Spatial Distribution Characteristics and Influencing Factors of the Success or Failure of China’s Overseas Arable Land Investment Projects—Based on the Countries along the “Belt and Road”

Abstract

:1. Introduction

2. Literature Review

3. Research Design

3.1. Research Methods

3.1.1. Nearest Neighbor Index

3.1.2. Gini Coefficient

3.1.3. Spatial Autocorrelation

3.1.4. Logit Regression Model

3.2. Indicator Selection and Data Sources

3.2.1. Indicator Selection

- Explained variables. A dummy variable is constructed to represent the success or failure of China’s overseas arable land investment projects in the host country. The value of successful investment is 1, and the value of investment failure is 0.

- Explanatory variables. The project characteristics, host country’s economic base, resource endowment, business environment, degree of openness, institutional environment and bilateral relations between the two countries will all have an impact on the success or failure of an investment project.

- (a)

- As the core of overseas arable land investment, the contracted area and use of arable land are important factors affecting the success or failure of investment [37]. The development of overseas arable land investment can bring rental income, taxation, jobs and new technologies to the host country, and, to a certain extent, it can be supported by the local government and people. However, due to the political sensitivity of arable land investment, as the contracted area increases, the local residents may panic or even block the investment due to the influence of public opinions such as the “China threat theory” and “neocolonialism” [48], resulting in project failure. The contracted arable land is mostly used for agricultural production and non-food crop production. The more uses, the higher the requirements for the business entity and the greater the risk, which may reduce the success rate of the project. The longer the investment period, and the deeper the investor’s understanding of the local government, the public and the market of the host country, the more conducive it is to the successful operation of the project. Overseas arable land investment generally has two modes: sole proprietorship and joint venture. If the host country participates in the joint venture, it will help to reduce policy discrimination, public opinion risks, etc., and can speed up the operation of the enterprise.

- (b)

- The economic base reflects the persistence of a country’s investment environment, which is characterized by the level of development and economic growth. A better economic foundation is the fundamental guarantee for the level of return and security of China’s companies’ investment in overseas arable land [49]. The better the economic foundation of the host country, the greater the market demand and investment space, and the greater the probability of project success.

- (c)

- The resource endowment is represented by the per capita arable land area, the per capita renewable inland freshwater resources, the proportion of agricultural employment and the grain yield per unit. Resource endowment is the basis for overseas arable land investment. The higher the endowment, the more conducive to investment. However, countries with excellent resources and a good environment will also attract other competitors; there may be malicious slander and other incidents in the competition process, which will be detrimental to the image of enterprises and even China as a whole, and hinder the development of the project.

- (d)

- The business environment of the host country is characterized by the business convenience index, the degree of protection of small and medium investors, the difficulty of contract execution and the proportion of the total tax rate. The business environment is related to the capital, human resources, time and opportunity costs of an enterprise’s production and operation activities. An open, transparent, fair and good business environment can promote the marketization of investment activities [50]; by simplifying procedures, providing protection policies and reducing taxation, the company’s start-up time and operating costs are reduced, which will help China’s companies to adapt to the host country’s business environment, reduce the difficulty of survival and promote successful investment.

- (e)

- The degree of openness of the host country is represented by the number of investment protection policies towards China, the globalization index and the proportion of foreign investment. Countries with a high degree of openness are more tolerant of foreign investors and can provide preferential policies to attract investment. As a result, foreign investors have higher autonomy to operate independently [51], which can improve the success rate of investment.

- (f)

- We use public discourse power, political stability, government efficiency, supervision quality, the rule of law level and corruption control ability to characterize the host country’s institutional environment. The main function of institutions is to create an orderly market environment and reduce market uncertainty to facilitate the conductance of economic activities. An excellent institutional environment in a country means that the government is more effective, the protection of contracts and property rights is stronger, and the investment risk of enterprises is lower [52], which is conducive to the success of investment.

- (g)

- The bilateral relationship is represented by the language similarity between China and the host country, the signing length of the bilateral investment agreement, the partnership, the length of the establishment of diplomatic relations and the number of high-level mutual visits. Language similarity represents the cultural distance between China and the host country. Having a common language between the two countries means that they have similar cultural values, which can reduce information asymmetry and make it easier for both parties to communicate and reach business agreements [53]. The remaining variables all represent the political relationship between China and the host country. A friendly bilateral political relationship can provide China’s enterprises with higher property rights protection and residual claiming ability [54], which guarantees the success of project investment. The selection and description of the variables are shown in Table 1.

