The Capitalization of School Quality in Rents in the Beijing Housing Market: A Propensity Score Matching Method

Abstract

:1. Introduction

2. Literature Review

2.1. School Quality Capitalization

2.2. Measurements of School Quality Capitalization and Treatment Effects Analyses

2.3. “Tenant Discrimination” in the Housing Market of China

2.4. School Quality Capitalization in China

3. The Case of Beijing

3.1. Rental Housing Market and the Equitable Housing Policy

3.2. Beijing Primary School Enrollment Policies

4. Data and Models

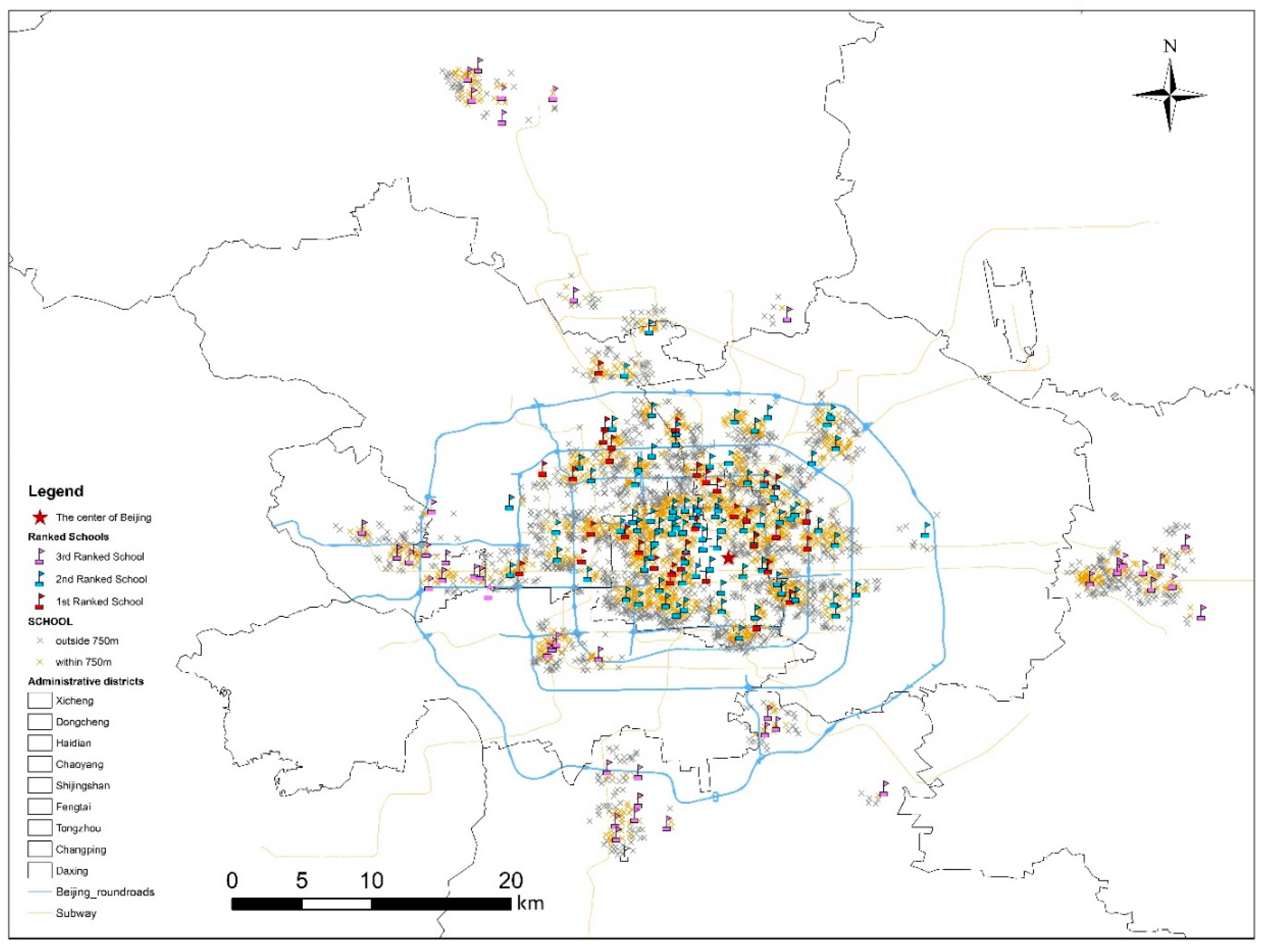

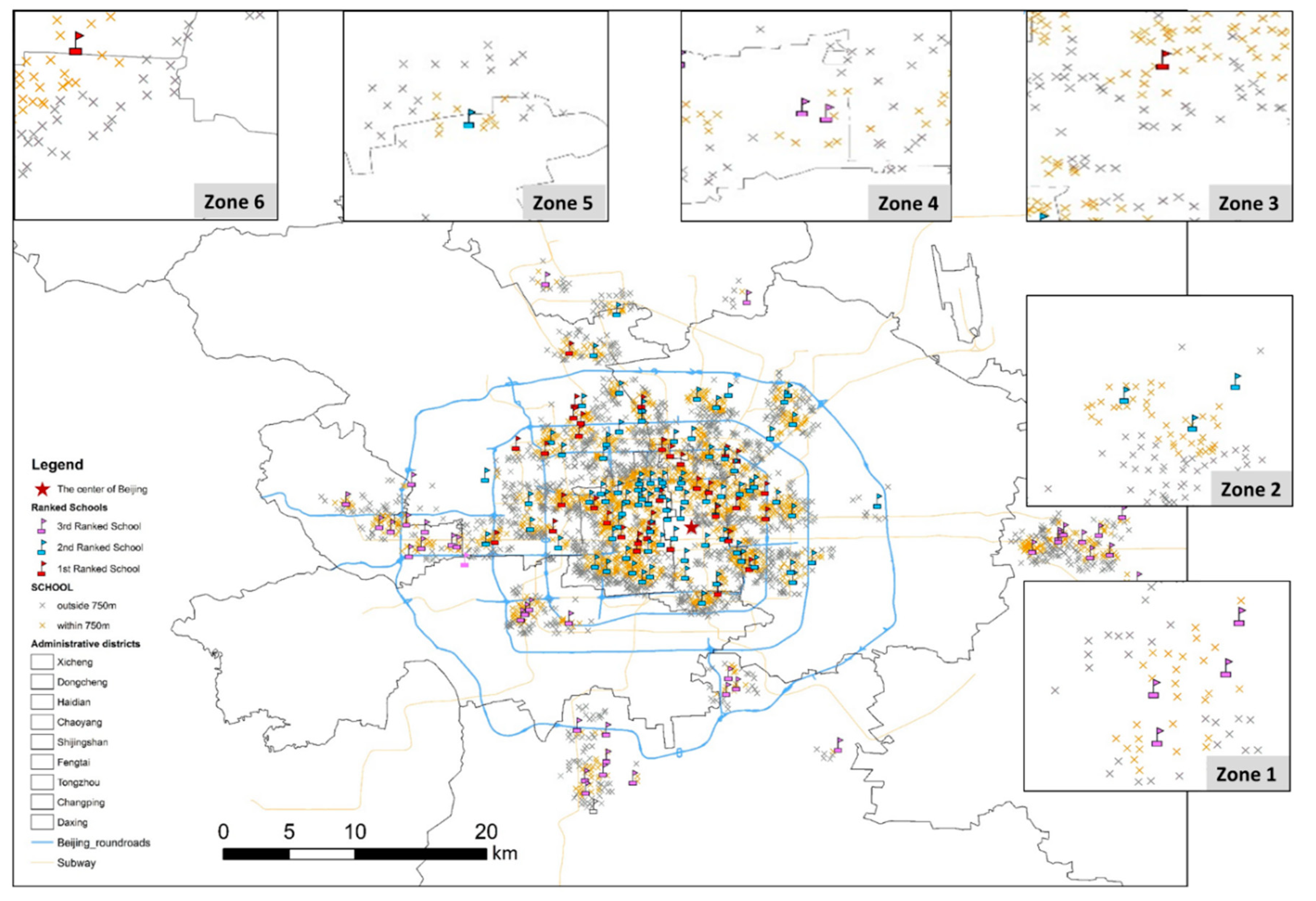

4.1. Study Area and Data

4.2. The Hedonic Rent Model

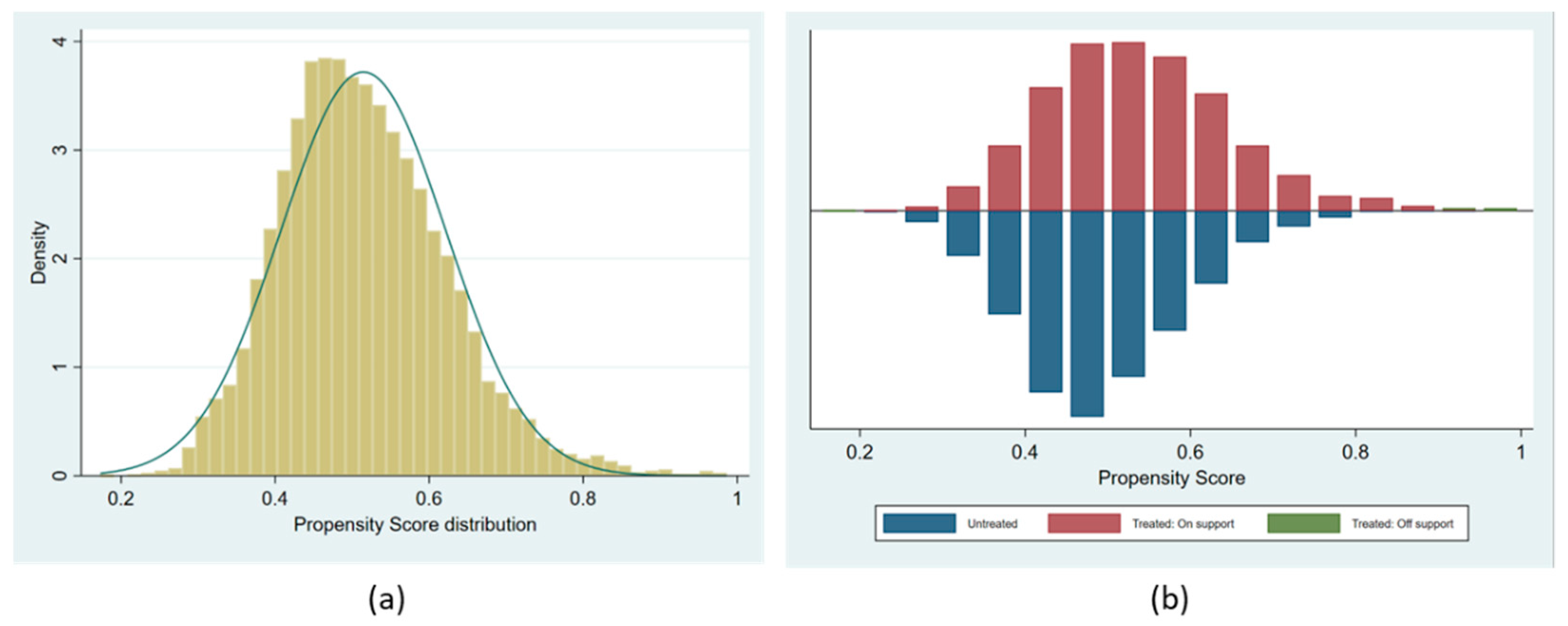

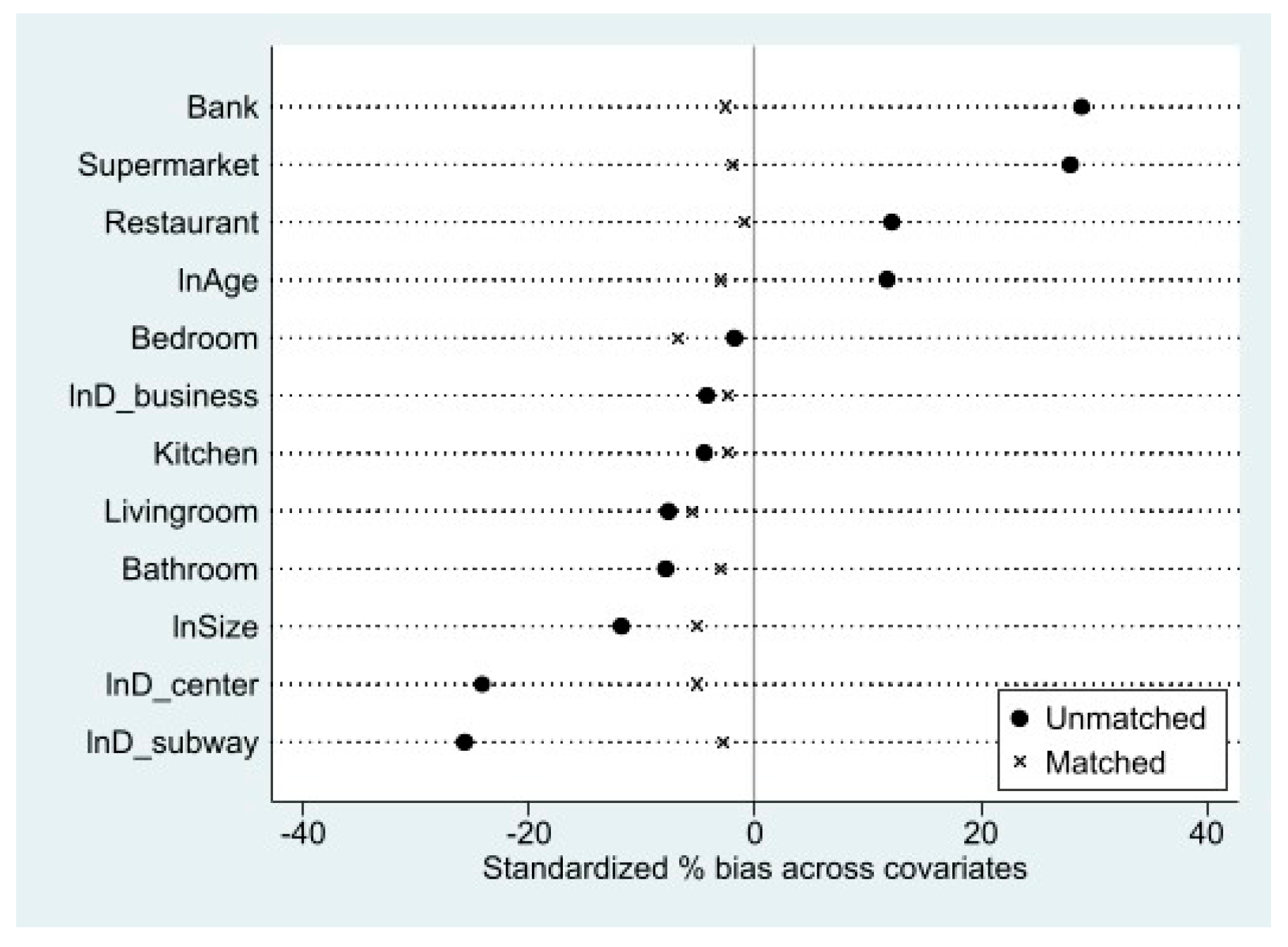

4.3. The Propensity Score Matching (PSM) Method

