3.1. Cement Production Process and ESG Indicators

This representation in

Figure 1 provides a comprehensive overview of the cement production process, highlighting each key stage: raw meal grinding (

m = 1), calcination (

m = 2), cement grinding (

m = 3), and the three batching processes (

m = 4,

m = 5,

m = 6). A notable innovation in this process is the integration of waste from other industries as alternative raw materials. Particularly during the calcination stage (

m = 2), the high temperature, strong turbulence, and prolonged retention time effectively process the waste. The calcination yields useful by-products like sludge and slag, as well as essential elements such as silicon, aluminum, iron, and calcium, which are then recycled back into the production process. This strategy not only aids in waste management but also contributes to cost reduction, making the process more efficient and sustainable.

This study establishes specific objectives for the years 2023 to 2025, aimed at decreasing greenhouse gas emissions and improving resource recycling. The goals for greenhouse gas reduction, based on the 2016 baseline, are focused on CO2 emissions of cementitious material per ton. While the targets for 2023 and 2024 remain undefined, the ambition for 2025 is set at an 11% reduction. In terms of resource recycling, the study sets quantitative targets: 114 ten thousand tons in 2023, increased to 120 ten thousand tons in 2024, and further to 125 in 2025. These targets reflect a strategic move towards enhancing sustainability within the industry.

Key ESG indicators from the cement sustainability report are integrated into the study [

24]. The emphasis is on reducing CO

2 emissions and using alternative raw materials. The model applies the Theory of Constraints to systematically reduce CO

2 emissions annually while increasing the use of alternative materials. This approach aims to align with environmental sustainability, reduce the carbon footprint, and improve resource efficiency, demonstrating a commitment to sustainable industrial practices.

3.2. Research Assumptions

This model sets 3 periods to simulate the evolution of corporate production decisions and profitability when facing more stringent emission reduction requirements over time. The 3-period model can reflect the gradual increases in emission reduction efforts and alternative material usage, as well as their impact on corporate profits. Theoretically, the model can be extended to encompass more periods to simulate and predict corporate decision-making behaviors over a longer time horizon. However, considering the complexity of parameters, it is appropriate to currently set it as 3 periods.

This study uses the cement industry as a case to examine the impact of carbon tax and carbon credit (carbon right) costs on ESG indicators and corporate profitability. By integrating Activity-Based Costing and the Theory of Constraints, a production decision model for the enterprise is established. Mathematical programming methods are then applied to explore the effects of carbon tax and carbon credit costs on ESG indicators and profit. To isolate external uncontrollable factors, the following assumptions are made:

The company primarily produces four products: Cement finished product (i = 1), Traditional concrete (i = 2), High-fluidity concrete (i = 3), and Self-compacting concrete (i = 4), with unit prices remaining constant during production.

Seven main raw materials are used: Clinker (j = 1), Gypsum (j = 2), alternative materials (j = 3), Cement (j = 4), Aggregates (j = 5), Water (j = 6), and Pyrite (j = 7), with material costs fixed throughout production.

Waste from other industries is incorporated as alternative materials, for instance, sludge, slag, and elements like silicon, aluminum, iron, and calcium, which are then used as raw materials. This not only aids in waste treatment but also reduces costs.

The usage of alternative materials is considered an ESG indicator for the company, with yearly increments aiming to achieve the “Net Zero Emissions by 2050” goal.

During production, all steps are categorized into unit-level, batch-level, and product-level operations.

According to regulations and policies, human resources may work overtime, but wages are calculated based on overtime rates. Additionally, the utilization rates of all machinery and labor are 100%, with no idle resources, and wage rates remain constant throughout production.

Carbon tax is levied on the production of each unit of product, thus the tax amount depends on the quantity produced.

The cap on carbon credit trading is limited by government regulations, assumed to be unchanged in the short term, and the trading costs of carbon credits for each company are zero.

The ratio of carbon emission reduction (CO2 in tons/binder material in tons) is progressively increased yearly to meet the “Net Zero Emissions by 2050” target.

