1. Introduction

Taxation is essentially a political and social issue, as it is inextricably linked with the common goals of any society. In modern polities the implementation of such goals (related to education, health, retirement, and many others) relies, at least in part, on resources collected through taxes. The classical perspective distinguishes between taxes on income, taxes on capital, and taxes on consumption. These taxes can be found in varying proportions in nearly all countries and historical ages. This list is completed in the 20th century with a fourth category, namely contributions to social insurance programmes. This article focuses on income taxation and the democratic principle according to which the structure of taxation and the destination of taxes should reflect the will of the citizens.

The process of accumulation of private capital after the Industrial Revolution gave rise to an unprecedented concentration of wealth and, consequently, to skyrocketing inequalities. As sharp inequalities can be easily linked to political conflict, starting with the last decades of the 19th century, both academics and politicians became growingly interested in developing tools of social redistribution. In many Western polities, progressive income taxation was first adopted in the years preceding the First World War as ‘a way of limiting the inequalities produced by industrial capitalism while maintaining respect for private property and the forces of competition’ [

1]. Initially, tax rates were set quite low. After the war, the top rates were rapidly raised to compensate for the difficult economic situation. As the welfare state expanded between 1910 and 1980, the top rates of progressive income taxation in the wealthy countries continued to rise; they were stabilized after 1980 [

1].

Today, progressive income taxation schemes are still regarded as a highly effective tool of social redistribution [

2] and a powerful instrument for reducing social inequalities. For more than a century, their very existence has been taken for granted across Western democracies, without facing any sort of real challenge from economic theory. The only points of debate have been the number of income tax brackets and the top rates of taxation.

The overall landscape of taxation has changed rapidly in the Central and Eastern European (CEE) post-communist countries. Many of these countries have decided to replace progressive taxation with a flat-rate alternative in a very short time frame. Seventeen of them implemented some sort of single tax rate on the earned income of all taxpayers from 1994 to 2011 [

3,

4,

5]. The line-up was opened up in 1994 by a bold movement of the Estonian economically liberal government (for more details, see [

3]). Later, similar public policies spread in the CEE region in a process of cross-national emulation [

6]. The adoption of some sort of flat tax rapidly became the signal that these countries were ‘open for business’ [

4] and consequently turned into a matter of regional and international competitiveness.

The idea was not exactly new. Its origins are usually linked to a ‘

Wall Street Journal’ article of Robert Hall and Alvin Rabushka [

7], which advocated for a simplifying tax system based on two core principles: all incomes should be taxed only once, and all types of income should be taxed at the same rate. They argued their solution would come with many advantages, among which were providing simplification, improving incentives for paying taxes, lowering the costs of compliance with the tax system, and improving capital formation [

8]. Their ideas were met with reluctance in most Western societies and opposed by international financial institutions [

3]. However, they found a fertile soil in many CEE countries, where many right-wing politicians regarded the flat tax as a panacea for all the problems of post-communist transition: the state’s incapacity to collect taxes, lack of economic competitiveness, a desperate need to attract foreign investment, rising unemployment, and citizens’ limited fiscal literacy [

3,

4].

Regardless of the diversity of CEE countries in terms of economies and political systems, there are limited variations in the design of the flat tax programs adopted by them. In most cases, flat tax reform lowered the top marginal tax rates on personal income, widely seen as an incentive for greater economic activity and driving taxpayers out of the shadow economy [

4]. The occurrence of these two effects was later contested [

9], but an increase in the competitiveness of these countries in attracting direct foreign investments was clearly visible in the following period [

10].

These CEE countries had a tradition of politically consensual progressive income taxation, and the turn towards the flat tax was politically highly divisive. This was an extreme change for these countries, as previously no conflicting views on taxation along partisan lines existed [

3]. Suddenly, different parts of the political spectrum were in a state of disagreement over the flat tax. However, as very little is known about public opinion on taxation in CEE countries, it is unclear whether (and to what extent) this polarization was translated into a societal level [

5]. Moreover, the short-term impact of this fiscal revolution for the poorer segments of the societies was not obvious. The personal income taxes poorer citizens paid did not necessarily increase, either due to the new rate implemented (see [

9]), or to the various exemptions or deductions applied [

3].

