1. Introduction

Due to the specificity of properties being a category of economic goods, the property market exhibits a high potential for disequilibria. Property price fluctuates around the reproduction value of the property rather than tending to a neoclassical equilibrium. The COVID-19 pandemic and the war in Ukraine shocked the property market both on the demand and on the supply side through various impulses—fiscal spending [

1], changes in the labor market [

2], lockdowns and breakdowns of construction [

3,

4], the outflow of construction workers [

5], new immigrants [

6], and last, but not least, inflationary pressures and decreased housing affordability [

7] urging the need for social housing [

8]. In the case of the Czech Republic we can observe also the impact of monetary policy shocking the property market. Monetary policy, being very loose during the COVID pandemic [

9], boosted demand for properties. Subsequent monetary tightening barely froze the property market [

10]. The price of properties, in reaction to the mentioned shocks, has seen a truly dynamic development, remarkably differing across regions. In our paper we show that the magnitude of the fluctuation of the price cycle tends to be higher in regions with cheap properties, meaning simply that properties of higher value lose their value in “bad times” more slowly and mildly compared to “low end” properties. The downward rigidity of prices is especially more observable for more expensive properties. This can be attributed to a range of factors, including the desirability of properties in higher-end areas, the relatively stable financial position of owners of these properties, and the ability of these owners to wait for better market conditions to sell their properties.

On the other hand, properties in lower-end areas tend to be more susceptible to market fluctuations, as their owners may be more likely to be financially vulnerable, and may need to sell their properties quickly to meet their financial obligations. As a result, properties in these areas may experience more significant price fluctuations in response to changes in market conditions.

Overall, the research suggests that the property market is highly susceptible to disequilibrium, and that the value of properties is subject to significant swings in response to changes in market conditions. With the aim to confirm this hypothesis, we offer a comparative analysis of property price development in two regions of the Czech Republic that fit best to the mentioned scheme—two economically and structurally different regions in the Czech Republic in terms of the impact of crisis on the real estate market. These are the Prague region and the Karlovy Vary region. We selected these regions because one—belonging to one country the property market faces the same historical, regulatory, monetary, fiscal, and other policy environment, and two—because these two regions represent the “high end” and the “low end” in the price scale on the Czech property market. The property price differences mainly reflect the economic and structural characteristics described below:

The prague region fulfills the role of a natural center of politics, international relations, education, culture, and economy. Prague is also an important city in Central Europe. Prague is the largest city and at the same time the capital of the Czech Republic. It covers an area of 496 km

2. The central location and attractiveness within the Czech Republic and Europe predestined Prague to the role of not only an important travel destination, but also a crossing point for a number of important transit routes [

11].

Prague is characterized by a high number of people who commute to Prague for work, using a developed transport infrastructure [

12]. The attractiveness for foreign entrepreneurs and multinational companies also contributes to the wealth of the region. In the next period, an increase in the number of residents can be expected, mainly due to job opportunities and people moving for work.

The Karlovy Vary region is located in the west of the Czech Republic. The region consists of three districts—Cheb district, Karlovy Vary district, and Sokolov district, and there are a total of 134 municipalities. With its area (3310 km

2), the Karlovy Vary region ranks among the smallest regions in the Czech Republic. One of the most important industries in the Karlovy Vary region is the spa industry [

13].

The Karlovy Vary region is currently struggling with population decline and a whole range of structural problems. The Karlovy Vary region will be one of the most affected regions in terms of the European Union’s move away from heavy industry. Massive subsidy support from the European Union is planned for the Karlovy Vary region, which is to ensure the transition from heavy industry to industry using renewable energy sources. Despite the significant support here, it can be expected that there will be a significant decrease in job opportunities in the entire region and that many people will leave the region for better earnings in other regions.

Table 1 shows a comparison of basic statistical data for both regions.

Figure 1 marks the investigated regions on the map of the Czech Republic.

The study aims to identify the reasons for differences in price dynamics and rigidities of different properties in the market. To achieve this goal, the study offers an in-depth analysis of the property market from an economic point of view.

By understanding these factors, the study seeks to provide valuable insights into the workings of the property market and the reasons why prices may fluctuate differently across different types of properties. For example, the study may shed light on why properties in certain locations or of a certain quality may experience less price volatility compared to others, or why certain properties may be more resistant to changes in market conditions.

Moreover, the study may provide valuable insights for property owners, investors, and policymakers, who need to understand the dynamics of the property market to make informed decisions. By understanding the underlying economic factors that affect the property market, these stakeholders can better anticipate changes in property values, plan their investment strategies, and formulate policies that promote stability and growth in the market.

In summary, the study offers a comprehensive analysis of the property market from an economic perspective, with the aim of providing a better understanding of the factors that affect price dynamics and rigidities of different types of properties. The insights provided by the study can be valuable for a wide range of stakeholders and can inform decision-making processes in the property market.

In our study, we defined the following research questions:

How has the significant turnover in the Czech Republic’s real estate market in 2022 impacted the overall economy and housing affordability?

To what extent has the increase in mortgage prices influenced the decline in new mortgages and completed real estate transactions?

How do the price cycles and recovery rates in the property market differ between poorer regions, such as the Karlovy Vary region, and more affluent regions, such as Prague?

What role has the war in Ukraine played in the increasing demand for rental properties in the Czech Republic, and how might this affect the long-term housing market?

How will the anticipated deterioration of the macroeconomic situation impact the availability of owner-occupied and rental housing in different regions of the Czech Republic?

2. Literature Review

The specific characteristics of properties make the property market particularly susceptible to disequilibrium. Unlike other goods, properties have unique features that make them difficult to compare with other goods in the market. Properties have a fixed location, size, and other intrinsic characteristics that cannot be easily replicated or duplicated. This lack of comparability makes it difficult to achieve a neoclassical equilibrium in the property market. Case [

16] argues that the arbitrage on the property market is costly as property acquisition is connected to the transaction and maintenance costs and tax burden. Gilber [

17] adds that risk aversion, high value, and low liquidity of properties compared to other investments make the property reservation price highly specific and differing for each buyer. Real estate is seen as the best store of value in times of high inflation [

18], volatile markets [

19], and insufficient pension system [

20], as properties, attract investors under uncertainty at stock markets, as well as for diversification purposes [

21]. In this regard, the decision to buy a property is made independently of the potential profit from its rental. This is an important feature for understanding property price formation as property price is less dependent on its yield than financial assets [

22]. Property prices will increase all the time, and investors believe in their future continuous increase. An inertial trend of property prices has been confirmed by Case or Leinberger [

23,

24]. All the mentioned factors may induce a biased perception of property price by the buyer which, in combination with the inelastic supply of new properties, stands behind property price fluctuation during the property price cycle, thus property prices tend to fluctuate around the reproduction value of the property, which is the cost of replacing the property with a similar one. This reproduction value is influenced by a range of factors, such as the cost of construction, land prices, and other factors that influence the cost of replacing the property. As a result, property prices are subject to significant swings in response to changes in market conditions.

Vast research has been published exploring fluctuations of property prices and property market rigidities in relation to the affordability of housing, a contentious issue of current policy debates. Cetin and Yildirim [

25] examined the determinants of house prices and their effect on housing affordability. The authors found that factors such as income, mortgage interest rates, and macroeconomic indicators have a significant impact on housing affordability, and that measures such as subsidies and tax exemptions can help to improve affordability. Zeng and Liu [

26] analyzed the relationship between housing prices and economic growth in China. The authors found that housing prices are positively related to economic growth, and that measures such as increased housing supply and improved access to mortgage credit can help to address housing affordability issues. Oyekale and Alamu [

27] explored the affordability of rental housing. The authors found that rental housing is unaffordable for many households, particularly those with lower incomes, and that government policies such as subsidies and rent control can help to improve affordability. Gholizadeh and Zare [

28] examined the relationship between apartment prices and urban development. The authors found that factors such as population growth and urbanization contributed to increases in apartment prices, and that measures such as improved urban planning and increased housing supply can help to address affordability issues. A study by Natarajan et al. [

29] explored the impact of COVID-19 on the rental housing market. The authors found that the pandemic led to decreased demand for rental housing, particularly in urban areas, and that measures such as rent subsidies and eviction moratoriums can help to address affordability issues.

