1. Introduction

In recent years, particularly during the COVID-19 pandemic, many countries have seen a consistent rise in public debt. This trend has sparked concerns about its potential effects on sustained economic growth. According to the conventional view, rooted in the Ricardian Equivalence theory, the negative impacts of rising public debt could be offset by an equal increase in private savings. This suggests that the overall national savings would remain unchanged, thus not influencing growth (e.g.,

Barro 1974). Conversely, if Ricardian Equivalence is not applicable, another strand of the literature believes that increased public debt could negatively affect long-term economic growth (e.g.,

Blanchard 1985;

Elmendorf and Gregory Mankiw 1999).

Recent studies have shifted towards exploring potential nonlinear dynamics within the debt–growth nexus, examining how accumulating debt might adversely affect economic growth, particularly when debt levels surpass certain thresholds. A seminal study by

Reinhart and Rogoff (

2010) posits that public debt begins to impede economic growth when the debt-to-GDP ratio exceeds 90%. Using threshold regression models, studies by

Afonso and Jalles (

2013);

Caner et al. (

2010);

Cecchetti et al. (

2011) identified varying thresholds of debt-to-GDP ratios, 85%, 77%, and 59%, respectively, at which public debt begins to harm economic growth. However,

Kourtellos et al. (

2013) were unable to confirm a significant threshold effect for public debt when adjusting for endogeneity concerns.

The above-mentioned studies provide mixed evidence about the nonlinear effects of public debt on economic growth and two main challenges emerge. Firstly, these findings are obtained under strong assumptions of homogeneity in threshold levels across different countries. Commonly, heterogeneity is modeled as a unit-specific, time-invariant fixed effect. For example,

Chudik et al. (

2017) examines a dynamic heterogeneous panel threshold model with cross-sectional dependent errors, yet this approach still assumes a uniform threshold level for all countries. Likewise,

Eberhardt and Presbitero (

2015) model the long-run relationship between public debt and growth as heterogeneous across countries. However, they introduce nonlinearities at the country level by using pre-determined thresholds. Employing the grouped fixed-effect estimator proposed by

Bonhomme and Manresa (

2015),

Gómez-Puig et al. (

2022) examine the heterogeneous link between public debt and economic growth by identifying the latent group patterns within fixed effects. Nevertheless, their research is limited to a linear panel model, neglecting potential nonlinear impacts. In short, the complexity of heterogeneous threshold modeling and the extensive data requirement may be reasons why few studies have concurrently addressed the two critical aspects—nonlinearity and heterogeneity—that are central to the debt–growth relationship. To identify heterogeneous threshold levels, there is a pressing need for applied researchers to develop a new model, that can balance the use of flexible methods for modeling unobserved heterogeneity with the development of parsimonious specifications that are feasible within the constraints of limited datasets. Secondly, conventional threshold regression models assume a discontinuous regression function at the true threshold level, which may not be suitable in this context. It is not intuitively expected to observe an abrupt jump in the economic growth rate when the public debt ratio increases marginally at the turning point.

Chan and Tsay (

1998) introduce a continuous threshold autoregressive model, which enables a piece-wise linear function of the threshold variable. Building on this,

Hansen (

2017) expands the framework by proposing tests for a threshold effect and inferring the regression parameters in a continuous threshold model with an unknown threshold parameter, termed the kink threshold regression (KTR) model. This model is also applied to re-examine the issue of public debt overhang, albeit under the assumption of a uniform threshold level. Motivated by previous work, we employ a panel kink threshold regression model with latent group structures to re-examine the debt–growth puzzle. Our contribution is twofold, encompassing both methodological and empirical approaches, and can be outlined as follows.

In terms of methodology, the proposed model extends the panel threshold regression model with latent group structures of

Miao et al. (

2020) by incorporating a continuous threshold effect. It is important to note that the theoretical distinction of the KTR model lies in its continuity property, setting it apart from the standard (discontinuous) threshold regression (TR) model. Firstly, the asymptotic distribution of the least squares estimator of the threshold in the KTR model and the TR model are quite different. In the KTR model, the estimator yields a normal distribution, whereas in the TR model, the estimator follows a two-sided Brownian motion with a diminishing threshold effect (see

Hansen 2000), or a Poisson distribution under the fixed-threshold-effect assumption (see

Chan 1993). Secondly, even though the KTR model can be perceived as a constrained TR model,

Hidalgo et al. (

2019) emphasizes that mistakenly estimating a KTR model within the TR framework of

Hansen (

2000) without considering the continuity of the true model results in an irregular Hessian matrix. This irregularity leads to the least squares estimator of the threshold parameter converging at a cube root-n convergence rate, slower than the root-n convergence rate observed for the KTR model, as demonstrated by

Hansen (

2017). All these references imply that the methodology outlined in

Miao et al. (

2020) cannot be directly applied to address the latent group structure problem in a KTR model and necessitates a conversion of our theoretical contribution. This model enables variations in threshold and slope coefficients across individuals through a group-based pattern within a continuous-threshold-effect framework, effectively addressing the previously mentioned two challenges. The proposed data-driven method aligns with other studies in panel latent group structures (e.g.,

Bonhomme and Manresa 2015;

Su et al. 2016;

Bonhomme et al. 2022), balancing the trade-off between the limited flexibility of homogeneity assumptions and the extensive data requirements of heterogeneity inherently. We present the estimation strategy and show the latent group structure can be estimated consistently with a probability that approaches 1. This extends theorem 3.1 from

Miao et al. (

2020) to the context of continuous threshold effects.