Like other countries in the region, Romania has seen an abrupt shift from progressive to flat-rate taxation in 2005, implemented by the coalition government led by the right-wing Justice and Truth Alliance. Using survey data from the Romanian Election Study (RES), this article investigates the determinants of public support for flat-rate personal income taxation (PIT) in Romania eight years after the tax reform. The validity of typical explanations of attitudes towards fiscal policies (self-interest, ideology, trust, political knowledge, socio-demographics) is assessed for the Romanian context. The analysis adds a new element to the debate, namely social solidarity as a determinant of support for flat-rate PIT. The article contributes to the literature on the sustainability of tax reforms in CEE countries by addressing an aspect ignored in the debate, namely how public opinion addresses the issue. It mainly asks three questions. What is the level of support for flat-rate PIT in Romania? What are the main determinants of this support? Does social solidarity bring a reliable contribution to the efforts of explaining fiscal preferences, particularly in times of societal crises?

In

Section 2, the article discusses the main explanations of individual preferences for progressive and flat-rate taxation schemes.

Section 3 describes the path towards flat-rate personal income taxation in the Romanian context, with a focus on the political framework of adoption, the position of the main actors, and the few pieces of information on citizens’ views on the topic.

Section 4 covers the methodological aspects of the study. The main findings and conclusions are presented and discussed extensively in

Section 5 and

Section 6.

2. Literature Overview

The literature on the determinants of individual preferences for one taxation scheme or another is rather limited, and mostly focuses on explaining the support for progressive taxation. A classic assumption that much of the literature relies upon is the famous Meltzer–Richard [

11] theorem, according to which rising inequalities will lead to demand for greater redistribution and hence progressive taxation. Thus, the more unequal a society, the larger the group of people that would benefit from higher taxation of those earning above the average income [

5]. Consequently, income and an individual’s position in the overall income distribution should influence the preference for progressive or flat taxation. Income functions as a measure of

self-interest, and is considered a strong determinant of taxation policy preferences by many recent studies [

5,

12,

13,

14]. High-income earners are less in favour of progressive taxation policies than low-income earners, and are more likely to support flat taxes [

14,

15].

Together with self-interest,

ideology is widely discussed as one of the strongest determinants of preferences for public social spending [

16,

17], with the assumption that left-leaning individuals are more supportive of redistribution than right-leaning ones. In addition, the impact of self-interest on redistribution preferences is expected to be weaker among left-wing individuals [

16]. However, there is little empirical research testing these assumptions. The conclusion of Stiers et al. [

14] is that right-wing Belgian respondents are more likely to support a flat tax. Their data also show that the relation between ideology and support for flat taxation is moderated by political sophistication: higher sophisticated respondents are more likely to bring support for a flat tax in line with their ideological opinions [

14].The findings of Fernández-Albertos and Kuo [

13] on Spain fit into the same pattern, with conservative individuals preferring lower PIT progressivity ratios.

Considerations about

fairness are also investigated as an explanatory factor of citizens’ fiscal policy preferences. A considerable body of research argues that the demand for tax progressivity increases when economic outcomes within a society are perceived as unfair [

5,

18,

19,

20]. Limberg [

20] differentiates among three dimensions of fairness perception with an influence on tax preferences. For the first one (background), demand for redistributive measures in a society is higher if success is perceived as dependent upon family background, and thus intergenerational mobility is low [

21]. For the second one (individual), people tend to be less supportive of progressive PIT if they perceive economic success or differences in social standing as a result of an individual’s work, performance, or talent [

5,

19]. For the third dimension (structural), support for progressive taxation is higher when people perceive that a subgroup of a population is treated beneficially by the state [

5,

19].

