Do Environmental Taxes Affect Carbon Dioxide Emissions in OECD Countries? Evidence from the Dynamic Panel Threshold Model

Abstract

:1. Introduction

2. Literature Review

3. Methodology

4. Data

5. Results and Discussion

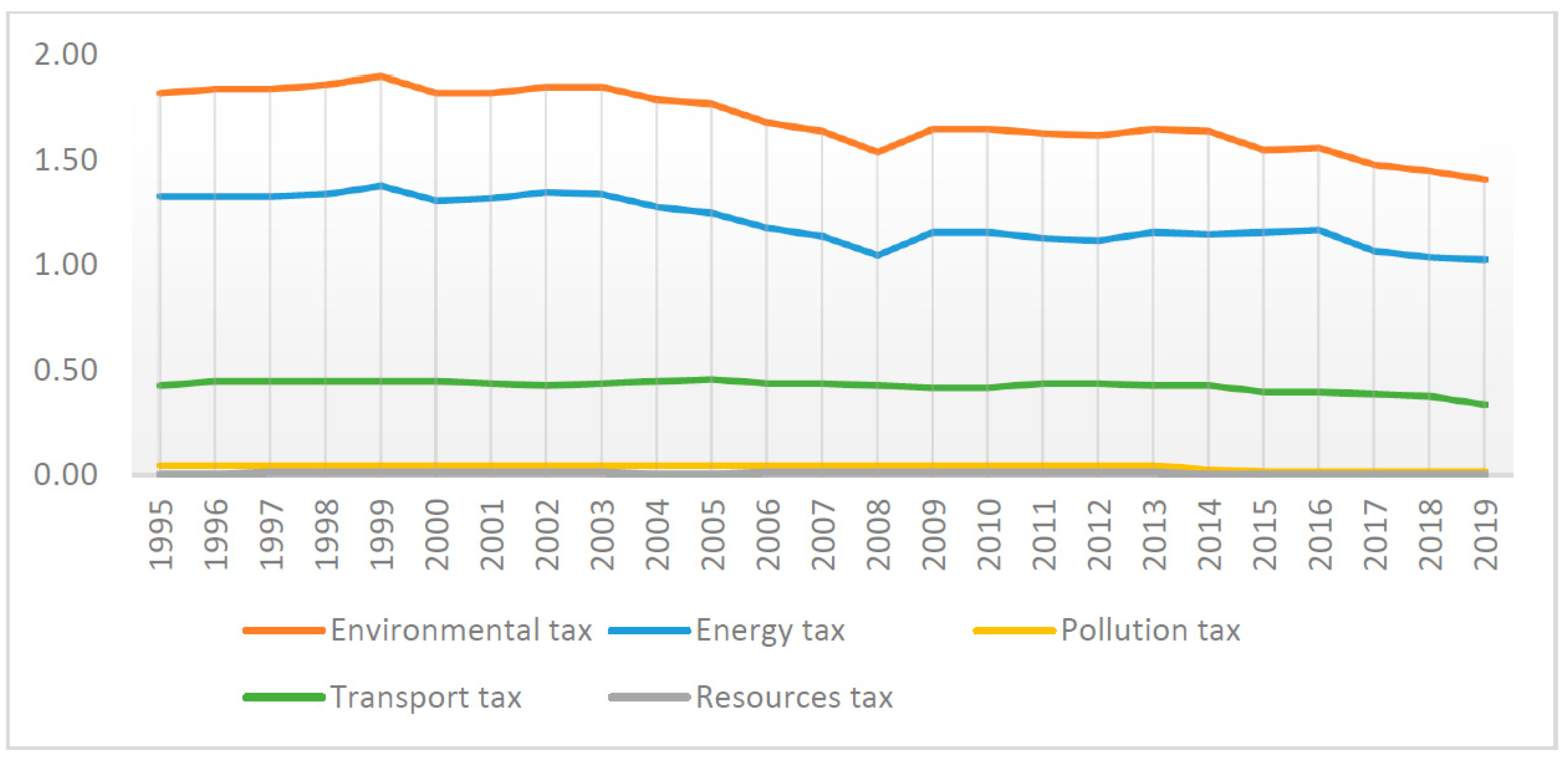

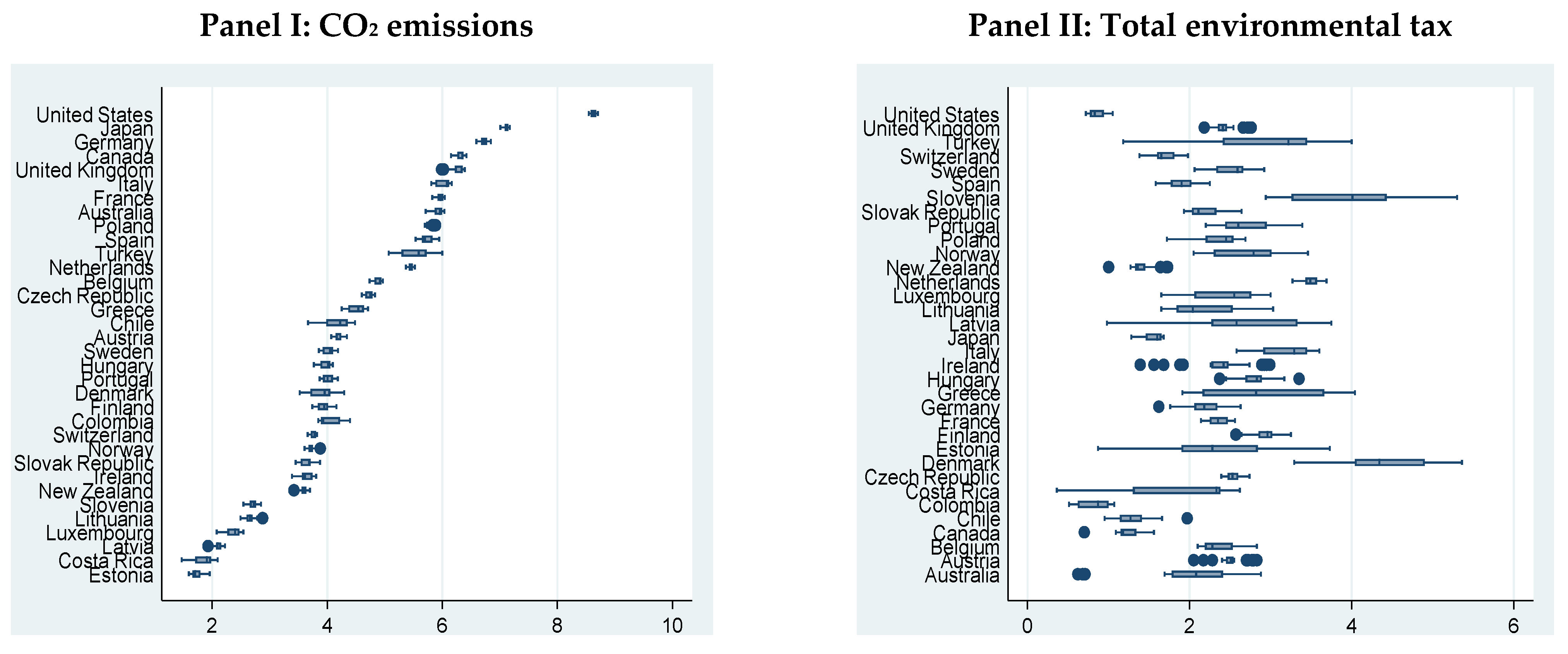

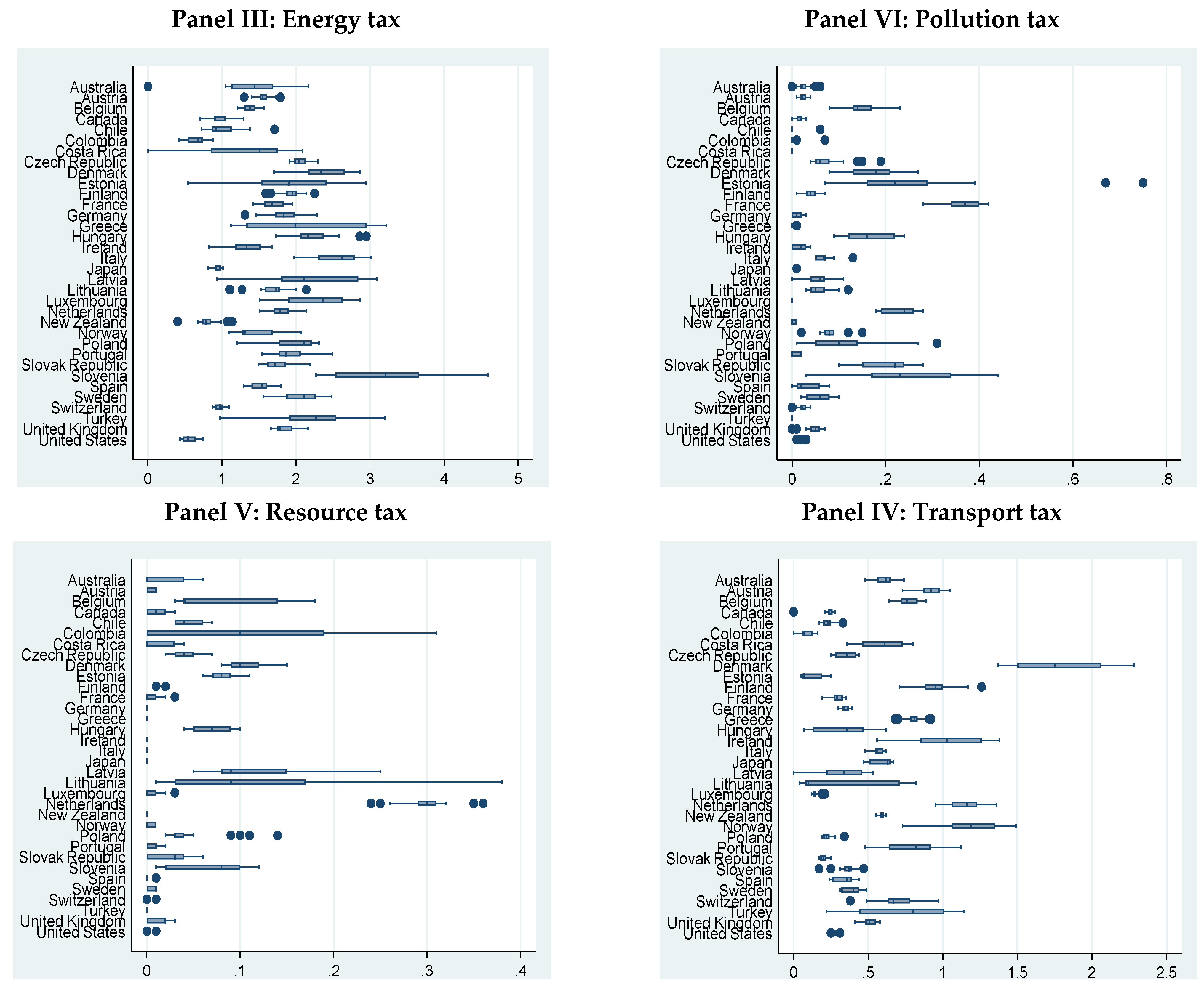

5.1. Preliminary Analysis

5.2. Unit Root Analysis

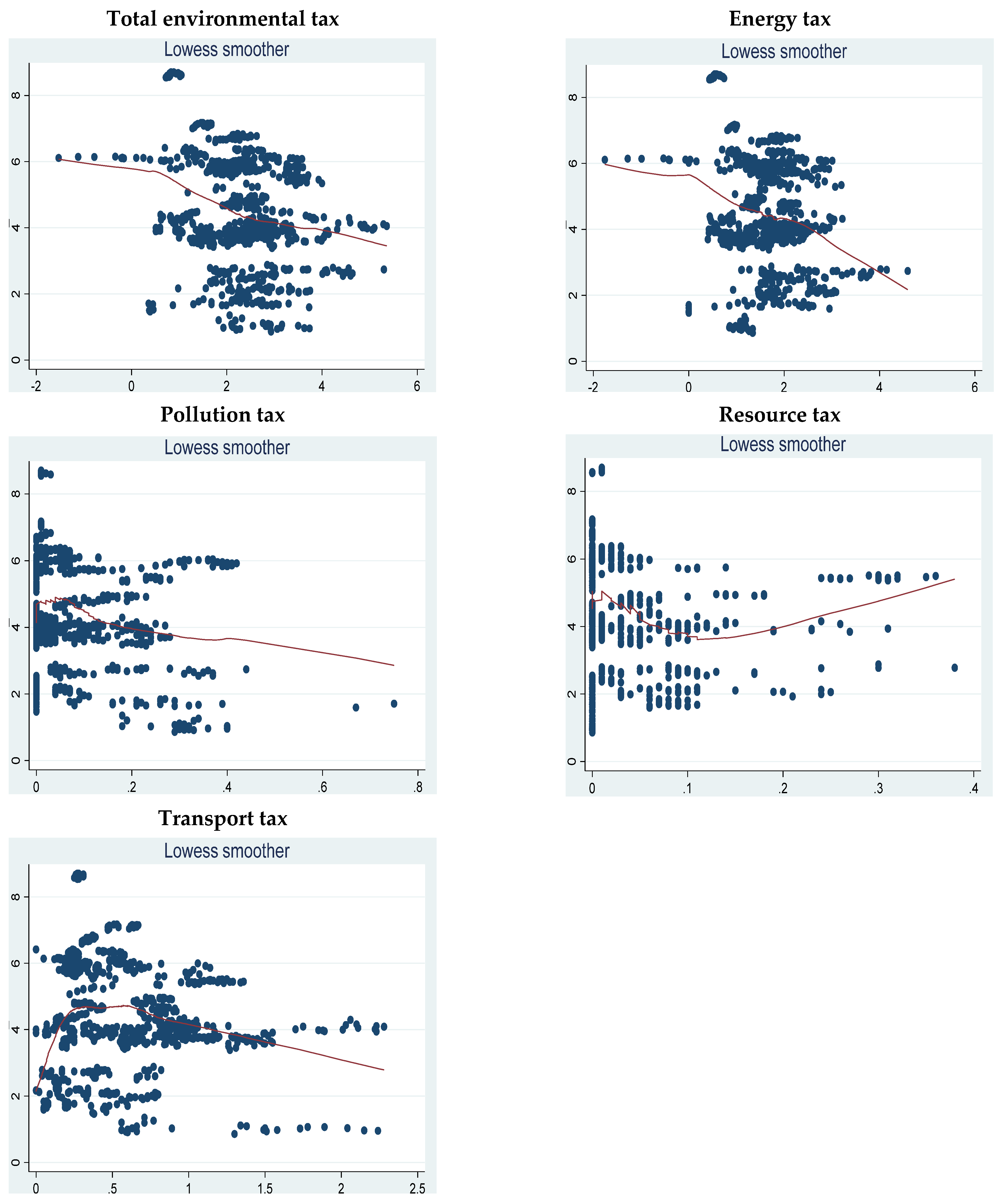

5.3. Locally Weighted Scatterplot Smoothing Analysis

5.4. Conventional Dynamic Panel Regression Analysis

5.5. Dynamic Panel Threshold Regression Analysis

6. Conclusions and Policy Recommendations

