Study on Price Bubbles of China’s Agricultural Commodity against the Background of Big Data

Abstract

:1. Introduction

2. Literature Review

3. Methods and Data

3.1. Theoretical Model

3.2. Method

3.2.1. Bubble Test Method

3.2.2. Bubble Date Stamping

3.2.3. Data Processing Procedures

3.3. Data

4. Empirical Results

4.1. Bubbles Test for Agricultural Commodity Prices

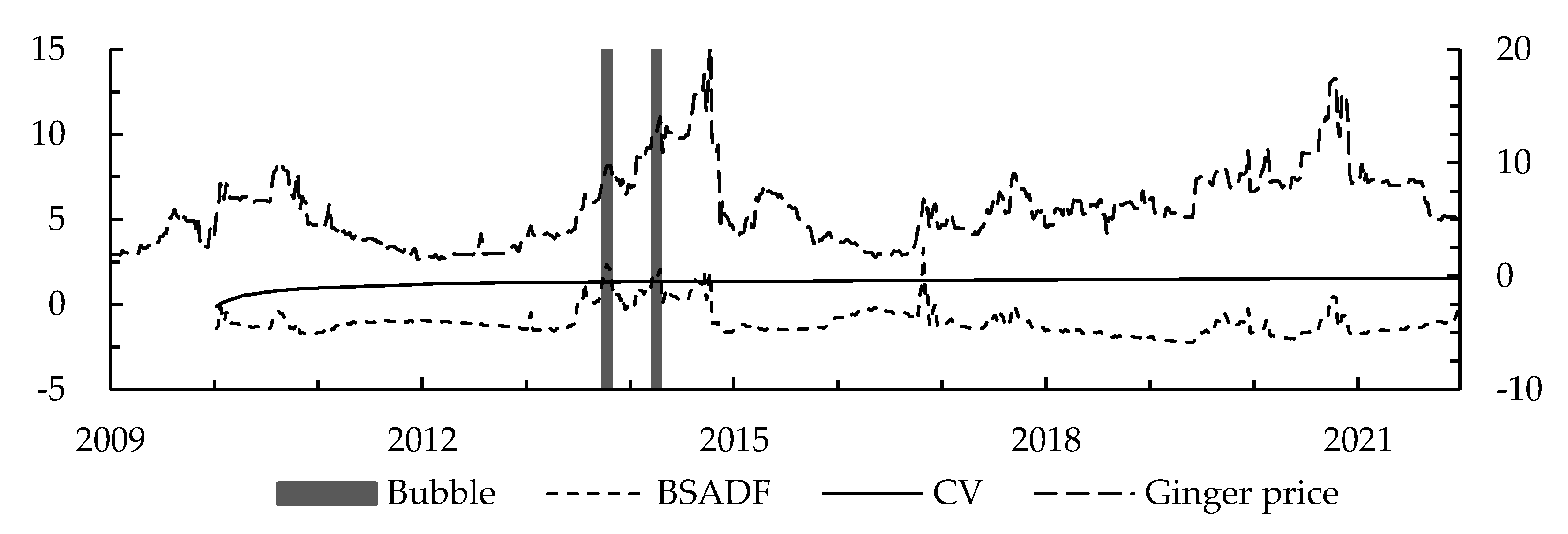

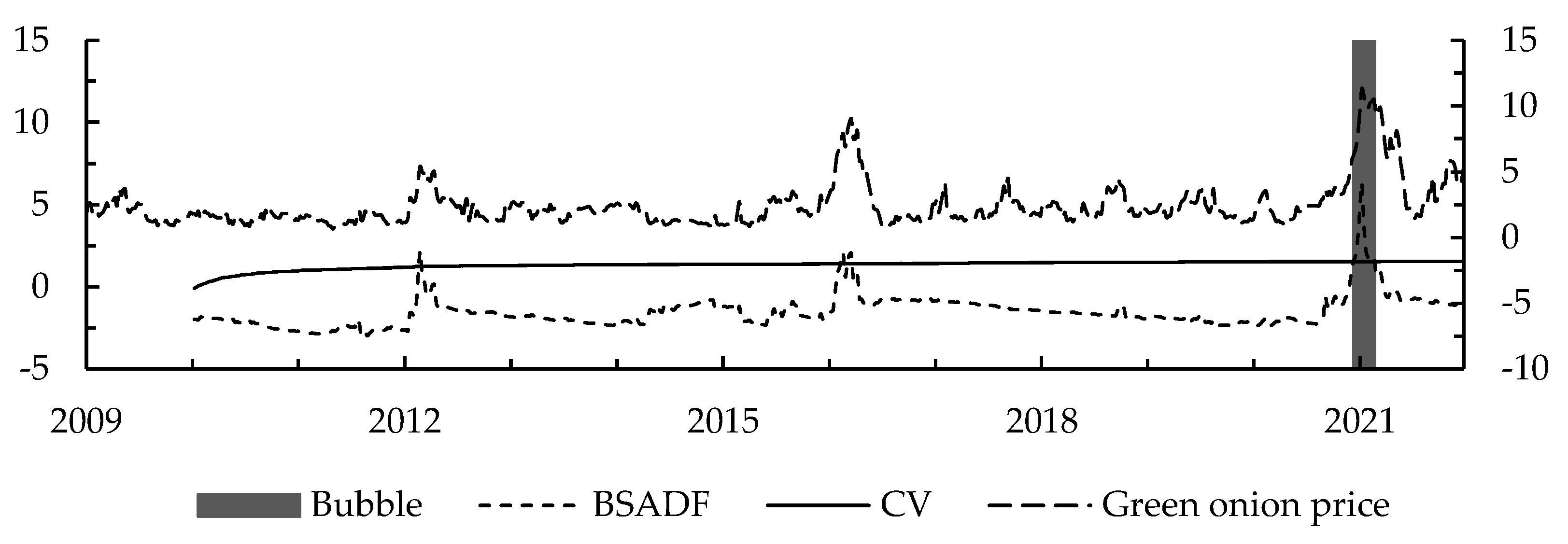

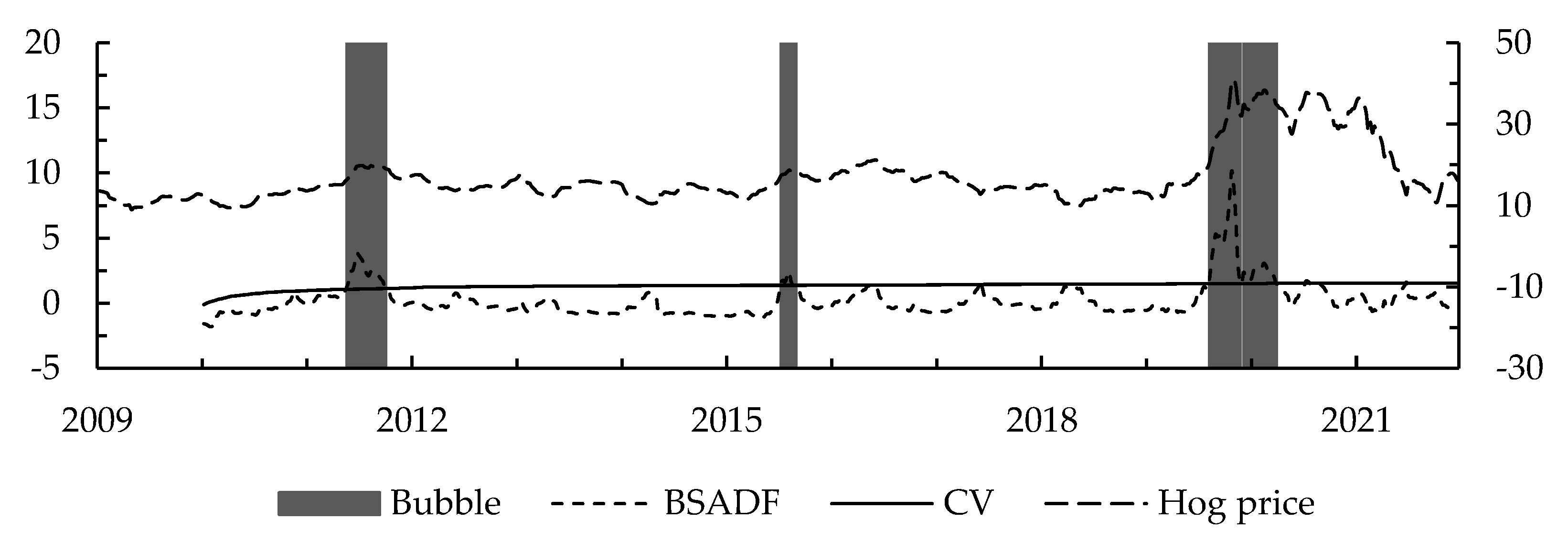

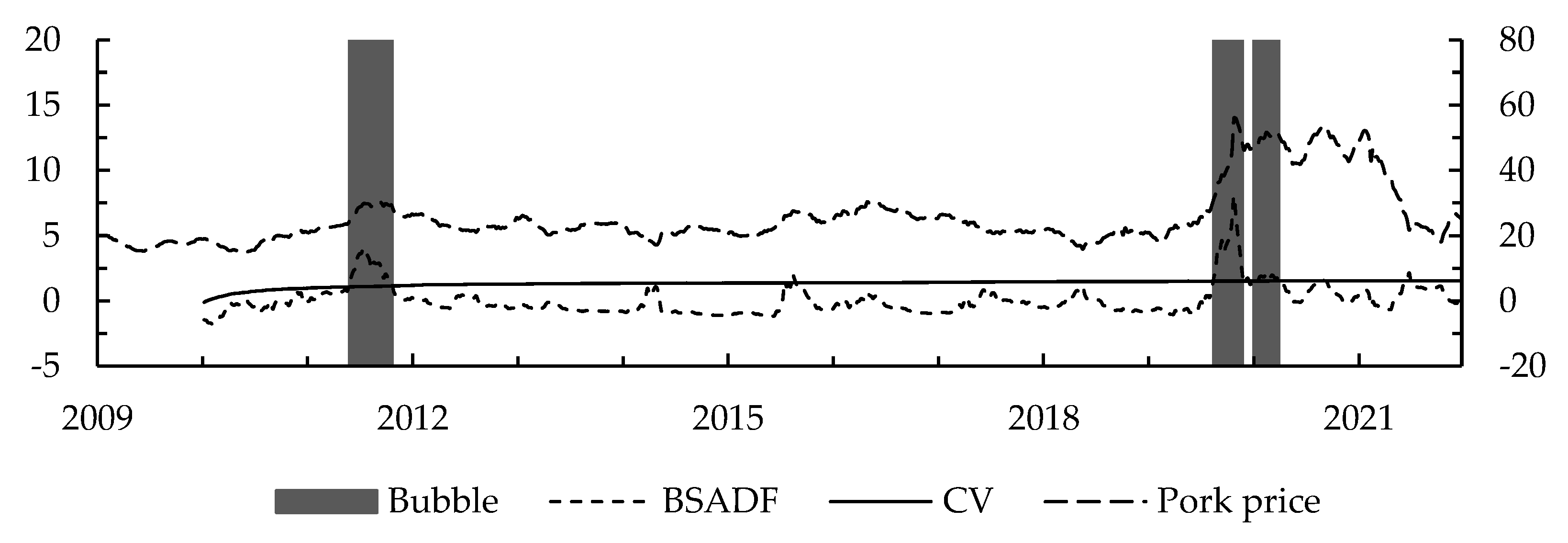

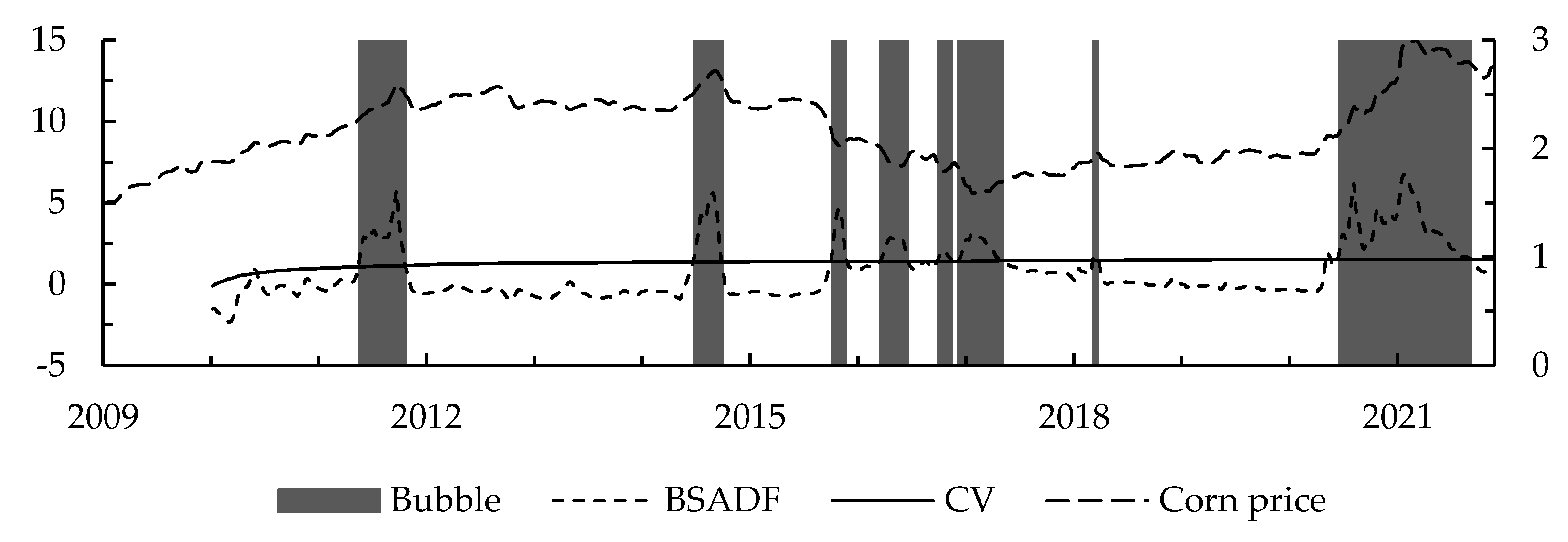