Various perspectives on

trust are also approached as determinants of individual preferences for tax policy. The general expectation is that people are more willing to contribute to collective redistribution only if they trust others doing the same [

22]. However, ‘others’ might mean other individuals (social trust) or the state authorities (political trust). In a comparative study on 26 welfare states, Roosma et al. [

22] conclude that social trust is a strong predictor of contentedness with the ‘classical’ progressive tax systems: “high trust strengthens the feeling that others pay their fair share of taxes”, while “low social trust explains tax revolt, implying that people reject redistribution via taxes because they do not trust others to pay their fair share”. Political trust is an entirely different story, as distrust towards authorities increases support for progressive PIT, especially among low- and middle-income groups [

5,

23].

Age and

education are also discussed in relation to fiscal preferences. Support for progressive taxation increases with age [

5,

14,

19,

24]. For CEE countries, this is usually explained as an effect of socialization under state socialism among older cohorts [

5,

25]. However, the trend is similar when Western societies are investigated [

14,

22]. The relation between education and preferences for taxation is less straightforward. In a comparative analysis of 32 countries, Limberg [

20] finds that people with a higher level of education have a lower demand for tax progressivity. Roosma et al. [

22] conclude that higher education attainment is a good predictor of contentedness with the current tax scheme, while lower education favours an attitude of tax revolt. Other studies find no significant effect of education on tax preferences [

5,

13,

19].

Quite unexpectedly, although various perspectives on the concept are frequently put forward in relation to the welfare state and redistribution,

solidarity is almost never investigated as a determinant of fiscal preferences. The exception is a recent article by Cabelkova and Smutka [

26]. As a broad concept, solidarity is described as some sort of bond that holds a group or a community together [

27]. Contemporary sociology usually conceptualizes solidarity as embodied in individuals [

28], frequently regarding it as an individual latent orientation towards being benevolent, sympathetic, committed to, and concerned with the fate of other people [

29,

30]. In line with this, Stjernø [

31] approaches solidarity as a form of “preparedness to share resources with others by personal contribution to those in struggle or in need and through taxation and redistribution organised by the state”, originating in either morality or reciprocity. These targets of solidarity are social groups that may be located closer or more remotely in relation to the individual, and thus various levels of solidarity are discussed: family/local solidarity, social solidarity, and global solidarity [

32,

33,

34,

35]. A reasonable expectation, partially confirmed in the analyses of Cabelkova and Smutka [

26] of citizens from the Czech Republic, is that there is a strong and positive relation between solidarity and preferences for progressive PIT.

The impact of several other determinants at individual or country level on individual taxation preferences is seldom assessed in the literature. Thus, there are rather inconsistent results on the influence of:

gender [

14,

26],

religiosity [

20,

36,

37],

egalitarian values [

38],

party identification [

39],

political sophistication [

14],

unemployment rate [

20],

social inequalities [

5], and

economic development [

5,

20].

3. The Path to Flat Personal-Income Taxation in Romania

The idea of a shift towards a flat-rate PIT in Romania was initially put on the public agenda in 2003 by the Romanian Academic Society (SAR), an influential Bucharest think tank widely perceived as neoliberal in orientation [

40]. SAR [

41] advocated in favour of a flat tax of around 18%, portrayed as a ‘genuine fiscal revolution’ which could simplify the calculation and collection of taxes and stimulate economic growth via a massive reduction in tax evasion. The idea found a surprising supporter in the person of the social democrat minister of finance Mihai Tănăsescu, who put it on the political agenda and apparently even gained the support of the then prime minister, Adrian Năstase [

40,

42]. However, the Social Democrats abandoned the idea due to the opposition of the Romanian President Ion Iliescu, the de facto leader of their party [

42], which raised a nervous reaction from SAR [

43].

Subsequently, the flat tax was proposed as a central topic of the electoral agenda by the right-wing Justice and Truth PNL-PD Alliance (ADA) in the hard-fought national elections of 2004 [

42]. Following the election of Traian Băsescu as President, a coalition government was formed around the Justice and Truth Alliance, with the liberal Călin Popescu-Tăriceanu as prime minister. In its first meeting on 29 December 2004, the new cabinet adopted the Emergency Government Ordinance No. 138/2004, introducing the flat tax and other fiscal measures. In the race to adopt and implement a flat PIT rapidly, the Popescu-Tăriceanu government infringed the tax code stipulations requiring a six-month waiting period for tax policy changes [

44,

45]. Thus, the changes took effect only three days later.