3.3. Objective Function

3.3.1. General Formula for the Objective Function

The objective is to maximize profit (

π). This is calculated as the total revenue from cement and concrete sales minus the total costs, which include direct material costs, direct labor costs, batch-level operational costs, product-level operational costs, carbon emission costs, and fixed expenses. To maximize profit (

π), the formula is defined as follows:

This objection function encapsulates the comprehensive cost structure and revenue streams within a cement and concrete business, taking into account various direct and indirect expenses as well as the environmental costs associated with carbon emissions. The goal is to optimize these variables to achieve the highest possible profit while maintaining operational efficiency and environmental compliance.

The general form of a multi-period objective function might be expressed as:

These definitions provide a structured framework for the mathematical modeling of the cement production process, taking into account various factors like product types, raw materials, production processes, and temporal dynamics.

| Maximization of profit |

| i | Product index where i = 1 to 4. Products are: i = 1 (Finished Cement), i = 2 (Traditional Concrete), i = 3 (High Fluidity Concrete), i = 4 (Self-compacting Concrete). |

| j | Raw material index where j = 1 to 7. Raw materials are: j = 1 (Clinker), j = 2 (Gypsum), j = 3 (Alternative Materials), j = 4 (Cement), j = 5 (Aggregates), j = 6 (Water), j = 7 (Chemical Additives). |

| m | Process index where m = 1 to 6. Processes are: m = 1 (Raw Meal Grinding), m = 2 (Calcination), m = 3 (Cement Grinding), m = 4, m = 5, m = 6 (Batching). |

| t | Time period index where t = 1 to 3. |

| Unit price of the ith product for different time periods (t = 1, 2, 3). |

| Quantity of the ith product in period t (i = 1~4; t = 1~3). |

| Quantity of the jth raw material required for producing one unit of the ith product during the tth time period (i = 1~4; j = 1~7; t = 1~3). |

| Total direct labor costs at points , and respectively. |

| Non-negative variables for period t, with at most two adjacent variables being non-zero (t = 1~3). |

| Unit batch-level cost in the mth process (m = 3~6). |

| Resource consumption per batch for the ith product in the mth batch-level process (i = 1~4; m = 3~6). |

| Number of batches for the ith product in the mth process during period t (i = 1~4; m = 3~6; t = 1~3). |

| Number of batches for the ith product in the mth batch-level process (i = 1~4; m = 3~6). |

| Unit product-level cost in the mth process (m = 3~6). |

| Resource consumption for the ith product in the mth product-level process (i = 1~4; m = 3~6). |

| Binary variable for period t, determining whether the ith product is produced (1 if produced, 0 otherwise) (i = 1~4; t = 1~3). |

| Total fixed cost in period t (t = 1~3). |

3.3.2. Direct Material Cost Function

This study assumes cement producers primarily use seven raw materials: clinker (j = 1), gypsum (j = 2), alternative materials (j = 3), cement (j = 4), aggregates (j = 5), water (j = 6), and Pyrite (j = 7). In the multi-period model, the usage of alternative materials (j = 3) will be progressively increased each year to meet the ESG targets by 2025, with the direct costs of these materials factored into the profit function.

Symbol Definitions:

| Unit cost of the jth raw material, (j = 1~7) |

| Quantity of the jth raw material required per unit of the ith product (i = 1~4; j = 1~7; t = 1~3) |

| Upper limit on the available quantity of the jth raw material in period t (j = 1~7; t = 1~3) |

| Lower limit on the available quantity of the jth raw material in period t (j = 3; t = 1~3) |

3.3.3. Direct Labor Cost Function

In the cement production process, direct labor, including regular and overtime hours, is a key component. This study assumes that the total direct labor cost function is a continuous piecewise linear function, as illustrated in

Figure 2. If the required direct labor hours exceed regular working hours, two different wage rates are applied for the two types of labor hours. It’s assumed that the wage rates for each segment in

Figure 2 are WR

0, WR

1, and WR

2, representing different rates for varying work hour segments.

Associated constraints for the labor cost function are also defined:

Symbol Definitions:

| Quantity of the ith product in period t, (i = 1~4; t = 1~3) |

| Non-negative variables where at most two adjacent variables are not 0, (t = 1~3) |

| Dummy variables (0, 1), where only one can be 1 for each period (t = 1~3) |

| Labor hours required to produce one unit of the ith product in the mth process. |

| The total number of labor hours under normal circumstances |

| Maximum number of labor hours falling in the first overtime segment, as shown in Figure 2 |

| Maximum number of labor hours in the second overtime segment, as indicated in Figure 2 |

3.3.4. Batch-Level Operational Costs

It’s assumed that four operational activities in the cement production process require estimation of machine handling costs: cement grinding (m = 3) and three batching processes (m = 4, m = 5, m = 6). These costs are deducted in the profit function.

