity Issues. Financial Management 15: 27–44. [Google Scholar] [CrossRef]

- Atiase, Rowland K., Haidan Li, Somchai Supattarakul, and Senyo Tse. 2005. Market reaction to multiple contemporaneous earnings signals: Earnings announcements and future earnings guidance. Review of Accounting Studies 10: 497–525. [Google Scholar] [CrossRef]

- Baker, Malcolm, and Jeffrey Wurgler. 2007. Investor sentiment in the stock market. Journal of Economic Perspectives 21: 129–51. [Google Scholar] [CrossRef]

- Ball, Ray, and Philip Brown. 1968. An Empirical Evaluation of Accounting Income Numbers. Journal of Accounting Research 6: 159–78. [Google Scholar] [CrossRef]

- Bao, Dichu, Yongtae Kim, G. Mujtaba Mian, and Lixin Su. 2019. Do managers disclose or withhold bad news? Evidence from short interest. The Accounting Review 94: 1–26. [Google Scholar]

- Barber, Brad M., and Terrance Odean. 2008. All that glitters: The effect of attention and news on the buying behavior of individual and institutional investors. The Review of Financial Studies 21: 785–818. [Google Scholar] [CrossRef]

- Barberis, Nicholas, and Richard Thaler. 2003. A survey of behavioral finance. Handbook of the Economics of Finance 1: 1053–128. [Google Scholar]

- Begley, Joy, and Paul E. Fischer. 1998. Is there information in an earnings announcement delay? Review of Accounting Studies 3: 347–63. [Google Scholar] [CrossRef]

- Below, Scott D., and Keith H. Johnson. 1996. An analysis of shareholder reaction to dividend announcements in bull and bear markets. Journal of Financial and Strategic Decisions 9: 15–26. [Google Scholar]

- Bing, Li, Keith C. C. Chan, and Carol Ou. 2014. Public sentiment analysis in twitter data for prediction of a company’s stock price movements. Paper presented at 2014 IEEE 11th International Conference on e-Business Engineering, Guangzhou, China, November 5–7; pp. 232–39. [Google Scholar]

- Birz, Gene. 2017. Stale economic news, media and the stock market. Journal of Economic Psychology 61: 87–102. [Google Scholar] [CrossRef]

- Bollen, Johan, Huina Mao, and Xiaojun Zeng. 2011. Twitter mood predicts the stock market. Journal of Computational Science 2: 1–8. [Google Scholar] [CrossRef]

- Botosan, Christine A. 1997. Disclosure level and the cost of equity capital. Accounting Review 72: 323–49. [Google Scholar]

- Boudoukh, Jacob, Ronen Feldman, Shimon Kogan, and Matthew Richardson. 2019. Information, trading, and volatility: Evidence from firm-specific news. Review of Financial Studies 32: 992–1033. [Google Scholar] [CrossRef]

- Chambers, Anne E., and Stephen H. Penman. 1984. Timeliness of reporting and the stock price reaction to earnings announcements. Journal of Accounting Research 2: 21–47. [Google Scholar] [CrossRef]

- Chan, Wesley S. 2003. Stock price reaction to news and no-news: Drift and reversal after headlines. Journal of Financial Economics 70: 223–60. [Google Scholar] [CrossRef]

- Charitou, Melita, Andreas Patis, and Adamos Vlittis. 2010. The market reaction to the appointment of an outside CEO: An empirical investigation. Journal of Economics and International Finance 2: 272–77. [Google Scholar]

- Christensen, Theodore E., Toni Q. Smith, and Pamela S. Stuerke. 2004. Public pre-disclosure information, firm size, analyst following, and market reactions to earnings announcements. Journal of Business Finance & Accounting 31: 951–84. [Google Scholar]

- Chuthanondha, Siriyos. 2020. Do managements tell us the whole truth and nothing but the truth? Impact of textual sentiment in financial disclosure to future firm performance and market response in Thailand. International Journal of Monetary Economics and Finance 13: 244–52. [Google Scholar] [CrossRef]

- Dellavigna, Stefano, and Joshua M. Pollet. 2009. Investor inattention and friday earnings announcements. Journal of Finance 64: 709–49. [Google Scholar] [CrossRef]