4.2. Date Stamping of Agricultural Commodity Price Bubbles

4.3. Characteristics of Agricultural Commodity Price Bubbles

4.4. Causes of Agricultural Commodity Price Bubbles

4.4.1. Causes of Small Agricultural Commodity Price Bubbles

4.4.2. Causes of Livestock Product Price Bubbles

4.4.3. Causes of Corn Price Bubbles

4.5. Discussion of Empirical Results

5. Conclusions and Recommendations

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Li, J.; Li, C.; Chavas, J.P. Food price bubbles and government intervention: Is China different? Can. J. Agric. Econ. 2017, 65, 135–157. [Google Scholar] [CrossRef]

- Qian, J.; Ito, S.; Zhao, Z. The effect of price support policies on food security and farmers’ income in China. Aust. J. Agr. Resour. Ec. 2020, 64, 1328–1349. [Google Scholar] [CrossRef]

- Javed Awan, M.; Mohd Rahim, M.S.; Nobanee, H.; Munawar, A.; Yasin, A.; Zain, A.M. Social media and stock market prediction: A big data approach. Comput. Mater. Contin. 2021, 67, 2569–2583. [Google Scholar] [CrossRef]

- Giot, P. The information content of implied volatility in agricultural commodity markets. J. Futur. Mark. Futur. Options Other Deriv. Prod. 2003, 23, 441–454. [Google Scholar] [CrossRef]

- Caballero, R.J.; Krishnamurthy, A. Bubbles and capital flow volatility: Causes and risk management. J. Monet. Econ. 2006, 53, 35–53. [Google Scholar] [CrossRef] [Green Version]

- Gilbert, C.L. How to understand high food prices. J. Agr. Econ. 2010, 61, 398–425. [Google Scholar] [CrossRef]

- Xie, H.; Wang, B. An empirical analysis of the impact of agricultural product price fluctuations on China’s grain yield. Sustainability 2017, 9, 906. [Google Scholar] [CrossRef] [Green Version]

