Determinants of Bank Closures: What Ensures Sustainable Profitability in Mobile Banking?

Abstract

:1. Introduction

2. Background

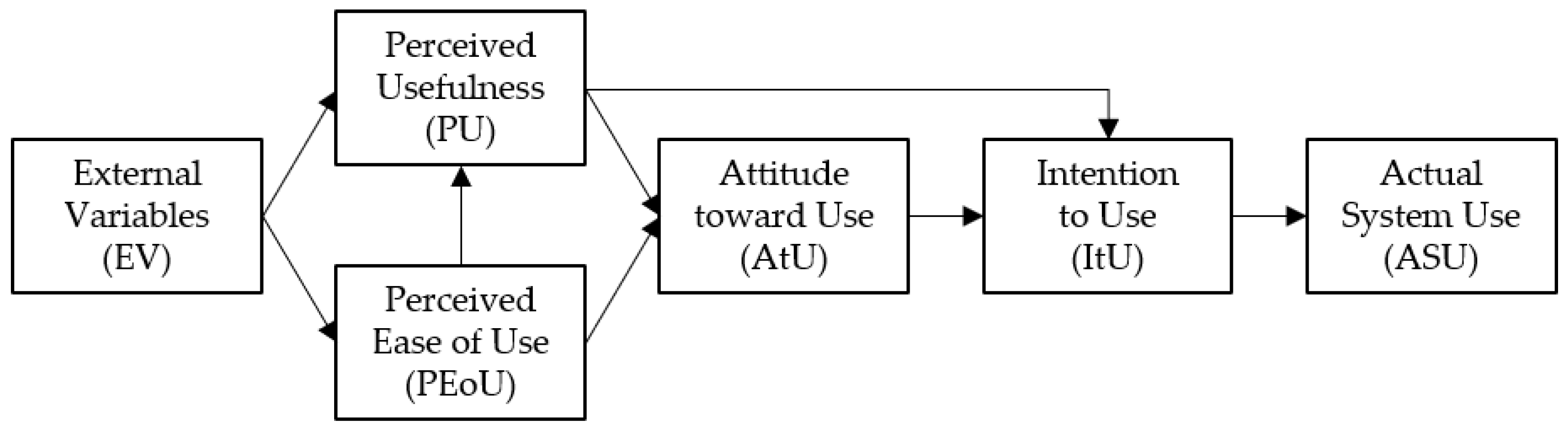

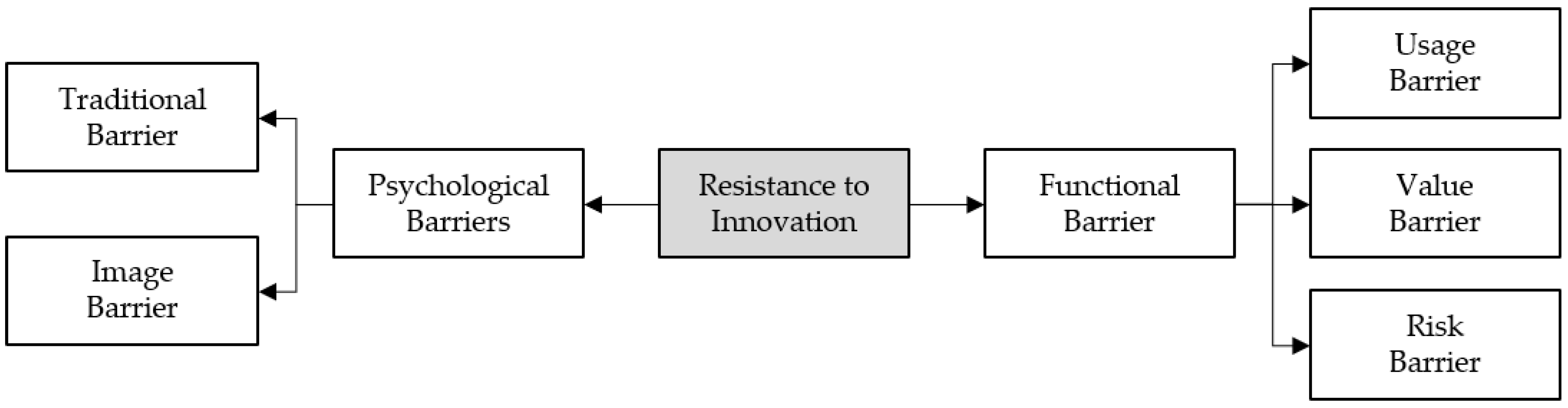

2.1. The Development of a Self-Service Channel and Customer Responses

2.2. FinTech Development and Smart Financing

2.3. Bank Profitability Analysis and Financial Services

3. Methodology

3.1. Data Collection and Descriptive Analysis

3.2. Hypotheses

4. Results

4.1. Test for H1

4.2. Test for H2

5. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Chun, K.W.; Kim, H.; Lee, K. A study on research trends of technologies for Industry 4.0; 3D printing, artificial intelligence, big data, cloud computing, and internet of things. In Advanced Multimedia and Ubiquitous Engineering; Springer: Singapore, 2018; pp. 397–403. [Google Scholar]

- Mehdiabadi, A.; Tabatabeinasab, M.; Spulbar, C.; Yazdi, A.K.; Birau, R. Are We Ready for the Challenge of Banks 4.0? Designing a Roadmap for Banking Systems in Industry 4.0. Int. J. Financial Stud. 2020, 8, 32. [Google Scholar] [CrossRef]

- Setiawan, B. Internal Working Conditions and Well-being of Bank Employees during the Pandemic: A Case Study of Yogya-karta City. J. Econ. Res. Soc. Sci. 2022, 6, 107–114. [Google Scholar]

- Sharma, S.K.; Sharma, M. Examining the role of trust and quality dimensions in the actual usage of mobile banking ser-vices: An empirical investigation. Int. J. Inf. Manag. 2019, 44, 65–75. [Google Scholar] [CrossRef]

- Giovanis, A.; Assimakopoulos, C.; Sarmaniotis, C. Adoption of mobile self-service retail banking technologies: The role of technology, social, channel and personal factors. Int. J. Retail. Distrib. Manag. 2018, 47, 9. [Google Scholar] [CrossRef]