- Diamond, Douglas W. 1984. Financial intermediation and delegated monitoring. The Review of Economic Studies 51: 393–414. [Google Scholar] [CrossRef]

- Dougal, Casey, Joseph Engelberg, Diego Garcia, and Christopher A. Parsons. 2012. Journalists and the Stock Market. Review of Financial Studies 25: 639–79. [Google Scholar] [CrossRef]

- Doyle, Jeffrey T., and Matthew J. Magilke. 2009. The timing of earnings announcements: An examination of the strategic disclosure hypothesis. Accounting Review 84: 157–82. [Google Scholar] [CrossRef]

- Du, Shuili, and Kun Yu. 2021. Do corporate social responsibility reports convey value relevant information? Evidence from report readability and tone. Journal of Business Ethics 172: 253–74. [Google Scholar] [CrossRef]

- Easley, David, and Jon Kleinberg. 2010. Networks, Crowds, and Markets: Reasoning about a Highly Connected World. Cambridge: Cambridge University Press, vol. 1. [Google Scholar]

- Easley, David, Nicholas M. Kiefer, Maureen O’hara, and Joseph B. Paperman. 1996. Liquidity, information, and infrequently traded stocks. The Journal of Finance 51: 1405–36. [Google Scholar] [CrossRef]

- Engelberg, Joseph E., and Christopher A. Parsons. 2011. The Causal Impact of Media in Financial Markets. The Journal of Finance 66: 67–97. [Google Scholar] [CrossRef]

- Fama, Eugene F., Lawrence Fisher, Michael C. Jensen, and Richard Roll. 1969. The adjustment of stock prices to new information. International Economic Review 10: 1–21. [Google Scholar] [CrossRef]

- Fang, Lily, and Joel Peress. 2009. Media coverage and the cross-section of stock returns. Journal of Finance 64: 2023–52. [Google Scholar] [CrossRef]

- Fernández, Beatriz Cuellar, Yolanda Fuertes Callén, and José Antonio Laínez Gadea. 2011. Stock price reaction to non-financial news in European technology companies. European Accounting Review 20: 81–111. [Google Scholar] [CrossRef]

- Feuerriegel, Stefan, and Nicolas Pröllochs. 2021. Investor reaction to financial disclosures across topics: An application of latent Dirichlet allocation. Decision Sciences 52: 608–28. [Google Scholar] [CrossRef]

- Gao, Meng, and Jiekun Huang. 2020. Informing the market: The effect of modern information technologies on information production. The Review of Financial Studies 33: 1367–411. [Google Scholar] [CrossRef]

- Gentzkow, Matthew, and Jesse M. Shapiro. 2010. What drives media slant? Evidence from US daily newspapers. Econometrica 78: 35–71. [Google Scholar]

- Ghosh, Chinmoy, and J. Randall Woolridge. 1988. An analysis of shareholder reaction to dividend cuts and omissions. Journal of Financial Research 11: 281–94. [Google Scholar] [CrossRef]

- Griffin, John M., Nicholas H. Hirschey, and Patrick J. Kelly. 2011. How important is the financial media in global markets? The Review of Financial Studies 24: 3941–92. [Google Scholar] [CrossRef]

- Guest, Nicholas M. 2021. The Information Role of the Media in Earnings News. Journal of Accounting Research 59: 1021–76. [Google Scholar] [CrossRef]

- Haggard, K. Stephen, Xiumin Martin, and Raynolde Pereira. 2008. Does voluntary disclosure improve stock price informativeness? Financial Management 37: 747–68. [Google Scholar] [CrossRef]

- Hermalin, Benjamin E., and Michael S. Weisbach. 2012. Information Disclosure and Corporate Governance. The Journal of Finance 67: 195–233. [Google Scholar] [CrossRef]

- Holmström, Bengt. 1979. Moral hazard and observability. The Bell Journal of Economics 10: 74–91. [Google Scholar] [CrossRef]

- Howton, Shawn D., Shelly W. Howton, and Steven B. Perfect. 1998. The market reaction to straight debt issues: The effects of free cash flow. Journal of Financial Research 21: 219–28. [Google Scholar] [CrossRef]

