Customer Attitude toward Digital Wallet Services

, , , , and

, , , , and

Abstract

:1. Introduction

- The increased dynamic, uncertainty and complexity of the economic situation affect consumers’ requirements, preferences and payment habits. According to the results obtained from a recent global study of Juniper Research [8], more than five billion people (60% of world population) will be using digital wallets by 2026 and “super applications” drive the adoption of e-payments in many countries.

- The latest developments in modern technologies, such as blockchain and artificial intelligence, have the potential to enhance the methods and channels for digital payments [9] and e-wallets as payment tools.

- Propose a theoretical framework that facilitates the systematic analysis of customer data and can reveal hidden relationships.

- Collect and systemize customer dataset about their experience and preferences in online payments (age, residential area, monthly income per household member, attitudes, characteristics of customers’ payments, specific problems).

- Identify the key factors affecting customer intention to use e-wallets and offer methods for their determination according to the review of previous similar research.

- Create and validate a model based on factors from the literature and assess their influence on customer attitude to e-wallets.

2. State of the Art Review of Digital Wallet Platforms

2.1. Key Features of Electronic Wallets

- Near Field Communication (NFC) and Quick Response (QR) code functionality—These in-store features improve customer experience in retail shops.

- The dashboard—The control panel informs users about upcoming bills or how the user spent their money. In addition, some digital wallets have a budget management and expense-tracking module in their applications.

- Chatbot functionality—For e-wallet owners, this can be a valuable supplement to existing communication channels. For e-wallet providers, chatbots can help improve their customer service by offering 24/7 support.

2.2. Digital Wallet Software Products and Their Feature Comparison

3. Related Work

3.1. Customer Satisfaction with Digital Wallet Services and Its Measurement

3.2. Comparison of Existing Models for Customer Satisfaction toward Digital Wallets

3.3. Main Factors Affecting Consumer Intention to Adopt e-Wallet Payments

- 1.

- Perceived usefulness

- 2.

- Perceived ease of use

- 3.

- Social influence

- 4.

- Facilitating conditions

- 5.

- Lifestyle compatibility

- 6.

- Perceived Trust

4. Research Methodology

4.1. Questionnaire Design and Data Collection

4.2. Questionnaire Measurements and Scales

4.3. Data Analysis Methods

- The model is robust to data non-normality.

- The method is appropriate for a relatively small sample size.

- The generated models can be easily interpreted because complex relationships between variables can be visualized in an intuitive way.

- The method is efficient and scalable. PLS-SEM can be used for large models with many indicators and latent variables.

- PLS-SEM can handle formative constructs [49].

5. Data Analysis

5.1. Customers’ Data Collection

5.2. Data Storage

5.3. SEM Model of Customer Attitude to e-Wallets

- Formulate hypotheses about latent variables and their relationships.

- Determine indicators for latent variables.

- Perform numerical modeling and assess the quality of the model.

- Evaluate the model fit. If the model fits the data, proceed to Step 5. Otherwise, return to Step 3 and improve the model.

- Interpret the obtained results.

6. Conclusions and Future Research

- An online survey was conducted to collect a dataset of customers’ opinions regarding their willingness to adopt e-wallet payments. Based on a demographic analysis of survey data, the majority of respondents (95%) reside in urban areas, with 29% being under 30 years old and 74% being female. Around one-third of respondents (30%) reported using the Internet for more than four hours per day. In terms of education, respondents were split roughly equally between high school, bachelor’s degree and master’s or doctoral studies. Analysis of customer sentiment revealed that a majority (72%) expressed a positive attitude toward e-wallets as a convenient tool for cashless transactions. Just a quarter (25%) of the respondents reported that their interest in e-wallets has risen due to the pandemic.

- The customers were grouped into two statistically significant clusters. The first cluster consisted of respondents who reported higher levels of satisfaction in perceived usefulness, perceived ease of use, facilitating conditions and lifestyle compatibility. On the other hand, the second cluster included those who reported relatively low levels of satisfaction in social influence and perceived trust.