The main fiscal measure adopted was the introduction of a flat tax rate of 16% on personal income. This replaced the previous system of progressive taxation, in place between 1990 and 2004, with rates of 18%, 23%, 28%, 34%, and 40%, corresponding to five income brackets [

46]. Thus, the new rate was even lower than the previous bottom marginal tax rate on personal income. The profit tax rate was also reduced from 25% to 16%. Dividends paid to individuals, interest income, and capital gains were subject to final withholding taxes at lower rates than 16% [

9].

Despite being adopted in a manner that lacked any form of political debate, the flat-rate PIT scheme has never been really challenged since 2005. Although it was put into practice by right-leaning actors that supported the idea of lower and simpler taxes, the flat tax policy transcended partisan politics, and became the very label of a business-friendly and internationally competitive economy [

44]. In 2018, the flat tax rate was lowered from 16% to 10%, as part of a new ‘fiscal revolution’ implemented by a coalition government formed around the left-wing Social Democratic Party (PSD).

Many years after its initial implementation, political criticisms of the flat tax remain rather few and isolated in Romania. The main critical voices come from the academic community, which criticized the flat tax for side effects in terms of increasing social inequalities [

47], insufficient resources for the state budget [

48,

49], shifting the taxation burden towards labour and consumption [

42], and increasing the commercial deficit [

49].

However, the overall appeal of the new fiscal scheme among the general population is largely unknown. Apparently, its smooth acceptance may have been related to the fact that the tax rate adopted in 2005 was reducing the tax burdens for all citizens, as compared to the previous situation. At least in theory, everyone benefited from the decrease in PIT rate, although the rich had more to gain than the poor.

Public support for flat-rate taxation was rarely measured in national surveys in Romania in the almost two decades since its adoption. In a 2009 pre-electoral RES survey, only 38.3% of the respondents (44% of the valid responses) were in favour of a unique PIT rate, no matter how big an individual’s income is. Support for the flat tax was even lower in 2013, after a period of economic trouble, when only 30.6% of those surveyed (35.9% of the valid responses) were favourable toward it. The two measurements were taken from the same sample, using the same question format, as part of a RES long-term panel survey [

50]. Thus, the drop in support was not due to a different question format, sample structure or sampling strategy.

Three years later, another RES survey [

51] found a preference for progressive taxation for 74.7% of the population (78.9% of the valid responses), while its rejection rate (thus, a preference for flat tax) was 12%. Finally, in 2022, support for a unique PIT rate was calculated at 23%, using data from a Friedrich Ebert Foundation study [

24]. Although the results of these studies are not perfectly comparable, mainly due to variations in the question format, they suggest that the preference for the flat tax within the population has never been as widespread as it is among politicians. Apart from this, it follows a descending trend, in an apparent synchronicity with the succession of social and economic crises faced by the citizens in recent years.

4. Data and Methods

In order to investigate the determinants of support for the flat PIT in Romania, this article employs data from a post-electoral survey (N = 1105) conducted on the occasion of the Romanian legislative election held in December 2012 [

50]. Data were collected between 15 December 2012 and 30 January 2013, via tablet-assisted personal interviews (TAPI) in households, using a two-stage stratified probability sample, representative for the Romanian adult population. Briefly, the composition of the sample was: 51.8% women, 48.2% men; 25.5% aged below 35, 35.8% aged 35 to 54, 38.7% aged above 55; 1.4% with no formal education, 17% with higher education (BA, MA, PhD); and 43.5% residents in rural areas, 56.5% residents in urban areas.

This source of data was used for two reasons. First, it is the only source of publicly available survey data providing a reliable measurement of fiscal preferences in the aftermath of an economic crisis, which meant, for Romania, harsh cuts in welfare programs. Second, it is the only survey dataset for Romania which includes the items typically employed for measuring solidarity in its main dimensions [

32,

33,

34].