The related constraint functions are:

Symbol Definitions:

| Unit machine handling cost for the mth process |

| Resource consumption per batch for the ith product in the mth process (i = 1~4; m = 3~6) |

| Output per batch for the ith product in the mth process (i = 1~4; m = 3~6) |

| Maximum available resources for the mth batch-level operation (m = 3~6) |

3.3.5. Product-Level Operational Costs

It is assumed that product-level operation costs, specifically for product batching, need to be estimated for four activities: cement grinding (m = 3) and three batching processes (m = 4, m = 5, m = 6). These product batching costs are subtracted from the profit function.

Constraint inequality includes:

Symbol Definitions:

| Unit cost of product batching for the mth process |

| Resource consumption for the ith product in the mth process (i = 1~4; m = 3~6) |

| Dummy variable (0, 1) for period t, determining whether the ith product is produced (i = 1~4; t = 1~3) |

| Maximum available resources for the mth product-level operation (m = 3~6) |

3.3.6. Constraints of Machine Hours

It’s assumed that three types of automated equipment are used in the manufacturing process: raw meal grinding (m = 1), calcination (m = 2), and cement grinding (m = 3), replacing traditional manual labor to enhance efficiency.

The related constraint inequality for machine hours is:

Symbol Definitions:

| Machine hours required to complete one unit of the ith product in the mth process (m = 1~3) |

| Upper limit of available machine hours for the mth process (m = 1~3) |

3.4. Carbon Tax Cost Function Model

3.4.1. Model 1: Continuous Incremental Progressive Tax Rate Function for Carbon Tax

This study develops a model for a continuous incremental progressive carbon tax function for the cement industry. The cost functions for multiple periods are designed to optimize profit while considering carbon tax expenses. The models are summarized as follows:

Figure 3 shows the function of carbon tax cost in the continuous incremental progressive tax rate. In

Figure 3, the upper limit of carbon emission quantity in the first, second and third sections is

,

and

, the carbon tax costs at the three points of

,

and

are

,

and

respectively, and the carbon tax rates are

,

and

respectively.

General expression of carbon tax cost function in

Figure 3 is shown as follows:

The general formula of the carbon tax cost function (15) is derived from this representation. It is a function of the company’s total carbon emissions (q) and is applied in a mathematical programming model. The model includes assumed carbon tax costs function (16), which are deducted from the company’s total profit, along with related restrictions (17)–(25).

Multi-Period Carbon Tax in Objective Function:

In Model 1, the study establishes the upper limits for carbon emissions at each stage as

. The carbon emissions generated from the

mth process for producing one unit of the

ith product are denoted by

(where m ranges from 1 to 6). The variables

are non-negative, and at most two consecutive variables can be non-zero (for periods

t = 1 to 3). The variables

are dummies (0 or 1), with only one being 1 in any given period (

t = 1 to 3). If

is set to 1, the other two are zero, and in (20) and (21),

would be zero, while in (18) and (19),

are less than or equal to 1. In (22), the sum of

equals 1. Consequently, from (17), it is determined that the total carbon emissions of the company for the first period are

, and the carbon tax cost is

. Alternatively, for a given period

t, if

= 1, then

are zero by (23) and (25). It means that the carbon tax cost is in the second segment of

Figure 3. On the other hand, the variables

are non-negative, and at most two consecutive variables can be non-zero (for periods

t = 1 to 3). If the point is in the second segment of

Figure 3, then

and

are non-zero and their sum is 1 by (22). Thus, the corresponding carbon tax cost is

by (16) and the corresponding carbon emission quantity is

.