5. Results

5.1. The Baseline Regression Results

5.2. Model Misspecification Adjustment

5.3. Heterogeneity Analysis of School Quality Capitalization

5.3.1. Differences in Ranked Schools’ Capitalization

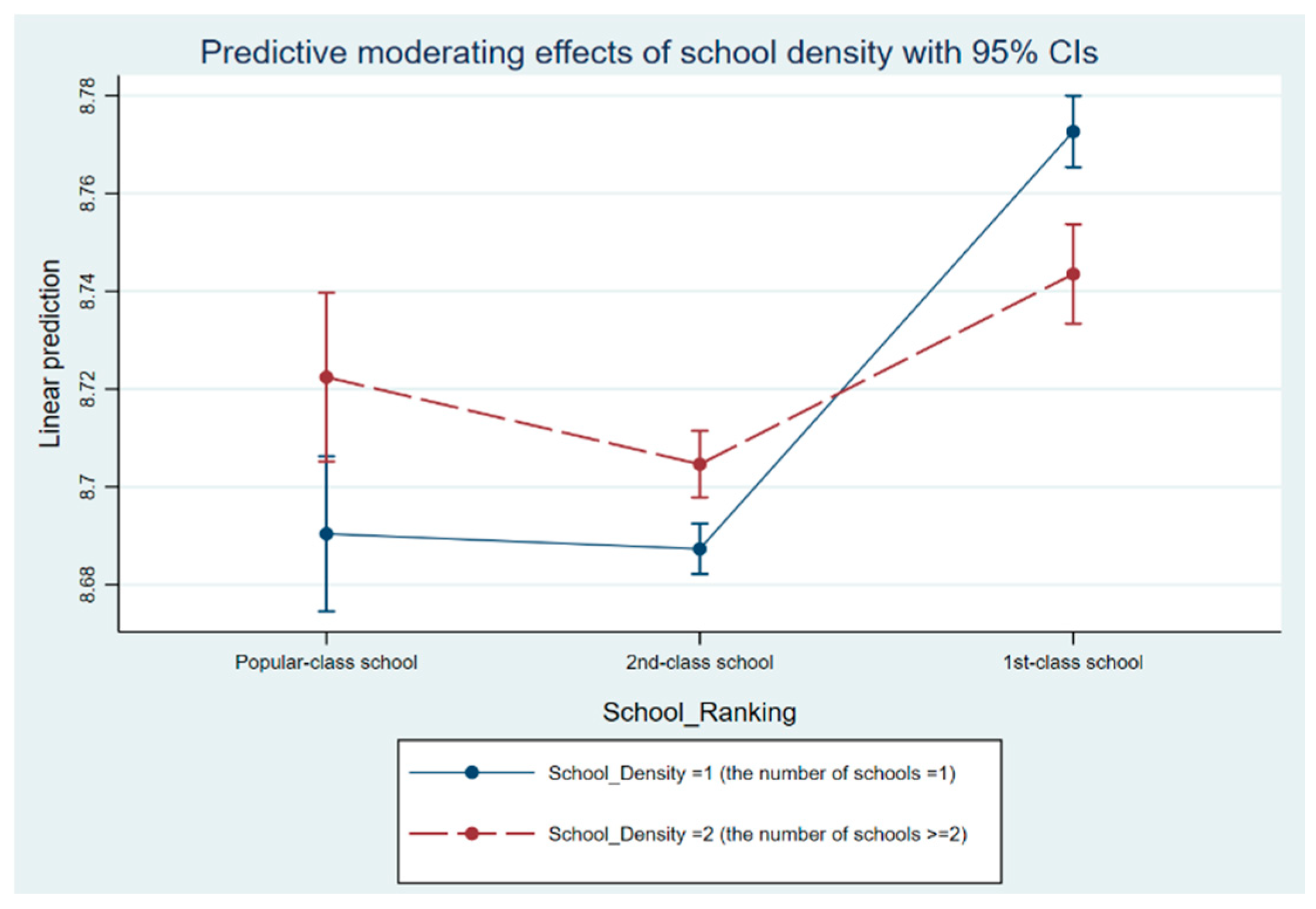

5.3.2. Moderating Effects of Quality School Density on Capitalization

5.3.3. School Capitalization in Different Segmented Zones

5.3.4. Ranked Schools’ Capitalization before and after the Equitable Housing Policy

6. Conclusions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Beracha, E.; Hardin, W.G. The Capitalization of School Quality into Renter and Owner Housing. Real Estate Econ. 2018, 46, 85–119. [Google Scholar] [CrossRef]

- Gibbons, S.; Machin, S. Valuing English primary schools. J. Urban Econ. 2003, 53, 197–219. [Google Scholar] [CrossRef] [Green Version]

- Haurin, D.R.; Brasington, D. School quality and real house prices: Inter- and intrametropolitan effects. J. Hous. Econ. 1996, 5, 351–368. [Google Scholar] [CrossRef] [Green Version]

- Feng, H.; Lu, M. School quality and housing prices: Empirical evidence from a natural experiment in Shanghai, China. J. Hous. Econ. 2013, 22, 291–307. [Google Scholar] [CrossRef]

- Zheng, S.; Hu, W.; Wang, R. How Much Is a Good School Worth in Beijing? Identifying Price Premium with Paired Resale and Rental Data. J. Real Estate Financ. Econ. 2016, 53, 184–199. [Google Scholar] [CrossRef]

- Zhang, M.; Chen, J. Unequal school enrollment rights, rent yields gap, and increased inequality: The case of Shanghai. China Econ. Rev. 2018, 49, 229–240. [Google Scholar] [CrossRef]