Combining the insights from the literature discussed above with specific expectations for the case of Romania, this article aims at testing six hypotheses on how individual-level characteristics influence the preference for the rather recently implemented flat-rate personal income taxation. These hypotheses are summarized below.

H1. Respondents with higher incomes are more likely to support the flat tax.

H2. Older respondents are more likely to disagree with flat taxation.

H3. Respondents attaining higher levels of education have a stronger preference for the flat PIT.

H4. Right-wing-oriented individuals are more likely to support flat taxation.

H5. Respondents with higher levels of social solidarity are less likely to support the flat tax.

H6. The more respondents distrust public authorities, the more likely they are to disagree with the flat tax.

To provide empirical testing of the six hypotheses, a sequence of logistic regression analyses was run, using SPSS Statistics version 23. A comprehensive presentation of the variables included is provided in the following paragraphs. The exact wording of the RES survey questions employed is presented in

Appendix A.

4.1. Dependent Variable

The dependent variable is individual

support for a flat tax rate. It is a binary variable, generated based on the RES question asking respondents to express their agreement with the statement that ‘people should pay the same tax rate, no matter how much they earn’. Responses collected on a 4-point scale (‘fully agree’, ‘agree’, ‘disagree’, ‘fully disagree’) were subject to recoding in a binary format, where ‘1’ means ‘support for a flat tax rate’ and ‘0’ means ‘lack of such support’. This question format is different from the standard survey question employed in studies about fiscal preferences, asking respondents about their agreement with the statement that the government should actively reduce differences in income levels (see the discussion on this in [

14]). It comes with a clear advantage in clarity compared to the traditional question, which might have been subject to various interpretations (the choice of a progressive taxation scheme is not the only available solution for reducing income differences). Nonetheless, the RES question format provides less analytical flexibility compared to the alternative employed in the Belgian Electoral Study of 2019 used by Stiers et al. [

14].

4.2. Independent Variables

The socio-economic and demographic independent variables included in the model account for personal income, education, age, and gender. Self-declared personal income for the previous month is collected in Romanian lei (RON) using an open-ended question format and then transformed in thousands RON (divided by 1000) for an easier representation of its impact. This variable is expected to provide a picture of how self-interest affects fiscal preferences. Education is measured as the ‘number of school years completed’ and ranges from 0 to 26 in the RES sample. Respondent’s age is calculated as the mathematical difference between the year of data collection and the reported year of birth. Finally, gender is coded ‘1’ for male respondents and ‘0’ for the females.

The attitudinal independent variables in the model include ideology, political trust, and social solidarity.

Ideology is measured in the RES questionnaire as self-placement on a left–right 0–10 continuum, in which 0 is the most extreme position to the left and 10 the most extreme to the right. As the item is often referred to as problematic in the context of post-communist Romania (see [

52]), an individual’s self-declared right-leaning orientation (7–10 score) is considered as a likely predictor of support for a flat PIT. Thus, the initial 0–10 left-right scale is recoded into a binary format, where ‘1’ is a respondent self-identified as having a right-leaning political orientation, while ‘0’ covers all alternative stances. The

political trust item employed in the model requests respondents to assess their level of trust in the Romanian Government on a scale from 0 to 10, where 0 is ‘no trust at all’ and 10 is ‘full trust’.

Social solidarity is measured as an additive index combining two indicators: expressed concern for the living conditions of the poor and of the unemployed (

r = 0.756). The exact RES question asks respondents to assess the extent to which they feel ‘concerned about the living conditions and the welfare’ of the poor/unemployed. The answers are collected on a scale from 0 to 10, where 0 means ‘not at all’ and 10 ‘very much’. The resulting index of social solidarity ranges from 0 to 20, higher values reflecting stronger levels of social solidarity. The approach is similar to the one employed by Rusu and Gheorghiță [

53] in an attempt to measure transnational solidarity based on European Values Study (EVS) data.

