Income and Asset Situation of Companies Producing Arable Crops in the Visegrad Countries

Abstract

:1. Introduction

- What were the harvested areas, average yields, and selling prices for the main arable crops (wheat, barley, maize, rapeseed) grown in the V4 countries during the examined period?

- How did the farm size and consequent concentration of companies producing arable crops in the V4 countries evolve during the period 2018–2020?

- How did the profitability of companies producing arable crops in the V4 countries evolve during the period 2018–2020?

- How did the financial situation of companies producing arable crops in the V4 countries evolve during the period 2018–2020?

- What correlation can be demonstrated between farm size and its financial efficiency?

2. Literature Review

3. Materials and Methods

3.1. Data Collection and Sample Size

3.2. Analysis of Company Size and Concentration

3.3. Analysis of Financial Performance

3.4. Analysis of Financial Performance

4. Results and Discussion

4.1. The Role of Main Crop (Wheat, Barley, Maize, and Rapeseed) Production in the V4 Countries

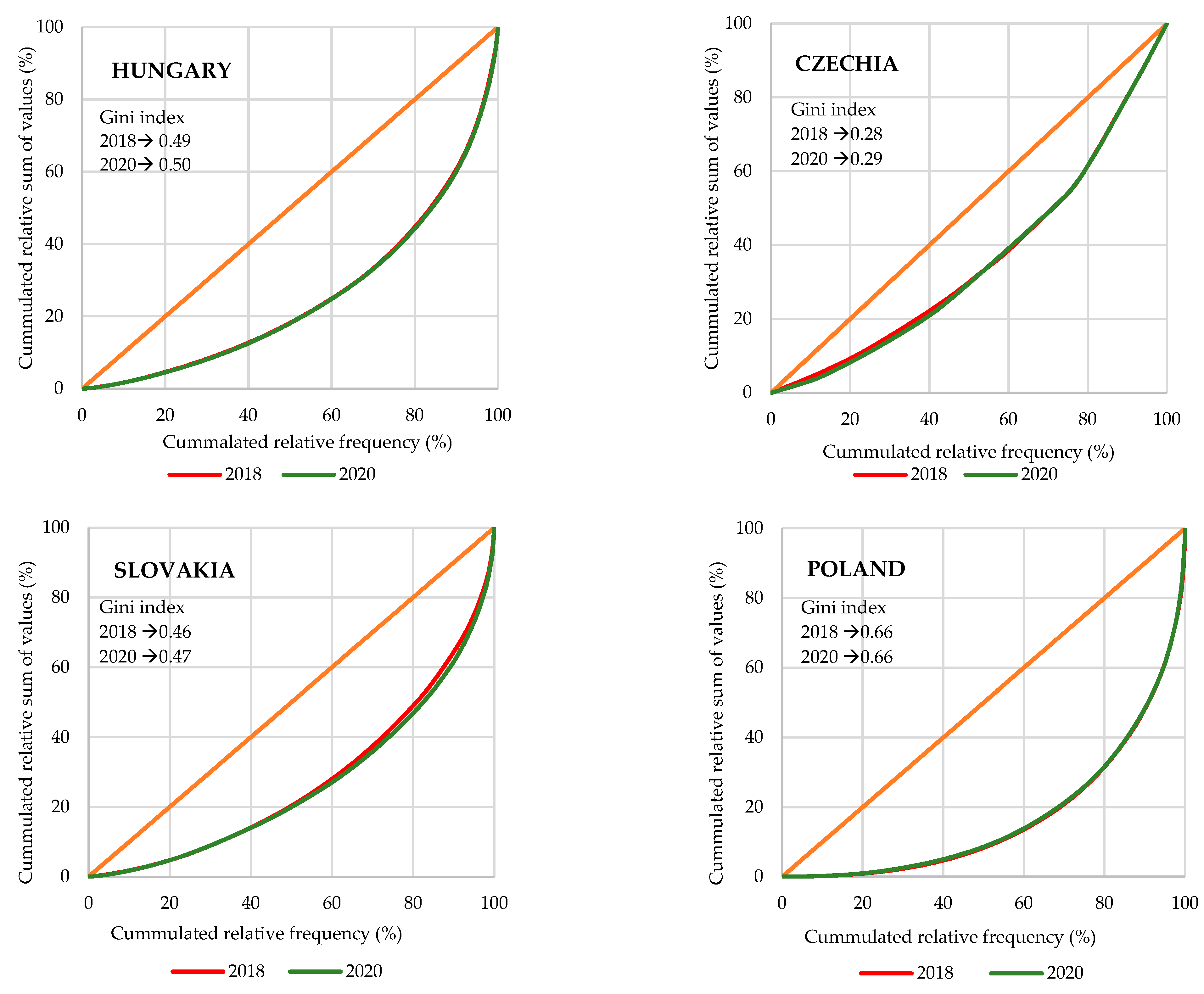

4.2. Size and Concentration of Companies Producing Arable Crops in the V4 Countries

- Micro-enterprises: net sales revenue and total assets are up to 2 million EUR.

- Small enterprises: net sales revenue or total assets are higher than 2 million EUR, but net sales revenue and total assets are maximum 10 million EUR.

- Medium enterprises: net sales revenue or total assets are higher than 10 million EUR, but net sales revenue is up to 50 million EUR and total assets is maximum 43 million EUR.

- Large enterprises: total assets exceeding 43 million EUR or net sales revenue exceeding 50 million EUR.

4.3. Income and Asset Situation of Companies Producing Arable Crops in the V4 Countries