- Huson, Mark R., Paul H. Malatesta, and Robert Parrino. 2004. Managerial succession and firm performance. Journal of Financial Economics 74: 237–75. [Google Scholar] [CrossRef]

- Huynh, Thanh D., and Daniel R. Smith. 2017. Stock price reaction to news: The joint effect of tone and attention on momentum. Journal of Behavioral Finance 18: 304–28. [Google Scholar] [CrossRef]

- Jacobs, Brian W., Vinod R. Singhal, and Ravi Subramanian. 2010. An empirical investigation of environmental performance and the market value of the firm. Journal of Operations Management 28: 430–41. [Google Scholar] [CrossRef]

- Jegadeesh, Narasimhan, and Joshua Livnat. 2006. Revenue surprises and stock returns. Journal of Accounting and Economics 41: 147–71. [Google Scholar] [CrossRef]

- Johnson, George Alfred, Robert M. Brown, and Dana J. Johnson. 1994. The market reaction to voluntary corporate spinoffs: Revisited. Quarterly Journal of Business and Economics 33: 44–59. [Google Scholar]

- Jung, Michael J., James P. Naughton, Ahmed Tahoun, and Clare Wang. 2018. Do firms strategically disseminate? Evidence from corporate use of social media. The Accounting Review 93: 225–52. [Google Scholar] [CrossRef]

- Kahneman, Daniel, and Amos Tversky. 2013. Prospect theory: An analysis of decision under risk. In Handbook of the Fundamentals of Financial Decision Making: Part I. Singapore: World Scientific, pp. 99–127. [Google Scholar]

- Kothari, Sabino P., Susan Shu, and Peter D. Wysocki. 2009. Do managers withhold bad news. Journal of Accounting Research 47: 241–76. [Google Scholar] [CrossRef]

- Kumar, Satish. 2017. New evidence on stock market reaction to dividend announcements in India. Research in International Business and Finance 39: 327–37. [Google Scholar] [CrossRef]

- Kwon, Spencer Yongwook, and Johnny Tang. 2020. Extreme Events and Overreaction to News. Available online: https://ssrn.com/abstract=3724420 (accessed on 17 August 2023).

- Lang, Mark, and Russell Lundholm. 1993. Cross-sectional determinants of analyst ratings of corporate disclosures. Journal of Accounting Research 31: 246–71. [Google Scholar] [CrossRef]

- Leland, Hayne E., and David H. Pyle. 1977. Informational asymmetries, financial structure, and financial intermediation. The Journal of Finance 32: 371–87. [Google Scholar] [CrossRef]

- Leuz, Christian, and Robert E. Verrecchia. 2000. The economic consequences of increased disclosure. Journal of Accounting Research 38: 91–124. [Google Scholar] [CrossRef]

- Lin, Steve, Peter F. Pope, and Steven Young. 2003. Stock market reaction to the appointment of outside directors. Journal of Business Finance & Accounting 30: 351–82. [Google Scholar]

- Lonie, Alasdair A., Gunasekarage Abeyratna, David M. Power, and C. Donald Sinclair. 1996. The stock market reaction to dividend announcements: A UK study of complex market signals. Journal of Economic Studies 23: 32–52. [Google Scholar] [CrossRef]

- Lyon, Thomas, Yao Lu, Xinzheng Shi, and Qie Yin. 2013. How do investors respond to Green Company Awards in China? Ecological Economics 94: 1–8. [Google Scholar] [CrossRef]

- Masulis, Ronald W., and Ashok N. Korwar. 1986. Seasoned equity offerings: An empirical investigation. Journal of Financial Economics 15: 91–118. [Google Scholar] [CrossRef]

- Neuhierl, Andreas, Anna Scherbina, and Bernd Schlusche. 2013. Market reaction to corporate press releases. Journal of Financial and Quantitative Analysis 48: 1207–40. [Google Scholar] [CrossRef]

- Nofer, Michael, and Oliver Hinz. 2015. Using Twitter to Predict the Stock Market: Where is the Mood Effect? Business and Information Systems Engineering 57: 229–42. [Google Scholar] [CrossRef]

