1. Introduction

Water, as one of the most widely distributed substances on earth, exists almost everywhere and plays a vital role for both the environment and humanity [

1]. However, rapid population growth, and increasingly rapid urbanization, continued economic development, unprecedented technological innovations, drastic land cover alterations, and climate change have led to a global water supply crisis [

2]. Presently, the sustainability of water resource utilization has become a global issue that, if not controlled, will eventually pose a serious threat to human health and survival [

3]. Therefore, the evaluation of the development and sustainability of regional water resources has become an issue that scientists worldwide have relentlessly explored [

4]. China’s water resources are currently under pressure as a water-scarce country in terms of water resources per capita [

5]. Subsequently, various Chinese regions have started to compile water resource balance sheets on a pilot program basis [

6]. This process helps to facilitate local governments in counting the changes in the quantity and stock of water resource assets while evaluating the level of regional water resource asset management [

7,

8]. However, because of the lack of a basis for identifying and accounting for the elements of the water resource balance sheet, the establishment of a systematic and standardized method for preparing the water resource balance sheet is a practical problem that needs to be solved [

9]. As a result, scholars have studied water resource balance sheets in terms of both theoretical research and practical application [

10].

In terms of theoretical research, the fuzzy comprehensive evaluation method that considers water quantity and quality has become the main method for scholars to measure the value of water resources. Jia [

11] used a fuzzy mathematical model to dynamically evaluate the value of water resources from three aspects: (1) water resources, (2) water quality, and (3) socioeconomic conditions in Nanjing from 2011 to 2015. Regarding natural, economic, and social factors as a breakthrough, Li [

12] applied the fuzzy comprehensive evaluation model to appreciate the water resource value of the Hani Terrace. Adopting water quality, water resources, population density, and national income as evaluation factors, Cai [

13] determined the value of water resources in Chengdu by using a fuzzy comprehensive evaluation method. From the perspective of natural, social, economic, and ecological environmental factors that affect the value of water resources from the perspective of high-quality development, Li [

14] determined the value of water resources in Hubei Province using fuzzy mathematics. Zhao and Chen [

15] utilized the fuzzy pricing model of urban water resources to capture the value of water resources in Jinan City, China. Since uncertainty exists in the fuzzy integrated evaluation method, and the energy analysis theory [

16] addresses this issue successfully because of its definition of uniform criteria, an increasing number of scholars are adopting the emergy analysis method to value water resources. Taking the Yellow River Basin as the research object, Wang [

17] calculated the value of water resources in the agricultural system by applying the emergy theory and method, followed by the study of spatial distribution characteristics and influencing factors of water resource value in the agricultural system, using the spatial autocorrelation analysis method and spatial regression model. Based on the water resource system, Wang and He [

18] systematically explored the quantity evaluation of groundwater resources using the emergy analysis method for ecological economics, constructing a framework for the emergy evaluation of groundwater resources. According to the principle of mutually beneficial equilibrium, Zhang [

19] estimated the value of water resources in Ordos on the south bank of the Inner Mongolia Autonomous Region based on the emergy theory, and then proposed a pricing model for transfers of water rights from agriculture to industry in water-deficient areas of China. In terms of agricultural, industrial, domestic, and recreational sectors, Guan [

20] estimated the value of water resources in the Xiaohong River Basin by the emergy analysis theory.

In terms of practical applications, derived from the accounting of water resource assets and liabilities, scholars have made a series of research results in the compilation of water resource balance sheets based on the system of environmental–economic accounting and the system of water environmental–economic accounting. Based on accounting and statistics, Qin et al. [

21] proposed a balance sheet structure for water resources, which accounted for water resource assets and liabilities. Utilizing accounting and statistical accounting principles, Jia et al. [

22] proposed water resource balance sheet accounting. Zhou et al. [

23] constructed a physical water accounting system for vouchers, books, and statements. Tian et al. [

24] designed a physical quantity accounting table and value-type balance sheet for water resources. Jian et al. [

25] established an accounting framework for multi-attribute water resource assets and liabilities. Jiao et al. [

26] maintained that the preparation of a water resource balance sheet should consider the accounting object and measurement method. Using the environmental replacement cost method, Liu [

27] explored accounting for the value of water resource liabilities and compiled a water resource balance sheet. Taking the Yangtze River Basin as the research object, Tang et al. [

28] used a case analysis method to analyze the preparation method and procedure for the water resource balance sheet, which fully demonstrated the preparation process of the water resource balance sheet. Focusing on the protection of the water environment in public project governance, Liu and Miao [

29] linked project governance with the water resources balance sheet and conducted research based on this aspect. Predicated on the water resource accounting theory and Australian water accounting standards, Hong [

30] developed an accounting framework for China’s water resource accounting entity. Li and Song [

31] conducted statistics on the quantity and value of water resource assets and liabilities in the Tibet Autonomous Region, forming a system of base table-auxiliary, table-main, and table-total tables. The preparation of a water resource balance sheet further strengthened the accounting and management of water resources, provided a basis for water resource protection, which was conducive to transforming economic development, and guided economic development towards green and sustainable development.