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Data Availability Statement

Conflicts of Interest

References

- Tey, Y.S.; Brindal, M. Factors Influencing Farm Profitability. In Sustainable Agriculture Reviews; Lichtfouse, E., Ed.; Springer: Cham, Switzerland, 2015; pp. 235–255. [Google Scholar] [CrossRef]

- Hatfield, K.J.; Boote, B.A.; Kimball, L.H.; Ziska, R.C.; Izaurralde, D.; Ort, A.M.; Thomson, D. WolfeFirst. Climate Impacts on Agriculture: Implications for Crop Production. Agron. J. 2011, 103, 351–370. [Google Scholar] [CrossRef] [Green Version]

- Spiertz, H. Challenges for Crop Production Research in Improving Land Use, Productivity and Sustainability. Sustainability 2013, 5, 1632–1644. [Google Scholar] [CrossRef] [Green Version]

- Abhilash, P.C.; Tripathi, V.; Edrisi, S.A.; Dubey, R.K.; Bakshi, M.; Dubey, P.K.; Singh, H.B.; Ebbs, S.D. Sustainability of crop production from polluted lands. Energ. Ecol. Environ. 2016, 1, 54–65. [Google Scholar] [CrossRef] [Green Version]

- Gliessmann, S.R. Transforming food and agriculture systems with agroecology. Agric. Hum. Values 2020, 37, 547–548. [Google Scholar] [CrossRef] [PubMed]

- Fróna, D.; Szenderák, J.; Harangi-Rákos, M. The Challenge of Feeding the World. Sustainability 2019, 11, 5816. [Google Scholar] [CrossRef] [Green Version]

- Fróna, D.; Szenderák, J.; Harangi-Rákos, M. Economic effects of climate change on global agricultural production. Nat. Conserv. 2021, 44, 117–139. [Google Scholar] [CrossRef]

- Halecki, W.; Bedla, D. Global Wheat Production and Threats to Supply Chains in a Volatile Climate Change and Energy Crisis. Resources 2022, 11, 118. [Google Scholar] [CrossRef]

- European Commission. Common Agricultural Policy Funds; European Commission: Brussels, Belgium. Available online: https://agriculture.ec.europa.eu/common-agricultural-policy/financing-cap/cap-funds_en (accessed on 12 August 2022).