- OuYang, Zhe, Jia Xu, Jiuchang Wei, and Yang Liu. 2017. Information asymmetry and investor reaction to corporate crisis: Media reputation as a stock market signal. Journal of Media Economics 30: 82–95. [Google Scholar] [CrossRef]

- Panyagometh, Kamphol. 2020. The effects of pandemic event on the stock exchange of Thailand. Economies 8: 90. [Google Scholar] [CrossRef]

- Rogers, Jonathan L., Douglas J. Skinner, and Sarah L. C. Zechman. 2016. The role of the media in disseminating insider-trading news. Review of Accounting Studies 21: 711–39. [Google Scholar] [CrossRef]

- Rothschild, Michael, and Joseph Stiglitz. 1978. Equilibrium in competitive insurance markets: An essay on the economics of imperfect information. In Uncertainty in Economics. Cambridge: Academic Press, pp. 257–80. [Google Scholar]

- Sankaraguruswamy, Srinivasan, Jianfeng Shen, and Takeshi Yamada. 2013. The relationship between the frequency of news release and the information asymmetry: The role of uninformed trading. Journal of Banking & Finance 37: 4134–43. [Google Scholar]

- Segal, Benjamin, and Dan Segal. 2016. Are managers strategic in reporting non-earnings news? Evidence on timing and news bundling. Review of Accounting Studies 21: 1203–44. [Google Scholar] [CrossRef]

- Skinner, Douglas J. 1994. Why firms voluntarily disclose bad news. Journal of Accounting Research 32: 38–60. [Google Scholar] [CrossRef]

- Sletten, Ewa. 2012. The effect of stock price on discretionary disclosure. Review of Accounting Studies 17: 96–133. [Google Scholar] [CrossRef]

- Solomon, David H., and Eugene F. Soltes. 2012. Managerial Control of Business Press Coverage. Available online: https://ssrn.com/abstract=1918138 (accessed on 17 August 2023).

- Suijs, Jeroen. 2005. Voluntary disclosure of bad news. Journal of Business Finance & Accounting 32: 1423–35. [Google Scholar]

- Tetlock, Paul C. 2007. Giving content to investor sentiment: The role of media in the stock market. The Journal of Finance 62: 1139–68. [Google Scholar] [CrossRef]

- Tetlock, Paul C. 2011. All the news that is fit to reprint: Do investors react to stale information? The Review of Financial Studies 24: 1481–512. [Google Scholar] [CrossRef]

- Tippins, Michael J., and Robert A. Kunkel. 2006. Winning a Clio advertising award and its relationship to firm profitability. Journal of Marketing Communications 12: 1–14. [Google Scholar] [CrossRef]

- Truong, Nguyen Xuan. 2017. How does market react to corporate spin-offs in Australia? Journal of Economic Development 24: 54–74. [Google Scholar] [CrossRef]

- Tsileponis, Nikolaos, Konstantinos Stathopoulos, and Martin Walker. 2020. Do corporate press releases drive media coverage? The British Accounting Review 52: 100881. [Google Scholar] [CrossRef]

- Tumarkin, Robert, and Robert F. Whitelaw. 2001. News or noise? Internet postings and stock prices. Financial Analysts Journal 57: 41–51. [Google Scholar] [CrossRef]

- Wu, Chen-Hui, and Chan-Jane Lin. 2017. The impact of media coverage on investor trading behavior and stock returns. Pacific Basin Finance Journal 43: 151–72. [Google Scholar] [CrossRef]

- Zhang, Justine, Cristian Danescu-Niculescu-Mizil, Christina Sauper, and Sean J. Taylor. 2018. Characterizing online public discussions through patterns of participant interactions. Proceedings of the ACM on Human-Computer Interaction 2: 1–27. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| SET. | Number of Firms | MAI | Number of Firms |

