Land Financialization, Uncoordinated Development of Population Urbanization and Land Urbanization, and Economic Growth: Evidence from China

Abstract

:1. Introduction

2. Institutional Background and Hypotheses

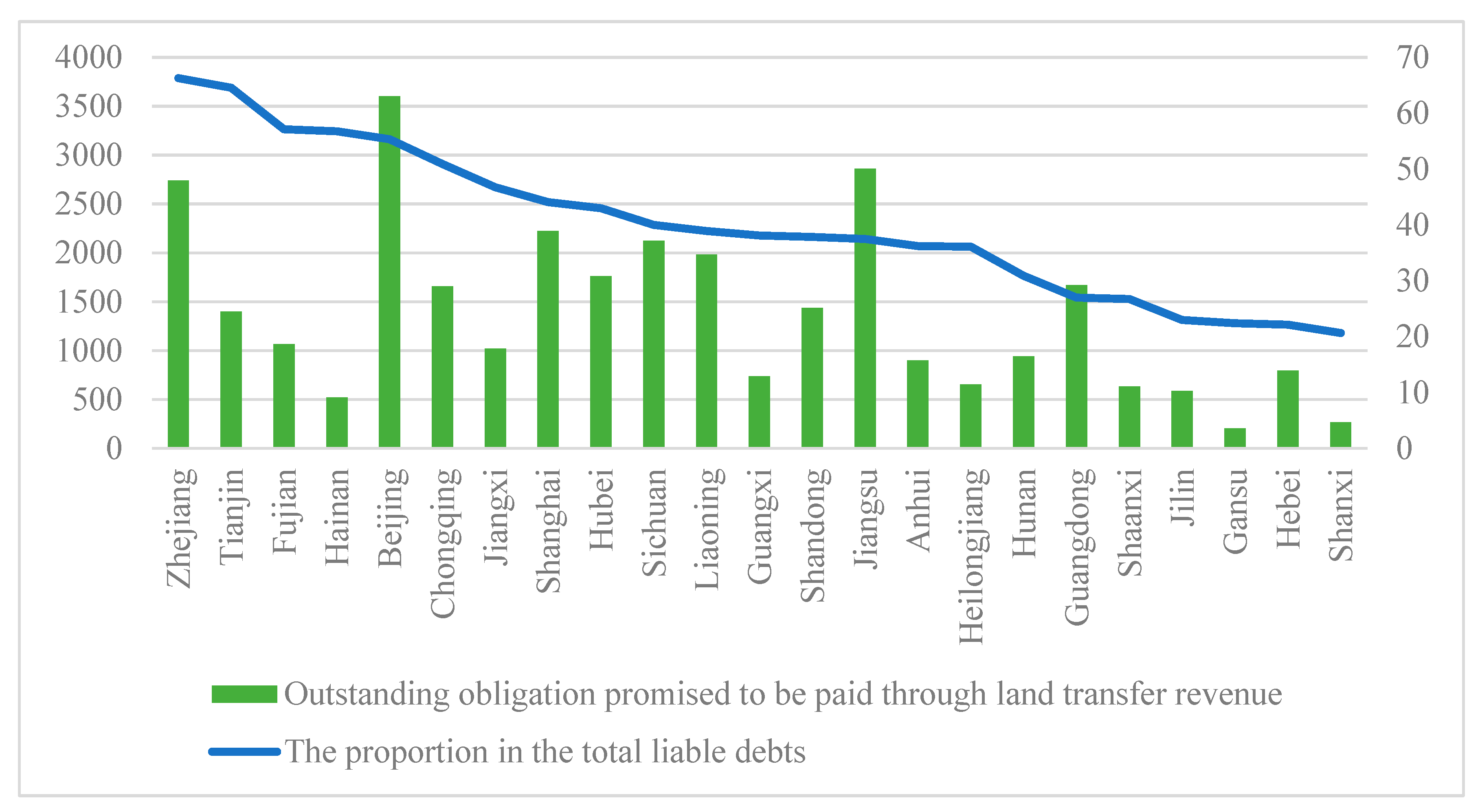

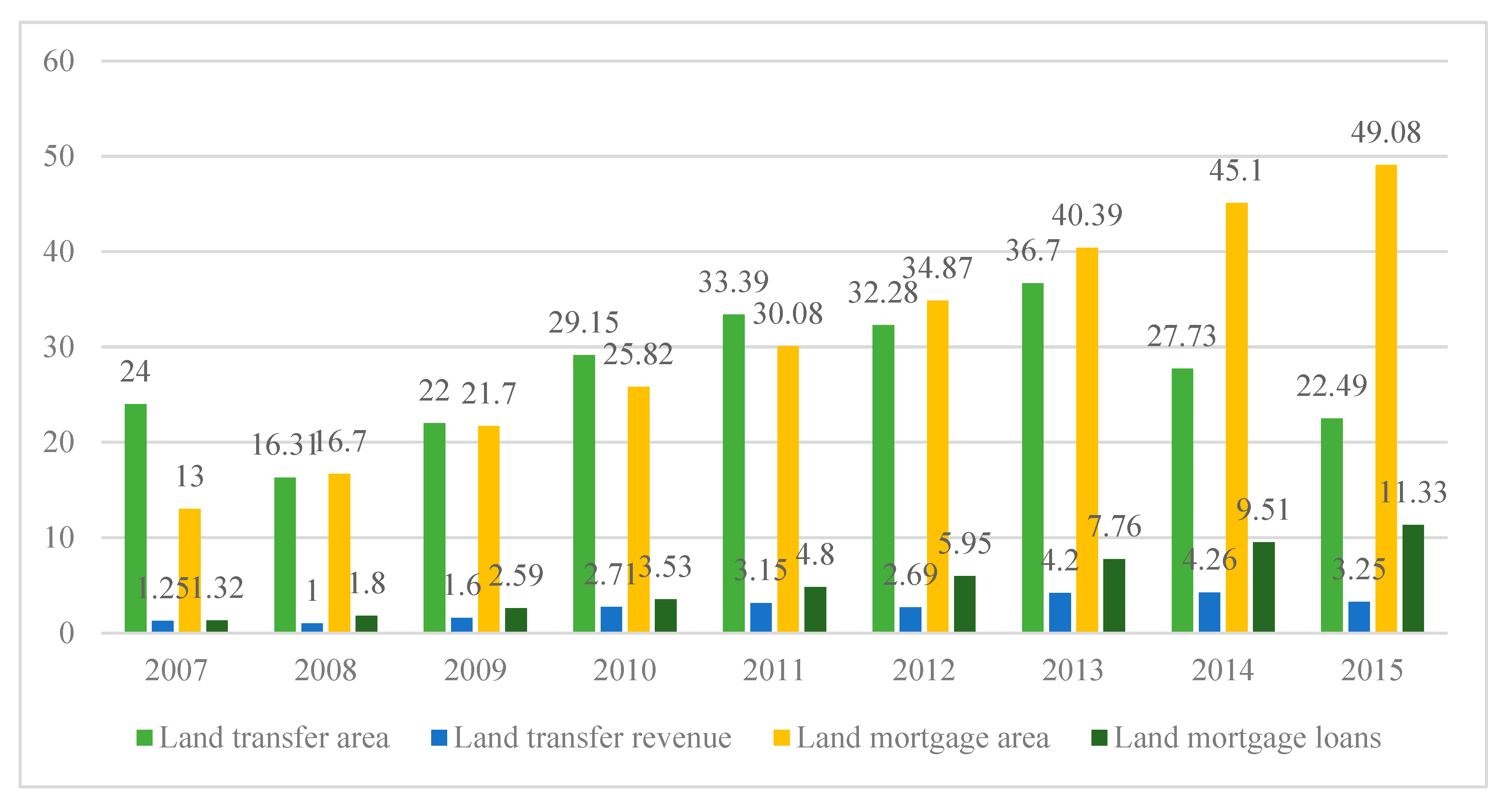

2.1. The Formation and Evolution of the Financing of Urban Development in China

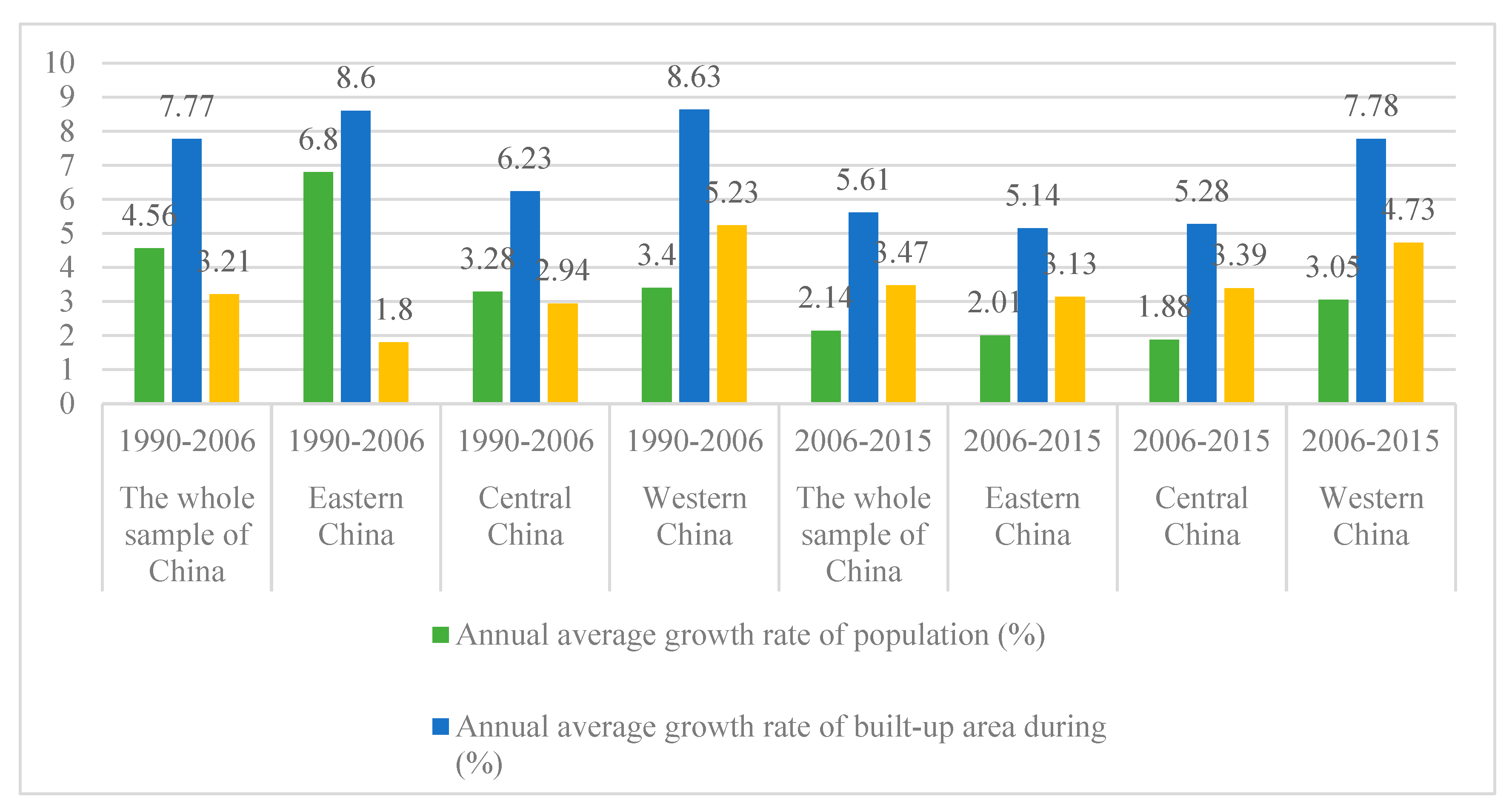

2.2. Land Financialization, the Uncoordinated Development of Population Urbanization and Land Urbanization, and Economic Growth

3. Model, Data and Variable

3.1. Econometric Model

3.2. Data Source and Variable Selection

3.2.1. Dependent Variables

3.2.2. Independent Variable

3.2.3. Moderating Variable

3.2.4. Control Variables

4. Measuring the Impact of Land Financialization on the Uncoordinated Development of Population Urbanization and Land Urbanization