Apart from these, an index of objective

political knowledge completes the list of independent variables. It is calculated as the number of correct responses to a sequence of five political-knowledge items included in the RES questionnaire, and ranges from 0 (least) to 5 (best). The choice behind the inclusion of a measure of political knowledge as a control variable in the model originates in the findings of Stiers et al. [

14], according to which more informed individuals have better capabilities to match personal interests with their position on fiscal preferences.

5. Results and Discussion

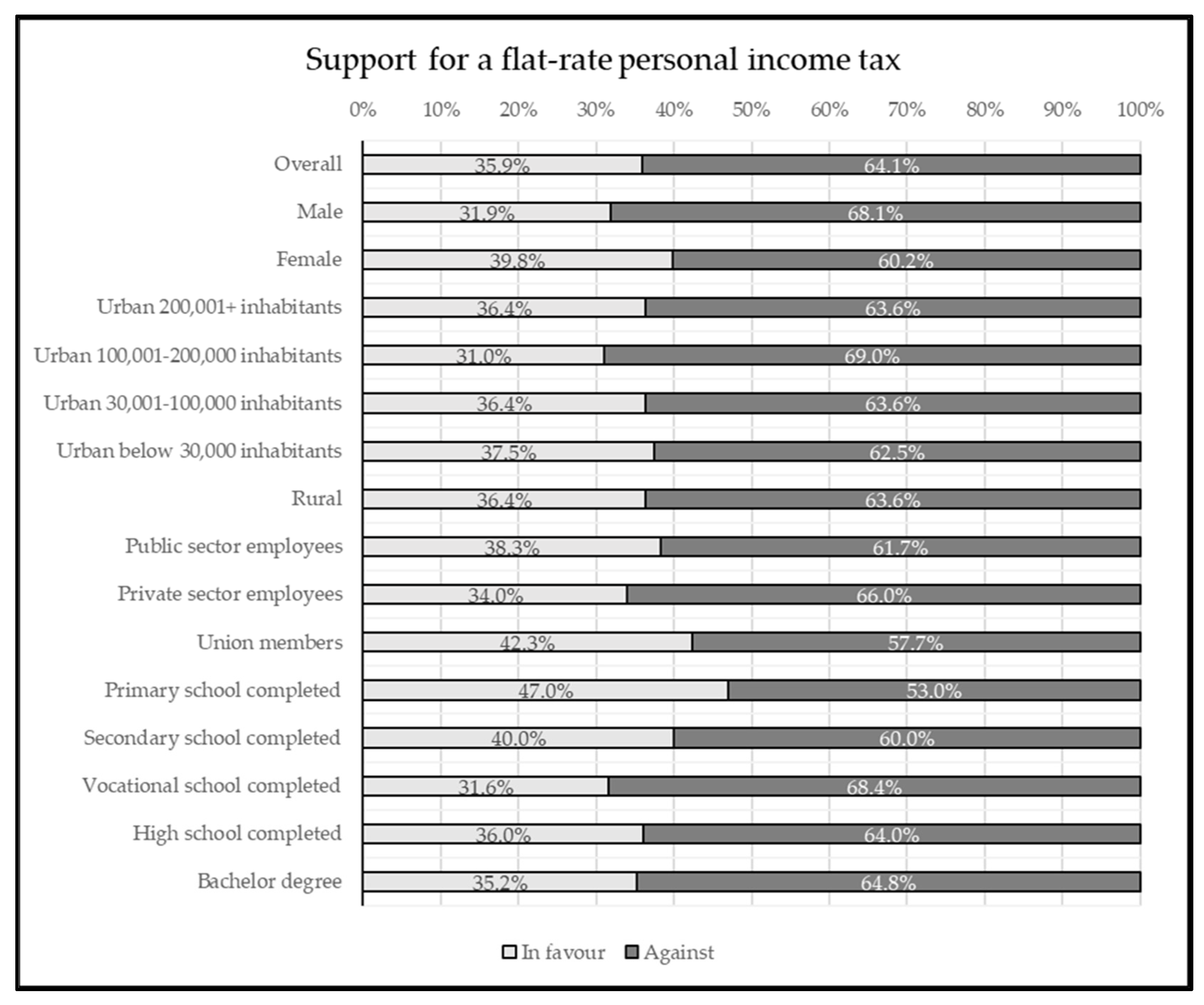

Political discourse often assumes the existence of a widespread support for the flat PIT within Romanian society. However, a descriptive analysis of the RES survey data collected in the aftermath of the 2008–2011 economic crisis shows that the flat tax is far less popular among the Romanian citizens than politicians might have thought. Only a third of the respondents with a valid opinion (35.9%) think people should pay the same tax rate, no matter how much they earn. Eight years after the implementation of a flat-rate PIT, and once the emotional effect of reduced tax burdens has faded, a vast majority of respondents (64.1%) have a clear preference against it. Of course, it is a long shot to say that their rejection of flat-rate PIT is a genuine proof of a large social agreement on an extensive redistributive function of the state.

Figure 1 presents the distribution of support for a flat-rate PIT across the overall sample and within various social categories. The category represented as being favourable to the flat tax includes respondents that agreed (‘fully agree’ or ‘agree’) with the statement that ‘people should pay the same tax rate, no matter how much they earn.’ These initial results suggest that the support for a flat-rate PIT is remarkably similar across different social categories, with rather small variations. Nevertheless, the preference for the flat tax is slightly higher among lower-educated respondents (47% among those having completed only primary school, 40% among those having completed secondary school) and union members (42.3%).

