The Way to Invest: Trading Strategies Based on ARIMA and Investor Personality

Abstract

:1. Introduction

- Adding investor personality theory to the portfolio model expands the rationality of the investment.

- Expanded the application of Sharpe ratio in the investment field by applying the generalized Sharpe ratio to portfolio models.

- A novel investment strategy portfolio model based on investor personality is proposed.

- Expanded the theory of investment personality theory applied to the stock investment market.

- Assuming no unpredictable fluctuations in the stock market during the forecast period due to large political factors.

- Conservative and aggressive investors follow the principle of limited rationality.

- Conservative investors are more sensitive to changes in tax rates.

- Tax changes will not significantly affect the investment enthusiasm of aggressive investors.

2. Dynamic Trading Strategy Based on ARIMA

2.1. Predictive Modeling

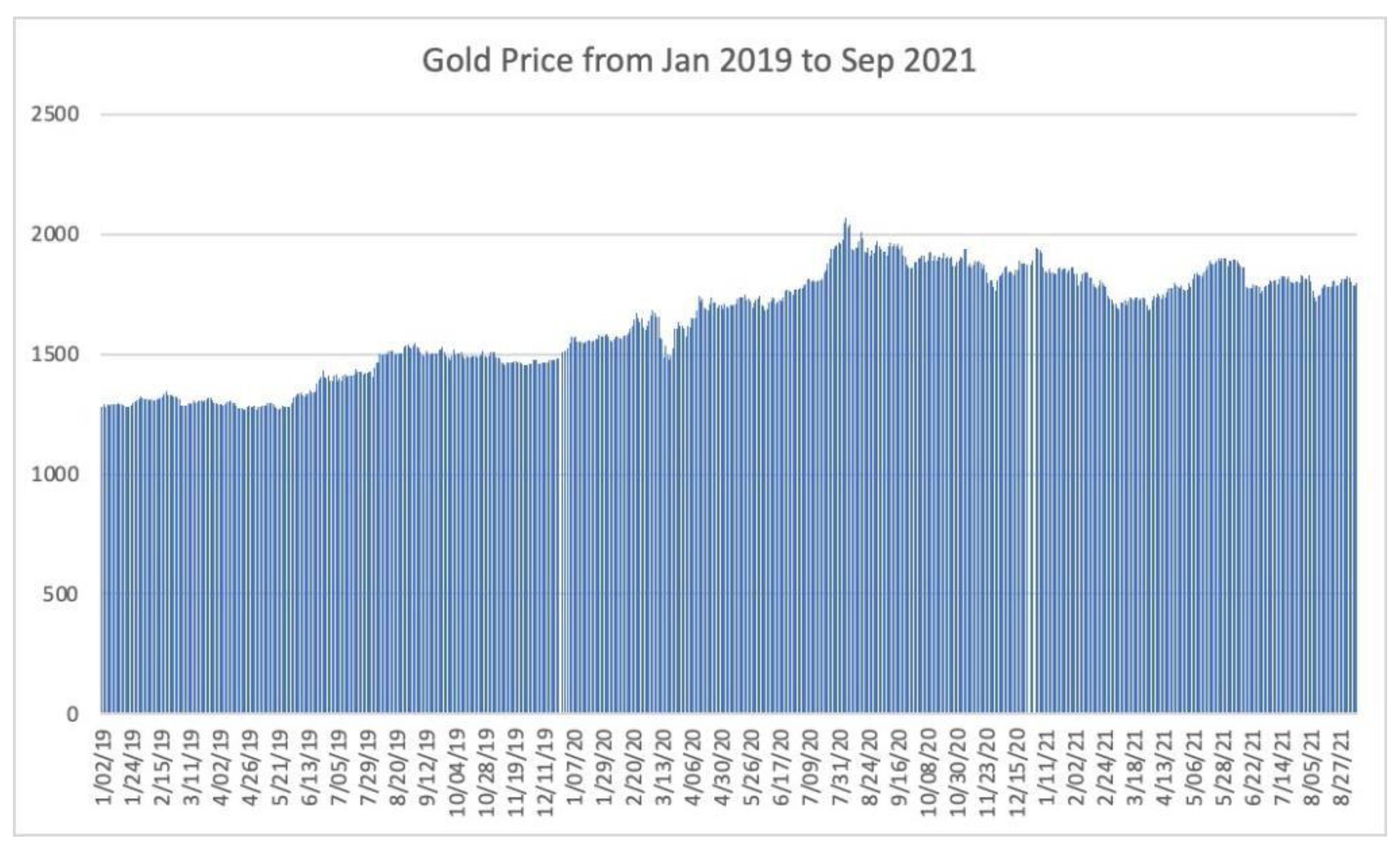

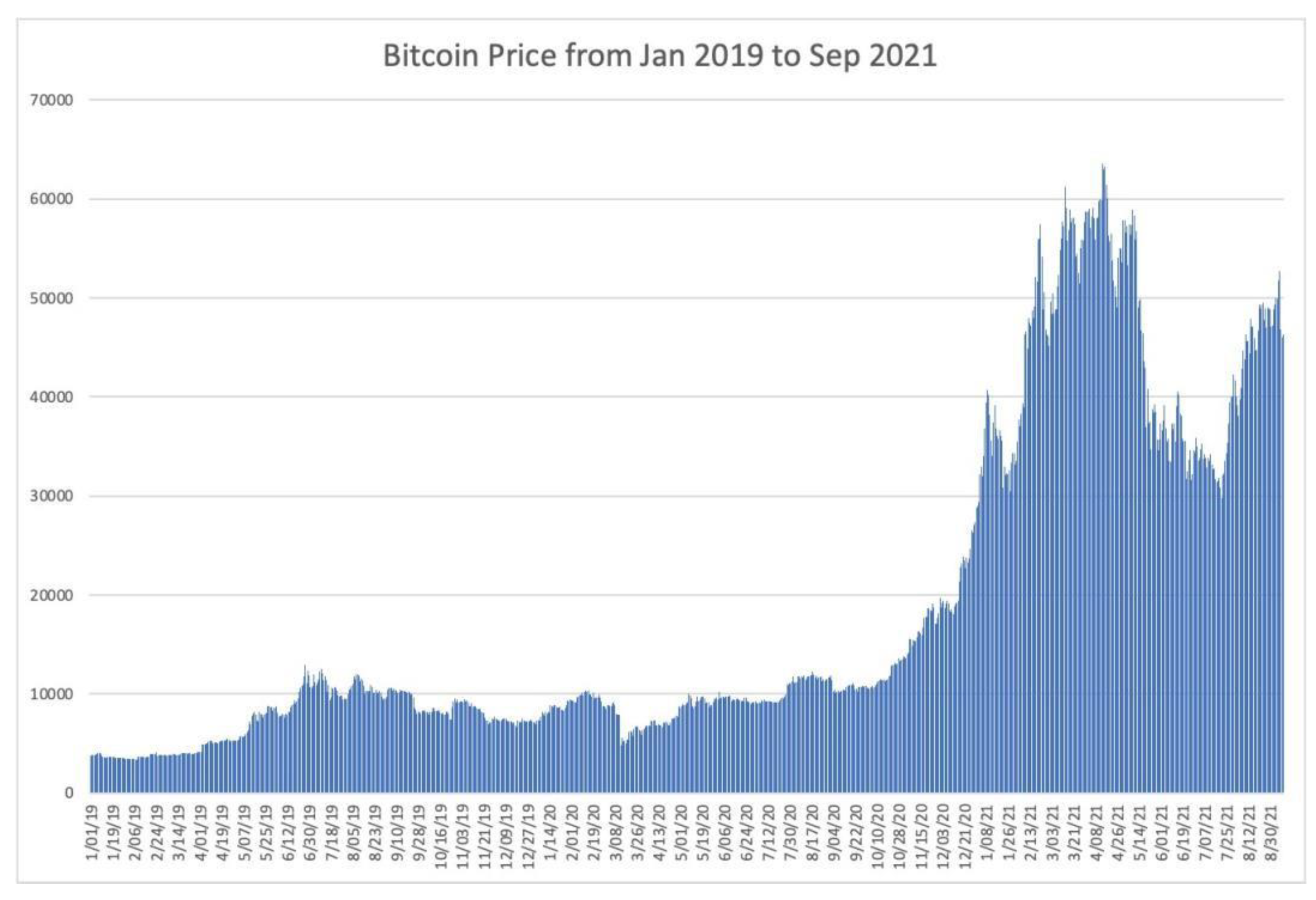

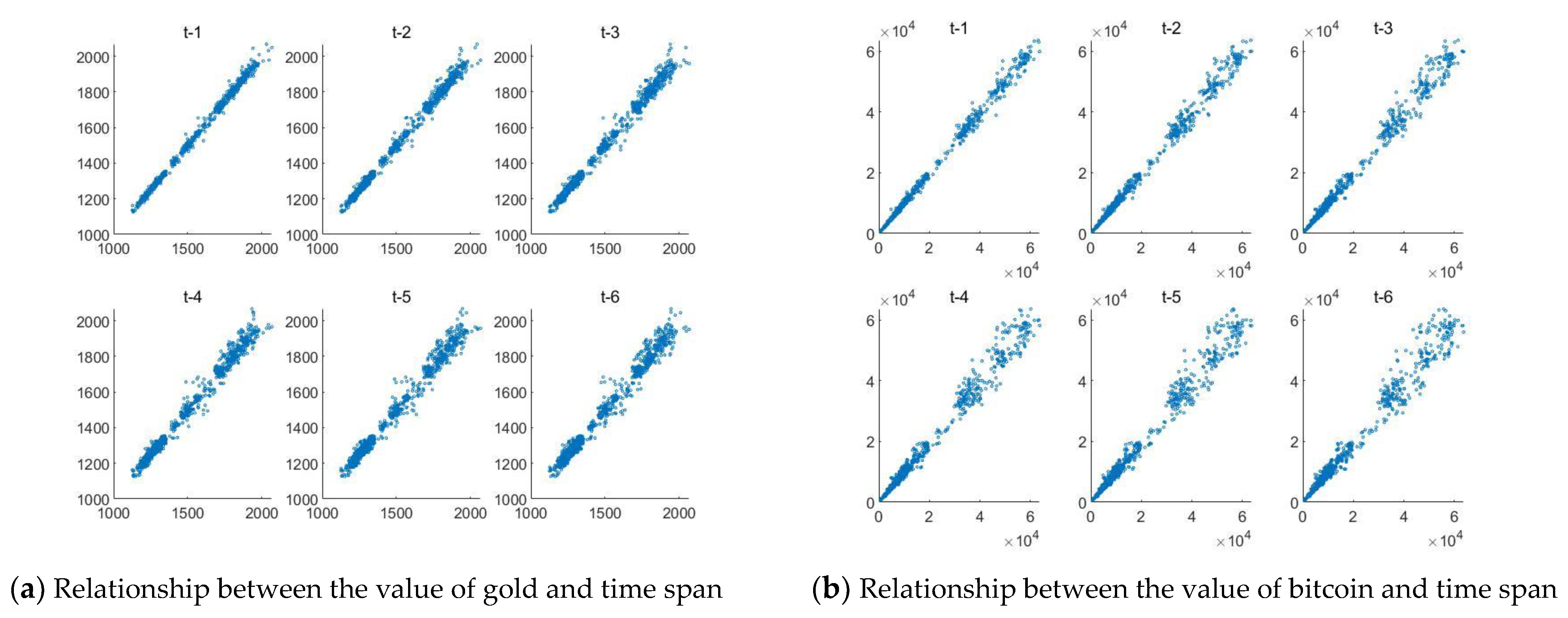

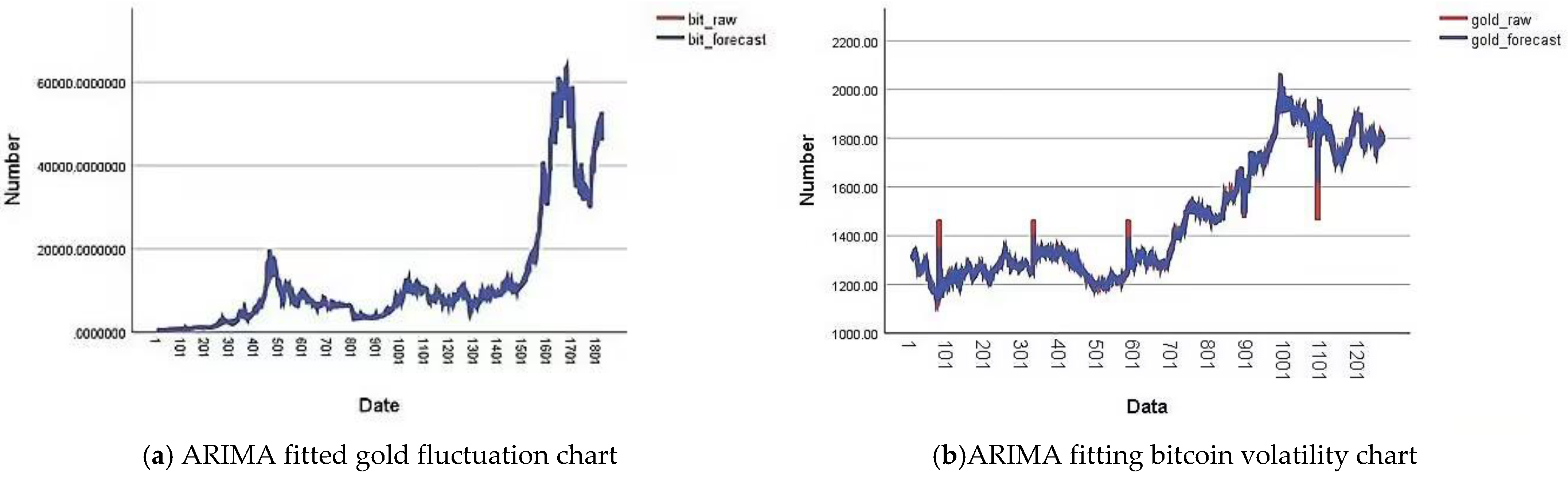

2.1.1. Settlement Price Forecast Analysis

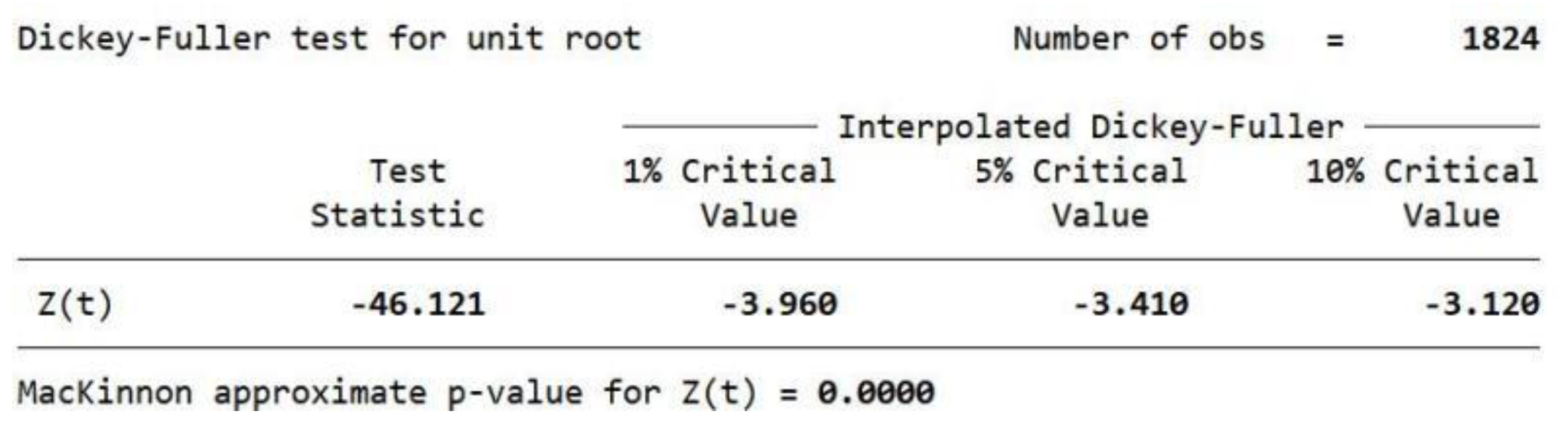

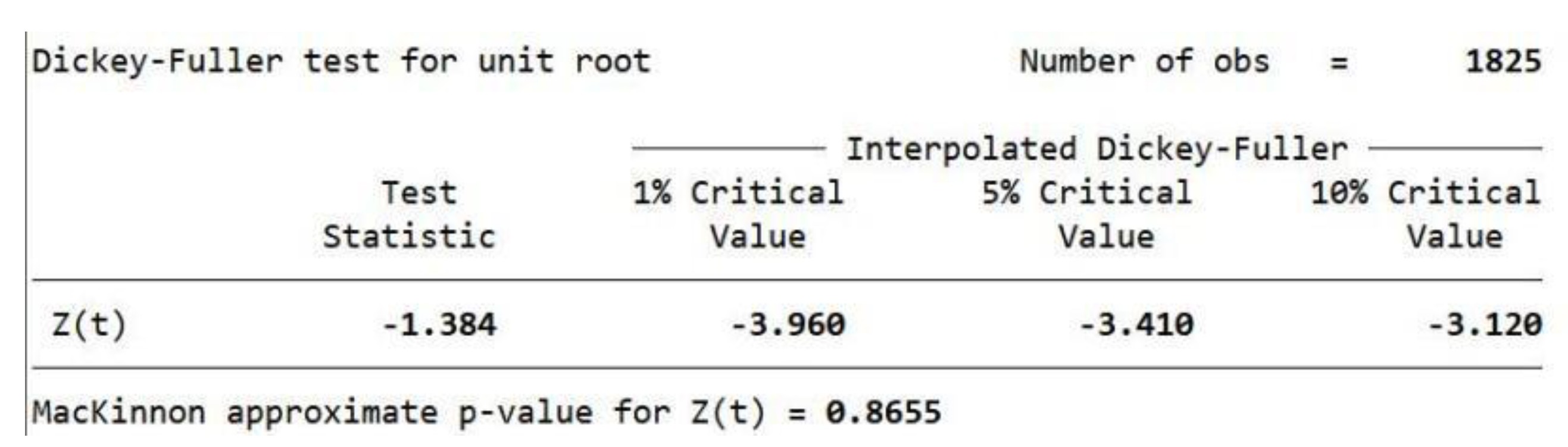

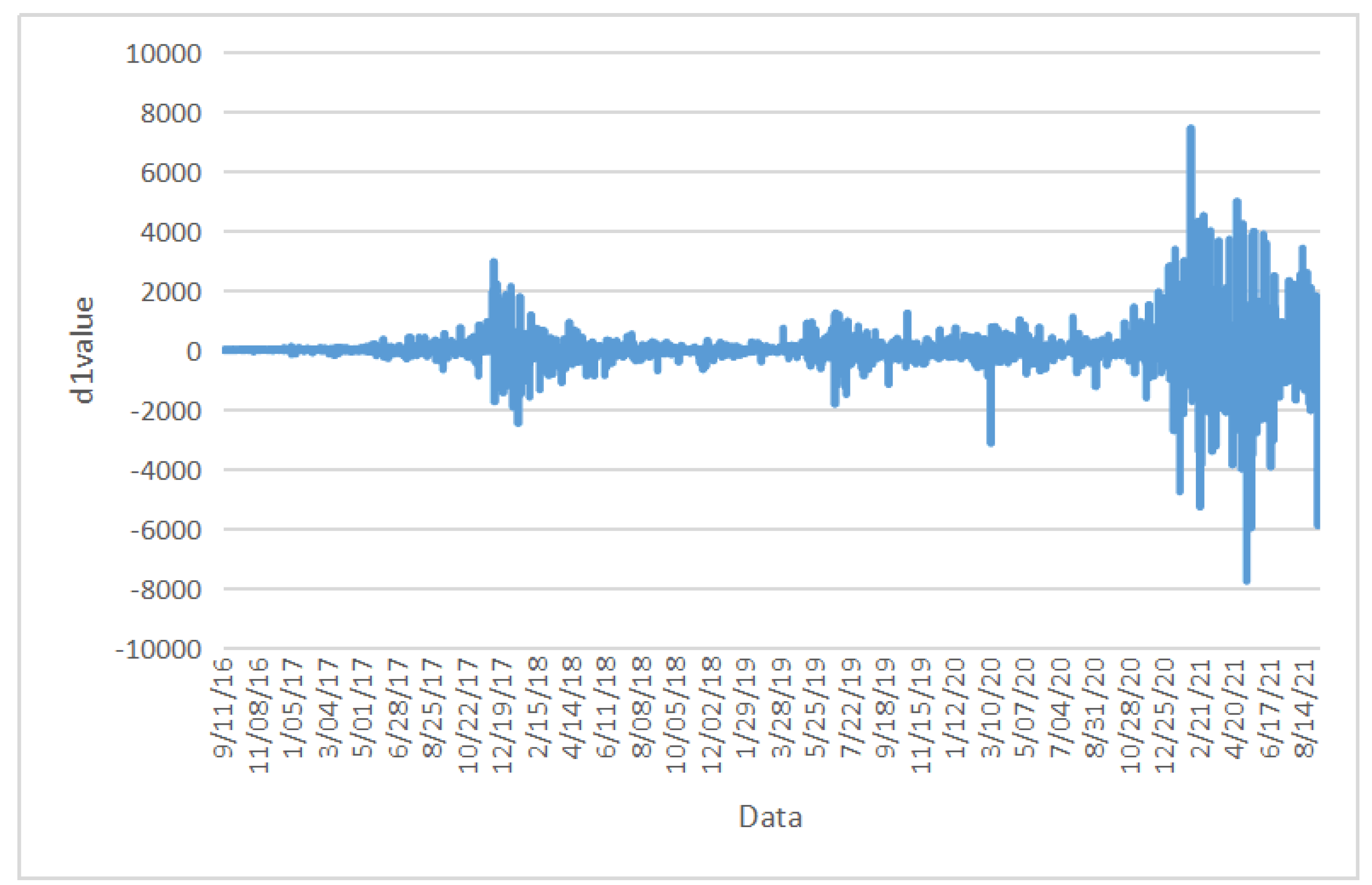

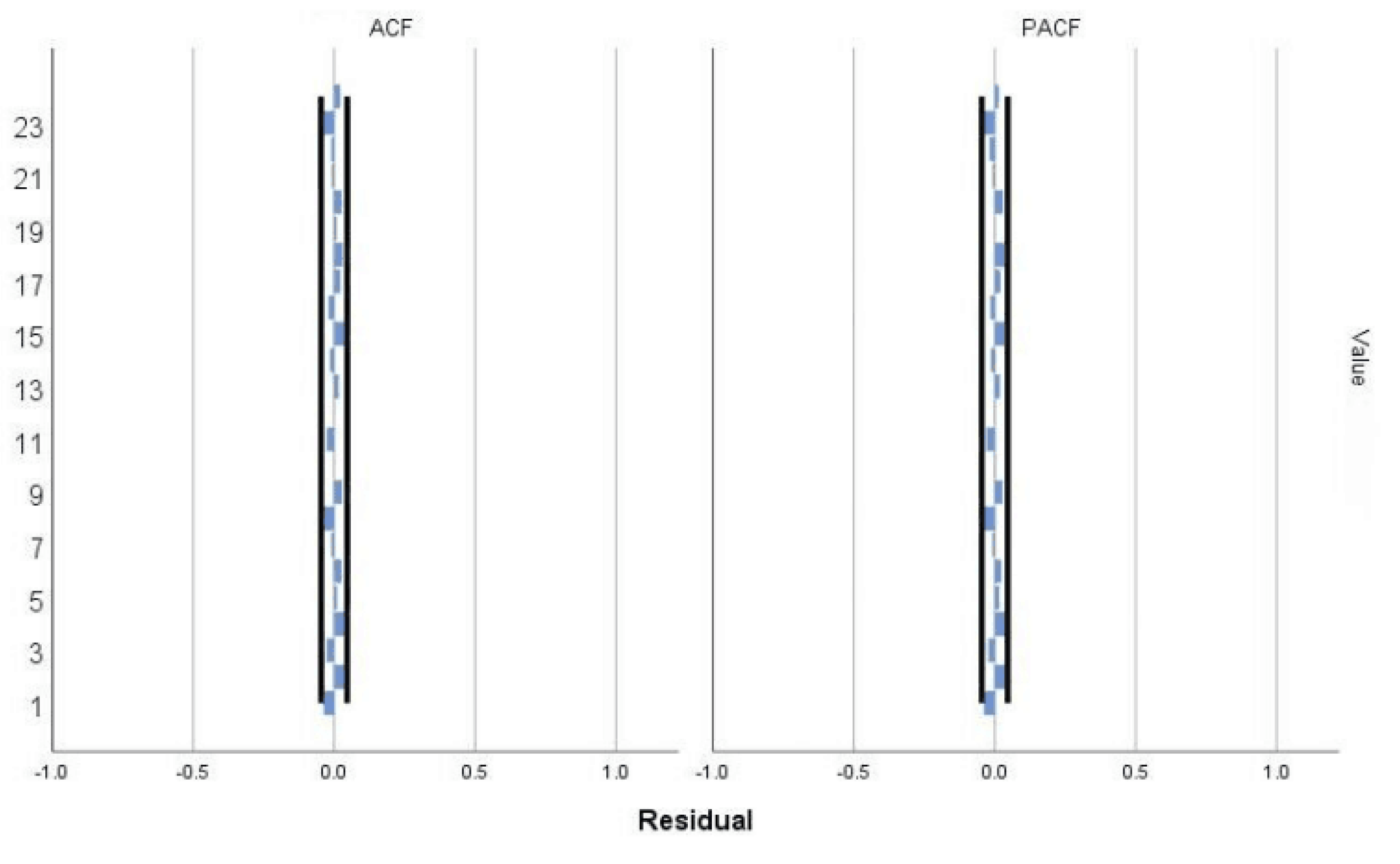

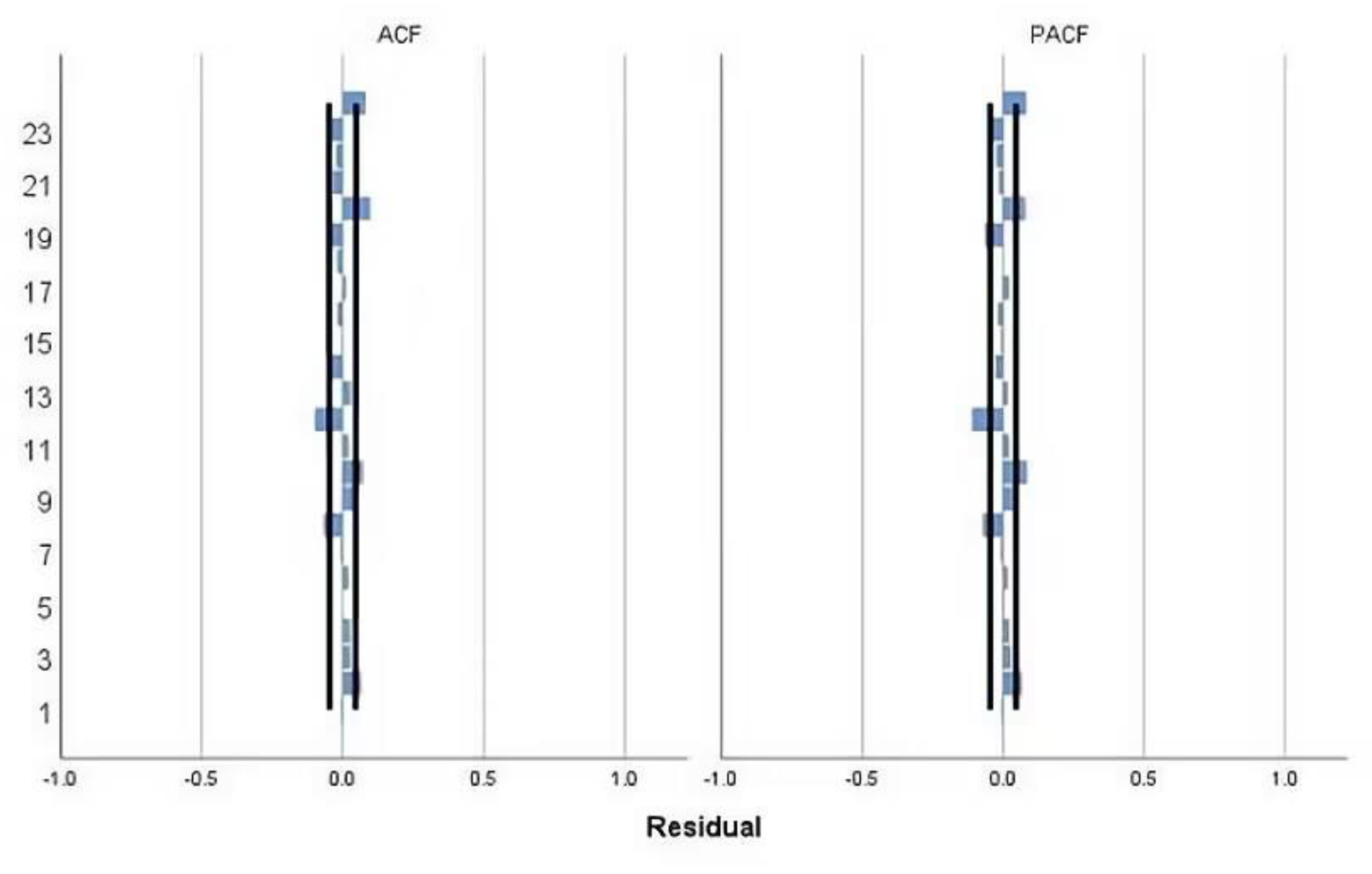

2.1.2. ARIMA (Autoregressive Integrated Moving Average Model)