4.1. Benchmark Results

4.2. Robustness Checks

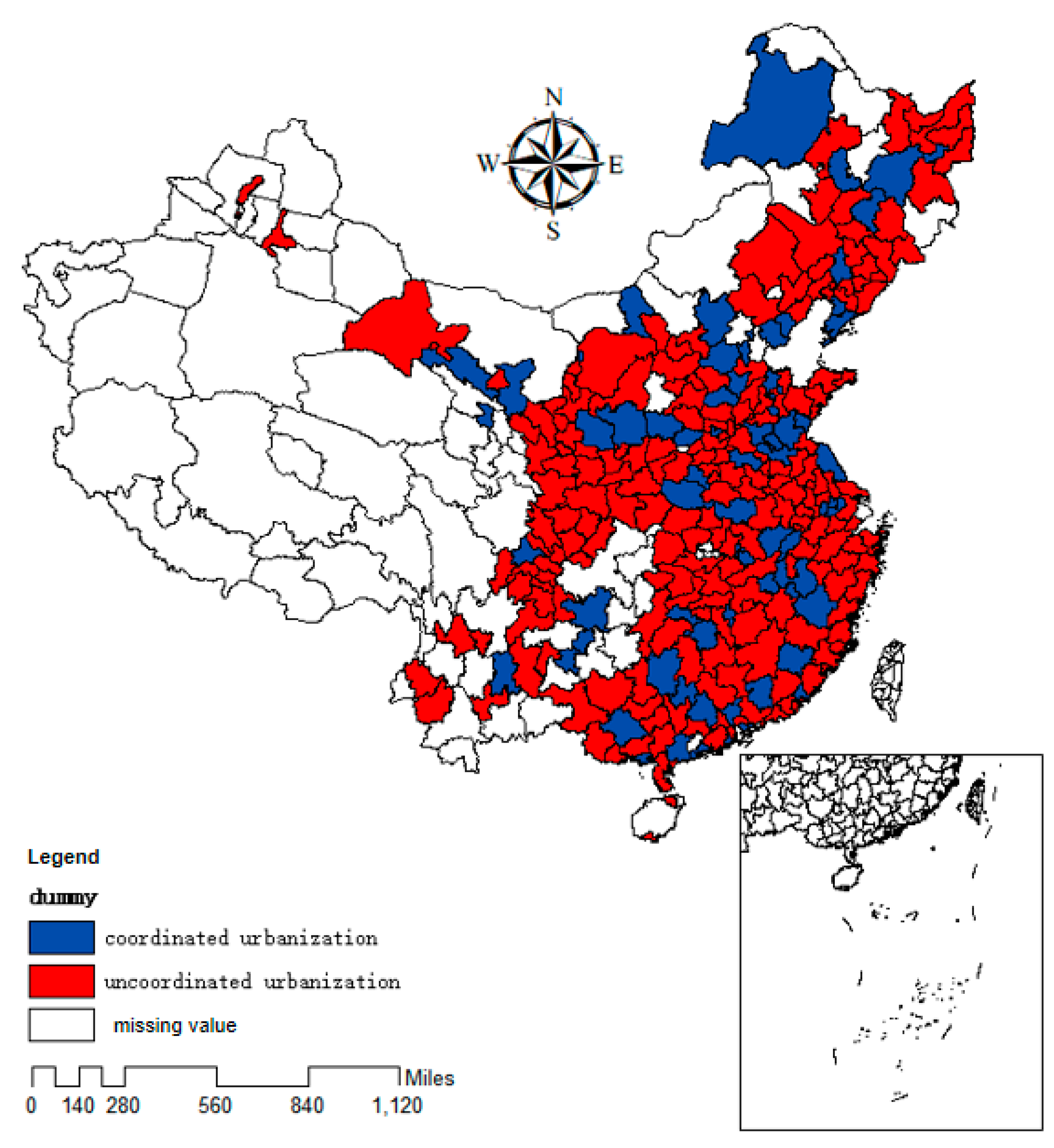

4.3. Moderating Effect of Urban Development Pressure on the Uncoordinated Development of Population Urbanization and Land Urbanization Caused by Land Financialization

5. Land Financialization, the Uncoordinated Development of Population Urbanization and Land Urbanization, and Economic Growth

6. Conclusions and Discussion

Author Contributions

Funding

Conflicts of Interest

Appendix A

References

- Duranton, G.; Puga, D. Micro-foundations of urban agglomeration economies. In Handbook of Regional and Urban Economics; Elsevier: Amsterdam, The Netherlands, 2004; Volume 4, pp. 2063–2117. [Google Scholar]

- Bertinelli, L.; Black, D. Urbanization and growth. J. Urban Econ. 2004, 56, 80–96. [Google Scholar] [CrossRef]

- Fujita, M.; Mori, T. The role of ports in the making of major cities: Self-agglomeration and hub-effect. J. Dev. Econ. 1996, 49, 93–120. [Google Scholar] [CrossRef]

- Ding, C.; Lichtenberg, E. Land and urban economic growth in China. J. Reg. Sci. 2011, 51, 299–317. [Google Scholar] [CrossRef]

- Du, D. The causal relationship between land urbanization quality and economic growth: Evidence from capital cities in China. Qual. Quant. 2017, 51, 2707–2723. [Google Scholar] [CrossRef]

- Zhu, F.K.; Zhang, F.R.; Li, C.; Jiao, P.F.; Wang, J.X. Coordination and regional difference of urban land expansion and demographic urbanization in china during 1993–2008. Prog. Geogr. 2014, 33, 647–656. [Google Scholar]

- Wang, Z.K. The Imbalance in Regional Economic Development in China and Its Reasons; Palgrave Macmillan: London, UK, 2015. [Google Scholar]

- Gail, J. Communication and Space; China Building Industry Press: Beijing, China, 2003. [Google Scholar]

- Liu, S. Risks and reform of Land-Based development model. Int. Econ. Rev. 2012, 2, 92–109. [Google Scholar]