Stec, Grzebyk and Pierścieniak [

30] highlight the importance of understanding socio-economic development in EU countries, which has direct implications for the real estate market. By examining factors such as demographic and labor market potentials, economic, social, and technical potentials, the authors provide insights that can help assess the dynamics and performance of the real estate market in these countries.

Within this broader context, we expect the cheaper property segment and region with lower property prices to suffer from depressed demand more severely; these price cycle fluctuations will happen with greater magnitude. We expect to find also a greater downward rigidity of prices in the high-priced region. The analysis to follow uses primary data for testing the mentioned hypothesis.

We managed to find several articles that deal with real estate market research at the regional level. For example, Bangura and Lee [

31] explore house price linkages between Greater Sydney and coastal cities in NSW, Australia, finding strong connections with the Illawarra region but not the Hunter region. The results highlight the importance of spatial connectivity and migration patterns in shaping regional housing markets, with potential policy implications for addressing imbalances between growth areas. Yoshida and Kato [

32] investigate housing affordability in Osaka Prefecture, Japan, finding that both the quantity and quality of affordable private rental apartments for multiple households are problematic, with a decline in the role of old wooden low-rent housing and limited availability of larger units for low-income groups. Bangura and Lee [

33] examine homeownership affordability determinants in Greater Sydney using LGA data, finding that while house price and median personal income are key drivers across all regions, Western Sydney is more sensitive to these factors and additional determinants, emphasizing the importance of submarket analysis. Bin, Gardiner and Liu [

34] propose a regional house price mining and forecasting (RHPMF) framework to analyze the spatial distribution and temporal evolution of urban real estate markets, using context-aware matrix factorization and demonstrating its effectiveness through case studies in Virginia Beach, Philadelphia, and Los Angeles. Ploessl and Just [

35] examine the relationship between news coverage and sentiment and residential real estate prices in Germany at a regional level, finding that news-based indicators significantly impact prices and can lead them up to two quarters, potentially reflecting investor sentiment, and demonstrating the value of quantifying qualitative data from texts.

3. Materials and Methods

In the following text, figures based on source data from the EVAL software are displayed. The EVAL software collects data from real estate advertising from the entire Czech Republic. Data collection is carried out regularly in a period of once a month since 2007. Data on apartments for sale and apartments for rent are recorded. All recorded data is checked for data reliability. The EVAL software also collects data on changes made in Cadaster of Real Estate. Cadaster of Real Estate of the Czech Republic is a set of data about real estate in the Czech Republic, including their inventory and description and their geometric specification and position. Parts of it are records of property and other material rights and other legally stipulated rights to these real estates. Cadaster of real estate contains many important data about parcels and selected buildings and their owners. It is thus possible to identify increases or decreases in real estate transactions anywhere in the Czech Republic. Various statistical outputs can be generated from the obtained data.

The EVAL software was developed by one of the co-authors of this article in 2007. Since then, it has gone through many updates. This is specialized software used at CTU in Prague. This software is not available for general use to other potential customers. There are also no plans to offer this software to the general professional public. More detailed information about the functioning of the EVAL software can be found in older articles by the co-authors of this article.

The Czech Republic offers its citizens various types of housing, from apartments to family houses. The most widespread type of housing in the Czech Republic is apartments, which are often found in large cities and urban areas. These apartments can range in size from small studio apartments to large multi-bedroom units. Another popular type of housing is townhouses, which are often found in suburban areas and represent a middle ground between apartments and single-family homes. Single-family homes are also available in the Czech Republic but are usually more expensive and often found in rural areas. This article analyzes flats and apartments in all cities and towns in the Karlovy Vary Region and the Prague Region.

The EVAL software is structured into several sub-modules that work together:

Internet link collection module.

Module for downloading full text of advertisements and exporting data.

Module for filtering data.

Module for data evaluation.

3.1. Internet Link Collection Module

This part of the software tool systematically crawls the real estate internet servers and records current internet links to real estate sales or rental offers in the database.

3.2. Module for Downloading Full Text of Advertisements and Exporting Data

This part of the EVAL software has the task of automatically downloading the full text of the advert by machine and exporting data from the text of the recorded adverts to enable further statistical evaluation of the development of the real estate market. For each property category under study, a custom data structure has been defined, which is exported/retrieved from the texts of the recorded advertisements.

3.3. Module for Filtering Data

The database files created by the Module for downloading the full text of advertisements and exporting data are then analyzed for data veracity. Each recorded quote is thus assessed in terms of objectivity and correctness of the presented information, completeness of the presented information, etc. In the event of irregularities being detected, the bid under consideration is excluded from further statistical processing.

3.4. Module for Data Evaluation

This part of the EVAL software creates source documents for the creation of statistical reports describing the development of the real estate market according to the user’s requirements. The time evolution and dependencies between many monitored real estate parameters are examined.

