Developments of Efficient Trigonometric Quantile Regression Models for Bounded Response Data

Abstract

:1. Introduction

2. Preliminary Knowledge

2.1. Trigonometric Classes of Distributions

2.2. UGHN Distribution

3. Trigonometric UGHN Distributions

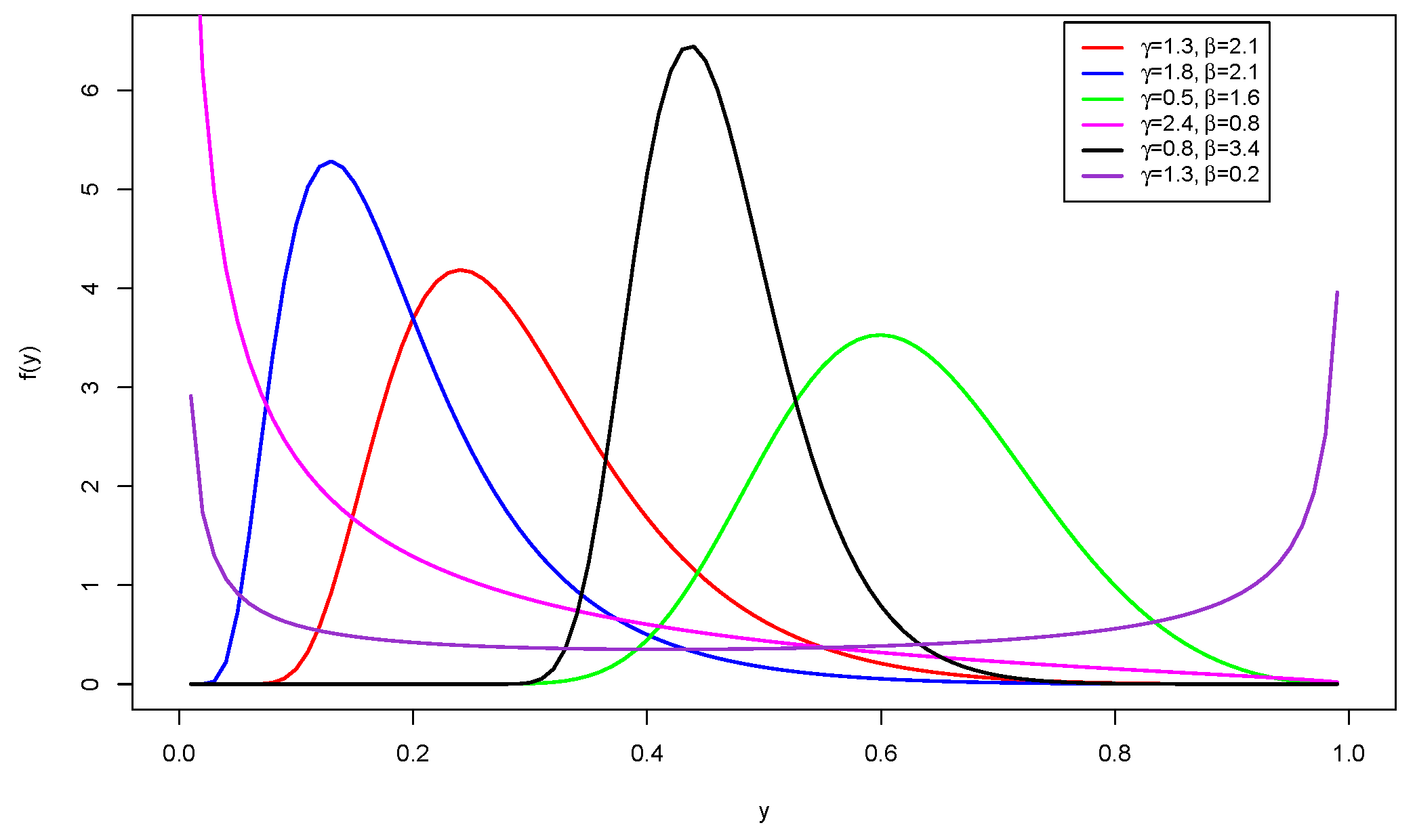

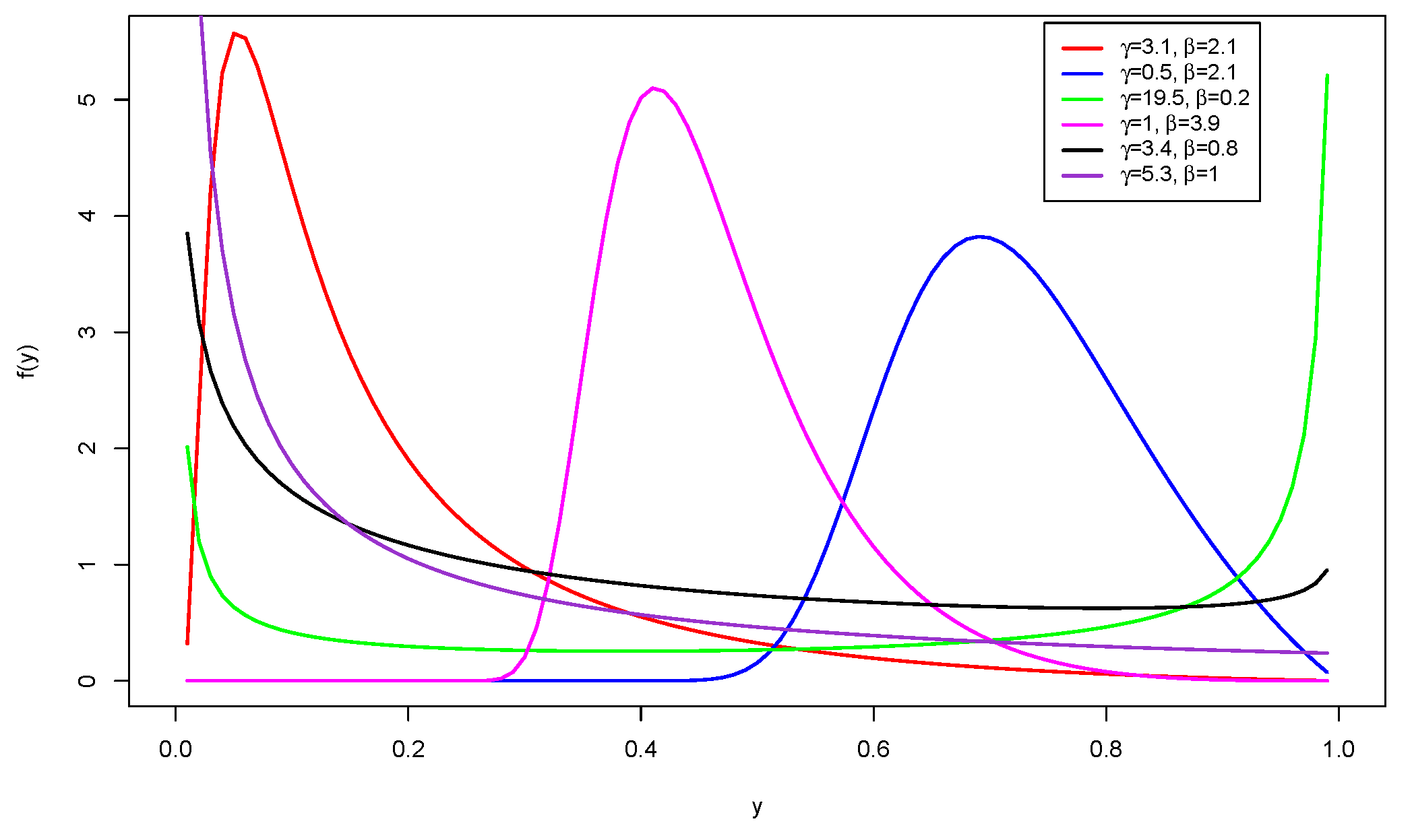

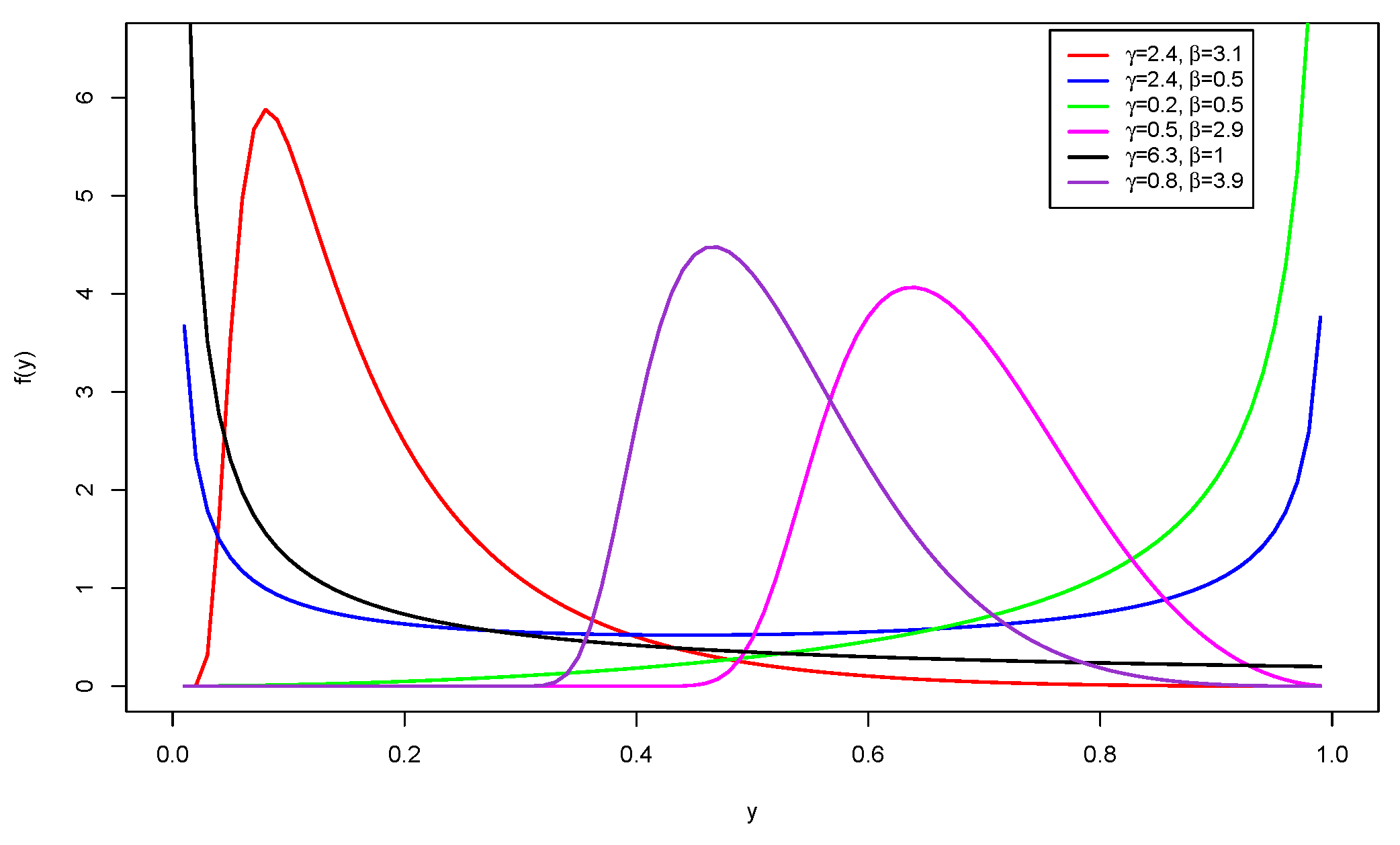