- Quiroga, S.; Suárez, C.; Fernández-Haddad, Z.; Phillipidis, G. Levelling the playing field for European Union agriculture: Does the Common Agricultural Policy impact homogeneously on farm productivity and efficiency? Land Use Policy 2017, 68, 179–188. [Google Scholar] [CrossRef]

- EUROSTAT. Farms and Farmland in the European Union—Statistics. 2022. Available online: https://ec.europa.eu/eurostat/statistics-explained/index.php?title=Farms_and_farmland_in_the_European_Union_-_statistics#Farms_in_2020 (accessed on 20 July 2023).

- FAOSTAT. Database of Food and Agricultural Organization of the United Nations. Available online: http://www.fao.org/faostat/en/#data (accessed on 16 July 2022).

- Kis, G.; Kacz, K. Analysis of Agricultural Holdings of the Visegrad Four in the Post-Accession Period. Acta Reg. Environ. 2014, 11, 36–40. [Google Scholar] [CrossRef] [Green Version]

- Fertő, I.; Bakucs, Z.; Bojnec, S.; Latruffe, L. Short communication: East-West European farm investment behaviour—The role of financial constraints and public support. Span. J. Agric. Res. 2017, 15, e01SC01. [Google Scholar] [CrossRef] [Green Version]

- Czubak, W.; Pawlowski, K.P.; Sadowski, A. Outcomes of farm investment in Central and Eastern Europe: The role of financial public support and investment scale. Land Use Policy 2021, 108, 105655. [Google Scholar] [CrossRef]

- Kocsis, J.; Major, K. A General overview of agriculture and profitability in agricultural enterprises in Central Europe. In Managing Agricultural Enterprises—Exploring Profitability and Best Practice in Central Europe; Bryła, P., Ed.; Palgrave Macmilla: Cham, Switzerland, 2018; pp. 243–246. [Google Scholar] [CrossRef]

- Szabo, L.; Grznar, M.; Zelina, M. Agricultural performance in the V4 countries and its position in the European Union. Agr. Econ. 2018, 64, 337–346. [Google Scholar] [CrossRef] [Green Version]

- Fenyves, V.; Pető, K.; Szenderák, J.; Harangi-Rákos, M. The capital structure of agricultural enterprises in the Visegrad countries. Agr. Econ. 2020, 66, 160–167. [Google Scholar] [CrossRef]

- Ladvenicová, J.; Bajuspvá, Z.; Gurcik, L.; Cerveny, D. Dupont Analysis of Farms in V4 Countries. Visegr. J. Bioecon. Sustain. Dev. 2019, 8, 82–86. [Google Scholar] [CrossRef]

- Koszorús, G.; Tarnóczi, T. Performance factors of the listed companies in the Visegrad Countries and Romania. Netw. Intell. Stud 2020, 8, 17–25. [Google Scholar]

- Galaczka, A.; Cybert, A. The efficiency of production factors on agricultural farms of the Visegrad Group. Polityki Eur. Finans. Mark. 2020, 24, 70–80. [Google Scholar]

- Langemeier, M.R.; Rodney, J.D. Measuring the impact of farm size and speacialization on financial performance. J. Am. Soc. Farm Manage. Rural. Apprais. 2000, 90, 90–96. [Google Scholar]

- Felföldi, J.; Sulyok, D.; Czakó, I.; Kovács, K. Management issues of cropping with sorghum in the production structure—A case study of Hungary. Apstract 2022, 16, 1–11. [Google Scholar] [CrossRef]

- Takácsné György, K.; Takács, I. A magyar mezőgazdaság versenyképessége a hatékonyságváltozások tükrében. Sci. J. Agric. Econ. 2016, 60, 31–50. [Google Scholar] [CrossRef]

- Szőllősi, L.; Béres, E.; Szűcs, I. Effects of modern technology on broiler chicken performance and economic indicators—A Hungarian case study. Ital. J. Anim. Sci. 2021, 20, 188–194. [Google Scholar] [CrossRef]

- Milics, G.; Matecny, I.; Magyar, F.; Varga, P.M. Data-based agriculture in the V4 countries—Sustainability, efficiency and safety. Sci. Secur. 2021, 2, 491–503. [Google Scholar] [CrossRef]