4. Results and Discussion

4.1. Availability of Owner-Occupied Housing

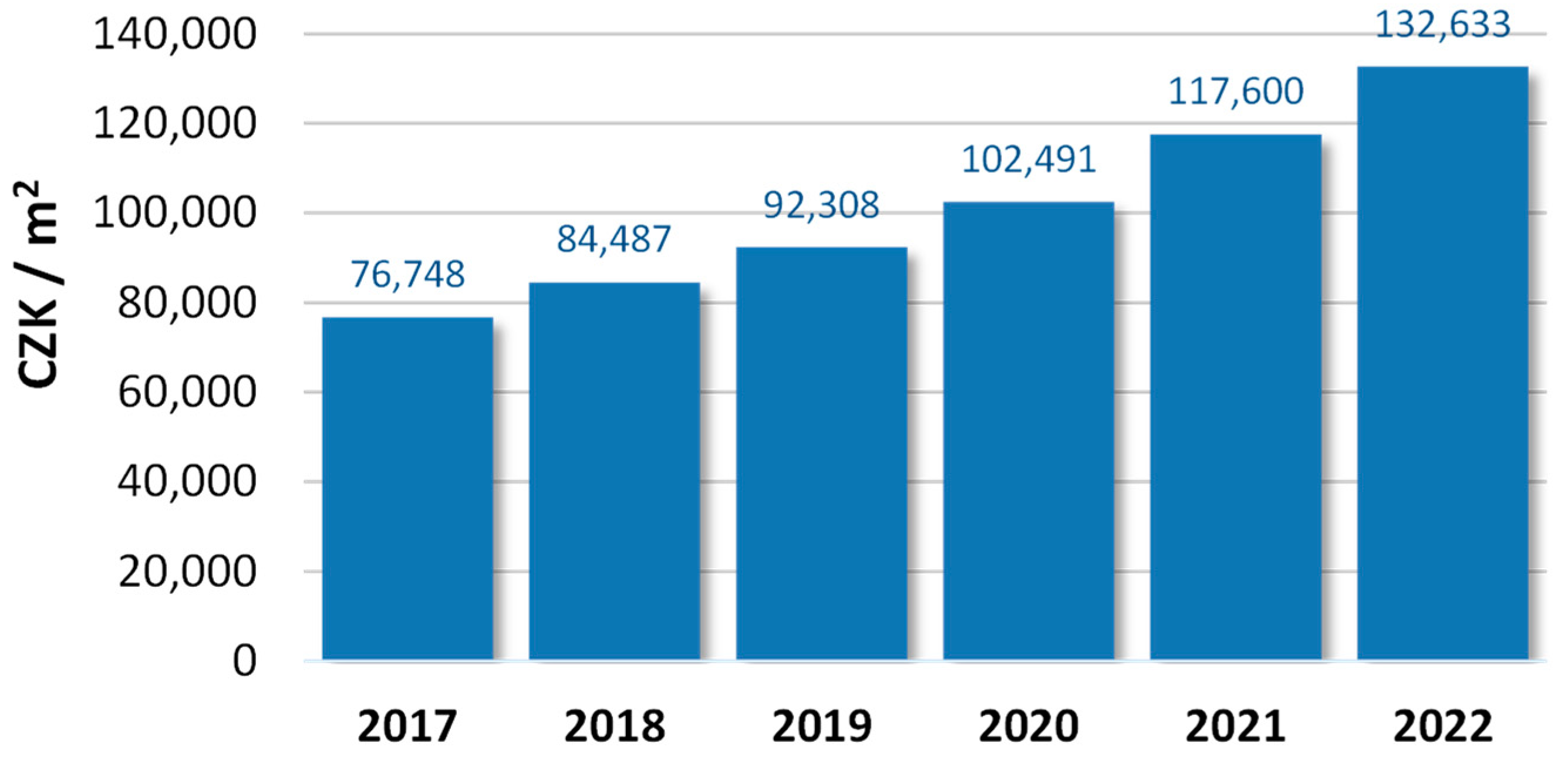

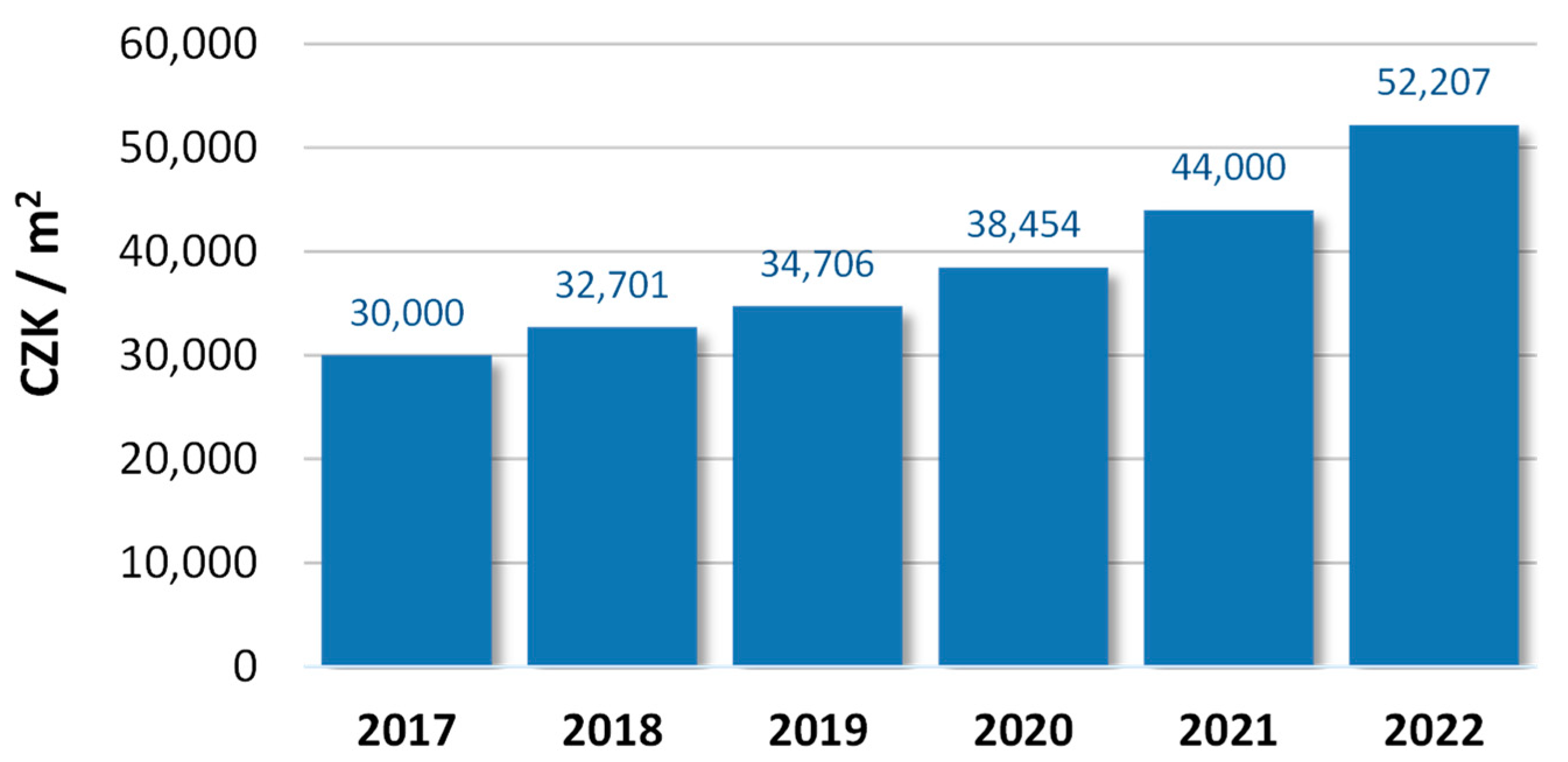

Figure 2 and

Figure 3 show the differences in the availability of owner-occupied housing in the Prague region and the Karlovy Vary region. The blue columns show the median offer price for one square meter of the apartment’s floor area. There are significant differences in the price level between the Prague region and the Karlovy Vary region. This is due, among other things, to significantly better job opportunities in Prague and the wider availability of services. During the years 2017 to 2022, there was a significant increase in the price level in both regions, reflecting the trend of overall property appreciation across Europe.

Property price appreciation in Prague has been observed to a larger extent, in nominal and also in relative terms. The values in the white box show how many years are needed to save for an older average apartment with a floor area of 70 square meters. At the same time, additional entry costs of CZK 350,000 are expected, which will be used to put the apartment into proper use. The calculation also includes the average wages in both regions for individual years, which were taken from the data of the Czech Statistical Office. It is assumed that the entire earnings will be used to pay off the apartment.

When comparing both regions, we find that the availability of owner-occupied housing is significantly worse in the Prague region. Currently, it takes 17.9 years of savings to attain the average older apartment with a floor area of 70 square meters. In addition, the situation in the Prague region has significantly worsened over the last five years. There is a gap between household income and the purchase price of real estate. Real estate thus becomes less affordable, which leads to the fact that a greater number of households will use rental housing.

In the Karlovy Vary region, the availability of owner-occupied housing is also deteriorating over time, but the situation is deteriorating significantly more slowly (9.8 years in 2022). In the Karlovy Vary region, a person with an average salary can reasonably afford to own his/her housing if he/she is interested in owning. In contrast, this rule no longer applies to the Prague region.

