1. Introduction

The implementation of information systems—or enterprise resource planning (ERP) systems—in the construction sector has failed in many companies [

1]. Many researchers are addressing the issue of how the implementation of ERP systems in the environment of construction companies can be evaluated (for example, [

1,

2]). Information systems can be helpful in managing economic parameters, as well as safety, in construction [

3]. More sustainability can also be achieved by using ERP systems and intelligent information systems. This can have a positive impact on management processes [

4]. ERP systems and intelligent technologies can increase productivity and various key performance indicators in construction [

5]. The studies by Lao and Zhang, Lee and Kim, and Hadidi, Assaf, and Alkhiami have responded by developing and researching implementation models for the implementation of ERP in construction [

6,

7,

8,

9]. Another study on small businesses in Australia discussed success factors [

10]. Venkatraman and Fahd address the development of cloud ERP systems [

11]. Svensson and Thoss conducted a study with a sample of small enterprises and discussed risk factors [

12]. Svensson and Thoss have also discussed the development of and degree of need for ERP systems [

13]. However, none of the available studies have quantified the effects of ERP systems on economic sustainability in the construction sector; in particular, no studies have examined this issue with regard to the needs of intelligent and sustainable management in construction companies.

This issue is broad. To address the connection between the suggestion for and the use of information systems as part of design in the construction industry, it is necessary to perceive this process as complex. Therefore, designing and modeling parameters through economic indicators and designing sustainability should be processes continuously connected to architectural design. Hence, architectural design supported by information technologies is a broad topic, and the economic part is also significant from the complex perspective. The consequences include appropriate selection and assistance in the decision-making process regarding the selection of a suitable architectural solution, which also has an impact on the economic side. Therefore, information systems supporting design should be perceived more broadly and comprehensively.

1.1. Economic Sustainability and ERP Systems in the Construction Industry

ERP systems have an important role in the construction industry, which is to assist in and automate the management of resources. Such resources include economic savings, financial resources, and human and material resources, and all this with the aim of economic sustainability. In construction companies, ERP systems are used for cost management and, therefore, financial management—not only in the company, but also when managing projects. Likewise, human resources planning across projects implemented by such companies is a suitable area for ERP systems. Finally, ERP systems concern the management of logistics and material stocks. An important issue is communication and the exchange of information, which can be made more efficient thanks to ERP systems.

Many organizations use integrated management systems, which are better known as ERP systems. Using these systems has led to a discussion about the methods for their evaluation, which must consider multiple perceptions and criteria. Their successful use is also possible through cost parameters [

14]. A study from Saudi Arabia focused on ERP systems in the construction industry and their impact on various economic indicators. Based on the ranking compiled, costs represented the most important parameter, with an index of around 75% [

2]. When adopting enterprise resource planning systems, companies seek tangible benefits, such as cost reduction, increased productivity and efficiency, and business growth. A study has been conducted that used statistical analysis to quantify the critical success factors that influence the integration and the benefits derived from the use of ERP systems. Furthermore, in this study, attention was directed to costs as one of the critical indicators and parameters of economic sustainability [

9,

10,

11,

12,

13,

14,

15]. Lee, Lee, and Lee proposed a methodology for assessing the implementation of ERP in enterprises. The results showed that the most significant effect of using ERP was on business management; most of this impact concerned data management and control. As users became familiar with ERP, the data entry time decreased. The method involves less time and fewer costs with greater use [

16].

We know that the construction industry has several specific aspects. Specific materials and their development play a key role in every industry [

17]. Several studies have focused on cost optimization in construction and its simulation [

18]. However, none have focused on the issue of costs and ERP systems. The key success factors were defined in a study that identified five basic groups of these indicators: project effectiveness, satisfaction of key stakeholders, organizational strategic goals, innovation and development in the construction industry, and a comprehensive impact on society [

19]. Mellado, Lou, and Becerra have also discussed the importance of several parameters, the so-called iron triangle, noting that parameters such as cost, time, and quality are not sufficient for evaluation [

20]. It is necessary to measure the performance of a construction organization from the point of view of competition. The core indicators can be divided into the following groups: profitability and asset management; the satisfaction of critical stakeholders; the predictability of time and costs; environment, health, and safety (EHS); quality awareness; and low staff turnover [

21]. A very stimulating study described the continuity of the circular economy and key performance indicators and made suggestions for the development of a methodology and a new indicator (index) for this area [

22]. The impact of ERP systems on economic sustainability has been examined sporadically and the nature of this topic has not yet been clarified.

Despite the shifts in current technologies and the opportunities offered by them, in many (mainly developing) countries, their use does not reflect the current trends in and possibilities of information systems regarding the management of construction companies [

23]. A comparative study from Germany, Slovenia, and Croatia described the application of modern management approaches in the management of construction companies. Such approaches do not focus on specific economic indicators, and the management of resources and projects is random. They do not support goals and results [

24]. Therefore, the primary tool for improving performance is the measurement of performance [

25]. Another study states that quality, customer satisfaction, costs, time, business performance, health and safety, the environment, productivity, and people can be included among the key performance indicators [

26].