- Hu, L.; He, S.; Luo, Y.; Su, S.; Xin, J.; Weng, M. A social-media-based approach to assessing the effectiveness of equitable housing policy in mitigating education accessibility induced social inequalities in Shanghai, China. Land Use Policy 2020, 94, 104513. [Google Scholar] [CrossRef]

- Oates, W.E. The Effects of Property Taxes and Local Public Spending on Property Values: An Empirical Study of Tax Capitalization and the Tiebout Hypothesis. J. Political Econ. 1969, 77, 957–971. [Google Scholar] [CrossRef]

- Black, S.E.; Machin, S. Housing Valuations of School Performance. In Handbook of the Economics of Education; Elsevier: Amsterdam, The Netherlands, 2011; Volume 3. [Google Scholar] [CrossRef]

- Bogart, W.T.; Cromwell, B.A. How Much Is a Neighborhood School Worth? J. Urban Econ. 2000, 47, 280–305. [Google Scholar] [CrossRef]

- Kuminoff, N.V.; Pope, J.C. Do “capitalization effects” for public goods reveal the public’s willingness to pay? Int. Econ. Rev. 2014, 55, 1227–1250. [Google Scholar] [CrossRef]

- Nguyen-Hoang, P.; Yinger, J. The capitalization of school quality into house values: A review. J. Hous. Econ. 2011, 20, 30–48. [Google Scholar] [CrossRef]

- Wen, H.; Xiao, Y.; Zhang, L. School district, education quality, and housing price: Evidence from a natural experiment in Hangzhou, China. Cities 2017, 66, 72–80. [Google Scholar] [CrossRef]

- Brasington, D.M. Capitalization and community size. J. Urban Econ. 2001, 50, 385–395. [Google Scholar] [CrossRef]

- Brasington, D.M. The demand for local public goods: The case of public school quality. In Public Finance Review; SAGE Publications Inc.: Shozende Oaks, CA, USA, 2002; Volume 30, pp. 163–187. [Google Scholar] [CrossRef] [Green Version]

- Brasington, D.M. Size and school district consolidation: Do opposites attract? Economica 2003, 70, 673–690. [Google Scholar] [CrossRef]

- Guerrieri, V.; Hartley, D.; Hurst, E. Endogenous gentrification and housing price dynamics. J. Public Econ. 2013, 100, 45–60. [Google Scholar] [CrossRef] [Green Version]

- Chin, H.C.; Foong, K.W. Influence of School Accessibility on Housing Values. J. Urban Plan. Dev. 2006, 132, 120–129. [Google Scholar] [CrossRef]

- Wen, H.; Xiao, Y.; Hui, E.C.M.; Zhang, L. Education quality, accessibility, and housing price: Does spatial heterogeneity exist in education capitalization? Habitat Int. 2018, 78, 68–82. [Google Scholar] [CrossRef]

- Yuan, F.; Wei, Y.D.; Wu, J. Amenity effects of urban facilities on housing prices in China: Accessibility, scarcity, and urban spaces. Cities 2020, 96, 102433. [Google Scholar] [CrossRef]

- Brasington, D.M. Private Schools and the Willingness to Pay for Public Schooling. Educ. Financ. Policy 2007, 2, 152–174. [Google Scholar] [CrossRef]

- Li, H.; Wei, Y.D.; Wu, Y.; Tian, G. Analyzing housing prices in Shanghai with open data: Amenity, accessibility and urban structure. Cities 2019, 91, 165–179. [Google Scholar] [CrossRef]

- Han, J.; Cui, L.; Yu, H. Pricing the value of the chance to gain admission to an elite senior high school in Beijing: The effect of the LDHSE policy on resale housing prices. Cities 2021, 115, 103238. [Google Scholar] [CrossRef]

- Park, H.; Tidwell, A.; Yun, S.; Jin, C. Does school choice program affect local housing prices?: Inter- vs. intra-district choice program. Cities 2021, 115, 103237. [Google Scholar] [CrossRef]

- Austin, P.C.; Stuart, E.A. Moving towards best practice when using inverse probability of treatment weighting (IPTW) using the propensity score to estimate causal treatment effects in observational studies. Stat. Med. 2015, 34, 3661–3679. [Google Scholar] [CrossRef]

- Kling, J.R.; Liebman, J.B.; Katz, L.F. Experimental analysis of neighborhood effects. Econometrica 2007, 75, 83–119. [Google Scholar] [CrossRef] [Green Version]

- Wodtke, G.T.; Harding, D.J.; Elwert, F. Neighborhood effects in temporal perspective: The impact of long-term exposure to concentrated disadvantage on high school graduation. Am. Sociol. Rev. 2011, 76, 713–736. [Google Scholar] [CrossRef]

- Öst, C.E.; Wilhelmsson, M. The long-term consequences of youth housing for childbearing and higher education. J. Policy Modeling 2019, 41, 845–858. [Google Scholar] [CrossRef]

- Wilhelmsson, M. Energy Performance Certificates and Its Capitalization in Housing Values in Sweden. Sustainability 2019, 11, 6101. [Google Scholar] [CrossRef] [Green Version]

- Zou, J.; Chen, Y.; Chen, J. The complex relationship between neighbourhood types and migrants’ socioeconomic integration: The case of urban China. J. Hous. Built Environ. 2020, 35, 65–92. [Google Scholar] [CrossRef]

- Wu, Q.; Wallace, M. Hukou stratification, class structure, and earnings in transitional China. Chin. Sociol. Rev. 2021, 53, 223–253. [Google Scholar] [CrossRef]

- Chen, Y.; Feng, S. The education of migrant children in China’s urban public elementary schools: Evidence from Shanghai. China Econ. Rev. 2019, 54, 390–402. [Google Scholar] [CrossRef]

- The New-type Urbanization Plan 2014–2020. Available online: http://www.gov.cn/zhengce/2014-03/16/content_2640075.htm (accessed on 16 March 2014).

- Huang, Y. Renters’ housing behaviour in transitional urban China. Hous. Stud. 2003, 18, 103–126. [Google Scholar] [CrossRef]

- Huang, Y.; Jiang, L. Housing inequality in transitional Beijing. Int. J. Urban Reg. Res. 2009, 33, 936–956. [Google Scholar] [CrossRef]

- Tao, L.; Hui, E.C.M.; Wong, F.K.W.; Chen, T. Housing choices of migrant workers in China: Beyond the Hukou perspective. Habitat Int. 2015, 49, 474–483. [Google Scholar] [CrossRef]

- Chen, J.; Wu, Y. The Possible Conflict between the Housing Rights and the Rights to Public Services Availability in the Process of “Equal Rights between Buyer and Tenant”—Renting for Living or Renting for Rights. Acad. Mon. 2019, 2, 44–56. [Google Scholar]

- Wen, H.; Xiao, Y.; Hui, E.C.M. Quantile effect of educational facilities on housing price: Do homebuyers of higher-priced housing pay more for educational resources? Cities 2019, 90, 100–112. [Google Scholar] [CrossRef]

- Zheng, S.Q.; Kahn, M.E. Land and residential property markets in a booming economy: New evidence from Beijing. J. Urban Econ. 2008, 63, 743–757. [Google Scholar] [CrossRef]

- Kuang, L.; Hao, Q.; Liang, P.; Shen, L.; Wang, X.; Luo, Y. A research on China’s Rental Housing Market Demand and Its Future Development Trend. Dev. Financ. Res. 2018, 6, 65–87. [Google Scholar] [CrossRef]

- Chen, Z.; Chen, J. Tenant Share of Families Supply Structure of Rental Housing and Housing Price. Stat. Res. 2018, 35, 28–37. [Google Scholar] [CrossRef]

- Advice on Accelerating the Development of the Rental Housing Market in Large and Medium Cities with Net Population Inflow. Available online: https://www.mohurd.gov.cn/gongkai/fdzdgknr/tzgg/201707/20170720_232676.html (accessed on 20 July 2017).