3.2.2. Data Sources

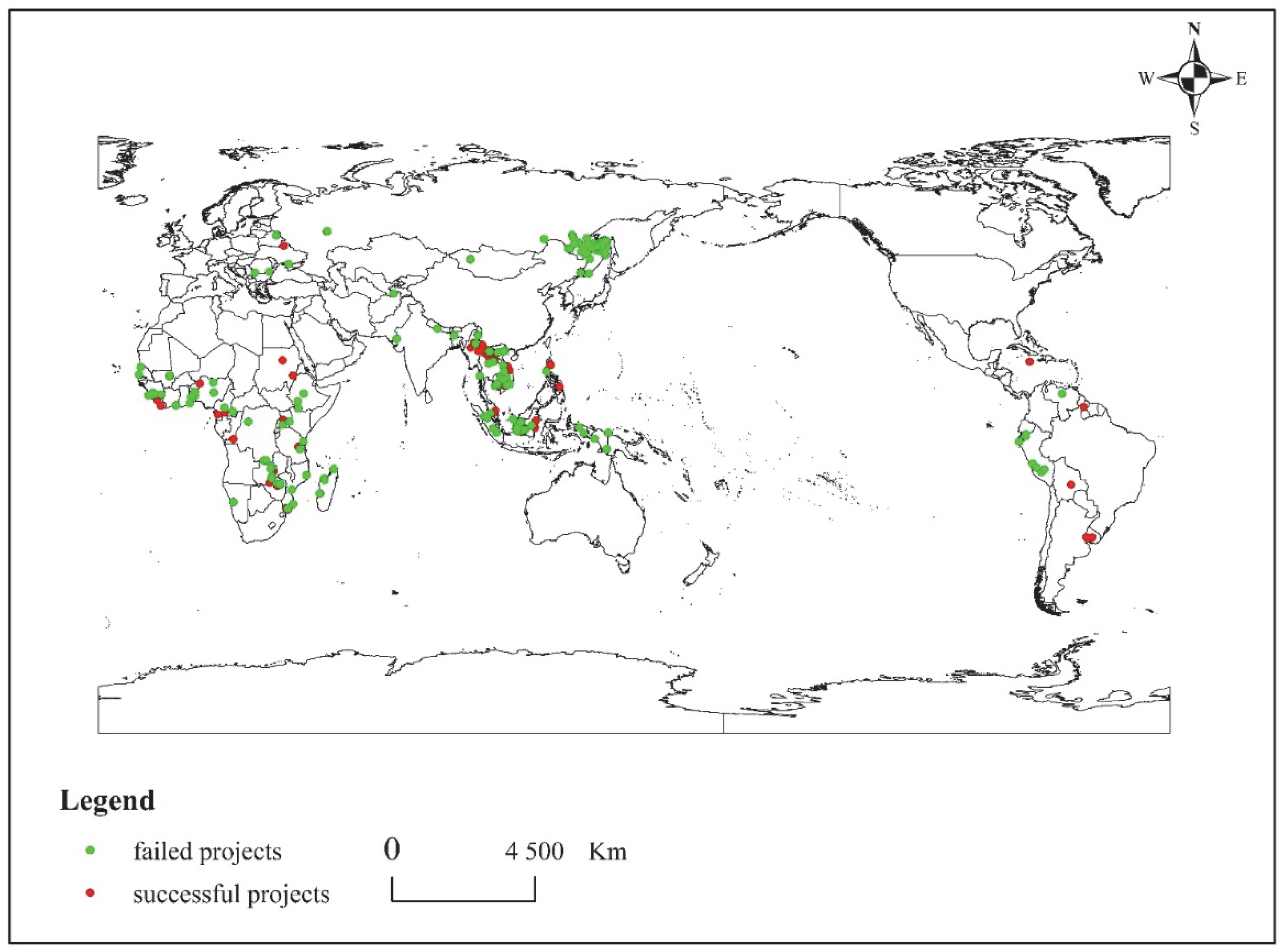

4. The Status and Spatial Distribution Characteristics of Successful and Failed Investment Projects

4.1. The Current Situation of China’s Overseas Arable Land Investment Projects

4.2. Spatial Pattern Characteristics of Success or Failure of Arable Land Investment Projects

4.2.1. Analysis of the Nearest Neighbor Index

4.2.2. Analysis of the Gini Coefficient

4.2.3. Analysis of the Spatial Autocorrelation

5. Influencing Factors of Success of Arable Land Investment Projects

5.1. Baseline Regression Results

5.2. Heterogeneity Analysis

5.3. Robustness Test

6. Discussion

7. Conclusions and Policy Suggestions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Robertson, B.; Pinstrup-Andersen, P. Global land acquisition: Neo-colonialism or development opportunity? Food Secur. 2010, 2, 271–283. [Google Scholar] [CrossRef]

- Toft, K.H. Are land deals unethical? The ethics of large-scale land acquisitions in developing countries. J. Agric. Environ. Ethics 2013, 26, 1181–1198. [Google Scholar] [CrossRef]

- Antonelli, M.; Siciliano, G.; Turvani, M.E.; Rulli, M.C. Global investments in agricultural land and the role of the EU: Drivers, scope and potential impacts. Land Use Policy 2015, 47, 98–111. [Google Scholar] [CrossRef]

