1. Introduction

There has been a significant increase in real house price growth in most advanced economies since the 1970s. Kishor and Marfatia [

1] found a steady increase in average real house price growth in 15 OECD countries, with Australia showing the highest average quarterly growth of 0.74% between March 1975 and December 2013. More recently, Australia’s average quarterly house price growth of 2.77% ranked above Canada (2.33%), the Netherlands (2.55%), the United Kingdom (1.28%), and the United States (2.55%) over March 2020 and December 2021 [

2]. Factors such as the rapid growth in house prices across advanced markets, increasing neoliberal housing policies, and the recent issue of housing financialisation, especially in countries with a capitalist sociopolitical background, have resulted in a significant decline in the homeownership rate. In the United States, for instance, the homeownership rate was below other advanced economies during 2000–2018 [

3], and this has caused heterogeneous effects among households in the country [

4]. According to a report by the Local Government Association [

5], homeownership rates among young people in the United Kingdom have decreased compared to 20 years ago. Similarly, an Australian Parliament report prepared by Hall and Thomas [

6] shows that home ownership rates significantly declined between 1971 and 2016, particularly for the age group of 22–34, which dropped from 57% to 44.6%. Various factors have accounted for this worsening home ownership. Acolin et al. [

7], for instance, highlighted rigid lending criteria as a critical barrier to entry. Bourassa and Shi [

8] (2017) identified borrowing constraints and ethnicity as contributing factors to the declining home ownership rate. The issue of income growth failing to catch up with rising house prices was raised by Bourassa and Shi [

8], Blundell et al. [

9], and Bangura and Lee [

10,

11]. Moreover, the use of housing investment for speculative wealth generation has been evident recently [

12].

The COVID-19 pandemic exacerbated the issue of home ownership, culminating in the development of significant economic stimulus packages, some of which were targeted at first home buyers (FHBs) either directly or indirectly [

13]. In the United Kingdom, the central bank reduced the cash rate by 65 basis points to 0.1% and the government introduced a new mortgage guarantee scheme from April 2021 for home buyers with a deposit of almost 5% on homes with a cap value of GBP 600,000, together with the extension of the stamp duty land tax exemption until June 2021 (International Monetary Fund (IMF) [

14]). Further, the Coronavirus Act 2020 offered more protection to social and private tenants by delaying the period that landlords can evict tenants [

15]. According to IMF [

14], the COVID-19 response policies of Fannie Mae and Freddie Mac in the United States include providing mortgage forbearance for a period of 12 months and waiving related late fees, suspending reporting to credit bureaus of delinquency that is related to forbearance, extending foreclosure sales and evictions of borrowers to 60 days, and providing loan modification options. In Australia, policies such as early superannuation withdrawal in two separate cases of AUD 10,000 each, home lending rate reduction, first home loan deposit scheme, and Homebuilder, a cash grant to new home builders or significant renovators, are considered to have a direct relationship with first home buyers (FHBs) [

16], while income supplementary programs such as JobKeeper and JobSeeker, as well as a moratorium on evictions, and mortgage payment pauses are not directly targeted at FHBs, but they may have some financial implications for this cohort in the housing market (economic responses to the COVID-19 recession with direct and indirect benefits to FHBs are summarised in

Appendix A). The Homebuilder program was introduced by the former Commonwealth Minister for Housing, former Commonwealth Treasurer, and the former Prime Minister of Australia on 4 June 2020 to propel economic growth and boost jobs in the housing construction sector during the COVID-19 pandemic. Homebuilder provides eligible owner–occupiers a grant to build a new home or substantially renovate an existing home. A grant of AUD 25,000 was offered to those contracts entered between 4 June 2020 and 31 December 2020, and later, an AUD 15,000 grant was offered to eligible contracts entered between 1 January 2021 and 31 March 2021. The Treasury initial forecast of the Homebuilder was around 27,000 grants at a total cost of approximately AUD 678.3 million across the country. However, by 24 June 2022, Homebuilder had successfully offered a total of 100,214 grants to eligible recipients, with an approximate value of AUD 2.3 billion in total grant funding. This discrepancy can be attributed to the resulting overheated residential construction industry caused by heightened construction activities that culminated in significant material, land, and labour supply issues (Australian Department of the Treasury (ADT) [

17]). In the context of global cities, such policies will help to mitigate the vulnerability that cities are prone to during external shocks [

18].