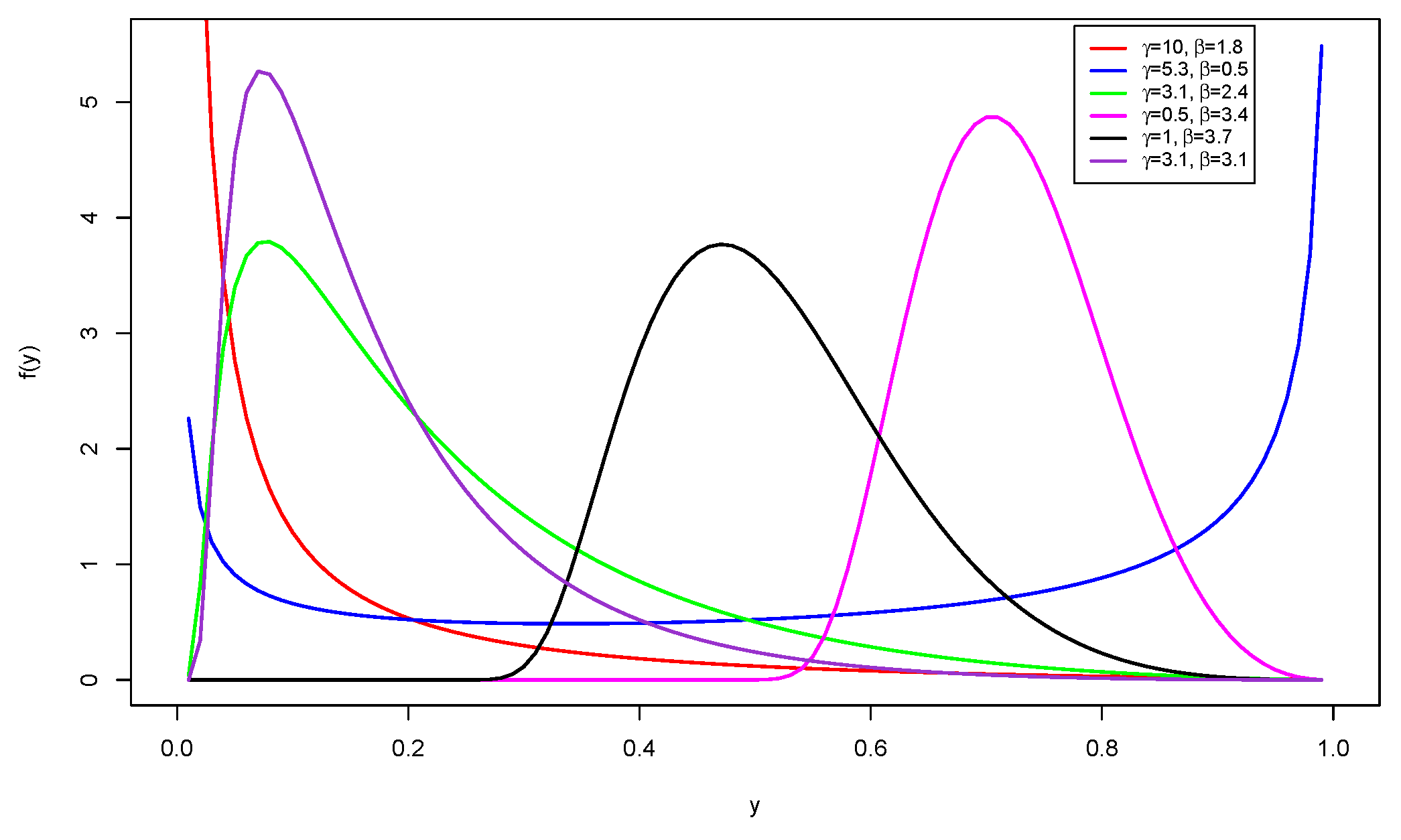

3.1. SUGHN Distribution

3.2. CUGHN Distribution

3.3. TUGHN Distribution

3.4. SCUGHN Distribution

4. Quantile PDFs of the Trigonometric Forms of the UGHN Distribution

5. Quantile Regression Model, Estimation and Residual Analysis

5.1. Quantile Regression Model

5.2. Parameter Estimation

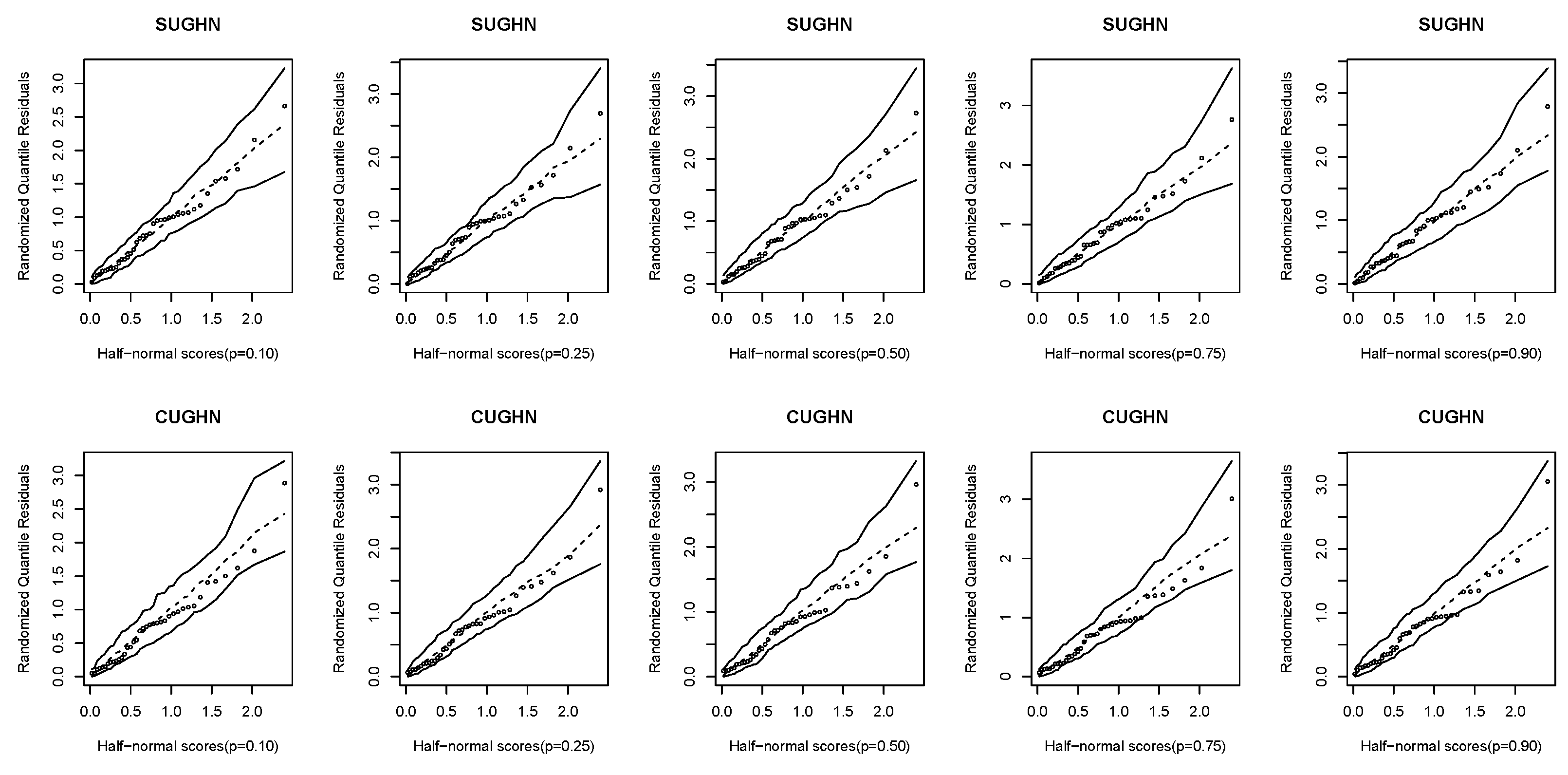