- Deininger, K. Challenges posed by the new wave of farmland investment. J. Peasant Stud. 2011, 38, 217–247. [Google Scholar] [CrossRef]

- Lu, X.H.; Ke, S.G.; Cheng, T.; Chen, T. The impacts of large-scale OFI on grains import: Empirical research with double difference method. Land Use Policy 2018, 76, 352–358. [Google Scholar] [CrossRef]

- Chen, Y.F.; Li, X.D.; Wang, L.J.; Wang, S.H. Is China different from other investors in global land acquisition? Some observations from existing deals in China’s going global strategy. Land Use Policy 2017, 60, 362–372. [Google Scholar] [CrossRef]

- Grindle, A.K.; Siddiqi, A.; Anadon, L.D. Food security amidst water scarcity: Insights on sustainable food production from Saudi Arabia. Sustain. Prod. Consum. 2015, 2, 67–78. [Google Scholar] [CrossRef]

- FAO; UNCTAD; World Bank Group. Principles for responsible agricultural investment that respects rights, livelihoods, and resources. World Bank Publ. 2010, 1, 8–10. [Google Scholar]

- FAO. The Future of Food and Agriculture-Alternative Pathways to 2050s; Food and Agriculture Organization: Roma, Italy, 2018. [Google Scholar]

- Hall, R. Land grabbing in Southern Africa: The many faces of the investor rush. Rev. Afr. Political Econ. 2011, 38, 193–214. [Google Scholar] [CrossRef]

- United Nations Development Program. The Millennium Development Goals Report 2015; United Nations: New York, NY, USA, 2015. [Google Scholar]

- Fang, T.; Chimenson, D. The internationalization of Chinese firms and negative media coverage: The case of Geely’s acquisition of Volvo cars. Thunderbird Int. Bus. Rev. 2017, 59, 483–502. [Google Scholar] [CrossRef]

- Wang, Y.M.; Sarkar, A.; Ma, L.Y.; Wu, Q.; Wei, F. Measurement of Investment Potential and Spatial Distribution of Arable Land among Countries within the “Belt and Road Initiative”. Agriculture 2021, 11, 848. [Google Scholar] [CrossRef]

- Baird, I. The global land grab meta-narrative, Asian money laundering and elite capture: Reconsidering the Cambodian context. Geopolitics 2014, 19, 431–453. [Google Scholar] [CrossRef]

- Kenney-Lazar, M. Plantation rubber, land grabbing and social-property transformation in Southern Laos. J. Peasant Stud. 2012, 39, 1017–1037. [Google Scholar] [CrossRef]

- Siciliano, G.; Rulli, M.C.; Odorico, P.D. European large-scale farmland investments and the land-water-energy-food nexus. Adv. Water Resour. 2017, 110, 579–590. [Google Scholar] [CrossRef] [Green Version]

- Otsuki, K.; Schoneveld, G.; Zoomers, A. From land grabs to inclusive development? Geoforum 2017, 83, 115–118. [Google Scholar] [CrossRef]

- Pedersen, R.H.; Buur, L. Beyond land grabbing. Old morals and new perspectives on contemporary investments. Geoforum 2016, 72, 77–81. [Google Scholar] [CrossRef]

- Borras, S.M.; Hall, R.; Scoones, I.; White, B. Towards a better understanding of global land grabbing: An editorial introduction. J. Peasant Stud. 2011, 38, 209–216. [Google Scholar] [CrossRef] [Green Version]

- Mnmichael, P. The land grab and corporate food regime restructuring. J. Peasant Stud. 2012, 39, 681–701. [Google Scholar] [CrossRef]

- Seaquist, J.W.; Johansson, E.J.; Nicholas, K.A. Architecture of the global land acquisition system: Applying the tools of network science to identify key vulnerabilities. Env. Res. Lett. 2014, 9, 114006. [Google Scholar] [CrossRef]

- Daniel, S.; Mittal, A. The Great Land Grab: Rush for World’s Farm Land Threatens Food Security for the Poor; The Oak Land Institute: Berkeley, CA, USA, 2009. [Google Scholar]

- Oliveira, G.D.L.T. Chinese land grabs in Brazil? Sinophobia and foreign investments in Brazilian soybean agribusiness. Globalizations 2018, 15, 114–133. [Google Scholar] [CrossRef]

- Zoomers, A.; Noorloos, F.V.; Otsuki, K.; Steel, G.; Westen, G.V. The rush for land in an urbanizing world: From land grabbing toward devel oping safe, resilient, and sustainable cities and landscapes. World Dev. 2017, 92, 242–252. [Google Scholar] [CrossRef]

- Hak, S.; Mcandrew, J.; Neef, A. Impact of government policies and corporate land grabs on indigenous people’s access to com mon lands and livelihood resilience in Northeast Cambodia. Land 2018, 7, 122. [Google Scholar] [CrossRef] [Green Version]

