1. Introduction

The literature on prioritizing rental housing supply in housing policy continues to be published worldwide [

1,

2,

3]. The argument is that more rental units are needed to serve mid-to-low-income households. In Australia, build-to-rent (BTR) has become an essential tenure due to rapid demographic changes, overpriced homeownership, and affordable rental housing supply gaps [

4,

5,

6,

7]. The BTR industry is attracting significant foreign institutional capital as investors continue to explore alternative investment avenues [

8,

9,

10,

11,

12,

13,

14,

15]. With Australia’s rising house prices and rental stress, this asset class has found a unique place in the residential property market. Dozens of BTR projects are already in operation, while many developments are under construction [

16,

17]. This asset class is expected to fill the gap in the rental stock and provide affordable rental housing.

The marriage between institutional investors and the private rental market is often described as a perfect match due to the increased demand for purpose-built rental apartments in Australia’s most-cosmopolitan cities. BTR, a highly desired asset class for institutional investors, offers a long-term investment strategy, tenure security, and value for money to renters through its world-class amenities and property management services [

15]. Its performance has proven relatively rewarding in the U.S. and U.K., providing a platform for increased economic development, employment, revenue generation, and foreign direct investment. As Australia’s housing markets continue to face affordable housing supply challenges, there is a need to advance this sector to resolve these challenges.

For this asset class to gain recognition and wider coverage in Australia, the government’s facilitative role must be expanded in several ways. First, the sector must harness the political support needed to make it successful, and second, the right platforms must be created to attract more institutional capital. In recent years, stakeholders have shown much optimism about the ability of BTR to provide affordable housing supply outcomes in Australia [

18]. Although showing massive progress, BTR is operated as a hybrid, an intermediate between residential and commercial [

19], and in its present form, it commands relatively higher rents than other rental units in typical Australian suburbs. From the institutional investor’s perspective, BTR is a financial asset and a good avenue to generate steady incomes and diversification benefits. Conversely, policymakers are looking at how this asset class can provide affordable housing. Australia’s National Rental Affordability Scheme (NRAS), which was established to provide affordable housing, was ended in 2013 due to the many challenges. No new scheme has been set up since then to provide 20% below-market affordable housing in the private rental market. BTR, which began to pick up in 2016, is providing decent rental accommodation. Interest rates continue to rise post-COVID-19, causing serious financial stress for mortgage-assisted homeowners and first-home buyers [

20]. A BTR housing model with an affordable housing mandate is expected to complement affordable housing supply, especially considering the generous support the industry enjoys from the government. At the moment, most BTR housing focuses on market-rate rents, not just in Australia but in other countries; an example was given by [

21] concerning residential REITs in Japan.

There is a gap in the literature regarding the conceptualization of Australia’s BTR housing model, especially whether it is a private or social investment. While the literature broadly focuses on several aspects of the asset class, such as financial viability, critical success factors, different modalities, and systematic risks or barriers [

4,

22,

23,

24,

25,

26,

27], within Australia’s housing policy, little is known about what BTR entails and whether it can provide an effective pathway towards increasing affordable rental housing supply. Using two operational BTR platforms in Australia and stakeholder engagements through interviews, this paper assesses BTR in light of affordable housing. It examines the government incentives offered to BTR investors and the expectations for social investment.

3. Methodology

This paper used the constructivist grounded theory methodology (CGT) to investigate Australia’s BTR housing model and its closeness to affordable housing. The Australian Government supports the BTR industry, yet this asset class is priced as a premium product; rents are slightly higher than those for BTS apartments. This has opened conversations about the cost of the incentives to the government, specifically if there are any social benefits in the form of affordable rental housing. CGT helps us to understand expert views through inductive reasoning and analysis of these views. The CGT is applied in the housing literature to understand and develop theories on various phenomena [

67,

68,

69] and is also used in other fields [

70,

71,

72]. It is appropriate for this research because of the evolving nature of BTR in Australia, where there are a limited number of operational BTR projects and many planned, proposed, and pipeline projects.

In understanding the workings of Australia’s emerging BTR industry, exploratory qualitative methods were used to collect the data. A set of leading questions was developed for discussions in semi-structured interviews based on the gaps found in the literature. The interviewees included policy experts, fund managers, property developers, and property companies. The interviewees are stakeholders in Australia’s BTR industry through their involvement in BTR development, policy research, or consulting. The policy experts are people in government, academia, and private consultants involved in policymaking, especially in the BTR industry. Experts in academia are academics who have written articles and policy insights on Australia’s BTR industry.

The method used for selecting the interviewees was snowball sampling. This method allowed the indexed interviewee to recommend and introduce colleagues and experts within their network connected to the BTR industry in different capacities across the sectors in Australia. The total sample size for the interviews was 20, of which 15 responded and agreed to participate in the study (i.e., n = 15), representing a 75% response rate. The interviews were conducted via Microsoft Teams and Zoom apps for an average of 40 min and recorded, transcribed, and exported into NVivo 12 for data analysis. To resolve potential biases with the response rate, two BTR projects were selected by purposive sampling from two Australian states, New South Wales and Victoria, to examine property characteristics that provide an understanding of BTR housing. This helped to compare BTR with affordable housing in the Australian context.