- Lundberg, C.; Abman, R. Maize price volatility and deforestation. Am. J. Agr. Econ. 2022, 104, 693–716. [Google Scholar] [CrossRef]

- Mao, Q.; Ren, Y.; Loy, J. Price bubbles in agricultural commodity markets and contributing factors: Evidence for corn and soybeans in China. China Agr. Econ. Rev. 2021, 13, 91–122. [Google Scholar] [CrossRef]

- Li, J.; Chavas, J.P.; Etienne, X.L.; Li, C. Commodity price bubbles and macroeconomics: Evidence from the Chinese agricultural markets. Agr. Econ. 2017, 48, 755–768. [Google Scholar] [CrossRef]

- Chen, Q.; Weng, X. Information flows between the US and China’s agricultural commodity futures markets-based on VAR-BEKK-Skew-t model. Emerg. Mark. Financ. Trade 2018, 54, 71–87. [Google Scholar] [CrossRef]

- Zhang, Y.; Li, C.; Xu, Y.; Li, J. An attribution analysis of soybean price volatility in China: Global market connectedness or energy market transmission? Int. Food Agribus. Man. 2021, 24, 15–25. [Google Scholar] [CrossRef]

- Gürkaynak, R.S. Econometric tests of asset price bubbles: Taking stock. J. Econ. Surv. 2008, 22, 166–186. [Google Scholar] [CrossRef]

- Phillips, P.C.; Wu, Y.; Yu, J. Explosive behavior in the 1990s Nasdaq: When did exuberance escalate asset values? Int. Econ. Rev. 2011, 52, 201–226. [Google Scholar] [CrossRef] [Green Version]

- Phillips, P.C.; Shi, S.; Yu, J. Testing for multiple bubbles: Historical episodes of exuberance and collapse in the S&P 500. Int. Econ. Rev. 2015, 56, 1043–1078. [Google Scholar]

- Phillips, P.C.; Shi, S.; Yu, J. Testing for multiple bubbles: Limit theory of real-time detectors. Int. Econ. Rev. 2015, 56, 1079–1134. [Google Scholar] [CrossRef] [Green Version]

- Shiller, R. Do stock prices move too much to be justified by subsequent changes in dividends? Am. Econ. Rev. 1981, 71, 421–736. [Google Scholar]

- Leroy, S.F.; Porter, R.D. The present-value relation: Tests based on implied variance bounds. Econometrica 1981, 49, 555–574. [Google Scholar] [CrossRef]

- Tirole, J. Asset bubbles and overlapping generations. Econometrica 1985, 53, 1499–1528. [Google Scholar] [CrossRef]

- West, K.D. A specification test for speculative bubbles. Q. J. Econ. 1987, 102, 553–580. [Google Scholar] [CrossRef] [Green Version]

- Diba, B.T.; Grossman, H.I. Explosive rational bubbles in stock prices? Am. Econ. Rev. 1988, 78, 520–530. [Google Scholar]

- Froot, K.A.; Obstfeld, M. Intrinsic Bubbles: The Case of Stock Prices. Am. Econ. Rev. 1991, 81, 1189–1214. [Google Scholar]

- Phillips, P.C.B.; Yu, J. Dating the timeline of financial bubbles during the subprime crisis. Quant. Econ. 2011, 2, 455–491. [Google Scholar] [CrossRef] [Green Version]

- Su, C.; Li, Z.; Tao, R.; Si, D. Testing for multiple bubbles in bitcoin markets: A generalized sup ADF test. Jpn. World Econ. 2018, 46, 56–63. [Google Scholar] [CrossRef]

- Etienne, X.L.; Irwin, S.H.; Garcia, P. Bubbles in food commodity markets: Four decades of evidence. J. Int. Money Financ. 2014, 42, 129–155. [Google Scholar] [CrossRef] [Green Version]

- Su, C.; Li, Z.; Chang, H.; Lobonţ, O. When Will Occur the Crude Oil Bubbles? Energ. Policy 2017, 102, 1–6. [Google Scholar] [CrossRef]