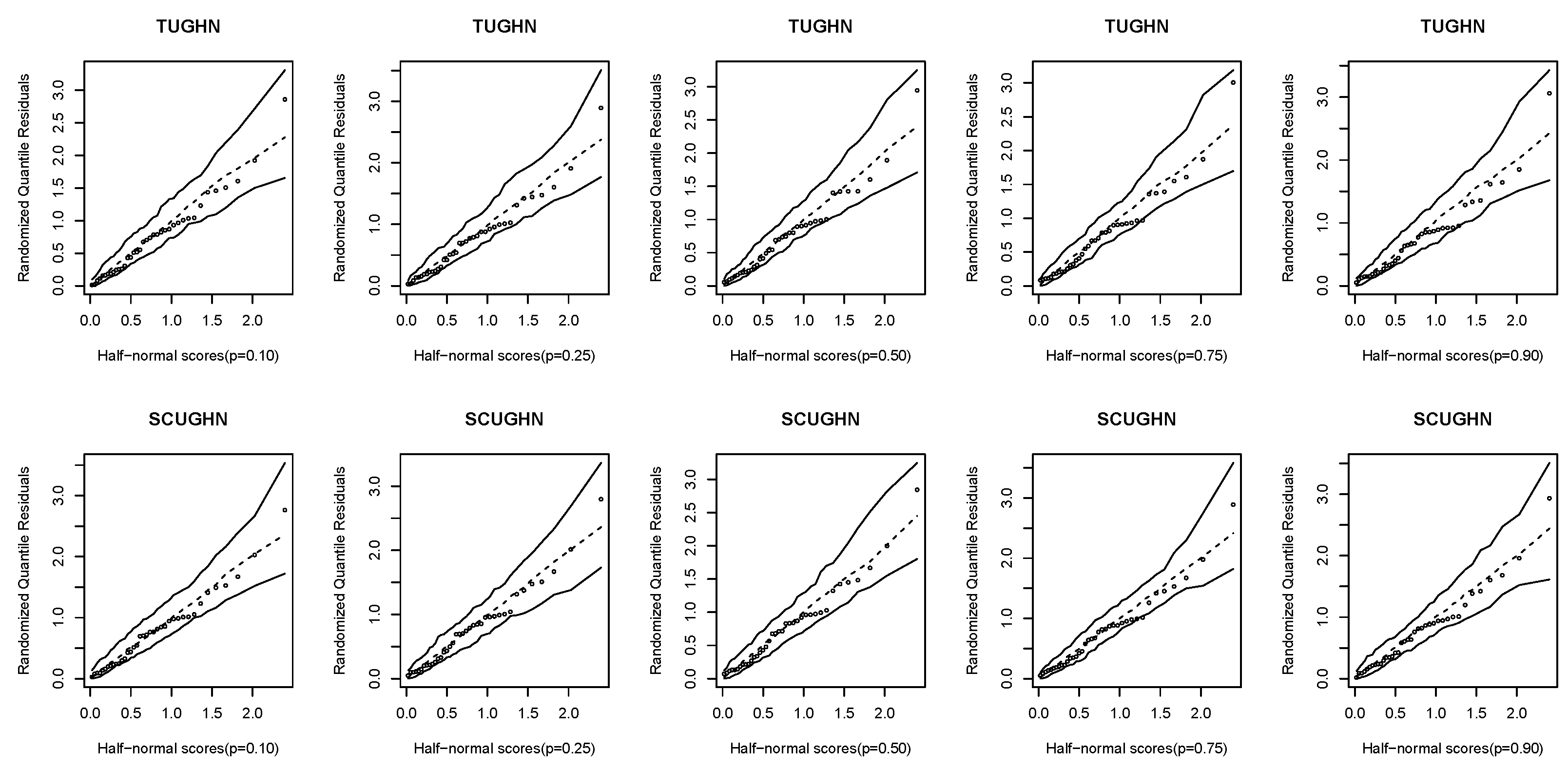

5.3. Residual Analysis

6. Monte Carlo Simulations

- For the SUGHN distribution, for any , we considerwhere and is an observation from the standard uniform distribution.

- For the CUGHN distribution, we considerwhere .

- For the TUGHN distribution, we considerwhere .

- For the SCUGHN distribution, we considerwhere .