- Sheng, Y.; Zhao, M. Regulations in the era of new-type urbanisation and migrant workers’ settlement intentions: The case of Beijing. Popul. Space Place 2021, 27, e2394. [Google Scholar] [CrossRef]

- Chan, K.W.; Zhang, L. The Hukou System and Rural-Urban Migration in China: Processes and Changes; Cambridge University Press: Cambridge, UK, 1999. [Google Scholar]

- Chen, M.; Wu, Y.; Liu, G.; Wang, X. City economic development, housing availability, and migrants’ settlement intentions: Evidence from China. Growth Chang. 2020, 51, 1239–1258. [Google Scholar] [CrossRef]

- Wang, T. Rural migrants in China: Barriers to education and citizenship. Intercult. Educ. 2020, 31, 578–591. [Google Scholar] [CrossRef]

- Yi, C.; Huang, Y. Housing Consumption and Housing Inequality in Chinese Cities During the First Decade of the Twenty-First Century. Hous. Stud. 2014, 29, 291–311. [Google Scholar] [CrossRef]

- Black, S.E. Do better schools matter? Parental valuation of elementary education. Q. J. Econ. 1999, 114, 577–599. [Google Scholar] [CrossRef] [Green Version]

- Ha, W.; Yu, R. Quasi-Experimental Evidence of a School Equalization Reform on Housing Prices in Beijing. Chin. Educ. Soc. 2019, 52, 162–185. [Google Scholar] [CrossRef]

- Machin, S. Houses and schools: Valuation of school quality through the housing market. Labour Econ. 2011, 18, 723–729. [Google Scholar] [CrossRef]

- Kain, J.F.; Quigley, J.M. Measuring the Value of Housing Quality. J. Am. Stat. Assoc. 1970, 65, 532–548. [Google Scholar] [CrossRef]

- Rosen, S. Hedonic Prices and Implicit Markets: Product Differentiation in Pure Competition. J. Political Econ. 1974, 82, 34–55. [Google Scholar] [CrossRef]

- Shipman, J.E.; Swanquist, Q.T.; Whited, R.L. Propensity score matching in accounting research. Accounting Rev. 2017, 92, 213–244. [Google Scholar] [CrossRef]

- Hu, M.; Lin, Z.; Liu, Y. Amenities, Housing Affordability, and Education Elites. J. Real Estate Finance Econ. 2022, 1–28. [Google Scholar] [CrossRef]

- Rosenbaum, P.R.; Rubin, D.B. The central role of the propensity score in observational studies for causal effects. Biometrika 1983, 70, 41–55. [Google Scholar] [CrossRef]

- Lechner, M. A Note on the Common Support Problem in Applied Evaluation Studies. Ann. Écon. Stat. 2008, 91–92, 217. [Google Scholar] [CrossRef] [Green Version]

- Rosenbaum, P.R.; Rubin, D.B. Constructing a Control Group Using Multivariate Matched Sampling Methods That Incorporate the Propensity Score. Am. Stat. 1985, 39, 33–38. [Google Scholar]

- Caliendo, M.; Kopeinig, S. Some practical guidance for the implementation of propensity score matching. J. Econ. Surv. 2008, 22, 31–72. [Google Scholar] [CrossRef] [Green Version]

- Abadie, A.; Drukker, D.; Herr, J.L.; Imbens, G.W. Implementing Matching Estimators for Average Treatment Effects in Stata. Stata J. Promot. Commun. Stat. Stata 2004, 4, 290–311. [Google Scholar] [CrossRef] [Green Version]

- Heckman, J.; Ichimura, H.; Smith, J.; Todd, P. Characterizing Selection Bias Using Experimental Data. Econometrica 1998, 66, 1017. [Google Scholar] [CrossRef]

- Abadie, A.; Imbens, G. Simple and Bias-Corrected Matching Estimators for Average Treatment Effects; National Bureau of Economic Research: Cambridge, MA, USA, 2002. [Google Scholar] [CrossRef]

- Cole, S.R.; Hernan, M.A. Constructing Inverse Probability Weights for Marginal Structural Models. Am. J. Epidemiol. 2008, 168, 656–664. [Google Scholar] [CrossRef]

- Kranker, K.; Blue, L.; Forrow, L.V. Improving Effect Estimates by Limiting the Variability in Inverse Propensity Score Weights. Am. Stat. 2021, 75, 276–287. [Google Scholar] [CrossRef] [Green Version]

- Robins, J.; Sued, M.; Lei-Gomez, Q.; Andrea, R. Comment: Performance of Double-Robust Estimators When “Inverse Probability” Weights Are Highly Variable. Stat. Sci. 2007, 22, 523–539. [Google Scholar] [CrossRef]

- Wilhelmsson, M. Spatial models in real estate economics. Hous. Theory Soc. 2002, 19, 92–101. [Google Scholar] [CrossRef]

- Imbens, G.W. Matching Methods in Practice: Three Examples. J. Hum. Resour. 2015, 50, 373–419. [Google Scholar] [CrossRef] [Green Version]

- Zhang, S.; Wang, L.; Lu, F. Exploring housing rent by mixed geographically weighted regression: A case study in Nanjing. ISPRS Int. J. Geo-Inf. 2019, 8, 431. [Google Scholar] [CrossRef] [Green Version]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Variable | Definition | Obs | Mean | S.D. | Min | Max |

|---|---|---|---|---|---|---|

| Rent | The monthly rent of rental housing unit (RMB/month) | 49,438 | 6596.21 | 3450.23 | 1000 | 30,000 |

| SCHOOL | Binary variable, if the nearest quality school is located within 750 m radius neighborhood of rental housing or not | 49,438 | 0.51 | 0.50 | 0 | 1 |

| Treatment (within 750 m) = 1, if the nearest quality school locates within a 750 m radius neighborhood | 25,437 | 1 | 0 | 1 | 1 | |

| Control (out of 750 m) = 0, otherwise. | 24,001 | 0 | 0 | 0 | 0 | |

| School_Ranking | Categorical variable, three categories of quality schools’ ranking | 49,438 | 1.95 | 0.64 | 1 | 3 |

| =1, if popular-class schools located in the outer districts; | 11,583 | - | - | - | - | |