BTR housing is a new form of rental accommodation owned and managed by an institutional investor, with long-term security and extra amenities, while affordable housing commands no more than 30% of renters’ income [

14,

51]. The study looked at location, services, amenities, infrastructure, the investors behind the projects, lease duration, etc. Only two were chosen for this research because most BTR projects across Australia are proposed, planned, or under construction. BTR projects under construction were excluded because the development may be altered based on the client’s change of mind. Nonetheless, the case study projects summarize the product as it operates in Australia. Important information was also sourced from the Australian Property Council, the Australian Property Institute, the

Australian Financial Review newspaper, the

Urban Developer, CoreLogic

®, and Australian Property Data.

The interview findings were analyzed qualitatively. Following studies by [

15,

36], the study examined Australia’s BTR housing model in light of existing government support. Thematic analysis was adopted in accordance with [

73]. The process included familiarization of transcripts, identifying relevant codes, generating initial themes, reviewing the themes, and naming and defining the themes. The themes identified from the NVivo results are discussed to represent the factors that make the BTR asset class affordable or unaffordable in its present form. Two mechanisms were adopted to control for biases and minimize subjectivity. First, the findings were reviewed with peers to ensure they were consistent and coherent with the research question. Second, the interview findings were verified from different data sources for authenticity.

4. Findings and Discussion

Build-to-rent housing is largely perceived as a financial asset rather than an avenue to increase affordable housing. As housing investments evolve from simple buy–sell arrangements to advanced investment vehicles, they are traded on various platforms to generate good returns. The innovative investment vehicles trade housing for profit rather than seeing it as a home. More broadly, this approach depletes the social value of housing, discarding potential avenues to use it as a social investment. This is more common with recent housing models, and a prominent example is BTR. The conversations surrounding BTR are good for knowledge advancement and policymaking. The fact that BTR is seen as a financialized commodity and a potential avenue for social investment is good for every party involved. The former commands more support among stakeholders than the latter. However, financialized BTR is attracting criticism from independent experts and policymakers in terms of the cost of handing out incentives without expecting social investment. Similar sentiments were raised in Australia concerning the government’s first-home-buyer grants and the peculiarities of negative gearing, among others. This study used stakeholder views and two BTR projects, A and B, to assess whether they could generate affordable housing outcomes. For this discussion, affordable housing, as defined by the Australian Government, is housing that is appropriate for the needs of moderate-to-low-income households that are priced so that these households can meet living costs, including food, clothing, transport, medical care, etc. The Government mostly provides subsidies to reduce the rents to levels the target group can pay for. Does BTR qualify for affordable housing, given the support the industry is enjoying from the Government?

The findings from this study showed broadly that, although most BTR investors are profit-driven, and the asset itself is set out as a premium product, it has the potential to generate affordable housing outcomes in Australia. Three themes explain BTR as predominantly premium housing, that is housing designed for mid-to-high-income households. The first theme relates to the irony of scaling up affordable housing through BTR. The second explains the role of the inner-city locational attribute of the asset class, and the third theme is the extra facilities and property management services. On the flip side, BTR is not always premium housing, at least not in the Australian sense. Several BTR projects have been developed to offer affordable housing, either in their entirety or as an inclusion, just that the market BTR dominates more than affordable BTR. The differences and similarities between the two pathways are exposited to validate the interview findings.

4.1. The Conundrum of Scalability

It is suggested that BTR cannot meet the affordable housing requirements of mid-to-low-income households in Australia. However, the findings of previous studies by [

74] show that the private rental market can play a crucial role in this pursuit. The level of participation depends on the nature of the scheme in question and the Government’s policy direction. The arguments about BTR providing the necessary scale for affordable housing are quite paradoxical given the current state of the pipeline and operational projects across the country. By comparing the affordable housing supply gaps in Australia to the BTR apartments coming up, BTR may not be the answer to the supply problem. To assess whether the BTR industry could fill affordable housing supply shortfalls in Australia, Interviewee 9, a policy expert from the industry, stated:

BTR is not affordable housing. Politicians think of BTR as a panacea for affordable housing. It’s not that. It’s only 175,000 apartments; we are talking about 10.3 million properties in Australia. It’s a drop in the ocean to what is needed, and you can’t expect institutional investors to prop up the government’s inaction on affordable housing. It is an asset class that is no different to commercial and core retail investing. It’s like investing in a bridge or a toll road and is not driven to investing in housing. And so, will it provide a solution to Australian affordable housing? No, it won’t. It’ll go some way to provide another institutional asset class. It’s not the panacea for social or affordable housing. It won’t even provide the solution to market housing.

(Interviewee 9, policy expert)

The main justification for bringing more institutional investors onto the scene is to foster large-scale rental housing investment. This statement corroborates the findings of [

30,

31,

60,

63], which reveal that an institutionalized private rental market is needed to increase the rental stock and promote economies of scale. Comparatively, the scale at which BTS and mum-and-dad landlords will add to the rental stock is far from the capacity of BTR investors. This is largely due to financial constraints and the lack of capacity to develop and manage huge rental projects. BTR is perceived as a better avenue to meet the numbers for affordable rental housing. The challenge is the unfavorable regulatory and fiscal environment. Apart from the recent reforms to reduce land taxes by several states, BTR investors in Australia battle with high land taxes, GST and stamp duty fees, and foreign investor restrictions to get their projects running.

