1. Introduction

For the past two years, the ongoing global pandemic of the coronavirus outbreak (COVID-19) has received wide coverage by the media. The panic-laden news regarding the daily number of confirmed COVID-19 cases and deaths exert important effects on financial markets in almost all countries around the world, influencing investors’ decisions (

Dyhrberg 2016a;

Ji et al. 2020;

Le et al. 2021;

Milewski and Milewska 2021;

Naeem et al. 2021;

Rokicki et al. 2022;

Salisu and Ogbonna 2021). In response to the novel pandemic, the RavenPack data science team has developed four live and interactive indices (Panic, Sentiment, Infodemic, and Media Coverage)

1 to monitor the global and local positive and negative news articles and public posts about the COVID-19 outbreak. The coronavirus-related indices were proposed to help data-driven professionals in measuring the influence of the COVID-19 pandemic on world affairs.

Zhang et al. (

2018) utilized the multifractal detrended cross-correlation analysis approach to quantify the cross-correlations between Bitcoin and online searches using google. Their results showed that the changes of Google Trends and returns of Bitcoin are highly cross-correlated.

Broadstock and Zhang (

2019) found that the political and economic news, especially from social media, could significantly impact the movements of share prices. They used Twitter messages from social media to develop sentiment measures and showed that these sentiments have pricing power towards intraday stock returns in some US companies.

Chen et al. (

2020) used the hourly Google search queries on COVID-19-related words to examine the effect of fear sentiment caused by the coronavirus outbreak on Bitcoin price. Their findings indicated that Bitcoin failed to act as a safe haven during the outbreak of the coronavirus.

Cepoi (

2020) employed the quantile regression to model the first, second, and third quartiles of the stock returns based on the COVID-19 RavenPack news in six affected countries severely by the pandemic (Spain, USA, UK, France, Germany, and Italy). The author noticed that fake news has a negative nonlinear impact on the first and second quartiles of returns, and gold does not behave as a safe havens asset during the pandemic.

Tan (

2021) examined the impact of COVID-19 pandemic news on Borsa Istanbul by utilizing the quantile regression approach. He found that the dependence between COVID-19-related news and the returns of Borsa Istanbul have an asymmetric dependence—the the correlation coefficient between both variables varies in strength and direction at different quantiles.

Haroon and Rizvi (

2020) showed that the panic induced by coronavirus news can lead to a significant increase in the volatilities in the equity markets perceived to be highly affected by the pandemic.

Shi and Ho (

2021) used the RavenPack Dow Jones News Analytics database to explore the effect of sentiment on changes of volatility in the Dow Jones stocks. He proposed a Markov regime-switching fractionally integrated exponential GARCH model and showed that negative sentiment significantly increases the volatility states of intraday stock returns.

Bouri et al. (

2021) found that the daily newspaper-based index of uncertainty related to infectious diseases can enhance the prediction of gold’s realized variance.

Sun et al. (

2021) found that economic-related announcements and coronavirus-related news do not induce unreasonable investment behaviors.

Béjaoui et al. (

2021) utilized the fractional autoregressive vector model, fractional error correction model, and impulse response functions to analyze the nexus between Bitcoin, social media, and the COVID-19 pandemic. They found that Bitcoin prices and social media networks were influenced by the pandemic.

It has been shown that the responses to negative and positive news are asymmetric—that the impact of negative news on investors’ attitudes is much greater than positive news (see

Soroka 2006). The search for safe commodity assets under conditions of uncertainty is a natural action for most investors.

Kakinaka and Umeno (

2021) showed that the COVID-19 pandemic enhances the herding behavior of investors in the short term but not in the long term. and

Mnif and Jarboui (

2021) found that the COVID-19 pandemic has lessened the herding bias.

Urquhart (

2018) studied investor attention using a trends search for Bitcoin in Google data. He found that the attention to Bitcoin on the previous day has no impact on predicting the volatility and returns of Bitcoin. On the other hand,

Urquhart (

2018) showed that the high realized Bitcoin volatility and returns in the previous days can highly impact the investor attention of Bitcoin. Although

Klein et al. (

2018) and

Smales (

2019) showed that Bitcoin is more volatile than other assets and it should not be treated as a potential safe haven compared with gold,

Shahzad et al. (

2019) suggested that, at best, gold and Bitcoin can be classified as a weak safe-haven assets in some cases. Several authors have suggested that gold and digital cryptocurrencies, especially Bitcoin, can be treated as strategic commodity safe assets during stressful periods (see

Dwita Mariana et al. 2021;

Dyhrberg 2016b;

Guzmán et al. 2021;

Le et al. 2021;

Mnif et al. 2020;

Urquhart and Zhang 2019). In this regard,

Mahdi et al. (

2021) utilized the support vector machine (SVM) algorithm to predict cryptocurrency prices according to the quantile classification of the price of gold during the COVID-19 pandemic.

