Econometrics 2024, 12(2), 9; https://doi.org/10.3390/econometrics12020009 (registering DOI) - 16 Apr 2024

Abstract

►

Show Figures

For a panel data linear regression model with both individual and time effects, empirical studies select the two-way random-effects (TWRE) estimator if the Hausman test based on the contrast between the two-way fixed-effects (TWFE) estimator and the TWRE estimator is not rejected. Alternatively,

[...] Read more.

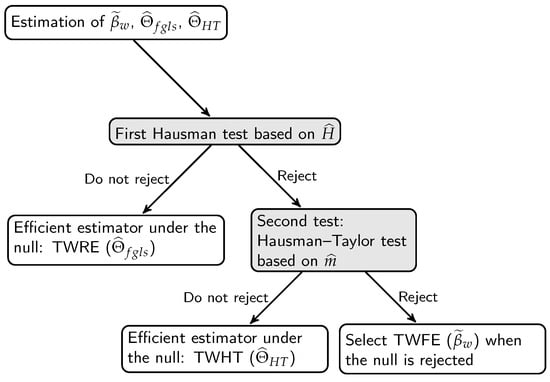

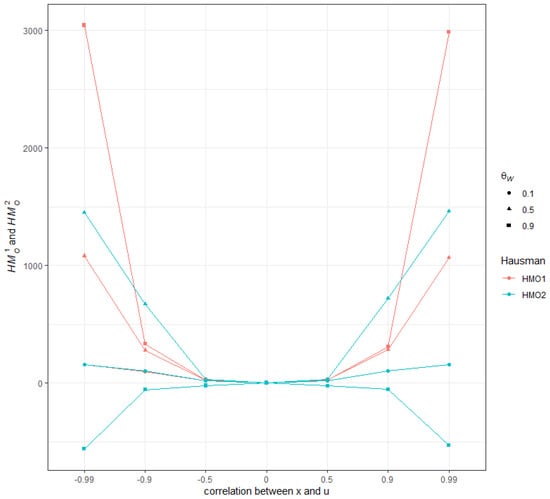

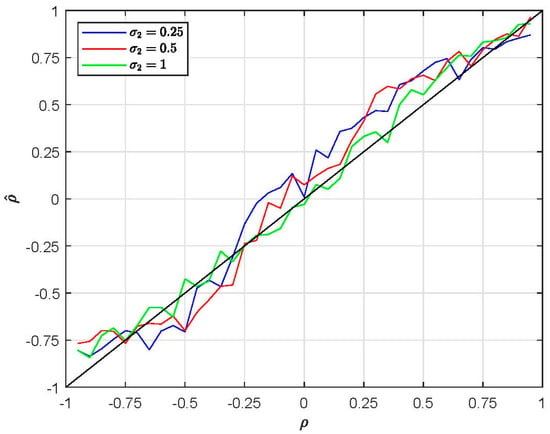

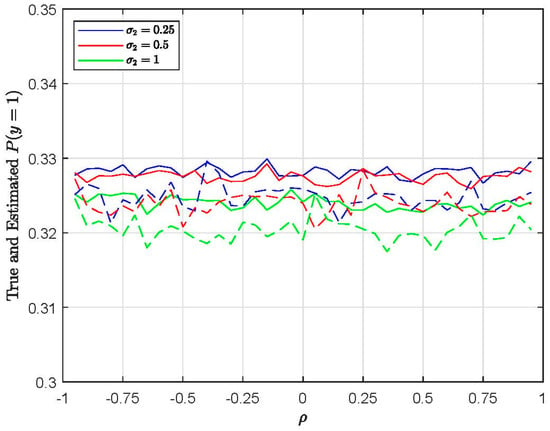