- Partners, H.Q. Private financial sector investment in farmland and agricultural infrastructure. OECD Food Agric. Fish. Pap. 2010, 33, 5–27. [Google Scholar]

- Schoenberger, L.; Hall, D.; Vandergeest, P. What happened when the land grab came to Southeast Asia? J. Peasant Stud. 2017, 44, 697–725. [Google Scholar] [CrossRef]

- Constantin, C.; Luminita, C.; Vasile, A.J. Land grabbing: A review of extent and possible consequences in Romania. Land Use Policy 2017, 62, 143–150. [Google Scholar] [CrossRef]

- Mcmichael, P. Land grabbing as security mercantilism in international relations. Globalizations 2013, 10, 47–64. [Google Scholar] [CrossRef]

- Kolstad, I.; WIIG, A. What determines Chinese outward FDI? J. World Bus. 2012, 47, 26–34. [Google Scholar] [CrossRef]

- Coscieme, L.; Pulselli, F.M.; Niccolucci, V.; Patrizi, N.; Sutton, P.C. Accounting for “land-grabbing” from a biocapacity viewpoint. Sci. Total Environ. 2016, 539, 551–559. [Google Scholar] [CrossRef]

- Lu, X.H.; Ke, S.G. Research on China’s grain supply security based on overseas farmland investment. China Popul. Resour. Environ. 2017, 5, 102–110. [Google Scholar] [CrossRef]

- Aha, B.; Ayitey, J.Z. Biofuels and the hazards of land grabbing: Tenure (in) security and indigenous farmers’ investment decisions in Ghana. Land Use Policy 2017, 60, 48–59. [Google Scholar] [CrossRef]

- Bawa, R. Will the nanomedicine “patent land grab” thwart commercialization? Nanomedicine 2005, 1, 346–350. [Google Scholar] [CrossRef] [PubMed]

- Friis, C.; Nielsen, J. Small-scale land acquisitions, large-scale implications: Exploring the case of Chinese banana investments in Northern Laos. Land Use Policy 2016, 57, 117–129. [Google Scholar] [CrossRef]

- Hules, M.; Singh, S.J. India’s land grab deals in Ethiopia: Food security or global politics? Land Use Policy 2017, 60, 343–351. [Google Scholar] [CrossRef]

- Zhou, H.C. Government agreements, institutional environment and foreign land investment. Financ. Trade Econ. 2014, 8, 71–84. [Google Scholar]

- McCarthy, J.; Prudham, S. Neoliberal Nature and the Nature of Neoliberalism. Geoforum 2004, 35, 275–283. [Google Scholar] [CrossRef]

- Johanson, J.; Vahlne, J.E. The Internationalization Process of the Firm-a Model of Knowledge Development and Increasing Forei gn Market Commitments. J. Int. Bus. Stud. 1977, 8, 23–32. [Google Scholar] [CrossRef] [Green Version]

- Witt, M.A.; Lewin, A.Y. Outward Foreign Direct Investment as Escape Response to Home Country Institutional Constraints. J. Int. Bus. Stud. 2007, 38, 579–594. [Google Scholar] [CrossRef]

- Anderson, E.; Gatignon, H. Modes of Foreign Entry: A Transaction Cost Analysis and Propositions. J. Int. Bus. Stud. 1986, 17, 1–26. [Google Scholar] [CrossRef] [Green Version]

- Dunning, J.H. Location and the Multinational Enterprises: A Neglected Factor. J. Int. Bus. Stud. 1998, 29, 45–65. [Google Scholar] [CrossRef]

- Mudambi, R.; Navarra, P. Institutions and International Business: A Theoretical Overview. Int. Bus. Rev. 2002, 11, 635–646. [Google Scholar] [CrossRef]

- Tobin, J.; Rose-Ackerman, S. When BITs Have Some Bite: The Political-economic Environment for Bilateral Investment Treaties. Rev. Int. Organ. 2011, 6, 1–32. [Google Scholar] [CrossRef]

- Gao, Y.N.; Fu, J. 3D nearest neighbor index model combined with Nano-CT to analyze SiC particles in ZrB2–SiC ceramics. Ceram. Int. 2022, in press. [CrossRef]

- Lambert, P.J. Lidia Ceriani and Paolo Verme’s paper “The origins of the Gini index: Extracts from Variabilità e Mutabilità (1912) by Corrado Gini”. J. Econ. Inequal. 2012, 10, 419–420. [Google Scholar] [CrossRef]

- Zhao, L.; Wu, D.T.; Wang, Z.H.; Qu, L.P.; Yu, W. Spatio-temporal pattern and influencing factors of the allocation of rural basic education resources in China. Econ. Geogr. 2018, 38, 39–49. [Google Scholar]