1.2. Key Performance Indicators and Economic Sustainability in Construction

Depending on the nature of the project, key indicators may differ. One study highlighted the importance of the procurement process itself and the definition of key performance factors at this stage. The authors identified the following factors in the context of public procurement for public construction projects: bid valuation costs as a percentage of the contract value, the number of changes in the introductory bid price, the time from the first bid to the actual award, the average delay in payment of the primary receivables, the average delay in the payment of agreed changes, and the average time for approval of agreed changes [

27]. Lindhard and Larsen examined 25 key factors considered important in managing construction projects. Of these, the authors identified cost, time, quality, and the availability of information and knowledge among managers as the most critical [

28]. Improving quality, sustainable construction, and reducing construction costs have been identified as the three key performance indicators in construction [

29]. Other research has also pointed to the need to address the issue of KPIs, with three of the ten KPIs surveyed being identified as very important; namely, cost, quality, and time [

30]. Navaz and collogues, based on observations from a survey of experts in the cement industry, identified 14 KPIs. Such rankings provide insight into what industry experts consider to be important KPIs and how they can be used to achieve economic sustainability [

31,

32].

Other research worldwide has also pointed to the cost side as a key performance indicator [

33]. Some studies have focused on cost planning, effectiveness, and predictability, as well as changes in cost planning [

34,

35]. Other studies have highlighted the importance of information systems and technologies. For example, one study aimed to compare the benefits of tracking and retrieving information through BIM technologies versus tracking key performance indicators [

36]. In this study, the relationship between information technologies and KPIs was addressed, based on which we made the scientific assumption that information systems can impact selected KPIs. The importance of technology for project management in the construction industry has been the subject of research where, in addition, critical success factors for construction projects were addressed [

37]. The construction industry has defined sustainability as meeting the requirements of the construction sector while balancing environmental protection, social welfare, and economic prosperity [

38]. Further research has pointed to the fact that sustainability in construction focuses mainly on environmental and social aspects. However, it is crucial to address economic sustainability within this complex of construction projects and construction companies [

39]. Many studies have demonstrated that sustainability in construction is linked to environmental and economic aspects but less so for social aspects [

40]. More information in

Table 1. The context linking environmental sustainability and economics has also been discussed in another study in Singapore [

41]. Assessing sustainability in construction is necessary from several perspectives. First, in terms of life-cycle sustainability assessment, it is essential to consider sustainability criteria that include environmental, social, and economic sustainability categories. Each category includes several sustainability indicators (SPIs) associated with different phases of a building’s life cycle [

42]. Due to the effort to transform the construction industry, it is desirable to understand and evaluate the perception and performance of construction companies in the field of sustainability. Another study has examined this relationship; i.e., the performance of construction companies in terms of various aspects of sustainability, including economic sustainability [

42]. Life-cycle-assessment (LCA) research in the construction sector has focused on improving social, economic, and environmental sustainability indicators [

43]. In this context, identifying and selecting key performance indicators and indicators of economic sustainability is undertaken on the basis of the penetration of the indicators, as they are essential indicators that also define the economic conditions of projects. The relationship between selected key indicators of performance and economic sustainability—and, thus, the dependence of the former on the latter—in the construction sector and in industry research has also been confirmed in another study [

31]. Furthermore, based on the recognized method of life-cycle sustainability assessment (LCSA), it has been confirmed that the perception of sustainability in buildings can be used as an assessment of sustainability, including for economic dimensions [

44,

45,

46].

The fact that selected information technologies can be used as tools for sustainability in the construction industry can also be concluded from research in Nigeria. According to this study, cloud computing has become a valuable platform for sustainability in many countries [

52]. The needs of digitalization and the use of information technologies were also emphasized by the study, which proposed a methodology for the digital documentation of design decisions that includes the intention behind and the justification of design solutions in the information modeling of buildings [

37,

53].

Based on the mentioned studies, it is possible to formulate scientific questions focused on the relationship between the use of ERP systems in the management of construction projects and their impacts on the costs and revenues of construction companies. Therefore, these two key performance indicators can represent the main parameters of the economic sustainability of construction projects and construction companies.

The tools supporting these activities are also important in the design and architectural design phases to improve results [

54]. Production and building planning are generally a key part of the production management of manufacturing enterprises. Computerized automation started in previous decades and, with wider and more advanced material requirements for planning, enterprise resource planning exists today in every industry [

55]. For design disciplines, building information modeling is considered an extension to it in the form of computer-aided design, whereas for non-design disciplines, it is perceived more as an intelligent data management system [

56]. In design, it is necessarily perceived as complex due to the economic parameter designs. It is recommended that architecture, engineering, and construction should use more advanced technologies to minimize human intervention and improve real-time capabilities [

57].

Despite the enormous number of studies on ERP system solutions from different perspectives, more comprehensive perspectives and research are needed in connection to the solution design phase. The impacts of various information systems have already been mapped many times. However, studies with an emphasis on designing economic sustainability are absent. This research, therefore, highlights this view of how these corporate information systems help in architecture and construction and how they contribute to the economic sustainability of projects and companies operating in the construction industry.