There is a narrative that the BTR industry is a potential substitute for the discontinued National Rental Affordability Scheme (NRAS). However, the asset class in its present form is another institutional asset comparable to commercial and retail assets. This view was exposited by Interviewees 5 and 6, who said that BTR was in a class of its own and could not be compared to any other existing residential asset in Australia. The envisaged benefits of scaling affordable housing supply through BTR do not appear realistic in Australia, at least not in the short term. This notwithstanding, this ideology must not be downgraded as it has proven effective in the U.S. and the U.K., according to the findings of a previous study by [

38]. It is a fact that market-rate BTR is increasing the rental stock in Australia, but what of the affordability side of it? Interviewee 6, a policy expert from the industry, stated:

I think there can be a lot more flexibility to allow for larger-scale build-to-rent with the inclusion of affordable housing. And I don’t think that’s necessarily a government issue. I think it’s more the developers who are not picking up on it. For example, a developer can provide one affordable housing dwelling in a 400-unit development. The flexibility on the design may be the cause of the setbacks.

(Interviewee 6, policy expert).

The issue of developers making room for inclusionary housing is an important one. Interviewee 6 believed that developers play a vital role in producing affordable housing. The challenge is how flexible they are with designing BTR. For instance, how would the outlook of the affordable housing apartments differ from that of the market rate ones? In any case, if all BTR developers adjust their designs and include affordable housing, how many units will be added to the market? This is an important consideration for including affordable housing in BTR developments. Scalability is one of the main reasons why BTR cannot be relied on as affordable housing. What the asset class is churning out in Australia is market-rate rental housing designed for mid-to-high-income households. With the few BTR investors offering affordable housing by inclusion, the numbers may not catch up with market demand. The Queensland Government’s pilot BTR scheme, which is designed to offer affordable housing, provides a more-expansive one-go pathway to speed up supply. It could be the most-effective channel for playing the numbers game in this discourse.

4.2. Inner-City Locational Attributes

Conventional knowledge in property valuation teaches that the closer a property is to the central business district (CBD), the more likely it is for that property to generate higher rents. The intense competition for BTR in inner-city areas and its convenience to renters contribute massively to the high rents charged on the asset. Predominantly institutional investors own it, so any arguments against the locational similarities with inner-city social housing projects may not hold. The BTR product, which is currently operating in Australia, thrives on its locational advantage; that is, it is a rental tenure designed and situated in inner-city areas and middle suburbs. It provides proximity to city centers, reduces commuting costs, and lessens the search costs for prospective renters since most of the projects are found within a reasonable radius of the CBD. Interviewees 3, 6, 7, 8, and 10 stated that BTR rents were high because the asset was in prime areas, providing easy access to infrastructure and social amenities. Without government support, reducing the rent could reduce the financial viability of BTR. Interviewee 1, a BTR developer, stated:

So, our project is close to the city, and the rents are set by how we define the market. If we are comparing to the private landlord rental market, which is all we must compare to in Australia at this stage, the rents set above market. And when you look at the UK in the US, they typically sit around 20% above market. There are multiple factors for that. One is that they are brand new buildings, so when we compare them to private landlord rental dwellings in a postcode, you might have 30- to 40-year-old dwellings that you’re comparing to. It is not a fair comparison in that sense.

(Interviewee 1, BTR developer)

This same interviewee acknowledged that the intense competition for land in inner-city areas contributes to high land costs, thereby underscoring the need to charge higher rents. The space in inner-city areas is highly limited and competed for by commercial and retail investors. This makes the land acquisition process a daunting one for BTR developers. However, the demand for housing in inner-city areas is generally correspondingly high, especially compared to peripheral areas. This automatically raises the rents charged on BTR in these inner-city areas. The research revealed that the BTR project selected for the study commanded higher rents than other rental units. One of the interesting findings is that investors participated in the project to provide a different “style” of private renting characterized by superior amenities and services. This shift in housing delivery contributes to the high rent charged on the asset class. Interviewees 11 and 5, a policy expert and property manager, stated, respectively:

We’ve done analysis and found that the rents of initial BTR developments coming up in Sydney is, say, 20% premium to the wider market. One of them, which recently opened last month, is clearly aimed at a premium or an upper end of the market, which is because of the inclusions and where the price points are.

(Interviewee 11, policy expert)

…there’s still a lot of confusion about the affordability side of BTR. So, I’ve spoken to a lot of people who assume BTR is an affordable residential model, but in fact, it’s quite a high-end model.

(Interviewee 5, property manager)

This asset class improves the quality of Australia’s rental stock massively and promises investors good returns. The views solicited from the interviews show that BTR rents are generally too high to qualify as affordable housing.