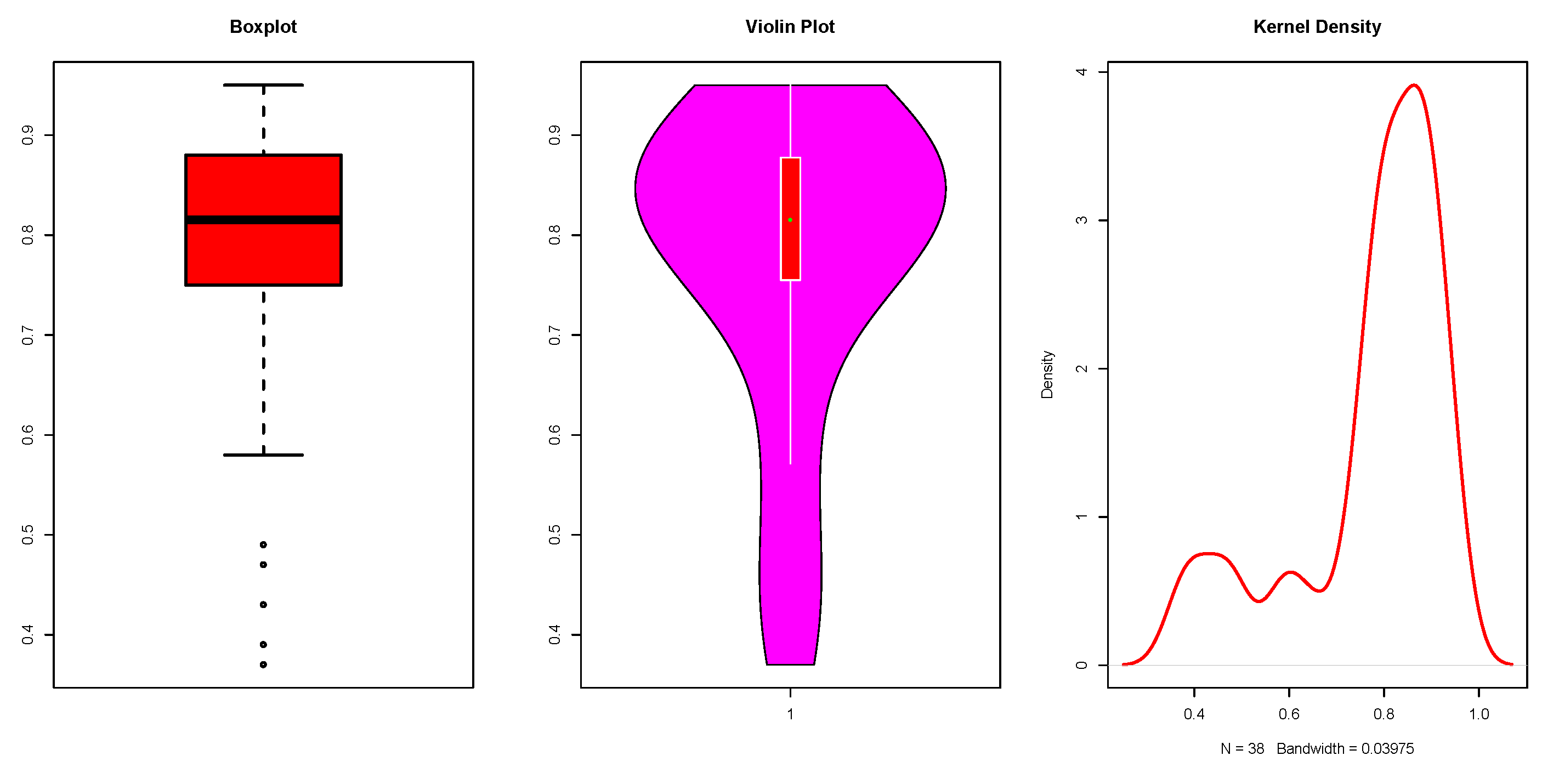

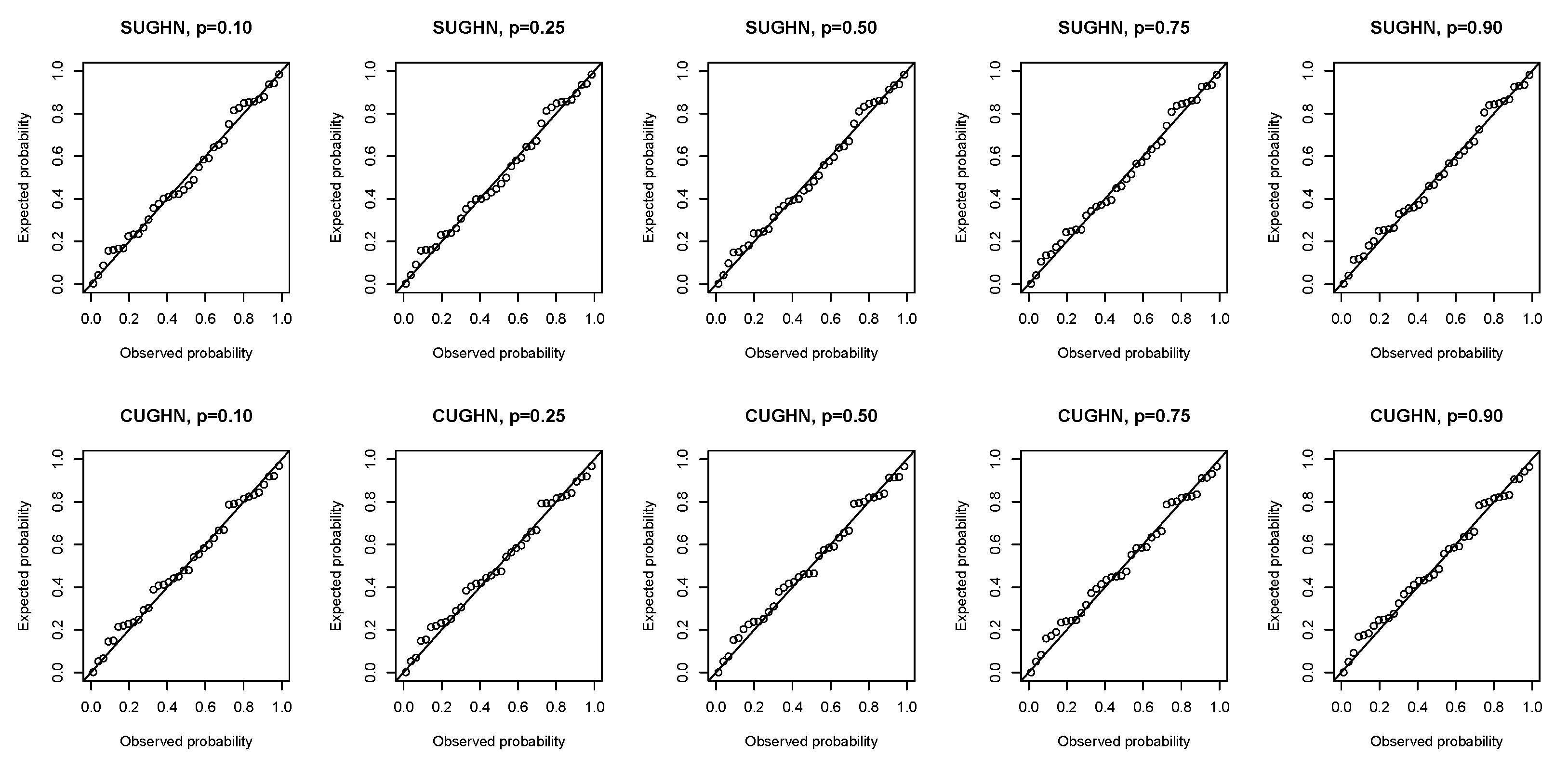

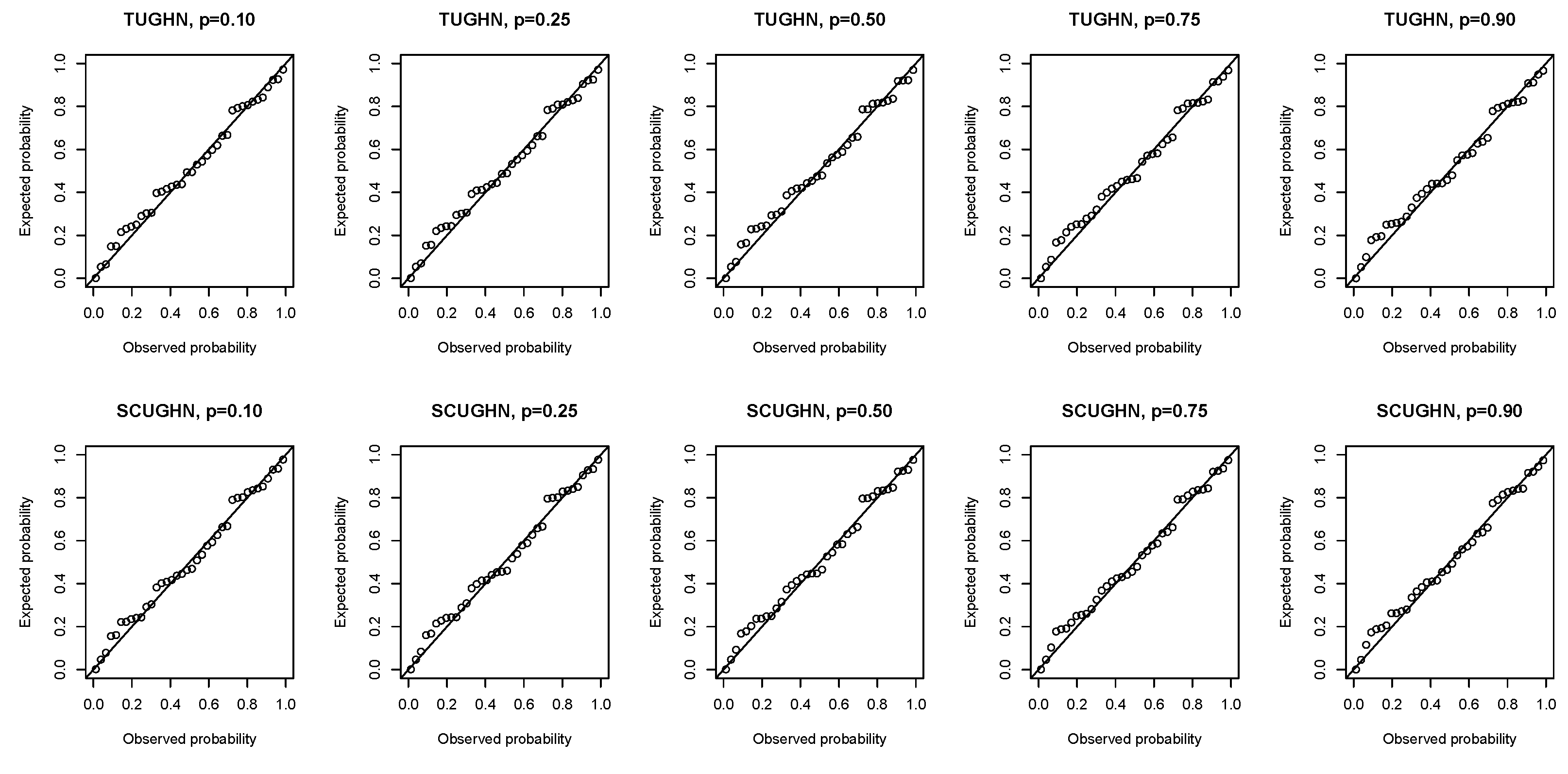

7. Empirical Application

8. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Ferrari, S.; Cribari-Neto, F. Beta regression for modelling rates and proportions. J. Appl. Stat. 2004, 31, 799–815. [Google Scholar] [CrossRef]

- Mazucheli, J.; Alves, B.; Korkmaz, M.Ç; Leiva, V. Vasicek quantile and mean regression models for bounded data: New formulations, mathematical derivations and numerical applications. Mathematics 2022, 10, 1389. [Google Scholar] [CrossRef]

- Altun, E. The log-weighted exponential regression model: Alternative to the beta regression model. Commun. Stat. Theory Methods 2021, 50, 2306–2321. [Google Scholar] [CrossRef]

- Altun, E.; El-Morshedy, M.; Eliwa, M.S. A new regression model for bounded response variable: An alternative to the beta and unit-Lindley regression models. PLoS ONE 2021, 16, e0245627. [Google Scholar] [CrossRef] [PubMed]

- Altun, E.; Cordeiro, G.M. The unit-improved second-degree Lindley distribution: Inference and regression modeling. Comput. Stat. 2020, 35, 259–279. [Google Scholar] [CrossRef]

- Mazucheli, J.; Menezes, A.F.B.; Chakraborty, S. On the one parameter unit-Lindley distribution and its associated regression model for proportion data. J. Appl. Stat. 2019, 46, 700–714. [Google Scholar] [CrossRef] [Green Version]