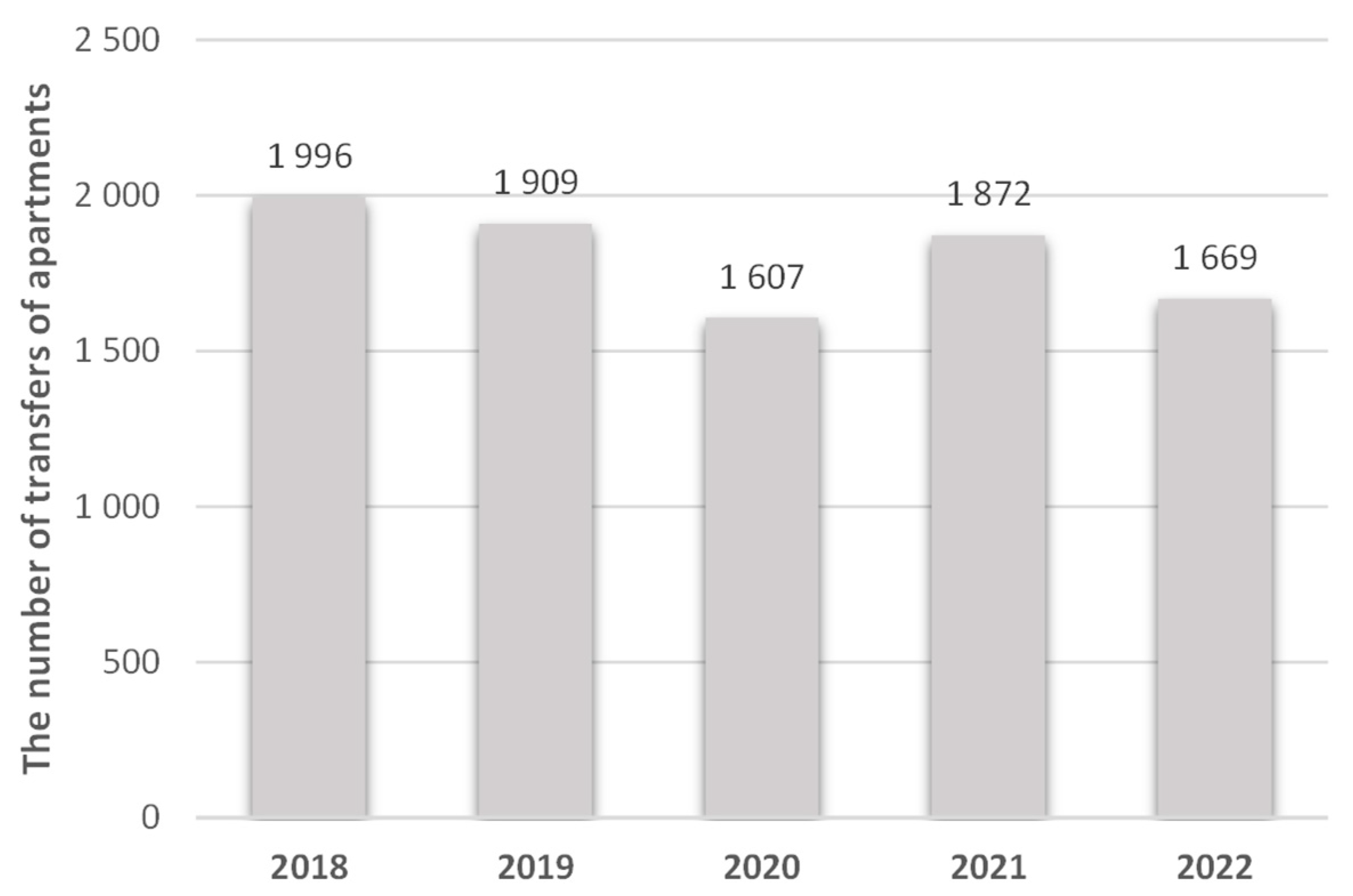

4.2. Apartment Ownership Changes

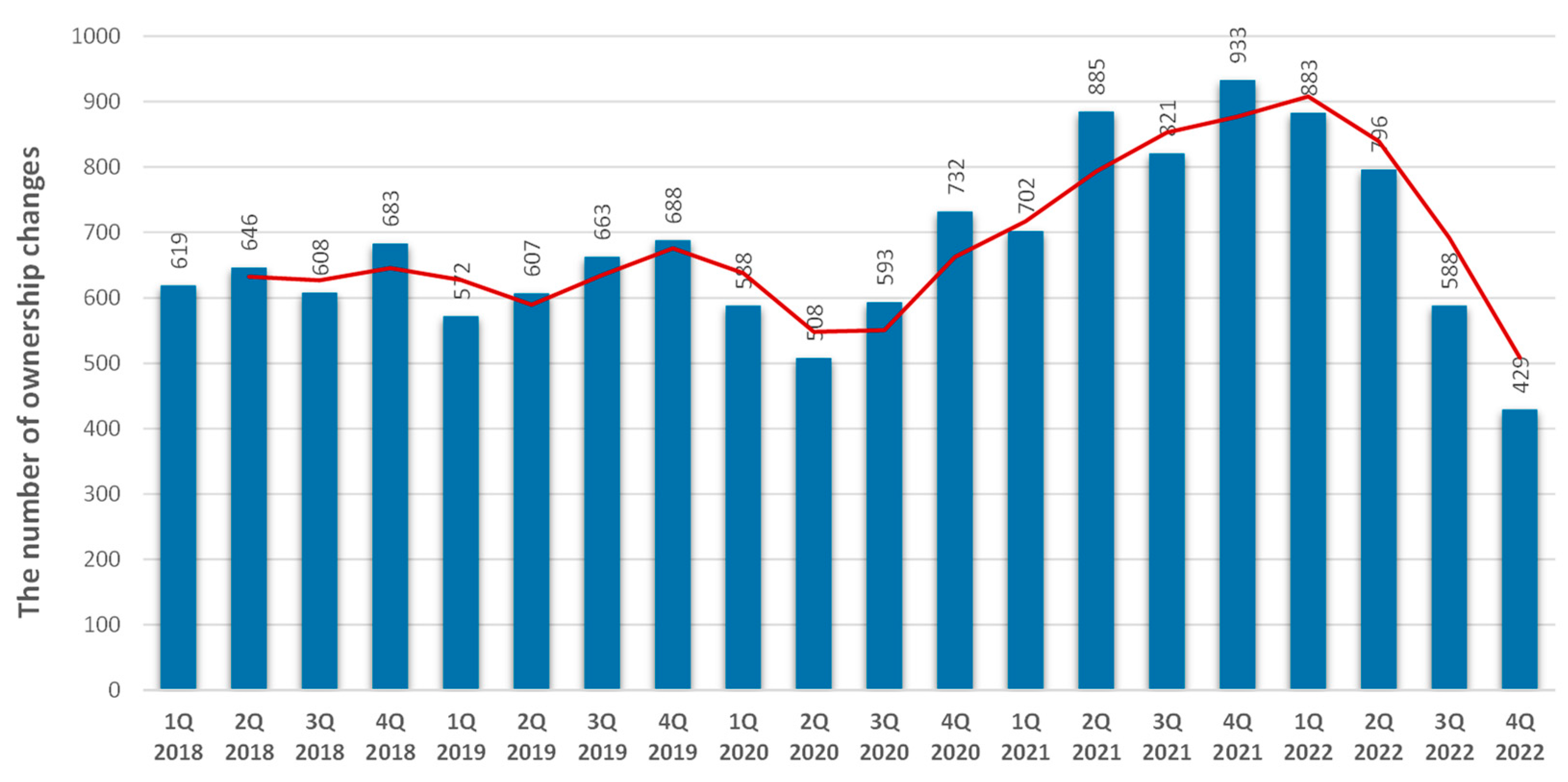

Figure 4 and

Figure 5 show how many changes in apartment ownership occurred in individual quarters between 2018 and 2022 in both monitored regions. The values shown represent the actual number of transactions as recorded by the Cadaster of Real Estate. These are only changes of ownership, for which the Cadaster of Real Estate also recorded information about the purchase price of the property. This means that these figures do not capture ownership changes related to gifts and inheritance of real estate, as these transactions are made independently from property prices. The red curve shows the trend line in the form of a moving average (period 2).

During the COVID-19 pandemic, a significant increase in real estate transactions can be observed. This is due to a number of factors including, for example, more time the investors had for exploring new investment opportunities. In addition, many households received unexpected support from the state, and at the same time spending opportunities were significantly limited. In consequence, households’ savings increased significantly [

36]. Furthermore, there was concern about the impending high inflation, so investors looked for all potential investment opportunities that would ensure the preservation of the value of their capital. Real estate was considered the best instrument.