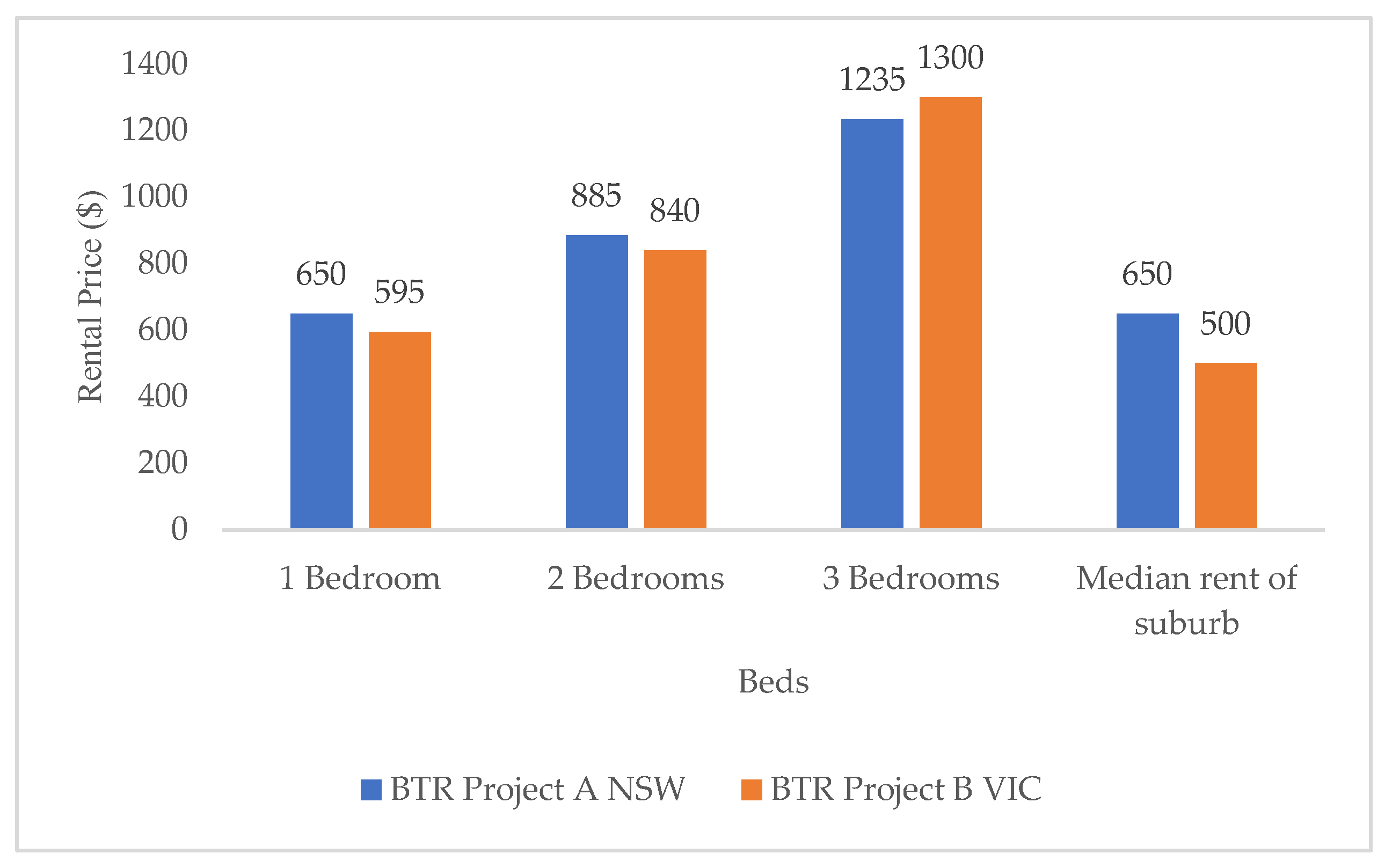

Figure 1 compares the rents of two BTR projects, A and B, in New South Wales and Victoria from January to August 2023 against the median rents for residential dwellings in the suburbs where these projects are situated. Projects A and B are currently being operated in the market, and the rents presented here are the minimum rents charged for 1-, 2-, and 3-bedroom apartments, respectively.

Figure 1 shows that rents for 1-, 2-, and 3-bedroom apartments were generally higher than the rents charged on other rental properties in the same suburbs, as stated by the interviewees. Except for 1-bedroom apartments, the rent of the 2- and 3-bedroom BTR apartment types were higher than the median rent, to the extent that BTR rents were almost twice that for the 3-bedroom apartment. The BTR buildings were brand new, being relatively new developments compared to most build-to-sell apartments on the market. Although not proven, the rents charged on the current BTR projects in Australia may also be influenced by the happenings in other countries. BTR investors are fond of comparing their projects with those in the U.S. and the U.K. The interviewees acknowledged that the asset class had been successful in those countries and that investors were looking to replicate this success in Australia. In summary, the high rents charged on BTR developments in Australia can be attributed to the inner-city locational attributes. There is increased housing demand in the city, and BTR buildings, apart from being brand-new, are accessible to essential amenities in the CBD. Unless this model is modified, BTR, in its present form, may not accurately qualify as affordable housing.