2.1.3. SESM (Second Exponential Smoothing Method)

2.1.4. Comparison of the Accuracy of Prediction Models

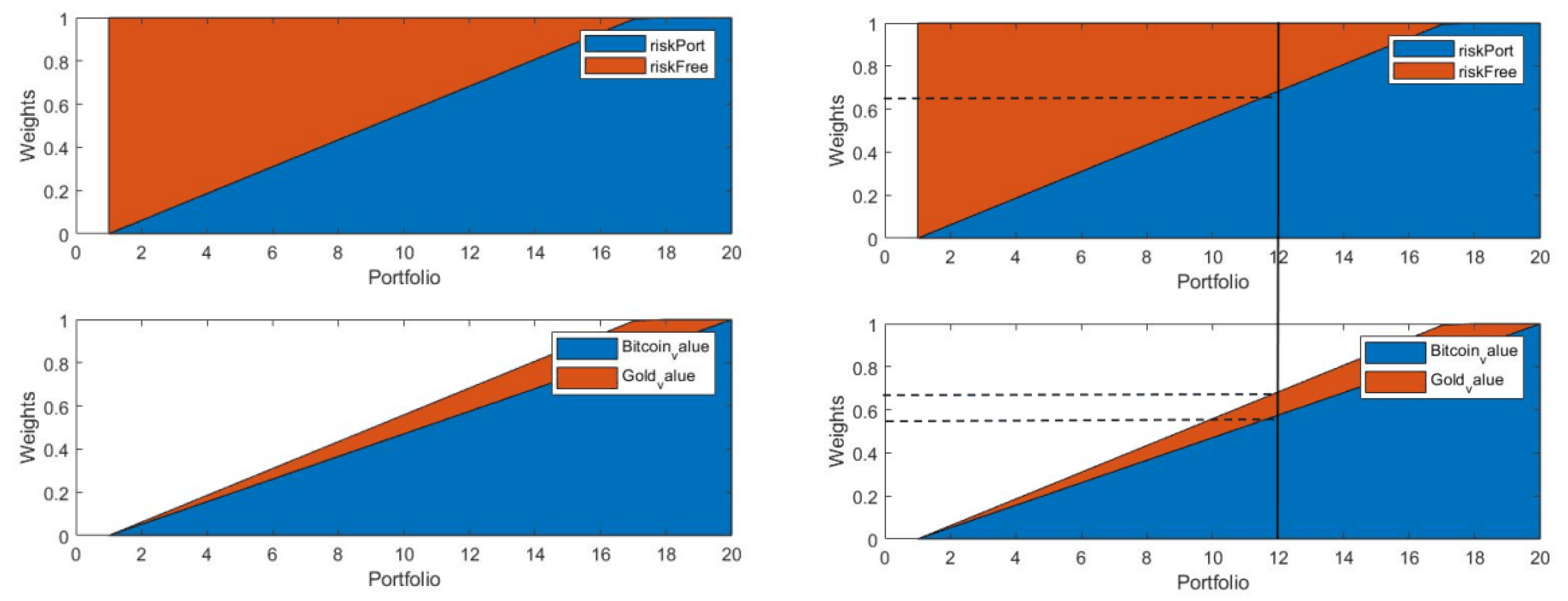

2.2. Quantitative Trading Strategies Based on Dynamic Programming

2.2.1. Dynamic Planning Problem Analysis

| Algorithm 1 Simulation of asset investment |

| Input: original assets C, G, B, risk factor risk, data predicted from the original data, days to be invested, working days flag, growth rate of assets R. Output: the final distribution of the total value of assets V. 1: for t=1 to # of day do 2: if then 3: allocate (data, asset table, risk) 4: Calculate the optimal solution for asset allocation under risk for the three assets according to Date using the portfolio toolbox function to divide the funds Q 5: G, B change amount for commission payment 6: Evaluate the total value of C, G, B according to R 7: else 8: Calculate the optimal solution for only two assets under risk according to Date, as above 9: end if 10: end for return V |

