An Improved SPEA2 Algorithm with Local Search for Multi-Objective Investment Decision-Making

Abstract

:1. Introduction

2. Methodology

- (1)

- For all sub targets, A is not worse than B, that is .

- (2)

- There is at least one sub goal that makes A better than B, which is , .

2.1. The Basic Theory of SPEA2

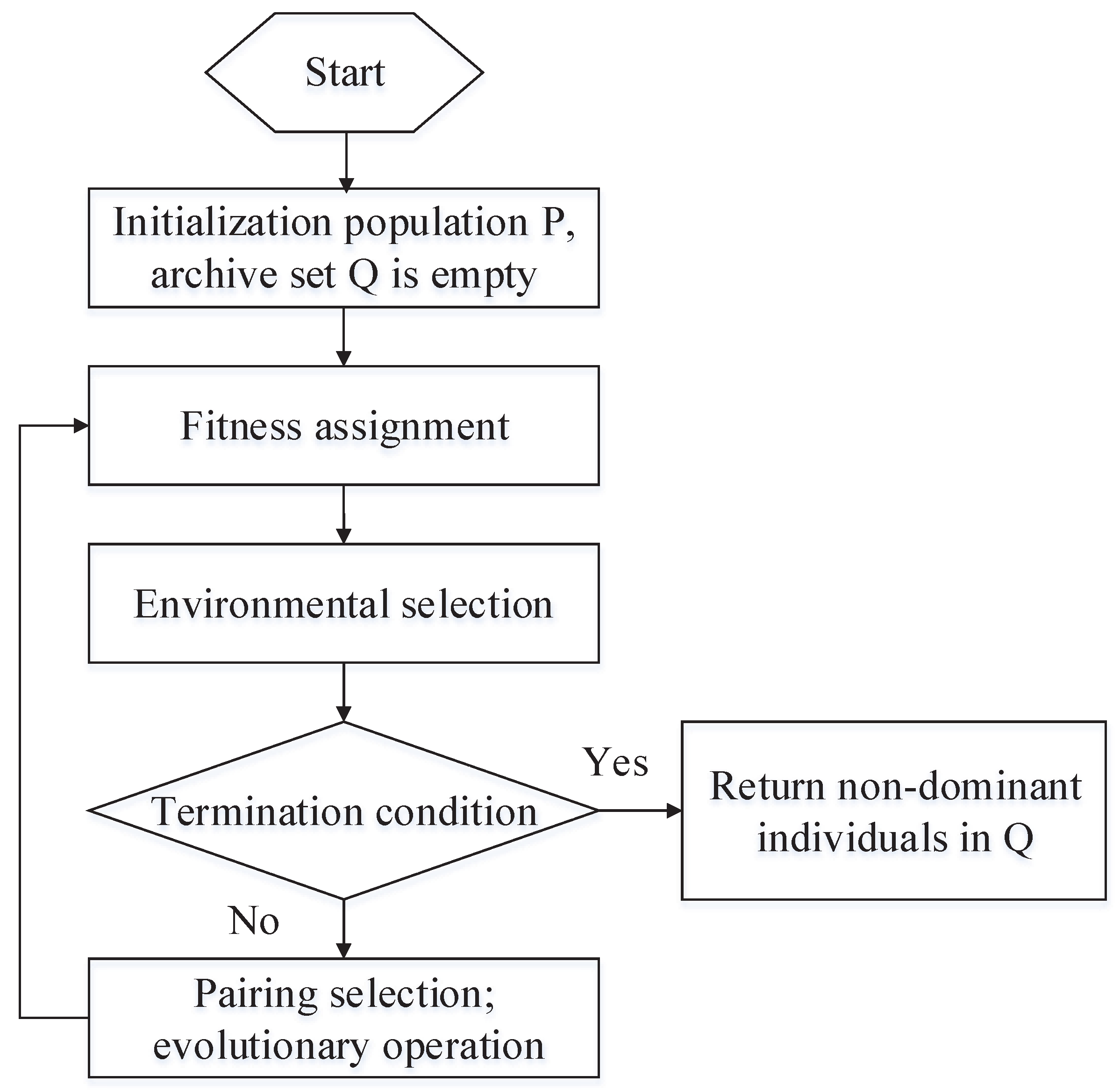

2.2. Improved SPEA2

2.2.1. Local Search Strategy

2.2.2. Crossover Operator

2.2.3. Individual Updating Strategy