Bitcoin and gold, like several assets in financial data, have always been highly volatile commodities (

Kim et al. 2020,

2021). Using the ordinary least squares regression model (OLS) to estimate the parameters in such cases can distort the results significantly, whereas the estimates based on the quantile regression models are more robust against outliers compared with OLS models. One shortcoming of using the quantile regression approach is the fact that it cannot easily capture the asymmetric link between the variables. In this regard,

Sim and Zhou (

2015) proposed the quantile-on-quantile regression (QQR) approach to capture the overall dependency between variables.

There is a growing amount of recent financial literature on utilizing the QQR in applications related to cryptocurrencies, gold, oil, and other financial markets and assets. For example,

Bouri et al. (

2017) utilized two approaches based on quantile regression and quantile-on-quantile regression and showed that Bitcoin can act as a hedge against global uncertainty at shorter investment horizons.

Iqbal et al. (

2021) utilized the QQR approach to explore the impact of the COVID-19 pandemic on the top 10 cryptocurrencies globally. Their results revealed that the prices of most digital currencies increased when the COVID-19 had small negative shocks. Only Bitcoin, CRO, ADA, and Ethereum could hold steady when COVID-19 had a huge intensity change.

In this article, we utilize quantile-on-quantile regression (QQR) to examine the relationship between RavenPack COVID-19 news and cryptocurrency and gold returns by modeling the quantiles of the daily returns as a regressand (dependent variable) on the quantiles of the news-based index associated with coronavirus outbreak as a regressor (independent variable). We consider Bitcoin as a proxy for the cryptocurrency market as it is well known as the largest-capped, most prominent digital currency. To the best of our knowledge, this study is the first to use the quantile-on-quantile technique to analyze the effect of COVID-19-related news on Bitcoin and gold returns.

In the rest of the paper,

Section 2 provides brief details about the four selected indices developed from RavenPack regarding COVID-19 news and the study of the local linear quantile regression and quantile-on-quantile regression models.

Section 3 presents descriptive statistics and reports the findings based on the QR and QQR approaches that we use to explore the association between COVID-19 pandemic news and Bitcoin (and gold) returns. The

Section 4 concludes this article.

3. Empirical Results and Discussion

3.1. Summary Statistics

To examine the impact exerted by news-based indices associated with coronavirus outbreaks on two commodities (gold and Bitcoin), we use 374 days from 23 January 2020 to 1 September 2021.