- Yousuf, A.; Kozlovskyi, S.; Mahfod, L.J.; Rauf, A.; Felfoldi, J. How does strategic flexibility make a difference for companies? An example of the Hungarian food industry. Probl. Perspect. Manag. 2022, 20, 374–386. [Google Scholar] [CrossRef]

- Yousuf, A.; Haddad, H.; Pakurár, M.; Kozlovskyi, S.; Felföldi, J. The Effect of Operational Flexibility on Performance: A Field Study on Small and Medium-sized Industrial Companies in Jordan. Montenegrin J. Econ. 2019, 15, 47–60. [Google Scholar] [CrossRef]

- Ren, C.; Liu, S.; van Grinsve, H.; Reis, S.; Shuqin, J.; Liu, H.; Gu, B. The impact of farm size on agricultural sustainability. J. Clean. Prod. 2019, 220, 357–367. [Google Scholar] [CrossRef]

- Sheng, Y.; Chancellor, W. Exploring the relationship between farm size and productivity: Evidence from the Australian grains industry. Food Policy 2019, 84, 196–204. [Google Scholar] [CrossRef]

- Wicki, L. Size vs effectiveness of agricultural farms. Ann. Pol. Assoc. Agric. Aribus. Econ. 2019, 21, 285–296. [Google Scholar] [CrossRef] [Green Version]

- Lerman, Z.; Schreinemachers, P. Individual Farming as a Labour Sink: Evidence from Poland and Russia. Comp. Econ. Stud. 2005, 47, 675–695. [Google Scholar] [CrossRef]

- Hornowski, A.; Parzonko, A.; Kotyza, P.; Kondraszuk, T.; Bórawski, P.; Smutka, L. Factors Determining the Development of Small Farms in Central and Eastern Poland. Sustainability 2020, 12, 5095. [Google Scholar] [CrossRef]

- Wieliczko, B.; Kurdys-Kujawska, A.; Sompolska-Rzechula, A. Savings of Small Farms: Their Magnitude, Determinants and Role in Sustainable Development. Example of Poland. Agriculture 2020, 10, 525. [Google Scholar] [CrossRef]

- Kocsis, J.; Major, K. Managerial Challenges in Central European Agricultural Enterprises. In Managing Agricultural Enterprises—Exploring Profitability and Best Practice in Central Europe; Bryła, P., Ed.; Palgrave Macmilla: Cham, Switzerland, 2018; pp. 267–284. [Google Scholar] [CrossRef]

- Lambert, D.; Bayda, V. The Impacts of Farm Financial Structure on Production Efficiency. J. Agric. Appl. Econ. 2005, 37, 277–289. [Google Scholar] [CrossRef] [Green Version]

- Simionov, I.A.; Mogodan, A.; Petrea, S.M.; Nica, A.; Cristea, D.S.; Rosenberg, S.; Cristea, V. Comparative Study between Romania and Visegrad Countries, Related to Agricultural Sector Performance. In Proceedings of the 36th International Business Information Management Association (IBIMA), Granada, Spain, 4–5 November 2020; pp. 8897–8952. [Google Scholar]

- EUROSTAT. Database. Available online: https://ec.europa.eu/eurostat/databrowser/view/EF_M_FARMLEG__custom_6928237/default/table?lang=en (accessed on 20 July 2023).

- Zgłobicki, W.; Karczmarczuk, K.; Baran-Zgłobicka, B. Intensity and Driving Forces of Land Abandonment in Eastern Poland. Appl. Sci. 2020, 10, 3500. [Google Scholar] [CrossRef]

- EMIS. Database of Emerging Market Information System; London. Available online: https://www.emis.com/php/dashboard/index (accessed on 14 March 2022).

- European Central Bank. Euro Foreign Exchange Reference Rates. 2023. Available online: https://www.ecb.europa.eu/stats/policy_and_exchange_rates/euro_reference_exchange_rates/html/index.en.html (accessed on 23 July 2023).