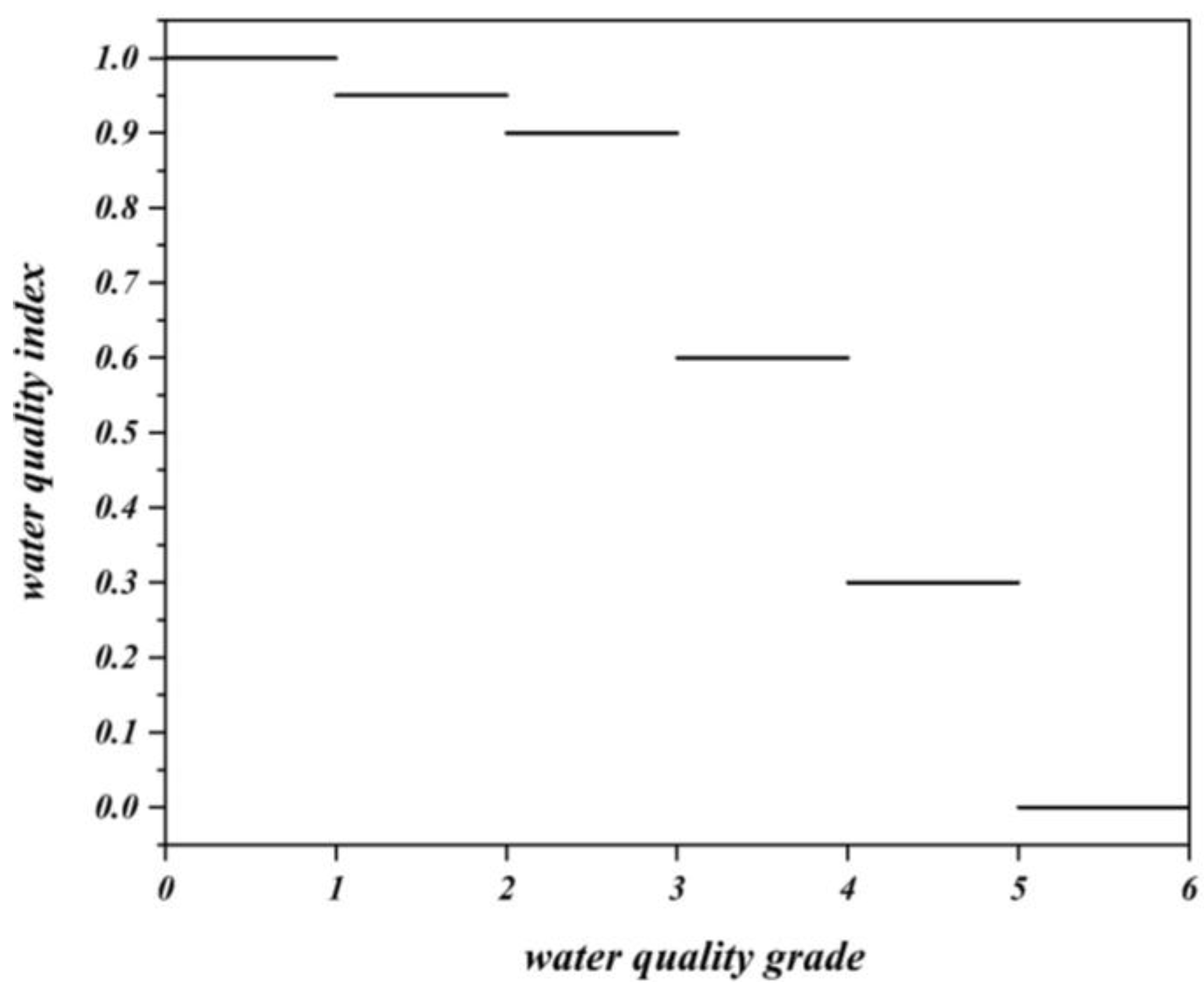

The above research explores the theory and application of water resource asset accounting. In theory, based on the concept and connotation of water resource assets and liabilities, the accounting method is proposed. In terms of application, specific preparation work was conducted using the water balance sheet framework. However, the current research needs to be further developed in the following aspects: (1) The current accounting methods often focus on the value of water resources, and the majority do not consider water use efficiency. The integrated water use efficiency reflects the different results of water resource utilization caused by the differences between industrial and water use structures, and how that affects water resource assets and liabilities. (2) Few studies have investigated the impact of water quality accounting. When water quantity and water use efficiency are constant, water quality levels are higher and the corresponding assets are higher. Studying only water quantity and water use efficiency, while neglecting the economic benefits of water quality, results in an inaccurate calculation of water resource assets and liabilities. This leads to a lack of rigor and integrity in the study of water resource balance sheets. Consequently, comprehensive water use efficiency has become a key factor in measuring water resource assets and liabilities, and it is also necessary to consider water quality when calculating the value of water resource assets and liabilities. In summary, this study proposes the improved four-stage DEA model to calculate the comprehensive water use efficiency coefficient, determines the comprehensive water quality coefficient according to the water quality grade, and then utilizes the comprehensive water use efficiency, comprehensive water quality coefficient, and their respective weights to determine the comprehensive coefficient of assets and liabilities. Simultaneously, it measures the size of water resource assets based on the correlation between water use and efficiency, and finally compiles the water resource balance sheet. Moreover, from the perspective of unified accounting of water quantity and quality, the concepts, connotations, and methods of calculating the comprehensive water use efficiency coefficient, the comprehensive water quality coefficient, and comprehensive coefficient are proposed and explained. Furthermore, calculation methods for water resource assets, liabilities, and net assets are addressed. Finally, a calculation system for water resource assets and liabilities for the unified accounting of water quality and quantity is constructed, which improves the accounting method for water resources, lays the foundation for the institutionalization and proceduralization of the water resource balance sheet, and highlights the direction of efforts for innovative water resource management methods.