Despite the variation in the nature and scope of COVID-19 policy interventions across nations, as argued by Blundell et al. [

9], it is still glaring that the crisis will continue to escalate inequalities among households. This raises questions around the success and externalities of these intervention policies on potential FHBs. To address these questions, we conducted a case study of New South Wales (NSW), Australia’s most populous state, where affordable entry-level housing has declined significantly [

11,

19]. Further, Sydney, the capital of NSW is the least affordable city of Australia in terms of housing and the second least affordable globally [

10,

11,

20]. This means that, being a highly urbanised city, Greater Sydney will continue to experience what Ribeiro and Gonçalves [

21] described as new and continuing challenges in providing housing and other essential services. These reasons make NSW an interesting case study. Our study focuses on the external impacts of stimulus packages on first home buyers (FHBs) during the COVID-19 pandemic. We assess the effectiveness of these policies in promoting entry into the housing market and investigate whether they provided direct or indirect assistance to FHBs in competing against other market participants, such as investors or cash buyers.

This study contributes to the literature in the following ways. First, to the best of our knowledge, the study is likely the first attempt to evaluate the effectiveness of economic stimulus packages aimed at facilitating FHBs’ entry into the housing during the COVID-19 pandemic. Even though extensive studies have examined the effects of government policies, such as fiscal stimulus and monetary policy interventions to aid economic recovery [

9,

22,

23], limited research has been carried out on the association between such policies and FHBs. Given the decline in housing affordability, we examine whether government policies assist or hinder FHBs in entering the housing market. The findings are strongly linked to cities’ resilience by highlighting the challenges that FHBs face in accessing affordable housing during a global shock, such as the COVID-19 pandemic. Housing affordability is an essential component of urban resilience as it affects a city’s ability to attract and retain a diverse workforce, sustain local economies, and support social cohesion [

3,

18]. The study’s emphasis on the unintended consequences of economic stimulus policies, such as inflating property prices and exacerbating inequality, could inform policymakers in developing more effective housing policies that promote urban resilience. By promoting more equitable access to affordable housing, cities can become more resilient to withstand global shocks [

19].

Second, this study differs from previous COVID-19 research as it employs a qualitative analysis, rather than quantitative modelling on empirical data, to investigate the externalities of economic stimulus packages on FHBs for the first time. By using this approach, the study can gain insights into the perceptions and experiences of FHBs regarding COVID-19 policies, which can reveal the complexity and subtlety of their perspectives. Through this in-depth exploration of the issues, the study can develop a thorough understanding of the subject matter, particularly the potential externalities of these packages on FHBs [

24]. Specifically, FHBs may have unique experiences and perspectives on COVID-19 related policies that may not be fully captured by quantitative modelling. A qualitative analysis can provide a more comprehensive understanding of their experiences. Further, a qualitative analysis can help to uncover the diversity of these effects. By exploring the experiences of FHBs, the study can shed light on the specific challenges and opportunities faced by this group during the pandemic. By understanding the perceptions and experiences of FHBs, policymakers and practitioners can develop more effective interventions and policies that address the unique challenges faced by this group.

The rest of the paper is structured as follows.

Section 2 presents the related literature, while

Section 3 discusses the data and methodology of the study. The findings and analyses of the results are presented in

Section 4, and

Section 5 summarises the findings and presents the policy implications.