- Act XXXIV of 2004 on the Small- and Medium-Sized Enterprises and Supporting Their Development. Available online: https://net.jogtar.hu/jogszabaly?docid=a0400034.tv (accessed on 1 March 2022).

- Hunyadi, L.; Vita, L. A sokaság leírása egy ismérv szerint. In Statisztika I; Budapesti Corvinus Egyetem: Budapest, Hungary, 2008; pp. 118–120. [Google Scholar]

- Horváth, S.; Kopányi, M. Aktíva-piacok, tényezőárak, jövedelemmegoszlás. In Mikroökonómia; Koppányi, M., Ed.; KJK-Kerszöv: Budapest, Hungary, 2004; p. 433. [Google Scholar]

- Ukav, I. Market Structures and Concentration Measuring Techniques. Asian J. Agric. Ext. Econ. Soc. 2017, 19, 1–16. [Google Scholar] [CrossRef]

- Dimic, M.; Paunivic, S. Concentration Measuring Techniques in Banking Sector-Lorenz Curve and Gini Coefficient. Econ. Anal. Appl. Res. Emerg. Mark. 2019, 52, 137–151. [Google Scholar]

- Weisstein, E.W. Gini Coefficient. Available online: https://mathworld.wolfram.com (accessed on 18 July 2023).

- Hamad, M.; Tarnóczi, T. An efficiency analysis of companies operating in the pharmaceutical industry in the Visegrad Countries. Intellect. Econ. 2021, 15, 131–155. [Google Scholar] [CrossRef]

- Vavrina, J.; Lacina, L. Profitability of foodstuff processing companies in V4 countries during the 2008–2012 economic crises. Soc. Econ. 2018, 40, 245–270. [Google Scholar] [CrossRef]

- Pille, P.; Paradi, J.C. Financial performance analysis of Ontario (Canada) Credit Unions: An application of DEA in the regulatory environment. Eur. J. Oper. Res. 2002, 139, 339–350. [Google Scholar] [CrossRef]

- Glushchenko, A.V.; Slozhenkina, M.I.; Samedova, E.N.; Mosolova, D.A. Financial risks of sustainable development of small agricultural enterprises assessed to ensure national food security. IOP Conf. Ser. Earth Environ. Sci. 2020, 548, 082061. [Google Scholar] [CrossRef]

- Molnár, S.; Szőllősi, L. Economic issues of duck production: A case study from Hungary. Apstract 2017, 11, 61–67. [Google Scholar] [CrossRef]

- European Commission. EU Agricultural Outlook for Markets, Income and Environment, 2021–2031; European Commission, DG Agriculture and Rural Developments: Brussels, Belgium, 2022. [Google Scholar] [CrossRef]

- Peltonen-Sainio, P.; Jauhiainen, L.; Trnka, M.; Olesen, J.E.; Calanca, P.; Eckersten, H.; Eitzinger, J.; Gobin, A.; Kersebaum, K.C.; Kozyra, J.; et al. Coincidence of variation in yield and climate in Europe. Agric. Ecosyst. Environ. 2010, 139, 483–489. [Google Scholar] [CrossRef]

- Némethová, J.; Svobodová, H.; Vežník, A. Changes in Spatial Distribution of Arable Land, Crop Production and Yield of Selected Crops in the EU Countries after 2004. Agriculture 2022, 12, 1697. [Google Scholar] [CrossRef]

- Střeleček, F.; Losová, J.; Zdenek, R. Comparison of subsidies in the Visegrad Group after the EU accession. Agr. Econ. 2009, 9, 415–423. [Google Scholar] [CrossRef] [Green Version]

- Liliane, T.N.; Charles, M.S. Factors affecting yield of crops. In Agronomy: Climate Change and Food Security; Amanullah, S.K., Ed.; IntechOpen: London, UK, 2020; pp. 9–24. [Google Scholar] [CrossRef]

- Rudinskaya, T.; Náglová, Z. Analysis of Consumption of Nitrogen Fertilisers and Environmental Efficiency in Crop Production of EU Countries. Sustainability 2021, 13, 8720. [Google Scholar] [CrossRef]