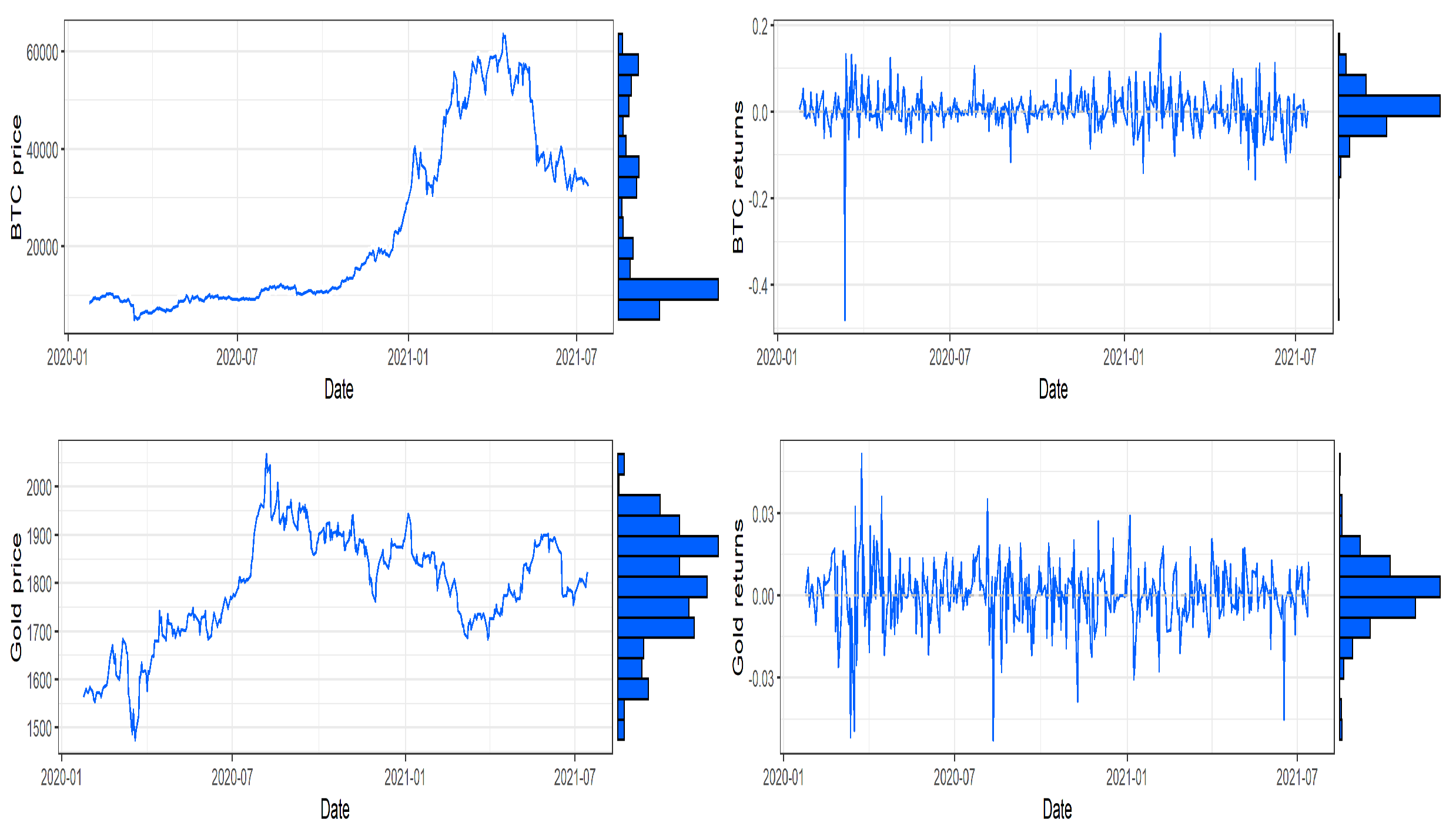

Figure 1 shows the daily Bitcoin and gold prices (left panels) and returns (right panels) throughout the sample period. The graphs show that the prices of Bitcoin are observed to slowly increase during the beginning of the pandemic and then peak remarkably until the mid of May 2021 before they steeply declined, when Tesla announced that it would suspend its vehicle purchases using Bitcoin (

https://www.bbc.com/news/business-57096305 accessed on 5 May 2022).

Regarding gold, it is seen that the prices increased from the beginning of the pandemic until the mid of August 2020, and then they started to fluctuate and decline slowly. The dynamics of returns of gold and Bitcoin show clear evidence of volatility clustering with several outliers and excess positive kurtosis, as seen from the histogram plots, suggesting leptokurtic (heavy-tailed) distributions.