1.3. Research Gap and Problem Statement

Among the main reasons why it is necessary to assess economic sustainability in architecture and construction is the complexity of the perception of sustainability and its direct connection to economic parameters and indicators. Enterprise resource planning represents an effective tool that can support the design of economic sustainability through information technologies. It is a new gap in this area highlighted by the present point of view. It is, therefore, necessary to pay attention to it. Information technology should be used to support the design of construction and architectural projects. Planning and designing are equally important for economic sustainability. These technologies benefit from being seen as supporting tools for decision making and parameter design. Therefore, the assumption that these information systems represent one of the key factors for the design and success of projects is justified. Unfortunately, this topic has not yet been investigated in any studies.

The results of this research can help in better understanding the rationale behind the use of ERP systems in the construction industry and explain how these systems help and support the design of economic sustainability as one of the design dimensions in the construction industry.

ERP systems represent a financially demanding investment in every company. Each implementation should have clearly defined goals and expectations. The theoretical background indicates that there is an assumption that ERP systems contribute to intelligent and sustainable management in construction companies. The implementation of an ERP system should have a positive effect on selected key performance indicators. Economic sustainability was considered when defining these key performance indicators. Therefore, costs and revenues were selected as the subject of research.

When studying economic sustainability (as one of the components of comprehensive sustainability in construction), it is crucial to define the relationship with key performance indicators. Based on the research mentioned above, costs and revenues were identified as key performance indicators that are part of economic sustainability. Based on this relationship, hypotheses for these selected key performance indicators were determined and understood as indicators for the impact on economic sustainability. The relationship between key performance and economic sustainability indicators—and, thus, their dependence on each other—has also been confirmed by research [

38].

The aim of the research was to analyze the impact of the implementation of ERP systems on selected key performance indicators (costs and revenues). We assumed that ERP systems have a positive effect on costs and on revenues. Based on this, hypotheses regarding the impacts on costs and revenues were established.

Hypothesis A. Cost savings: ERP systems reduce the costs of construction enterprises as one economic sustainability parameter.

Further hypotheses were established as follows:

Hypothesis HA0. ERP systems do not reduce the costs of construction enterprises.

Hypothesis HA1. ERP systems reduce the costs of construction enterprises.

In other words, after the implementation of ERP systems, the costs in construction companies should decrease, so there should be savings. Cost parameters before and after the implementation of ERP systems were monitored. In addition, the cost-effectiveness and utilization rate of ERP systems, which may vary the effect depending on the exploitation level, were examined.

Hypothesis B. Revenue increases: ERP systems increase the revenues of construction enterprises as one economic sustainability parameter.

Further hypotheses were established as follows:

Hypothesis HB0. ERP systems do not increase the revenues of construction enterprises.

Hypothesis HB1. ERP systems increase the revenues of construction enterprises.

In other words, the assumption is that the use of an ERP system will lead to an increase in revenues in construction companies. Therefore, revenues were examined in the period before and after the implementation of ERPs. In addition, the exploitation levels of the ERP systems in construction enterprises and the correlation between them was also examined.

2. Research Methods

2.1. Data Collection and Research Sample

A questionnaire was the main form of data collection. It contained questions focused on the research issues and on the basic characteristics of the research sample. The essential characteristics of the survey sample are described in detail in the table. The central part contained questions focused on the exploitation level of ERP systems in construction enterprises and the impact on selected variables (selected key performance indicators).

Based on random selection from a database of construction companies with a proportional representation in accordance with the state of the industry, 1276 construction companies were selected and approached to participate in this research. Among these companies addressed, 125 respondents (construction companies) answered the research questions and participated in the research. They were both international companies and companies operating in Slovakia. However, only 55 of the companies used ERP systems. Thus, 55 respondents could be used for the research in correlation with the examined variables (i.e., the impact of ERP systems on costs and revenues).

Data collection was performed for eight months from October 2021 to May 2022. Respondents were randomly selected from a database of construction companies obtained from the Statistical Office. The sample size for each category was based on the ratio of the number of real enterprises in the Slovak national economy to the number of enterprises in the construction sector. For these reasons, the research sample represented the structure of the industry. Respondents were contacted by email, and there was an opportunity to contact them again if necessary to supplement and explain important information. Anonymous address checking was automatically set up to avoid duplicating the questionnaire, which would have led to data distortion.

The participants in construction projects represent the construction industry. These participants are, to a large extent, the implementers of construction works and activities, as well as the main suppliers and sub-contractors. Designers are another important group. Investors also had to be represented in the research. The construction activities they performed are specified in more detail in

Figure 1b, where the representation of respondents is based on construction activities. The specific focuses of projects depend on the sizes of the companies. Large companies generally undertake transport and engineering projects; however, this is not a rule. These companies also participate in residential projects.

The representation of the enterprises according to size and according to the classification in terms of construction activity can be seen in detail in

Figure 1. Large enterprises accounted for about 13% of respondents while 22% were medium-sized, and about 65% of the survey involved small and micro-enterprises. It is important to note that the structure of the sample reflected the distribution of subjects in the economies of the Visegrád Four countries (which include Slovakia), the characteristics and conditions of which are comparable. The construction industry in these countries accounts for a significant share of the GDP.

The companies undertake the construction of residences, transport projects, and other infrastructure. This study also focused on whether there were differences in the results for these groups, as shown in

Figure 1. This was not confirmed (see the Results and Discussion section). From the present point of view, it was not one of the important factors, even though, with other questions, such differences can be noted and should be investigated.