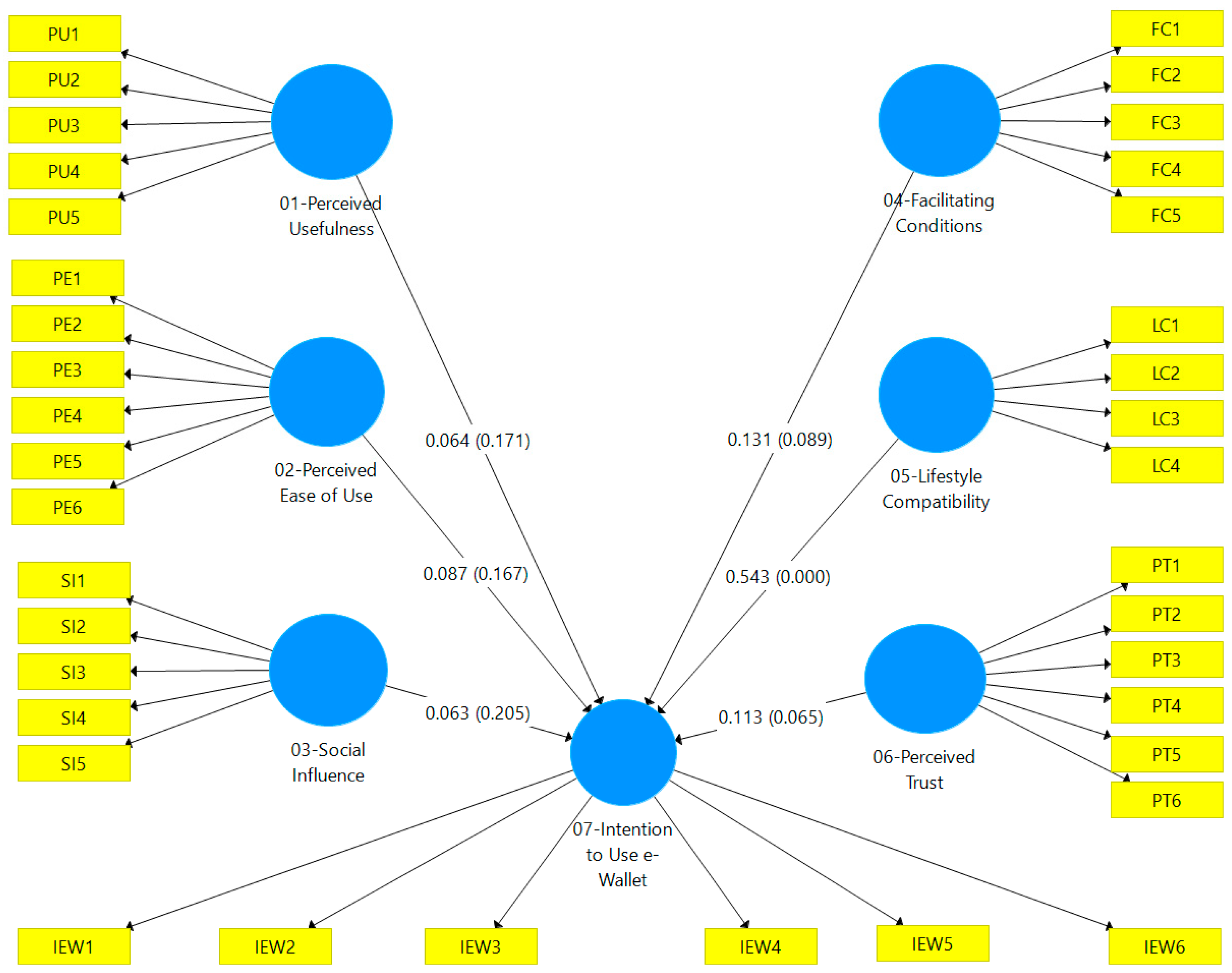

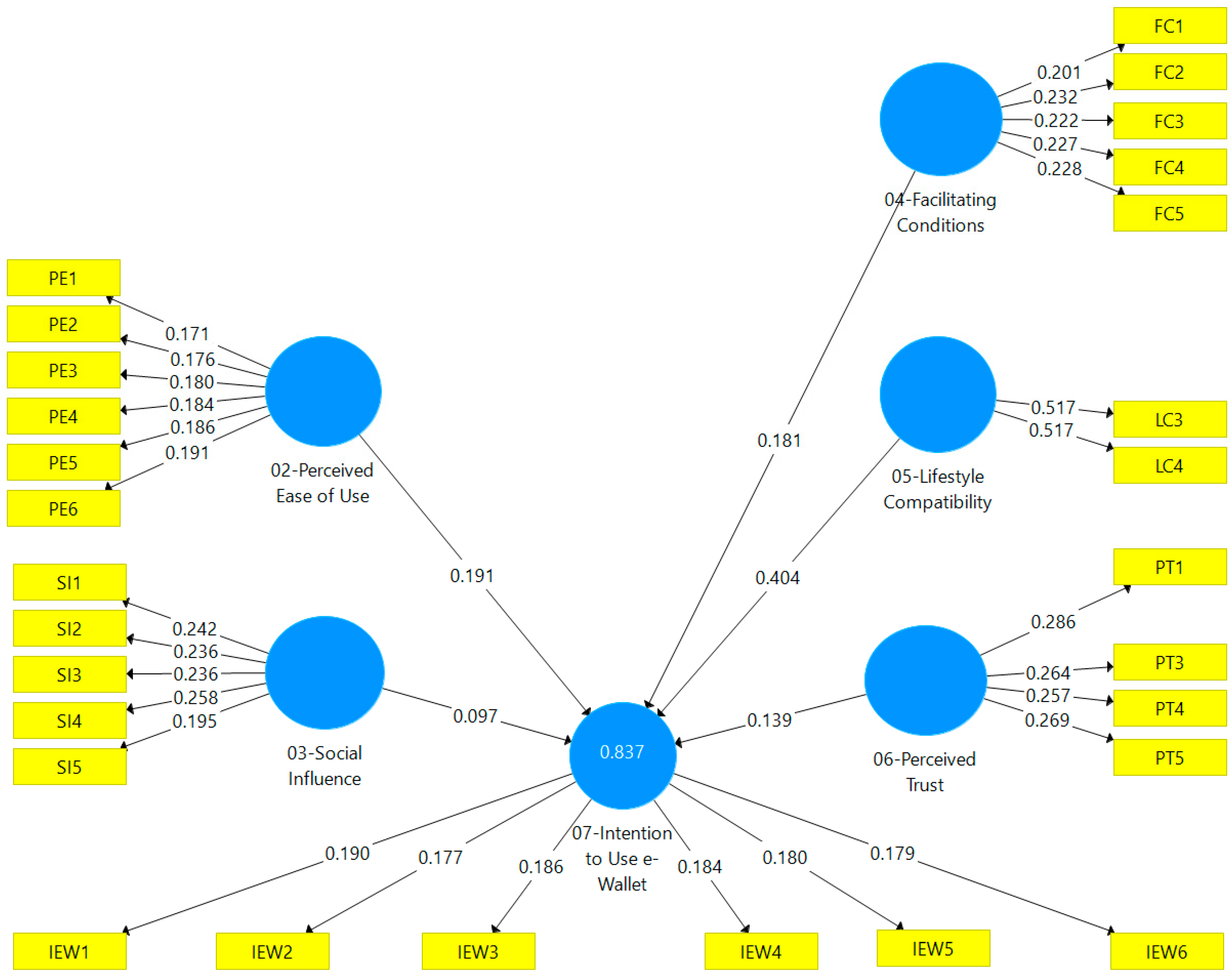

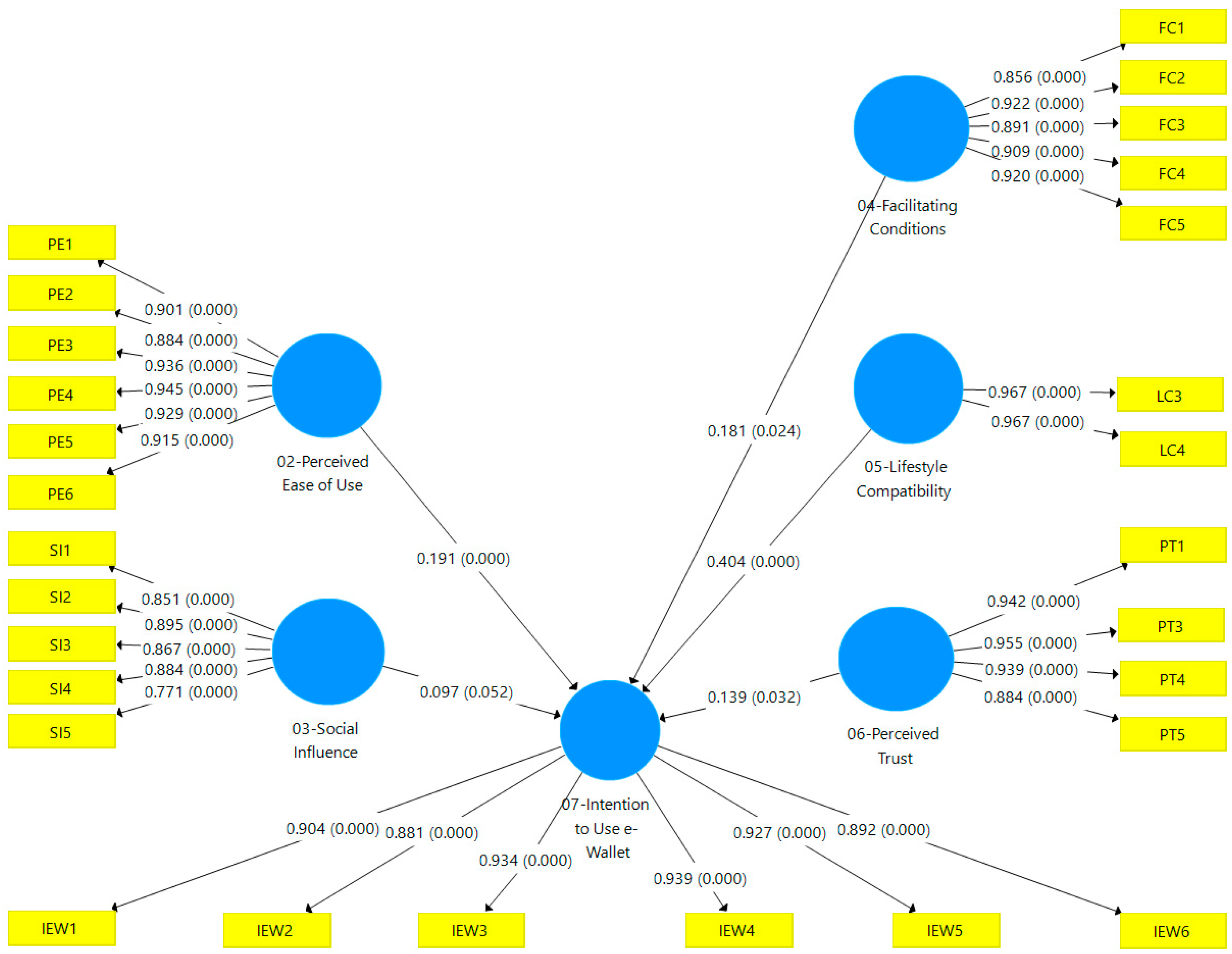

- The developed theoretical causal (SEM) model has revealed that hypotheses H2, H3, H4, H5 and H6, which postulated a significant impact of perceived ease of use, social influence, facilitating conditions, lifestyle compatibility and perceived trust on customer adoption of e-wallets, were supported by our testing. Conversely, hypothesis H1, which suggested that perceived usefulness affects customer attitude, was rejected. Additionally, our analysis of hypothesis H7 indicated that customers’ intention to adopt e-wallets was not affected by socio-economic factors such as age, gender, education level, time spent online or area of residence. The only factor that was found to have a significant effect on customers’ attitude was their past experience with e-wallets.

- At a micro-level, electronic store owners can employ them to enhance and expand their payment systems.

- At a national level, they can be utilized to ensure the efficient operation of national payment systems, including the timely issuance of public money in the form of cash and, potentially, digital currency in the future.

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Shaw, N.; Eschenbrenner, B.; Baier, D. Online Shopping Continuance after COVID-19: A Comparison of Canada, Germany and the United States. J. Retail. Consum. Serv. 2022, 69, 103100. [Google Scholar] [CrossRef]

- World Bank. The Global Findex Database 2021: Financial Inclusion, Digital Payments, and Resilience in the Age of COVID-19. Available online: https://www.worldbank.org/en/publication/globalfindex (accessed on 15 February 2023).