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- World Meteorological Organization. WMO Provisional State of the Global Climate 2022. 2022. Available online: https://library.wmo.int/doc_num.php?explnum_id=11359 (accessed on 1 December 2022).

- Goddard Space Flight Center. Vital Signs. 2022. Available online: https://climate.nasa.gov/vital-signs/sea-level (accessed on 15 November 2022).

- Friedlingstein, P.; O’sullivan, M.; Jones, M.W.; Andrew, R.M.; Hauck, J.; Olsen, A.; Peters, G.P.; Peters, W.; Pongratz, J.; Sitch, S.; et al. Global carbon budget 2022. Earth Syst. Sci. Data 2022, 14, 4811–4900. [Google Scholar] [CrossRef]

- Climate Watch. Historical GHG Emissions. 2022. Available online: https://www.climatewatchdata.org/ghg-emissions (accessed on 15 November 2022).

- Bilgili, F.; Koçak, E.; Bulut, Ü. The dynamic impact of renewable energy consumption on CO2 emissions: A revisited Environmental Kuznets Curve approach. Renew. Sustain. Energy Rev. 2016, 54, 838–845. [Google Scholar] [CrossRef]

- Baloch, M.A.; Mahmood, N.; Zhang, J.W. Effect of natural resources, renewable energy and economic development on CO2 emissions in BRICS countries. Sci. Total Environ. 2019, 678, 632–638. [Google Scholar]

- Khan, I.; Zakari, A.; Ahmad, M.; Irfan, M.; Hou, F. Linking energy transitions, energy consumption, and environmental sustainability in OECD countries. Gondwana Res. 2022, 103, 445–457. [Google Scholar] [CrossRef]

- Lv, Z.; Li, S. How financial development affects CO2 emissions: A spatial econometric analysis. J. Environ. Manag. 2021, 277, 111397. [Google Scholar] [CrossRef]