The SK NACE code serves statistical purposes. It represents the main activity or the groups of activities that can serve to identify the operation of a company across various branches (for example, the construction field is divided into building projects, civil engineering projects, and specialized construction works).

Data on costs and income were obtained from the official financial and accounting sources of the companies; they were primarily obtained from income statements and profit and loss statements, as well as portals and the Statistical Office. The data could be traced and verified for the companies that mentioned a name. To ensure the correctness of the data, in they were verified for the selected companies.

2.2. Data Processing

Data processing was performed using effective statistical methods. The first step was data separation. This involved separating the data that had been collected and distributing it for the periods before and after the implementation of ERP systems. Respondents indicated the exploitation level, as well as the cost level and revenues, before and after implementation. The program STATISTICS and MS Excel were used in the data processing.

Respondents reported the ERP exploitation level on a scale from 1 (low exploitation level) to 5 (high exploitation level). They also reported the level of costs through the rate or the percentage change. The same was reported for revenues. As already mentioned, data on expenses and profits were obtained from official documents from accounting sources and the Statistical Office. These indicators were verified. In cooperation with the financial departments of the construction companies, project managers carefully selected the required information. The impact categorizations used to quantify these results were also explained as part of the request for the provision of the data. Groups of influence were selected and, thus, impact was determined based on the description and explanation of the level represented by the impact on the selected results of the company in the context of economic sustainability. Values from 1 to 5 were used to describe concrete management activities and planning related to the design of economic indicators in the management of construction projects. The frequency of use of the systems was also determined based on this. Company sizes were also considered in this scale and information.

The goal of the F-test of the equality of two variances is to verify whether two sample sets come from a distribution with the same variance, which means verifying whether both sets show approximately the same variance for the observed random variable. This test assumes the normality of the observed values in both sample sets. For these purposes, Fisher’s F-test was performed.

To verify the accuracy of the data and the suitability and relevance of the research questions asked through the questionnaire, Cronbach’s alpha was used. The statistical test for measurement of reliability is [

49,

58]:

where

N is number of items,

c is the average covariance between item pairs, and

v is the average variance [

54].

Pearson correlation analysis was used to evaluate the dependence and, thus, the hypotheses. This research was based on Pearson correlation, also known as Pearson product moment correlation (PPMC), which indicates a linear relationship between two datasets. Simply put, it answers the question of whether there is any dependence between the variables under study [

52]:

Based on this, the hypotheses were evaluated. Descriptive statistics were used to assess the trend and the results were confirmed with a significance test that indicated whether there was a strong correlation or not. It is only possible to accept results where there is a strong correlation; otherwise, one cannot be sure that the identified connection is not just a coincidence.

2.3. Research Limitations

Since this topic is still under investigation and companies do not work under stable conditions during research, this study has some limitations that need to be considered when interpreting the results and generalizing the conclusions.

In the first place, it is a matter of abstracting other factors that could affect the companies’ results and, thus, distort the reasons they were obtained. Therefore, only construction companies that undertook no further innovations during the period under review that could have had any impact on the economic indicators under investigation were invited to take part in the research. The companies also stated that no known events in the construction market or the economy could have significantly affected these results. The survey also considered information on how long the company had been operating in the market. Companies that had been recently founded were not invited to participate in the research. These statements mainly concern competitors, since none of the competitors brought an innovative new product to the market, and there were no known events, such as the entry of a new strong player into the market. From a macroeconomic point of view, inflation could have been a factor that could have influenced the results. Considering the time of implementation of the survey and the evaluation of the economic results for 2021 and earlier, this impact was minimal, as this macro-indicator was consistent in the monitored period. Currently, the situation is different. According to predictions and the development of inflation over the last observed period, the situation may be different. However, based on the opinions of several project managers and economists, the effects of using information systems manifest regardless of price developments. This claim can also be substantiated by the fact that our research did not look at and quantify indicators in terms of nominal values but as relative indicators. The advantage is that this approach abstracts from similar situations, such as a decrease or an increase in price levels.

The level of exploitation of ERP systems was given on a scale of 1 to 5, and the assessment was up to the respondent. Therefore, companies could not always determine the level adequately. However, to eliminate inaccuracies in data collection, the level and the method of assessment were thoroughly explained in the description to ensure that the respondents’ indicators were correctly quantified.

The questionnaire was addressed to the management of construction companies. However, the specifics of its completion were anonymous. Only the position of the person responsible for filling it in was indicated. Given the questionnaire’s acceptance and the effort to participate in the survey, it was assumed that the respondents had this information.

The two most used indicators among the key performance indicators relevant to the scope of the research were selected. Based on the literature, we specified this selection in more detail above and provided an explanation of why the subject of the research was costs and revenues. Of course, for a comprehensive understanding and analysis of key performance indicators for economic sustainability in managing construction inputs, it would be appropriate to extend this research to other parameters in the future.

3. Results and Discussion

In this research, we worked with a sample of construction companies that implemented an ERP system and could evaluate the results of the selected KPIs before and after implementation.