- Mazucheli, J.; Korkmaz, M.Ç.; Menezes, A.F.B.; Leiva, V. The unit generalized half-normal quantile regression model: Formulation, estimation, diagnostics and numerical applications. Soft Comput. 2023, 27, 279–295. [Google Scholar] [CrossRef]

- Abubakari, A.G.; Luguterah, A.; Nasiru, S. Unit exponentiated Fréchet distribution: Actuarial measures, quantile regression and applications. J. Indian Soc. Probab. Stat. 2022, 23, 387–424. [Google Scholar] [CrossRef]

- Mustapha, M.H.B.; Nasiru, S. Unit gamma/Gompertz quantile regression with applications to skewed data. Sri Lankan J. Appl. Stat. 2022, 23, 49–73. [Google Scholar] [CrossRef]

- Shekhawat, K.; Sharma, V.K. An extension of J-shaped distribution with application to tissue damage proportions in blood. Sankhya B Indian J. Stat. 2020, 83, 548–574. [Google Scholar] [CrossRef]

- Korkmaz, M.Ç.; Korkmaz, Z.S. The unit log-log distribution: A new unit distribution with alternative quantile regression modeling and educational measurements applications. J. Appl. Stat. 2023, 50, 889–908. [Google Scholar] [CrossRef]

- Ribeiro, T.F.; Pena-Ramírez, F.A.; Guerra, R.R.; Cordeiro, G.M. Another unit Burr XII quantile regression model based on the different reparameterization applied to dropout in Brazilian undergraduate courses. PLoS ONE 2022, 17, e0276695. [Google Scholar] [CrossRef]

- Chesneau, C.; Artault, A. On a comparative study on some trigonometric classes of distributions by the analysis of practical datasets. J. Nonlinear Model. Anal. 2021, 3, 225–262. [Google Scholar]

- Souza, L. New Trigonometric Classes of Probabilistic Distributions. Ph.D. Thesis, Universidade Federal Rural de Pernambuco, Recife, Brazil, 2015. [Google Scholar]

- Korkmaz, M.M.Ç. The unit generalized half normal distribution: A new bounded distribution with inference and application. Sci. Bull.-Univ. Politeh. Bucharest Ser. A 2020, 82, 133–140. [Google Scholar]

- Souza, L.; Junior, W.R.O.; de Brito, C.C.R.; Chesneau, C.; Ferreira, T.A.E.; Soares, L. On the Sin-G class of distributions: Theory, model and application. J. Math. Model. 2019, 7, 357–379. [Google Scholar]

- Souza, L.; Junior, W.R.O.; de Brito, C.C.R.; Chesneau, C.; Ferreira, T.A.E.; Soares, L. General properties for the Cos-G class of distributions with applications. Eurasian Bull. Math. 2019, 2, 63–79. [Google Scholar]

- Souza, L.; Junior, W.R.O.; de Brito, C.C.R.; Chesneau, C.; Ferreira, T.A.E. Tan-G class of trigonometric distributions and its applications. Cubo 2019, 23, 1–20. [Google Scholar] [CrossRef]

- Souza, L.; de Oliveira, W.R.; de Brito, C.C.R.; Chesneau, C.; Fernandes, R.; Ferreira, T.A. Sec-G class of distributions: Properties and applications. Symmetry 2022, 14, 299. [Google Scholar] [CrossRef]

- Ampadu, C.B. The Tan-G family of distributions with illustration to data in the health sciences. Phys. Sci. Biophys. J. 2019, 3, 000125. [Google Scholar]

- Tomy, L.; Satish, G. A review study on trigonometric transformations of statistical distributions. Biom. Biostat. Int. J. 2021, 10, 130–136. [Google Scholar]

- Kumar, D.; Singh, U.; Singh, S.K. A new distribution using sine function—Its application to bladder cancer patients data. J. Stat. Appl. Probab. 2015, 4, 417–427. [Google Scholar]

- Aldahlan, M.A. Sine Fréchet model: Modeling of COVID-19 death cases in Kingdom of Saudi Arabia. Math. Probl. Eng. 2022, 2022, 2039076. [Google Scholar] [CrossRef]

- Ahmadini, A.A.H. Statistical inference of sine inverse Rayleigh distribution. Comput. Syst. Sci. Eng. 2022, 41, 405–414. [Google Scholar]

- Almetwally, E.M.; Meraou, M.A. Application of environmental data with new extension of Nadarajah-Haghighi distribution. Comput. J. Math. Stat. Sci. 2022, 1, 26–41. [Google Scholar] [CrossRef]

- Cooray, K.; Ananda, M. A generalization of the half-normal distribution with applications to lifetime data. Commun. Stat.—Theory Methods 2008, 37, 1323–1337. [Google Scholar] [CrossRef]

- R Core Team. R: A Language and Environment for Statistical Computing; R Foundation for Statistical Computing: Vienna, Austria, 2020; Available online: https://www.R-project.org/ (accessed on 5 October 2022).

- Cox, D.R.; Hinkley, D.V. Theoretical Statistics; Chapman and Hall/CRC: London, UK, 1974. [Google Scholar]

- Dunn, P.K.; Smyth, G.K. Randomized quantile residuals. J. Comput. Graph. Stat. 1996, 5, 236–244. [Google Scholar]

- Atkinson, A.C. Two graphical displays of outlying and influential observations in regression. Biometrika 1981, 68, 13–20. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Parameter | n | SUGHN | CUGHN | TUGHN | SCUGHN | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| AE | AB | RMSE | AE | AB | RMSE | AE | AB | RMSE | AE | AB | RMSE | ||

| 25 | 0.2199 | 0.2611 | 0.3371 | 0.3131 | 0.3391 | 0.4645 | 0.3413 | 0.3645 | 0.5001 | 0.3646 | 0.3725 | 0.5218 | |

| 50 | 0.1989 | 0.2272 | 0.2814 | 0.2482 | 0.2758 | 0.3674 | 0.2708 | 0.2933 | 0.3970 | 0.2907 | 0.2874 | 0.4122 | |

| 100 | 0.1813 | 0.1928 | 0.2306 | 0.1938 | 0.2265 | 0.2812 | 0.2061 | 0.2349 | 0.3012 | 0.2186 | 0.2093 | 0.2938 | |

| 150 | 0.1771 | 0.1734 | 0.2034 | 0.1844 | 0.2093 | 0.2559 | 0.1943 | 0.2188 | 0.2752 | 0.2080 | 0.1795 | 0.2630 | |

| 200 | 0.1692 | 0.1578 | 0.1827 | 0.1834 | 0.1930 | 0.2310 | 0.1908 | 0.1978 | 0.2446 | 0.2006 | 0.1501 | 0.2209 | |

| 25 | 0.3508 | 0.3667 | 0.5715 | 0.3840 | 0.4076 | 0.6396 | 0.4060 | 0.4269 | 0.6664 | 0.4106 | 0.4256 | 0.6736 | |

| 50 | 0.2804 | 0.2949 | 0.4585 | 0.3486 | 0.3661 | 0.5738 | 0.3656 | 0.3837 | 0.6017 | 0.3580 | 0.3645 | 0.5953 | |

| 100 | 0.2476 | 0.2531 | 0.3785 | 0.2495 | 0.2705 | 0.4263 | 0.2606 | 0.2798 | 0.4505 | 0.2471 | 0.2483 | 0.4411 | |