|---|---|---|---|

| Agro & Food Industry | 49 | Agro & Food Industry | 7 |

| Agribusiness | 11 | Consumer Products | 9 |

| Food and Beverage | 38 | Financials | 8 |

| Consumer Products | 36 | Industrial | 28 |

| Fashion | 18 | Property & Construction | 14 |

| Home and Office Products | 11 | Resources | 10 |

| Personal Products and Pharmaceuticals | 7 | Services | 34 |

| Financials | 54 | Technology | 7 |

| Banking | 11 | TOTAL | 117 |

| Finance and Securities | 29 | ||

| Insurance | 14 | ||

| Industrials | 83 | ||

| Automotive | 15 | ||

| Industrial Materials and Machinery | 13 | ||

| Packaging | 16 | ||

| Paper and Printing Materials | 1 | ||

| Petrochemicals and Chemicals | 14 | ||

| Steel and Metal Products | 24 | ||

| Property & Construction | 92 | ||

| Construction Materials | 16 | ||

| Construction Services | 23 | ||

| Property Development | 53 | ||

| Resources | 47 | ||

| Energy and Utilities | 46 | ||

| Mining | 1 | ||

| Services | 98 | ||

| Commerce | 21 | ||

| Health Care Services | 19 | ||

| Media and Publishing | 24 | ||

| Professional Services | 3 | ||

| Tourism and Leisure | 11 | ||

| Transportation and Logistics | 20 | ||

| Technology | 36 | ||

| Electronic Components | 9 | ||

| Information and Comm. Technology | 27 | ||

| Companies Under Rehabilitation | 3 | ||

| TOTAL | 498 |

| Type of Information | Timing of Disclosure |

|---|---|

| 1. Shareholders’ meeting | Immediately |

| 2. Dividend payment | Immediately |

| 3. Acquisition or disposition of assets | Immediately |

| 4. Connected transactions | Immediately |

| 5. Capital increase | Immediately |

| 6. A major change in shareholding structure | Immediately |

| 7. Investment in another company, resulting in the other company becoming a subsidiary | Immediately |

| 8. Termination of a subsidiary status | Immediately |

| 9. Making/filing tender offer | Immediately |

| 10. Merger | Immediately |

| 11. Litigation or major dispute | Immediately |

| 12. Providing financial assistance to other persons | Immediately |

| 13. Debt payment default | Immediately |

| 14. Borrowing or issuance of bonds | Immediately |

| 15. New product launch or major development | Immediately |

| 16. Significant commercial contract gain or loss | Immediately |

| 17. Change in accounting policies/accounting period | Immediately |

| 18. Head office relocation | Three working days |

| 19. Change in Director, CEO, Executive, Chief Financial Officer, and Chief Accountant | Three working days/immediately (change of CEO) |

| Category | Subcategory | Corp. Press Releases | Newspapers Articles | Description |

|---|---|---|---|---|

| No. of Obs. | No. of Obs. | |||

| A. Company Awards and Milestones | Company Award | 512 | 1183 |

|

| Product Award | 45 | 115 |

| |

| Reaching a Milestone | 127 | 466 |

| |

| B. Commercial Contract Gain/Loss | Customer Loss | 7 | 498 |

|

| Customer Win | 933 | 3923 |

| |

| New Partnership | 1895 | 7971 |

| |

| C. Dividend Payments | Dividend—Decreased | 625 | 11 |

|

| Dividend—Generic | 1734 | 823 |

| |

| Dividend—Increased | 13 | 39 |

| |

| Dividend—Special/Interim | 595 | 80 |

| |

| D. Financial Performance | Strong Financial Performance | 4026 | 9452 |

|

| Weak Financial Performance | 3808 | 4200 |

| |

| Preannouncement—Negative | 17 | 682 |

| |

| Preannouncement—Positive | 626 | 9345 |

| |

| Restatement | 117 | 45 |

| |

| E. Debt and Equity Offerings | Debt Issuance | 372 | 709 |

|

| Equity Issuance | 772 | 839 |

| |

| Share Buyback | 77 | 140 |

| |

| F. Legal and Compliance | Legal Problem | 157 | 1432 |

|

| Legal Problem Concludes | 162 | 476 |

| |

| SEC Investigation | 14 | 302 |

| |

| Noncompliance | 125 | 270 |

| |

| Return to Compliance | 4 | 91 |

| |

| G. Merger, Acquisitions, and Divestments | Acquisition—Certain | 512 | 948 |

|

| Acquisition—Intent | 42 | 555 |

| |

| IPO | 53 | 255 |

| |

| Merger | 4 | 78 |

| |

| Spinoff—Certain | 305 | 341 |

| |

| Spinoff—Intent | 3 | 200 |

| |

| H. Management/Organization Change | Addition | 2433 | 593 |

|

| Promotion | 10 | 101 |

| |

| Reorganization | 232 | 304 |

| |

| Retirement | 23 | 38 |

| |

| Termination | 1016 | 292 |

| |

| I. Company Hosts or Attend Meetings/Events | Company-Sponsored Event | 800 | 1924 |