In response to high inflationary pressures, the Czech National bank adopted various measures tightening the so far loose monetary policy specified in the following text. The property market reacted strongly. In the second half of 2022, there was a significant turnover in the real estate market and a significant decrease in transactions. During this period, there was a sharp increase in interest rates for mortgage loans and thus at the same time a reduction in the availability of owning housing. At the same time, households’ concerns about the recession are growing.

If we compare the number of transactions per person, we find that in the Prague region, there is an average of one real estate transaction per quarter per 370 inhabitants, while in the Karlovy Vary region there is only one real estate transaction per quarter per 1892 inhabitants. It was confirmed that the wealthier the region, the greater the turnover in the real estate market.

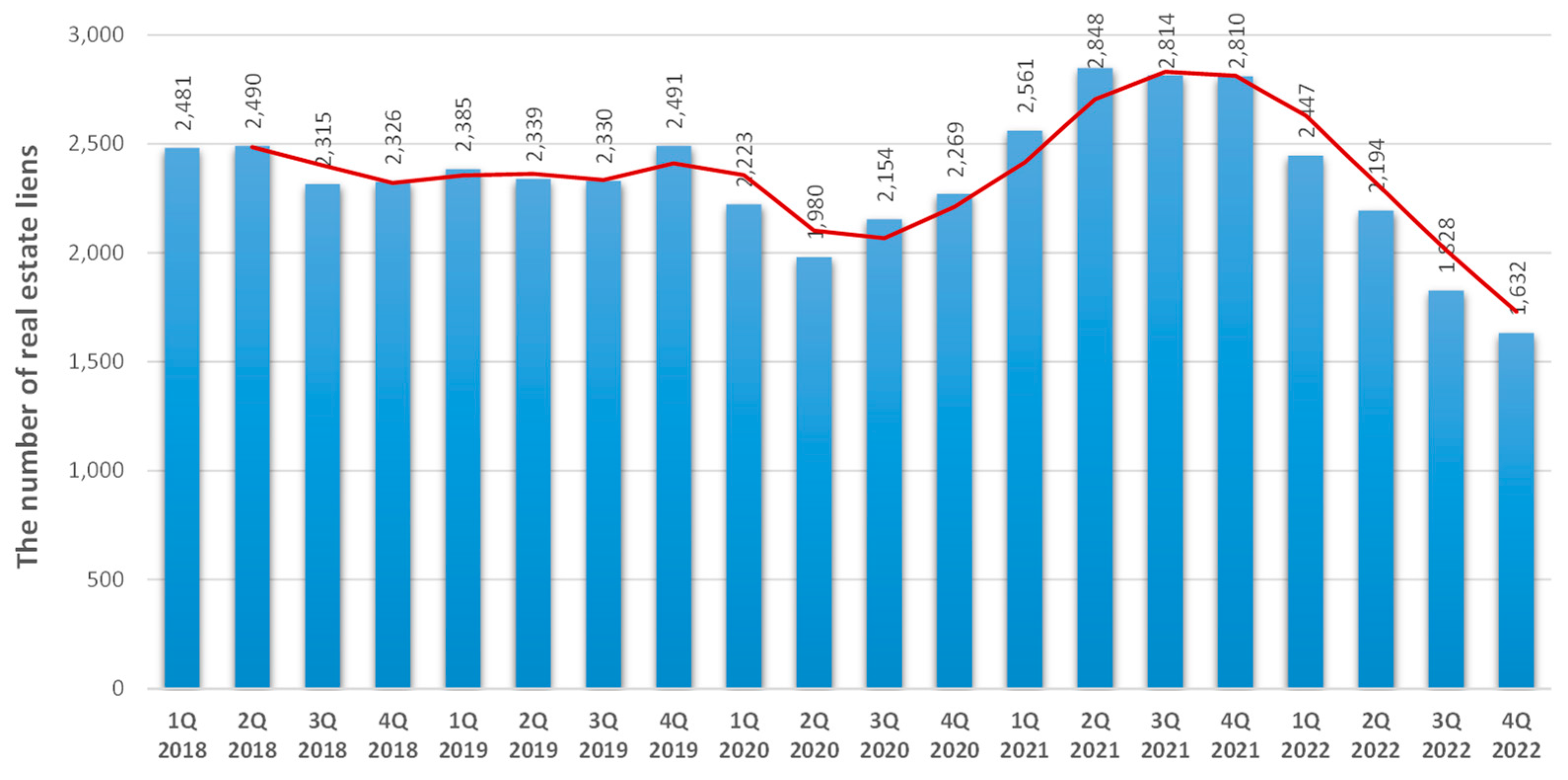

4.3. Real Estate Liens

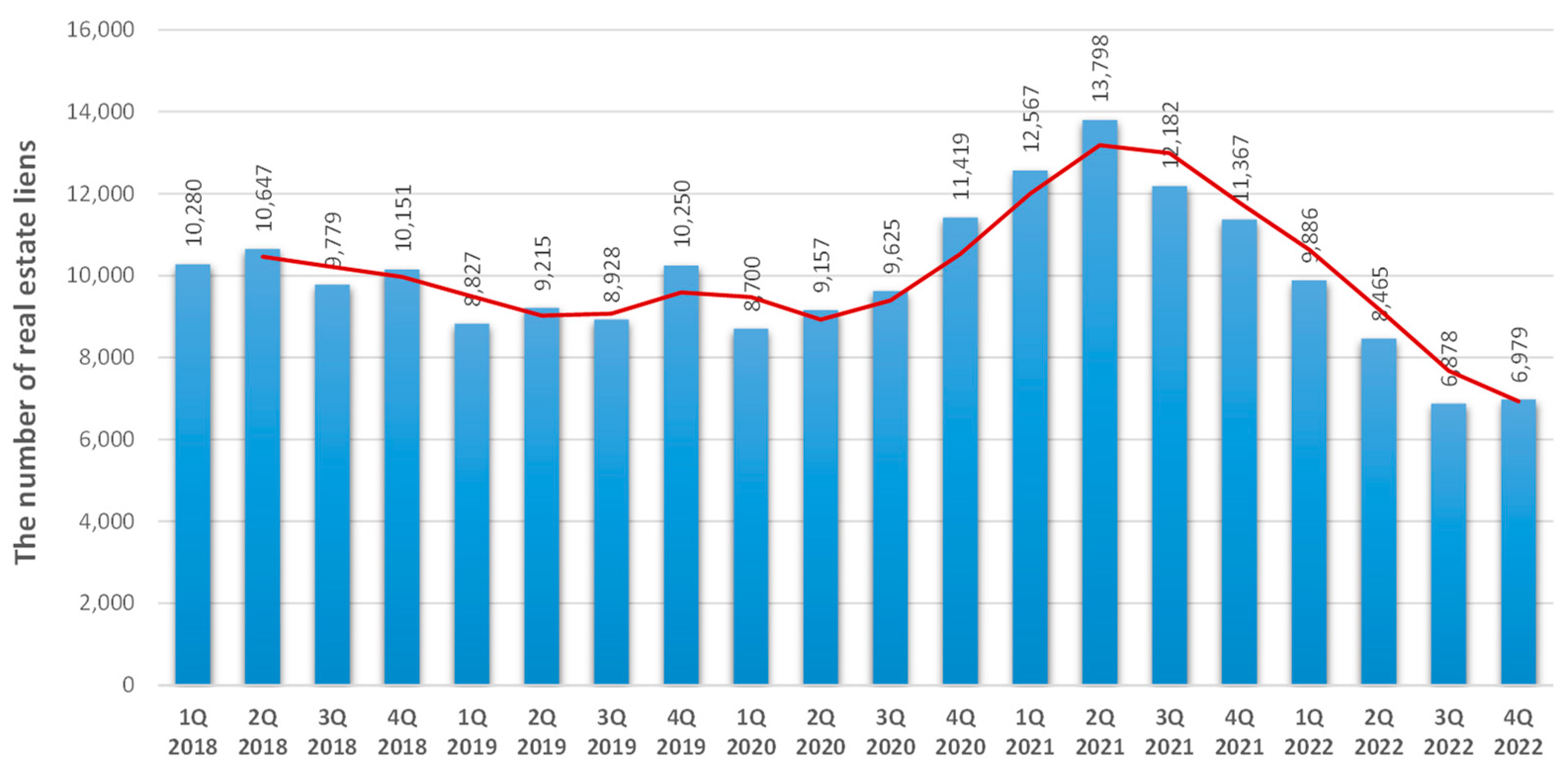

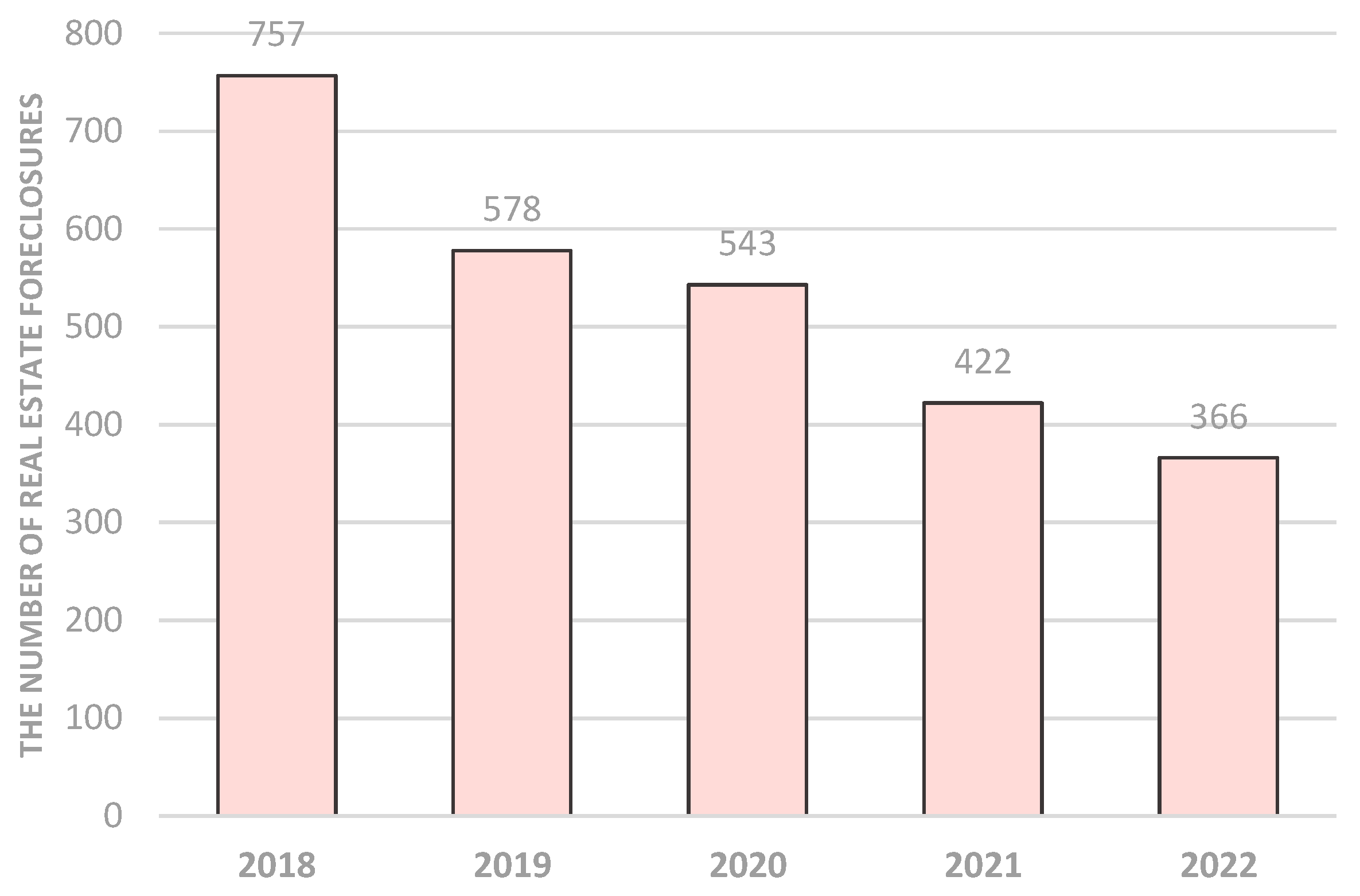

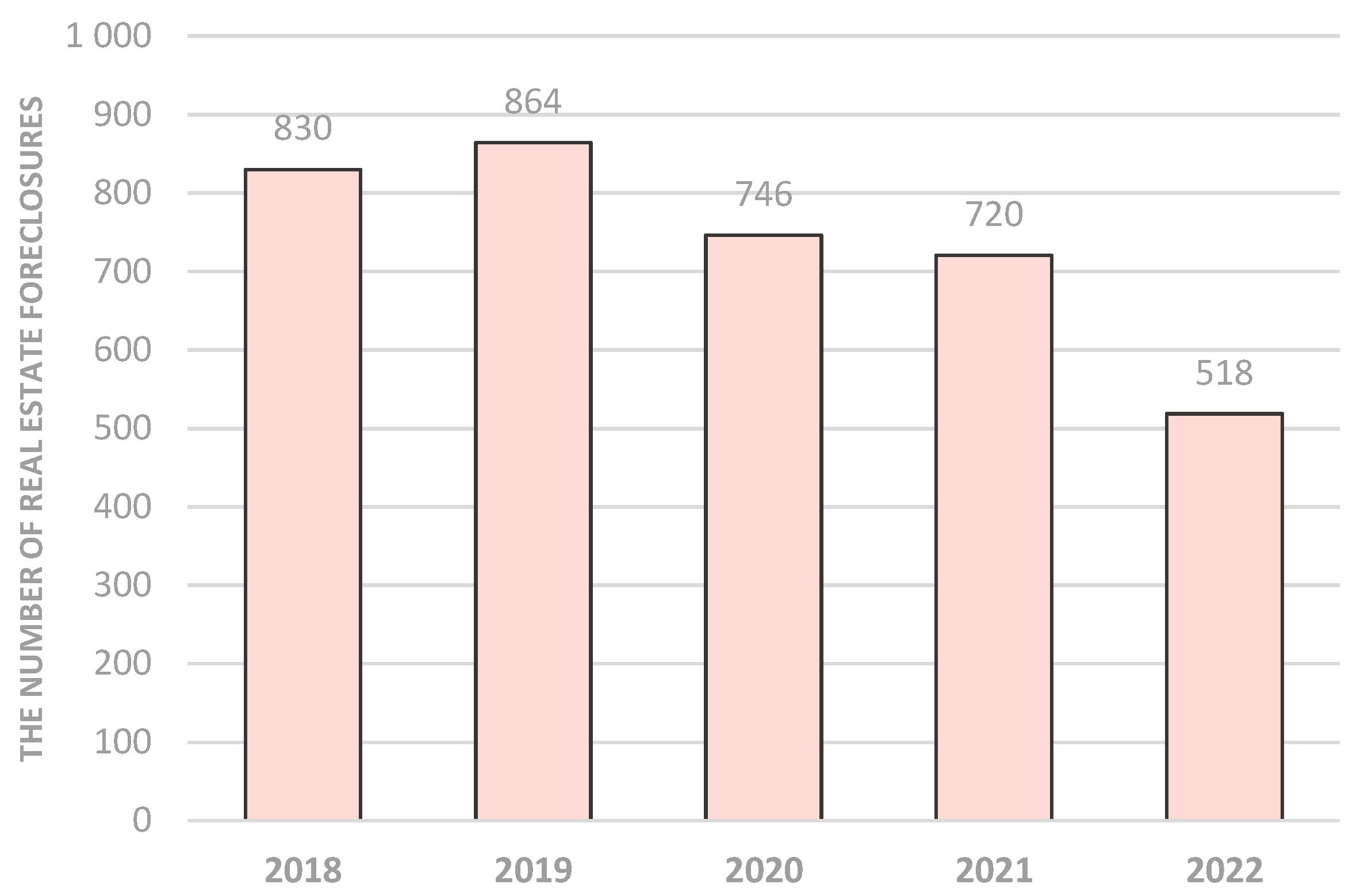

Figure 6 and

Figure 7 show the number of new entries of the right of lien (pawn right) on real estate without distinguishing between the type of real estate and new loans or loan refixations. The figures depict rights of lien relating to apartments, commercial real estate and land. Unfortunately, it was not possible to filter out separate data concerning only liens of apartments from the source data. Publicly accessible data in the Cadaster of Real Estate have a specific structure that does not provide this information.