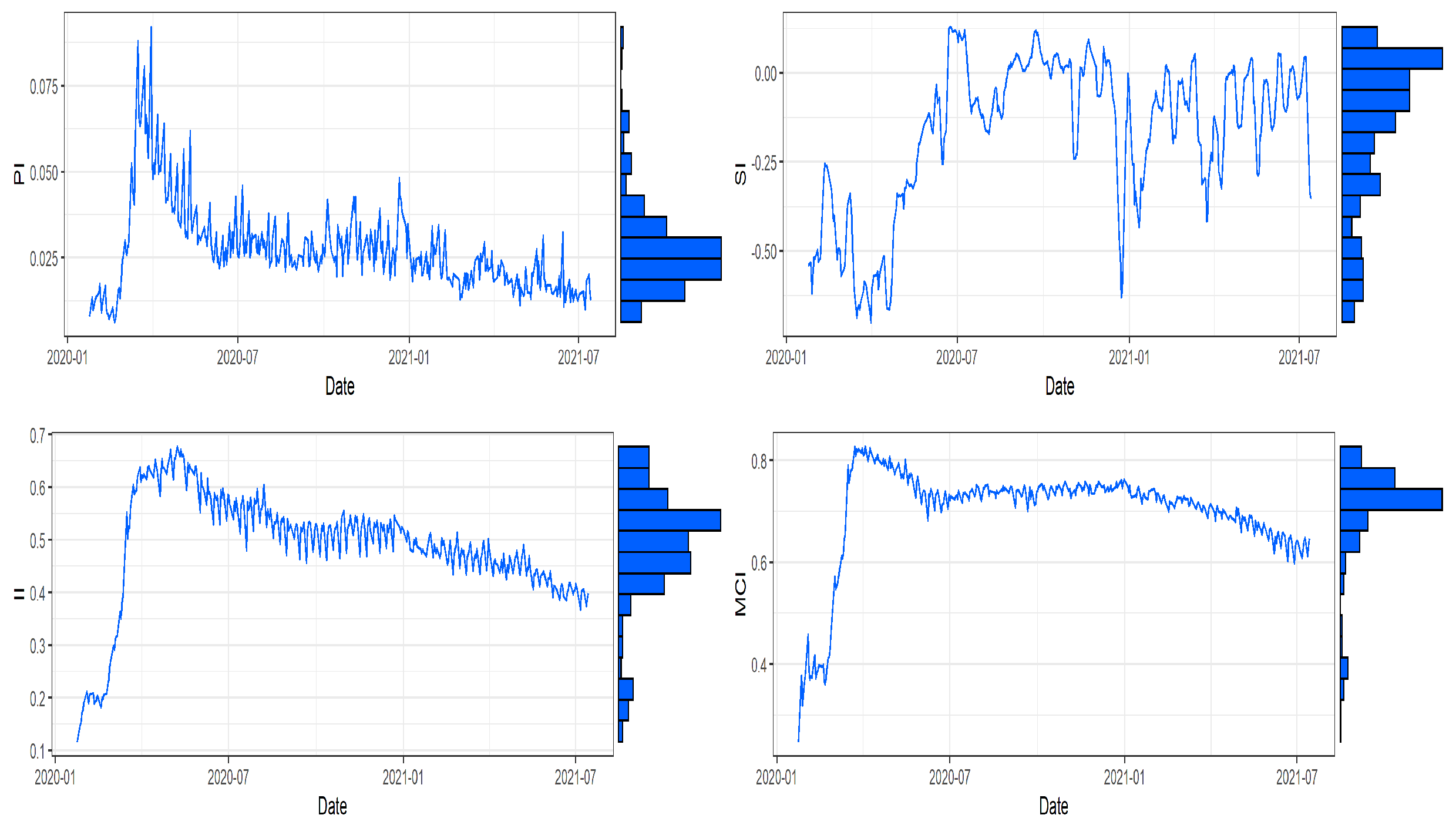

The distribution and trend evolution of daily coronavirus pandemic-related news are plotted in

Figure 2. The graphs demonstrate that all indices (except Sentiment index) reached their highest points by 30 March 2020. This date corresponds to the smallest value of fear sentiment news. Comparing the daily evolution of the Bitcoin and gold returns in

Figure 1 with the trend patterns of all the coronavirus-associated indices in

Figure 2, we noticed positive associations (except for Sentiment index). The correlation between Bitcoin (and gold) returns and the Sentiment index is very weakly negative, indicating that positive sentiment (or optimism) tends to decrease the returns, whereas negative sentiment (or pessimism) is linked to large returns.

Table 2 provides descriptive statistics for all time series data. The daily mean and median of the Bitcoin return are about

. This translates into a monthly return of about

per month and into an annualized return of about

per year. On the other hand, the daily mean and median of the gold return are about

, which can be translated into a monthly return of about

per month and into an annualized return of about

per year. The very small positive values in Bitcoin and gold annualized returns indicate that both commodities could still act as safe havens during the ongoing pandemic.

To test the null hypothesis that the data have a normal distribution, with skewness and excess kurtosis being zeros, we performed a Jarque–Bera (J-B) test statistic. All

p-values of J-B tests are significant at levels less than 1%. Results in

Figure 1 and

Figure 2 and

Table 2 clearly indicate that the distributions of the variables are not normally distributed, hence providing a good reason for utilizing the QQR approach to accommodate the heavy tails data.