4. Discussion

In contrast to the ‘Australian Water Resources Accounting Standards,’ which uses the quantity of water resources to represent water resource assets, this study compiled a water resource balance sheet from the perspective of unified accounting of water quantity and quality, breaking through the value accounting method that only focuses on water quantity, ignoring water quality and other factors. Simultaneously, it combined the attributes of water resources with socioeconomic attributes. Next, bringing water resources into full integration with the agriculture, industry, construction, and service industries by linking industrial structure with the water consumption structure, then the economic, environmental, and ecological values of water resources was comprehensively considered. Subsequently, the concept, connotation, and method of calculating comprehensive water use efficiency, comprehensive water quality, and comprehensive coefficients were proposed and explained. Finally, a method of calculating resource assets, liabilities, and net assets was discussed, and a system for calculating water resource assets and liabilities based on unified accounting of water quantity and quality was constructed. Meanwhile, it provided diversified quantitative information on water resources, water quality, and water quantity in Hubei Province from 2011 to 2020, reflected the fluctuation of water resource assets, liabilities, and net assets in Hubei Province from 2011 to 2020, and provided useful information for the planning, development, management, and protection of water resources. This method is straightforward, adaptable, intuitive, clear, and has a good reference value.

From a temporal perspective, the water resources assets, liabilities, and net assets of water resources in each prefecture-level city showed an ‘N’ trend from 2011 to 2020; specifically, water assets, liabilities, and net water assets showed an upward trend in 2011–2016, followed by a slow decline in 2016–2019, but a larger increase in 2020. The continuous drought in 2016 caused a slow decline in the total amount of water resources. Hence, water resource assets, liabilities, and net assets showed a slow downward trend from 2016 to 2019. Although Hubei Province is rich in water resources, water use efficiency is low due to climate reasons, and there is an uneven spatial and temporal distribution of precipitation. Accordingly, it is necessary to improve the carrying capacity effects of economic development on water resources, enhance the utilization efficiency of water resources, and consider green development as a significant aspect of economic development. In 2020, the total amount of water resources increased to a large extent because of the wet season; thus, the water resources assets, liabilities, and net assets of water resources increased.