- Khan, M.; Ozturk, I. Examining the direct and indirect effects of financial development on CO2 emissions for 88 developing countries. J. Environ. Manag. 2021, 293, 112812. [Google Scholar] [CrossRef]

- Brown, L.; McFarlane, A.; Das, A.; Campbell, K. The impact of financial development on carbon dioxide emissions in Jamaica. Environ. Sci. Pollut. Res. 2022, 29, 25902–25915. [Google Scholar] [CrossRef] [PubMed]

- Yao, Y.; Ivanovski, K.; Inekwe, J.; Smyth, R. Human capital and CO2 emissions in the long run. Energy Econ. 2020, 91, 104907. [Google Scholar] [CrossRef]

- Khan, M. CO2 emissions and sustainable economic development: New evidence on the role of human capital. Sustain. Dev. 2020, 28, 1279–1288. [Google Scholar] [CrossRef]

- Li, X.; Ullah, S. Caring for the environment: How CO2 emissions respond to human capital in BRICS economies? Environ. Sci. Pollut. Res. 2022, 29, 18036–18046. [Google Scholar] [CrossRef]

- Managi, S.; Hibiki, A.; Tsurumi, T. Does trade openness improve environmental quality? J. Environ. Econ. Manag. 2009, 58, 346–363. [Google Scholar] [CrossRef]

- Mutascu, M. A time-frequency analysis of trade openness and CO2 emissions in France. Energy Policy 2018, 115, 443–455. [Google Scholar] [CrossRef]

- Zmami, M.; Ben-Salha, O. An empirical analysis of the determinants of CO2 emissions in GCC countries. Int. J. Sustain. Dev. World Ecol. 2020, 27, 469–480. [Google Scholar] [CrossRef]

- Iqbal, N.; Abbasi, K.R.; Shinwari, R.; Guangcai, W.; Ahmad, M.; Tang, K. Does exports diversification and environmental innovation achieve carbon neutrality target of OECD economies? J. Environ. Manag. 2021, 291, 112648. [Google Scholar] [CrossRef]

- Dauda, L.; Long, X.; Mensah, C.N.; Salman, M.; Boamah, K.B.; Ampon-Wireko, S.; Dogbe, C.S.K. Innovation, trade openness and CO2 emissions in selected countries in Africa. J. Clean. Prod. 2021, 281, 125143. [Google Scholar] [CrossRef]

- Mongo, M.; Belaïd, F.; Ramdani, B. The effects of environmental innovations on CO2 emissions: Empirical evidence from Europe. Environ. Sci. Policy 2021, 118, 1–9. [Google Scholar] [CrossRef]

- Vehmas, J.; Kaivo-Oja, J.; Luukkanen, J.; Malaska, P. Environmental taxes on fuels and electricity—Some experiences from the Nordic countries. Energy Policy 1999, 27, 343–355. [Google Scholar] [CrossRef]

- Eurostat. Environmental Tax Statistics. 2023. Available online: https://ec.europa.eu/eurostat/statistics-explained/index.php?title=Environmental_tax_statistics (accessed on 12 February 2023).

- OECD. Environmental Policy Instruments, OECD (Database); OECD: Paris, France, 2022. [Google Scholar] [CrossRef]

- Doğan, B.; Chu, L.K.; Ghosh, S.; Truong HH, D.; Balsalobre-Lorente, D. How environmental taxes and carbon emissions are related in the G7 economies? Renew. Energy 2022, 187, 645–656. [Google Scholar] [CrossRef]

- Wolde-Rufael, Y.; Mulat-Weldemeskel, E. Do environmental taxes and environmental stringency policies reduce CO2 emissions? Evidence from 7 emerging economies. Environ. Sci. Pollut. Res. 2021, 28, 22392–22408. [Google Scholar] [CrossRef] [PubMed]

- Sezgin, F.H.; Bayar, Y.; Herta, L.; Gavriletea, M.D. Do environmental stringency policies and human development reduce CO2 emissions? Evidence from G7 and BRICS economies. Int. J. Environ. Res. Public Health 2021, 18, 6727. [Google Scholar] [CrossRef]

- U.S. Energy Information Administration. International. 2023. Available online: https://www.eia.gov/international/overview/world (accessed on 12 March 2023).

- Seo, M.H.; Shin, Y. Dynamic panels with threshold effect and endogeneity. J. Econ. 2016, 195, 169–186. [Google Scholar] [CrossRef] [Green Version]

- Seo, M.H.; Kim, S.; Kim, Y.J. Estimation of dynamic panel threshold model using Stata. Stata J. 2019, 19, 685–697. [Google Scholar] [CrossRef]

- Lee, C.C.; Xing, W.; Lee, C.C. The impact of energy security on income inequality: The key role of economic development. Energy 2022, 248, 123564. [Google Scholar] [CrossRef]

- Zaghdoudi, T.; Maktouf, S. Threshold effect in the relationship between environmental taxes and CO2 emissions: A PSTR specification. Econ. Bull. 2017, 37, 2086–2094. [Google Scholar]

- Aydin, C.; Esen, Ö. Reducing CO2 emissions in the EU member states: Do environmental taxes work? J. Environ. Plan. Manag. 2018, 61, 2396–2420. [Google Scholar] [CrossRef]

- Esen, Ö.; Yıldırım, D.Ç.; Yıldırım, S. Pollute less or tax more? Asymmetries in the EU environmental taxes–Ecological balance nexus. Environ. Impact Assess. Rev. 2021, 91, 106662. [Google Scholar] [CrossRef]

- Bolarinwa, S.T.; Akinlo, A.E. Is there a nonlinear relationship between financial development and income inequality in Africa? Evidence from dynamic panel threshold. J. Econ. Asymmetries 2021, 24, e00226. [Google Scholar] [CrossRef]