- Guan, X.; Wei, H.; Lu, S.; Dai, Q.; Su, H. Assessment on the urbanization strategy in China: Achievements, challenges and reflections. Habitat Int. 2018, 71, 97–109. [Google Scholar] [CrossRef]

- Tan, M.; Li, X.; Xie, H.; Lu, C. Urban land expansion and arable land loss in China—A case study of Beijing–Tianjin–Hebei region. Land Use Policy 2005, 22, 187–196. [Google Scholar] [CrossRef]

- Ye, L.; Wu, A.M. Urbanization, Land Development, and Land Financing: Evidence from Chinese Cities. J. Urban Aff. 2014, 36, 354–368. [Google Scholar] [CrossRef]

- Jin, X.; Long, Y.; Sun, W.; Lu, Y.; Yang, X.; Tang, J. Evaluating cities’ vitality and identifying ghost cities in China with emerging geographical data. Cities 2017, 63, 98–109. [Google Scholar] [CrossRef]

- Au, C.-C.; Henderson, J.V. How migration restrictions limit agglomeration and productivity in China. J. Dev. Econ. 2006, 80, 350–388. [Google Scholar] [CrossRef] [Green Version]

- Hertel, T.; Zhai, F. Labor market distortions, rural–urban inequality and the opening of China’s economy. Econ. Model. 2006, 23, 76–109. [Google Scholar] [CrossRef] [Green Version]

- Shu, C.; Xie, H.; Jiang, J.; Chen, Q. Is Urban Land Development Driven by Economic Development or Fiscal Revenue Stimuli in China? Land Use Policy 2018, 77, 107–115. [Google Scholar] [CrossRef]

- Jin, H.; Qian, Y.; Weingast, B.R. Regional decentralization and fiscal incentives: Federalism, Chinese style. J. Public Econ. 2005, 89, 1719–1742. [Google Scholar] [CrossRef]

- Pan, F.; Zhang, F.; Zhu, S.; Wójcik, D. Developing by borrowing? Inter-jurisdictional competition, land finance and local debt accumulation in China. Urban Stud. 2017, 54, 897–916. [Google Scholar] [CrossRef]

- Tan, R.; Beckmann, V.; Berg, L.V.D.; Qu, F. Governing farmland conversion: Comparing China with the Netherlands and Germany. Land Use Policy 2009, 26, 961–974. [Google Scholar] [CrossRef]