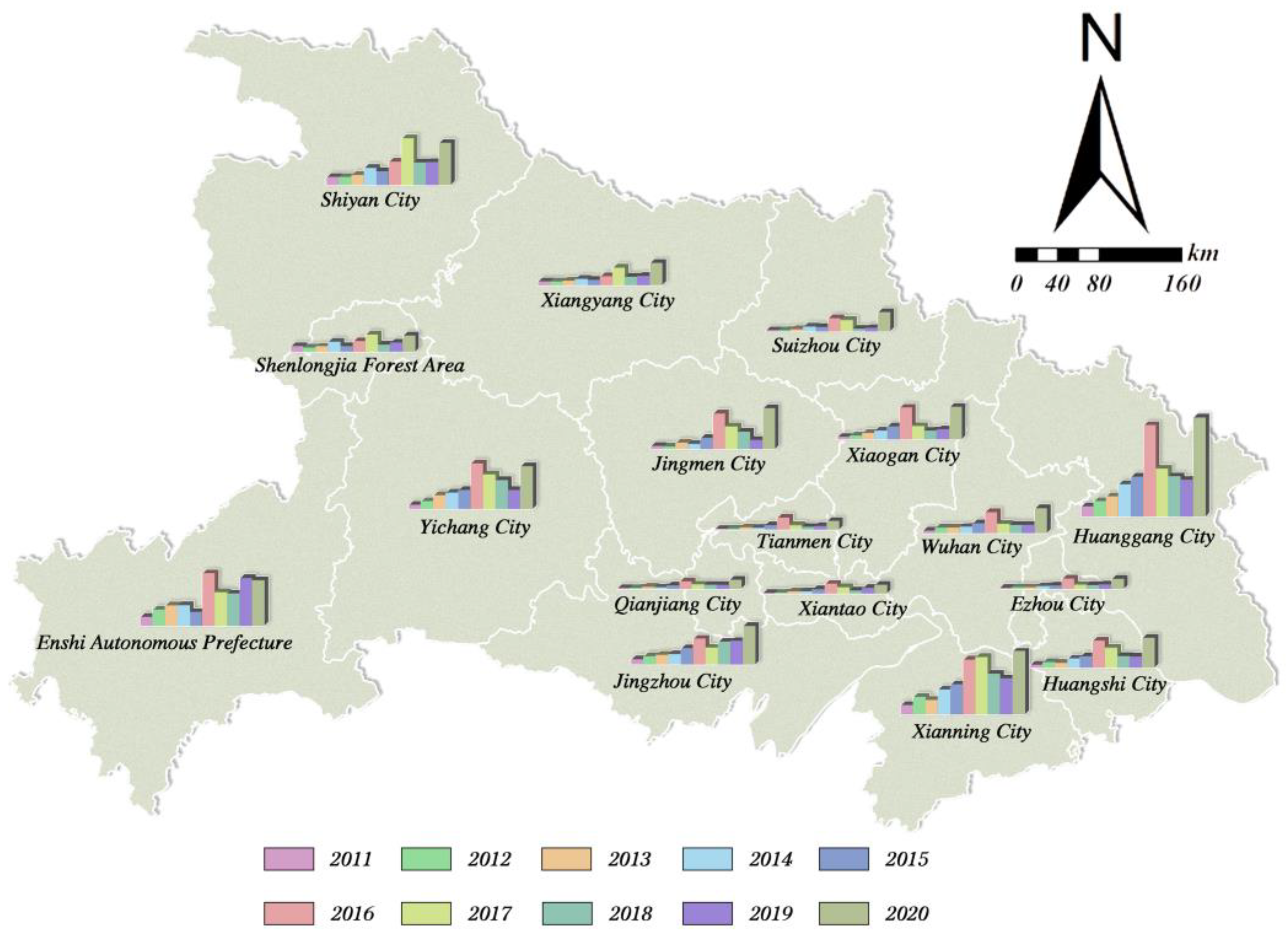

From the perspective of prefecture-level cities, based on the accounting theory and model calculation methods, the water resource assets, liabilities, and net assets show the same trend. The top four water resource assets belong to Enshi Autonomous Prefecture, Yichang City, Huanggang City, and Jingzhou City. This is due to abundant rainfall, the fact that water resources that have not been overexploited, and the good water quality; therefore, the comprehensive strength of water quality and quantity compared to that of other cities has obvious advantages, while the level of economic development is relatively high. In contrast, the Shenlongjia forest area, Ezhou City, Xiantao City, Tianmen City, and Qianjiang City ranked lower. This is attributed to the fact that they are prefecture-level cities with small volumes of water, low rainfall, and relatively poor water quality. Among them, although the water quality of the Shenlongjia forest area is quite remarkable, its comprehensive strength is lower than that of other cities due to the small volume of the forest area, very low rainfall, primitive natural environment, presence of few industries, and lower economic development level. The top two water resource liabilities belong to Huanggang City and Xianning City, and the water resource assets and liabilities of Huanggang City and Xianning City are relatively high due to their comprehensive level of economic development and medium-level water quality. However, the high precipitation influences the higher value of water resource assets, and the water resource liabilities are relatively high. The top four net assets of water resources belong to Enshi Autonomous Prefecture, Yichang City, Jingzhou City, and Huanggang City, and the primary reason is that the value of water resource assets is high, and that of water resource liabilities is low. Furthermore, Huanggang City has high water resource liabilities; however, its water resource assets are ranked high. Therefore, its ranking is moved back one place, and the overall water resource net assets ranking is also relatively high. In contrast, the Shenlongjia forest area, Ezhou City, Qianjiang City, Tianmen City, and Xiantao City, which are at the bottom of the list, have a relatively low value of water resource assets and a relatively high value of water resource liabilities; therefore, the net value of water resource assets obtained by subtracting the two is also relatively low. Among these, the net assets of water resources in the Shenlongjia forest area were negative in some years because of the small differences between its water resources assets and liabilities.

From a regional point of view, the assets, liabilities, and net assets of water resources in the eastern, central, and western parts of Hubei Provinces showed significant differences, but an overall upward trend. The changing trend of the three regions was the same during the study period, and was also consistent with the changing trend of the entire province. Meanwhile, the regional difference model of water resource assets, liabilities, and net assets is roughly the same as that of the economic level. The economy of the eastern region is relatively developed, the market mechanism is relatively perfect, market competition is relatively fierce, the resource input has changed to the intensive type, and comprehensive water use efficiency is high. Simultaneously, although the water quality is relatively poor, the water quantity is relatively rich; therefore, the value of