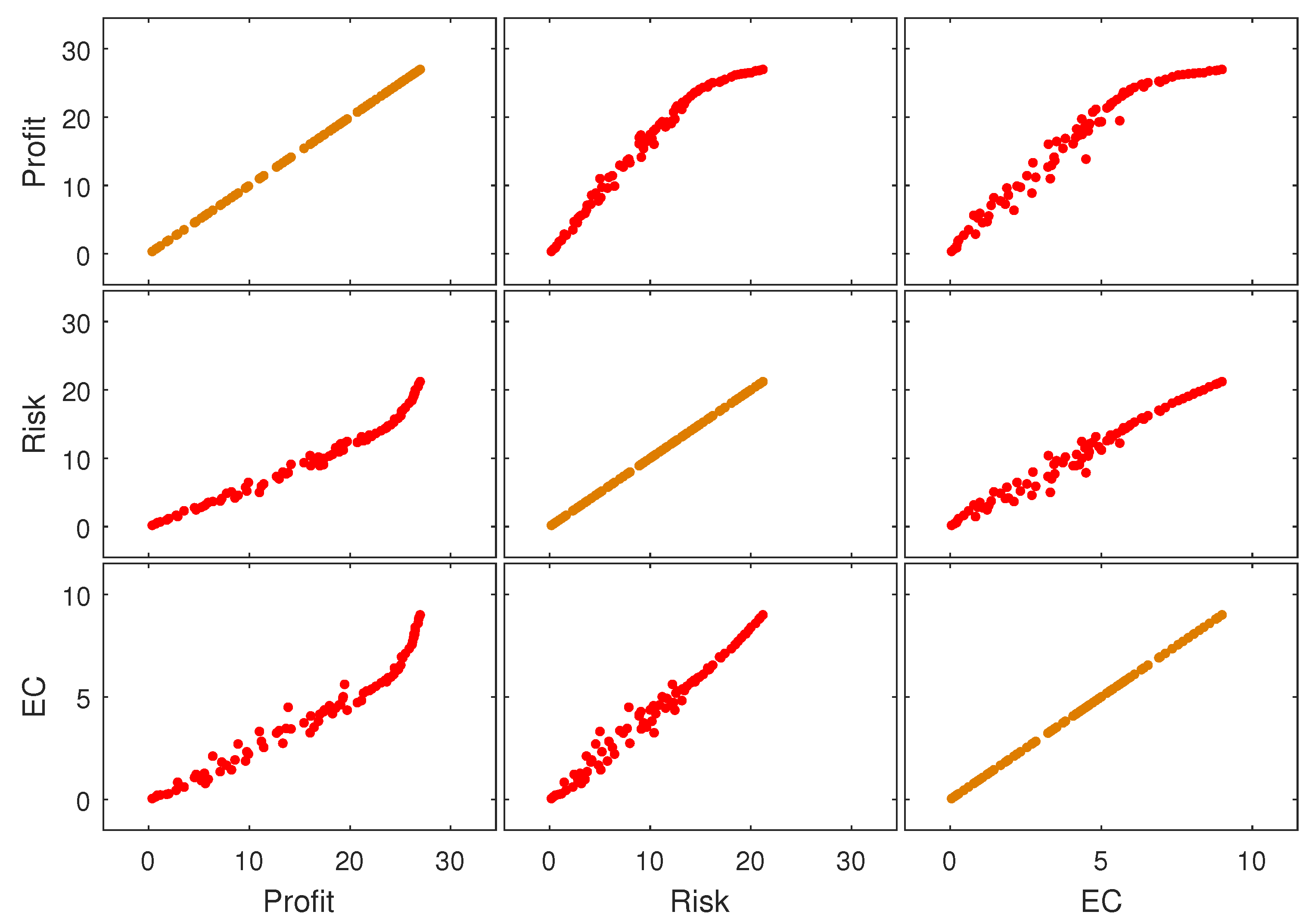

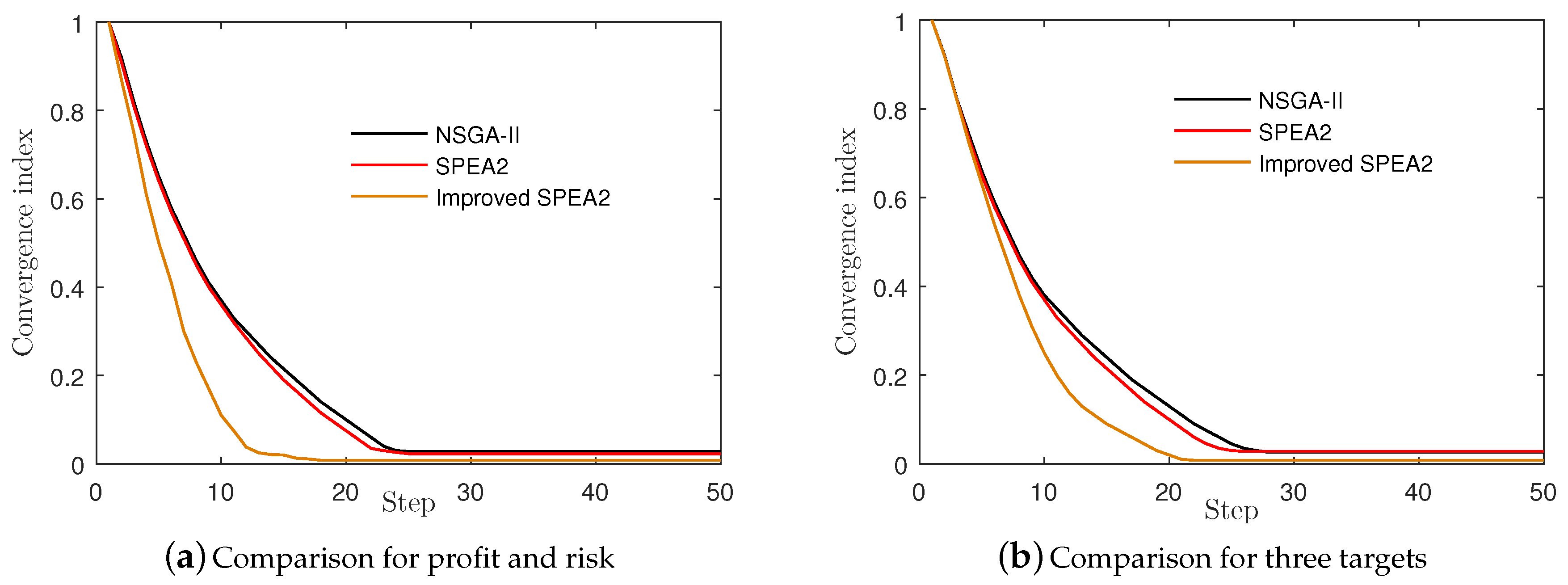

2.3. Evaluation Criteria

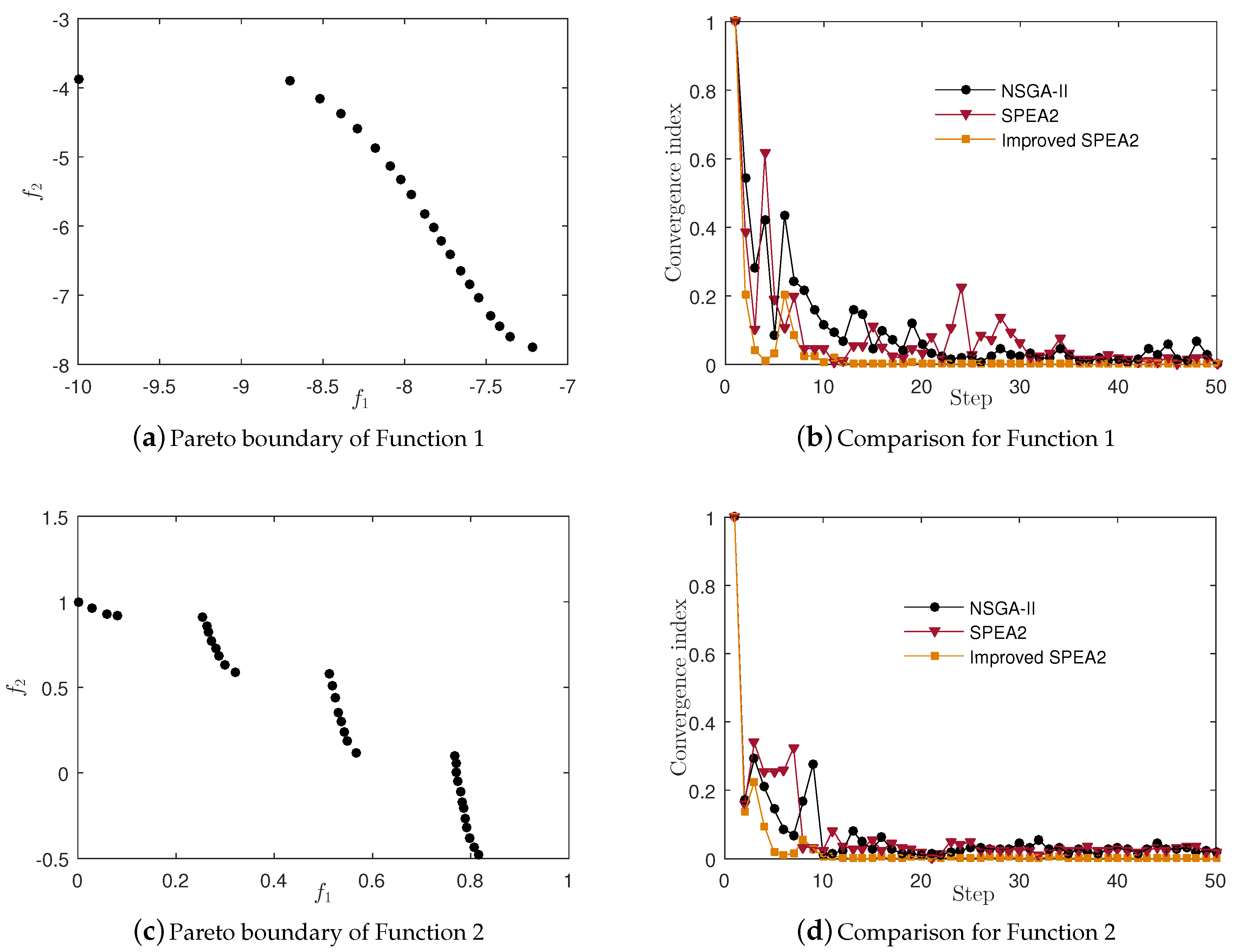

2.4. Validity Test

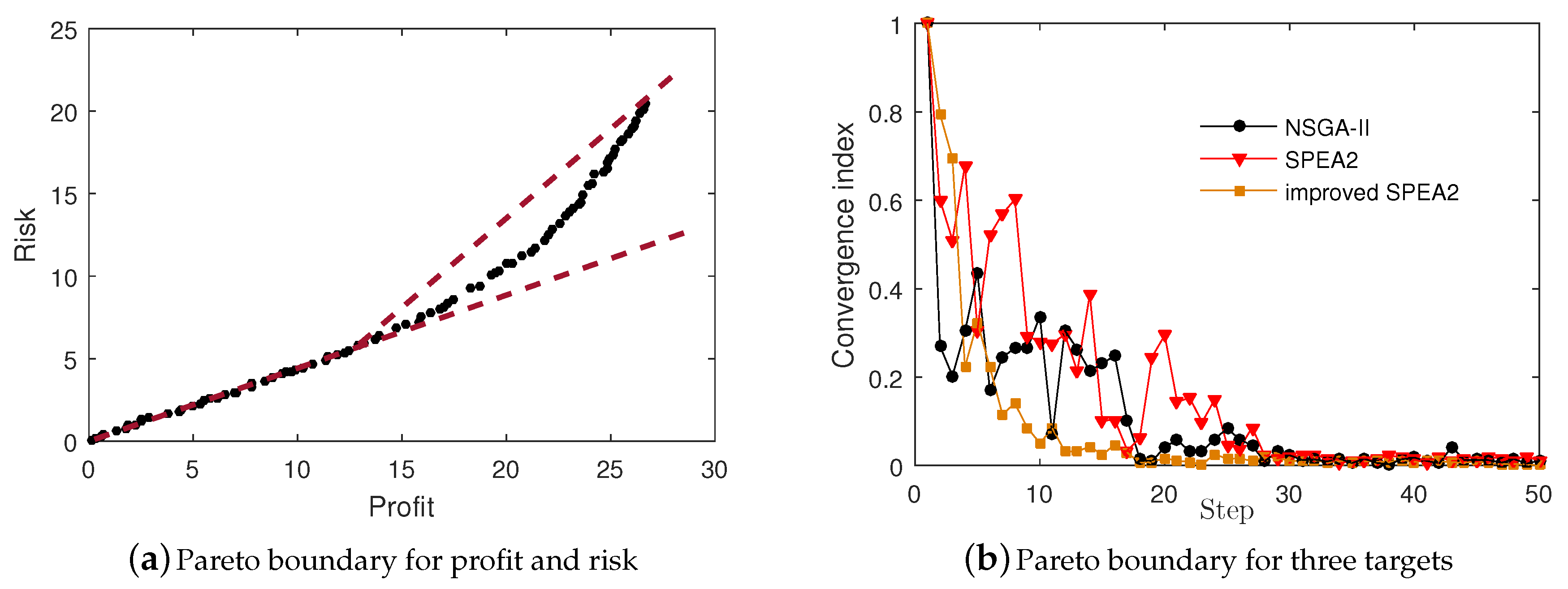

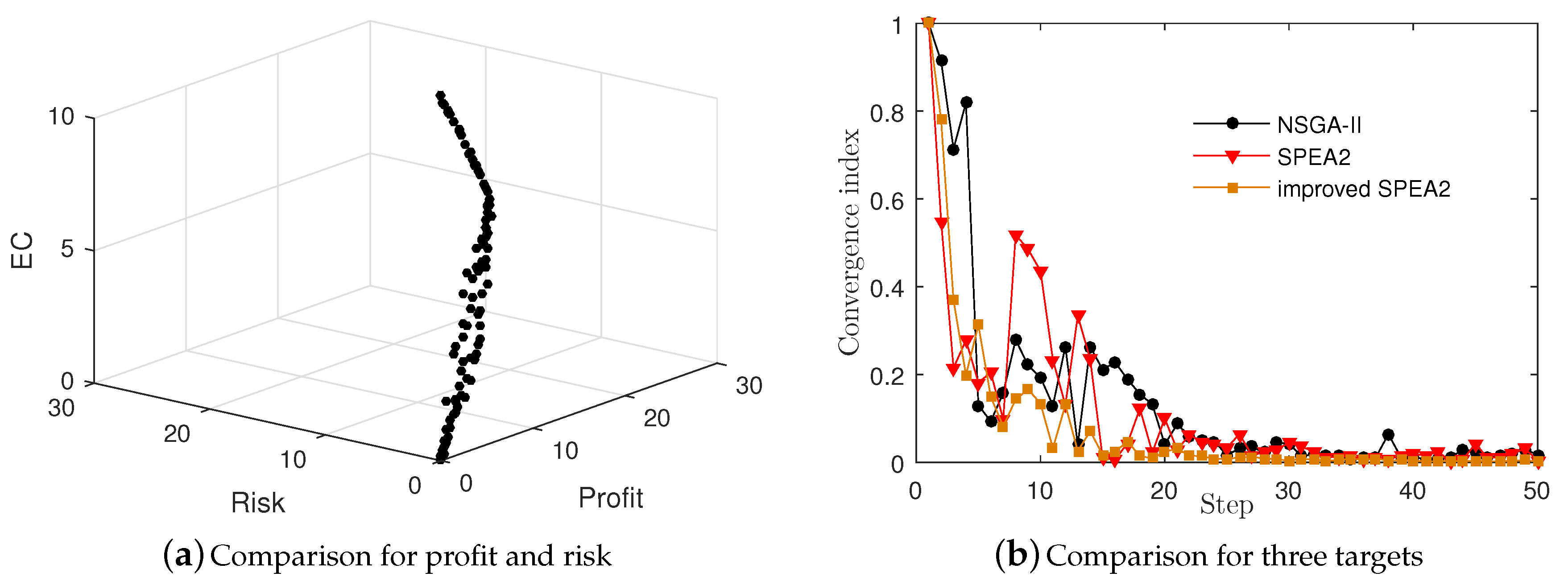

3. Multi-Objective Decision-Making in Enterprise Investment

4. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Bruno, S.; Ahmed, S.; Shapiro, A.; Street, A. Risk neutral and risk averse approaches to multistage renewable investment planning under uncertainty. Eur. J. Oper. Res. 2016, 250, 979–989. [Google Scholar] [CrossRef]

- Ye, S.; Tiong, R.L.K. NPV-at-Risk Method in Infrastructure Project Investment Evaluation. J. Constr. Eng. Manag. 2000, 126, 227–233. [Google Scholar] [CrossRef]