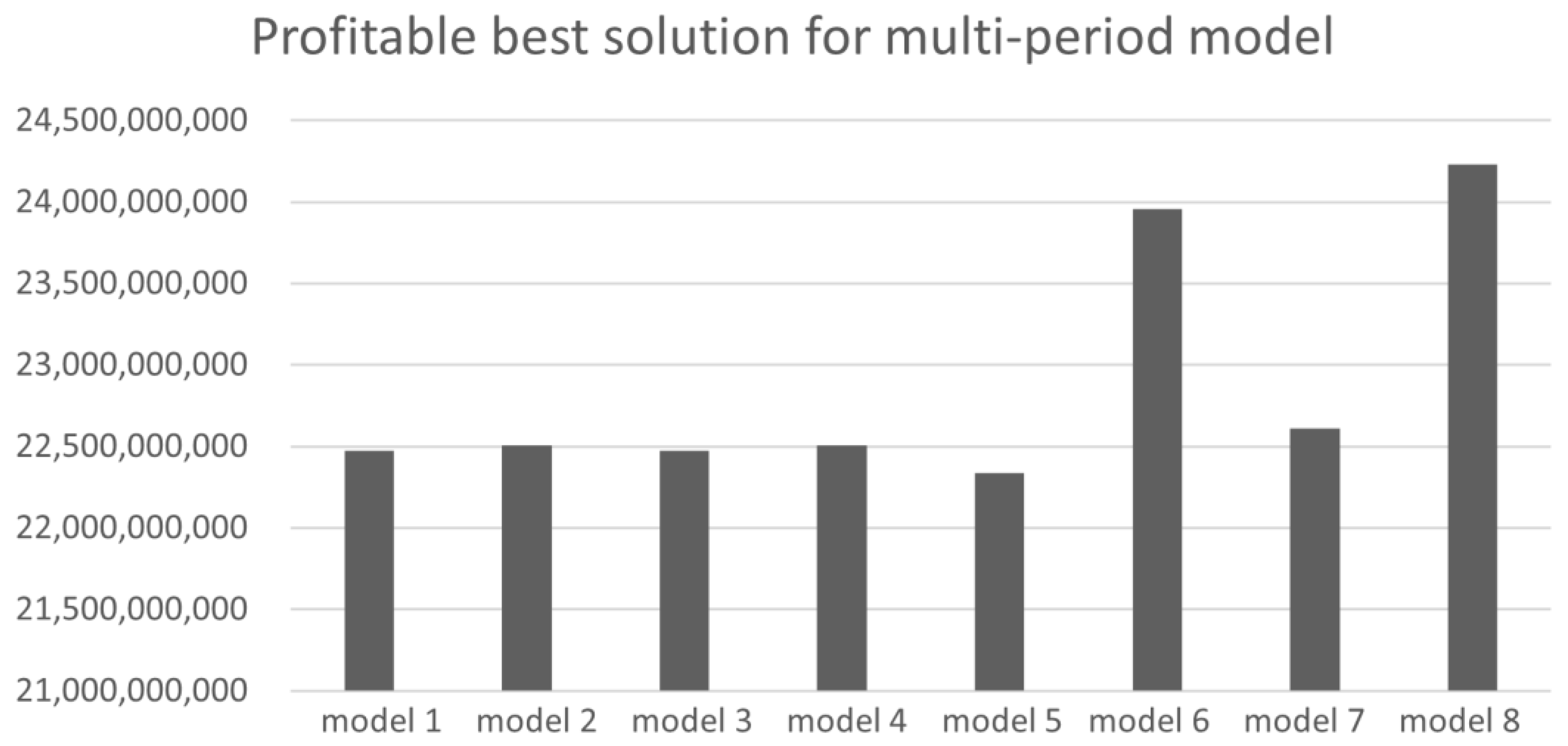

In the example, the total optimized profit across three periods (t = 1 to 3) amounts to $22,473,270,000. The profit is highest in the initial period, with subsequent periods showing a decline due to increased use of alternative materials and stricter carbon emission limits. The model also captures a decreasing trend in carbon emission ratios to over the considered timeframe.

3.4.2. Model 2: Continuous Incremental Progressive Carbon Tax Function with Tax Exemption

Model 2 of the study considers continuous incremental progressive carbon tax function with tax exemption. The carbon tax cost function of the progressive tax rate for continuous allowance increase is illustrated in

Figure 4. In this figure,

represents the total carbon emissions granted by the government for tax exemption, which are not subject to taxation within the carbon emission allowance. The first, second, and third interval have a capped carbon emission quantity at

,

and

respectively.

,

and

denote the cost of carbon tax at these respective levels while

,

and

represent their corresponding tax rates.