- Kabir, M.A.; Saidin, S.Z.; Ahmi, A. Adoption of E-payment Systems: A Review of Literature. In Proceedings of the International Conference on E-Commerce, Kuching, Malaysia, 20–22 October 2015; pp. 112–120. [Google Scholar]

- Traver, C.G.; Laudon, K.C. E-Commerce 2017: Business, Technology, Society, 13th ed.; Pearson: New York, NY, USA, 2018. [Google Scholar]

- Taghiloo, M.; Agheli, M.A.; Rezaeinezhad, M.R. Mobile Based Secure Digital Wallet for Peer to Peer Payment System. Int. J. UbiComp 2010, 1, 1–11. [Google Scholar] [CrossRef]

- Appriss Retail. The Rise in Contactless Payments during COVID-19. Available online: https://blog.apprissretail.com/blog/the-rise-in-contactless-payments-during-covid-19 (accessed on 15 February 2023).

- Worldpay. Global Payments Report (Published in 2020). Available online: https://worldpay.globalpaymentsreport.com/en (accessed on 15 February 2023).

- Juniper Research 2022. Digital Wallets: Market Forecasts, Key Opportunities and Vendor Analysis 2022–2026. Available online: https://www.juniperresearch.com/researchstore/fintech-payments/digital-wallet-research-report (accessed on 15 February 2023).

- Barroso, M.; Laborda, J. Digital Transformation and the Emergence of the Fintech Sector: Systematic Literature Review. Digit. Bus. 2022, 2, 100028. [Google Scholar] [CrossRef]

- Naysary, B. Big Data Analytics Application in Multi-Criteria Decision Making: The Case of eWallet Adoption. Available online: https://ssrn.com/abstract=4076471 (accessed on 5 April 2023).