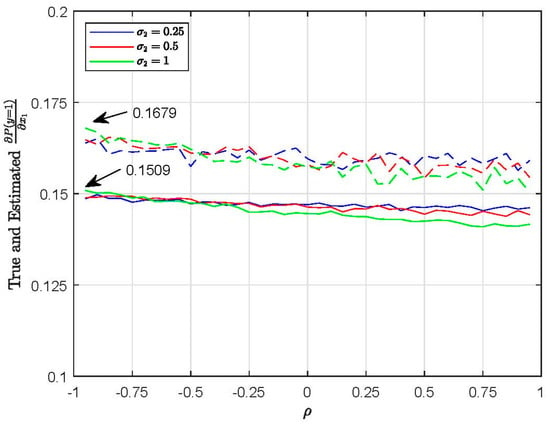

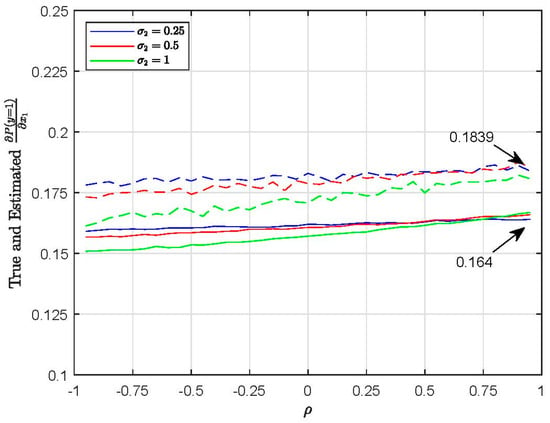

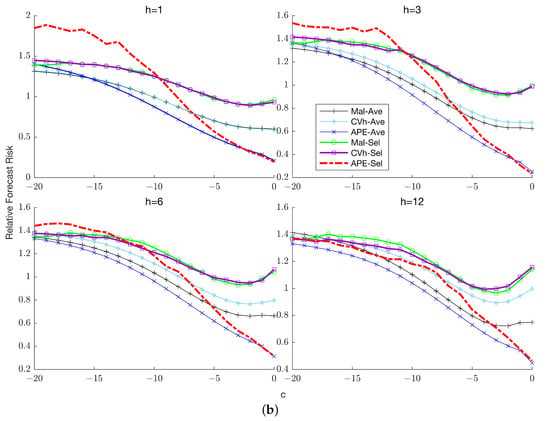

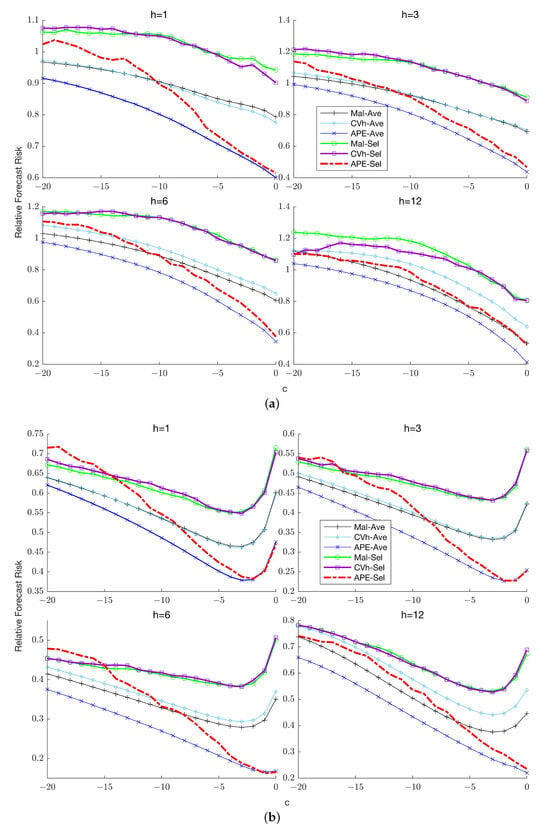

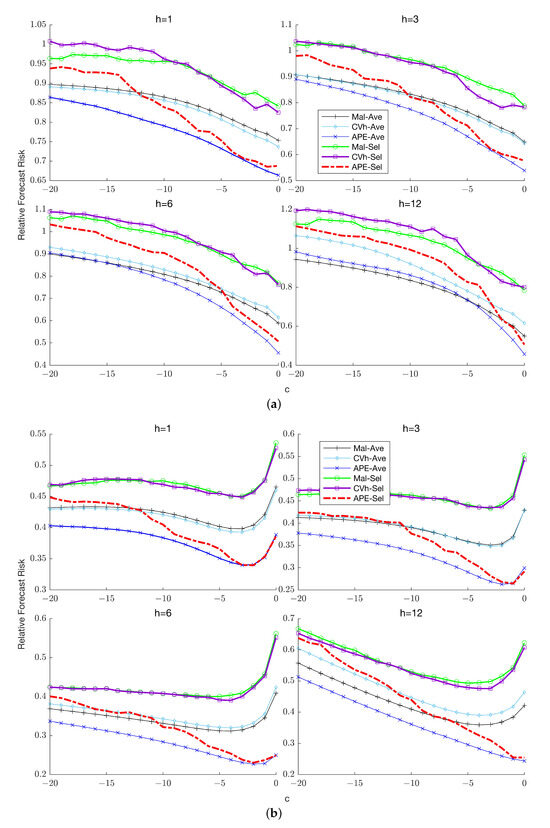

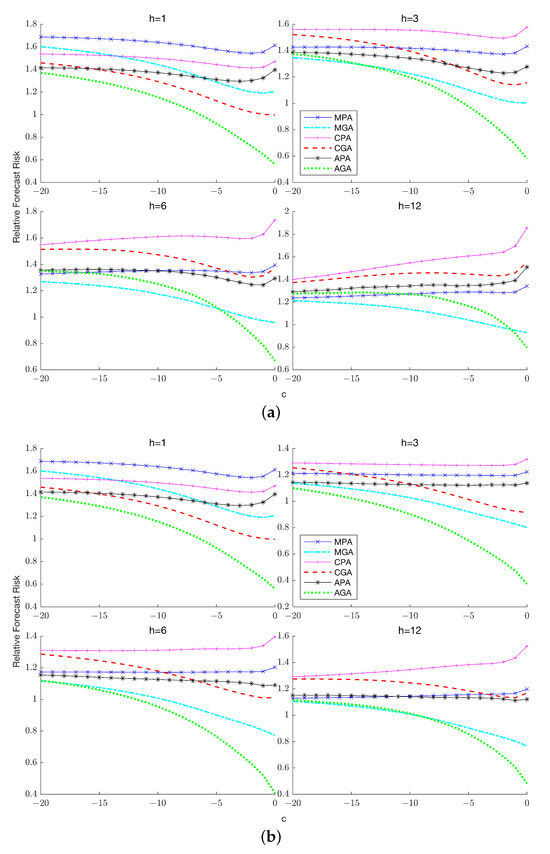

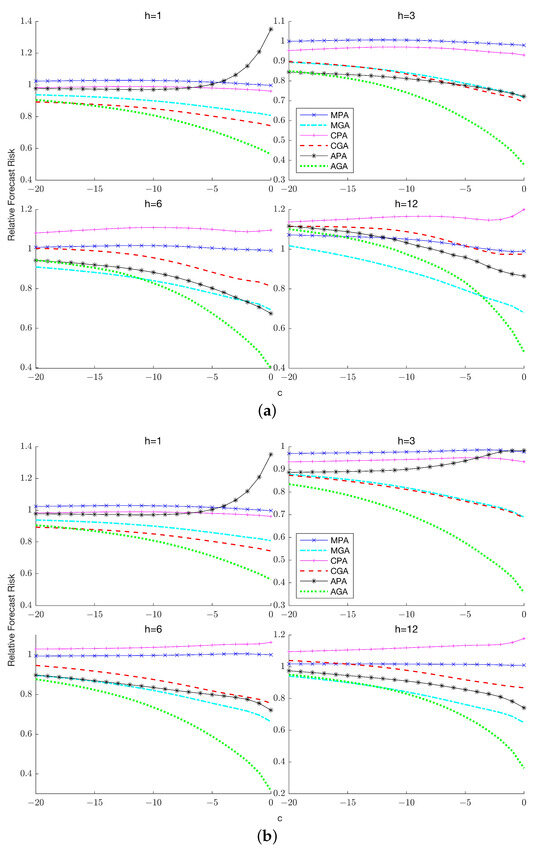

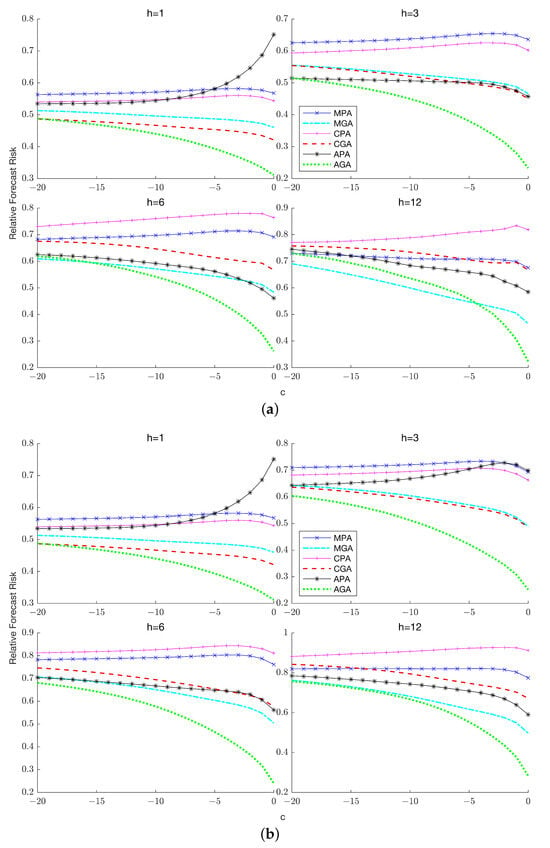

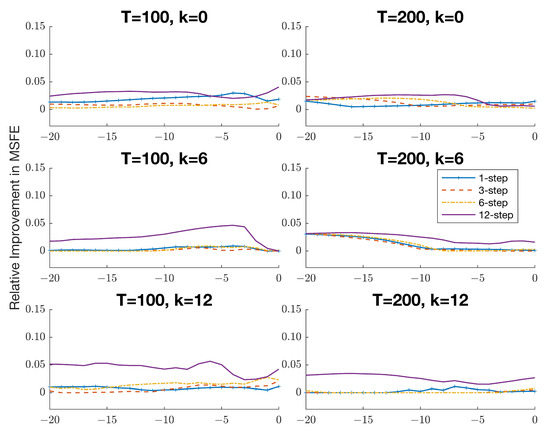

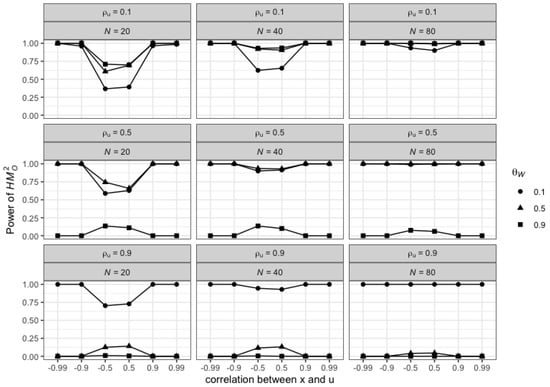

For a panel data linear regression model with both individual and time effects, empirical studies select the two-way random-effects (TWRE) estimator if the Hausman test based on the contrast between the two-way fixed-effects (TWFE) estimator and the TWRE estimator is not rejected. Alternatively, they select the TWFE estimator in cases where this Hausman test rejects the null hypothesis. Not all the regressors may be correlated with these individual and time effects. The one-way Hausman-Taylor model has been generalized to the two-way error component model and allow some but not all regressors to be correlated with these individual and time effects. This paper proposes a pretest estimator for this two-way error component panel data regression model based on two Hausman tests. The first Hausman test is based upon the contrast between the TWFE and the TWRE estimators. The second Hausman test is based on the contrast between the two-way Hausman and Taylor (TWHT) estimator and the TWFE estimator. The Monte Carlo results show that this pretest estimator is always second best in MSE performance compared to the efficient estimator, whether the model is random-effects, fixed-effects or Hausman and Taylor. This paper generalizes the one-way pretest estimator to the two-way error component model.

Full article

Figure 1

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}