The data shows a significant drop in the number of newly granted real estate loans from mid-2022. This is due to the fact that the Czech National Bank significantly raised the base interest rates (2-week repo rate: 2017—0.25% p.a., 2022—7.00% p.a.) and at the same time tightened the conditions for providing mortgages [

9]. For that reason, people who can take out a mortgage have been significantly reduced, and the property market split one into a supported social rental housing available for households whose housing spendings are above a threshold of 35% of their net salary, and second into apartments for high-income households. The middle class has almost lost all hope of buying their homes. Currently, this is a contentious issue above all for the young generation. The high price level of real estate also works against potential borrowers. In 2021, for a typical development project, it was estimated that 40% of the apartments were sold for cash and 60% were sold with the use of a mortgage. At the end of 2022, this ratio has changed significantly so that more than 80% of apartments are sold for cash. Currently, only creditworthy investors and borrowers operate in the real estate market [

37].

By comparing data from both monitored regions, we find that the drop in the number of liens is higher in the Prague region. This is caused by the fact that real estate prices in Prague are very high, and people are forced to borrow higher amounts and thus more easily fall out during the assessment of creditworthiness by the bank.

Following our analysis, we anticipate a more significant and broader scope of the price cycle in the economically weaker region (Karlovy Vary region, as per our study) and a sluggish rebound of the property market, which validates the presence of slow market adjustment processes and persistent imbalances in the property market. Simultaneously, we can observe greater resistance to price decreases in the luxury segment of the property market and in the region with higher property prices (Prague).

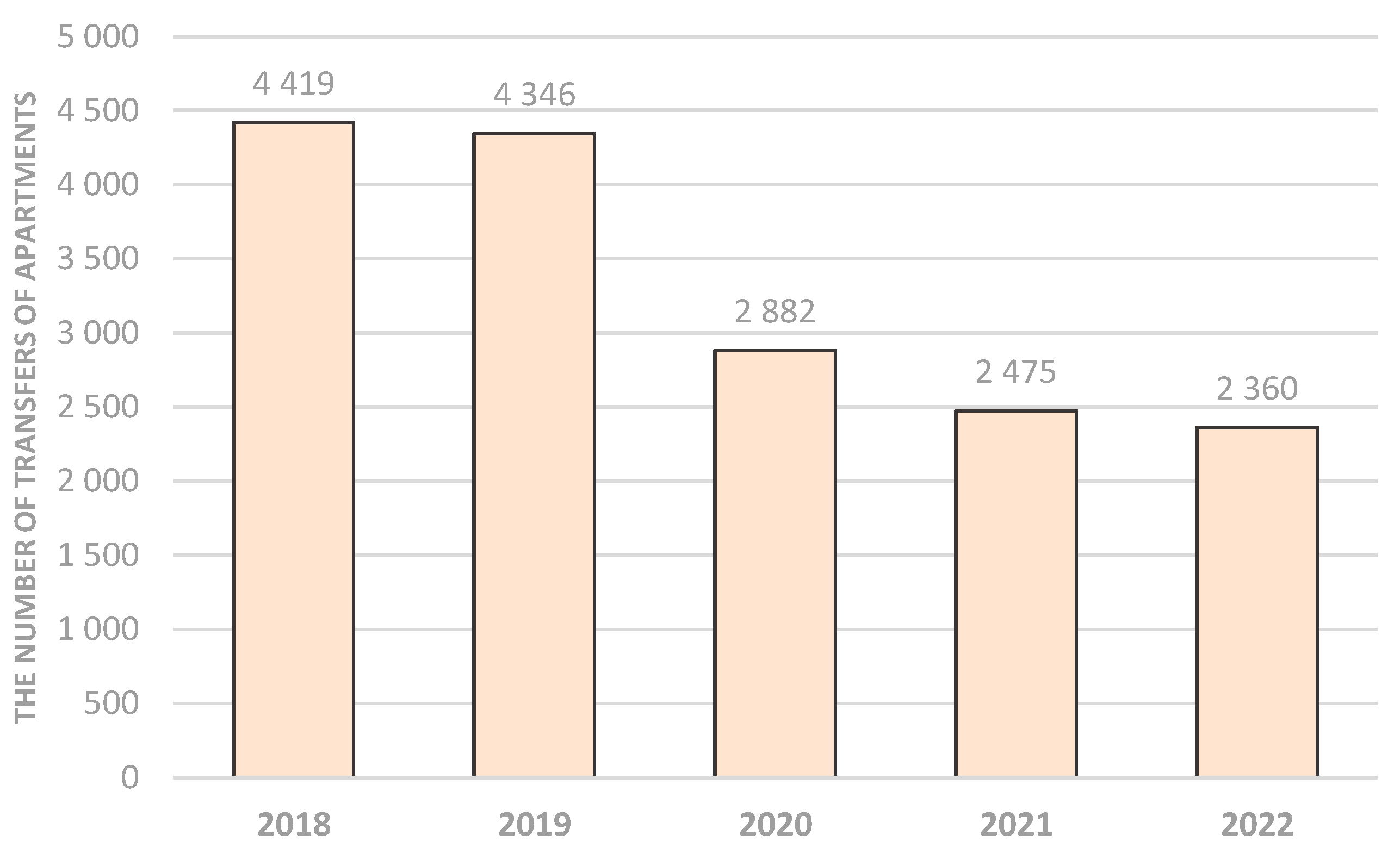

4.4. Transfers of Apartments from Housing Cooperatives to Private Ownership

There are two basic forms of apartment ownership in the Czech Republic: personal apartment ownership and cooperative apartment ownership.

Personal apartment ownership has a fundamental advantage in that the new owner is rewritten in the Cadaster database (through the registration of her/his ownership right) and the new owner can do whatever he wants with the apartment, for example, he can use it as collateral to arrange a mortgage or rent this apartment to any tenant.

Cooperative apartment ownership means that the real owner of the entire apartment building is the housing cooperative, and the user of this apartment acts only as a tenant of the apartment. The user of the apartment is also a member of the housing cooperative and has various rights and obligations associated with this apartment and a share in the ownership of the housing cooperative. The basic disadvantage is that he cannot use this apartment as collateral to arrange a mortgage. At the same time, the possibilities of further subletting this apartment are limited. In some cases, the management of the housing cooperative must agree with the subtenant.

Due to these advantages and disadvantages, the market value of personally owned apartments is approximately 10 to 20 percent higher than cooperatively owned apartments.

Figure 8 and

Figure 9 show the number of transfers of apartments from housing cooperatives to personal ownership. Over time, many housing cooperatives have been disappearing and being replaced by personal ownership of individuals. Many active co-owners of apartment buildings are pushing to the management of housing cooperatives for the transfer to personal ownership. This pressure is higher in locations with a higher real estate price level. In the Prague region, this process is slowly coming to an end, because most of the housing cooperatives have already disappeared, but in the Karlovy Vary region, we can still observe the continuation of this process.