5. Conclusions and Implications

The COVID-19 pandemic led to Australia’s first recession in 30 years, prompting the government to implement significant monetary and fiscal stimulus measures that facilitated a rapid economic recovery. However, these measures had both direct and indirect effects on first home buyers (FHBs) in NSW, raising questions around the link between COVID-19 and economic stimulus packages on FHBs, their effectiveness in promoting entry into the housing market, and their role in supporting FHBs amid competition from investors and cash buyers. To address these questions, a conceptual framework was developed, drawing on the housing financialisation to explore the externalities of COVID-19 economic policy responses. The study utilised a qualitative design with primary data sources to provide a comprehensive understanding of the issue at hand.

Primary data were collected via an anonymous survey of FHB who had been actively looking or had completed a purchase since March 2020. A total of 61 respondents were sourced through a public platform and the mortgage broking industry, which were categorised into various demographics, such as financial capacity, location, level of government assistance, or purchase price. To facilitate the analysis, Nvivo software was used to generate a deductive and inductive coding structure. By examining the gaps highlighted, we make the following contributions to the literature with three important findings.

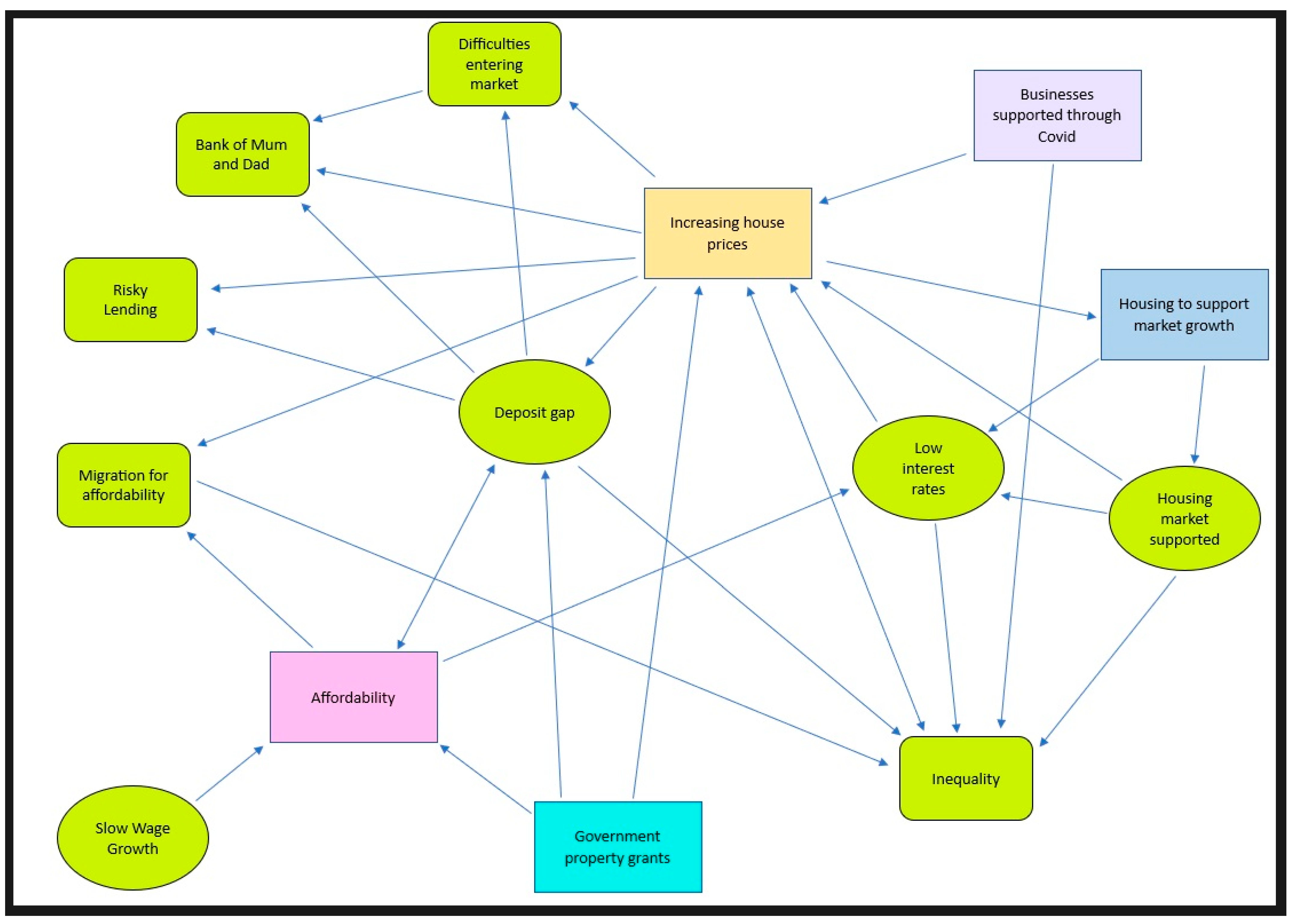

This study provides a novel exploration of the relationship between COVID-19 and economic stimulus packages on first home buyers (FHBs) and reveals that the externalities of these policies are having unexpected consequences. Despite some positive outcomes, such as short-term increases in FHB participation due to lower interest rates, the overheated property market fuelled by expansionary fiscal and monetary policies is disadvantageous for many prospective FHBs, who fear they may never be able to afford homeownership. Consequently, FHBs with FOMO are modifying their expectations and behaviours, such as relocating to more affordable regions or taking on higher levels of debt or risking rushing into a property without completing thorough due diligence, only to find issues with the property once they moved in. This study’s findings have implications for policymakers and macroeconomists, highlighting the need to mitigate the unintended negative consequences of economic stimulus policies on potential FHBs.