4.3. Extra Facilities and Property Management Services

BTR provides renters with a wide range of property and facility management services. In property valuation, buildings with more services and finishes are priced higher than those without because they cost more to build and manage. They also address the limitations associated with build-to-sell apartments and mum-and-dad-financed units. The quality services provided offer a certain lifestyle for its target renters. Interviewee 6, a policy expert from the industry, stated:

I understand how they get to look after their residents, and I know that with that rent comes a fully equipped gym, community events planned for the year, multiple people on site, and security on site.

(Interviewee 6, policy expert)

Apart from a gym facility, 24/7 on-site staff, and security personnel, BTR tenants get access to in-built shops and recreational centers, such as a children’s playground and a swimming pool. Interviewees also revealed that BTR projects offer easy access to centrally positioned amenities that may not be present within the BTR building itself, for example, schools, hospitals, trains, trams, etc., confirming the conception of BTR as a premium product due to these extra services and facilities. The cost of these services is part of the rent and not paid for separately. Interviewee 1, a BTR developer, stated:

Within build-to-rent, you get a lot of additional things that you don’t get in a private rental, especially from us. What we are providing so you get all your appliances included, so your fridge, washing machine, microwave, dryer, and all those things are included, which aren’t included in a typical rental. We also pay the water bill and the gas bill for the dwelling. We have zero bonds, so you can move into our apartment without paying a bond.

(Interviewee 1, BTR developer)

Our research also revealed that BTR offers more-secure, long-term leases than others, sometimes between 3 and 5 years, ensuring good security for tenants. Interviewee 1, a BTR developer, stated that BTR tenants enjoy more benefits than tenants in other units, such that the trade-off for the higher rents was justifiably reasonable. The views of industry experts inclined towards the fact that BTR is a novel asset class and must be treated as such, reiterating that the rent charged was a good value for the money for those who could afford it. This presupposes that the target group for BTR may not necessarily belong to the low-income group. The policy experts interviewed raised serious concerns about the high rents of BTR apartments, arguing that the government supported BTR developers through the treasurer’s 50% land tax concession. Market surveys revealed that BTR projects in Sydney, Melbourne, and some parts of Brisbane command rents 20% above the market rate, making them more expensive than build-to-sell (BTS) apartments and mum-and-dad units. This is worrying, as the lower end of the market cannot afford to rent in BTR, raising questions about its place in Australia’s housing policy.

To steer Australia’s housing policy in the right direction, the interviewees revealed some interesting opinions about the evolving asset class. Some perceived BTR from a liberalistic market-driven point of view, while others saw it as a viable option for social investment. From the institutional investor’s perspective, this asset class could be remodeled into a financial asset to obtain the benefits of diversification, a thinking that was common among return-oriented investors who wanted to expand their portfolios with fewer correlated assets. In contrast, the housing policy experts viewed BTR as a potential avenue for institutional investors to make social investments such that, while one party was looking at making steady returns, the other was looking at how the asset could be used for social advantage. Interviewee 7, a policy expert from academia, stated:

In the current context, the way BTR is a luxury product, it doesn’t make sense to subsidize it. It makes sense to subsidize it only if it’s a social affordable product, not when it’s a private market luxury product. At what cost will the subsidies for a luxury product affect the cost of subsidies for social and public housing? Even for that matter, subsidies for ownership housing like the First Homeowner Grant and negative gearing are being criticized because it comes at the cost of social housing and public housing. So, we need to be very careful about what we are proposing to make. What kind of BTR, how viable is it, and for whom?

(Interviewee 7, policy expert)

Some level of clarity is required in the discourse on government support to guide the efforts of the Federal and State Governments to boost the BTR industry in Australia. Otherwise, the unconditional support given to the sector could generate perverse incentives detrimental to the well-being of most mid-to-low-income households that rent in Australia. This finding confirms the finding of [

32] that government support could have a negative effect, causing further housing inequality in cities. If we suppose that the support given to BTR is left open, albeit without any eligibility conditions, then institutional investors may eventually enrich themselves by developing more high-end apartments for the market, likely exacerbating the already severe housing unaffordability. It is, therefore, important to analyze the investment decision of institutional investors towards the asset class very critically, including, for instance, their opinions on the asset’s competitiveness, expectations, and challenges. These steps will clarify the place of BTR within the fabric of the private rental market so that analysts can properly prepare the asset class for valuation, forecasting, and modelling purposes.

Based on the stakeholder views drawn from the interviews, this study found that the asset class is not a suitable pathway for affordable rental housing supply. The research presented the following empirical findings. First, the intention to scale up rental housing supply through BTR is not realistic in the short term, given the unfriendly fiscal and regulatory environment. Second, the inner-city locational attributes of the asset class render it a premium product and far from affordable for most moderate-to-low-income households in Australia. The land acquisition process for a typical BTR developer is daunting, making it impossible to offer the units at or below the market rate. Lastly, BTR provides extra property management services, absent in build-to-sell and mum-and-dad units. The cost of using these services is included in the pricing, raising the rents above the median rents in a typical Australian suburb.