- Polinsky, A.M.; Shavell, S. Pigouvian taxation with administrative costs. J. Public Econ. 1982, 19, 385–394. [Google Scholar] [CrossRef] [Green Version]

- Roach, B.; Lennox, E.; Codur, A.M. Microeconomics and the Environment; Global Development and Environment Institute, Tufts University: Medford, OR, USA, 2019. [Google Scholar]

- Williams, R.C., III. Environmental taxation. In Working Paper No. 22303; National Bureau of Economic Research: Cambridge, MA, USA, 2016. [Google Scholar]

- Guo, L.; Wang, Y. How does government environmental regulation “unlock” carbon emission effect?—Evidence from China. Chin. J. Popul. Resour. Environ. 2018, 16, 232–241. [Google Scholar] [CrossRef]

- Sinn, H.W. Introductory comment–the green paradox: A supply-side view of the climate problem. Rev. Environ. Econ. Policy 2015, 9, 239–245. [Google Scholar] [CrossRef] [Green Version]

- Xie, P.; Jamaani, F. Does green innovation, energy productivity and environmental taxes limit carbon emissions in developed economies: Implications for sustainable development. Struct. Chang. Econ. Dyn. 2022, 63, 66–78. [Google Scholar] [CrossRef]

- Tao, R.; Umar, M.; Naseer, A.; Razi, U. The dynamic effect of eco-innovation and environmental taxes on carbon neutrality target in emerging seven (E7) economies. J. Environ. Manag. 2021, 299, 113525. [Google Scholar] [CrossRef] [PubMed]

- Chien, F.; Sadiq, M.; Nawaz, M.A.; Hussain, M.S.; Tran, T.D.; Le Thanh, T. A step toward reducing air pollution in top Asian economies: The role of green energy, eco-innovation, and environmental taxes. J. Environ. Manag. 2021, 297, 113420. [Google Scholar] [CrossRef] [PubMed]

- Telatar, O.M.; Birinci, N. The effects of environmental tax on Ecological Footprint and Carbon dioxide emissions: A nonlinear cointegration analysis on Turkey. Environ. Sci. Pollut. Res. 2022, 29, 44335–44347. [Google Scholar] [CrossRef] [PubMed]

- Sarpong, K.A.; Xu, W.; Gyamfi, B.A.; Ofori, E.K. Can environmental taxes and green-energy offer carbon-free E7 economies? An empirical analysis in the framework of COP-26. Environ. Sci. Pollut. Res. 2023, 30, 51726–51739. [Google Scholar] [CrossRef]

- Ahmad, M.; Satrovic, E. Modeling combined role of renewable electricity output, environmental regulations, and coal consumption in ecological sustainability. Ecol. Inform. 2023, 75, 102121. [Google Scholar] [CrossRef]

- Meireles, M.; Robaina, M.; Magueta, D. The effectiveness of environmental taxes in reducing CO2 emissions in passenger vehicles: The case of Mediterranean countries. Int. J. Environ. Res. Public Health 2021, 18, 5442. [Google Scholar] [CrossRef]

- Wolde-Rufael, Y.; Mulat-Weldemeskel, E. Effectiveness of environmental taxes and environmental stringent policies on CO2 emissions: The European experience. Environ. Dev. Sustain. 2022, 25, 5211–5239. [Google Scholar] [CrossRef]

- Akkaya, Ş.; Hepsag, A. Does fuel tax decrease carbon dioxide emissions in Turkey? Evidence from an asymmetric nonlinear cointegration test and error correction model. Environ. Sci. Pollut. Res. 2021, 28, 35094–35101. [Google Scholar] [CrossRef]

- Hepsag, A. Testing for cointegration in nonlinear asymmetric smooth transition error correction models. Commun. Stat.-Simul. Comput. 2021, 50, 400–412. [Google Scholar] [CrossRef]

- Ahmad, M.; Satrovic, E. How do transportation-based environmental taxation and globalization contribute to ecological sustainability? Ecol. Inform. 2023, 74, 102009. [Google Scholar] [CrossRef]

- Ulucak, R.; Kassouri, Y. An assessment of the environmental sustainability corridor: Investigating the nonlinear effects of environmental taxation on CO2 emissions. Sustain. Dev. 2020, 28, 1010–1018. [Google Scholar] [CrossRef]

- Kremer, S.; Bick, A.; Nautz, D. Inflation and growth: New evidence from a dynamic panel threshold analysis. Empir. Econ. 2013, 44, 861–878. [Google Scholar] [CrossRef] [Green Version]

- Ben-Salha, O.; Hakimi, A.; Zaghdoudi, T.; Soltani, H.; Nsaibi, M. Assessing the Impact of Fossil Fuel Prices on Renewable Energy in China Using the Novel Dynamic ARDL Simulations Approach. Sustainability 2022, 14, 10439. [Google Scholar] [CrossRef]

- Nepal, R.; Musibau, H.O.; Jamasb, T. Energy consumption as an indicator of energy efficiency and emissions in the European Union: A GMM based quantile regression approach. Energy Policy 2021, 158, 112572. [Google Scholar] [CrossRef]

- Voumik, L.C.; Islam, M.A.; Rahaman, A.; Rahman, M.M. Emissions of carbon dioxide from electricity production in ASEAN countries: GMM and quantile regression analysis. SN Bus. Econ. 2022, 2, 133. [Google Scholar] [CrossRef]

- Bakhsh, S.; Yin, H.; Shabir, M. Foreign investment and CO2 emissions: Do technological innovation and institutional quality matter? Evidence from system GMM approach. Environ. Sci. Pollut. Res. 2021, 28, 19424–19438. [Google Scholar] [CrossRef] [PubMed]

- United Nations. World Economic Situation and Prospects (WESP) 2022; United Nations: New York, NY, USA, 2022. [Google Scholar]