- Losová, J.; Zdenek, R. Key Factors Affecting the Profitability of Farms in the Czech Republic. Agris-Line Pap. Econ. Inform. 2014, 6, 21–36. [Google Scholar] [CrossRef]

- Vavrina, J.; Ruzicková, K.; Martinovicová, D. The CAP reform beyond 2023: The economic performance of agricultural enterprises within the Visegrad Group. Acta Univ. Agric. Silvic. Mendel. Brun. 2012, 60, 451–462. [Google Scholar] [CrossRef] [Green Version]

- Akimowicz, M.; Magrini, M.-B.; Ridier, A.; Bergez, J.-E.; Requier-Desjardins, D. What Influences Farm Size Growth? An Illustration in Southwestern France. Appl. Econ. Perspect. Policy 2013, 35, 242–269. [Google Scholar] [CrossRef]

- Clapp, J. The problem with growing corporate concentration and power in the global food system. Nat. Food 2021, 2, 404–408. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Indicators | Hungary | Czechia | Slovakia | Poland |

|---|---|---|---|---|

| Contribution of agriculture to GDP (%) | 2.5 | 0.9 | 0.7 | 2.0 |

| Gross value added of agriculture (at basic prices, million EUR) | 3420 | 1935 | 642 | 10,306 |

| Value of agricultural output (at basic prices, million EUR) | 8398 | 5633 | 2348 | 26,406 |

| Value of crop output (at basic prices, million EUR) | 4939 | 3303 | 1289 | 12,925 |

| Share of crop production (%) | 58.8 | 58.6 | 54.9 | 48.9 |

| Indicators | Hungary | Czechia | Slovakia | Poland |

|---|---|---|---|---|

| Farm type: total | ||||

| Farm number (legal form: legal person/company) | 8690 | 4260 | 3610 | 7370 |

| Share from total farms (%) | 3.7 | 14.9 | 18.4 | 0.6 |

| Utilized agricultural area by companies (ha) | 2,450,390 | 1,908,710 | 1,518,430 | 1,280,170 |

| Share from total utilized agricultural area (%) | 70.2 | 38.8 | 81.5 | 8.7 |

| Average farm size of companies (ha/farm) | 220 | 575 | 421 | 174 |

| Farm type: Specialist cereals, oilseed, and protein crops (calculated with Standard Output) | ||||

| Farm number (legal form: legal person/company) | 3490 | 890 | 1160 | 2400 |

| Share from total farms (%) | 1.5 | 3.1 | 5.9 | 0.2 |

| Utilized agricultural area by companies (ha) | 1,023,250 | 521,270 | 162,450 | 537,670 |

| Share from total utilized agricultural area (%) | 20.8 | 14.9 | 33.2 | 3.6 |

| Average farm size of companies (ha/farm) | 293 | 586 | 532 | 224 |

| Farm type: General field cropping (calculated with Standard Output) | ||||

| Farm number (legal form: legal person/company) | 1150 | 660 | 640 | 3010 |

| Share from total farms (%) | 0.5 | 2.3 | 3.3 | 0.2 |

| Utilized agricultural area by companies (ha) | 196,760 | 207,470 | 83,430 | 311,430 |

| Share from total utilized agricultural area (%) | 4.0 | 5.9 | 3.3 | 2.1 |

| Average farm size of companies (ha/farm) | 171 | 314 | 130 | 103 |

| Farm type: Mixed cropping (calculated with Standard Output) | ||||

| Farm number (legal form: legal person/company) | 480 | 60 | 40 | 150 |

| Share from total farms (%) | 0.2 | 0.2 | 0.2 | 0.0 |

| Utilized agricultural area by companies (ha) | 67,540 | 39,470 | 22,150 | 12,550 |