Figure 3 displays the correlation coefficients between Bitcoin and gold returns and the four indices induced by the coronavirus news. The correlations vary between

(between Bitcoin and Sentiment index) and

(between Bitcoin and Panic index). For gold returns, the correlations vary from

(between gold and Sentiment index) and

(between gold and Panic index). The very weak correlations between all of the indices induced by the pandemic news and Bitcoin and gold returns indicate that the the traditional ordinary least squares approach will not be able to capture the connection between COVID-19-related news and Bitcoin (and gold) returns. In

Section 3.2, we show that the parameter estimates based on the QR approach, in most cases, are mostly statistically insignificant and tenuous. On the other hand, in

Section 3.3, we show that the QQR offers more information about the link between pandemic-related news and Bitcoin (and gold) returns.

To get a sense of the quantiles of key variables in this paper, graphs in

Figure 4 of Bitcoin and gold return quantiles show similar patterns with returns below approximately the 35th percentile being negative.

Figure 4 presents similar plots for all of the indices (except for the fear sentiment) generated by the COVID-19 pandemic news. Because of the nature of the sentiment index, its quantile plot can be seen in the same manner as other indices. For example, a large negative value of sentiment has a similar interpretation to a large positive panic value.

3.2. Estimates of the QR Model

Several authors noticed that the responses to negative and positive news are asymmetric—that the impact of negative news (as independent variables) on stock returns (as a dependent variable) is much greater than positive news (see

Soroka 2006;

Tan 2021). Such asymmetric responses cannot be captured easily by the traditional quantile regression (QR) technique, as the QR model is developed to uncover the distribution of the dependent variable based on symmetrical (not asymmetrical) effects of independent variables. In such a case, the quantile-on-quantile regression (QQR) is a more robust approach that can be used to provide a more complete picture of dependence. The QQR approach is developed to estimate the effect of the quantiles of an independent variable on the quantiles of the dependent variable.

We first explore what the QR approach can say about the effect of good and bad news related to the COVID-19 pandemic

3 on Bitcoin and gold returns. The QR model in Equation (

4) for the estimated

-quantile of the returns,

, can be written as

where

for

are the estimated parameters as functions of

. The estimated parameters and their corresponding

p-values are given in

Table 3 and

Table 4. The results suggest that only intercept coefficient

makes a significant contribution to the model. This is justifiable as the intercept coefficient reflects the level of

for given levels of

and

; hence, a higher return quantile has a larger intercept parameter. On the other hand, in almost all cases, the effects of COVID-19-related news and 1-lag returns are very weak, as the associated

p-values indicate insufficient evidence to conclude that

and

are significantly different from zero.