| =2, if 2nd-class schools located in the inner districts; | 28,773 | - | - | - | - | |

| =3, if 1st-class schools located in the inner districts; | 9082 | - | - | - | - | |

| School_Density | Categorical variable, the number of high-quality schools within 750 m neighborhood | 25,437 | 1.32 | 0.47 | 1 | 2 |

| =1, if there is only one high-quality school | 17,173 | 1 | 0 | 1 | 1 | |

| =2, if there are more than two high-quality schools (two also included) | 8264 | 2 | 0 | 2 | 2 | |

| Size | The construction area of the rental housing unit (m2) | 49,438 | 73.93 | 31.55 | 9 | 446.38 |

| Age | Housing age up to 2019 | 49,438 | 21.72 | 9.79 | 1 | 79 |

| Bedroom | The number of bedrooms in the rental housing unit | 49,438 | 1.81 | 0.69 | 1 | 4 |

| Livingroom | The number of living rooms in the rental housing unit | 49,438 | 2.02 | 0.43 | 1 | 4 |

| Kitchen | The number of kitchens in the rental housing unit | 49,438 | 1.99 | 0.09 | 1 | 3 |

| Bathroom | The number of bathrooms in the rental housing unit | 49,438 | 2.11 | 0.34 | 1 | 4 |

| Supermarket | Number of supermarkets within a 500 m radius neighborhood | 49,438 | 27.06 | 15.80 | 0 | 158 |

| Bank | Number of bank services within a 500 m radius neighborhood | 49,438 | 8.18 | 7.61 | 0 | 118 |

| Restaurant | Number of restaurants within a 500 m radius neighborhood | 49,438 | 247.72 | 168.75 | 0 | 2108 |

| District | The district where the rental housing unit locates at | 49,438 | 5.13 | 2.62 | 1 | 9 |

| D_School | The distance to the nearest high-quality school (km) | 49,438 | 0.77 | 0.36 | 0.01 | 1.50 |

| D_Center | The distance to the city center (km) | 49,438 | 11.72 | 7.55 | 0.11 | 40.42 |

| D_Subway | The distance to the nearest subway station (km) | 49,438 | 0.86 | 0.76 | 0.1 | 40.17 |

| D_Business | The distance to the nearest business center (km) | 49,438 | 2.16 | 2.58 | 0.05 | 55.90 |