- Senali, M.G.; Iranmanesh, M.; Ismail, F.N.; Rahim, N.F.A.; Khoshkam, M.; Mirzaei, M. Determinants of Intention to Use e-Wallet: Personal Innovativeness and Propensity to Trust as Moderators. Int. J. Hum.-Comput. Interact. 2022, 38, 1–13. [Google Scholar] [CrossRef]

- Abbasi, G.A.; Sandran, T.; Ganesan, Y.; Iranmanesh, M. Go cashless! Determinants of Continuance Intention to Use E-wallet Apps: A Hybrid Approach Using PLS-SEM and fsQCA. Technol. Soc. 2022, 68, 101937. [Google Scholar] [CrossRef]

- Tang, S.; Wu, Z.; Zhang, X.; Wang, G.; Ma, X.; Zheng, H.; Zhao, B.Y. Towards Understanding the Adoption and Social Experience of Digital Wallet Systems. In Proceedings of the Hawaii International Conference on System Sciences (HICSS), Maui, HI, USA, 8–11 January 2019. [Google Scholar]

- Ryan, F.; Pascoe, A. The role of WeChat Pay and Alipay in DC/EP. The Role of WeChat Pay and Alipay in DC/EP. In The Flipside of China’s Central Bank Digital Currency; Australian Strategic Policy Institute: Canberra, Australia, 2020; pp. 19–22. [Google Scholar]

- Drenten, J. Digital Payment,“Venmo Me” Culture, and Sociality. In The Routledge Handbook of Digital Consumption, 2nd ed.; Llamas, R., Belk, R., Eds.; Routledge: Abingdon, UK, 2022; pp. 98–110. [Google Scholar]

- Acker, A.; Murthy, D. What is Venmo? A Descriptive Analysis of Social Features in the Mobile Payment Platform. Telemat. Inform. 2020, 52, 101429. [Google Scholar] [CrossRef]

- Tang, Y.M.; Chau, K.Y.; Hong, L.; Ip, Y.K.; Yan, W. Financial Innovation in Digital Payment with WeChat towards Electronic Business Success. J. Theor. Appl. Electron. Commer. Res. 2021, 16, 1844–1861. [Google Scholar] [CrossRef]

- Jiang, X.N. Analysis of WeChat Pay Based on Technology Acceptance Model. In Proceedings of the 7th International Conference on Social Sciences and Economic Development (ICSSED 2022), Wuhan, China, 25–27 March 2022; pp. 668–675. [Google Scholar]

- Esther Krupa, M. A Study on Users Perception towards Selected E-wallets (Google Pay & Paytm) Among College Students. Gedrag Organ. 2022, 35, 318–327. [Google Scholar]

- Rahuman, M.A.; Khader, A.A. Comparative Study of Customer Satisfaction on Google Pay and Phonepe Mobile Apps. Int. J. Latest Res. Humanit. Soc. Sci. 2022, 5, 165–167. [Google Scholar]

- Liébana-Cabanillas, F.; García-Maroto, I.; Muñoz-Leiva, F.; Ramos-de-Luna, I. Mobile payment adoption in the age of digital transformation: The case of Apple Pay. Sustainability 2020, 12, 5443. [Google Scholar] [CrossRef]

- Manickam, T.; Vinayagamoorthi, G.; Gopalakrishnan, S.; Sudha, M.; Mathiraj, S.P. Customer Inclination on Mobile Wallets with Reference to Google-Pay and PayTM in Bengaluru City. Int. J. E-Bus. Res. 2022, 18, 1–16. [Google Scholar] [CrossRef]

- Gomachab, R.; Maseke, B.F. The Impact of Mobile Banking on Customer Satisfaction: Commercial Banks of Namibia (Keetmanshoop). J. Internet Bank. Commer. 2018, 23, 1–18. [Google Scholar]

- de Sena Abrahão, R.; Moriguchi, S.N.; Andrade, D.F. Intention of Adoption of Mobile Payment: An Analysis in the Light of the Unified Theory of Acceptance and Use of Technology (UTAUT). RAI Rev. Adm. E Inovação 2016, 13, 221–230. [Google Scholar] [CrossRef] [Green Version]

- Lin, H.Y.; Wang, M.H.; Chen, H.T. Determinants for Consumer Adoption of Mobile Payment Technology. Int. J. e-Educ. e-Bus. e-Manag. e-Learn. 2019, 9, 146–159. [Google Scholar] [CrossRef]

- Malik, A.; Suresh, S.; Sharma, S. An Empirical Study of Factors Influencing Consumers’ Attitude towards Adoption of Wallet Apps. Int. J. Manag. Pract. 2019, 12, 426–442. [Google Scholar] [CrossRef]

- Phan, T.N.; Ho, T.V.; Le-Hoang, P.V. Factors Affecting the Behavioral Intention and Behavior of Using E-wallets of Youth in Vietnam. J. Asian Financ. Econ. Bus. 2020, 7, 295–302. [Google Scholar] [CrossRef]

- Yang, M.; Mamun, A.A.; Mohiuddin, M.; Nawi, N.C.; Zainol, N.R. Cashless Transactions: A Study on Intention and Adoption of e-Wallets. Sustainability 2021, 13, 831. [Google Scholar] [CrossRef]

- Shane, J.M.S.S.; Chan, T.J.; Mohan, Y.M. Factors Affecting the Intention to Adopt E-Wallet Services during COVID-19 Pandemic. J. Arts Soc. Sci. 2022, 5, 28–40. [Google Scholar]

- Wardana, A.A.; Saputro, E.P.; Wahyuddin, M.; Abas, N.I. The Effect of Convenience, Perceived ease of use, and Perceived Usefulness on Intention to Use E-wallet: Empirical Study on Generation Z in Surakarta. In Proceedings of the International Conference on Economics and Business Studies (ICOEBS 2022), Sukarta, Indonesia, 5–6 December 2022; Volume 655, pp. 386–395. [Google Scholar]

- Kınış, F.; Tanova, C. Can I Trust My Phone to Replace My Wallet? The Determinants of E-Wallet Adoption in North Cyprus. J. Theor. Appl. Electron. 2022, 17, 1696–1715. [Google Scholar] [CrossRef]