3.3. Estimates of the QQR Model

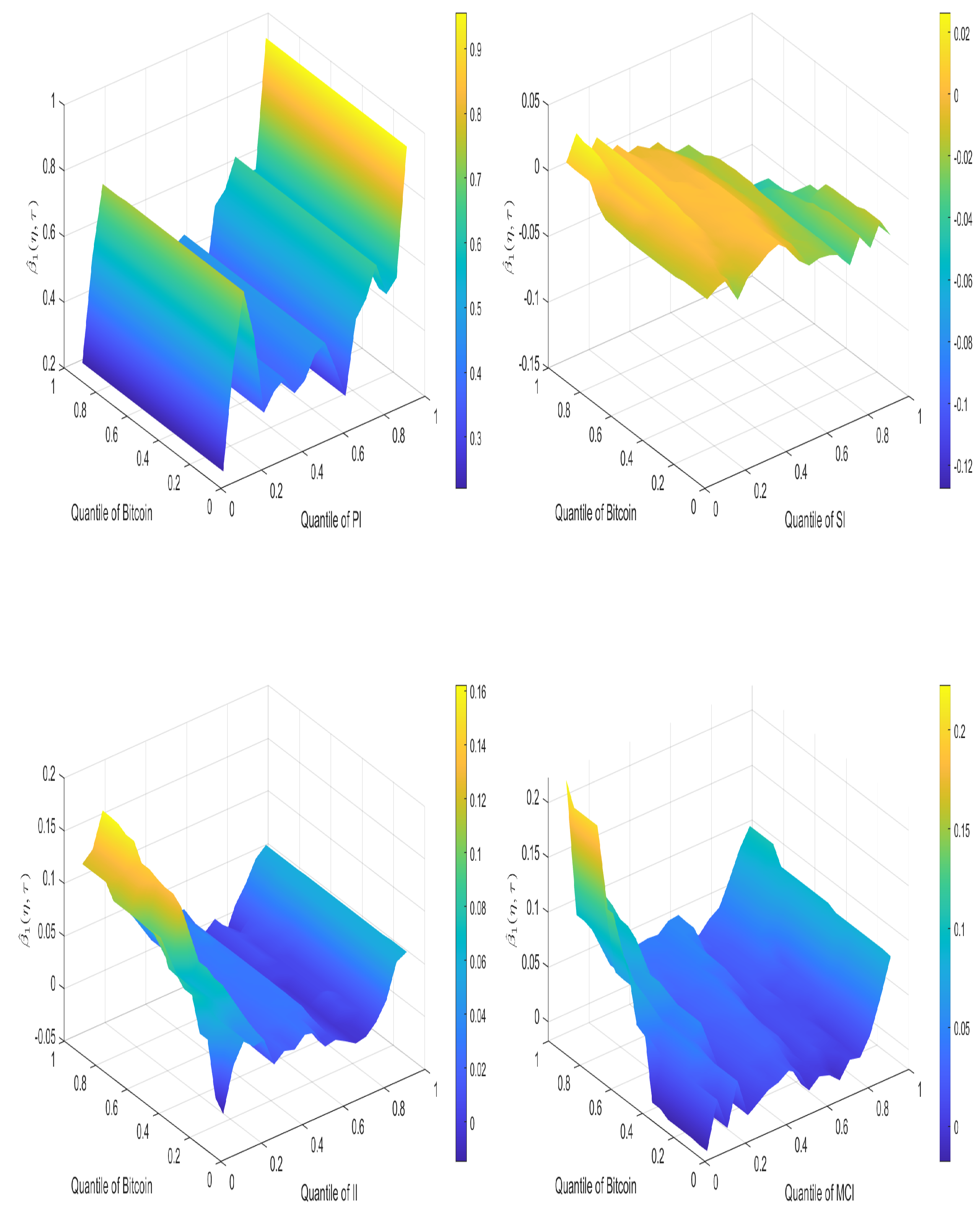

Figure 5 and

Figure 6 present the empirical results from the quantile-on-quantile regression approach that we use to model the daily news-based indices associated with COVID-19 outbreaks and daily returns of Bitcoin and gold. The

x,

y, and

z-axes in the 3D graphs display the

th quantiles of indices induced by coronavirus news, the

th quantiles of returns, and the slope (

) coefficient, respectively. In each graph, the values of the beta coefficient and the relationship move from down to up as the color moves from dark blue (downward), green (middle), and dark yellow (upward). All colors in the vertical bars in

Figure 5 have positive values, whereas the colors move from negative (downward) to positive (upward) in the vertical bars in

Figure 6.

Several interesting results can be concluded from the graphs in

Figure 5. First, the nexus between the media panic index (PI) and Bitcoin returns is dominantly weak, as seen from the fact that the blue color spreads throughout the graph with the exception of the presented yellow color in the uppermost quantiles (90th–95th) of the panic index and all quantiles of Bitcoin returns. The link between uppermost quantiles of the Panic news index and Bitcoin indicates a positive strong association. This means that severely panic-laden news has a positive effect on returns of Bitcoin at most of Bitcoin’s quantiles, and Bitcoin can act as a hedge against media-induced panic.

Examining the Infodemic index (II) and Media Coverage index (MCI), graphs show almost identical patterns of predominantly weak and positive associations with Bitcoin returns for the great majority of combinations of various quantiles. The relation between II and Bitcoin returns is strong in the area represented by the lowermost quantiles (5th–15th) of II and medium to higher quantiles (40th–95th) of Bitcoin returns. For the MCI, the strong relationship is presented in the area represented by the lowermost quantiles (5th–10th) of II and the uppermost quantiles (70th–95th) of Bitcoin returns. Such an asymmetric impact confirms our previous findings that Bitcoin acts as a hedge with a weak safe haven against small and large shocks of infodemic and media coverage induced by coronavirus-related news.

Unlike other indices, the graph shows a strong positive effect of the news Sentiment index (SI) on Bitcoin returns at lower to middle (5th–60th) quantiles of the Sentiment index and all quantiles of Bitcoin returns, after which it turns to be negative from middle to uppermost (60th–95th) quantiles of the Sentiment index and all quantiles of Bitcoin returns. These findings suggest that the fear sentiment induced by coronavirus-related news plays a major role in driving the value of Bitcoin more than other indices.

Moving to gold, the empirical results regarding the cross-sectional dependence between the quantiles of daily news-based indices associated with COVID-19 outbreaks and quantiles of daily returns of gold are presented in

Figure 6.