- Hofman, I.; Ho, P. China’s ‘developmental outsourcing’: A critical examination of Chinese global ‘land grabs’ discourse. J. Peasant Stud. 2012, 39, 1–48. [Google Scholar] [CrossRef]

- Von, B.J.; Meinzen-Dick, R. Land grabbing’ by foreign investors in developing countries: Risks and opportunities. IFPRI Policy Brief 2009, 13, 1–4. [Google Scholar]

- Shin, Y.; Niu, Z. An analysis of host country determinants of China’s outward FDI. Asia-Pac. J. Bus. Commer. 2014, 6, 55–69. [Google Scholar]

- Holburn, G.L.F.; Zelner, B.A. Political Capabilities, Policy Risk, and International Investment Strategy: Evidence from the Global Electric Power Generation Industry. Strateg. Manag. J. 2010, 31, 1290–1315. [Google Scholar] [CrossRef]

- Cheung, Y.W.; Qian, X.W. Empirics of China’s Outward Direct Investment. Pac. Econ. Rev. 2009, 14, 312–341. [Google Scholar] [CrossRef] [Green Version]

- Rugman, A.M.; Verbeke, A. A Perspective on Regional and Global Strategies of Multinational Enterprises. J. Int. Bus. Stud. 2004, 35, 3–18. [Google Scholar] [CrossRef] [Green Version]

- Globerman, S.; Shapiro, D. Global Foreign Direct Investment Flows: The Role of Governance Infrastructure. World Dev. 2002, 30, 1899–1919. [Google Scholar] [CrossRef]

- Qi, Y.; Rao, G. Institutional risk preference and asymmetric role of institutional distance: An examination on the OFDI of China. Discret. Dyn. Nat. Soc. 2021, 6, 3506404. [Google Scholar] [CrossRef]

- Lu, X.H.; Li, Y.; Ke, S.G. Spatial distribution pattern and its optimization strategy of China’s overseas farmland investments. Land Use Policy. 2020, 91, 104355. [Google Scholar] [CrossRef]

- Mills, E.N. Framing China’s role in global land deal trends: Why Southeast Asia is key. Globalizations 2018, 15, 168–177. [Google Scholar] [CrossRef]

- Han, J.; Lu, X.H.; Kuang, B. Analysis of the spa tial distribution and geo-relationship factors influencing paths of host countries for China’s overseas farmland investment. China Land Sci. 2020, 34, 79–88. [Google Scholar]

- Han, J.; Pan, Z.C.; Lu, X.H. Spatial distribution and influencing factors analysis of China’s overseas farmland investment projects in Southeast Asia. J. Nat. Resour. 2021, 36, 1521–1534. [Google Scholar]

- Borras, S.; Franco, J.C. From Threat to Opportunity? Problems with the Idea of a “Code of Conduct” for Land- Grabbing. Yale Hum. Rights Dev. Law J. 2010, 13, 507–523. [Google Scholar]

{kind=link}

| Variable Type | Variable Name | Variable Description | Maximum | Minimum | Mean |

|---|---|---|---|---|---|

| Project characteristics | Production area | Area of cultivated land that has been placedinto production (hm2). | 274,053.00 | 0.00 | 2602.15 |

| Production | Whether it has enteredinto production (Yes = 1, No = 0) | 1.00 | 0.00 | 0.31 | |

| Duration of investment | Duration from the earliest signing time to the statistical period (years) | 51.00 | 0.00 | 12.52 | |

| Contracted area | (hm2) | 627,072.00 | 0.00 | 33,976.22 | |

| Hostcountry participation in the investment | Yes = 1, No = 0 | 1.00 | 0.00 | 0.36 | |

| Investment purposes | Types of investment purposes | 4.00 | 1.00 | 1.54 | |

| Economic basis | Level of development | GDP per capita (dollars) | 14,315.99 | 423.64 | 4938.91 |

| Economic growth | GDP growth rate (%) | 8.36 | −8.10 | 3.81 | |

| Resource endowments | Arable land per capita | (hectares/person) | 0.84 | 0.03 | 0.35 |

| Renewable inland freshwater resources per capita | (m3/person) | 310,880.29 | 93.40 | 18,821.04 | |

| The proportion of people employed in agriculture | (%) | 72.13 | 5.83 | 34.92 | |

| Cereal yield | (kg/ha) | 6005.70 | 502.50 | 3344.10 | |

| Business environment | Ease of Doing Business Index | 1 = The most business-friendly regulations. The larger the index, the lower the convenience | 188.00 | 12.00 | 100.68 |

| The degree of protection for small and medium-sized investors | The greater the value, the higher the degree of protection | 88.00 | 10.00 | 48.27 | |

| Ease of contract execution | — | 72.25 | 22.21 | 52.34 | |

| The total tax rate as a percentage of business profits | (%) | 83.70 | 15.60 | 36.37 | |