water resource assets and net assets is relatively high, and that of water resource liabilities are low. In the west, despite the good water quality, and the fact that the economic development level is relatively low, the water resource utilization efficiency is low, and the water quantity is relatively low. Due to these reasons, the values of water resource assets and net assets are relatively low, and that of water resource liabilities are high. Based on the above analysis, this paper systematically puts forward the following countermeasures to increase the value of water resource assets and reduce that of water resource liabilities.

First, this study recommends promoting green transformation and the upgrading of agriculture to improve water resources assets. Agricultural water consumption accounts for the largest proportion of the actual water consumption in Hubei Province. From the “Hubei Province 2020 Water Resources Bulletin”, it can be seen that the effective utilization coefficient of farmland irrigation water in Hubei Province is only 0.528, and it is necessary to improve the utilization efficiency of agricultural irrigation water to improve water resources assets in Hubei Province. Based on this, the Hubei provincial government should save water to improve water quantity, optimize the water use structure, improve water use efficiency, reduce water consumption, and improve water resources assets. At the same time, Hubei Province needs to promote green transformation and the upgrading of agricultural technology, improve agricultural irrigation technology, and change sprinkler irrigation and flood irrigation into drip irrigation when necessary to reduce water waste. The transformation and upgrading of traditional agriculture is an effective means to improving the utilization efficiency of water resources. According to local characteristics, the development of regionally advantageous agriculture and the optimization of the layout of the agricultural industry is also important. According to the endowment of local water resources of each municipal area in Hubei Province, as well as the water demand and irrigation water demand of various crops, the rational layout is adopted to improve the effective utilization rate of water resources and improve the water resources assets.

Second, this study recommends strengthening the cross-regional joint prevention and co-governance mechanism to improve water resources assets. Hubei Province should establish a two-level water resource joint prevention and co-governance mechanism inside and outside the province to achieve effective supervision and management of water resources asset inflow, outflow and internal circulation, so as to improve water resource assets. The special geographical location of Hubei Province is very unique. Therefore, it is very important to establish a water resources joint prevention and co-governance mechanism with other provinces and cities in the upper, middle and lower reaches in order to understand the flow of water resource assets and the outside world. In addition, the municipal units in Hubei Province should also formulate a unified water resources joint prevention and co-governance system, and clarify the tasks to the municipal individuals below Hubei Province. According to the actual situation of individual water resources at the municipal level, the province should standardize the individual water resource protection standards, understand the internal circulation direction of water resource assets, and improve water resource assets.