- Baabdullah, A.M.; Rana, N.P.; Alalwan, A.A.; Islam, R.; Patil, P.; Dwivedi, Y.K. Consumer Adoption of Self-Service Technologies in the Context of the Jordanian Banking Industry: Examining the Moderating Role of Channel Types. Inf. Syst. Manag. 2019, 36, 286–305. [Google Scholar] [CrossRef]

- Filotto, U.; Caratelli, M.; Fornezza, F. Shaping the digital transformation of the retail banking industry. Empirical evidence from Italy. Eur. Manag. J. 2021, 39, 366–375. [Google Scholar] [CrossRef]

- Rafique, H.; Almagrabi, A.O.; Shamim, A.; Anwar, F.; Bashir, A.K. Investigating the acceptance of mobile library appli-cations with an extended technology acceptance model (TAM). Comput. Educ. 2020, 145, 103732. [Google Scholar] [CrossRef]

- Parasuraman, A. Technology Readiness Index (TRI) a multiple-item scale to measure readiness to embrace new technologies. J. Serv. Res. 2020, 2, 307–320. [Google Scholar] [CrossRef]

- Compernolle, M.V.; Buyle, R.; Mannens, E.; Vanlishout, Z.; Vlassenroot, E.; Mechant, P. “Technology readiness and ac-ceptance model” as a predictor for the use intention of data standards in smart cities. Media Commun. 2020, 6, 127–139. [Google Scholar]

- Dhagarra, D.; Goswami, M.; Kumar, G. Impact of Trust and Privacy Concerns on Technology Acceptance in Healthcare: An Indian Perspective. Int. J. Med. Inform. 2020, 141, 104164. [Google Scholar] [CrossRef]

- Bradford, M.; Florin, J. Examining the role of innovation diffusion factors on the implementation success of enterprise re-source planning systems. Int. J. Account. Inf. Syst. 2003, 4, 205–225. [Google Scholar] [CrossRef]