| (1) Default | (2) PSCORE | (3) IPW | (4) Matched | |

|---|---|---|---|---|

| VARIABLE | lnR | lnR | lnR | lnR |

| SCHOOL | 0.0062 *** | 0.0058 *** | 0.0095 *** | 0.0060 *** |

| (3.75) | (3.53) | (5.20) | (3.61) | |

| pscore (SCHOOL) | - | 0.6322 *** | - | - |

| (9.31) | ||||

| lnSize | 0.5947 *** | 0.6392 *** | 0.5956 *** | 0.5927 *** |

| (89.64) | (76.35) | (63.27) | (89.39) | |

| lnAge | −0.1381 *** | −0.1391 *** | −0.1293 *** | −0.1386 *** |

| (−49.13) | (−49.57) | (−41.42) | (−49.30) | |

| Bedroom | 0.0510 *** | 0.0266 *** | 0.0551 *** | 0.0519 *** |

| (20.58) | (7.19) | (16.12) | (20.99) | |

| Livingroom | 0.0149 *** | 0.0245 *** | 0.0120 *** | 0.0154 *** |

| (5.61) | (8.69) | (4.23) | (5.84) | |

| Kitchen | −0.1382 *** | −0.0781 *** | −0.1256 *** | −0.1431 *** |

| (−6.28) | (−3.38) | (−5.28) | (−6.51) | |

| Bathroom | 0.1338 *** | 0.1468 *** | 0.1380 *** | 0.1331 *** |

| (33.06) | (34.32) | (24.45) | (32.92) | |

| lnD_center | −0.2294 *** | −0.2000 *** | −0.2335 *** | −0.2281 *** |

| (−60.41) | (−40.62) | (−51.17) | (−60.08) | |

| lnD_subway | −0.0658 *** | −0.0050 | −0.0603 *** | −0.0649 *** |

| (−35.57) | (−0.74) | (−28.65) | (−35.12) | |

| lnD_business | −0.0275 *** | −0.0481 *** | −0.0302 *** | −0.0265 *** |

| (−20.20) | (−18.40) | (−18.19) | (−19.54) | |

| Supermarket | −0.0026 *** | −0.0047 *** | −0.0026 *** | −0.0026 *** |

| (−31.14) | (−18.93) | (−20.31) | (−31.49) | |

| Bank | 0.0035 *** | −0.0004 | 0.0040 *** | 0.0043 *** |

| (20.04) | (−0.95) | (21.66) | (24.98) | |

| Restaurant | 0.0001 *** | 0.0003 *** | 0.0001 *** | 0.0001 *** |

| (17.28) | (15.26) | (12.38) | (16.39) | |

| Constant | 6.6052 *** | 5.9795 *** | 6.5570 *** | 6.6164 *** |

| (129.89) | (69.25) | (107.61) | (130.14) | |

| Fixed district effects | Yes | Yes | Yes | Yes |

| Fixed time effects | Yes | Yes | Yes | Yes |

| Control propensity score | No | Yes | No | No |

| Control inverse probability weight | No | No | Yes | No |

| VIF (SCHOOL) | 1.1 | 1.1 | 1.01 | 1.1 |

| No. of observations | 49,438 | 49,438 | 49,438 | 49,324 |

| R-sq | 0.830 | 0.830 | 0.823 | 0.831 |

| adj. R-sq | 0.830 | 0.830 | 0.822 | 0.831 |

| Unmatched (U)/ | Mean | %Bias | % Reduced | t-Test | V(T)/V(C) | ||

|---|---|---|---|---|---|---|---|

| VARIABLE | Matched (M) | Treated | Control | |Bias| | |||

| lnSize | U | 4.21 | 4.25 | −11.8 | −13.1 | 1.01 | |

| M | 4.21 | 4.23 | −5.1 | 56.9 | −5.72 | 1.02 | |

| lnAge | U | 3.00 | 2.95 | 11.7 | 12.99 | 0.96 * | |

| M | 3.00 | 3.01 | −3 | 74.1 | −3.42 | 0.98 | |

| Bedroom | U | 1.80 | 1.82 | −1.9 | −2.07 | 0.99 | |

| M | 1.80 | 1.85 | −6.9 | −271.3 | −7.77 | 0.99 | |

| Livingroom | U | 2.01 | 2.04 | −7.7 | −8.53 | 0.96 * | |

| M | 2.01 | 2.03 | −5.6 | 27.3 | −6.42 | 1.06 * | |

| Kitchen | U | 1.99 | 2.00 | −4.5 | −4.94 | 1.69 * | |

| M | 1.99 | 2.00 | −2.4 | 45.8 | −2.6 | 1.31 | |

| Bathroom | U | 2.10 | 2.13 | −8 | −8.85 | 0.81 * | |

| M | 2.10 | 2.11 | −3.1 | 61.6 | −3.51 | 0.88 * | |

| lnD_center | U | 2.21 | 2.35 | −24.2 | −26.85 | 1.08 * | |

| M | 2.21 | 2.24 | −5.1 | 79.1 | −5.63 | 1.02 | |

| lnD_subway | U | −0.36 | −0.23 | −25.7 | −28.59 | 0.76 * | |

| M | −0.36 | −0.34 | −2.8 | 89.2 | −3.16 | 0.80 * | |

| lnD_business | U | 0.39 | 0.42 | −4.2 | −4.72 | 0.68 * | |

| M | 0.39 | 0.41 | −2.4 | 42.7 | −2.72 | 0.67 * | |

| Supermarket | U | 29.18 | 24.82 | 28 | 31 | 1.39 * | |

| M | 28.93 | 29.24 | −2 | 92.8 | −2.04 | 0.82 * | |

| Bank | U | 9.23 | 7.07 | 28.9 | 31.96 | 2.12 * | |

| M | 8.93 | 9.12 | −2.6 | 91.2 | −2.95 | 0.98 | |

| Restaurant | U | 257.64 | 237.22 | 12.1 | 13.47 | 0.95 * | |

| M | 256.37 | 257.90 | −0.9 | 92.5 | −1.02 | 0.92 * | |

| (1) | (2) | (3) | (4) | |

|---|---|---|---|---|

| Matched | Popular-Class School | 2nd-Class School | 1st-Class School | |

| VARIABLE | lnR | lnR | lnR | lnR |

| SCHOOL | 0.0060 *** | 0.0321 *** | −0.0075 *** | 0.0298 *** |

| (3.61) | (11.52) | (−3.39) | (7.94) | |

| lnSize | 0.5927 *** | 0.4022 *** | 0.6084 *** | 0.7091 *** |

| (89.39) | (35.71) | (68.14) | (45.45) | |

| lnAge | −0.1386 *** | −0.1850 *** | −0.1373 *** | −0.1175 *** |

| (−49.30) | (−42.03) | (−35.21) | (−16.16) | |

| Bedroom | 0.0519 *** | 0.0755 *** | 0.0509 *** | 0.0312 *** |

| (20.99) | (18.19) | (15.30) | (5.36) | |

| Livingroom | 0.0154 *** | 0.0176 *** | 0.0247 *** | 0.0014 |

| (5.84) | (4.39) | (6.79) | (0.20) | |

| Kitchen | −0.1431 *** | −0.1652 *** | −0.1364 *** | −0.1631 ** |

| (−6.51) | (−3.30) | (−5.45) | (−2.48) | |

| Bathroom | 0.1331 *** | 0.1299 *** | 0.1363 *** | 0.1079 *** |

| (32.92) | (17.46) | (26.37) | (10.55) | |

| Constant | 6.6164 *** | 8.2305 *** | 6.6583 *** | 6.4300 *** |

| (130.14) | (67.23) | (113.52) | (41.79) | |

| Fixed urban district effects | Yes | Yes | Yes | Yes |

| Fixed time effects | Yes | Yes | Yes | Yes |

| Control the accessibility attributes | Yes | Yes | Yes | Yes |

| Control the amenity attributes | Yes | Yes | Yes | Yes |

| No. of observations | 49,324 | 11,582 | 28,721 | 9021 |

| R-sq | 0.831 | 0.799 | 0.789 | 0.803 |

| adj. R-sq | 0.831 | 0.798 | 0.788 | 0.802 |

| Moderating Effects Model | |

|---|---|

| VARIABLE | lnR |

| 2nd-class School (Popular-class School is the default) | −0.0031 |

| (−0.31) | |

| 1st-class School | 0.0823 *** |

| (8.04) | |

| School_Density (≥2; school number =1 is default) | 0.0320 *** |

| (6.17) | |

| Interaction (2nd-class School#School_Density) | −0.0147 ** |

| (−2.40) | |

| Interaction (1st-class School#School_Density) | −0.0612 *** |

| (−7.90) | |

| lnSize | 0.5958 *** |

| (63.94) | |

| lnAge | −0.1416 *** |

| (−35.62) | |

| Bedroom | 0.0641 *** |

| (18.89) | |

| Livingroom | 0.0185 *** |

| (5.00) | |

| Kitchen | −0.1601 *** |

| (−5.72) | |

| Bathroom | 0.1209 *** |

| (20.72) | |

| Constant | 6.7815 *** |

| (102.79) | |

| Fixed urban district effects | Yes |

| Fixed time effects | Yes |

| Control the accessibility attributes | Yes |

| Control the amenity attributes | Yes |

| No. of observations | 25,323 |

| R-sq | 0.827 |

| adj. R-sq | 0.826 |

| Zone 1 | Zone 2 | Zone 3 | Zone 4 | Zone 5 | Zone 6 | |

|---|---|---|---|---|---|---|

| VARIABLE | lnR | lnR | lnR | lnR | lnR | lnR |

| SCHOOL | 0.0334 *** | −0.0083 *** | 0.0314 *** | 0.1157 *** | 0.0082 | −0.0600 *** |

| (11.97) | (−3.68) | (8.09) | (3.59) | (0.65) | (−3.07) | |

| lnSize | 0.4058 *** | 0.6158 *** | 0.7120 *** | 0.4220 *** | 0.3435 *** | 0.4547 *** |

| (35.73) | (67.59) | (43.73) | (5.74) | (14.60) | (10.46) | |

| lnAge | −0.1831 *** | −0.1374 *** | −0.1171 *** | −0.1369 * | −0.0723 *** | −0.1751 *** |

| (−41.89) | (−34.50) | (−15.37) | (−1.94) | (−4.71) | (−6.71) | |

| Bedroom | 0.0753 *** | 0.0489 *** | 0.0310 *** | 0.0909 * | 0.1084 *** | 0.0728 *** |

| (18.11) | (14.38) | (5.13) | (1.94) | (10.70) | (4.20) | |

| Livingroom | 0.0162 *** | 0.0230 *** | −0.0004 | −0.0151 | 0.0472 *** | 0.0360 * |

| (4.03) | (6.22) | (−0.06) | (−0.29) | (3.24) | (1.81) | |

| Kitchen | −0.1636 *** | −0.1391 *** | −0.1842 ** | 0.0000 | −0.0386 | 0.0816 |

| (−3.26) | (−5.46) | (−2.48) | (.) | (−0.44) | (1.33) | |

| Bathroom | 0.1267 *** | 0.1372 *** | 0.1083 *** | 0.0675 | 0.0828 *** | 0.0521 * |

| (17.16) | (26.28) | (10.37) | (1.54) | (2.70) | (1.67) | |

| lnD_center | −0.4521 *** | −0.2441 *** | −0.1782 *** | −1.9685 *** | −0.0441 * | −0.2153 * |

| (−33.82) | (−51.60) | (−20.25) | (−6.14) | (−1.86) | (−1.74) | |

| lnD_subway | −0.1128 *** | −0.0420 *** | −0.0643 *** | 0.2419 *** | −0.1066 *** | 0.0186 |