Third, this study recommends identifying the individuals responsible for water pollution to reduce water resource liabilities. A sewage responsibilities list for the municipal unit should be set up to uniformly manage water pollution in the jurisdictional area. Next, it is necessary to strictly monitor the water quantity and water quality of the provincial and municipal demarcation points, avoid the influence of negative externalities, and strictly prohibit the phenomenon of shirking responsibility. If there is serious water pollution, it should be clear who is responsible for the problem and appropriate action needs to be taken. Finally, it is necessary to clarify reward and punishment measures. After a completed judicial process, if any punishment is required, it must be severe enough for the offenders in order for future potential offenders to respect the laws, so as to improve water resources and reduce water resources liabilities. At the same time, the ecological compensation mechanism should also be integrated into water resources management, and a horizontal water resources ecological compensation mechanism in the Yangtze River Basin and a joint ecological compensation mechanism in Hubei Province should be established. “Who pollutes, who compensates,” lists the individuals causing the pollution who should pay compensation, and the individuals with better water resource management practices can obtain compensation. If the overall water resource management effect is poor, the government can step in and manage this part of the fund as the overall water resource protection investment reserve, so as to reduce the water resource liability.

Finally, this study recommends establishing a water resource management supervision team to reduce water resource liabilities. Hubei Province should establish a water resource management supervision team to implement the real-time supervision of water resource management and reduce water resources liabilities. On the one hand, there should be clear standards of reward and punishment measures for the effectiveness of water resource management, and their timely implementation should be ensured to reduce water resources liabilities. On the other hand, the reasonable allocation of human, capital, and other resources can be carried out through the supervision group, which also ensures the effectiveness of resource utilization and reduces the debt of water resources. At the same time, we should also establish an ecological compensation mechanism among provinces and cities in the Yangtze River Basin, and use water resource liabilities as an indicator to measure the performance of provinces, cities and the audit of cadres leaving office, in order to reduce water resources liabilities. The supervision group should also continue to promote the implementation of the ‘river and lake chief system’, and carry out water pollution control, water resource protection, and water environment management for rivers, lakes, and reservoirs in the administrative region of Hubei Province, so that water resource management can be implemented through timely supervision, resulting in effectiveness, thereby reducing water resources liabilities.

5. Conclusions

From the perspective of unified accounting of water quantity and quality, the system and method for the calculation of water resource assets and liabilities based on the unified accounting of water quality and quantity are proposed in this paper. The correlation coefficients in the calculation system are calculated by reasonable methods, and the water resource assets and liabilities of 17 cities in Hubei Province from 2011 to 2020 are calculated and comprehensively analyzed. Accordingly, the following conclusions are drawn.

(1) Taking Hubei Province as the research object, the water resource assets, liabilities, and net assets of prefecture-level cities from 2011 to 2020 were analyzed and calculated. The results show that from a temporal perspective, the water resource assets, liabilities, and net assets of each prefecture-level city from 2011 to 2020 are increasing overall, albeit with fluctuations. From the perspective of prefecture-level cities, the top four water resource assets belong to Enshi Autonomous Prefecture, Yichang City, Huanggang City, and Jingzhou City; the top two water resource liabilities belong to Huanggang City and Xianning City; and the top four net assets of water resources belong to Enshi Autonomous Prefecture, Yichang City, Jingzhou City, and Huanggang City. From a regional perspective, the water resource assets, liabilities, and net assets of water resources in the eastern, central, and western regions of Hubei Province show obvious differences, however, the overall trend is increasing, albeit with fluctuations. The trends of the three major regions were basically the same during the study period, which is consistent with the trend in the province. The regional difference model of water resource assets, liabilities, and net assets is roughly the same as the economic level difference model.

(2) Hubei Province is rich in water resources, however, due to climate reasons and the uneven spatial and temporal distribution of precipitation, water use efficiency is low. Thus, it is necessary to improve the carrying capacity of economic development for water resources, improve the utilization efficiency of water resources, and consider green development as an important aspect of economic development. The calculation results of this research can play a guiding role in the scientific management and allocation of water resources in Hubei Province. The unified accounting of water quantity and quality provides a basis for the quantitative evaluation of water resource management levels, which will effectively improve the governance capacity of the water resource ecological and economic system.

In the future, to provide practical support for decision-makers and regional managers, it is of great significance to conduct more detailed and accurate research. For example, groundwater can be used as an independent and significant factor in the model, with additional detailed research being performed, including the obtention of more agricultural information such as that on crop species, surface water weight, and groundwater consumption.

,

,

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}