Empirically, using the dataset of

Chudik et al. (

2017), encompassing data from forty countries spanning from 1980 to 2010, the empirical results determine that the optimal number of groups is three and recover the group structures. For all countries, two groups benefit significantly from increasing public debt, up to a certain threshold, beyond which the significance diminishes. Within the subset of OECD countries, the group—made up of sixteen out of twenty-one OECD countries—exhibits an inverse U-shaped relationship between public debt and economic growth. The findings indicate the presence of a heterogeneous threshold effect, suggesting that any contradictory conclusions in the previous studies might stem from overlooking this heterogeneous impact on the way countries manage their debt obligations.

The rest of the paper is organized as follows.

Section 2 describes the panel kink threshold regression model and the estimation strategy.

Section 3 details the assumptions and establishes the consistency of the estimators for group membership. In

Section 4, we evaluate the finite-sample performance of our model through Monte Carlo simulations. The empirical results of our study are presented in

Section 5.

Section 6 concludes the paper. Technical proofs are relegated to the

Appendix A and

Appendix B.

3. Asymptotic Results

In this section, the limiting distributions of the estimators for the group structure are discussed. Below, we list some regularity conditions used to derive the consistency of the group structure estimator.

Assumption 1. (i) For each , , where is the smallest sigma field generated by .

(ii) Across i , are mutually independent of each other.

(iii) For all i, are strictly stationary mixing process with mixing coefficients satisfying for some constants & .

Assumption 2. (i) For some and some constants , , , , and .

(ii) The parameter spaces and are compact such that and .

(iii) has a density function and is continuous over and .

(iv) Let and . For some constants , as , we have There exists a constant such that for all (vi) For all and , we have for some constants .

(vii) For any and , for some constants , we have (viii) For all : .

(ix) As , and .

Assumption 1 is similar to assumptions A.1 (i)–(iii) of

Miao et al. (

2020) and assumptions A.2 (a)–(c) of

Su and Chen (

2013) and is standard in the literature. Assumption 1 (i) assumes the martingale difference sequence condition and Assumption 1 (ii) is the cross-sectional independence. Assumption 1 (iii) imposes the strong mixing condition.

3Assumptions 2 (i)–(ii) are the regularity conditions. Assumption 2 (iii) is similar to assumption 1.4 of

Hansen (

2017) and requires that the threshold variable,

, has a bounded density function. Assumption 2 (iv) ensures the non-colinearity, similar to assumption A.4(ii) in the

Miao et al. (

2020), but specifies that it requires to hold for each individual. Assumption 2 (v), paralleling assumption A2 of

Miao et al. (

2020) and assumption 1 (g) of

Bonhomme and Manresa (

2015), extends the full-rank condition in the standard kink regression model to encompass cases with latent groups. Assumptions 2 (vi)–(viii) are needed for the identification and mirror assumption A.3 (i)–(iii) of

Miao et al. (

2020). Specifically, Assumption 2 (vi) requires the group-specific coefficients (slope and threshold) to be distinct from each other. Assumption 2 (vii) is inferred from Assumption 2 (vi). Assumption 2 (viii) ensures that each group size is sufficiently large that is asymptotically non-negligible. Assumption 2 (ix) is similar to assumption A.3 (iv) of

Miao et al. (

2020) and defines the relative magnitude of individual size

N and period size

T, fitting many empirical macroeconomic applications, including ours.

Theorem 1. Given Assumptions 1 and 2, as , we have Theorem 1 extends theorem 3.1 of

Miao et al. (

2020) to allow for the continuous threshold effect and is similar to theorem 2 of

Bonhomme and Manresa (

2015). This theorem specifies that, as

, the probability of accurately estimating the group structure approaches 1. Therefore, given the latent group structure can be estimated at a faster rate (see Lemma A3 in the

Appendix A for the rate of recovering the latent group structure) than the convergence rate of the estimators of the slope and kink threshold parameters of the pooled panel kink regression model (see

Hansen 2017), similar to

Miao et al. (

2020), we can establish the estimators of the slope and kink threshold parameters of the panel kink regression model with latent groups asymptotically equivalent to the infeasible estimators that are obtained as if the group structure is known a priori.