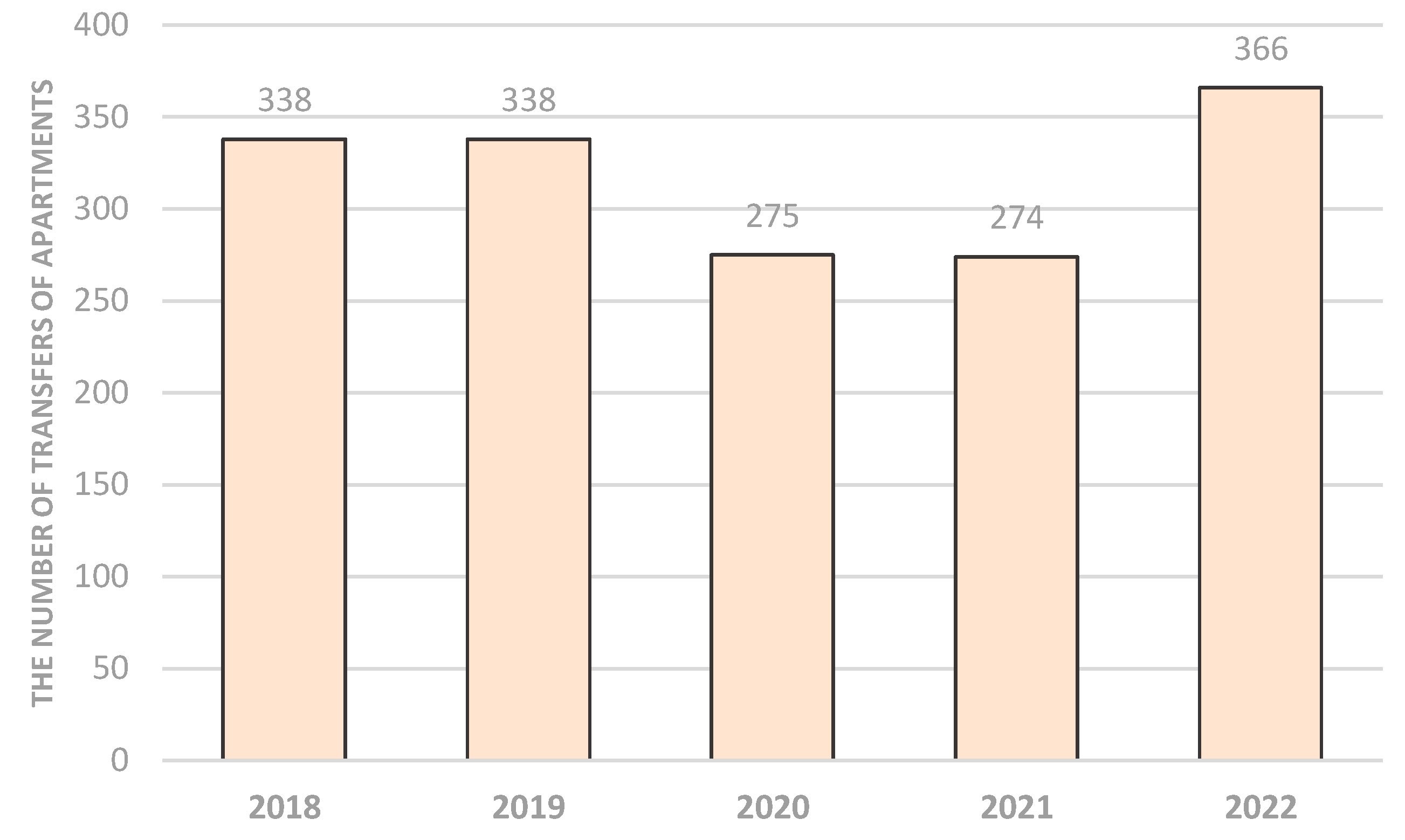

4.5. Transfers of Apartment Ownership from the State and Municipalities to Personal Ownership

After 1990, there were significant changes in the ownership of apartments in the Czech Republic. Until 1990, most apartments were owned by the state and municipalities. However, after 1990, the state and municipalities sold these apartments to existing tenants on a large scale in the process of privatization [

38]. The main reasons included the very neglected technical condition of the housing stock, a high degree of rent regulation, many problems with tenants (non-payment of rent, damage to the apartment, complaints from neighbors, etc.), and high operating costs for maintaining the housing stock [

39].

The existing tenants were very interested in buying the apartments, as the purchase price was very low and did not correspond to the normal market value. The main part of the apartment privatization ended around 2015 and since then only a limited number of apartments have been sold to existing tenants.

Privatization of apartments took place on such a large scale that, especially in large cities, there is now a negative situation where the cities currently lack social apartments, which are needed for key professions that ensure the running of the city (teachers, policemen, firefighters, nurses, etc.). Currently, cities are starting new construction of social housing. However, these new apartments must meet current technical standards, and the costs of their construction are thus very high. It is obvious that city management has not thought strategically in the area of apartment privatization in the long term. As mentioned above, the most affected group of residents are young adults, who no longer have a chance to acquire an apartment in personal ownership under favorable conditions, because there is nothing to transfer anymore.

Figure 10 and

Figure 11 show the development of the privatization of apartments between 2018 and 2022. For both regions, the list includes only those authorities that implemented more than 20 apartment transfers per year.

4.6. Real Estate Foreclosures

Figure 12 and

Figure 13 describe the development of the number of real estate foreclosures in both monitored regions. Even though the economic situation is worsening, and unemployment is slightly increasing, the number of real estate foreclosures is decreasing, especially in the Prague region. We see the cause of this phenomenon in the fact that during the COVID-19 pandemic, the state provided large social benefits to all citizens, which increased household savings. Currently, however, these savings have already decreased significantly, and the liquidity of households, partly also due to unprecedented inflation, can be expected to worsen.

In general, however, the number of properties in foreclosure in the Czech Republic is very low compared to other EU countries. Overdue rent or mortgage payments in 2020 in the Czech Republic concerned only 1.7% of debtors, in the EU it was 3.2% of debtors [

40].

Between 2015 and 2020, many people in the Czech Republic took out a mortgage at very low-interest rates, when they agreed on a refixation period, usually between five and eight years. This period will gradually end for them, and they will have to negotiate a new mortgage agreement under new conditions, when two to three times higher interest rates can be expected. The current average interest rate for mortgages is 6.34% p.a., while in May 2021 this rate was at 2.4% p.a. [

41]. A deterioration in the repayment of mortgages can therefore be expected in the near future.

5. Conclusions

This paper documents that in 2022 there was a significant turnover in the real estate market in the Czech Republic. Due to the remarkable increase in the price of mortgages, the number of new mortgages and the number of realized real estate transactions fell significantly. Currently, buyers are waiting to see if there will be a drop in real estate prices, and the real estate market as a whole has frozen. Based on our analysis, we expect a bigger and wider magnitude of the price cycle in the poorer region (the Karlovy Vary region in our analysis) and slower recovery of the property market, confirming slow market adjustment mechanisms and long-lasting disequilibrium present on the property market. At the same time, a higher downward rigidity in prices can be observed in the high-end segment of the property market and also for the high property priced region (Prague).

Beyond our analysis, a currently resonant issue is the affordability of owner-occupied housing is decreasing due to very high real estate prices and high interest rates for mortgages. The consequence is an increased demand for rental properties. The significant growth in demand for rental properties was also supported by the war in Ukraine, when the Czech Republic provided housing to a very high number of refugees compared to other EU countries.

In the next period, due to the deterioration of the macroeconomic situation, a further deterioration in the availability of owner-occupied and rental housing can be expected. Bigger problems in the real estate market will occur in poorer regions of the Czech Republic, which include, for example, the Karlovy Vary region.

,

,

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}