- Talwar, S.; Talwar, M.; Kaur, P.; Dhir, A. Consumers’ resistance to digital innovations: A systematic review and frame-work development. Australas. Mark. J. (AMJ) 2003, 28, 286–299. [Google Scholar] [CrossRef]

- Lashitew, A.A.; van Tulder, R.; Liasse, Y. Mobile phones for financial inclusion: What explains the diffusion of mobile money innovations? Res. Policy 2019, 48, 1201–1215. [Google Scholar] [CrossRef]

- Farah, M.F.; Hasni, M.J.S.; Abbas, A.K. Mobile-banking adoption: Empirical evidence from the banking sector in Pakistan. Int. J. Bank Mark. 2018, 17, 215. [Google Scholar] [CrossRef]

- Shareef, M.A.; Baabdullah, A.; Dutta, S.; Kumar, V.; Dwivedi, Y.K. Consumer adoption of mobile banking services: An empirical examination of factors according to adoption stages. J. Retail. Consum. Serv. 2018, 43, 54–67. [Google Scholar] [CrossRef] [Green Version]

- Allen, F.; Gu, X.; Jagtiani, J. A Survey of Fintech Research and Policy Discussion. Rev. Corp. Finance 2021, 1, 259–339. [Google Scholar] [CrossRef]

- Ashta, A.; Herrmann, H. Artificial intelligence and fintech: An overview of opportunities and risks for banking, investments, and microfinance. Strat. Chang. 2021, 30, 211–222. [Google Scholar] [CrossRef]

- Cheng, M.; Qu, Y. Does bank FinTech reduce credit risk? Evidence from China. Pac.-Basin Finance J. 2020, 63, 101398. [Google Scholar] [CrossRef]

- Hong, K.; Lee, J.W. Banking and Finance in the Republic of Korea. In Routledge Handbook of Banking and Finance in Asia; Routledge: London, UK, 2020; pp. 106–120. [Google Scholar]

- Nguyen, T.H. Impact of Bank Capital Adequacy on Bank Profitability under Basel II Accord: Evidence from Vietnam. J. Econ. Dev. 2020, 45, 31–36. [Google Scholar]

- Wang, C.-W.; Chiu, W.-C.; King, T.-H.D. Debt maturity and the cost of bank loans. J. Bank. Finance 2017, 112, 105235. [Google Scholar] [CrossRef]

- Caby, J.; Ziane, Y.; Lamarque, E. The impact of climate change management on banks profitability. J. Bus. Res. 2022, 142, 412–422. [Google Scholar] [CrossRef]

- Leo, M.; Sharma, S.; Maddulety, K. Machine Learning in Banking Risk Management: A Literature Review. Risks 2019, 7, 29. [Google Scholar] [CrossRef] [Green Version]

- Li, F.; Lu, H.; Hou, M.; Cui, K.; Darbandi, M. Customer satisfaction with bank services: The role of cloud services, security, e-learning and service quality. Technol. Soc. 2020, 64, 101487. [Google Scholar] [CrossRef]

- Fida, B.A.; Ahmed, U.; Al-Balushi, Y.; Singh, D. Impact of Service Quality on Customer Loyalty and Customer Satisfaction in Islamic Banks in the Sultanate of Oman. SAGE Open 2020, 10, 9517. [Google Scholar] [CrossRef]

- Wongsansukcharoen, J. Effect of community relationship management, relationship marketing orientation, customer engagement, and brand trust on brand loyalty: The case of a commercial bank in Thailand. J. Retail. Consum. Serv. 2021, 64, 102826. [Google Scholar] [CrossRef]

- Davis, K.; Oever, P.V.D. Age Relations and Public Policy in Advanced Industrial Societies. Popul. Dev. Rev. 1981, 7, 2761. [Google Scholar] [CrossRef]

- Myles, J.F. ConflictCrisis, and the Future of Old Age Security. In Readings in the Political Economy of Aging; Routledge: London, UK, 2019; pp. 168–176. [Google Scholar]