4 4. Monte Carlo Simulation

In this section, we propose Monte Carlo simulations to test the performance of the estimator with a small sample size. We list the data-generating processes (DGPs) and the Monte Carlo results, where we first consider the static model, and then a dynamic model suits our empirical application. We have

DGP1:

where

,

,

denotes the group-specified fixed effect, and

and

are group-specified slopes.

is the threshold value. We set the number of groups to be three, thus

is chosen among

. We set the parameters

,

. We propose a diminishing threshold effect, with

. Following the theory, the group identification does not rely on the heterogeneous threshold effect across groups; to test that, the Monte Carlo simulation focuses on two cases, (1) homogeneous group-specific threshold values, where we set

; (2) heterogeneous group-specific threshold values, with threshold values

. We repeat the Monte Carlo simulation 1000 times and the results are shown in

Table 1,

Table 2 and

Table 3.

Table 1 reports the Monte Carlo results for the homogeneous group-specific threshold value DGP and

Table 1 shows the results for the heterogeneous group-specific threshold value DGP. It is worth noting that for both DGPs with homogeneous and heterogeneous thresholds across groups, as seen from the mean squared error (MSE) panels, our estimator displays convergence when either the number of

N or

T increases. In

Table 3, we also report the average misclassification frequency (MF) in

Table 3 across replications, where for each replication we define

. The estimation results show that with either

N or

T increasing, we observe a decreasing misclassification frequency. In the most unfavorable scenario, the average rate of misclassification with our approach stands at approximately

, indicating the effectiveness of our proposed method. Also, with a fixed

N and

T, the estimators with a homogeneous threshold DGP have a smaller

, compared with heterogeneous threshold DGPs. This observation aligns with the results presented in

Miao et al. (

2020). Theoretical indications from the study suggest that in threshold regression, group identification hinges on the variation in slopes across groups. The distinct threshold effects specific to each group do not contribute to the identification process.

DGP2:

where

and again we keep the number of groups as three. We set

,

, and

, which suggests a dynamic model with stationary process and a diminishing threshold effect. Again, we consider two DGPs that cover both homogeneous group-specified threshold values (

) and heterogeneous group-specific threshold values (

). We repeat the Monte Carlo simulation 1000 times and report the results in

Table 4,

Table 5 and

Table 6.

Again,

Table 4 and

Table 5 report the Monte Carlo results for the homogeneous and heterogeneous group-specified threshold effects, respectively. Similar to the results in DGP1 with a static setup, the Monte Carlo results in DGP2 show convergence when either

N or

T increases. We can observe the convergence in

Table 4 with homogeneous group-specific threshold value cases and

Table 5 with heterogeneous group-specific threshold values. In

Table 6, the Monte Carlo results show that the misclassification frequency decreases as

N or

T increases.

5. Empirical Results

In this section, we estimate the panel kink regression model with latent groups in Equation (

1). We explore the heterogeneous nonlinear effect of public debt on economic growth. There is a growing concern that current debt trajectories in several economies around the world are not sustainable, implying risks to long-term growth and stability. Following the threshold methodology introduced by

Hansen (

2000),

Kourtellos et al. (

2013) explored their presence in the context of public debt and the ability of countries to handle their debt obligations. The idea is that public debt levels that are above a particular threshold value may have different implications for growth compared to more moderate levels of debt; see, for example,

Reinhart and Rogoff (

2010), who found that for countries with debt-to-GDP over 90 percent, debt can have adverse consequences on growth. However, most of the early literature on the public debt–growth nexus suffered from a number of conceptual and methodological issues, especially from the failure to adequately account for heterogeneity. Specifically, research had been focused on whether debt is above or below a particular public debt threshold value. The alternative that has been considered is simply that there is no nonlinearity in the effect of public debt on growth. In our approach, we tackle the issue of heterogeneity by considering and estimating the optimal number of groups and recovering different group structures that indicate the presence of a heterogeneous threshold effect, suggesting that any contradictory conclusions in the previous studies might stem from overlooking this heterogeneous impact on the way countries manage their debt obligations.

5.1. Data

We employ a balanced panel dataset that includes forty countries spanning from 1980 to 2010, obtained from

Chudik et al. (

2017). Of these, twenty-one are in the OECD, which is often considered as a rich country club (see

Appendix C Table A1 for the list of countries used in this paper). The public debt-to-GDP ratio, represented as

, is calculated by taking the logarithm.