- Raninda, R.; Wisnalmawati, W.; Oetomo, H. The Effect of Perceived Usefulness, Perceived Ease of Use, Perceived Security, and Cashback Promotion on Behavioral Intention to the DANA E-Wallet. J. Ilm. Manaj. Kesatuan 2022, 10, 63–72. [Google Scholar] [CrossRef]

- Davis, F.D. Perceived Usefulness, Perceived Ease of Use, and User Acceptance of Information Technology. MIS Q. 1989, 13, 319–340. [Google Scholar] [CrossRef] [Green Version]

- Venkatesh, V.; Davis, F.D. A Theoretical Extension of the Technology Acceptance Model: Four Longitudinal Field Studies. Manag. Sci. 2000, 46, 186–204. [Google Scholar] [CrossRef] [Green Version]

- Venkatesh, V.; Morris, M.G.; Davis, G.B.; Davis, F.D. User Acceptance of Information Technology: Toward a Unified View. MIS Q. 2003, 27, 425–478. [Google Scholar] [CrossRef] [Green Version]

- Venkatesh, V.; Bala, H. Technology Acceptance Model 3 and a Research Agenda on Interventions. Decis. Sci. J. 2008, 39, 273–315. [Google Scholar] [CrossRef] [Green Version]

- Sarmah, R.; Dhiman, N.; Kanojia, H. Understanding Intentions and Actual Use of Mobile Wallets by Millennial: An Extended TAM Model Perspective. J. Indian Bus. Res. 2021, 13, 361–381. [Google Scholar] [CrossRef]

- Tian, Y.; Chan, T.J.; Suki, N.M.; Kasim, M.A. Moderating Role of Perceived Trust and Perceived Service Quality on Consumers’ Use Behavior of Alipay e-wallet System: The Perspectives of Technology Acceptance Model and Theory of Planned Behavior. Hum. Behav. Emerg. Technol. 2023, 5276406, 14. [Google Scholar] [CrossRef]

- Teo, S.C.; Law, P.L.; Koo, A.C. Factors Affecting Adoption of E-wallets among Youths in Malaysia. J. Inf. Syst. Technol. Manag. 2020, 5, 39–50. [Google Scholar] [CrossRef]

- Shaw, N.; Sergueeva, K. The Non-monetary Benefits of Mobile Commerce: Extending UTAUT2 with Perceived Value. Int. J. Inf. Manag. 2019, 45, 44–55. [Google Scholar] [CrossRef]

- Muhtasim, D.A.; Tan, S.Y.; Hassan, M.A.; Pavel, M.I.; Susmit, S. Customer Satisfaction with Digital Wallet Services: An Analysis of Security Factors. Int. J. Adv. Comput. Sci. Appl. 2022, 13, 195–206. [Google Scholar] [CrossRef]

- Oliveira, T.; Thomas, M.; Baptista, G.; Campos, F. Mobile Payment: Understanding the Determinants of Customer Adoption and Intention to Recommend the Technology. Comput. Hum. Behav. 2016, 61, 404–414. [Google Scholar] [CrossRef]

- Lwoga, E.T.; Lwoga, N.B. User Acceptance of Mobile Payment: The Effects of User-Centric Security, System Characteristics and Gender. Electron. J. Inf. Syst. Dev. Ctries 2017, 81, 1–24. [Google Scholar] [CrossRef] [Green Version]

- Chawla, D.; Joshi, H. Role of Mediator in Examining the Influence of Antecedents of Mobile Wallet Adoption on Attitude and Intention. Glob. Bus. Rev. 2020. [Google Scholar] [CrossRef]

- Pandey, S.; Chawla, D. Engaging M-commerce Adopters in India: Exploring the Two Ends of the Adoption Continuum across Four M-commerce Categories. J. Enterp. Inf. Manag. 2019, 32, 191–210. [Google Scholar] [CrossRef]

- Karjaluoto, H.; Shaikh, A.A.; Leppäniemi, M.; Luomala, R. Examining Consumers’ Usage Intention of Contactless Payment Systems. Int. J. Bank Mark. 2019, 38, 332–351. [Google Scholar] [CrossRef]

- Ilieva, G.; Yankova, T.; Dzhabarova, Y.; Ruseva, M.; Angelov, D.; Klisarova-Belcheva, S. Impact of COVID-19 Pandemic on Cus-tomer Attitude toward E-wallet Payments. In Mendeley Data; Elsevier: Amsterdam, The Netherlands, 2023. [Google Scholar]

- Beran, T.N.; Violato, C. Structural Equation Modeling in Medical Research: A Primer. BMC Res. Notes 2010, 3, 267. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Shiau, W.L.; Sarstedt, M.; Hair, J.F. Internet Research Using Partial Least Squares Structural Equation Modeling (PLS-SEM). Internet Res. 2019, 29, 398–406. [Google Scholar] [CrossRef]

- McKinsey. Consumer Trends in Digital Payments. Available online: https://www.mckinsey.com/industries/financial-services/our-insights/banking-matters/consumer-trends-in-digital-payments (accessed on 15 February 2023).

- Ringle, C.M.; Wende, S.; Becker, J.-M. SmartPLS 3; SmartPLS GmbH: Bönningstedt, Germany, 2015. [Google Scholar]

- Pett, M.A.; Lackey, N.R.; Sullivan, J.J. Making Sense of Factor Analysis: The Use of Factor Analysis for Instrument Development In Health Care Research; Sage Publications: Thousand Oaks, CA, USA, 2003. [Google Scholar]

- Hair, J.F., Jr.; Black, W.C.; Babin, B.J.; Andreson, R.E. Multivariate Data Analysis, 7th ed.; Pearson: Edinburgh, UK, 2014. [Google Scholar]

- Fornell, C.; Bookstein, F.L. Two Structural Equation Models: LISREL and PLS Applied to Consumer Exit-voice Theory. J. Mark Res. 1982, 19, 440–452. [Google Scholar] [CrossRef] [Green Version]

- Rahi, S.; Ghani, M.; Alnaser, F.; Ngah, A. Investigating the Role of Unified Theory of Acceptance and Use of Technology (UTAUT) in Internet Banking Adoption Context. Manag. Sci. Lett. 2018, 8, 173–186. [Google Scholar] [CrossRef]