| Share from total utilized agricultural area (%) | 1.4 | 1.1 | 1.2 | 0.1 |

| Average farm size of companies (ha/farm) | 141 | 658 | 554 | 84 |

| Crops (million ha) | 2018–2020 Average | 2021 | 2026 * | 2031 * |

|---|---|---|---|---|

| Common wheat | 21.4 | 21.7 | 21.3 | 21.1 |

| Barley | 11.2 | 10.4 | 10.5 | 10.1 |

| Maize | 8.7 | 9.1 | 8.8 | 8.9 |

| Rapeseed | 5.5 | 5.3 | 5.6 | 5.1 |

| Total arable area | 99.5 | 98.8 | 98.5 | 98.1 |

| ROS (%) | Hungary | Czechia | Slovakia | Poland | ||||

|---|---|---|---|---|---|---|---|---|

| Number of Companies (pc) | Distribution (%) | Number of Companies (pc) | Distribution (%) | Number of Companies (pc) | Distribution (%) | Number of Companies (pc) | Distribution (%) | |

| <0 | 74 | 9.00 | 2 | 11.76 | 48 | 21.24 | 245 | 25.34 |

| 0–4.9 | 239 | 29.08 | 5 | 29.41 | 98 | 43.36 | 101 | 10.44 |

| 5–9.9 | 225 | 27.37 | 4 | 23.53 | 41 | 18.14 | 102 | 10.55 |

| 10–14.9 | 125 | 15.21 | 4 | 23.53 | 23 | 10.18 | 100 | 10.34 |

| 15–19.9 | 79 | 9.61 | 1 | 5.88 | 9 | 3.98 | 71 | 7.34 |

| >20 | 80 | 9.73 | 1 | 5.88 | 7 | 3.10 | 348 | 35.99 |

| Total | 822 | 100.00 | 17 | 100.00 | 226 | 100.00 | 967 | 100.00 |

| Weighted mean | 7.73 | 6.35 | 4.56 | 9.54 | ||||

| Relative standard deviation (%) | 100 | 160 | 145 | 479 | ||||

| Median | 6.76 | 5.36 | 3.40 | 11.82 | ||||

| ROA (%) | Hungary | Czechia | Slovakia | Poland | ||||

|---|---|---|---|---|---|---|---|---|

| Number of Companies (pc) | Distribution (%) | Number of Companies (pc) | Distribution (%) | Number of Companies (pc) | Distribution (%) | Number of Companies (pc) | Distribution (%) | |

| <0 | 68 | 8.27 | 2 | 11.76 | 46 | 20.35 | 212 | 21.92 |

| 0–4.9 | 339 | 41.24 | 8 | 47.06 | 129 | 57.08 | 342 | 35.37 |

| 5–9.9 | 251 | 30.54 | 6 | 35.29 | 33 | 14.60 | 200 | 20.68 |

| 10–14.9 | 103 | 12.53 | 1 | 5.88 | 15 | 6.64 | 90 | 9.31 |

| 15–19.9 | 29 | 3.53 | 0 | 0.00 | 3 | 1.33 | 45 | 4.65 |

| >20 | 32 | 3.89 | 0 | 0.00 | 0 | 0.00 | 78 | 8.07 |

| Total | 822 | 100.00 | 17 | 100.00 | 226 | 100.00 | 967 | 100.00 |

| Weighted mean | 5.24 | 3.84 | 2.75 | 3.52 | ||||

| Relative standard deviation (%) | 97 | 177 | 143 | 182 | ||||

| Median | 5.09 | 3.33 | 2.21 | 3.91 | ||||

| Equity to Total Asset Ratio (%) | Hungary | Czechia | Slovakia | Poland | ||||

|---|---|---|---|---|---|---|---|---|

| Number of Companies (pc) | Distribution (%) | Number of Companies (pc) | Distribution (%) | Number of Companies (pc) | Distribution (%) | Number of Companies (pc) | Distribution (%) | |