- Shindul-Rothschild, J.; Williamson, J.B. Future Prospects for Aging Policy Reform. In Critical Perspectives on Aging; Routledge: London, UK, 2020; pp. 325–340. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Commercial Bank | Manned Branch | Unmanned Branch |

|---|---|---|

| Shinhan Bank | 784 | 2589 |

| Kookmin Bank | 925 | 3060 |

| KEB-Hana Bank | 624 | 2524 |

| Woori Bank | 792 | 2163 |

| NH Bank | 1118 | 2252 |

| Year | Establishment | Closure | Diff. |

|---|---|---|---|

| 2017 | 127 | 244 | −117 |

| 2018 | 71 | 60 | 11 |

| 2019 | 63 | 71 | −8 |

| 2020 | 25 | 88 | −63 |

| 2021 | 8 | 276 | −268 |

| Variable | Requirement |

|---|---|

| Customers’ ID (Pre-masked) | Primary key (unique value) has only one value |

| Age | 0 = under 20 s, 1 = 30 s, 2 = 40 s, 3 = 50 s, 4 = over 60 s |

| Age group | 0 = including and under 55, 1 = over 55 |

| Customer classification | 0 = PB, 1 = PRB, 2 = PfB, 3 = PsB, 4 = SME |

| Branch classification | 0 = closed branch, 1 = nearby branch from closed one |

| Branch closure date | Nearby branch applies null value |

| Number of online transactions per year | Distinct var. before/after closure: create additional var. |

| Number of mobile transactions per year | Same as above |

| Number of online & mobile transactions | Same as above |

| Online banking activation | If the number of annual banking transactions is greater than 1, otherwise 0 |

| Mobile banking activation | Same as above |

| Gross annual net income | Distinct var. before/after closure: create additional var. |

| Online banking net income | Same as above |

| Mobile banking net income | Same as above |

| Other accrued net income | Same as above |

| Number of financial products annually | Same as above |

| Division | Period before Branch Closure | Period after Bank Closure | Change (%) | |||

|---|---|---|---|---|---|---|

| Number of customers | Youth and young people (Including and under the age of 55) | 311,710 | 69.2% | 322,048 | 68.8% | |

| Middle-aged and the elderly people (Over the age of 55) | 136,768 | 30.8% | 146,056 | 31.2% | ||

| Total | 448,478 | 100.0% | 468,104 | 100.0% | ||

| Activated customers, activation rate of online & mobile banking (persons, %) | Youth and young people | 201,676 | 64.7% | 294,996 | 91.6% | 26.9% |

| Middle-aged and elderly people | 13,950 | 10.2% | 80,039 | 54.8% | 44.6% | |

| Total | 215,626 | 48.1% | 375,035 | 80.1% | 32.0% | |

| Annual online & mobile banking transactions (cases) | Youth and young people | 45,193,060 | 110,328,492 | |||

| (Per person) | 225 | 374 | 66.2% | |||

| Middle-aged and elderly people | 518,186 | 8,324,024 | ||||

| (Per person) | 37 | 104 | 181.1% | |||

| Total | 45,711,246 | 118,652,516 | ||||

| (Per person) | 262 | 478 | 82.4% | |||

| Gross annual net income (per person, KR Won) | Youth and young people | 455,708 | 477,092 | |||

| Middle-aged and elderly people | 468,256 | 503,572 | ||||

| Net income generated from online & mobile banking per year (per person, KR Won) | Youth and young people | 306,692 | 67.3% | 339,690 | 71.2% | |

| Middle-aged and elderly people | 63,682 | 13.6% | 159,128 | 31.6% | ||

| Annual face-to-face (counter) net profit (per person, KR Won) | Youth and young people | 149,016 | 32.7% | 137,402 | 28.8% | |

| Middle-aged and elderly people | 404,574 | 86.4% | 344,439 | 68.4% | ||

| No. | Closed Branch | Nearby Branch | No. | Closed Branch | Nearby Branch |

|---|---|---|---|---|---|

| 1 | Bundang Sunae-dong | Bundang Central | 23 | Ujangsan Station | Hwagok Station |