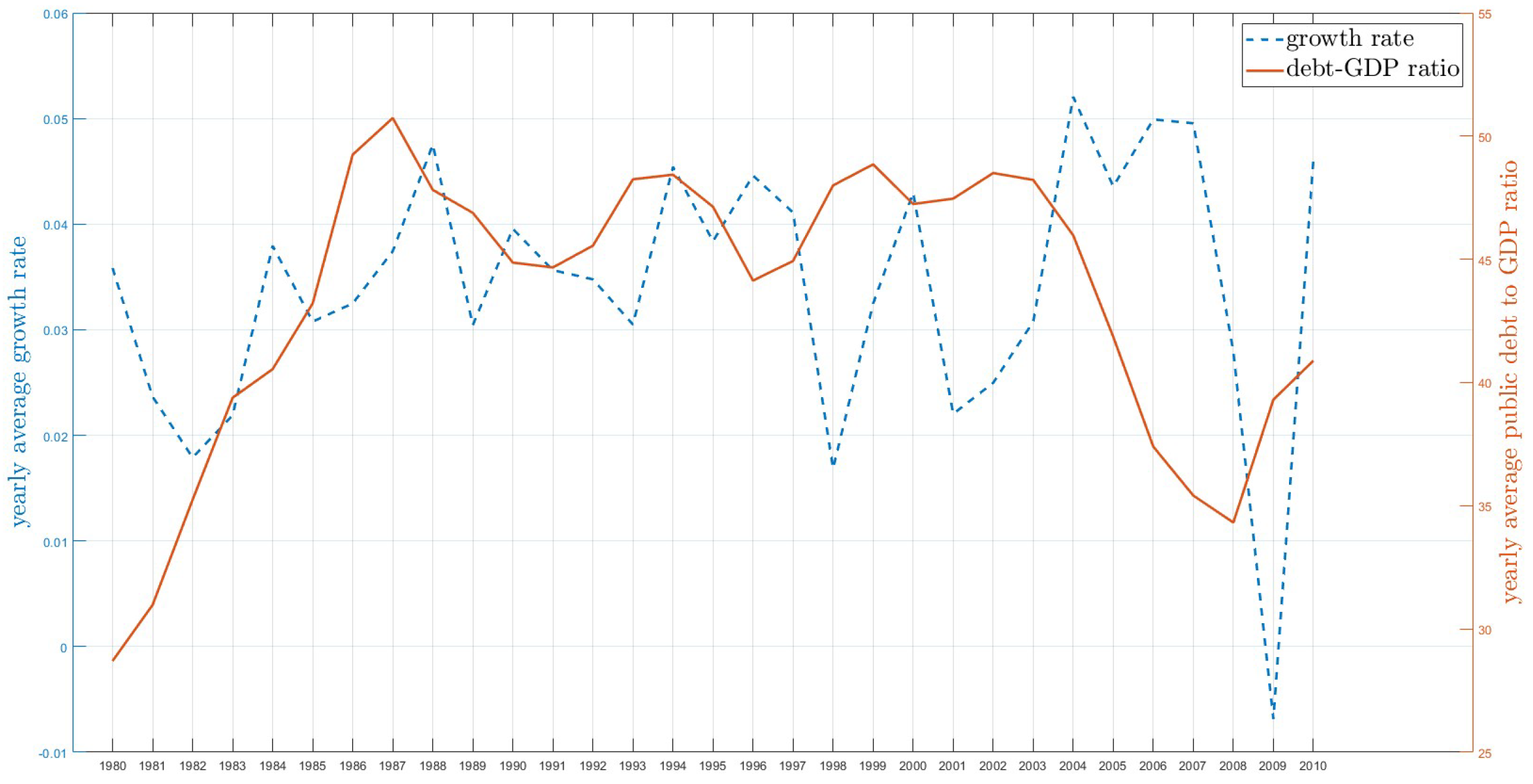

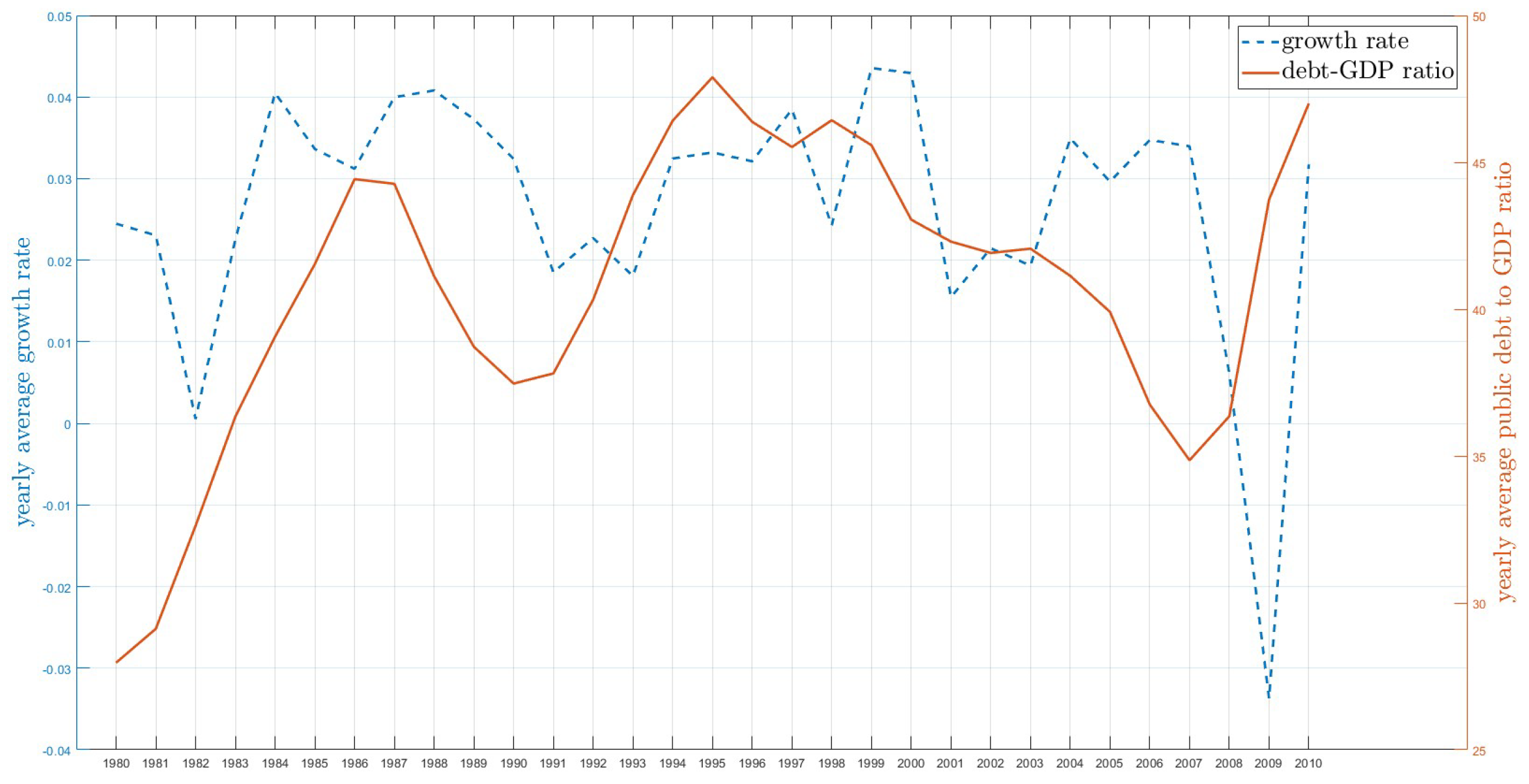

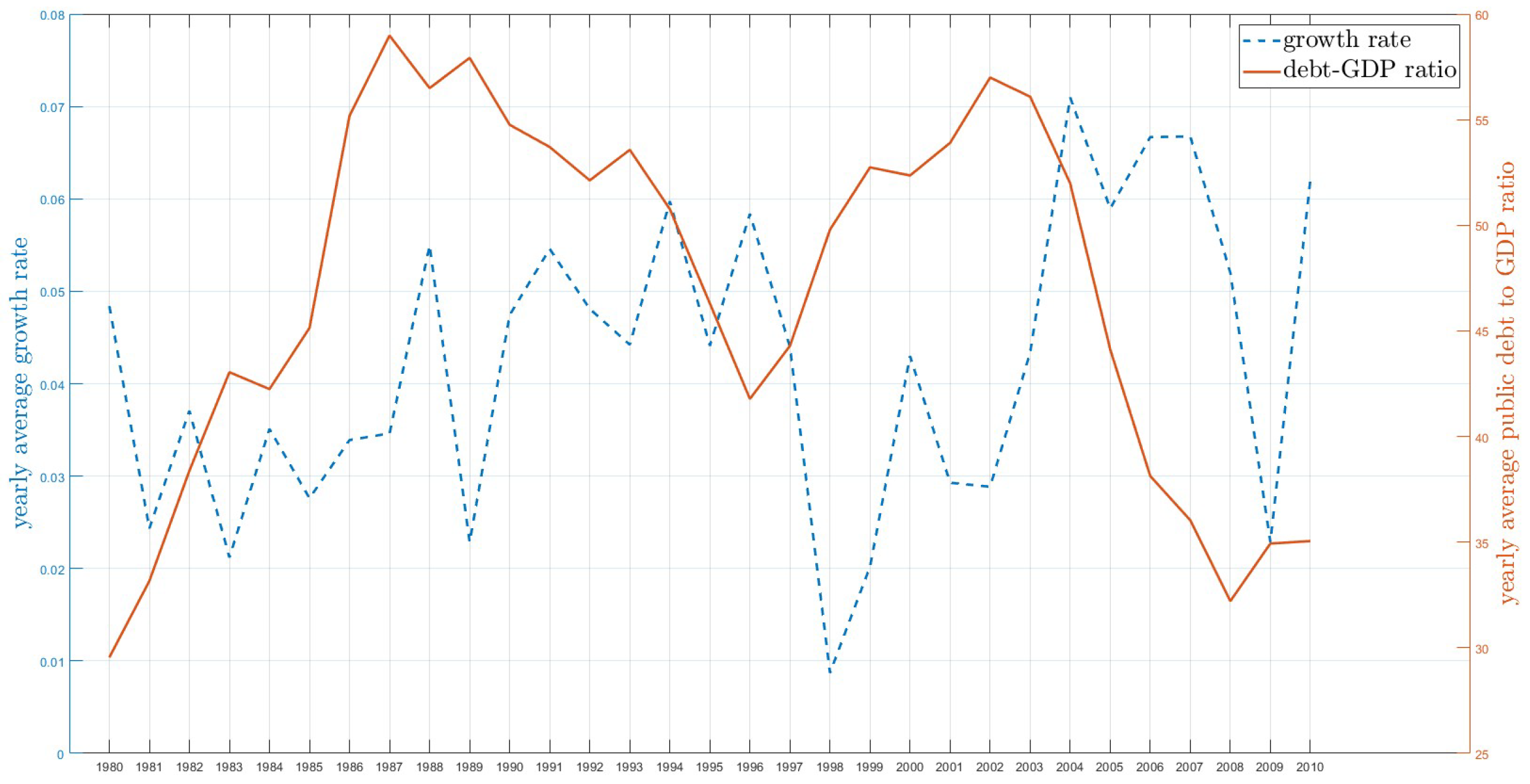

Figure 1,

Figure 2 and

Figure 3 depict time-series plots of yearly average economic growth versus the yearly average public debt-to-GDP ratio for all countries, as well as separately for OECD and non-OECD countries. A visual examination of these plots reveals a common trend between the two variables, indicating