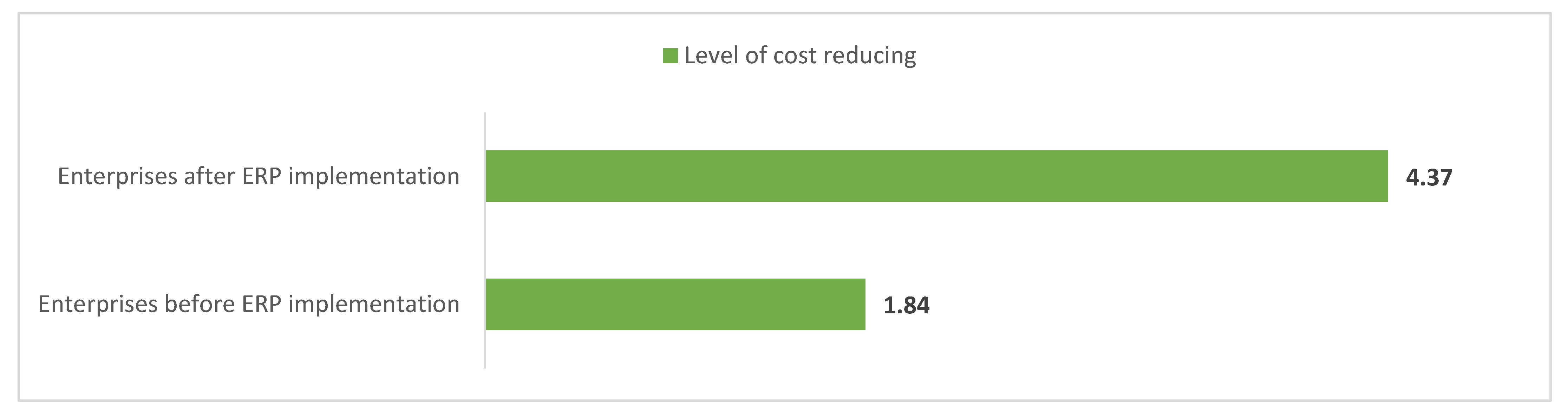

Figure 2 indicates the different levels of costs before and after the implementation of ERP systems in construction companies; i.e., the level of cost reduction. After implementing the ERP system, the levels of cost reductions for the companies were higher than before the implementation.

Businesses use various ERP systems from global developers and companies. Considering the nature of business and the field of construction, one of the basic modules is the project management tool. Based on the extent and complexity of use, the respondents were asked to indicate the level of use and the scope of their ERP systems. The ERPs were mainly products from big players, such as Oracle Fusion Cloud ERP, SAP Business One, Microsoft Dynamics 365, Acumatica, Odoo, and ERPNext, but some were also from national companies, such as KROS Onix, IFS, Helios, etc.

We assumed that the use of an ERP system would lead to an increase in revenues in construction companies. Therefore, revenues were examined in the period before and after ERP implementation. In addition, the level of exploitation of ERP systems in construction enterprises and the correlation between these levels and revenues were also examined.

It is important to discuss what these values mean and their causes. As part of the research, several construction companies were contacted. However, because not all companies have implemented ERP systems, only the results for companies that implemented ERP systems and provided data from the periods before and after implementation were considered. It should also be emphasized that we sought to refine these results for other effects. The construction companies did not invest in innovation in the year they implemented the ERP systems. The companies also declared that, from their point of view, the conditions on the market did not change significantly for them, and they did not notice anything unusual.

Figure 3 shows the frequency for each cost reduction interval. The most significant interval was the cost reduction interval from 5.87 to 17.87%. This value was achieved in 20 projects. A significantly large group (12 respondents) pointed to cost savings of more than 29%. The

p value reached a value of 0.04492, representing a high probability and, thus, indicating that the hypothesis was accepted. These results and their summarization are further commented on below.

In view of the scientific problem,

Figure 4 indicates the average changes in the costs of construction companies after implementing ERP solutions. These are average values that depend on the frequency and level of use of the ERP systems. This means that construction companies that used ERP systems to a low extent after implementation were classed in category 1. Category 5 represents construction companies that made full use of ERP systems.

These results were tested using the Person correlation test and Fisher’s

t-test. They confirmed a significant correlation when the value of

r reached −0.95508244 (

Table 2). The results show that the influence of these tools on the design of economic sustainability was considerable.

Construction companies that used ERP systems at level 5 achieved an average cost reduction of 39.48%, while level 4 use of ERP systems achieved an average cost reduction of 31.65%. Construction companies that used ERP to the lowest extent achieved an average cost reduction of 1.45%. This graph clearly shows that construction companies that use ERP systems achieve higher average cost savings.

These results suggest a relationship between the use of ERP systems and success in reducing costs (as one of the key performance indicators).