4.4. How Different Is BTR from Affordable Housing?

Two BTR projects, A and B, were selected to identify the property characteristics that differentiate BTR from affordable housing. The developers were interviewed to gather information on the projects. The case study projects were in two states in Australia: New South Wales and Victoria. Affordable housing characteristics were gathered from projects operating under the National Rental Affordability Scheme and from community and public housing providers. Based on the findings from the two approaches, the differences between BTR and affordable housing were identified and compared and are presented in

Table 1.

Table 1 presents the BTR asset class as an upgrade of affordable housing in Australia. In addition to being new developments, most BTR projects provide tenants with a high-quality lifestyle and high-quality rental living. As a result, BTR stands on its own as an asset class and is not comparable to other rental tenures in Australia. To suggest that BTR is wholly affordable housing is flawed in many respects, at least in its present form. The luxurious attribute of the asset class reasonably justifies the high rents charged on it. Supporting this sector without eligibility criteria for investors raises certain sentiments about fairness and housing equity. The asset class may rightly be classified as a luxury product, providing the least opportunity to meet the housing requirements of mid-to-low-income households in Australia. Without the required regulatory reforms such as land release and land and withholding tax concessions, profit-oriented institutional investors will likely continue running BTR as a financial asset without considering affordable housing supply. This study found that a crop of affordable BTR projects was coming into the supply chain due to various supporting structures set up by the NSW, VIC, and QLD Governments. These are showing that it is possible to generate affordable housing outcomes with BTR, a view that is contrary to the position of many experts.