that the public debt-to-GDP ratio captures the pattern of economic growth in all scenarios. However, a closer comparison of

Figure 2 and

Figure 3 reveals an asymmetric co-movement between these variables in OECD versus non-OECD countries, pointing to the club-based heterogeneity in the impact of public debt on economic growth. This observation motivates us to further explore the identification of unobserved group structures and the uncovering of group-based heterogeneity.

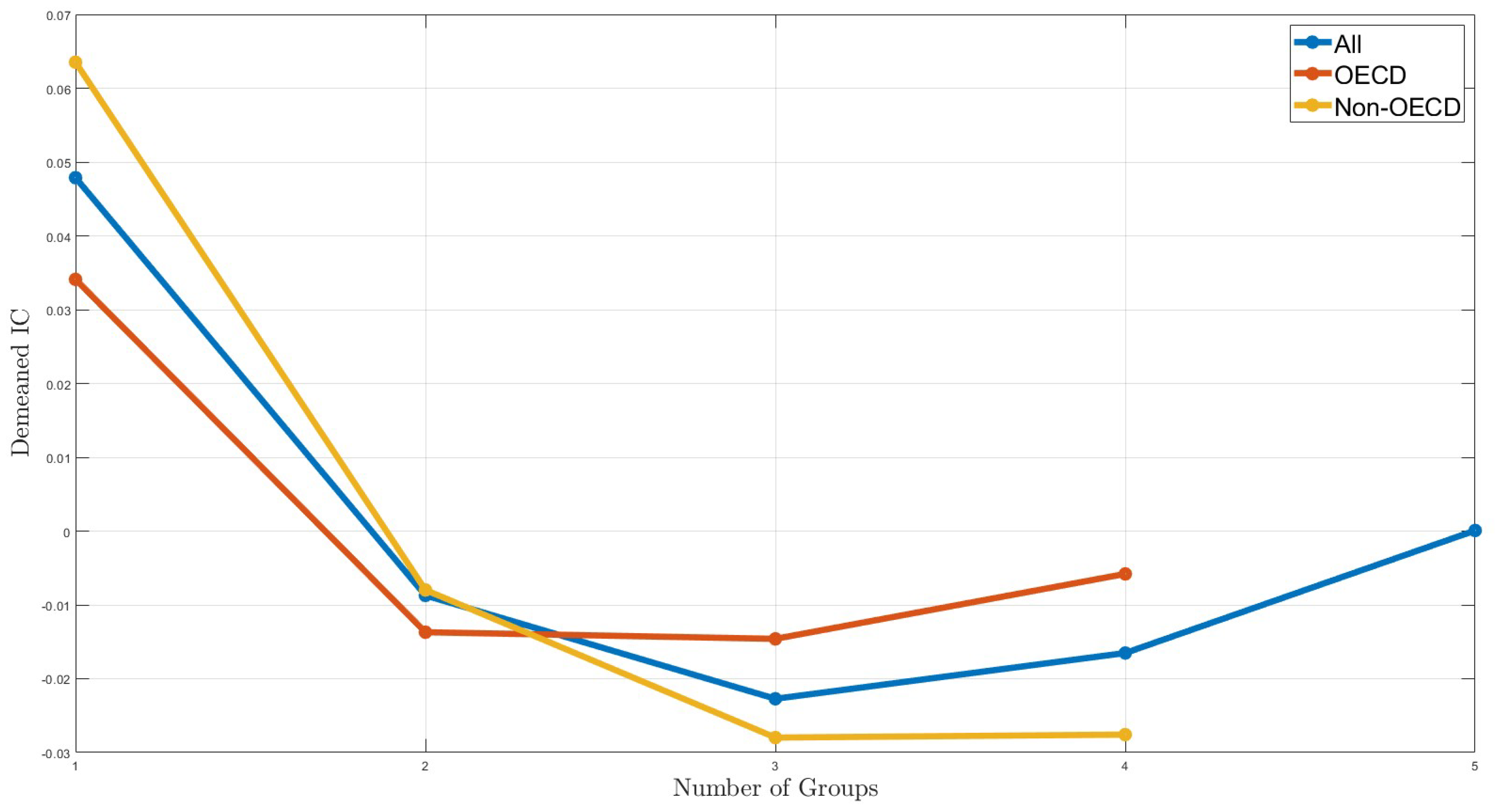

5.2. Identifying the Number of Groups

Since the true number of groups

is unobserved, we follow

Miao et al. (

2020) and employ a BIC-type information criterion (IC) to ascertain the number of groups. This method is outlined as follows:

where

represents the mean squared error for a given group number

and

is the tuning parameter used for the penalty term.