These preliminary findings pave the way for an in-depth analysis of the determinants of the variations in public support for the flat rate. As explained in the previous sections of this article, both socio-economic and demographic variables and attitudinal factors are explored. To this purpose, three logistic regression models explaining support for the flat-rate PIT were run. Model M1 employs only socio-economic and demographic predictors (income, education, age, and gender). Model M2 employs attitudinal and knowledge predictors (ideology, political trust, social solidarity, and political knowledge). The third one (M3) combines both categories of predictors in a single regression. The results are summarised in

Table 1.

On a primary layer of analysis, these results indicate a significant impact of several individual determinants that are compatible with the larger framework of studies dedicated to fiscal preferences in Western Europe and CEE.

Income is in a positive relation with support for the flat tax (H1 hypothesis), but its effect is borderline significant (

b coefficient is +0.285 at

p = 0.058) in the M3 combined model. Thus, high-income earners are stronger supporters of flat-rate taxes, which validates the traditional assumption that citizens tend to favour the public policies that they stand to benefit from [

54]. This result is in line with an extensive sequence of studies that put income in a negative relation with support for progressive taxation [

5,

14,

15] or in a positive relation with the preference for a flat-rate taxation [

14,

26].

Furthermore, the analysis provides evidence for the idea that higher

educational achievements tend to confine the preference for a flat tax, which suggests a relation quite opposite to the one assumed in the H3 hypothesis. Education has similar effects in both models M1 (

b = −0.050) and M3 (

b = −0.060), and ranks second in the list of determinants of tax preferences in the combined model based on the Wald statistic. Such negative effect is in contrast with the findings of both Limberg [

20] and Bădescu et al. [

24], but is not counterintuitive. Educated (thus sophisticated) people are expected to be more capable of figuring out the deeper implications of a public policy, beyond immediate self-interest. Thus, they may value more the implications of redistribution via progressive taxation for the community or society as a whole, moving from self-interest to ‘well-understood self-interest’ [

55]. Such an interpretation is largely speculative, but is in line with the arguments of Stiers et al. [

14]. However, a major obstacle for this perspective is the lack of any significant impact of

political knowledge in any of the regression models run.