- Almazroa, M.; Gulliver, S. Understanding the Usage of Mobile Payment Systems—The Impact of Personality on the Continuance Usage. In Proceedings of the 4th International Conference on Information Management (ICIM), London, UK, 25–27 May 2018; pp. 188–194. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Digital Wallet | Supported Platforms | Payment Services | Payment Methods | In-Store Technologies |

|---|---|---|---|---|

| PayPal | Web, iOS, Android | Online and mobile payments, invoicing and checkout | Bank cards, bank transfers, PayPal balance | NFC, QR codes |

| Alipay | Web, iOS, Android | Online and mobile payments, invoicing and checkout | Bank cards, bank transfers, AliPay balance | NFC, QR codes, facial recognition |

| Amazon Pay | Web, iOS, Android | Online and mobile payments, checkout | Bank cards, bank transfers, Amazon Pay balance | QR codes |

| Venmo | Web, iOS, Android | P2P transfers, in-app purchases | Bank cards, bank transfers, Venmo balance | QR codes |

| Dwolla | Web, iOS, Android | Online, mobile, invoicing and recurring payments | Bank transfer only | – |

| WeChat Pay | iOS, Android | Online and mobile payments, P2P transfers | Bank cards, WeChat Pay balance | NFC, QR codes, facial recognition |

| Google Wallet | Web, iOS, Android | Online and mobile payments, P2P transfers | Bank cards, bank transfers, Google Wallet balance | NFC, QR codes |

| Apple Pay | iOS, Apple Watch | Online and mobile payments, P2P transfers | Bank cards, bank transfers, Apple Pay balance | NFC |

| Samsung Wallet | Android, Samsung smart watches | Online and mobile payments | Bank cards, bank transfers, Samsung Wallet balance | NFC, MST * |

| Cash App | iOS, Android | P2P transfers, Bitcoin purchases | Bank cards, bank transfers, Cash App balance | QR codes |

| Shop Pay | iOS, Android | Online checkout service | Bank cards, Apple Pay, Google Wallet, UPI **, Net banking | QR codes |

| Meta Pay | iOS, Android | Online payments | Bank cards, PayPal, Shop Pay | NFC, QR codes |

| PayTM | iOS, Android | P2P and peer-to-merchant transfers | Bank cards, UPI, Net banking | QR codes, sound-based payments |

| PhonePe | iOS Android | Money transfers, offline and online payments | Bank cards, UPI, Net banking | NFC, QR codes |

| YooMoney | iOS, Android | Online and offline payments | Bank cards, e-wallet, cash | NFC, QR codes |

| Reference | Utilized Algorithm | Evaluation Metrics (Number) | Statistically Significant Factors (Number) | R2 |

|---|---|---|---|---|

| Davis 1989 [34] | MLR | Usefulness, Ease of Use (2) Usage | Usefulness (1) | 0.31–0.74 |

| Venkatesh and Davis 2000 [35] | PLS-SEM | Perceived usefulness, Perceived ease of use, Subjective norm (3) | Perceived usefulness, Perceived ease of use, Subjective norm (3) | 0.37–0.52 |

| Venkatesh et al. 2003 [36] | PLS-SEM | Effort expectancy, Performance expectancy, Social influence, Facilitating conditions (4) | Effort expectancy, Performance expectancy (2) | 0.36–0.77 |

| Venkatesh and Bala 2008 [37] | PLS-SEM | Perceived usefulness, Perceived ease of use, Subjective norm, Voluntariness (4) | Perceived usefulness, Perceived ease of use (2) | 0.40–0.53 |

| de Sena Abrahão et al. 2016 [24] | PLS-SEM | Perceived expectations, Effort expectations, Social influence, Perceived risk, Perceived cost (5) | Perceived expectations, Effort expectations, Social influence, Perceived risk (4) | 0.762 |

| Lin et al. 2019 [25] | PLS-SEM | Perceived expectancy, Effort expectancy, Social influence, Facilitating conditions, Hedonic motivation, Price value, Security (7) | Perceived expectancy, Hedonic motivation, Security (3) | 0.660 |

| Malik et al. 2019 [26] | MLR | Performance expectancy, Ease of use, Social influence, Enjoyment, Incentives, Aesthetics, Trust (7) | Performance expectancy, Incentives, Trust (3) | 0.207–0.300 |

| Phan et al. 2020 [27] | PLS-SEM | Effort expectancy, Performance expectancy, Social influence, Security and privacy (4) | Performance expectancy, Social influence (2) | – |

| Yang et al. 2021 [28] | PLS-SEM | Perceived usefulness, Perceived ease of use, Social influence, Facilitating conditions, Lifestyle compatibility, Perceived trust (6) | Usefulness, Ease of use, Social influence, Lifestyle compatibility, Perceived trust (5) | 0.726 |

| Shane et al. 2022 [29] | PLS-SEM | Performance expectancy, Effort expectancy, Social influence, Facilitating conditions, Promotional benefits, Perceived trust (6) | Performance expectancy, Facilitating conditions (2) | 0.478 |

| Wardana et al. 2022 [30] | PLS-SEM | Convenience, Perceived usefulness, Perceived ease of use (3) | Convenience, Perceived usefulness, Perceived ease of use (3) | 0.603 |

| Kınış and Tanova 2022 [31] | PLS-SEM | Customer knowledge, Perceived ease of use, Perceived usefulness, Trust (4) | Customer knowledge, Perceived ease of use, Perceived usefulness, Trust (4) | 0.49–0.69 |

| Raninda et al. 2022 [32] | MLR | Perceived usefulness, Perceived ease of use, Perceived security, Cashback promotion (4) | Perceived usefulness, Perceived ease of use, Perceived security, Cashback promotion (4) | 0.570 |

| Naysary 2022 [10] | ML, AHP | Usefulness, Risk, Ease of use, Customer service, User interface, Trust, Promotional reward, Associated costs, Interoperability, Security (10) | Customers’ clusters, e-wallets’ ranking | – |