5 Then, the optimal number of groups is chosen by

where

is the maximum number of groups, as determined by empirical research. Due to the data requirement, we set

for the full sample, covering all countries, while for the subsamples,

is applied separately to OECD and non-OECD countries.

Figure 4 shows the de-meaned IC values for different numbers of groups, revealing that the IC curves reach their lowest point at

for all sample selections.

6 Therefore, we select three as the optimal number of groups for our subsequent analysis.

5.3. Estimation Results

We then proceed to estimate the model (

1) by setting

(indicating no latent group, our benchmark) and using

(as determined by the IC criterion). The results of these estimations using the full sample of all countries are summarized in

Table 7.

Assuming a homogeneous kink threshold effect across all countries, we find the estimated tipping point to be 40.45%. However, in contrast to the conventional view, the pooled panel kink regression analysis reveals that higher public debt leads to lower growth in countries with lower debt levels and it appears to benefit economies with higher debt levels.

When analyzing the results of the panel kink regression with latent group structures, the estimations for group 1 align with the counter-intuitive results from the benchmark. The results suggest a negative impact on economic growth when a country’s debt-to-GDP ratio is below 43.51%, becoming insignificant above this level. However, only seven countries fall into group 1. The results for groups 2 and 3 are particularly notable, indicating threshold heterogeneity, where the impact of public debt on growth varies depending on the group members. Specifically, for group 2, the turning point is at 44.28%, where public debt fosters economic growth up to this level, after which the positive effect disappears. Group 3, with the highest threshold of 58.14%, exhibits a significant positive impact of public debt on growth when below this level, but this effect becomes insignificant once the threshold is exceeded. Notably, group 2 experiences a more substantial impact in the lower regime, indicating these countries benefit most from public debt. Consistent with the existing literature (e.g.,

Baum et al. 2013), our results for groups 2 and 3 indicate that while the impact of public debt on GDP growth is initially positive and statistically significant, it declines to near zero, and loses significance beyond specific public debt-to-GDP ratios.