- OECD. Revenue Statistics 2019; OECD Publishing: Paris, France, 2019. [Google Scholar]

- Pesaran, M.H. General diagnostic tests for cross-sectional dependence in panels. Empir. Econ. 2021, 60, 13–50. [Google Scholar] [CrossRef]

- Pesaran, M.H. A simple panel unit root test in the presence of cross-section dependence. J. Appl. Econ. 2007, 22, 265–312. [Google Scholar] [CrossRef] [Green Version]

- Bentum-Ennin, I. International reserves accumulation and economic growth in the West African Monetary Zone. Int. Res. J. Mark. Econ. 2014, 1, 31–56. [Google Scholar]

- Arellano, M.; Bond, S. Some tests of specification for panel data: Monte Carlo evidence and an application to employment equations. Rev. Econ. Stud. 1991, 58, 277–297. [Google Scholar] [CrossRef] [Green Version]

- Arellano, M.; Bover, O. Another look at the instrumental variable estimation of error-components models. J. Econ. 1995, 68, 29–51. [Google Scholar] [CrossRef] [Green Version]

- Blundell, R.; Bond, S. Initial conditions and moment restrictions in dynamic panel data models. J. Econ. 1998, 87, 115–143. [Google Scholar] [CrossRef] [Green Version]

- Danish; Ulucak, R.; Khan, S.-U.-D. Relationship between energy intensity and CO2 emissions: Does economic policy matter? Sustain. Dev. 2020, 28, 1457–1464. [Google Scholar]

- Satrovic, E.; Cetindas, A.; Akben, I.; Damrah, S. Do natural resource dependence, economic growth and transport energy consumption accelerate ecological footprint in the most innovative countries? The moderating role of technological innovation. Gondwana Res. 2023, in press. [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| # | Country | Developed | Developing | # | Country | Developed | Developing |

|---|---|---|---|---|---|---|---|

| 1 | Australia | X | 18 | Japan | X | ||

| 2 | Austria | X | 19 | Latvia | X | ||

| 3 | Belgium | X | 20 | Lithuania | X | ||

| 4 | Canada | X | 21 | Luxembourg | X | ||

| 5 | Chile | X | 22 | Netherlands | X | ||

| 6 | Colombia | X | 23 | New Zealand | X | ||

| 7 | Costa Rica | X | 24 | Norway | X | ||

| 8 | Czech Republic | X | 25 | Poland | X | ||

| 9 | Denmark | X | 26 | Portugal | X | ||

| 10 | Estonia | X | 27 | Slovak Republic | X | ||

| 11 | Finland | X | 28 | Slovenia | X | ||

| 12 | France | X | 29 | Spain | X | ||

| 13 | Germany | X | 30 | Sweden | X | ||

| 14 | Greece | X | 31 | Switzerland | X | ||

| 15 | Hungary | X | 32 | Turkey | X | ||

| 16 | Ireland | X | 33 | United Kingdom | X | ||

| 17 | Italy | X | 34 | United States | X |

| Tax Category | Definition |

|---|---|

| Total environmental tax | The sum of the four tax-base categories. |

| Energy tax | Includes taxes on energy products (fossil fuels and electricity), including those used in transportation, such as petrol and diesel. |

| Resource tax | Includes taxes on water extraction, forest products, hunting and fishing, mining royalties, and excavation taxes. |

| Pollution tax | Includes Sulphur Oxides (SOx) and Nitrogen Oxides (NOx) emission taxes, taxes on ozone-depleting substances such as chlorofluorocarbons, carbon tetrachloride and chlorofluoromethanes, taxes on wastewater discharge, taxes on the packaging, final disposal of solid waste, and other taxes. |

| Transport tax | Includes one-off import or sales taxes on transport equipment, recurrent taxes on ownership, registration or use of motor vehicles, and other transport-related taxes. Excise taxes on automotive fuels are not included. |

| Abbreviation | Variable | Source |

|---|---|---|

| CO2 emissions (in MMtonnes) | U.S. Energy Information Administration | |

| GDP per capita (in constant 2015 US$) | World Development Indicators | |

| Energy intensity, measured as energy consumption per GDP (in Btu/2015$ GDP PPP) | U.S. Energy Information Administration | |

| Share of urban population | World Development Indicators | |

| Patents on environmental technologies | Organisation for Economic Cooperation and Development | |

| env_tax | Total environmental tax revenue (% GDP) | Organisation for Economic Cooperation and Development |

| ener_tax | Energy tax revenue (% GDP) | Organisation for Economic Cooperation and Development |

| res_tax | Resource tax revenue (% GDP) | Organisation for Economic Cooperation and Development |

| pol_tax | Pollution tax revenue (% GDP) | Organisation for Economic Cooperation and Development |

| tra_tax | Transport tax revenue (% GDP) | Organisation for Economic Cooperation and Development |

| Mean | Standard Deviation | Min | Max | Median | |

|---|---|---|---|---|---|

| 355.072 | 948.264 | 4.341 | 6015.538 | 62.645 | |

| env_tax | 2.355 | 0.861 | 0.36 | 5.36 | 2.385 |

| ener_tax | 1.688 | 0.671 | 0 | 4.59 | 1.71 |

| pol_tax | 0.075 | 0.101 | 0 | 0.75 | 0.03 |

| res_tax | 0.039 | 0.067 | 0 | 0.38 | 0.01 |

| tra_tax | 0.553 | 0.389 | 0 | 2.28 | 0.47 |

| 74.715 | 10.9 | 50.622 | 98.041 | 76.022 | |

| 10.693 | 4.564 | 0.92 | 33.53 | 10.08 | |

| 32,708.502 | 22,054.54 | 3911.573 | 112,417.88 | 32,332.101 | |

| 4675.319 | 1796.801 | 1561.279 | 12,285.078 | 4273.083 |

| Variables | env_tax | ener_tax | pol_tax | res_tax | tra_tax | ||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| 1.000 | |||||||||||