4.5. Government Support of Build-to-Rent in Australia

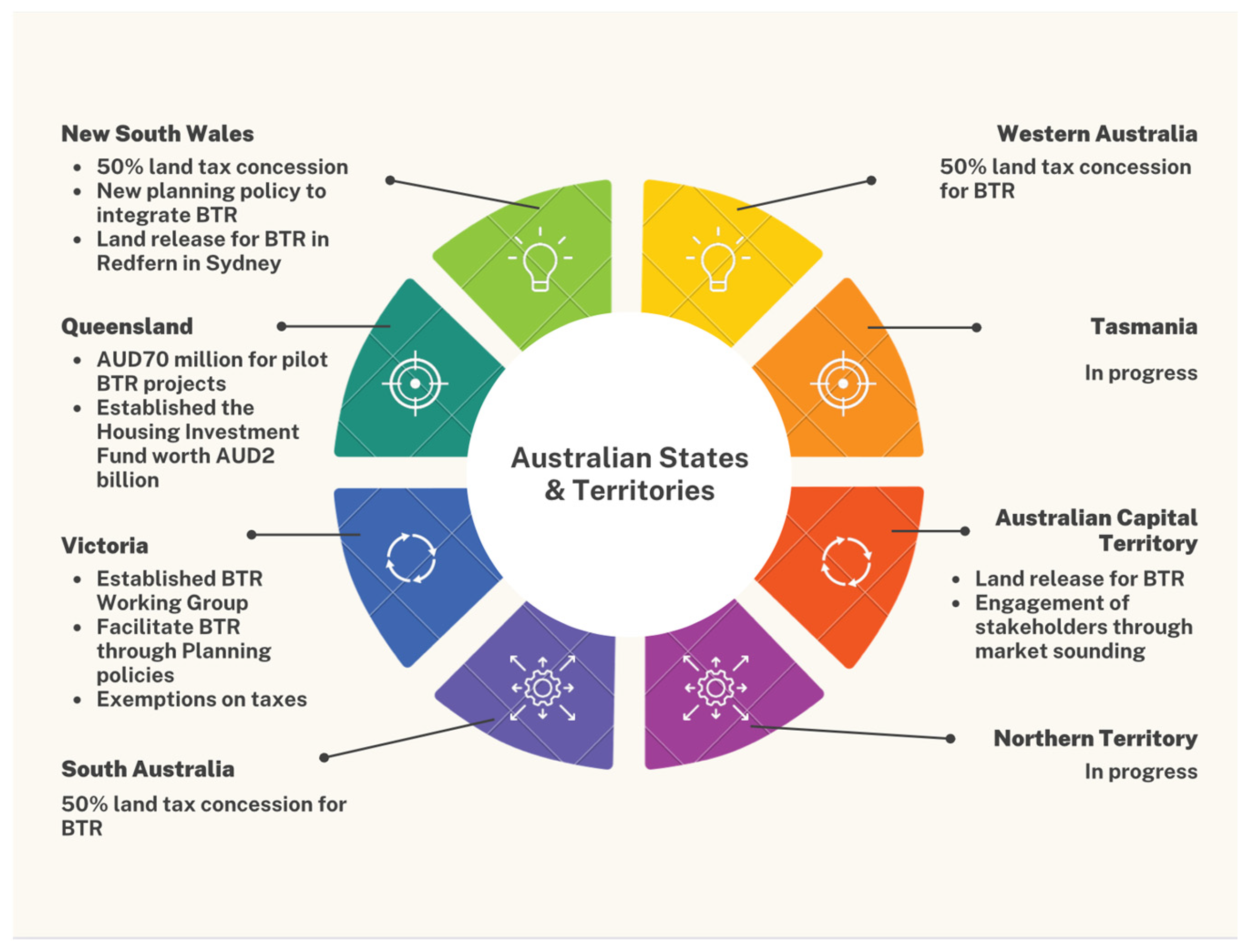

Australia comprises six states, New South Wales (NSW), Victoria (VIC), Queensland (QLD), Western Australia (WA), South Australia (SA), and Tasmania (TAS), and two territories (Australian Capital Territory (ACT) and the Northern Territory (NT)). Since it is the state and territory governments that regulate housing, they have embraced BTR differently and at varying rates, depending on the flow of institutional capital, the number of developments, and the stakeholder discourse to advance the sector. Other factors, such as the short- and long-term needs for rental housing, play a huge role. NSW, VIC, and QLD are progressing quite well with giving incentives to investors and facilitating the sector’s advancement. Experts posit that the other states took inspiration from these three to implement similar incentives and closely related support packages. The incentives provided to the BTR industry are meant to produce quality rental accommodation and, more importantly, to ensure that these apartments are affordable. From the policy perspective, there is no point in building rental apartments that are not affordable to most residents, especially given the size of pipeline developments.

Several reforms are required to make BTR affordable. The interview results revealed that various incentives will help to reduce development costs and facilitate approvals for the commencement of BTR projects. Interviewee 8, a policy expert from the industry, stated:

I think that it’s all about releasing land for BTR projects. This is where the government can really be engaged. The conversation should be about releasing land in practical locations that are useful to live in. The states will often have land which is well located but not necessarily for open-market residential use. These locations could be good because they are next to train stations and are best for transit-oriented development next to tram stops.

(Interviewee 8, policy expert)

Land release is undoubtedly an essential part of the development process. First, the ideal locations for BTR are predominantly within inner-city areas and, in some instances, middle suburbs. There is normally intense competition among commercial users for inner-city land. Aside from negotiating for the highly priced land in these areas, the initial stage of acquiring land is a challenge to BTR investors. Releasing land for BTR makes this stage easier and faster for developers to get their proposed projects running. The government can also use taxes to boost the BTR industry. Interviewee 10, a government policy expert, stated:

I think the big thing now is that BTR is not an affordable housing solution given the current tax situation. The Managed Investment Trust (MIT), Goods and Services Tax (GST), and land taxes are headwinds contributing to BTR becoming a more market-based product. Land taxes have been resolved in some states. More can be done with the MIT as it puts investors at a disadvantage and ultimately explains why BTR is priced above the market rent.

(Interviewee 10, policy expert).

A managed investment trust (MIT) in Australia is an investment vehicle set up to enable members of the public, including foreign investors, to invest passively in property. However, this study found that the MIT withholding taxes for foreign investors, along with land taxes and GST, is a major disincentive to investors, especially foreign-based ones. The Federal Government has recently reduced the MIT withholding tax for BTR investment after continuous lobbying from different stakeholder groups. Interviewee 10 posited that taxes contribute to the high rents that BTR can command and that the government could make additional reforms, in the form of supply-side incentives, to influence developers to reduce their rental rates in the long run.

Figure 2 lists the incentives given to BTR by various state and territory governments.

Through an MIT, the Australian Government provides tax concessions to foreign investors who invest in BTR. Over the years, a 30% withholding tax rate was applied to BTR. This was higher than the 15% charged on other property classes, such as BTS apartments and retail. Through continuous lobbying to reduce the withholding taxes, the Federal Government announced on 9 May 2023 in its budget that the 30% MIT withholding tax for BTR was reduced to 15% from 1 July 2023. This was a major step by the government to attract more foreign capital into BTR. Experts alluded to the MIT withholding tax concerns as being the focus of policy deliberations, describing it as the major point of discussion. The concession targets BTR projects with at least 50 apartments owned by the entity for at least 10 years and offers renters at least 3 years of tenure security.

The government also supports BTR through its National Housing Infrastructure Facility (NHIF), which was established to provide infrastructure support to unlock new housing development. The NHIF can be used for electricity, gas, water, sewerage, stormwater, roads, and telecommunication. Although it is stated that the NHIF is for social and affordable housing, the BTR sector can also benefit from this fund, and this is especially relevant to the BTR affordable housing pathway. To access the NHIF, applicants are required to assess their new housing developments against the conditions of the fund to ensure that all prospective applicants meet the eligibility criteria provided. If successful, the Federal Government provides infrastructure support to developers and BTR investors to unlock new housing at the state level. Finally, the government’s role in successfully integrating BTR within the framework of Australia’s planning scheme is paramount. Although the planning mechanisms are influenced more at the state level, the Federal Government needs to coordinate with the State and Territory Governments to ensure consistency. Activities with zoning and granting development permits for BTR developments can be facilitated using special mechanisms.

The Australian Government’s housing policy direction and, for that matter, the support for the BTR industry is positive. The recent reduction in the MIT withholding tax for BTR and other upcoming policies at the state level indicates a commitment to advancing the rental sector. However, stricter requirements, such as forcing BTR developers to include at least 20% affordable housing in their BTR developments, may be the breakthrough point. This is not a new practice, as it has worked well in the U.S., where, prior to development approval, developers are required to include affordable housing in their BTR projects.