Henceforth, we can express the carbon tax cost function in

Figure 4 as function (26), which serves as a general formula encompassing continuous carbon tax costs with allowances. When calculating the company’s overall profit, it is necessary to deduct the assumed carbon tax costs specified by (27) and (28) in this model. Constraints related to the cost of carbon taxes are defined by (28)–(36).

The general formula for the carbon tax cost function is:

In a multi-period scenario, the function is defined in the objective function as:

The related constraints for the carbon tax cost function are:

Thus, it means that the mathematical fuction f(q) is represented as (27) in the objective function and the associated constraints (28)–(36). If is set to 1, then and are constrained to be zero in (31) and (32). In (29) and (30), and are limited to be less than or equal to 1. In (33), the sum of and must equal 1. Therefore, based on (28), it can be determined that the total carbon emissions of the company are less than or equal to plus , with the carbon tax cost being .

In the example, the total best profit for the enterprise across multiple periods amounts to $22,506,340,000, with the highest profit achieved in the first period. The second and third periods show lower profits due to the consideration of increased lower limits for the use of alternative materials and reduced upper limits for carbon emissions. Additionally, the carbon emission ratio demonstrates a year-over-year declining trend.

3.4.3. Model 3: Continuous Incremental Progressive Carbon Tax Function with Carbon Trading

When the government allows carbon trading, in addition to the carbon tax costs, the costs and benefits of carbon credits must also be considered. Therefore, this section extends the continuous incremental progressive carbon tax cost function of

Section 3.4.1 by adding carbon trading functions to the model assumptions. This study assumes that the company uses a single carbon credit price (α) to purchase or sell carbon credits. Hence, the continuous incremental progressive carbon tax cost function, including the cost of carbon credits, is represented by (37).

The multi-period carbon tax objective function, with carbon trading, is formulated as follows:

The related constraints are as follows:

For periods t = 1 to 3, and are dummy variables, each taking a value of 0 or 1, with only one being 1 at any time. If is 1, then by (41), is 0, indicating that the company’s total carbon emissions qt fall within the range [0, ] by (39). This implies that the company doesn’t need to buy carbon credits and can even sell them, with the carbon emission costs being calculated as .

The multi-period continuous incremental progressive carbon tax function with carbon trading (Model 3) achieves an optimal profit of $22,744,860,000. By incorporating carbon credits as part of the profit function, the profits are higher compared to Model 1.

3.4.4. Model 4: Continuous Incremental Progressive Carbon Tax Objective Function (Including Tax Exemption and Carbon Credits)

This section builds upon the continuous incremental progressive carbon tax cost function from

Section 3.4.1 and incorporates the tax exemption granted by the government from

Section 3.4.2 as well as carbon trading from

Section 3.4.3 for the model’s assumptions. The study hypothesizes that the company operates carbon trading at a single carbon credit price (α), hence the continuous incremental progressive carbon tax cost function now includes the costs of tax exemption and carbon credits as represented by (42).

For the multi-period model, the continuous incremental progressive carbon tax cost function that includes both tax exemption and carbon credits is given by:

The related constraints are as follows:

If is set to 1, then = 0 by (46). Then, by (44), the company’s total carbon emissions qt will be within the range [0, , implying the company need not buy carbon credits and may sell them instead. At this point, the carbon emission cost is given by .

3.4.5. Model 5: Discontinuous Incremental Progressive Carbon Tax Objective Function

Figure 5 illustrates the carbon tax cost function for a discontinuous incremental progressive tax rate, composed of three consecutive sections. In

Figure 5, the maximum carbon emission limits for the first, second, and third sections are

,

and

, respectively. The carbon tax rates at these points are

,

, and

, and the carbon tax costs are calculated as

,

, and

, respectively.

Therefore, the carbon tax cost function illustrated in

Figure 5 can be represented by functions (47). This function serves as a general model for the discontinuous carbon tax cost function, which also corresponds to the company’s total carbon emissions (

q) and can be represented through a mathematical programming model. Function (48) is the assumed carbon tax costs in this model and must be deducted when calculating the company’s total profit, while (49)–(54) are the constraints related to carbon tax costs.

General Expression of Carbon Tax Cost Function:

Multi-Period Discontinuous Incremental Progressive Carbon Tax Cost Function:

If is 1 in the first period, according to (53), and are 0, and thus, based on (50), the total carbon emissions for the first period fall between [0, ], and the carbon tax cost is calculated as .