| Degree of openness | Number of investment protection policies towards China | — | 33.00 | 0.00 | 10.15 |

| Globalization Index | — | 81.55 | 43.73 | 59.31 | |

| Percentage of FDI to GDP | (%) | 32.76 | −11.62 | 3.94 | |

| Institutional quality | Public discourse power | Reflects the extent to which citizens of a country participate in the freedom of choice of government, expression, association and the media (−2.5−2.5) | 1.26 | −1.83 | −0.76 |

| Political stability | Reflects the degree of political stability of a country (−2.5−2.5) | 1.05 | −2.25 | −0.40 | |

| Government efficiency | Reflect the quality of a country’s public services, civil service, etc. (−2.5−2.5) | 1.00 | −1.66 | −0.38 | |

| Regulatory quality | Reflects the capacity of a government to formulate and implement sound policies and regulations (−2.5−2.5) | 0.67 | −2.36 | −0.49 | |

| Level of the rule of law | Reflects the agent’s perception of the degree of confidence and compliance with the rules of society (−2.5−2.5) | 0.62 | −2.32 | −0.69 | |

| Corruption control capabilities | Reflects the extent to which government control of public power is used for private gain (−2.5−2.5) | 1.25 | −1.54 | −0.76 | |

| Bilateral relations | Language similarity | — | 0.92 | 0.00 | 0.36 |

| The length of time for signing a bilateral investment treaty | (years) | 33.00 | 0.00 | 25.60 | |

| Partnerships | 0 = other relationships, 1 = comprehensive partnership, 2 = strategic partnership, 3 = comprehensive strategic partnership | 3.00 | 0.00 | 2.40 | |

| The length of time for the establishment of diplomatic relations | Length of diplomatic relations between the two countries (years) | 72.00 | 29.00 | 61.68 | |

| Number of senior leadership exchange visits | Level of political diplomacy between senior leaders (times) | 8.00 | 0.00 | 3.03 |

| Region | Country | Contracted Area (hm2) | Production Area (hm2) | Number of Contracts | Number of Productions |