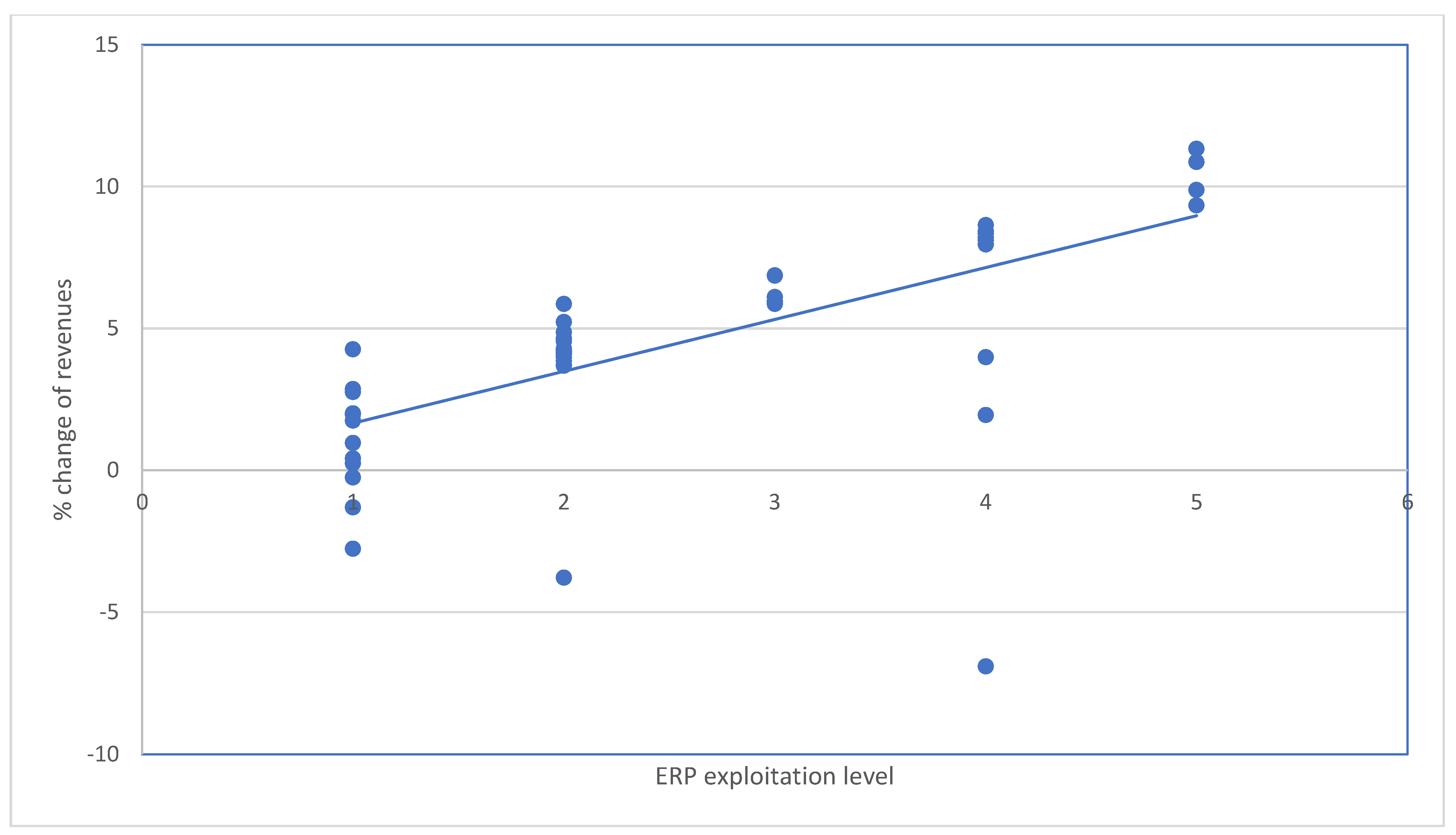

Figure 5 shows the correlations between the use of ERP systems and cost savings as percentages.

As can be seen in the graph, there was a relatively high correlation between the variables. Due to the difference in units of measure (degree of use of ERP systems on a scale from 1 to 5 and cost savings in percentages), the curves correlated with each other. Except in exceptional cases, such as research sample number 44, which demonstrated the opposite effect where costs did not fall but rose, this correlation is clear.

Figure 5 shows the relationship between the rate of use of ERP systems and the level of costs; respectively, the change in costs or the decrease in costs in selected construction projects. A trend curve can be seen in the graph that clearly shows that more significant reductions in costs were achieved with greater use of ERP systems. A Pearson correlation coefficient at the level of r −0.95508244, which represents a significant correlation, also confirmed significant dependence.

This may indicate a high degree of dependence, and it is essential to discuss why this situation occurred. As already mentioned, the survey involved respondents who confirmed that they did not implement any other innovations other than implementing the ERP system. They also declared no other fundamental changes for the construction company during the period under review from either macro or micro points of view.

Based on the above information, it can be stated that the changes (cost savings) that occurred after the implementation of the ERP system were caused by the implementation and use of the ERP system, as this was the only known innovation in the period under review. After analyzing costs and using other research data on costs, we concluded that savings were likely to have occurred in the costs of managing construction projects. These cost items include communication, information exchange, and documents. Likewise, in the design phase and in the context of economic sustainability, it is possible to say that there may have been indirect savings for material items and work with changes in project documentation. Furthermore, the results point to a trend indicating that savings also occurred for the capital itself. Better planning of financial resources leads to reductions in the costs for foreign resources (such as interest on and fees for real estate loans and the like). Better design and planning of financial resources thus also leads to an improvement in the design of economic sustainability.

As one of the key performance indicators, costs can be reduced in several ways, which are discussed in theories and applied by managers. Tracking cost items and comparing plans with reality are effective ways to optimize costs in the management of construction companies.