- Hamnett, C. Is Chinese urbanisation unique? Urban Stud. 2020, 57, 690–700. [Google Scholar] [CrossRef]

- He, C.; Zhou, Y.; Huang, Z. Fiscal decentralization, political centralization, and land urbanization in China. Urban Geogr. 2016, 37, 436–457. [Google Scholar] [CrossRef]

- Sun, J.; Chen, T.; Cheng, Z.; Wang, C.C.; Ning, X. A financing mode of Urban Rail transit based on land value capture: A case study in Wuhan City. Transp. Policy 2017, 57, 59–67. [Google Scholar] [CrossRef]

- Zhang, L.; Nian, Y.; Liu, J. Land market fluctuations and local government debts: Evidence from the municipal investment bonds in China. China Econ. Q. 2018, 17, 1103–1126. [Google Scholar]

- Zheng, S.; Sun, W.; Wu, J.; Wu, Y. Infrastructure investment, land leasing and real estate price: A unique financing and investment channel feo urban development in Chinese cities. Econ. Res. J. 2014, 49, 14–27. [Google Scholar]

- Chen, J.; Wu, F. Housing and land financialization under the state ownership of land in China. Land Use Policy 2020, 104844. [Google Scholar] [CrossRef]

- Yuan, F.C.; Kang, H.J. The Imbalance Between Human and Land in the Process of New Urbanization and Its Breakthrough. J. Chin. Acad. Goverance 2016, 4, 47–52. (In Chinese) [Google Scholar]

- Wu, Y.; Pagano, M.A. Municipal Communications Tax Revenue Reliance and Fiscal Impact of Possible Federal Preemption. Public Budg. Finance 2008, 28, 82–100. [Google Scholar] [CrossRef]

- Brehm, S. Fiscal Incentives, Public Spending, and Productivity—County-Level Evidence from a Chinese Province. World Dev. 2013, 46, 92–103. [Google Scholar] [CrossRef]

- Bo, L.; Mear, F.C.J.; Huang, J. New development: China’s debt transparency and the case of urban construction investment bonds. Public Money Manag. 2017, 37, 225–230. [Google Scholar] [CrossRef]

- Wu, F. Planning centrality, market instruments: Governing Chinese urban transformation under state entrepreneurialism. Urban Stud. 2018, 55, 1383–1399. [Google Scholar] [CrossRef] [Green Version]

- Lin, G.C.; Li, X.; Yang, F.F.; Hu, F.Z.Y. Strategizing urbanism in the era of neoliberalization: State power reshuffling, land development and municipal finance in urbanizing China. Urban Stud. 2015, 52, 1962–1982. [Google Scholar] [CrossRef]

- Cao, G.; Feng, C.; Tao, R. Local “Land Finance” in China’s Urban Expansion: Challenges and Solutions. China World Econ. 2008, 16, 19–30. [Google Scholar] [CrossRef]

- Bai, C.-E.; Hsieh, C.-T.; Song, Z. (Michael) The Long Shadow of a Fiscal Expansion. SSRN Electron. J. 2016. [CrossRef] [Green Version]

- Zhong, T.; Chen, Y.; Huang, X. Impact of land revenue on the urban land growth toward decreasing population density in Jiangsu Province, China. Habitat Int. 2016, 58, 34–41. [Google Scholar] [CrossRef]

- Weber, R. Selling City Futures: The Financialization of Urban Redevelopment Policy. Econ. Geogr. 2010, 86, 251–274. [Google Scholar] [CrossRef]

- Wu, F. Land financialisation and the financing of urban development in China. Land Use Policy 2019, 104412. [Google Scholar] [CrossRef]

- Chang, C.; Lu, M. Misery of new town—Density, Distance and Debt. China Econ. Q. 2017, 16, 1621–1642. [Google Scholar]

- Research Group on China’s Economic Growth. Urbanization, Fiscal expansion and Economic growth. Econ. Res. J. 2011, 46, 4–20. [Google Scholar]

- Qian, Y.; Roland, G. Federalism and the Soft Budget Constraint. Am. Econ. Rev. 1998, 88, 1143–1162. [Google Scholar] [CrossRef] [Green Version]

- Maskin, E.; Qian, Y.; Xu, C. Incentives, information, and organizational form. Rev. Econ. Stud. 2000, 67, 359–378. [Google Scholar] [CrossRef] [Green Version]

- Besley, T.; Case, A. Incumbent behavior: Vote-Seeking, Tax-Setting, and yardstick competition. Am. Econ. Rev. 1992, 85, 25–45. [Google Scholar]

- Tsui, K.-Y. Local tax system, intergovernmental transfers and China’s local fiscal disparities. J. Comp. Econ. 2005, 33, 173–196. [Google Scholar] [CrossRef]

- Zhou, L. Governing China’s Local Officials: An Analysis of Promotion Tournament Model. Econ. Res. J. 2007, 7, 36–50. [Google Scholar]

- Zhang, J.; Wang, J.; Yang, X.; Ren, S.; Ranab, Q.; Haocdefg, Y. Does local government competition aggravate haze pollution? A new perspective of factor market distortion. Socio Econ. Plan. Sci. 2020, 100959. [Google Scholar] [CrossRef]