3.4.6. Model 6: Discontinuous Incremental Progressive Carbon Tax Function with Tax Exemption

This section extends the discontinuous incremental progressive carbon tax function, incorporating a tax exemption as established in Model 5. The carbon tax function in Model 6 accounts for multiple periods.

Figure 6 illustrates the discontinuous incremental progressive carbon tax function with tax exemption. Here,

represents the total carbon emission quantity exempted from taxation by the government. The upper limits of carbon emissions for the first, second, and third segments are

,

and

, respectively. The carbon tax costs at these points are

,

, and

, with corresponding tax rates of

1,

and

.

The carbon tax cost function in

Figure 6 is represented by Function (55), serving as a general model for the discontinuous carbon tax cost function with a tax exemption. This function also relates to the company’s total carbon emissions (

q) and is represented through a mathematical programming model. Function (56) is the assumed carbon tax costs in this model, which must be deducted when calculating the company’s total profit. Constraints (57)–(62) are constraints related to the carbon tax costs.

General Expression of Carbon Tax Cost Function:

Multi-Period Discontinuous Incremental Progressive Carbon Tax Cost Function with Tax Exemption:

are described as dummy variables, which can only take values of 0 or 1. In this case, if is equal to 1, then according to (62), the rest of the variables must be 0. (59) suggests that this is part of a larger set of functions and conditions in the model. It implies a range or bracket of carbon emissions (, ], and the carbon tax cost for emissions within this range is given .

In the multi-period discontinuous incremental progressive carbon tax objective function—Model 6 (with tax exemption), the optimal profit is $23,958,560,000. The profit is highest in the first period and decreases in the second and third periods due to increased usage of alternative materials and lowered carbon emission limits. Additionally, the carbon emission ratio exhibits a declining trend annually.

3.4.7. Model 7: Discontinuous Incremental Progressive Carbon Tax Objective Function with Carbon Trading

With the introduction of carbon trading by the government, companies must consider the costs and benefits of carbon credits in addition to carbon tax expenses. This section continues from Model 5 (

Section 3.4.5), incorporating the discontinuous incremental progressive carbon tax cost function with carbon trading functions. The study assumes that companies buy or sell carbon credits at a single price (α). Therefore, the discontinuous incremental progressive carbon tax cost function, including the cost of carbon trading, is represented by functions (64).

Multi-Period Discontinuous Incremental Progressive Carbon Tax Objective Function (Including Carbon Trading):

and are dummy variables (0 or 1), where only one can be 1 in a given period. If is 1, then is 0 as per (68), and the total carbon emissions fall within [0, ] as per (66). This implies the company does not need to buy carbon credits and can even sell them, making the carbon emission cost at this point .

In Model 7, which integrates carbon trading with a discontinuous incremental progressive carbon tax system. In the multi-period model, the maximum profit (MAX π) reaches $22,610,140,000. This encompasses the profits, carbon tax costs, carbon emission ratios, and material quantities for each period, with the profits being highest in the first period and gradually decreasing due to heightened use of alternative materials and stricter emission limits. The inclusion of carbon trading significantly boosts the profit compared to previous models without it.

3.4.8. Model 8: Discontinuous Incremental Progressive Carbon Tax Function with Tax Exemption and Carbon Trading

This section extends the discontinuous incremental progressive carbon tax cost function from

Section 3.4.5, incorporating the tax exemption provided by the government as outlined in

Section 3.4.6 and the carbon trading mechanism as detailed in

Section 3.4.7. The model assumes that companies buy or sell carbon credits at a uniform price (α). Consequently, the carbon tax cost function in this model integrates the costs related to both tax exemption and carbon trading, as detailed in functions (69).

For the Multi-Period Scenario (Model 8):

This model defines and as dummy variables (either 0 or 1). When is 1, as per function (69), is 0. According to (73), if is 1, this indicates that the total carbon emissions of the company are within the range [0, , implying the company is not required to purchase carbon credits and may even sell them. In this case, the carbon emission costs are calculated as the sum of the costs in each segment minus the revenue from selling excess credits: .

In the multi-period scenario, the total optimal profit rises to $24,230,140,000. This increase is attributed to the model’s incorporation of tax exemptions and carbon trading, which optimizes profits across three periods. The model demonstrates the highest profitability among the discontinuous type models due to these combined factors.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}