| 150 | 0.2033 | 0.2109 | 0.3118 | 0.2584 | 0.2647 | 0.3990 | 0.2700 | 0.2774 | 0.4254 | 0.2434 | 0.2279 | 0.4028 | |

| 200 | 0.2059 | 0.2043 | 0.2857 | 0.2345 | 0.2352 | 0.3498 | 0.2448 | 0.2433 | 0.3737 | 0.2203 | 0.1909 | 0.3470 | |

| 25 | 0.8129 | 0.3233 | 0.3976 | 0.7769 | 0.4018 | 0.4743 | 0.7753 | 0.4297 | 0.4997 | 0.7407 | 0.4393 | 0.5159 | |

| 50 | 0.8129 | 0.2259 | 0.2860 | 0.8055 | 0.3024 | 0.3780 | 0.8027 | 0.3289 | 0.4062 | 0.7692 | 0.3292 | 0.4198 | |

| 100 | 0.8002 | 0.1564 | 0.1994 | 0.8148 | 0.2081 | 0.2654 | 0.8109 | 0.2234 | 0.2893 | 0.7841 | 0.2120 | 0.2959 | |

| 150 | 0.8069 | 0.1234 | 0.1572 | 0.8096 | 0.1679 | 0.2141 | 0.8083 | 0.1811 | 0.2325 | 0.7784 | 0.1603 | 0.2305 | |

| 200 | 0.8027 | 0.1093 | 0.1388 | 0.8085 | 0.1417 | 0.1830 | 0.8040 | 0.1499 | 0.1976 | 0.7808 | 0.1263 | 0.1930 | |

| 25 | 0.3193 | 0.0398 | 0.0539 | 0.3139 | 0.0376 | 0.0491 | 0.3132 | 0.0351 | 0.0460 | 0.3158 | 0.0340 | 0.0461 | |

| 50 | 0.3100 | 0.0271 | 0.0346 | 0.3057 | 0.0257 | 0.0328 | 0.3052 | 0.0240 | 0.0307 | 0.3075 | 0.0218 | 0.0297 | |

| 100 | 0.3041 | 0.0184 | 0.0232 | 0.3027 | 0.0177 | 0.0229 | 0.3025 | 0.0163 | 0.0213 | 0.3043 | 0.0137 | 0.0197 | |

| 150 | 0.3031 | 0.0147 | 0.0186 | 0.3030 | 0.0147 | 0.0188 | 0.3027 | 0.0135 | 0.0174 | 0.3041 | 0.0105 | 0.0155 | |

| 200 | 0.3021 | 0.0128 | 0.0162 | 0.3006 | 0.0119 | 0.0153 | 0.3005 | 0.0109 | 0.0142 | 0.3017 | 0.0080 | 0.0121 | |

| Parameter | n | SUGHN | CUGHN | TUGHN | SCUGHN | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| AE | AB | RMSE | AE | AB | RMSE | AE | AB | RMSE | AE | AB | RMSE | ||

| 25 | 0.2137 | 0.2103 | 0.2969 | 0.2794 | 0.2745 | 0.4073 | 0.3413 | 0.3645 | 0.5001 | 0.3184 | 0.3132 | 0.4681 | |

| 50 | 0.1847 | 0.1801 | 0.2462 | 0.2291 | 0.2270 | 0.3259 | 0.2708 | 0.2933 | 0.3970 | 0.2586 | 0.2540 | 0.3716 | |

| 100 | 0.1686 | 0.1529 | 0.2014 | 0.1917 | 0.1871 | 0.2561 | 0.2061 | 0.2349 | 0.3012 | 0.2127 | 0.2079 | 0.2920 | |

| 150 | 0.1500 | 0.1318 | 0.1721 | 0.1651 | 0.1605 | 0.2184 | 0.1943 | 0.2188 | 0.2752 | 0.1866 | 0.1840 | 0.2564 | |

| 200 | 0.1413 | 0.1230 | 0.1588 | 0.1567 | 0.1487 | 0.1973 | 0.1908 | 0.1978 | 0.2446 | 0.1765 | 0.1704 | 0.2306 | |

| 25 | 0.5507 | 0.4727 | 0.5355 | 0.5327 | 0.5480 | 0.5967 | 0.4060 | 0.4269 | 0.6664 | 0.5299 | 0.5809 | 0.6226 | |

| 50 | 0.5957 | 0.3815 | 0.4511 | 0.5811 | 0.4636 | 0.5254 | 0.3656 | 0.3837 | 0.6017 | 0.5679 | 0.5148 | 0.5681 | |

| 100 | 0.6046 | 0.2842 | 0.3542 | 0.5524 | 0.3841 | 0.4512 | 0.2606 | 0.2798 | 0.4505 | 0.5270 | 0.4443 | 0.5069 | |

| 150 | 0.6383 | 0.2454 | 0.3067 | 0.6230 | 0.3082 | 0.3767 | 0.2700 | 0.2774 | 0.4254 | 0.6001 | 0.3691 | 0.4372 | |

| 200 | 0.6409 | 0.2132 | 0.2729 | 0.6362 | 0.2741 | 0.3402 | 0.2448 | 0.2433 | 0.3737 | 0.6165 | 0.3300 | 0.4002 | |

| 25 | 0.4228 | 0.1988 | 0.2529 | 0.4197 | 0.2505 | 0.3123 | 0.7753 | 0.4297 | 0.4997 | 0.4357 | 0.3033 | 0.3744 | |

| 50 | 0.4044 | 0.1340 | 0.1701 | 0.4161 | 0.1796 | 0.2308 | 0.8027 | 0.3289 | 0.4062 | 0.4259 | 0.2258 | 0.2875 | |

| 100 | 0.3985 | 0.0890 | 0.1122 | 0.4094 | 0.1191 | 0.1519 | 0.8109 | 0.2234 | 0.2893 | 0.4127 | 0.1527 | 0.1934 | |

| 150 | 0.4008 | 0.0684 | 0.0868 | 0.4067 | 0.0943 | 0.1210 | 0.8083 | 0.1811 | 0.2325 | 0.4084 | 0.1216 | 0.1557 | |

| 200 | 0.4008 | 0.0606 | 0.0769 | 0.4055 | 0.0814 | 0.1042 | 0.8040 | 0.1499 | 0.1976 | 0.4065 | 0.1049 | 0.1345 | |

| 25 | 0.5426 | 0.0735 | 0.0971 | 0.5363 | 0.0716 | 0.0932 | 0.3132 | 0.0351 | 0.0460 | 0.5344 | 0.0664 | 0.0869 | |

| 50 | 0.5190 | 0.0469 | 0.0617 | 0.5163 | 0.0470 | 0.0603 | 0.3052 | 0.0240 | 0.0307 | 0.5162 | 0.0438 | 0.0564 | |

| 100 | 0.5107 | 0.0317 | 0.0401 | 0.5093 | 0.0326 | 0.0425 | 0.3025 | 0.0163 | 0.0213 | 0.5090 | 0.0303 | 0.0394 | |

| 150 | 0.5061 | 0.0252 | 0.0320 | 0.5074 | 0.0263 | 0.0335 | 0.3027 | 0.0135 | 0.0174 | 0.5074 | 0.0245 | 0.0312 | |

| 200 | 0.5045 | 0.0220 | 0.0282 | 0.5024 | 0.0212 | 0.0271 | 0.3005 | 0.0109 | 0.0142 | 0.5025 | 0.0197 | 0.0251 | |