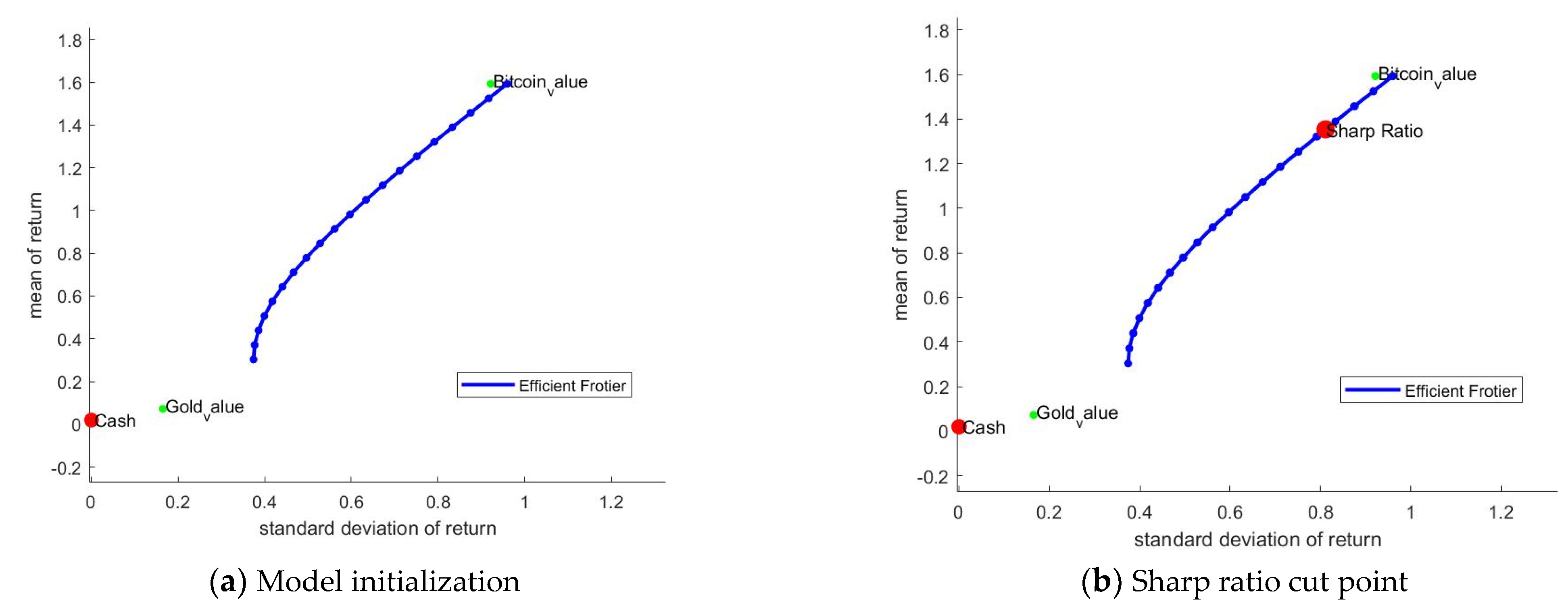

2.2.2. Mean-Variance Mode

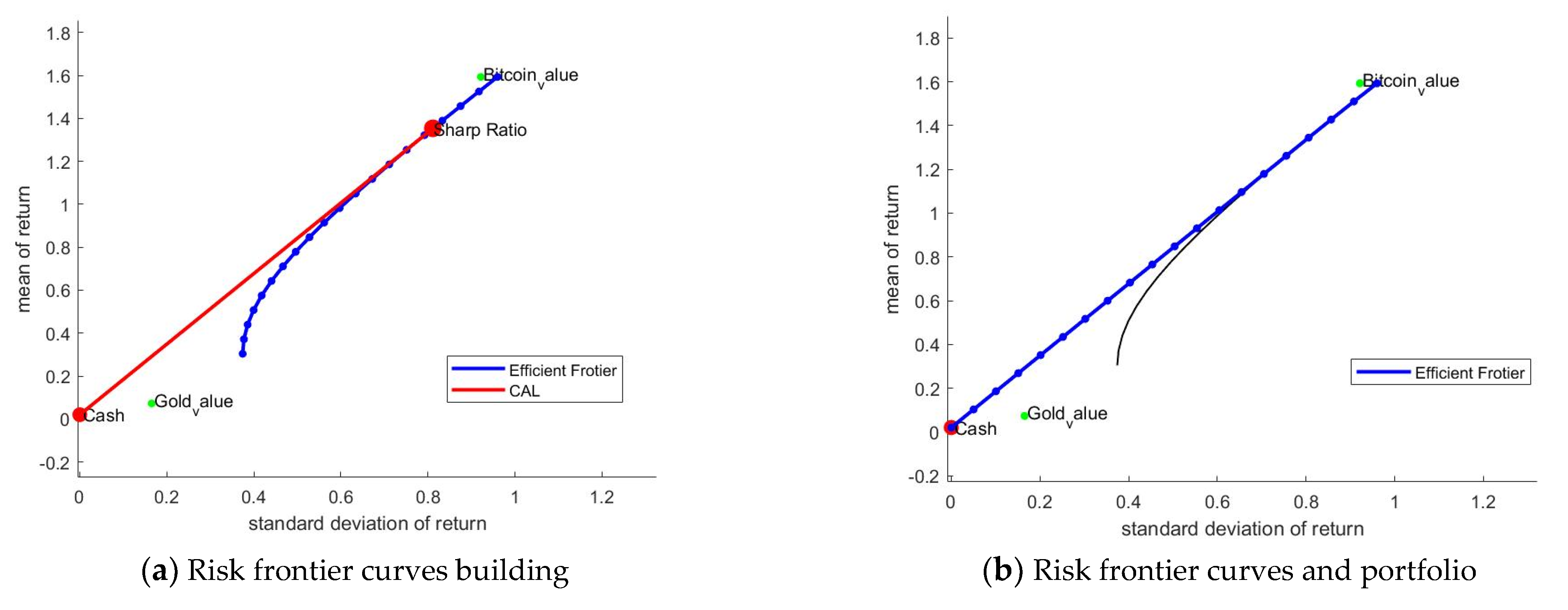

2.2.3. Combination of Effective Frontier and Sharpe Ratio

- The point on the efficient frontier curve that maximizes the expected return for a given expected risk

- The point on the efficient frontier curve that minimizes risk given the expected return

2.3. Analysis of the Advantages and Disadvantages of Prediction Models

3. Improvement of the Optimization of the Model

3.1. Planning Strategy Model Improvement

3.1.1. Optimization of Sharpe Ratio

3.1.2. Particle Swarm Optimization Algorithm

3.1.3. Model Stability Testing

4. Stability Analysis of the Model

5. Model Evaluation

5.1. Strength

- Comprehensive consideration:

- Making the best use of information:

- Excellent robustness of the model:

- Low time complexity:

- Improvements in data processing:

5.2. Weakness

- Insufficient data:

- Subjective assumptions about personality:

6. Conclusions

7. Future Research Direction

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Kannan, K.S.; Sekar, P.S.; Sathik, M.; Arumugam, P. Financial stock market forecast using data mining techniques. Proc. Int. Multiconference Eng. Comput. Sci. 2010, 1, 4. [Google Scholar]

- Tyson, E. Investing for Dummies, 6th ed.; John Wiley & Sons: Hoboken, NJ, USA, 2011. [Google Scholar]

- Mulyadi, M.S.; Anwar, Y.; Khalid, K.; Shawa, K.C.; Singh, G.; Ashraf, S.W.A. Gold versus stock investment: An econometric analysis. Int. J. Dev. Sustain. 2012, 1, 1–7. [Google Scholar]

- Ibrahim, M.H. Financial market risk and gold investment in an emerging market: The case of Malaysia. Int. J. Islam. Middle East. Financ. Manag. 2012, 4, 79–89. [Google Scholar]

- Selgin, G. Synthetic commodity money. J. Financ. Stab. 2015, 17, 92–99. [Google Scholar]