|---|---|---|---|---|---|

| Africa | Ethiopia | 27,400 | 0 | 3 | 0 |

| Benin | 10,000 | 0 | 2 | 0 | |

| Togo | 1200 | 0 | 1 | 0 | |

| Democratic Republic of the Congo | 195,817 | 10 | 5 | 1 | |

| Guinea | 36,900 | 0 | 1 | 0 | |

| Ghana | 40 | 0 | 1 | 0 | |

| Zimbabwe | 16,348 | 615 | 4 | 1 | |

| Cameroon | 128,308 | 31,420 | 4 | 2 | |

| Côte d’Ivoire | 1560 | 0 | 1 | 0 | |

| Liberia | 255,200 | 20,992 | 2 | 2 | |

| Madagascar | 35,970 | 2100 | 5 | 1 | |

| Mali | 26,174 | 7994 | 4 | 2 | |

| Mauritania | 638 | 0 | 1 | 0 | |

| Mozambique | 55,068 | 11,000 | 6 | 2 | |

| Namibia | 4375 | 0 | 1 | 0 | |

| Nigeria | 14,325 | 1000 | 3 | 1 | |

| Sierra Leone | 22,269 | 1845 | 4 | 1 | |

| Senegal | 400 | 0 | 1 | 0 | |

| Sudan | 11,953 | 2013 | 2 | 2 | |

| Tanzania | 7306 | 1400 | 3 | 1 | |

| Uganda | 2211 | 751 | 4 | 2 | |

| Zambia | 13,025 | 3015 | 8 | 2 | |

| total | 866,487 | 84,155 | 66 | 20 | |

| Asia | Pakistan | 15,000 | 0 | 1 | 0 |

| Philippines | 10,385 | 14,611 | 4 | 3 | |

| Cambodia | 199,202 | 7226 | 21 | 4 | |

| Laos | 349,438 | 75,384.54 | 36 | 24 | |

| Malaysia | 6548 | 4096 | 3 | 2 | |

| Mongolia | 10,011 | 0 | 2 | 0 | |

| Bangladesh | 283 | 0 | 1 | 0 | |

| Myanmar | 79,220 | 29,968 | 11 | 8 | |

| Nepal | 76 | 0 | 1 | 0 | |

| Tajikistan | 909 | 0 | 1 | 0 | |

| Indonesia | 959,588 | 114,066 | 35 | 9 | |

| Vietnam | 71,776 | 827 | 8 | 4 | |

| total | 1,702,436 | 246,179 | 124 | 54 | |

| South America | Bolivia | 12,500 | 12,500 | 1 | 1 |

| Ecuador | 51,546 | 0 | 2 | 0 | |

| Guyana | 627,072 | 274,053 | 1 | 1 | |

| Peru | 394,308 | 0 | 5 | 0 | |

| Venezuela | 60,000 | 0 | 1 | 0 | |

| Uruguay | 3988 | 3988 | 4 | 4 | |

| total | 1,149,414 | 290,541 | 14 | 6 | |

| Europe | Belarus | 100,000 | 0 | 1 | 0 |

| Bulgaria | 20,000 | 0 | 1 | 0 | |

| Russian Federation | 5,051,496 | 77,220 | 64 | 4 | |

| Romanian | 5772 | 0 | 1 | 0 | |

| Ukraine | 3797 | 4700 | 2 | 1 | |

| total | 5,181,065 | 81,920 | 69 | 5 | |

| North America | Jamaica | 18,000 | 18,000 | 1 | 1 |

| Oceania | Papua New Guinea | 494,010 | 0 | 3 | 0 |

| Total | — | 9,411,412 | 720,795 | 277 | 86 |

| Region | Successful Projects | Failed Projects | ||||

|---|---|---|---|---|---|---|

| Nearest Neighbor Index | Z-Test Value | p Value | Nearest Neighbor Index | Z-Test Value | p Value | |

| Entire | 0.385 | −10.920 | 0.000 | 0.321 | −17.950 | 0.000 |

| Asia | 0.497 | −7.076 | 0.000 | 0.458 | −8.671 | 0.000 |

| Africa | 0.722 | −2.377 | 0.017 | 0.599 | −5.209 | 0.000 |

| Other | 0.541 | −3.044 | 0.002 | 0.190 | −13.425 | 0.000 |

| Region | Gini Coefficient | Uniformity of Distribution | ||

|---|---|---|---|---|

| Successful | Failed | Successful | Failed | |

| Entire | 0.711 | 0.717 | 0.289 | 0.283 |

| Asia | 0.65 | 0.716 | 0.350 | 0.284 |

| Africa | 0.815 | 0.919 | 0.185 | 0.081 |

| Other | 0.611 | 0.342 | 0.389 | 0.658 |

| Type | Moran’s I Value | The Z-Value | Significance |

|---|---|---|---|

| Successful project | 0.180 | 4.243 | 0.004 |

| Failed project | 0.118 | 2.913 | 0.014 |

| Variable | Model 1 | Model 2 | Model 3 | Model 4 | Model 5 | Model 6 | Model 7 |

|---|---|---|---|---|---|---|---|

| Duration of investment | 0.024 | 0.022 | 0.024 | 0.033 | 0.033 | 0.031 | 0.026 |

| (0.025) | (0.025) | (0.026) | (0.026) | (0.026) | (0.026) | (0.026) | |

| Contracted area | 1.706 *** | 1.634 *** | 1.696 *** | 1.434 ** | 1.431 ** | 1.485 ** | 1.458 ** |

| (0.587) | (0.589) | (0.588) | (0.591) | (0.590) | (0.595) | (0.592) | |

| Area square | −0.107 *** | −0.102 *** | −0.105 *** | −0.092 *** | −0.092 *** | −0.094 *** | −0.092 *** |

| (0.035) | (0.035) | (0.035) | (0.035) | (0.035) | (0.035) | (0.035) | |

| Host country participation in the investment | −1.085 *** | −0.968 *** | −1.035 *** | −0.991 *** | −0.957 ** | −0.884 ** | −0.787 ** |

| (0.347) | (0.364) | (0.370) | (0.368) | (0.381) | (0.391) | (0.398) | |

| Type of investment purpose | −0.013 | −0.039 | 0.046 | 0.013 | 0.014 | 0.022 | −0.060 |

| (0.182) | (0.183) | (0.190) | (0.192) | (0.193) | (0.193) | (0.199) | |

| Economic basis | −0.592 | −0.523 | 0.803 | 0.535 | 0.605 | 0.299 | |

| (0.594) | (0.592) | (0.828) | (1.137) | (1.145) | (1.247) | ||

| Resource endowments | 4.074 ** | 4.063 ** | 4.326 ** | 4.460 ** | 5.728 ** | ||

| (1.940) | (1.946) | (2.096) | (2.081) | (2.250) | |||

| Business environment | 2.015 ** | 1.977 ** | 2.049 ** | 2.373 ** | |||

| (0.880) | (0.887) | (0.891) | (0.942) | ||||

| Degree of openness | 0.488 | 0.549 | −0.104 | ||||

| (1.415) | (1.414) | (1.499) | |||||

| Bilateral relations | −0.580 | −0.498 | |||||

| (0.719) | (0.733) | ||||||

| Institutional quality | 0.923 * | ||||||

| (0.546) | |||||||

| Constant term | −7.094 *** | −6.707 *** | −8.410 *** | −8.524 *** | −8.695 *** | −8.690 *** | −8.206 *** |

| (2.410) | (2.436) | (2.614) | (2.584) | (2.630) | (2.640) | (2.660) | |

| Sample size | 277 | 277 | 277 | 277 | 277 | 277 | 277 |

| Log likelihood | −153.975 | −153.469 | −151.195 | −148.494 | −148.434 | −148.109 | −146.598 |