| p | Model | |||||

|---|---|---|---|---|---|---|

| 0.1 | SUGHN | Estimates | 1.6257 | −0.1656 | −0.0643 | 1.0807 |

| Standard error | 0.2160 | 0.0422 | 0.0214 | 0.1330 | ||

| p-value | < | < | 0.0026 | < | ||

| CUGHN | Estimates | 1.7212 | −0.1865 | −0.0688 | 1.5740 | |

| Standard error | 0.2086 | 0.0427 | 0.0203 | 0.2028 | ||

| p-value | < | < | < | < | ||

| TUGHN | Estimates | 1.7408 | −0.1964 | −0.0680 | 1.7576 | |

| Standard error | 0.2180 | 0.0447 | 0.0193 | 0.2181 | ||

| p-value | < | < | < | < | ||

| SCUGHN | Estimates | 1.6884 | −0.1860 | −0.0652 | 1.9640 | |

| Standard error | 0.2292 | 0.0449 | 0.0198 | 0.2349 | ||

| p-value | < | < | 0.0010 | < | ||

| 0.25 | SUGHN | Estimates | 1.8765 | −0.1540 | −0.0607 | 1.0766 |

| Standard error | 0.2038 | 0.0398 | 0.0198 | 0.1327 | ||

| p-value | < | 0.0001 | 0.0022 | < | ||

| CUGHN | Estimates | 1.9474 | −0.1760 | −0.0652 | 1.5688 | |

| Standard error | 0.1999 | 0.0411 | 0.0189 | 0.2023 | ||

| p-value | < | < | 0.0006 | < | ||

| TUGHN | Estimates | 1.9661 | −0.1849 | −0.0644 | 1.7500 | |

| Standard error | 0.2106 | 0.0433 | 0.0180 | 0.2176 | ||

| p-value | < | < | < | < | ||

| SCUGHN | Estimates | 1.9274 | −0.1737 | −0.0615 | 1.9543 | |

| Standard error | 0.2195 | 0.0431 | 0.0184 | 0.2342 | ||

| p-value | < | < | 0.0008 | < | ||

| 0.5 | SUGHN | Estimates | 2.2111 | −0.1418 | −0.0571 | 1.0714 |

| Standard error | 0.1966 | 0.0373 | 0.0183 | 0.1324 | ||

| p-value | < | 0.0001 | 0.0018 | < | ||

| CUGHN | Estimates | 2.2820 | −0.1636 | −0.0612 | 1.5611 | |

| Standard error | 0.1967 | 0.0391 | 0.0175 | 0.2016 | ||

| p-value | < | < | 0.0004 | < | ||

| TUGHN | Estimates | 2.3123 | −0.1706 | −0.0603 | 1.7382 | |

| Standard error | 0.2083 | 0.0415 | 0.0165 | 0.2167 | ||

| p-value | < | < | 0.0003 | < | ||

| SCUGHN | Estimates | 2.2705 | −0.1593 | −0.0576 | 1.9403 | |

| Standard error | 0.2140 | 0.0412 | 0.0170 | 0.2330 | ||

| p-value | < | 0.0001 | 0.0007 | < | ||

| 0.75 | SUGHN | Estimates | 2.6239 | −0.1302 | −0.0540 | 1.0652 |

| Standard error | 0.2019 | 0.0349 | 0.0170 | 0.1319 | ||

| p-value | < | 0.0002 | 0.0015 | < | ||

| CUGHN | Estimates | 2.7527 | −0.1506 | −0.0576 | 1.5494 | |

| Standard error | 0.2105 | 0.0370 | 0.0161 | 0.2005 | ||

| p-value | < | < | 0.0004 | < | ||

| TUGHN | Estimates | 2.7884 | −0.1556 | −0.0566 | 1.7210 | |

| Standard error | 0.2216 | 0.0396 | 0.0153 | 0.2151 | ||

| p-value | < | < | 0.0002 | < | ||

| SCUGHN | Estimates | 2.7154 | −0.1450 | −0.0542 | 1.9211 | |

| Standard error | 0.2208 | 0.0391 | 0.0158 | 0.2312 | ||

| p-value | < | 0.0002 | 0.0006 | < | ||

| 0.9 | SUGHN | Estimates | 3.0927 | −0.1205 | −0.0517 | 1.0573 |

| Standard error | 0.2249 | 0.0327 | 0.0161 | 0.1314 | ||

| p-value | < | 0.0002 | 0.0013 | < | ||

| CUGHN | Estimates | 3.3459 | −0.1390 | −0.0547 | 1.5332 | |

| Standard error | 0.2518 | 0.0350 | 0.0152 | 0.1991 | ||

| p-value | < | < | 0.0003 | < | ||

| TUGHN | Estimates | 3.3563 | −0.1425 | −0.0539 | 1.6997 | |

| Standard error | 0.2577 | 0.0375 | 0.0145 | 0.2129 | ||

| p-value | < | 0.0001 | 0.0002 | < | ||

| SCUGHN | Estimates | 3.2286 | −0.1328 | −0.0517 | 1.9007 | |

| Standard error | 0.2458 | 0.0369 | 0.0150 | 0.2291 | ||

| p-value | < | 0.0003 | 0.0006 | < |

| p | Model | AIC | BIC | |

|---|---|---|---|---|

| 0.1 | SUGHN | −75.7186 | −67.7186 | −61.1682 |

| CUGHN | −73.9665 | −65.9665 | −59.4161 | |

| TUGHN | −73.6949 | −65.6949 | −59.1445 | |

| SCUGHN | −74.6806 | −66.6806 | −60.1303 | |

| 0.25 | SUGHN | −75.3022 | −67.3022 | −60.7519 |

| CUGHN | −73.5322 | −65.5322 | −58.9819 | |

| TUGHN | −73.2110 | −65.2110 | −58.6606 | |

| SCUGHN | −74.1924 | −66.1924 | −59.6421 | |

| 0.5 | SUGHN | −74.7427 | −66.7427 | −60.1924 |

| CUGHN | −72.8930 | −64.8930 | −58.3426 | |

| TUGHN | −72.4684 | −64.4684 | −57.918 | |

| SCUGHN | −73.4922 | −65.4922 | −58.9419 | |

| 0.75 | SUGHN | −74.1041 | −66.1041 | −59.5537 |

| CUGHN | −72.0697 | −64.0697 | −57.5193 | |

| TUGHN | −71.5349 | −63.5349 | −56.9846 | |

| SCUGHN | −72.6694 | −64.6694 | −58.1190 | |

| 0.9 | SUGHN | −73.5121 | −65.5121 | −58.9618 |

| CUGHN | −71.2425 | −63.2425 | −56.6921 | |

| TUGHN | −70.6513 | −62.6513 | −56.1010 | |

| SCUGHN | −71.9129 | −63.9129 | −57.3625 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Nasiru, S.; Chesneau, C. Developments of Efficient Trigonometric Quantile Regression Models for Bounded Response Data. Axioms 2023, 12, 350. https://doi.org/10.3390/axioms12040350

Nasiru S, Chesneau C. Developments of Efficient Trigonometric Quantile Regression Models for Bounded Response Data. Axioms. 2023; 12(4):350. https://doi.org/10.3390/axioms12040350

Chicago/Turabian StyleNasiru, Suleman, and Christophe Chesneau. 2023. "Developments of Efficient Trigonometric Quantile Regression Models for Bounded Response Data" Axioms 12, no. 4: 350. https://doi.org/10.3390/axioms12040350