- Popper, N. Digital gold: Bitcoin and the inside story of the misfits and millionaires trying to reinvent money. HarperCollins 2016. [Google Scholar]

- Yenidoğan, I.; Çayir, A.; Kozan, O.; Dağ, T.; Arslan, Ç. Bitcoin forecasting using ARIMA and PROPHET. In Proceedings of the 3rd international conference on computer science and engineering (UBMK), Sarajevo, Bosnia and Herzegovina, 20–23 September 2018; pp. 621–624. [Google Scholar]

- Brusov, P.; Filatova, T.; Chang, S.I.; Lin, G. Innovative investment models with frequent payments of tax on income and of interest on debt. Mathematics 2021, 9.13, 1491. [Google Scholar]

- Romigh, G.D.; Brungart, D.S.; Simpson, B.D. Free-field localization performance with a head-tracked virtual auditory display. IEEE J. Sel. Top. Signal Process. 2015, 9.5, 943–954. [Google Scholar]

- Zhang, L.; Aggarwal, C.; Qi, G.-J. Stock price prediction via discovering multi-frequency trading patterns. In Proceedings of the 23rd ACM SIGKDD International Conference on Knowledge Discovery and Data Mining, Halifax, NS, Canada, 13–17 August 2017. [Google Scholar]

- Brown, K.; Harlow, W.; Zhang, H. Investment Style Volatility and Mutual Fund Performance. J. Investig. Manag. 2021, 19, 78. [Google Scholar]

- Cakici, N.; Zaremba, A. Size, Value, Profitability, and Investment Effects in International Stock Returns: Are They Really There? J. Investig. 2021, 30, 65–86. [Google Scholar]

- Brusov, P.; Filatova, T. The Modigliani–Miller theory with arbitrary frequency of payment of tax on profit. Mathematics 2021, 9, 1198. [Google Scholar]

- Modigliani, F.; Miller, M. The cost of capital, corporate finance, and the theory of investment. Am. Econ. Rev. 1958, 48, 261–297. [Google Scholar]

- Modigliani, F.; Miller, M. Corporate income taxes and the cost of capital: A correction. Am. Econ. Rev. 1963, 53, 147–175. [Google Scholar]