- Byung-cheol, K.; Euysup, S.; Kenneth, F.R. Probability Distribution of the Project Payback Period Using the Equivalent Cash Flow Decomposition. Eng. Econ. 2013, 58, 112–136. [Google Scholar]

- Soderbaum, P. Benefit-Cost Analysis. A Political Economy Approach. J. Econ. 2016, 25, 261–263. [Google Scholar] [CrossRef]

- Asta, S.; Karapetyan, D.; Kheiri, A.; Özcan, E.; Parkes, A.J. Combining Monte-Carlo and Hyper-heuristic methods for the Multi-mode Resource-constrained Multi-project Scheduling Problem. Inf. Sci. 2016, 373, 476–498. [Google Scholar] [CrossRef]

- Xia, Y.; Liu, C.; Li, Y.Y.; Liu, N. A boosted decision tree approach using Bayesian hyper-parameter optimization for credit scoring. Expert Sys. Appl. 2017, 78, 225–241. [Google Scholar] [CrossRef]

- Furini, F.; Ljubic, I.; Sinnl, M. An effective dynamic programming algorithm for the minimum-cost maximal knapsack packing problem. Eur. J. Oper. Res. 2017, 262, 438–448. [Google Scholar] [CrossRef]

- Polychronopoulos, G.H.; Tsitsiklis, J.N. Stochastic shortest path problems with recourse. Networks 2015, 27, 133–143. [Google Scholar] [CrossRef]

- Facundo, B.; Caroline, P.C.C.; Pablo, M.; Eduardo, G. An Auto-Adaptive Multi-Objective Strategy for Multi-Robot Exploration of Constrained-Communication Environments. Appl. Sci. 2019, 9, 573. [Google Scholar]

- Smith, M.; Taffler, R. The incremental effect of narrative accounting information in corporate annual reports. J. Bus. Financ. Account. 2010, 22, 1195–1210. [Google Scholar] [CrossRef]

- Sharif, A.; Qin, R. Valuation of Lease Contracts with a Price Adjustment Option: An Application to the Maritime Transport Industry. Eng. Econ. 2014, 59, 30–54. [Google Scholar] [CrossRef]

- Kramer, D.B.; Zhang, T.; Cheruvelil, K.S.; Ligmann-Zielinska, A.; Soranno, P.A. A Multi-objective, Return on Investment Analysis for Freshwater Conservation Planning. Ecosystems 2014, 16, 823–837. [Google Scholar] [CrossRef]

- Peng, X.; Wang, W. Optimal investment and risk control for an insurer under inside information. Insur. Math. Econ. 2016, 69, 104–116. [Google Scholar] [CrossRef]

- Xiao, X.W.; Xiao, D.; Lin, J.G.; Xiao, Y.F. Overview on multi-objective optimization problem research. Appl. Res. Comput. 2011, 3, 001. [Google Scholar]

- Stevic, Z.; Pamucar, D.; Zavadskas, E.K.; Cirovic, G.; Prentkovskis, O. The selection of wagons for the internal transport of a logistics company: A novel approach based on rough BWM and rough SAW methods. Symmetry 2017, 9, 264. [Google Scholar] [CrossRef]

- Badi, I.; Ballem, M. Supplier Selection using rough BWM-MAIRCA model: A case study in pharmaceutical supplying in Libya. Decis. Mak. Appl. Manag. Eng. 2018, 1, 15–32. [Google Scholar] [CrossRef]

- Pamucar, D.; Stevic, Z.; Sremac, S. A New Model for Determining Weight Coefficients of Criteria in MCDM Models: Full Consistency Method (FUCOM). Symmetry 2018, 10, 393. [Google Scholar] [CrossRef]

- Nunic, Z. Manufacturer using the FUCOM-MABAC model. Oper. Res. Eng. Sci. Theor. Appl. 2018, 1, 13–28. [Google Scholar] [CrossRef]

- Bozanic, D.; Tesic, D.; Kocic, J. Multi-criteria FUCOM-Fuzzy MABAC model for the selection of location for construction of single-span bailey bridge. Decis. Mak. Appl. Manag. Eng. 2019, 2, 132–146. [Google Scholar] [CrossRef]