| env_tax | −0.23 *** | 1.000 | |||||||||

| ener_tax | −0.25 *** | 0.87 *** | 1.000 | ||||||||

| pol_tax | −0.10 *** | 0.42 *** | 0.34 *** | 1.000 | |||||||

| res_tax | −0.17 *** | 0.26 *** | 0.09 *** | 0.36 *** | 1.000 | ||||||

| tra_tax | −0.01 | 0.54 *** | 0.10 *** | 0.011 | 0.14 *** | 1.000 | |||||

| 0.29 *** | −0.18 *** | −0.30 *** | −0.13 *** | 0.07 ** | 0.145 *** | 1.000 | |||||

| −0.14 *** | −0.11 *** | −0.10 *** | −0.07 ** | 0.07 ** | −0.074 ** | 0.060 * | 1.000 | ||||

| 0.26 *** | 0.09 *** | −0.08 ** | −0.033 | −0.20 *** | 0.388 *** | 0.446 *** | −0.12 *** | 1.000 | |||

| 0.25 *** | 0.08 ** | −0.09 *** | −0.042 | −0.20 *** | 0.383 *** | 0.451 *** | −0.12 *** | 0.99 *** | 1.000 | ||

| 0.26 *** | −0.07 ** | −0.07 ** | 0.07 ** | 0.04 | −0.06 ** | 0.16 *** | −0.12 *** | 0.045 | 0.040 | 1.000 |

| Variable | Statistic | p-Value |

|---|---|---|

| 21.050 *** | 0.000 | |

| 102.080 *** | 0.000 | |

| 105.780 *** | 0.000 | |

| 47.510 *** | 0.000 | |

| 43.310 *** | 0.000 | |

| env_tax | 13.140 *** | 0.000 |

| ener_tax | 12.440 *** | 0.000 |

| res_tax | 2.260 ** | 0.024 |

| pol_tax | 14.050 *** | 0.000 |

| tra_tax | 1.990 ** | 0.046 |

| Variable | Constant | Constant and Trend | ||

|---|---|---|---|---|

| Statistic | p-Value | Statistic | p-Value | |

| Level | ||||

| 0.886 | 0.812 | −0.413 | 0.430 | |

| 0.458 | 0.684 | 0.04 | 0.484 | |

| −0.366 | 0.357 | 0.594 | 0.724 | |

| 9.689 | 1.000 | 9.706 | 1.000 | |

| −1.488 * | 0.068 | −1.161 | 0.123 | |

| env_tax | 0.748 | 0.773 | 2.363 | 0.991 |

| ener_tax | 1.428 | 0.923 | 2.728 | 0.997 |

| res_tax | 7.751 | 1.000 | 6.721 | 1.000 |

| pol_tax | 2.706 | 0.997 | 1.484 | 0.931 |

| tra_tax | 0.616 | 0.731 | −1.402 * | 0.080 |

| First difference | ||||

| −17.498 *** | 0.000 | −15.687 *** | 0.000 | |

| −4.857 *** | 0.000 | −5.122 *** | 0.000 | |

| −7.486 *** | 0.000 | −5.166 *** | 0.000 | |

| −7.857 *** | 0.000 | −7.723 *** | 0.000 | |

| −21.931 *** | 0.000 | −20.191 *** | 0.000 | |

| Δenv_tax | −14.963 *** | 0.000 | −13.596 *** | 0.000 |

| Δener_tax | −14.538 *** | 0.000 | −13.429 *** | 0.000 |

| Δres_tax | −7.283 *** | 0.000 | −5.871 *** | 0.000 |

| Δpol_tax | −12.299 *** | 0.000 | −10.841 *** | 0.000 |

| Δra_tax | −16.863 *** | 0.000 | −14.298 *** | 0.000 |

| First-Difference GMM | System GMM | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| env_tax | ener_tax | pol_tax | res_tax | tra_tax | env_tax | ener_tax | pol_tax | res_tax | tra_tax | |

| 0.400 *** (0.031) | 0.350 *** (0.034) | 0.415 *** (0.035) | 0.444 *** (0.034) | 0.337 *** (0.025) | 0.913 *** (0.018) | 0.943 *** (0.027) | 0.981 *** (0.008) | 0.968 *** (0.009) | 0.928 *** (0.015) | |

| 0.312 (0.241) | 0.735 ** (0.304) | 0.056 (0.197) | 0.060 (0.217) | 0.340 (0.270) | 1.062 (1.118) | 2.587 ** (1.025) | 1.679 *** (0.486) | 1.233 ** (0.558) | 0.087 (0.590) | |

| 0.019 (0.012) | −0.003 (0.017) | −0.039 *** (0.010) | −0.037 *** (0.012) | −0.027 ** (0.013) | −0.052 (0.056) | −0.130 ** (0.051) | −0.084 *** (0.024) | −0.061 ** (0.028) | −0.004 (0.029) | |

| 0.729 *** (0.039) | 0.734 *** (0.051) | 0.749 *** (0.046) | 0.711 *** (0.047) | 0.914 *** (0.043) | 0.098 *** (0.026) | 0.078 ** (0.031) | 0.035 *** (0.010) | 0.051 *** (0.014) | 0.051 * (0.028) | |

| −0.0007 ** (0.000) | −0.0005 * (0.000) | −0.0002 (0.000) | −0.0001 (0.000) | −0.0000 (0.001) | −0.0017 * (0.001) | −0.004 *** (0.001) | −0.001 *** (0.000) | −0.001 *** (0.000) | −0.002 *** (0.001) | |