Based on the above data and the performed tests, hypothesis HA0 that “ERP systems do not reduce the costs of construction enterprises” can be rejected at the significance level of 0.05 and, therefore, hypothesis HA1 can be accepted. If we accept hypothesis HA0, we can conclude that ERP systems reduce the costs of construction enterprises.

With the use of ERP systems, these cost items can be continuously monitored and evaluated. This leads to better information and data, based on which managers can make the right decisions. Sustainability in the management of construction companies (especially economic sustainability) can be achieved through efforts to keep key performance indicators under control. Cost management, supported by information and communication technologies, is a way to achieve this goal.

ERP systems have impacts on several cost items in terms of the structure and breakdown of costs. A negative impact was found for capital and investment costs, which logically increase after implementation. However, the economic benefit should be balanced by the savings in project management costs—that is, administrative costs due to automation, process efficiency, and work efficiency—and in the costs of communication and document sharing. ERP systems seem to be equally beneficial in reducing direct costs, such as the costs of construction materials or labor. Better planning leads to cost reductions in this area as well.

These considerations also had to be scientifically and statistically proven through other methods. Pearson correlation analysis showed a strong dependence between the variables. Our analysis confirmed the strong dependence, and these values can be seen in

Table 3.

The implementation of ERP systems significantly influenced the efforts of the intelligent and sustainable management of the construction companies researched in terms of costs. Based on these results, it can be said that ERP systems demonstrably contribute to a higher degree of economic sustainability in terms of cost management.

On this basis, the null hypothesis that ERP systems do not affect the costs of construction companies can be rejected; on the contrary, ERP systems have an impact on the costs of construction companies. Therefore, this proved that economic sustainability in terms of the selected key performance indicator (costs) was fulfilled.

Revenues were another key performance indicator examined. Based on the analysis of the research already conducted—which did not precisely confirm whether the relationship between the use of the ERP system and the level of sales was exact—we judged that there was a need to examine this area.

Looking at the changes in revenue before and after the implementation of ERP systems, in this case, there was a trend toward an increase in revenue after their implementation. This was because the difference between the revenues was not as significant as when looking at costs (

Figure 6).

An overall view of the development of construction companies’ revenues after implementing ERP systems is provided in

Figure 7. In most cases, the surveyed construction companies recorded an increase in sales after implementing the ERP system. However, the overall average change in revenue growth was smaller than the change in costs. The increase in sales was mainly recorded as 0 to 12%. However, some construction companies also saw a decline in sales. From this point of view, it can be seen that there was a trend toward an increase in sales at several construction companies after implementing ERP systems, but in a specific group, there was also a decrease or a minimal change.

Figure 7 shows the frequencies of particular intervals for the increase or decrease in sales after implementing ERP systems. Most respondents said they observed an increase in sales from 3 to 6.3%. Several businesses experienced a drop in sales. However, this trend was not significant.

Based on the tests, the value of r was found to be level (

Table 4). This was a moderately strong correlation. Assessing this dependence highlighted a trend. There is room for debate about whether the implementation of ERP systems in the phase for the design and modeling of economic sustainability was the main reason for these results. From an economic point of view, it is essential to look at the sources of revenue and the results of management for individual activities. The positive point is that, for all companies that reported high use of ERP systems for sustainable design of economic efficiency, these sales increased. This activity even represented the highest percentage increase, which can be attributed to the good economic results produced by the better planning and design of economic parameters and their impacts in the management of construction projects.

Figure 8 shows the average percentage changes in sales for individual groups. As can be seen, the construction companies using ERP systems achieved the highest increases in sales at 10.36%. The average increase in sales for all groups was also recorded. However, the less that ERP systems were used—at utilization rates of 3, 2, and 1—the smaller the average revenue growth was. This was not the case for group 4, which paradoxically recorded lower average revenue growth than construction companies that used ERP systems at level 3.

These first results suggested that the trend in and the positive effect of using ERP systems in the management of construction companies would most likely be demonstrated here as well. However, given the developments and these data, a strong correlation was not expected here. In other words, the relationship between the use of ERP systems and the results achieved for the market indicator would not be as strong as, for example, the results in terms of costs. These considerations were also confirmed by the mounting image (

Figure 9).

Comparing both curves makes it possible to see several defects in the mentioned data simulation. Some construction companies even saw a drop in sales. Their percentages were more significant than those observed with regard to changes in costs.

Figure 9 shows the relationship between the use rate of ERP systems and sales; i.e., the change in sales after implementing the ERP system. A trend curve can be seen in the graph indicating that, with greater use of ERP systems, there was a slight increase in sales. However, these results were less significant than the results for cost reduction. The Pearson correlation coefficient, which was at the level of r 0.651419296, did not indicate a significant correlation.

Before the final refutation of the investigated hypotheses, it is necessary to look at the data from the Pearson correlation analysis, as these data define the relationship between the investigated variables (

Table 5).

The Pearson correlation coefficient reached 0.651419296, which does not represent a strong correlation. Therefore, the null hypothesis that the use of ERP systems in construction companies does not affect revenue growth cannot be rejected based on this analysis. However, the opposite cannot be stated either—i.e., that the use of ERP systems affects sales growth—even though there was a certain degree of dependence there. Nevertheless, based on the scientific results, it can be concluded that this was a trend.