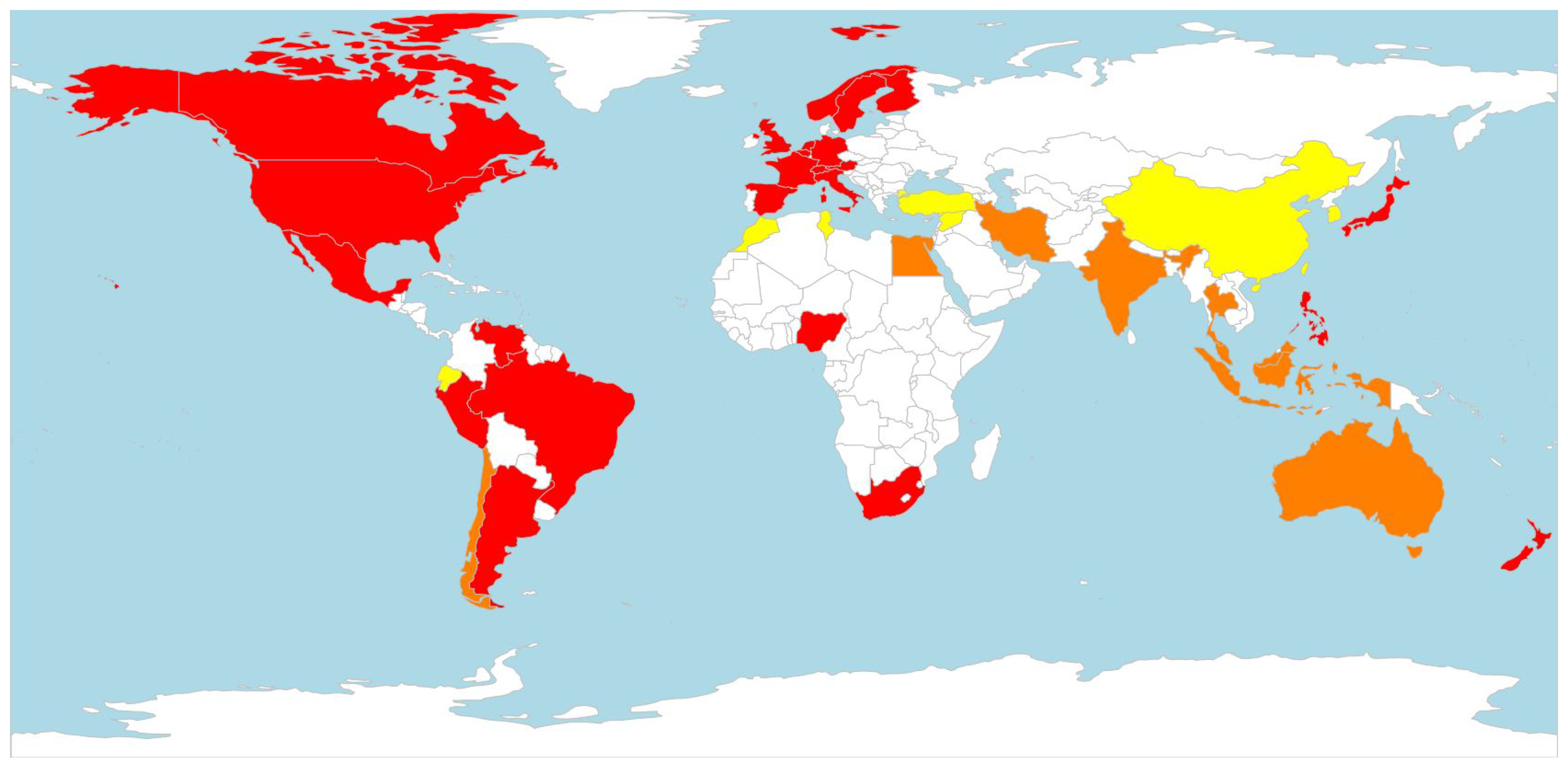

Figure 5 illustrates the world map with assigned group memberships. Interestingly, these classifications correlate to some extent with geographic location, economic development level, and the independence of the central bank. For instance, group 1, which includes countries like China and Turkey, is characterized by relatively weaker central bank independence. Group 2 is predominantly associated with the Indo-Pacific region. Meanwhile, group 3 encompasses the majority of the countries in the pan-American and European regions, indicating a distinct geographic and economic pattern in the grouping. In summary, the empirical findings emphasize the heterogeneity of threshold effects crucial in determining the influence of debt on growth.

As a robustness check on the impact of kink threshold heterogeneity, we also present the estimation results for OECD and non-OECD countries. The estimates from OECD and non-OECD countries are presented in

Table 8 and

Table 9, respectively. The estimation results reveal a distinct difference in the homogeneous kink threshold effect between OECD and non-OECD countries. Specifically, for OECD countries, the effect of debt on growth is insignificant in both regimes. In contrast, for non-OECD countries, the results are consistent with those of all countries shown in

Table 7, showing a significantly negative impact in the low regime and a positive impact in the high regime, both at the 5 percent level. Turning to the results with latent group structures, none of the groups align with the findings that assume homogeneity for either OECD or non-OECD countries, indicating the presence of heterogeneity in threshold effects. Interestingly, within the low-debt regime, 16 of the 21 OECD countries (group 3, OECD) show a significantly positive impact of debt on growth at the 1 percent level. Conversely, public debt has a positive impact on growth in just 7 out of 19 non-OECD countries (group 3, non-OECD) at the same level, but the effect size is much larger. Furthermore, only 2 out of 21 OECD countries (group 2, OECD) exhibit a significantly negative impact of public debt on growth in the low-debt regime, compared to 4 out of 19 non-OECD countries (group 2, non-OECD). In the high-debt regime, an inverse U-shaped relationship is supported by the majority of OECD countries (group 3, OECD), where the positive impact of public debt on growth turns significantly negative at the 10 percent level once the debt-to-GDP ratio exceeds 54.58%. In non-OECD countries, the impact of debt on growth becomes insignificant in the high-debt regime for groups 1 and 2, while group 3 sees a significantly larger positive impact on growth when the debt ratio exceeds 61.4%. These results highlight the parallels between OECD and non-OECD countries and provide further evidence of the importance of accounting for heterogeneous kink thresholds. Ignoring these group patterns, as seen in the pooled panel kink regression results in all sample selections, could lead to counter-intuitive conclusions and erroneous policy implications.

6. Conclusions

This paper makes an important contribution to the ongoing debate regarding the nonlinear relationship between public debt and economic growth. While the existing literature primarily assumes a homogeneous threshold effect of public debt on economic growth, our approach diverges by employing a panel kink regression model that incorporates latent group structures. This method allows us to explore the heterogeneous threshold effects based on unknown group patterns. We propose a least squares estimator and demonstrate the consistency of estimating group structures. Our findings reveal that the nonlinear relationship between public debt and economic growth is characterized by a heterogeneous threshold level, which varies among different groups, highlighting that the mixed results found in previous studies may stem from the arguably incorrect assumption of a homogeneous threshold effect.

In future investigations, researchers might explore various potential extensions. Our proposed method concentrates solely on exogenous variables, potentially encountering limitations in an endogenous framework. In cases where threshold variables or regressors exhibit endogeneity, researchers may address this issue by employing the control function approach introduced by

Zhang et al. (

2023). Incorporating two or more endogenous threshold variables, as in

Chen et al. (

2023), can also be intriguing. Another avenue for exploration involves a dynamic latent group structure setup, allowing for changes in group composition over time. Lastly, one could delve into a KTR model featuring multiple kinks, with a notable challenge being the efficient identification of multiple thresholds while avoiding the computational burden associated with a grid search method.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}