| 2 | Teheranro, Finance Center | Seolleung Corp. Finance | 24 | Moran Station | Seongnam Central |

| 3 | Gangnam-daero Center | Gangnam Finance | 25 | Bundang Jeongja-dong | Bundang |

| 4 | Jongno 3-ga | Jongno Finance | 26 | Park Dal-dong | Anyang Finance |

| 5 | Gachon University | Seongnam | 27 | Dongtan Cheonggye | Dongtan Station Finance |

| 6 | Ingye-dong | Suwon Central | 28 | Yeokgok | Bucheon Station |

| 7 | Banghwa-dong | Banghwa Station | 29 | Seoknam-dong | Gajwa-dong |

| 8 | Bundang Top Village | Yatap Station | 30 | Gocheok Intersection | Gaebong-dong |

| 9 | Shingeumho Station | Haengdang-dong | 31 | Heukseok-dong | Sangdo Station |

| 10 | Pyeongchang-dong | Hyoja-dong | 32 | Sindorim-dong | Guro Station |

| 11 | Wonhyo-ro | Yongsan Electronics | 33 | Siheung-daero | Siheung-dong |

| 12 | Samseongyo | Daehak-ro | 34 | Changdong Station | Nowon Station |

| 13 | Dangsan Central | Yeongdeungpo | 35 | Dongducheon | Yangju Finance |

| 14 | Walkerhill | Gwangjang-dong | 36 | Galhyeon-dong | Yeonsinnae |

| 15 | Pyeongchon (South) | Pyeongchon | 37 | Malli-dong | Mapo |

| 16 | Konjiam Finance | Gwangju Finance | 38 | Ahyeon-dong | Chungjeong-ro |

| 17 | Nonhyeon Station | Nonhyeon-dong | 39 | Yangjae Hibrand | Yangjae Station Finance |

| 18 | Bangi-dong | Jamsil Finance | 40 | Sinseol-dong | Changsin-dong Finance |

| 19 | Seongsan-dong | Sangam Finance | 41 | Gangseo | Gayang Station |

| 20 | Apgujeong (West) | Apgujeong Station | 42 | Daerim-dong | Daelim Central |

| 21 | Jukjeon | Jukjeon Central | 43 | Jeongneung | Gileum-dong |

| 22 | Cheongdam Station | Cheongdam-dong | 44 | Mangu-dong | Sangbong Station |

| Variables | Operational Definition | Abbreviation |

|---|---|---|

| Independent Var. | - Number of customers per branch (CST) | CST |

| - Number of secedes in closed branches (SCD) | SCD | |

| - Number of operational staffs per branch (STF) | STF | |

| - Operation and maintenance cost (OMC) | OMC | |

| - Real property cost for branch leasing (RPC) | RPC | |

| Dependent Var. | - Rate of return | RVN |

| Control (or Exogenous) Var. | - Total assets for each branch | TAS |

| - Current assets each branch | LQD | |

| - Debt ratio for each branch | FLV | |

| - KOSPI index daily (applied simultaneously) | KSP |

| Activated Customers (AC) | Non-Activated Customers (NC) | |||

|---|---|---|---|---|

| Youth and Young People (YY) | [YY-AC] | [YY-NC] | ||

| Closed branches vs. Nearby & post-integrated branches (Contribution to customer revenue through comparison of changes in bank net profit before and after branch closure-integration) | ||||