| 0.004 *** (0.001) | 0.005 *** (0.001) | 0.003 *** (0.001) | 0.003 *** (0.001) | 0.001 (0.002) | 0.001 ** (0.001) | −0.001 (0.001) | 0.00002 (0.000) | 0.0006 (0.000) | 0.001 * (0.001) | |

| env_tax | −0.024 *** (0.006) | - | - | - | - | −0.031 * (0.019) | - | - | - | - |

| ener_tax | - | −0.036 *** (0.008) | - | - | - | - | −0.090 * (0.050) | - | - | - |

| pol_tax | - | - | −0.126 *** (0.026) | - | - | - | −0.023 (0.043) | - | - | |

| res_tax | - | - | - | 0.011 (0.040) | - | - | - | - | −0.169 ** (0.082) | - |

| tra_tax | - | - | - | - | −0.142 *** (0.030) | - | - | - | - | 0.012 (0.032) |

| - | - | - | - | - | −5.837 (5.693) | 12.682 ** (5.117) | 8.123 ** (2.478) | 5.814 ** (2.845) | −0.616 (3.026) | |

| 1st order serial correlation (p-value) | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

| 2nd order serial correlation (p-value) | 0.122 | 0.089 | 0.143 | 0.162 | 0.0540 | 0.740 | 0.900 | 0.836 | 0.721 | 0.915 |

| Sargan test (p-value) | 0.227 | 0.348 | 0.336 | 0.183 | 0.963 | 0.115 | 0.699 | 0.091 | 0.150 | 0.007 |

| Number of countries | 34 | 34 | 34 | 34 | 34 | 34 | 34 | 34 | 34 | 34 |

| env_tax | ener_tax | pol_tax | res_tax | tra_tax | |

|---|---|---|---|---|---|

| Lower regime | |||||

| −0.143 ** (0.060) | 0.067 (0.072) | 0.053 (0.057) | 0.173 *** (0.054) | −0.048 (0.082) | |

| 5.180 *** (1.947) | 3.685 *** (1.424) | 2.099 (4.370) | −3.944 * (2.377) | −2.091 ** (1.009) | |

| −0.217 ** (0.099) | −0.154 ** (0.071) | −0.040 (0.212) | 0.247 ** 0.121) | 0.165 *** (0.048) | |

| 0.918 *** (0.104) | 0.816 *** (0.099) | 1.252 *** (0.270) | 0.844 *** (0.134) | 1.316 *** (0.103) | |

| −0.001 * (0.000) | −0.003 *** (0.001) | −0.002 (0.003) | −0.002 *** (0.000) | 0.0006 (0.001) | |

| 0.013 (0.011) | 0.025 *** (0.007) | 0.011 (0.017) | −0.020 (0.016) | −0.024 * (0.014) | |

| env_tax | −0.023 (0.038) | - | - | - | - |

| ener_tax | - | 0.015 (0.043) | - | - | - |

| pol_tax | - | - | −0.034 (0.046) | - | - |

| res_tax | - | - | - | −0.022 *** (0.008) | - |

| tra_tax | - | - | - | - | 0.137 (0.205) |

| Upper regime | |||||

| 0.038 (0.027) | 0.0216 (0.030) | 0.210 ** (0.087) | 0.064 (0.625) | 0.050 ** (0.020) | |

| −2.333 (2.266) | −0.463 (0.972) | 4.205 (4.989) | 29.347 ** (14.750) | 3.779 *** (0.983) | |

| 0.108 (0.115) | 0.033 (0.050) | −0.203 (0.248) | −1.650 ** (0.815) | −0.197 *** (0.048) | |

| 0.503 *** (0.158) | −0.178 (0.125) | 0.243 (0.290) | −0.038 (0.516) | 0.586 *** (0.164) | |

| −0.010 *** (0.003) | −0.006 ** (0.002) | 0.007 (0.006) | −0.019 * (0.011) | 0.002 (0.002) | |

| 0.004 (0.004) | −0.017 *** (0.005) | 0.015 * (0.009) | 0.180 ** (0.090) | 0.019 * (0.010) | |

| env_tax | −0.204 *** (0.068) | - | - | - | - |

| ener_tax | - | −0.107 * (0.057) | - | - | - |

| pol_tax | - | - | −0.293 *** (0.098) | - | - |

| res_tax | - | - | - | −0.477 (0.574) | - |

| tra_tax | - | - | - | - | −0.109 (0.252) |

| Threshold level (p-value) | 3.002 *** (0.000) | 1.991 *** (0.000) | 0.377 *** (0.000) | 0.170 *** (0.000) | 0.434 ** (0.013) |

| 95% confidence interval | 2.453–3.551% | 1.431–2.551% | 0.196–0.557% | 0.159–0.180% | 0.091–0.776% |

| Linearity test (p-value) | 0.000 *** | 0.000 *** | 0.000 *** | 0.000 *** | 0.000 *** |

| No. of countries | 34 | 34 | 34 | 34 | 34 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Al Shammre, A.S.; Benhamed, A.; Ben-Salha, O.; Jaidi, Z. Do Environmental Taxes Affect Carbon Dioxide Emissions in OECD Countries? Evidence from the Dynamic Panel Threshold Model. Systems 2023, 11, 307. https://doi.org/10.3390/systems11060307

Al Shammre AS, Benhamed A, Ben-Salha O, Jaidi Z. Do Environmental Taxes Affect Carbon Dioxide Emissions in OECD Countries? Evidence from the Dynamic Panel Threshold Model. Systems. 2023; 11(6):307. https://doi.org/10.3390/systems11060307

Chicago/Turabian StyleAl Shammre, Abdullah Sultan, Adel Benhamed, Ousama Ben-Salha, and Zied Jaidi. 2023. "Do Environmental Taxes Affect Carbon Dioxide Emissions in OECD Countries? Evidence from the Dynamic Panel Threshold Model" Systems 11, no. 6: 307. https://doi.org/10.3390/systems11060307