- Modigliani, F.; Miller, M. Some estimates of the cost of capital to the electric utility industry 1954–1957. Am. Econ. Rev. 1966, 56, 333–391. [Google Scholar]

- Black, F.; Litterman, R. Global Portfolio Optimization.Financ. Anal. J. 1992, 48, 28–43. [Google Scholar]

- Filatova, T.; Brusov, P.; Orekhova, N. Impact of advance payments of tax on profit on effectiveness of investments. Mathematics 2022, 10.4, 666. [Google Scholar]

- Zolfaghari, M.; Gholami, S. A hybrid approach of adaptive wavelet transform, long short-term memory and ARIMA-GARCH family models for the stock index prediction. Expert Syst. Appl. 2021, 182, 115149. [Google Scholar]

- Voulodimos, A.; Nikolaos, D.; Anastasios, D.; Eftychios, P. Deep learning for computer vision: A brief review. Comput. Intell. Neurosci. 2018, 2018, 7068349. [Google Scholar]

- Rubesam, A. Machine learning portfolios with equal risk contributions: Evidence from the Brazilian market. Emerg. Mark. Rev. 2022, 51, 100891. [Google Scholar]

- Wickham, H. ggplot2: Elegant Graphics for Data Analysis, 2nd ed.; Springer: Berlin/Heidelberg, Germany, 2016. [Google Scholar]

- Dospinescu, O.; Dospinescu, N. A profitability regression model of Romanian stock exchange’s energy companies. In Proceedings of the 17th International Conference on Informatics in Economy Education, Research & Business Technologies, Iasi, Romania, 17–20 May 2018. [Google Scholar]

- Brusov, P.; Filatova, T.; Orekhova, N.; Eskindarov, M. Modern Corporate Finance, Investments, Taxation and Ratings; Springer International Publishing: Berlin/Heidelberg, Germany, 2018. [Google Scholar]

- Du, Y. Application and analysis of forecasting stock price index based on combination of ARIMA model and BP neural network. In Proceedings of the 2018 Chinese Control and Decision Conference (CCDC), Shenyang, China, 9–11 June 2018. [Google Scholar]

- Garlapati, A.; Krishna, D.R.; Garlapati, K.; Yaswanth, N.m.S.; Rahul, U.; Narayanan, G. Stock Price Prediction Using Facebook Prophet and Arima Models. In Proceedings of the 2021 6th International Conference for Convergence in Technology (I2CT), Maharashtra, India, 2–4 April 2021. [Google Scholar]

- Huang, K.Y.; Jane, C.J. A hybrid model for stock market forecasting and portfolio selection based on ARX, grey system and RS theories. Expert Syst. Appl. 2009, 36.3, 5387–5392. [Google Scholar]

- Sadorsky, P. Forecasting solar stock prices using tree-based machine learning classification: How important are silver prices? N. Am. J. Econ. Financ. 2022, 61, 101705. [Google Scholar]

- Stosic, D.; Stosic, D.; Ludermir, T.B.; Stosic, T. Collective behavior of cryptocurrency price changes. Phys. A: Stat. Mech. Appl. 2018, 507, 499–509. [Google Scholar]

- Jain, P.; Jain, S. Can machine learning-based portfolios outperform traditional risk-based portfolios? The need to account for covariance misspecification. Risks 2019, 7, 74. [Google Scholar]

- Wang, G.; Wang, X.; Wang, Z.; Ma, C.; Song, Z. A VMD–CISSA–LSSVM Based Electricity Load Forecasting Model. Mathematics 2022, 10, 28. [Google Scholar]

- Munim, Z.H.; Shakil, M.H.; Alon, I. Next-day bitcoin price forecast. J. Risk Financ. Manag. 2019, 12, 103. [Google Scholar]

- Maller, R.A.; Durand, R.B.; Jafarpour, H. Optimal portfolio choice using the maximum Sharpe ratio. J. Risk 2010, 12, 49. [Google Scholar]

- Bodnar, T.; Schmid, W. Econometrical analysis of the sample efficient frontier. Eur. J. Financ. 2009, 15, 317–335. [Google Scholar]

- Wang, Y.; Yuankai, G. Forecasting method of stock market volatility in time series data based on mixed model of ARIMA and XGBoost. China Commun. 2020, 17, 205–221. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Aggressive | Intermediate | Conservative | |

|---|---|---|---|

| Return | 15,581.85 | 9869.34 | 3676.75 |

| MAPE | RMSE | |

|---|---|---|

| ARIMA | 0.026754 | 651,580.6 |

| SEME | 0.034827 | 742,891.6 |

| Aggressive | 1 | 2 | 3 | 4 | 5 | 6 | 7 |

|---|---|---|---|---|---|---|---|

| ratio_gold | 1% | 1.50% | 0.50% | 1% | 1% | 0.50% | 2% |

| ratio_bitcoin | 2% | 2% | 2% | 1.50% | 2.50% | 1% | 4% |

| return | 15,581 | 15,181 | 15,992 | 19,051 | 12,740 | 23,901 | 6599 |

| g_times | 1189 | 1176 | 1297 | 1218 | 1214 | 1362 | 1183 |

| b_times | 1372 | 1302 | 1452 | 1414 | 1289 | 1501 | 1275 |

| Intermediate | |||||||

| return | 8869 | 8636 | 9108 | 10,427 | 7542 | 12,589 | 4395 |

| g_times | 378 | 314 | 498 | 354 | 318 | 458 | 245 |

| b_times | 923 | 892 | 956 | 1136 | 893 | 1013 | 769 |

| Conservative | |||||||

| return | 3676 | 3632 | 3721 | 3939 | 3431 | 4272 | 2722 |

| g_times | 112 | 59 | 248 | 126 | 102 | 272 | 53 |

| b_times | 654 | 631 | 642 | 712 | 521 | 852 | 383 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Tang, X.; Xu, S.; Ye, H. The Way to Invest: Trading Strategies Based on ARIMA and Investor Personality. Symmetry 2022, 14, 2292. https://doi.org/10.3390/sym14112292

Tang X, Xu S, Ye H. The Way to Invest: Trading Strategies Based on ARIMA and Investor Personality. Symmetry. 2022; 14(11):2292. https://doi.org/10.3390/sym14112292

Chicago/Turabian StyleTang, Xiaoyu, Sijia Xu, and Hui Ye. 2022. "The Way to Invest: Trading Strategies Based on ARIMA and Investor Personality" Symmetry 14, no. 11: 2292. https://doi.org/10.3390/sym14112292