| Middle-aged and The elderly people (ME) | ||||

| [ME-AC] | [ME-NC] | |||

| Div. | Variance | DF | t-Value | p-Value |

|---|---|---|---|---|

| Pooled | Equal | 294,994 | 0.2584 | 0.248 |

| Satterthwaite | Unequal | 292,541,182 | 0.2581 | 0.248 |

| Equality of Variance | Num DF | Den DF | F-Value | p-Value |

| Fooled F | 151,304 | 143,692 | 1.05 | 0.7852 |

| Div. | Variance | DF | t-Value | p-Value |

|---|---|---|---|---|

| Pooled | Equal | 80,037 | 0.2152 | 0.351 |

| Satterthwaite | Unequal | 80,035,245 | 0.2150 | 0.351 |

| Equality of Variance | Num DF | Den DF | F-Value | p-Value |

| Fooled F | 40,407 | 39,632 | 1.02 | 0.842 |

| Div. | Variance | DF | t-Value | p-Value |

|---|---|---|---|---|

| Pooled | Equal | 27,050 | 0.3214 | 0.482 |

| Satterthwaite | Unequal | 27,048,254 | 0.3211 | 0.482 |

| Equality of Variance | Num DF | Den DF | F-Value | p-Value |

| Fooled F | 14,192 | 12,860 | 1010 | 0.754 |

| Div. | Variance | DF | t-Value | p-Value |

|---|---|---|---|---|

| Pooled | Equal | 66,017 | 15.0413 | <0.0001 |

| Satterthwaite | Unequal | 66,012,851 | 13.8547 | <0.0001 |

| Equality of Variance | Num DF | Den DF | F-Value | p-Value |

| Fooled F | 33,943 | 32,074 | 1.06 | 0.822 |

| Activated Customers (AC) | Non-Activated Customers (NC) | |||

|---|---|---|---|---|

| Youth and Young People (YY) | [YY-AC] CNP of Closed Brs. (=) CNP of Nearby Brs. | [YY-NC] CNP of Closed Brs. (=) CNP of Nearby Brs. | ||

| Comparison to CNP * (* CNP: Changes in bank net profit before and after branch closure) | ||||

| Middle-aged and The elderly people (ME) | ||||

| [ME-AC] CNP of Closed Brs. (=) CNP of Nearby Brs. | [ME-NC] CNP of Closed Brs. (<) CNP of Nearby Brs. | |||

| No. | RVN | CST | SCD | STF | OMC | RPC | TAS | LQD | FLV | KSP |

|---|---|---|---|---|---|---|---|---|---|---|

| 1 | −22.4 | −23.6 | −18.6 | −19.3 | −14.3 | −12.3 | −20.3 | −6.5 | −6.2 | −8.5 |

| 2 | −24.6 | −25.4 | −17.6 | −18.2 | −12.1 | −13.9 | −18.7 | −9.2 | −4.7 | −7.6 |

| 3 | −23.5 | −25.2 | −19.7 | −20.8 | −9.5 | −14.2 | −19.2 | −7.5 | −3.4 | −4.9 |

| 4 | −22.4 | −22.6 | −17.6 | −18.3 | −14.3 | −11.3 | −19.3 | −6.5 | −5.2 | −7.5 |

| 5 | −24.6 | −26.4 | −18.6 | −18.2 | −12.1 | −14.9 | −19.7 | −10.2 | −5.7 | −8.6 |

| 6 | −22.5 | −25.2 | −18.7 | −20.8 | −9.5 | −13.2 | −18.2 | −7.5 | −2.4 | −3.9 |

| 7 | −22.4 | −23.6 | −18.6 | −19.3 | −15.3 | −12.3 | −20.3 | −6.5 | −6.2 | −7.5 |

| 8 | −24.6 | −25.4 | −17.6 | −18.2 | −12.1 | −13.9 | −19.7 | −10.2 | −4.7 | −7.6 |

| 9 | −23.5 | −25.2 | −18.7 | −21.8 | −10.5 | −13.2 | −18.2 | −7.5 | −3.4 | −3.9 |

| 10 | −22.4 | −23.6 | −18.6 | −18.3 | −14.3 | −11.3 | −19.3 | −6.5 | −5.2 | −7.5 |

| 11 | −25.6 | −25.4 | −18.6 | −18.2 | −13.1 | −13.9 | −19.7 | −10.2 | −4.7 | −7.6 |

| 12 | −23.5 | −25.2 | −18.7 | −21.8 | −9.5 | −12.2 | −17.2 | −6.5 | −3.4 | −3.9 |

| 13 | −23.4 | −23.6 | −19.6 | −18.3 | −14.3 | −11.3 | −19.3 | −7.5 | −5.2 | −7.5 |