|

| Industry Event | 555 | 1189 |

| |

| Investor Meeting | 100 | 323 |

| |

| J. New Product Launch or Major Product Development | New Product | 790 | 3498 |

|

| Patent Award | 6 | 60 |

| |

| Product Approval | 43 | 304 |

| |

| Product Defect | 14 | 379 |

| |

| Research Success | 6 | 61 |

| |

| Updates and Upgrades | 349 | 2476 |

| |

| K. Business Strategy and Performance Outlook | Negative Credit News | 36 | 228 |

|

| Positive Credit News | 210 | 433 |

| |

| Business Downsizing | 129 | 588 |

| |

| Business Expansion | 1626 | 11,293 |

| |

| Declining Profitability/Outlook | 139 | 986 |

| |

| Improving profitability/Outlook | 347 | 3875 |

|

| A. Corporate Releases | ||||

| Size | No. of Obs. | Mean | Median | Std. Dev. |

| 1 (small) | 3793 | 0.86 | 0 | 1.19 |

| 2 | 4002 | 0.90 | 0 | 1.27 |

| 3 | 4518 | 1.02 | 1 | 1.35 |

| 4 | 4773 | 1.08 | 1 | 1.40 |

| 5 (large) | 9490 | 2.13 | 1 | 2.52 |

| B. Newspaper Articles | ||||

| Size | No. of Obs. | Mean | Median | Std. Dev. |

| 1 (small) | 4450 | 1.00 | 0 | 1.82 |

| 2 | 6188 | 1.40 | 0 | 2.99 |

| 3 | 7470 | 1.69 | 1 | 2.57 |

| 4 | 13,431 | 3.03 | 1 | 4.86 |

| 5 (large) | 43,078 | 9.65 | 5 | 14.30 |

| C. Combined | ||||

| Size | No. of Obs. | Mean | Median | Std. Dev. |

| 1 (small) | 8243 | 1.86 | 1 | 2.56 |

| 2 | 10,190 | 2.30 | 1 | 3.69 |

| 3 | 11,988 | 2.71 | 2 | 3.41 |

| 4 | 18,204 | 4.11 | 2 | 5.66 |

| 5 (large) | 52,568 | 11.78 | 6 | 15.99 |

| Category | Subcategory | Corp. Press Releases | Newspapers Articles | |||

|---|---|---|---|---|---|---|

| CAR | p-Value | CAR | p-Value | |||

| A | Company Awards and Milestones | Company Award | −0.132% | 0.268 | −0.192% | 0.008 |

| Product Award | −0.184% | 0.391 | 0.642% | 0.007 | ||

| Reaching a Milestone | 0.288% | 0.304 | 0.185% | 0.175 | ||

| B | Commercial Contract Gain/Loss | Customer Loss | −0.813% | n.a. | −0.111% | 0.463 |

| Customer Win | 0.166% | 0.128 | 0.184% | 0.001 | ||

| New Partnership | 0.111% | 0.171 | 0.030% | 0.400 | ||

| C | Dividend Payments | Dividend—Decreased | −1.354% | 0.000 | −0.968% | n.a |

| Dividend—Generic | −0.014% | 0.900 | 0.377% | 0.001 | ||

| Dividend—Increased | 0.324% | n.a. | 1.060% | 0.459 | ||

| Dividend—Special/Interim | 0.453% | 0.014 | −0.885% | 0.236 | ||

| D | Financial Performance | Strong Financial Performance | 0.331% | 0.000 | 0.239% | 0.000 |