Second, this study is likely one of the first to evaluate the effectiveness of economic stimulus packages aimed at facilitating FHBs’ entry into the housing market during the COVID-19 pandemic. More than 71% of the survey participants noted a rise in purchase prices during the study period. Furthermore, 83% of respondents claimed that the process has become more complex, making it more difficult to access homeownership. Although 72% of those surveyed were potentially eligible for government assistance in some way, just 30% were able to obtain support. Over 70% of respondents believed that the government does not provide sufficient assistance to FHBs, suggesting that government grants only inflate property prices, exacerbating the issue. These findings raise questions about the long-term efficacy of such packages in assisting FHBs. These results can be used to develop future economic stimulus packages or other housing policies aimed at facilitating FHBs’ entry into the housing market, particularly during global shocks.

The study’s third finding reveals an imbalanced property acquisition field for FHBs during the COVID-19 pandemic despite several economic stimulus packages aimed at promoting homeownership. The FHBs’ surveys emphasised inequality as the primary challenge faced by FHBs, with 48% of participants attributing the difficulties to investors and existing homeowners’ significant advantages. Policies such as negative gearing and capital gains tax waivers could intensify the issue of market entry. Expansionary monetary policies also contribute to inequality by inflating house prices and driving consumer demand. In turn, excessive property deflation is quickly addressed by governments, as seen at the start of the COVID-19 pandemic. Consequently, FHBs have had to relocate, lower their expectations, take on additional financial risks, or rely on intergenerational support. These unintended consequences could trigger policy reversal to combat the financialisation of the housing market to promote affordable housing and renting for FHBs. These findings can also guide international housing policymakers in supporting FHBs in a market with strong investor presence. While the study focuses on Australia, the results offer valuable insights into delivering effective government stimulus policies, allowing policymakers to allocate resources more judiciously.

Even though we examined the unintended consequences of COVID-19 economic policies on first home buyers, our study has some limitations, which include the sample size, the study period that was only limited to post-March 2020 when significant COVID-19-related economic policies and stimuli began to take effect, and the study being limited to the state of NSW only. Therefore, future research can expand the scope of this research topic by examining various housing markets and targeting diverse demographics.

{kind=link}

{kind=link}