- Li, Y.; Chevallier, J.; Wei, Y.; Li, J. Identifying price bubbles in the US, European and Asian natural gas market: Evidence from a GSADF test approach. Energy Econ. 2020, 87, 104740. [Google Scholar] [CrossRef]

- Caspi, I.; Katzke, N.; Gupta, R. Date stamping historical periods of oil price explosivity: 1876–2014. Energy Econ. 2018, 70, 582–587. [Google Scholar] [CrossRef]

- Khan, K.; Su, C.; Umar, M.; Yue, X. Do crude oil price bubbles occur? Resour. Policy 2021, 71, 101936. [Google Scholar] [CrossRef]

- Etienne, X.L.; Irwin, S.H.; Garcia, P. Price explosiveness, speculation, and grain futures prices. Am. J. Agr. Econ. 2015, 97, 65–87. [Google Scholar] [CrossRef]

- Wang, T.; Zhang, D.; Clive Broadstock, D. Financialization, fundamentals, and the time-varying determinants of US natural gas prices. Energy Econ. 2019, 80, 707–719. [Google Scholar] [CrossRef]

- Fama, E.F. Efficient capital markets: A review of theory and empirical work. J. Financ. 1970, 25, 383–417. [Google Scholar] [CrossRef]

- Diba, B.T.; Grossman, H.I. On the inception of rational bubbles. Q. J. Econ. 1987, 102, 697–700. [Google Scholar] [CrossRef]

- Evans, G.W. Pitfalls in testing for explosive bubbles in asset prices. Am. Econ. Rev. 1991, 81, 922–930. [Google Scholar]

- Homm, U.; Breitung, J. Testing for Speculative Bubbles in Stock Markets: A Comparison of Alternative Methods. J. Financ. Econom. 2012, 10, 198–231. [Google Scholar] [CrossRef]

- Ali, I.M.; Jusoh, Y.Y.; Abdullah, R.; Nor, R.N.H.; Arbaiy, N. A Conceptual Framework for Measuring the Performance of Big Data Analytics Process. Acta Inform. Malays. 2017, 1, 13–14. [Google Scholar] [CrossRef]

- Khan, K.; Derindere Köseoğlu, S. Is palladium price in bubble? Resour. Policy 2020, 68, 101780. [Google Scholar] [CrossRef]

- Zhang, X.; Liu, L.; Su, C.; Tao, R.; Lobonţ, O.; Moldovan, N. Bubbles in Agricultural Commodity Markets of China. Complexity 2019, 2019, 2896479. [Google Scholar] [CrossRef] [Green Version]

- Reicher, C.P.; Utlaut, J.F. Monetary policy shocks and real commodity prices. B.E. J. Macroecon. 2013, 13, 715–749. [Google Scholar] [CrossRef]

- Ma, M.; Wang, H.H.; Hua, Y.; Qin, F.; Yang, J. African swine fever in China: Impacts, responses, and policy implications. Food Policy 2021, 102, 102065. [Google Scholar] [CrossRef]

- Huang, X.; Huang, S.; Shui, A. Government spending and intergenerational income mobility: Evidence from China. J. Econ. Behav. Organ. 2021, 191, 387–414. [Google Scholar] [CrossRef]

- Han, Y.; Tan, S.; Zhu, C.; Liu, Y. Research on the emission reduction effects of carbon trading mechanism on power industry: Plant-level evidence from China. Int. J. Clim. Change Strateg. Manag. 2022; ahead-of-print. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Commodity | Mean | SD | Min | Max | Skew | Kurtosis | N |