- Li, H.; Zhou, L.-A. Political turnover and economic performance: The incentive role of personnel control in China. J. Public Econ. 2005, 89, 1743–1762. [Google Scholar] [CrossRef]

- Fu, Y.; Zhang, Y. Chinese Style Decentralization and Government Spending Bias: The Cost of Growth. Manag. World 2007, 3, 4–12. [Google Scholar]

- Qiao, B.Y.; Fan, J.Y.; Feng, X.Y. Fiscal Decentralization and Compulsory Primary Education in China. Soc. Sci. China 2005, 6, 37–46. [Google Scholar]

- Caldeira, E. Yardstick competition in a federation: Theory and evidence from China. China Econ. Rev. 2012, 23, 878–897. [Google Scholar] [CrossRef] [Green Version]

- Démurger, S.; Sachs, J.D.; Woo, W.T.; Bao, S.; Chang, G.; Mellinger, A. Geography, economic policy, and regional development in China. Asian Econ. Pap. 2002, 1, 146–197. [Google Scholar] [CrossRef] [Green Version]

- Lu, M. Cross-regional redistribution of the right to use Construction Land: A New Driving Force for China’s Economic growth. J. World Econ. 2011, 34, 107–125. [Google Scholar]

- Li, Y.; Jia, L.; Wu, W.; Yan, J.; Liu, Y. Urbanization for rural sustainability—Rethinking China’s urbanization strategy. J. Clean. Prod. 2018, 178, 580–586. [Google Scholar] [CrossRef]

- Halleux, J.-M.; Marcinczak, S.; Van Der Krabben, E. The adaptive efficiency of land use planning measured by the control of urban sprawl. The cases of the Netherlands, Belgium and Poland. Land Use Policy 2012, 29, 887–898. [Google Scholar] [CrossRef]

- Chen, J.; Zhou, Q. City size and urban labor productivity in China: New evidence from spatial city-level panel data analysis. Econ. Syst. 2017, 41, 165–178. [Google Scholar] [CrossRef]

- Xie, D. Local government competition, Monopolizes land supply and urbanization development imbalance. J. Financ. Econ. 2016, 42, 102–111. [Google Scholar]

- Fred, Y.Y. A quantitative relationship between per capita GDP and scientometric criteria. Scientometrics 2007, 71, 407–413. [Google Scholar]

- Duan, H.; Zhan, J.V. Fiscal transfer and local public expenditure in China: A case study of Shanxi Province. China Rev. 2011, 11, 57–88. [Google Scholar]

- Au, C.-C.; Henderson, J.V. Are Chinese Cities Too Small? Rev. Econ. Stud. 2006, 73, 549–576. [Google Scholar] [CrossRef] [Green Version]

- Qin, D.; Song, H. Sources of investment inefficiency: The case of fixed-asset investment in China. J. Dev. Econ. 2009, 90, 94–105. [Google Scholar] [CrossRef] [Green Version]

- Xiong, C.; Gao, H. The incongruity between population urbanization and spatial urbanization. Financ. Econ. 2012, 11, 102–108. [Google Scholar]

| 1 | Shanghai E-House Real Estate Research Institute, Local government’s dependence on Land Finance, 29 February 2016. https://finance.sina.com.cn/roll/2016-02-29/doc-ifxpvzah8335807.shtml. |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Variable | Definition | Obs | Mean | Standard Error | Minimum | Maximum |

|---|---|---|---|---|---|---|

| Logarithm of city-level built-up area | 2770 | 9.544 | 0.405 | 8 | 11.27 | |

| Logarithm of city-level permanent residents | 2770 | 4.549 | 0.708 | 2.703 | 6.750 | |

| Dummy variable of the uncoordinated development of population urbanization and land urbanization | 2770 | 0.668 | 0.471 | 0 | 1 | |

| Interest-bearing debt of local financing platform companies | 2770 | 6.239 | 3.815 | 0 | 12.17 | |

| Logarithm of GDP per capita | 2770 | 10.15 | 0.729 | 7.306 | 13.11 | |

| Ratio of the second and third industries’ added value in GDP | 2770 | 49.88 | 10.63 | 15.17 | 90.97 | |

| Ratio of the second and third industries’ added value in GDP | 2770 | 36.33 | 8.461 | 8.580 | 75.84 | |

| Logarithm of city-level population density | 2770 | 422.2 | 309.8 | 4.700 | 2648 | |

| Logarithm of local public expenditure per capita | 2770 | 8.310 | 0.734 | 6.305 | 11.51 | |

| Ratio of accumulated foreign direct investment (FDI) in capital stock | 2770 | 7.556 | 2.140 | 0 | 13.89 | |

| Logarithm of fixed-assets investment per capita | 2770 | 9.767 | 0.869 | 6.883 | 12.30 | |

| Logarithm of road area per capita | 2770 | 2.202 | 0.599 | 0.157 | 4.686 | |

| Amount of newly increased construction land | 2770 | 5.664 | 1.713 | 0 | 12.41 | |