Examining the graphical depiction of the Pandemic index (PI), we see a clear link between gold returns and panic-laden news associated with the COVID-19 pandemic. The graph demonstrates a huge decline in the value of gold at lowermost quantile (5th–10th) of the Panic news index and uppermost quantile (80th–95th) of gold returns. The link between the Panic index at lower quantiles (10th–30th) and all quantiles of gold returns is represented by blue (dark and light) and light green colors showing a gradual decrease of the negative effect of panic on the value of gold, yet this negative effect turns positive in the area that combines the 30th–80th quantiles of PI and then strong positive in the uppermost (80th–95th) quantiles of the Panic index and all quantiles of gold. Thus, the increase in the level of panic-laden news leads to an increase in the returns of gold, which suggests that gold acted as a safe haven and hedge against media-induced panic.

Although patterns show a strong negative influence of II and MCI on gold returns across the lowermost (5th–25th) quantiles of most of these indices, this negative impact gradually decreases in the grid that combines the 25th–85th quantiles, after which it becomes strong positive in the uppermost (85th–95th) quantiles. This finding indicates that gold acted as a hedge against media-induced II and MCI.

Lastly, the connections between the Sentiment index (SI) and gold returns are strong positive in the grid that combines the lowermost (5th–25th) quantiles of both variables, weak positive in the region that combines the 25th–60th quantiles of SI and almost all quantiles of gold returns, and negative in the area that combines the lowermost quantile of SI and uppermost quartiles (60th–95th) of gold returns and the area that combines the 60th–95th quantiles of SI and all quantiles of gold returns. This confirms the previous notion that the fear sentiment induced by coronavirus-related news plays a major role in driving the value of gold more than other indices.

To summarize the results obtained from

Figure 5 and

Figure 6, we conclude that Bitcoin and gold both can serve as a hedge against the daily index of level of pandemic news.

3.4. Robustness Check for the QQR Approach

In this section, we check the validity of the QQR technique (

Iqbal et al. 2021;

Shahzad et al. 2017;

Sim and Zhou 2015). The QQR model can be seen as an approach that decomposes the estimates of the traditional QR approach, which we can use to obtain a certain estimated parameter at various quantiles of an independent variable. In this article, QR model regresses the

th quantile of Bitcoin (and gold) returns on the indices generated by the COVID-19 pandemic news; hence, the QR parameters are indexed by

only. However, the QQR model regresses the

th quantile of Bitcoin (and gold) returns on the

th quantile of the indices generated by COVID-19 pandemic news, and, hence, its parameters are indexed by

and

. Thus, the QQR approach has more information about the association between COVID-19 pandemic news and Bitcoin (and gold) returns than the quantile approach would, as this relationship is perceived by the QQR approach to be inhomogeneous across

. Given this inherent property of decomposition in the QQR model, it is possible to recover the traditional QR estimates by using the QQR estimates. Specifically, the parameters of the QR model, indexed by

only, can be constructed by averaging the QQR coefficients along

based on the following formula:

where

is the length of the quantiles vector

.

In this regard, one can check the validity of the QQR approach by comparing the estimated by the quantile regression with the average of estimated by the quantile-on-quantile regression, where .