- Pamucar, D.; Lukovac, V.; Bozanic, D.; Komazec, N. Multi-criteria FUCOM-MAIRCA model for the evaluation of level crossings: case study in the Republic of Serbia. Oper. Res. Eng. Sci. Theor. Appl. 2018, 1, 108–129. [Google Scholar] [CrossRef]

- Xia, M.; Liu, W.; Wang, K.; Zhang, X.; Xu, Y. Non-intrusive load disaggregation based on deep dilated residual network. Electr. Power Syst. Res. 2019, 170, 277–285. [Google Scholar] [CrossRef]

- Xia, M.; Liu, W.; Shi, B.; Weng, L.; Liu, J. Cloud/snow recognition for multispectral satellite imagery based on a multidimensional deep residual network. Int. J. Remote Sens. 2019, 40, 156–170. [Google Scholar] [CrossRef]

- Gang, Z.; Zhixuan, L.; Jinwang, H.; Kaoshe, Z.; Fuchao, L.; Xin, Z. Multi-Objective Interval Prediction of Load Based on the Conditional Copula Function. Appl. Sci. 2019, 9, 955. [Google Scholar]

- Sadeghi, J.; Sadeghi, S.; Niaki, S.T.A. A hybrid vendor managed inventory and redundancy allocation optimization problem in supply chain management: An NSGA-II with tuned parameters. Comput. Oper. Res. 2014, 41, 53–64. [Google Scholar] [CrossRef]

- Ding, S.; Chen, C.; Xin, B.; Pardalos, P.M. A bi-objective load balancing model in a distributed simulation system using NSGA-II and MOPSO approaches. Appl. Soft Comput. 2018, 63, 249–267. [Google Scholar] [CrossRef]

- Deb, K.; Amrit, P.; Sameer, A.; Meyarivan, T.A. A fast and elitist multiobjective genetic algorithm: NSGA-II. IEEE Trans. Evol. Comput. 2002, 6, 182–197. [Google Scholar] [CrossRef]

- Salgueiro, Y.; Toro, J.L.; Bello, R.; Falcon, R. Multiobjective variable mesh optimization. Ann. Oper. Res. 2016, 258, 1–25. [Google Scholar] [CrossRef]

- Gong, M.; Jiao, L.; Du, H.; Bo, L. Multiobjective immune algorithm with nondominated neighbor-based selection. Evol. Comput. 2014, 16, 225–255. [Google Scholar] [CrossRef]

- Liefoogheabaac, A. A software framework based on a conceptual unified model for evolutionary multiobjective optimization: ParadisEO-MOEO. Eur. J. Oper. Res. 2011, 209, 104–112. [Google Scholar] [CrossRef]

- Zhao, F.; Lei, W.; Ma, W.; Liu, Y.; Zhang, C. An Improved SPEA2 Algorithm with Adaptive Selection of Evolutionary Operators Scheme for Multiobjective Optimization Problems. Math. Probl. Eng. 2016, 2016, 8010346. [Google Scholar] [CrossRef]

- Knowles, J.D.; Corne, D.W. Approximating the Nondominated Front Using the Pareto Archived Evolution Strategy. Evol. Comput. 2014, 8, 149–172. [Google Scholar] [CrossRef]

- Aguirre, A.H.; Rionda, S.B.; Coello, C.A.C.; Lizárraga, G.L.; Montes, E.M. Handling constraints using multiobjective optimization concepts. Int. J. Numer. Meth. Eng. 2010, 59, 1989–2017. [Google Scholar] [CrossRef]

- Yi, J.; Huang, D.; Fu, S.; He, H.; Li, T. Multi-Objective Bacterial Foraging Optimization Algorithm Based on Parallel Cell Entropy for Aluminum Electrolysis Production Process. IEEE Trans. Ind. Electron. 2016, 63, 2488–2500. [Google Scholar] [CrossRef]

- Yu, X.; Yu, X.; Lu, Y. Evaluating Multiobjective Evolutionary Algorithms Using MCDM Methods. Math. Probl. Eng. 2018, 2018, 1–13. [Google Scholar] [CrossRef]

- Muhammad, U.F.; Qazi, S.; Muhammad, A.; Imran, K.; Rehman, A.; Sunghwan, K. An Artificial Bee Colony Algorithm Based on a Multi-Objective Framework for Supplier Integration. Appl. Sci. 2019, 9, 588. [Google Scholar]