4.6. Reflections on BTR and Affordable Housing

Sceptics have given all the reasons why BTR housing cannot be viewed as an answer to affordable housing gaps in Australia. Indeed, based on the intrinsic characteristics of BTR, it is different from affordable housing. Australia’s housing market is full of market BTR (mBTR) with little affordable BTR (aBTR). This study interviewed three broad stakeholder groups, namely seven policy experts (Interviewees 3, 5, 6, 7, 8, 9, 10, and 11), five institutional investors (Interviewees 2, 12, 13, 14, and 15), and two property developers (Interviewees 1 and 4). As we advance towards bridging affordable housing supply gaps, the two options of mBTR and aBTR must be accurately defined and differentiated based on the product offered and the target group for which these projects are designed. Like MFH in the U.S., Australia must be more intentional about producing aBTR for mid-income households, especially for young professionals and public servants, including teachers, nurses, doctors, bankers, etc. The support package for BTR developers could be instituted to meet terms and conditions or eligibility criteria before investors benefit from the available incentives. This viewpoint will likely attract much criticism, especially from ideologists who promote market-driven rental properties. Of course, market BTR is also important for the high end of the renters’ spectrum. The perception of Australia’s BTR industry, as portrayed by most industry reports, holds much optimism for investors, but its position within the framework of the housing market is not completely understood. Currently, it is viewed as a financial asset from the investor’s perspective and a social asset from the housing policy perspective.

This study demonstrated that the BTR business model in Australia is predominantly market-designed. The explanation for this is that, first, before institutional investors can obtain their required risk-adjusted returns, they must price the rent in accordance with the amount invested, confirming the finding of previous studies by [

27] that the returns generated are important to institutional investors. The ultramodern facilities and amenities provided, as well as the high land prices in inner-city locations, contribute to the overall cost of construction. Furthermore, the fiscal and regulatory environment also adds to the development cost. In addition, according to the definition of affordable housing in Australia, it is almost impossible for institutional investors to provide affordable housing on the expected scale, given these factors. Earlier studies in Australia and other countries, such as the findings of [

9,

15,

38], have proven that, with the right reforms and engagement, profit-driven investors can provide affordable housing. Indeed, three institutional investors in Australia have embraced the idea of including affordable BTR in their developments. It has also been demonstrated that government pilot projects for aBTR are an important pathway to scaling up affordable rental housing supply in Australia.

5. Conclusions

There is a preconceived idea that Australia’s build-to-rent housing model is a premium product, meaning it is a high-end housing model designed mostly for mid-to-high-income earners. This presumption is based on institutional investors’ profit-driven business model and their unwillingness to take the acceptable risk of investing in affordable housing. However, some have also posited that BTR investors should produce affordable housing given the support they enjoy from the government. This study examined whether BTR could be used as an avenue for affordable housing supply. Expert views were solicited from 15 major stakeholders in Australia’s BTR sector. Although the position of the expert, that is whether a private consultant, developer, or policymaker, is likely to influence their view on BTR, their views presented interesting contributions to the affordable housing debate. For instance, given the exposure to return-driven investments, private consultants are likely to view BTR as a premium product, while policymakers are likely to go on the tangent of affordable housing. Nonetheless, the ingredients of their arguments were analyzed and discussed in this study. To minimize biases and increase the reliability of the findings, selected operational BTR projects across the country were inspected and examined against the interview findings to reach the conclusions expressed here.

Based on expert views and selected BTR projects being operated across Australia, the study concluded that BTR, in its present form, is predominantly a premium housing product. It found that the rental price sits above the median rental price of rental apartments in Australia and, therefore, cannot be completely relied on as a substitute for affordable rental housing. BTR pricing is influenced by its inner-city locational attributes, ultramodern facilities and services, and the newness of the buildings. Developers also state that they consider the trends in the U.S. and U.K. markets to set the rents. At the time of this empirical study, three major BTR developers in Australia had included affordable housing in their projects. We concluded that, given the right structures and additional reforms, the pathway for affordable BTR is also possible in Australia. Furthermore, state-led affordable BTR is also possible, as demonstrated in the Queensland Government’s pilot BTR projects, which are expected to deliver close to 490 affordable housing apartments in the first round of approvals. The various state and territory governments must arrange a special package for affordable BTR for mid-to-low-income households. The additional reforms include releasing designated land, implementing more land tax concessions, reducing the MIT withholding tax for BTR further, and using planning instruments to remove delays in development approvals. Just like the U.S. and U.K., BTR developers who want to enjoy these benefits must be compelled to include 20%, 30%, and 50% affordable housing in their BTR developments, depending on the specific locations in which these apartments are needed. Although market BTR must be given support to remain an integral part of Australia’s private rental market, affordable BTR requires additional attention to respond to the housing needs of young adults in Australia [

7]. With the right reforms, affordable BTR could be used as an avenue for bridging the affordable housing supply gaps in Australia.

{kind=link}

{kind=link}