| Weak Financial Performance | −2.472% | 0.000 | −2.094% | 0.000 | ||

| Negative Preannouncement | 0.090% | n.a. | −0.870% | 0.000 | ||

| Positive Preannouncement | 0.077% | 0.678 | 0.306% | 0.000 | ||

| Restatement | −0.760% | 0.130 | −0.042% | 0.387 | ||

| E | Debt and Equity Offerings | Debt Issuance | −0.107% | 0.601 | −0.093% | 0.456 |

| Equity Issuance | −0.902% | 0.000 | −0.601% | 0.004 | ||

| Share Buyback | 2.461% | 0.630 | 1.577% | 0.000 | ||

| F | Legal and Compliance | Legal Problem | −0.299% | 0.581 | −0.861% | 0.000 |

| Legal Problem Concludes | −0.244% | 0.656 | −0.384% | 0.010 | ||

| SEC Investigation | 0.262% | n.a. | −2.919% | 0.000 | ||

| Noncompliance | −0.093% | 0.909 | −3.108% | 0.000 | ||

| Return to Compliance | −13.068% | n.a. | −12.289% | 0.028 | ||

| G. | Mergers, Acquisitions, and Divestments | Acquisition—Certain | −0.208% | 0.369 | 0.035% | 0.803 |

| Acquisition—Intent | 0.614% | 0.398 | 0.198% | 0.306 | ||

| IPO | 0.417% | 0.490 | 0.099% | 0.685 | ||

| Merger | −0.483% | n.a. | −0.320% | 0.135 | ||

| Spinoff—Certain | 0.044% | 0.887 | 0.464% | 0.063 | ||

| Spinoff—Intent | −1.785% | n.a. | 0.559% | 0.049 | ||

| H. | Management/Organization Change | Addition | −0.563% | 0.000 | 0.059% | 0.709 |

| Promotion | −0.115% | n.a. | −0.268% | 0.090 | ||

| Reorganization | −0.005% | 0.989 | −0.240% | 0.423 | ||

| Retirement | −1.662% | n.a. | −0.418% | 0.347 | ||

| Termination | −0.343% | 0.023 | −0.100% | 0.689 | ||

| I. | Company Hosts or Attend Meetings/Events | Company-Sponsored Event | −0.185% | 0.060 | −0.132% | 0.041 |

| Industry Event | 0.058% | 0.648 | 0.040% | 0.640 | ||

| Investor Meeting | 0.125% | 0.452 | 0.081% | 0.679 | ||

| J. | New Product Launch or Major Product Development | New Product | 0.045% | 0.674 | 0.026% | 0.613 |

| Patent Award | 0.362% | n.a. | 0.836% | 0.221 | ||

| Product Approval | 0.229% | 0.534 | −0.142% | 0.355 | ||

| Product Defect | −2.085% | n.a. | −0.335% | 0.018 | ||

| Research Success | 0.552% | n.a. | −1.224% | 0.440 | ||

| Updates and Upgrades | 0.061% | 0.683 | −0.015% | 0.791 | ||

| K. | Business Strategy and Performance Outlook | Negative Credit News | −1.857% | 0.375 | −2.555% | 0.000 |

| Positive Credit News | −0.363% | 0.083 | −0.614% | 0.000 | ||

| Business Downsizing | 0.101% | 0.837 | 0.270% | 0.145 | ||

| Business Expansion | −0.089% | 0.370 | 0.033% | 0.296 | ||

| Declining Outlook | −1.050% | 0.017 | −0.488% | 0.000 | ||

| Improving Outlook | 0.401% | 0.081 | 0.229% | 0.000 | ||

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Supawat, L.; Arnat, L. Market Reaction to Corporate Releases and News Articles: Evidence from Thailand’s Stock Market. Int. J. Financial Stud. 2023, 11, 111. https://doi.org/10.3390/ijfs11030111

Supawat L, Arnat L. Market Reaction to Corporate Releases and News Articles: Evidence from Thailand’s Stock Market. International Journal of Financial Studies. 2023; 11(3):111. https://doi.org/10.3390/ijfs11030111

Chicago/Turabian StyleSupawat, Likittanawong, and Leemakdej Arnat. 2023. "Market Reaction to Corporate Releases and News Articles: Evidence from Thailand’s Stock Market" International Journal of Financial Studies 11, no. 3: 111. https://doi.org/10.3390/ijfs11030111