| Pseudo R2 | 0.103 | 0.106 | 0.119 | 0.135 | 0.135 | 0.137 | 0.146 |

| Prob > chi2 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

| LR chi2 | 35.24 | 36.25 | 40.80 | 46.20 | 46.32 | 46.97 | 49.99 |

| Variable | Model 8 (Africa) | Model 9 (Asia) | Model 10 (Other) | |||

|---|---|---|---|---|---|---|

| Coefficient | Standard Error | Coefficient | Standard Error | Coefficient | Standard Error | |

| Duration of investment | 0.058 | 0.046 | 0.167 ** | 0.069 | 0.091 | 0.099 |

| Contracted area | 0.612 | 1.403 | 2.472 ** | 1.26 | 3.42 | 4.703 |

| Area square | −0.001 | 0.087 | −0.176 ** | 0.079 | −0.182 | 0.238 |

| Host country participation in the investment | −1.983 ** | 0.997 | 0.315 | 0.587 | −20.873 | 5335.439 |

| Type of investment purpose | −0.316 | 0.412 | −0.577 * | 0.344 | 0.251 | 1.014 |

| Economic basis | 5.1 | 13.675 | 3.406 | 4.262 | 6.05 | 3.772 |

| Resource endowments | 12.066 | 9.471 | 2.884 | 5.589 | 10.493 | 10.509 |

| Business environment | 2.034 | 2.57 | −0.04 | 2.308 | −4.398 | 5.249 |

| Degree of openness | 6.808 | 6.204 | −2.52 | 2.513 | −6.581 | 9.263 |

| Bilateral relations | 4.501 | 3.725 | 0.31 | 2.242 | −5.686 | 2.84 |

| Institutional quality | −1.466 | 1.124 | −0.137 | 2.764 | 1.29 | 1.651 |

| A constant term | −15.467 ** | 6.967 | −10.259 * | 5.601 | −16.445 | 26.157 |

| Sample size | 66 | 124 | 87 | |||

| Log likelihood | −33.288 | −70.183 | −13.602 | |||

| Pseudo R2 | 0.178 | 0.174 | 0.358 | |||

| Prob>chi2 | 0.212 | 0.002 | 0.128 | |||

| LR chi2 | 14.39 | 29.46 | 15.14 | |||

| Variable | Model 11 | Model 12 | ||

|---|---|---|---|---|

| Coefficient | Standard Deviation | Coefficient | Standard Deviation | |

| Duration of investment | 0.016 | 0.016 | 0.086 | 0.072 |

| Contracted area | 0.864 ** | 0.342 | 3.361 ** | 1.383 |

| Area square | −0.054 *** | 0.02 | −0.197 ** | 0.081 |

| Host country participation in the investment | −0.486 ** | 0.225 | −2.124 ** | 1.013 |

| Type of investment purpose | −0.033 | 0.12 | −0.17 | 0.562 |

| Economic basis | 0.157 | 0.726 | 1.708 | 3.158 |

| Resource endowments | 3.335 ** | 1.298 | 16.243 *** | 5.905 |

| Business environment | 1.449 ** | 0.563 | 6.968 *** | 2.567 |

| Degree of openness | −0.016 | 0.883 | −0.869 | 4.161 |

| Bilateral relations | −0.323 | 0.434 | −1.963 | 1.991 |

| Institutional quality | 0.548 * | 0.315 | 3.051 ** | 1.383 |

| A constant term | −4.874 *** | 1.539 | −21.113 *** | 6.353 |

| Sample size | 277 | 277 | ||

| Log likelihood | −146.122 | - | ||

| Pseudo R2/R2 | 0.148 | 0.15 | ||

| Prob>chi2/prob>F | 0 | 0 | ||

| LR chi2 | 50.94 | - | ||

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ma, L.; Pan, Z.; Wang, Y.; Wei, F. Spatial Distribution Characteristics and Influencing Factors of the Success or Failure of China’s Overseas Arable Land Investment Projects—Based on the Countries along the “Belt and Road”. Land 2022, 11, 2090. https://doi.org/10.3390/land11112090

Ma L, Pan Z, Wang Y, Wei F. Spatial Distribution Characteristics and Influencing Factors of the Success or Failure of China’s Overseas Arable Land Investment Projects—Based on the Countries along the “Belt and Road”. Land. 2022; 11(11):2090. https://doi.org/10.3390/land11112090

Chicago/Turabian StyleMa, Linyan, Zichun Pan, Yameng Wang, and Feng Wei. 2022. "Spatial Distribution Characteristics and Influencing Factors of the Success or Failure of China’s Overseas Arable Land Investment Projects—Based on the Countries along the “Belt and Road”" Land 11, no. 11: 2090. https://doi.org/10.3390/land11112090