| 0–29.9 | 39 | 4.74 | 2 | 11.76 | 59 | 26.11 | 235 | 24.30 |

| 30–49.9 | 93 | 11.31 | 4 | 23.53 | 60 | 26.55 | 130 | 13.44 |

| 50–69.9 | 192 | 23.36 | 5 | 29.41 | 48 | 21.24 | 168 | 17.37 |

| >70 | 498 | 60.58 | 6 | 35.29 | 59 | 26.11 | 434 | 44.88 |

| Total | 822 | 100.00 | 17 | 100.00 | 226 | 100.00 | 967 | 100.00 |

| Weighted mean | 72.11 | 62.91 | 47.12 | 57.15 | ||||

| Relative standard deviation (%) | 28 | 30 | 57 | 71 | ||||

| Median | 75.30 | 63.65 | 48.66 | 65.05 | ||||

| Country | Variable 1 | Variable 2 | Correlation Coefficient (r) (Spearman) | p-Value |

|---|---|---|---|---|

| Hungary (n = 2466) | ROS | Net sales revenue | −0.014 | 0.491 |

| ROS | Total assets | 0.105 | 0.000 | |

| ROA | Net sales revenue | 0.021 | 0.290 | |

| ROA | Total assets | −0.085 | 0.000 | |

| Czechia (n = 51) | ROS | Net sales revenue | 0.014 | 0.921 |

| ROS | Total assets | 0.346 | 0.013 | |

| ROA | Net sales revenue | −0.002 | 0.991 | |

| ROA | Total assets | 0.204 | 0.152 | |

| Slovakia (n = 678) | ROS | Net sales revenue | −0.021 | 0.596 |

| ROS | Total assets | −0.014 | 0.729 | |

| ROA | Net sales revenue | −0.026 | 0.520 | |

| ROA | Total assets | −0.012 | 0.763 | |

| Poland (n = 2901) | ROS | Net sales revenue | −0.016 | 0.395 |

| ROS | Total assets | 0.000 | 0.981 | |

| ROA | Net sales revenue | 0.212 | 0.000 | |

| ROA | Total assets | −0.082 | 0.000 |

| Country | Dependent Variable (Y) | Independent Variable (X) | Correlation Coefficient (r) (Spearman) | p-Value | Linear Regression Model (Y = β0 + βX) | Coefficient of Determination (R2) | p-Value |

|---|---|---|---|---|---|---|---|

| Hungary (n = 2466) | EBIT | Net sales revenue | 0.464 | 0.000 | Y = 0.048 + 0.058X | 0.265 | 0.000 |

| EBIT | Total assets | 0.477 | 0.000 | Y = 0.048 + 0.039X | 0.256 | 0.000 | |

| Czechia (n = 51) | EBIT | Net sales revenue | 0.292 | 0.038 | Y = −0.075 + 0.111X | 0.177 | 0.002 |

| EBIT | Total assets | 0.552 | 0.000 | Y = −0.094 + 0.074X | 0.354 | 0.000 | |

| Slovakia (n = 678) | EBIT | Net sales revenue | 0.402 | 0.000 | Y = −0.028 + 0.055X | 0.253 | 0.000 |

| EBIT | Total assets | 0.418 | 0.000 | Y = 0.032 + 0.021X | 0.229 | 0.000 | |

| Poland (n = 2901) | EBIT | Net sales revenue | 0.546 | 0.000 | Y = 0.003 + 0.096X | 0.605 | 0.000 |

| EBIT | Total assets | 0.401 | 0.000 | Y = −0.044 + 0.054X | 0.535 | 0.000 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Szőllősi, L.; Erdős, A.D. Income and Asset Situation of Companies Producing Arable Crops in the Visegrad Countries. Agriculture 2023, 13, 1589. https://doi.org/10.3390/agriculture13081589

Szőllősi L, Erdős AD. Income and Asset Situation of Companies Producing Arable Crops in the Visegrad Countries. Agriculture. 2023; 13(8):1589. https://doi.org/10.3390/agriculture13081589

Chicago/Turabian StyleSzőllősi, László, and Adél Dorottya Erdős. 2023. "Income and Asset Situation of Companies Producing Arable Crops in the Visegrad Countries" Agriculture 13, no. 8: 1589. https://doi.org/10.3390/agriculture13081589