- Zhang, G.; Li, Z.; Hou, J.; Zhang, K.; Liu, F.; Zhang, X. Research on Combined Model Based on Multi-Objective Optimization and Application in Wind Speed Forecast. Appl. Sci. 2019, 9, 423. [Google Scholar] [CrossRef]

- Capitanescu, F.; Marvuglia, A.; Benetto, E.; Ahmadi, A.; Tiruta-Barna, L. Linear programming-based directed local search for expensive multi-objective optimization problems: application to drinking water production plants. Eur. J. Oper. Res. 2017, 262, 322–334. [Google Scholar] [CrossRef]

- Lejeune, M.A.; Shen, S. Multi-objective probabilistically constrained programs with variable risk: Models for multi-portfolio financial optimization. Eur. J. Oper. Res. 2016, 252, 522–539. [Google Scholar] [CrossRef]

- Basseur, M.; Burke, E.K. Indicator-based multi-objective local search. Neural Comput. Appl. 2012, 21, 1917–1929. [Google Scholar] [CrossRef]

- Sindhya, K.; Deb, K.; Miettinen, K. Improving convergence of evolutionary multi-objective optimization with local search: A concurrent-hybrid algorithm. Nat. Comput. 2011, 10, 1407–1430. [Google Scholar] [CrossRef]

- Bhuvana, J.; Aravindan, C. Memetic algorithm with Preferential Local Search using adaptive weights for multi-objective optimization problems. Soft Comput. 2016, 20, 1365–1388. [Google Scholar] [CrossRef]

- Xia, M.; Zhang, C.; Weng, L.; Liu, L.; Wang, Y. Robot path planning based on multi-objective optimization with local search. J. Intell. Fuzzy Sys. 2018, 35, 1755–1764. [Google Scholar] [CrossRef]

- Michalewicz, Z.; Deb, K.; Schmidt, M.; Stidsen, T. Test-case generator for nonlinear continuous parameter optimization techniques. IEEE Trans. Evol. Comput. 2000, 4, 197–215. [Google Scholar] [CrossRef]

- Henri, J.F.; Boiral, O.; Roy, M.J. Strategic cost management and performance: The case of environmental costs. Br. Account. Rev. 2016, 48, 269–282. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Year | Projects | |||||

|---|---|---|---|---|---|---|

| 1 | 2 | ⋯ | j | ⋯ | m | |

| 1 | ⋯ | ⋯ | ||||

| 2 | ⋯ | ⋯ | ||||

| ⋮ | ⋮ | ⋮ | ⋮ | ⋮ | ⋮ | ⋮ |

| i | ⋯ | ⋯ | ||||

| ⋮ | ⋮ | ⋮ | ⋮ | ⋮ | ⋮ | ⋮ |

| n | ⋯ | ⋯ | ||||

| Risk | ⋯ | ⋯ | ||||

| EC | ⋯ | ⋯ | ||||

| Year | A | B | C | D |

|---|---|---|---|---|

| 1 | 12.5 | 17.5 | ||

| 2 | 0 | 15 | ||

| 3 | 16.25 | 10 |

| Year | A | B | C | D |

|---|---|---|---|---|

| 1 | 16.52 | 13.47 | ||

| 2 | 7.27 | 11.89 | ||

| 3 | 19.66 | 3.33 |

| Year | A | B | C | D |

|---|---|---|---|---|

| 1 | 9.34 | 9.57 | ||

| 2 | 2.98 | 5.22 | ||

| 3 | 13.26 | 0.559 |

| Year | A | B | C | D |

|---|---|---|---|---|

| 1 | 13.60 | 2.41 | ||

| 2 | 3.17 | 8.45 | ||

| 3 | 18.10 | 0.148 |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Liu, X.; Zhang, D. An Improved SPEA2 Algorithm with Local Search for Multi-Objective Investment Decision-Making. Appl. Sci. 2019, 9, 1675. https://doi.org/10.3390/app9081675

Liu X, Zhang D. An Improved SPEA2 Algorithm with Local Search for Multi-Objective Investment Decision-Making. Applied Sciences. 2019; 9(8):1675. https://doi.org/10.3390/app9081675

Chicago/Turabian StyleLiu, Xi, and Dan Zhang. 2019. "An Improved SPEA2 Algorithm with Local Search for Multi-Objective Investment Decision-Making" Applied Sciences 9, no. 8: 1675. https://doi.org/10.3390/app9081675