| Variables of the Sample | No. of Consumers | Percentage (%) | |

|---|---|---|---|

| 1. Gender | Male | 67 | 26.1 |

| Female | 190 | 73.9 | |

| 2. Age | Under 20 | 64 | 24.9 |

| Between 21 and 30 | 75 | 29.2 | |

| Between 31 and 40 | 31 | 12.1 | |

| Between 41 and 50 | 60 | 23.3 | |

| Over 50 | 27 | 10.5 | |

| 3. Place of residence | City | 170 | 66.1 |

| Town | 73 | 28.4 | |

| Village | 14 | 5.4 | |

| 4. Municipality/Province | - | - | |

| 5. Monthly income per household member | Less than BGN 1320 | 132 | 51.4 |

| More than BGN 1320 | 125 | 48.6 | |

| 6. Education | High school | 99 | 38.5 |

| Bachelor | 79 | 30.7 | |

| Master | 73 | 28.4 | |

| PhD | 6 | 2.3 | |

| 7. Frequency of Internet usage per day | Less than 1 h | 37 | 14.4 |

| 1–4 h | 143 | 55.6 | |

| More than 4 h | 77 | 30.0 | |

| 8. Do you pay online? | Yes, via bank software | 143 | 55.6 |

| Yes, via software of non-banking organization | 23 | 8.9 | |

| Yes, via bank and non-bank software | 19 | 7.4 | |

| Other | 2 | 0.8 | |

| No | 70 | 27.2 | |

| 18. Average number of e-wallet payments (monthly) | Never | 53 | 20.6 |

| Between 1 and 5 times | 77 | 30.0 | |

| Between 6 and 10 times | 50 | 19.5 | |

| Between 11 and 15 times | 22 | 8.6 | |

| More than 15 times | 55 | 21.4 | |

| PU1 | PU2 | PU3 | PU4 | PU5 | PE1 | PE2 | PE3 | PE4 | |

|---|---|---|---|---|---|---|---|---|---|

| Cluster #1 | 4.269 | 4.11 | 3.909 | 4.274 | 4.224 | 3.886 | 3.708 | 4.137 | 4.146 |

| Cluster #2 | 1.816 | 1.789 | 1.684 | 1.842 | 1.737 | 1.737 | 1.711 | 1.895 | 1.842 |

| Difference | 2.454 | 2.32 | 2.224 | 2.432 | 2.487 | 2.149 | 1.997 | 2.242 | 2.304 |

| PE5 | PE6 | SI1 | SI2 | SI3 | SI4 | SI5 | FC1 | FC2 | |

| Cluster #1 | 4.151 | 4.192 | 3.466 | 3.507 | 3.644 | 3.826 | 3.443 | 3.685 | 3.991 |

| Cluster #2 | 1.921 | 1.684 | 1.632 | 1.658 | 1.816 | 1.711 | 1.789 | 1.789 | 1.816 |

| Difference | 2.23 | 2.508 | 1.834 | 1.849 | 1.828 | 2.116 | 1.653 | 1.895 | 2.175 |

| FC3 | FC4 | FC5 | LC1 | LC2 | LC3 | LC4 | PT1 | PT2 | |

| Cluster #1 | 3.954 | 3.726 | 3.817 | 3.858 | 4.023 | 3.986 | 3.772 | 3.749 | 3.721 |

| Cluster #2 | 1.816 | 1.605 | 1.632 | 1.658 | 1.579 | 1.658 | 1.632 | 1.711 | 1.684 |

| Difference | 2.139 | 2.121 | 2.186 | 2.201 | 2.444 | 2.328 | 2.14 | 2.038 | 2.037 |

| PT3 | PT4 | PT5 | PT6 | IEW1 | IEW2 | IEW3 | IEW4 | IEW5 | |

| Cluster #1 | 3.671 | 3.662 | 3.712 | 3.749 | 3.959 | 3.904 | 4.027 | 3.849 | 3.804 |

| Cluster #2 | 1.658 | 1.763 | 1.658 | 1.737 | 1.526 | 1.737 | 1.789 | 1.711 | 1.632 |

| Difference | 2.013 | 1.899 | 2.054 | 2.012 | 2.433 | 2.167 | 2.238 | 2.139 | 2.172 |

| IEW6 | AEW1 | AEW2 | AEW3 | AEW4 | AEW5 | ||||

| Cluster #1 | 3.662 | 3.968 | 3.918 | 4.068 | 3.233 | 2.836 | |||

| Cluster #2 | 1.526 | 1.947 | 1.763 | 1.789 | 1.711 | 2.605 | |||

| Difference | 2.136 | 2.021 | 2.155 | 2.279 | 1.522 | 0.23 |

| Indicator Variable | Factor Loading | Indicator Variable | Factor Loading | Indicator Variable | Factor Loading | Indicator Variable | Factor Loading |

|---|---|---|---|---|---|---|---|

| PE1 | 0.901 | SI2 | 0.895 | FC4 | 0.909 | PT5 | 0.884 |

| PE2 | 0.884 | SI3 | 0.867 | FC5 | 0.920 | IEW1 | 0.904 |

| PE3 | 0.936 | SI4 | 0.884 | LC3 | 0.967 | IEW2 | 0.881 |

| PE4 | 0.945 | SI5 | 0.771 | LC4 | 0.967 | IEW3 | 0.954 |

| PE5 | 0.929 | FC1 | 0.856 | PT1 | 0.942 | IEW4 | 0.939 |

| PE6 | 0.915 | FC2 | 0.922 | PT3 | 0.955 | IEW5 | 0.927 |

| SI1 | 0.851 | FC3 | 0.891 | PT4 | 0.939 | IEW6 | 0.892 |

| Factor | DG Rho | CR | AVE | VIF |

|---|---|---|---|---|

| Perceived ease of use | 0.964 * | 0.970 * | 0.884 * | 3.119 * |

| Social influence | 0.914 * | 0.931 * | 0.731 * | 2.720 * |

| Facilitating conditions | 0.944 * | 0.955 * | 0.810 * | 4.573 * |

| Lifestyle compatibility | 0.931 * | 0.967 * | 0.935 * | 3.370 * |

| Perceived trust | 0.949 * | 0.963 * | 0.866 * | 3.676 * |

| Intention to use e-wallet | 0.960 * | 0.968 * | 0.834 * |

| Factor | Perceived Ease of Use | Social Influence | Facilitating Conditions | Lifestyle Compatibility | Perceived Trust | Intention to Use e-Wallet |