| Pressure of urban economic development | 2770 | 1.159 | 0.240 | 1 | 3.397 | |

| inv_ | Pressure of urban investment | 2770 | 1.077 | 0.118 | 1 | 2.262 |

| human_rateit | Ratio of college students | 2770 | 1.584 | 2.198 | 0 | 12.936 |

| Model 1 | Model 2 | Model 3 | Model 4 | |

|---|---|---|---|---|

| FE | GMM | FE | GMM | |

| Variable | ||||

| 0.006 ** | 0.004 *** | 0.001 | −0.001 | |

| (0.003) | (0.001) | (0.003) | (0.001) | |

| 0.045 | 0.011 | −0.105 ** | 0.056 *** | |

| (0.047) | (0.022) | (0.042) | (0.015) | |

| −0.000 *** | −0.000 | 0.000 * | 0.000 | |

| (0.000) | (0.000) | (0.000) | (0.000) | |

| 0.022 | 0.111 *** | 0.055 ** | −0.091 ** | |

| (0.046) | (0.037) | (0.025) | (0.038) | |

| −0.026 | 0.005 | −0.026 | 0.050 | |

| (0.037) | (0.035) | (0.026) | (0.031) | |

| 0.007 *** | −0.009 *** | 0.002 | −0.003 | |

| (0.003) | (0.002) | (0.003) | (0.003) | |

| 0.004 | −0.009 *** | 0.002 | 0.004 | |

| (0.003) | (0.002) | (0.003) | (0.003) | |

| 0.001 | 0.000 | 0.008 ** | 0.019 *** | |

| (0.006) | (0.002) | (0.003) | (0.007) | |

| Lag | 0.894 *** | 0.914 *** | ||

| (0.018) | (0.023) | |||

| _cons | 8.681 *** | 0.668 *** | 4.892 *** | −0.072 |

| (0.406) | (0.212) | (0.433) | (0.231) | |

| Time effect | Y | Y | Y | Y |

| Regional effect | Y | Y | Y | Y |

| Hansen p | 0.907 | 0.304 | ||

| Adjusted R2 | 0.291 | 0.182 | ||

| N | 2763 | 2491 | 2765 | 2493 |

| Variable | Model 1 | Model 2 | Model 3 | Model 4 | Model 5 |

|---|---|---|---|---|---|

| LPM | PROBIT | LOGIT | IV-PROBIT | GMM | |

| 0.010 ** | 0.041 ** | 0.065 ** | 0.251 ** | 0.031 *** | |

| (0.004) | (0.017) | (0.029) | (0.113) | (0.008) | |

| 0.010 | −0.079 | −0.101 | 0.038 | 0.073 | |

| (0.048) | (0.290) | (0.498) | (0.299) | (0.239) | |

| −0.001 | −0.003 * | −0.005 * | −0.003 * | 0.000 | |

| (0.000) | (0.002) | (0.003) | (0.002) | (0.000) | |

| 0.141 ** | 0.655 ** | 1.121 ** | 0.508 * | 0.174 | |

| (0.061) | (0.285) | (0.487) | (0.306) | (0.286) | |

| 0.038 | 0.259 | 0.404 | 0.238 | −0.351 | |

| (0.042) | (0.185) | (0.309) | (0.192) | (0.236) | |

| 0.011 ** | 0.050 ** | 0.088 ** | 0.034 | 0.007 | |

| (0.004) | (0.023) | (0.038) | (0.025) | (0.014) | |

| 0.009 * | 0.041 | 0.074 | 0.024 | 0.023 | |

| (0.005) | (0.028) | (0.046) | (0.030) | (0.019) | |

| −0.030 *** | −0.135 *** | −0.222 *** | −0.119 *** | 0.010 | |

| (0.009) | (0.043) | (0.073) | (0.045) | (0.036) | |

| Lag | 0.123 *** | ||||

| (0.030) | |||||

| _cons | −1.603 ** | −17.579 | −13.567 * | −7.690 * | 0.339 |

| (0.694) | (170.690) | (7.188) | (4.316) | (1.442) | |

| Time effect | Y | Y | Y | Y | Y |

| Regional effect | Y | Y | Y | Y | Y |

| Hansen p | 0.390 | 0.380 | 0.162 | ||

| Adjusted R2 | 0.154 | ||||

| N | 2770 | 2770 | 2770 | 2770 | 2493 |

| Model 1 | Model 2 | Model 3 | Model 4 | Model 5 | |

|---|---|---|---|---|---|

| 0.046 ** | 0.041 ** | 0.038 ** | 0.046 * | 0.040 ** | |

| (0.018) | (0.020) | (0.018) | (0.025) | (0.017) | |

| −0.060 | −0.112 | 0.036 | 0.089 | −0.080 | |

| (0.271) | (0.354) | (0.364) | (0.285) | (0.290) | |

| −0.003 * | −0.001 | −0.002 | −0.002 | −0.003 * | |

| (0.002) | (0.001) | (0.002) | (0.002) | (0.002) | |

| −0.378 | −0.019 | 0.628 ** | 1.063 *** | 0.657 ** | |

| (0.248) | (0.313) | (0.290) | (0.363) | (0.285) | |

| 0.082 | 0.182 | 0.176 | 0.309 | 0.252 | |

| (0.191) | (0.204) | (0.189) | (0.233) | (0.185) | |

| 0.012 | −0.014 | 0.056 ** | 0.053 | 0.050 ** | |

| (0.022) | (0.026) | (0.023) | (0.039) | (0.023) | |

| 0.005 | −0.014 | 0.047 * | 0.068 | 0.041 | |