| 14 | −24.6 | −25.4 | −18.6 | −17.2 | −12.1 | −12.9 | −18.7 | −9.2 | −3.7 | −6.6 |

| 15 | −23.5 | −25.2 | −18.7 | −22.8 | −10.5 | −12.2 | −17.2 | −7.5 | −3.4 | −3.9 |

| … | … | … | … | … | … | … | … | … | … | … |

| 40 | −22.4 | −21.6 | −19.6 | −19.3 | −15.3 | −10.3 | −18.3 | −7.5 | −4.2 | −7.5 |

| 41 | −25.6 | −25.4 | −17.6 | −17.2 | −12.1 | −11.9 | −18.7 | −10.2 | −3.7 | −6.6 |

| 42 | −21.5 | −25.2 | −17.7 | −22.8 | −9.5 | −11.2 | −17.2 | −7.5 | −2.4 | −2.9 |

| 43 | −23.4 | −21.6 | −19.6 | −19.3 | −15.3 | −10.3 | −18.3 | −7.5 | −4.2 | −7.5 |

| 44 | −25.6 | −25.4 | −16.6 | −16.2 | −11.1 | −11.9 | −18.7 | −10.2 | −3.7 | −5.6 |

| Independent Var. | RVN | Result | |

|---|---|---|---|

| Closed Branch | CST | 0.04 | Sig ** |

| SCD | 0.02 | Sig ** | |

| STF | 0.03 | Sig ** | |

| OMC | 0.05 | Sig ** | |

| RPC | 0.01 | Sig *** | |

| Nearby & Post-integrated Branch | CST | 0.03 | Sig ** |

| SCD | <0.01 | Sig *** | |

| STF | 0.02 | Sig ** | |

| OMC | 0.03 | Sig ** | |

| RPC | <0.01 | Sig *** | |

| Independent Var. | RVN | |||

|---|---|---|---|---|

| Immediate | Accumulative | Wear-In Time | ||

| Closed Branch | CST | 0.009 | 0.358 ** | 3.6 |

| SCD | 0.013 ** | 0.421 ** | 2.9 | |

| STF | 0.008 | 0.377 ** | 3.5 | |

| OMC | 0.011 ** | 0.394 ** | 4.9 | |

| RPC | 0.014 ** | 0.449 *** | 2.7 | |

| Nearby & Post-integrated Branch | CST | 0.026 *** | 0.574 *** | 1.9 |

| SCD | 0.032 *** | 0.617 *** | 1.6 | |

| STF | 0.024 *** | 0.544 *** | 2.1 | |

| OMC | 0.023 ** | 0.517 *** | 2.3 | |

| RPC | 0.036 *** | 0.628 *** | 1.5 | |

| Year | Establishment | RVN |

|---|---|---|

| Closed Branch | CST | 2.73 |

| SCD | 2.94 | |

| STF | 2.47 | |

| OMC | 2.31 | |

| RPC | 2.81 | |

| Nearby & Post-integrated Branch | CST | 3.11 |

| SCD | 3.46 | |

| STF | 3.28 | |

| OMC | 3.17 | |

| RPC | 3.76 | |

| Sum of 5 vars for Closed Brs. << Sum of 5 vars for Nearby & Integrated Brs. | ||

| Kruskal–Wallis Statistics | 7.485 *** | |

| F-statistics | 9.177 *** | |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Cho, S.; Lee, Z.; Hwang, S.; Kim, J. Determinants of Bank Closures: What Ensures Sustainable Profitability in Mobile Banking? Electronics 2023, 12, 1196. https://doi.org/10.3390/electronics12051196

Cho S, Lee Z, Hwang S, Kim J. Determinants of Bank Closures: What Ensures Sustainable Profitability in Mobile Banking? Electronics. 2023; 12(5):1196. https://doi.org/10.3390/electronics12051196

Chicago/Turabian StyleCho, Soohyung, Zoonky Lee, Sewoong Hwang, and Jonghyuk Kim. 2023. "Determinants of Bank Closures: What Ensures Sustainable Profitability in Mobile Banking?" Electronics 12, no. 5: 1196. https://doi.org/10.3390/electronics12051196