| (−38.41) | (−15.75) | (−11.70) | (6.79) | (−5.74) | (1.03) | |

| lnD_business | −0.0028 | −0.0252 *** | −0.0342 *** | 0.1376 ** | −0.0123 | 0.0613 *** |

| (−0.86) | (−13.99) | (−9.08) | (2.43) | (−1.13) | (3.91) | |

| Supermarket | −0.0015 *** | −0.0028 *** | −0.0021 *** | −0.0046 | −0.0019 *** | −0.0001 |

| (−8.50) | (−25.35) | (−9.81) | (−1.23) | (−6.55) | (−0.11) | |

| Bank | 0.0012 *** | 0.0037 *** | 0.0048 *** | 0.0386 ** | 0.0061 *** | 0.0012 |

| (2.75) | (15.68) | (14.09) | (2.20) | (3.85) | (0.59) | |

| Restaurant | 0.0001 *** | 0.0001 *** | 0.0002 *** | 0.0010 | 0.0000 | 0.0002 ** |

| (7.42) | (10.66) | (10.91) | (1.28) | (0.97) | (1.98) | |

| Constant | 8.1981 *** | 6.8836 *** | 6.4635 *** | 12.4846 *** | 6.8127 *** | 7.0435 *** |

| (67.00) | (116.77) | (37.43) | (10.72) | (34.17) | (25.80) | |

| Fixed inner district effects | No | Yes | Yes | Yes | No | No |

| Fixed outer district effects | Yes | No | No | No | Yes | Yes |

| Control popular-class schools | Yes | No | No | Yes | No | No |

| Control 2nd-class schools | No | Yes | No | No | Yes | No |

| Control 1st-class schools | No | No | Yes | No | No | Yes |

| Fixed time effects | Yes | Yes | Yes | Yes | Yes | Yes |

| No. of observations | 11,454 | 27,801 | 8535 | 128 | 920 | 486 |

| R-sq | 0.802 | 0.784 | 0.795 | 0.858 | 0.823 | 0.871 |

| adj. R-sq | 0.801 | 0.784 | 0.794 | 0.797 | 0.815 | 0.860 |

| (1) Popular-Class School | (2) 2nd-Class School | (3) 1st-Class School | ||||

|---|---|---|---|---|---|---|

| lnR | lnR | lnR | lnR | lnR | lnR | |

| VARIABLE | Before | After | Before | After | Before | After |

| SCHOOL | 0.0315 *** | 0.0289 *** | −0.0088 * | −0.0081 | 0.0159 * | 0.0273 ** |

| (5.37) | (4.14) | (−1.69) | (−1.26) | (1.75) | (2.56) | |

| lnSize | 0.4212 *** | 0.4085 *** | 0.6267 *** | 0.5666 *** | 0.6984 *** | 0.6039 *** |

| (17.28) | (17.84) | (33.78) | (15.30) | (19.21) | (10.76) | |

| lnAge | −0.1606 *** | −0.1467 *** | −0.1233 *** | −0.1372 *** | −0.1053 *** | −0.1422 *** |

| (−16.33) | (−14.45) | (−13.65) | (−10.79) | (−6.82) | (−5.52) | |

| Bedroom | 0.0732 *** | 0.0834 *** | 0.0393 *** | 0.0676 *** | 0.0408 *** | 0.0390 ** |

| (7.84) | (9.53) | (5.59) | (5.40) | (3.42) | (1.98) | |

| Livingroom | 0.0072 | 0.0055 | 0.0100 | 0.0163 | −0.0163 | 0.0149 |

| (0.81) | (0.59) | (1.15) | (1.32) | (−1.03) | (0.60) | |

| Kitchen | 0.0238 | −0.0642 | −0.0560 | −0.1156 | −0.3370 | −0.5530 ** |

| (0.36) | (−0.90) | (−1.08) | (−1.11) | (−1.62) | (−2.41) | |

| Bathroom | 0.1245 *** | 0.1216 *** | 0.1503 *** | 0.1371 *** | 0.0966 *** | 0.1246 *** |

| (8.57) | (8.04) | (12.77) | (7.56) | (3.74) | (4.41) | |

| lnD_center | −0.4279 *** | −0.5230 *** | −0.2390 *** | −0.2369 *** | −0.1875 *** | −0.1969 *** |

| (−15.23) | (−16.12) | (−23.51) | (−14.83) | (−8.75) | (−8.64) | |

| lnD_subway | −0.1089 *** | −0.0807 *** | −0.0429 *** | −0.0429 *** | −0.0668 *** | −0.0544 *** |

| (−18.44) | (−11.91) | (−7.02) | (−5.65) | (−5.27) | (−3.13) | |

| lnD_business | −0.0111 | −0.0035 | −0.0229 *** | −0.0234 *** | −0.0331 *** | −0.0252 ** |

| (−1.52) | (−0.44) | (−5.04) | (−4.96) | (−3.64) | (−2.28) | |

| Supermarket | −0.0014 ** | −0.0009 ** | −0.0031 *** | −0.0028 *** | −0.0030 *** | −0.0029 *** |

| (−2.53) | (−2.01) | (−10.37) | (−9.17) | (−5.75) | (−4.14) | |

| Bank | −0.0000 | 0.0004 | 0.0033 *** | 0.0030 *** | 0.0044 *** | 0.0054 *** |

| (−0.04) | (0.33) | (5.30) | (4.17) | (5.58) | (4.23) | |

| Restaurant | 0.0002 *** | 0.0001 ** | 0.0001 *** | 0.0001 *** | 0.0002 *** | 0.0002 *** |

| (4.11) | (2.05) | (5.08) | (5.14) | (5.63) | (5.44) | |

| Constant | 7.7707 *** | 8.2898 *** | 6.5275 *** | 6.8879 *** | 7.0269 *** | 7.8017 *** |

| (40.89) | (41.19) | (51.05) | (32.58) | (16.71) | (13.32) | |

| Fixed urban district effects | Yes | Yes | Yes | Yes | Yes | Yes |

| Fixed time effects | Yes | Yes | Yes | Yes | Yes | Yes |

| No.of observations | 2155 | 1597 | 4825 | 3566 | 1576 | 1128 |

| R-sq | 0.832 | 0.842 | 0.793 | 0.786 | 0.796 | 0.782 |

| adj. R-sq | 0.830 | 0.840 | 0.792 | 0.785 | 0.794 | 0.778 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Song, Z. The Capitalization of School Quality in Rents in the Beijing Housing Market: A Propensity Score Matching Method. Buildings 2022, 12, 485. https://doi.org/10.3390/buildings12040485

Song Z. The Capitalization of School Quality in Rents in the Beijing Housing Market: A Propensity Score Matching Method. Buildings. 2022; 12(4):485. https://doi.org/10.3390/buildings12040485

Chicago/Turabian StyleSong, Zisheng. 2022. "The Capitalization of School Quality in Rents in the Beijing Housing Market: A Propensity Score Matching Method" Buildings 12, no. 4: 485. https://doi.org/10.3390/buildings12040485