| (0.028) | (0.032) | (0.028) | (0.047) | (0.028) | |

| −0.073 * | −0.058 | −0.120 *** | −0.119 ** | −0.135 *** | |

| (0.041) | (0.044) | (0.044) | (0.048) | (0.043) | |

| . | 0.017 | ||||

| (0.026) | |||||

| _cons | −1.413 | −8.447 | −14.357 | −15.958 *** | −17.907 |

| (606.945) | (203.141) | (701.848) | (5.341) | (269.780) | |

| Time effect | Y | Y | Y | Y | Y |

| Regional effect | Y | Y | Y | Y | Y |

| N | 2770 | 2770 | 2712 | 1939 | 2770 |

| Model 1 | Model 2 | Model 3 | Model 4 | Model 5 | Model 6 | |

|---|---|---|---|---|---|---|

| LPM | PROBIT | LPM | PROBIT | SDM | LPM | |

| Catch-Up Pressure in GDP | Catch-Up Pressure in Fixed-Assets Investment | Yardstick Competition | ||||

| land_ financialization | 0.010 ** | 0.041 ** | 0.011 ** | 0.046 *** | ||

| (0.004) | (0.017) | (0.004) | (0.018) | |||

| 0.065 | 0.193 | |||||

| (0.151) | (0.647) | |||||

| land_ financialization * GDP_pressure | 0.069 *** | 0.363 *** | ||||

| (0.025) | (0.112) | |||||

| 0.199 ** | 1.061 ** | |||||

| (0.090) | (0.429) | |||||

| land_ financialization * inv_pressure | 0.033 * (0.018) | 0.140 * (0.081) | ||||

| W * land_ financialization | 1.617 *** | 0.251 ** | ||||

| (0.225) | (0.113) | |||||

| _cons | −1.574 ** | −17.578 | −2.007 *** | −19.402 | 10.805 ** | −9.981 ** |

| (0.709) | (169.466) | (0.708) | (169.248) | (5.353) | (4.322) | |

| Controls | Y | Y | Y | Y | Y | Y |

| Time effect | Y | Y | Y | Y | Y | Y |

| Regional effect | Y | Y | Y | Y | Y | Y |

| Adjusted R2 | 0.319 | 0.320 | 0.768 | 0.164 | ||

| N | 2770 | 2770 | 2770 | 2770 | 2770 | 2770 |

| Model 1 | Model 2 | Model 3 | Model 4 | |

|---|---|---|---|---|

| Variables | Land use efficiency | Economic growth rate | ||

| uncoordinated | coordinated | uncoordinated | coordinated | |

| −0.006 * | 0.005 | 5.612 ** | 4.285 | |

| (0.003) | (0.007) | (2.223) | (5.459) | |

| ^2 | −2.733 ** | −2.062 | ||

| 0.020 | 0.160 | (1.102) | (2.727) | |

| (0.056) | (0.175) | |||

| 0.001 * | 0.000 | |||

| (0.000) | (0.000) | |||

| 0.080 * | 0.185 ** | 0.266 | 1.421 | |

| (0.047) | (0.075) | (1.459) | (3.812) | |

| 0.129 *** | 0.101 | 4.801 *** | 2.117 | |

| (0.034) | (0.063) | (1.213) | (1.850) | |

| 0.021 *** | 0.013 | |||

| (0.004) | (0.008) | |||

| 0.019 *** | 0.019 ** | −0.079 | −0.262 | |

| (0.005) | (0.008) | (0.078) | (0.202) | |

| −0.003 | 0.010 | 0.928 *** | 0.847 * | |

| (0.007) | (0.013) | (0.268) | (0.443) | |

| 3.581 | 12.835 * | |||

| (4.519) | (6.517) | |||

| human_rateit | 1.138 *** | 3.095 *** | ||

| (0.301) | (0.919) | |||

| _cons | 6.640 *** | 4.995 *** | −51.324 | −85.826 |

| (0.661) | (1.434) | (34.066) | (62.265) | |

| Adjusted R2 | 0.383 | 0.479 | 0.551 | 0.493 |

| N | 1850 | 920 | 1850 | 920 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ji, Y.; Guo, X.; Zhong, S.; Wu, L. Land Financialization, Uncoordinated Development of Population Urbanization and Land Urbanization, and Economic Growth: Evidence from China. Land 2020, 9, 481. https://doi.org/10.3390/land9120481

Ji Y, Guo X, Zhong S, Wu L. Land Financialization, Uncoordinated Development of Population Urbanization and Land Urbanization, and Economic Growth: Evidence from China. Land. 2020; 9(12):481. https://doi.org/10.3390/land9120481

Chicago/Turabian StyleJi, Yunyang, Xiaoxin Guo, Shihu Zhong, and Lina Wu. 2020. "Land Financialization, Uncoordinated Development of Population Urbanization and Land Urbanization, and Economic Growth: Evidence from China" Land 9, no. 12: 481. https://doi.org/10.3390/land9120481