|---|---|---|---|---|---|---|

| Perceived ease of use | 0.919 | |||||

| Social influence | 0.706 | 0.855 | ||||

| Facilitating conditions | 0.769 | 0.741 | 0.900 | |||

| Lifestyle compatibility | 0.768 | 0.733 | 0.775 | 0.967 | ||

| Perceived trust | 0.712 | 0.720 | 0.834 | 0.793 | 0.930 | |

| Intention to use e-wallet | 0.807 | 0.862 | 0.828 | 0.864 | 0.792 | 0.913 |

| Indicator Variable | Perceived Ease of Use | Social Influence | Facilitating Conditions | Lifestyle Compatibility | Perceived Trust | Intention to Use e-Wallet |

|---|---|---|---|---|---|---|

| PE1 | 0.901 | 0.636 | 0.668 | 0.691 | 0.654 | 0.698 |

| PE2 | 0.884 | 0.653 | 0.702 | 0.675 | 0.645 | 0.719 |

| PE3 | 0.936 | 0.651 | 0.692 | 0.690 | 0.665 | 0.737 |

| PE4 | 0.945 | 0.630 | 0.706 | 0.713 | 0.642 | 0.753 |

| PE5 | 0.929 | 0.639 | 0.729 | 0.712 | 0.659 | 0.762 |

| PE6 | 0.915 | 0.682 | 0.737 | 0.746 | 0.662 | 0.778 |

| SI1 | 0.633 | 0.851 | 0.647 | 0.635 | 0.623 | 0.670 |

| SI2 | 0.632 | 0.895 | 0.617 | 0.632 | 0.645 | 0.656 |

| SI3 | 0.584 | 0.867 | 0.654 | 0.599 | 0.592 | 0.656 |

| SI4 | 0.669 | 0.884 | 0.691 | 0.696 | 0.656 | 0.715 |

| SI5 | 0.481 | 0.771 | 0.545 | 0.560 | 0.554 | 0.540 |

| FC1 | 0.629 | 0.632 | 0.856 | 0.623 | 0.691 | 0.673 |

| FC2 | 0.734 | 0.676 | 0.922 | 0.704 | 0.746 | 0.780 |

| FC3 | 0.720 | 0.675 | 0.891 | 0.696 | 0.678 | 0.745 |

| FC4 | 0.670 | 0.674 | 0.909 | 0.743 | 0.837 | 0.762 |

| FC5 | 0.704 | 0.677 | 0.920 | 0.717 | 0.799 | 0.763 |

| LC3 | 0.768 | 0.703 | 0.775 | 0.967 | 0.718 | 0.835 |

| LC4 | 0.717 | 0.715 | 0.724 | 0.967 | 0.700 | 0.835 |

| PT1 | 0.697 | 0.688 | 0.775 | 0.717 | 0.942 | 0.781 |

| PT3 | 0.639 | 0.647 | 0.747 | 0.675 | 0.955 | 0.721 |

| PT4 | 0.651 | 0.679 | 0.762 | 0.668 | 0.939 | 0.703 |

| PT5 | 0.661 | 0.663 | 0.819 | 0.663 | 0.884 | 0.735 |

| IEW1 | 0.761 | 0.702 | 0.794 | 0.827 | 0.738 | 0.904 |

| IEW2 | 0.716 | 0.679 | 0.753 | 0.751 | 0.707 | 0.881 |

| IEW3 | 0.748 | 0.680 | 0.804 | 0.791 | 0.738 | 0.934 |

| IEW4 | 0.742 | 0.718 | 0.755 | 0.782 | 0.753 | 0.939 |

| IEW5 | 0.724 | 0.711 | 0.734 | 0.771 | 0.741 | 0.927 |

| IEW6 | 0.730 | 0.683 | 0.695 | 0.806 | 0.659 | 0.892 |

| Factor | Perceived Ease of Use | Social Influence | Facilitating Conditions | Lifestyle Compatibility | Perceived Trust | Intention to Use e-Wallet |

|---|---|---|---|---|---|---|

| Perceived ease of use | ||||||

| Social influence | 0.751 | |||||

| Facilitating conditions | 0.806 | 0.799 | ||||

| Lifestyle compatibility | 0.810 | 0.796 | 0.827 | |||

| Perceived trust | 0.745 | 0.775 | 0.882 | 0.780 | ||

| Intention to use e-wallet | 0.839 | 0.813 | 0.870 | 0.913 | 0.818 |

| Hypothesis | Sample Mean | Mean | SD | t Statistics | p Values | R2 | f2 | Q2 | |

|---|---|---|---|---|---|---|---|---|---|

| 02-Perceived ease of use 07-Intention to use e-wallet | 0.191 | 0.190 | 0.191 | 0.051 | 3.719 | 0.000 | 0.837 | 0.072 | 0.689 |

| 03-Social influence 07-Intention to use e-wallet | 0.097 | 0.093 | 0.097 | 0.049 | 1.958 | 0.052 | 0.021 | ||

| 04-Facilitating conditions 07-Intention to use e-wallet | 0.181 | 0.184 | 0.181 | 0.075 | 2.397 | 0.024 | 0.044 | ||

| 05-Lifestyle compatibility 07-Intention to use e-wallet | 0.404 | 0.405 | 0.404 | 0.069 | 5.827 | 0.000 | 0.296 | ||

| 06-Perceived trust 07-Intention to use e-wallet | 0.139 | 0.138 | 0.139 | 0.061 | 2.282 | 0.032 | 0.032 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ilieva, G.; Yankova, T.; Dzhabarova, Y.; Ruseva, M.; Angelov, D.; Klisarova-Belcheva, S. Customer Attitude toward Digital Wallet Services. Systems 2023, 11, 185. https://doi.org/10.3390/systems11040185

Ilieva G, Yankova T, Dzhabarova Y, Ruseva M, Angelov D, Klisarova-Belcheva S. Customer Attitude toward Digital Wallet Services. Systems. 2023; 11(4):185. https://doi.org/10.3390/systems11040185

Chicago/Turabian StyleIlieva, Galina, Tania Yankova, Yulia Dzhabarova, Margarita Ruseva, Delian Angelov, and Stanislava Klisarova-Belcheva. 2023. "Customer Attitude toward Digital Wallet Services" Systems 11, no. 4: 185. https://doi.org/10.3390/systems11040185