|---|---|---|---|---|---|---|---|

| Ginger | 6.01 | 3.32 | 1.50 | 20.00 | 1.04 | 1.27 | 674 |

| Garlic | 6.03 | 3.23 | 0.40 | 17.50 | 0.93 | 0.71 | 674 |

| Green onion | 2.40 | 1.70 | 0.65 | 11.30 | 2.60 | 7.68 | 674 |

| Hog | 16.98 | 6.80 | 8.98 | 40.98 | 1.82 | 2.55 | 674 |

| Pork | 25.50 | 9.01 | 14.86 | 56.02 | 1.77 | 2.29 | 674 |

| Corn | 2.17 | 0.34 | 1.49 | 3.00 | 0.27 | −0.79 | 674 |

| Commodity | SADF Test | GSADF Test | ||

|---|---|---|---|---|

| Statistical Value | Bubble | Statistical Value | Bubble | |

| Ginger | 0.85 | No | 3.27 *** | Yes |

| Garlic | 1.06 | No | 1.94 | No |

| Green onion | −0.40 | No | 6.32 *** | Yes |

| Hog | 7.86 *** | Yes | 10.15 *** | Yes |

| Pork | 6.16 *** | Yes | 8.02 *** | Yes |

| Corn | 1.98 ** | Yes | 6.76 *** | Yes |

| Commodity | Number of Bubbles | Bubble Weeks | Percentage of Bubble Weeks (%) | Maximum Single Bubble Duration |

|---|---|---|---|---|

| Ginger | 2 | 10 | 1.48 | 5 |

| Green onion | 1 | 11 | 1.63 | 11 |

| Hog | 4 | 60 | 8.90 | 20 |

| Pork | 3 | 49 | 7.27 | 22 |

| Corn | 8 | 154 | 22.85 | 64 |

| Commodity | Weeks of Positive Bubble | Weeks of Negative Bubble | Maximum Price Change (%) | Minimum Price Change (%) |

|---|---|---|---|---|

| Ginger | 10 | 0 | 11.68 | 0 |

| Green onion | 11 | 0 | 20.24 | 4.53 |

| Hog | 60 | 0 | 12.04 | 9.02 |

| Pork | 49 | 0 | 20.78 | 6.52 |

| Corn | 104 | 50 | 6.22 | 4.22 |

| Commodity | Ginger | Green Onion | Hog | Pork | Corn | Total Bubbles | Proportion (%) |

|---|---|---|---|---|---|---|---|

| 2009 | 0 | 0 | 0 | 0 | 0 | 0 | 0.00 |

| 2010 | 0 | 0 | 0 | 0 | 0 | 0 | 0.00 |

| 2011 | 0 | 0 | 20 | 22 | 23 | 65 | 22.89 |

| 2012 | 0 | 0 | 0 | 0 | 0 | 0 | 0.00 |

| 2013 | 5 | 0 | 0 | 0 | 0 | 5 | 1.76 |

| 2014 | 5 | 0 | 0 | 0 | 14 | 19 | 6.69 |

| 2015 | 0 | 0 | 8 | 0 | 7 | 15 | 5.28 |

| 2016 | 0 | 0 | 0 | 0 | 25 | 25 | 8.80 |

| 2017 | 0 | 0 | 0 | 0 | 18 | 18 | 6.34 |

| 2018 | 0 | 0 | 0 | 0 | 3 | 3 | 1.06 |

| 2019 | 0 | 0 | 20 | 15 | 0 | 35 | 12.32 |

| 2020 | 0 | 3 | 12 | 12 | 28 | 55 | 19.37 |

| 2021 | 0 | 8 | 0 | 0 | 36 | 44 | 15.49 |

| Total bubbles | 10 | 11 | 60 | 49 | 154 | 284 | 100.00 |

| Proportion (%) | 3.52 | 3.87 | 21.13 | 17.25 | 54.23 | 100.00 | — |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Wang, J.; Ma, K.; Zhang, L.; Wang, J. Study on Price Bubbles of China’s Agricultural Commodity against the Background of Big Data. Electronics 2022, 11, 4067. https://doi.org/10.3390/electronics11244067

Wang J, Ma K, Zhang L, Wang J. Study on Price Bubbles of China’s Agricultural Commodity against the Background of Big Data. Electronics. 2022; 11(24):4067. https://doi.org/10.3390/electronics11244067

Chicago/Turabian StyleWang, Jiayue, Kun Ma, Ling Zhang, and Jianzhong Wang. 2022. "Study on Price Bubbles of China’s Agricultural Commodity against the Background of Big Data" Electronics 11, no. 24: 4067. https://doi.org/10.3390/electronics11244067