However, the p value did not reach the level that would clearly statistically confirm these results; i.e., a probability of p 0.05. Based on this, the hypothesis Hb0, “ERP systems do not increase the revenues of construction enterprises”, cannot be refuted. The basis for this is the trend showing that, in many cases, the implementation of ERP systems led to an increase in sales. However, this claim was not statistically significantly confirmed based on the tests carried out.

Again, it is necessary to discuss why our expectations were not met and why the results did not confirm the expected situation, even though the conditions for this variable were even.

With their functionality, ERP systems can help control costs to a greater extent. However, the amount of revenue is affected by managerial skills and, thus, the right decisions, as well as many other factors. It is possible to reduce costs through monitoring. Monitoring cost items and finding ways to undertake such monitoring in practice should be based on up-to-date data. However, it is not possible to obtain another order based on ERP data. Other factors influence this. Therefore, from this point of view, it was not confirmed that implementing ERP systems would bring an increase in sales that could be statistically proven. On the other hand, however, it must be said that the opposite is not valid. Thus, ERP systems in some companies (the more significant ones) pointed to a positive effect. These claims can also be turned toward economic sustainability itself. Based on research where the relationship between selected key performance indicators and economic sustainability has been statistically confirmed [

40], it can be stated that the use of ERP systems has a positive impact on economic sustainability in the construction sector.

A comparative study from Germany, Slovenia, and Croatia described the application of modern management approaches in construction companies [

22]. The authors did not focus on specific economic indicators, and the management of resources and projects was, as described in the study, random. In the context of the perception of EPR systems as a narrower part of information systems, it is essential to mention that the savings at this scale cannot be compared with the results of this study. Above all, the economic sustainability perspective and the quantification of the impact of ICT use need to be present in previous research.

Drawing on the study where the importance of technology for project management in the construction industry was addressed and where the critical success factors for construction projects were investigated [

33], it is possible to agree with the statement that these technologies have an impact on these key performance indicators. This is also one of their benefits.

4. Conclusions

The exploitation of ERP systems in construction companies does not reach the highest level. Our research on the use of ERP systems in construction companies showed a lower level of use among small construction companies. ERP systems are used to a greater extent by large construction companies and some medium-sized ones. Utilization rates may have affected the research results or the results may have been altered to a greater extent.

This research focused on ERP systems and the impact of their implementation and use in construction companies, monitoring their effects on selected key performance indicators in the context of intelligent and sustainable management. Economic sustainability is understood as management that aims to achieve selected economic indicators at better values. ERP systems should help meet these business goals. In a thorough analysis, costs and revenues were selected from among the benchmarks. Their development in the context of the implementation and use of ERP systems is scientifically fascinating.

Therefore, this research looked at the relationship between the use of ERP systems in the management of construction companies and two variables (costs and revenues). We found a strong correlation between the utilization rates of ERP systems and cost reductions. Based on the above, it was accepted that ERP systems have a positive effect on reducing costs. Therefore, ERP systems contribute as intelligent tools to the sustainable management of construction companies.

However, this claim could not be confirmed when looking at the sales. The Pearson correlation analysis did not confirm a strong relationship between the degree of use of ERP systems and the rate of revenue growth. However, it should be emphasized that a specific positive trend was recorded here, and most construction companies achieved a weight gain after implementing ERP systems. However, there was also a group of companies that saw a decline.

The results highlight the need to discuss the dependence between the variables. Thus, ERP systems reduced costs and increased sales in architecture, engineering, and construction companies. It is also essential to look at the financial results and their composition. These results were positive in terms of the main economic activities of the enterprises, which leads to the indisputable conclusion that the design of economic sustainability through these systems is important.

In light of the results for the development of revenues, it is important to look at selected key performance indicators and expand the possible research questions. If the increase in sales was not demonstrably confirmed by the impact of the use of ERP systems in the management of construction companies (but only a trend where most companies saw an increase in revenues), is the same true for the satisfaction of the customers (clients) or the return of already satisfied customers? Alternatively, what is the level of performance of employees who have not brought new contracts (productivity)?

It is important to look at the possible limitations of the research and the factors involved. First, this research involved abstracting other factors that could affect the companies’ results and, thus, distort the reasons they were obtained. High levels of data integrity and consistency were ensured during the study through the verification of the results and data. From this point of view, these factors were effectively managed. The clear description used and the scalability of the data based on the clearly defined quantitative results achieved should have prevented subjective evaluation among the respondents. The basic financial data were obtained from official sources, such as accounting sources, profit and loss statements, and statistical offices, and through the use of clear rules and quantification methods.

The research shows that it is necessary to ensure that finances and the willingness of management to invest in these solutions are present. From this point of view, other studies (including those carried out by us in the past relating to implementation factors) should be treated similarly to the results of this research. The current situation in the world also deepens this problem, and this situation is expected to intensify in the future.

These are other unanswered questions where there is room for further research. Such research should comprehensively show the impact of using ERP systems on key performance indicators. Other parameters are also essential in intelligent management and economic sustainability to determine construction companies’ overall performance and success.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}