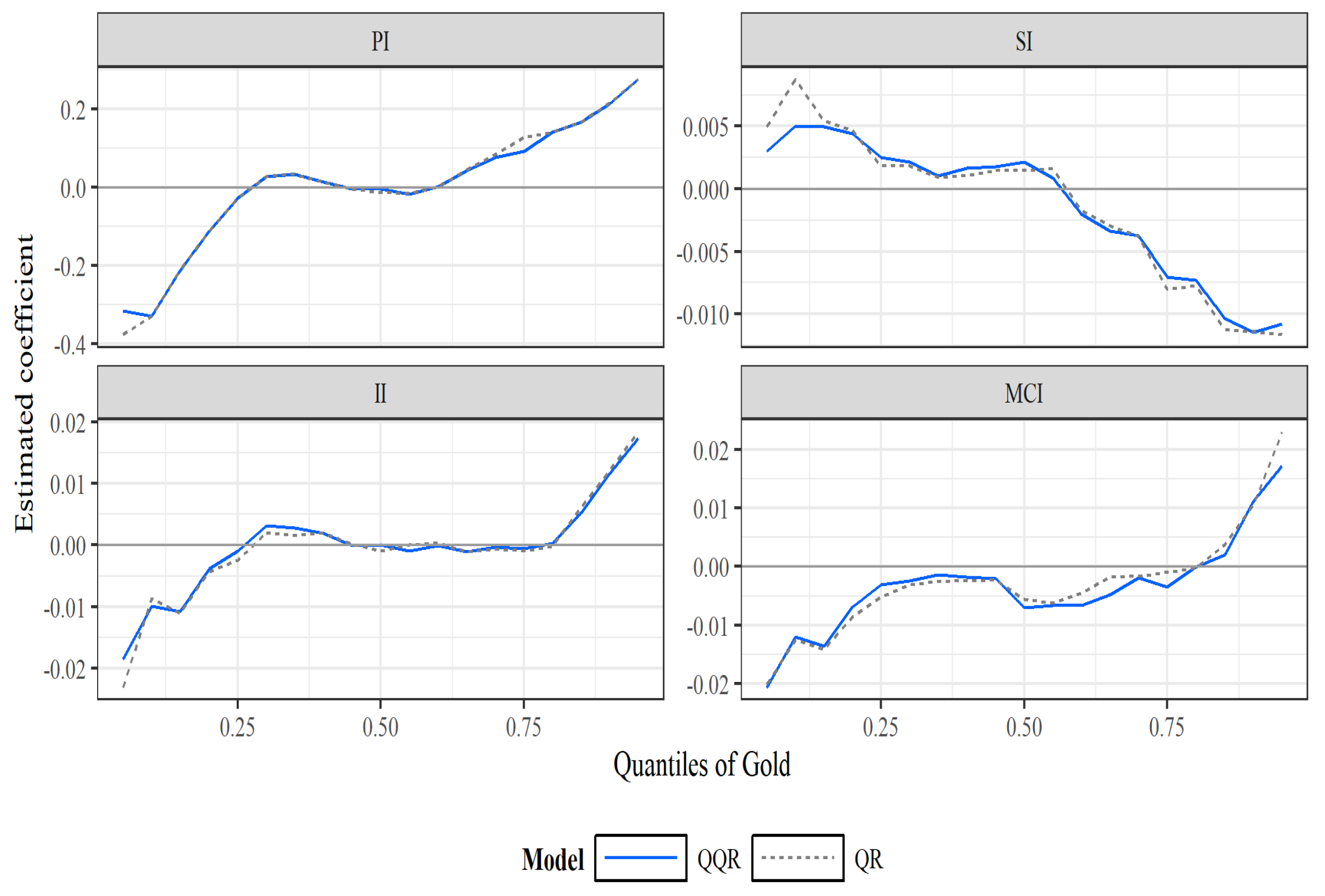

Figure 7 and

Figure 8 compare the estimates of the slope coefficient based on the QR and QQR approaches at various quantiles of Bitcoin and gold returns, respectively. The graphs show that the QQR estimates are nearly identical with the QR estimates, which validate the results that the QR estimates can be recovered from the QQ estimates.

4. Concluding Remarks

In this work, we utilize the quantile-on-quantile approach to model the relationship between the RavenPack news-based index associated with the coronavirus pandemic and the returns of two commodities, Bitcoin and gold, over the period 23 January 2020–30 September 2021.

In most cases, we find that the traditional quantile regression approach fails to discover the comprehensive relationship between the variables due to asymmetric impacts of positive and negative shocks in coronavirus-related news on the distribution of the Bitcoin and gold returns. On the other hand, we show that the quantile-on-quantile regression is a better approach to capture the overall dependency between variables.

Examining the impact of the coronavirus panic index on both commodities shows a positive relationship. The increase in the level of panic-laen news leads to an increase in the returns of Bitcoin and gold, which suggests that Bitcoin and gold acted as a safe haven and hedge against media-induced panic.

The impacts of Infodemic and Media Coverage indices on Bitcoin and gold demonstrate that the different levels of these indices affect the returns of Bitcoin and gold asymmetrically, and both commodities act as a hedge against the extreme levels of these indices.

Lastly, the outcomes show that the sentiment induced by coronavirus-related news plays a major role in driving the values of Bitcoin and gold more than other indices. More fear sentiment leads to an increase in the returns.

We conclude that COVID-19 pandemic-related news encourages people to invest in gold and Bitcoin as the outcome results reveal that both commodities, Bitcoin and gold, can serve as a hedge against pandemic-related news.

The idea that we use in this research can be extended to investigate the relationship between the RavenPack news-based index associated with coronavirus outbreak and other cryptocurrencies.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}