Gender completes the picture of ‘traditional’ determinants of fiscal preferences relevant for the Romanian case, providing another clear-cut effect: female respondents are much stronger supporters of flat-rate taxation than men (the

b coefficient for the ‘being a male’ dummy variable is constantly negative across models, with −0.421 in M1 and −0.343 in M3). This additional appetite of women for ‘equal’ taxation may have origins in a history of gender-based inequalities. In the light of such a background perspective, stronger support for the statement that ‘people should pay the same tax rate’ comes naturally. The conclusion that women are more in favour of flat-rate taxation than men is congruent with the results of other studies [

14,

26], but the element of novelty arises from the consistent statistical significance of the gender effect.

A further discussion on the influence of

political trust is needed at this point. In the simple M2 attitudinal model, trust in government is in a positive relation with support for the flat tax (

b = +0.055). In other words, highly trusting individuals are more likely to regard a unique tax rate for all incomes as a fair solution, as assumed in the H6 hypothesis. The conclusion is in line with the empirical evidence provided by Domonkos [

5] in favour of the idea that distrust in government fosters support for progressive taxation as some sort of mechanism of compensation for the less affluent. Unfortunately, the statistical significance of political trust drops below 0.05 in the combined M3 model.

Furthermore, the analyses run on the RES data do not find any evidence that age, ideology, or political knowledge have an influence on people’s fiscal preferences in the Romanian context. Thus, the regression models provide no support for hypotheses H2 and H4.

On a secondary level of analysis, the results successfully pinpoint a new element on the map of determinants of fiscal preferences, namely

social solidarity. Increased levels of concern for the living conditions of vulnerable people (the poor and the unemployed) come with a lower likelihood of support for the flat rate (the

b coefficient is −0.043 in M2 and −0.049 in M3), which provides empirical support for the H5 hypothesis and is in line with the recent findings of Cabelkova and Smutka [

26] for the Czech Republic. In other words, being preoccupied in an altruistic manner about the life of people at risk functions as a deterrent to agreeing that ‘rich people’ and ‘poor people’ should pay the same tax rate on their incomes. The Wald statistic calculated for both M2 and M3 suggests the index of social solidarity to be the strongest determinant of tax preference for the Romanian respondents.

Social solidarity appears to be a relevant and reliable negative predictor of support for a flat-rate PIT. The implications of such a finding are extensive for the medium and perhaps long-term prospects of the flat tax. As social solidarity tends to increase during crises [

30,

56], the unfortunate sequence of several major crises in a short timespan (a financial crisis, followed by a migrant crisis, the COVID-19 pandemic, and the overlapping humanitarian, social and economic crises related to the Ukraine war) is likely to bring about significantly more pressure from below for redistribution and progressive taxation. Therefore, a further descending trend in people’s preferences for this taxation scheme is foreseeable both in Romania and in other CEE countries. It remains to be seen whether, and the degree to which, these evolutions will occur and further translate into fiscal policies.

6. Conclusions

As in most of the CEE region, the adoption of the flat tax in Romania in 2005 worked as a signal to foreign investors that the country was open for business. A different pathway at that moment in time might have turned into competitive disadvantage in relation to other CEE countries in Romania’s effort to attract foreign investments. However, the country’s bet on the flat tax was more hazardous than in the case of most countries in the region, given the choice of a tax rate (16%) lower than the bottom rate in the previous progressive system (18%). Apparently, there were no serious financial analyses or simulations made by the Popescu-Tăriceanu cabinet pointing to this level of taxation as being optimal or at least sustainable. Nonetheless, the choice of a tax rate that everyone benefited from, due to the reduced burden for all citizens, secured what seemed to be a widespread support for the fiscal revolution. At that moment, future costs of the flat tax were diffuse and hard to assess.

This article joins the debate on flat-rate PIT in Romania with a perspective focused on citizens and their short- and medium-term support for this fiscal policy. It provides solid evidence for the idea that public support for the flat tax among Romanian citizens is lower than previously anticipated and has continuously narrowed over time. Moreover, the prospects are negative, given the context of the current sequence of overlapping societal crises, with massive implications from a policy perspective.

Another contribution of this article comes from the effort to provide an explanation of what drives public support for flat-rate personal income taxation in the specific context of post-communist Romania. It finds evidence that high-income earners, female respondents, and those with higher levels of political trust are more likely to support flat-rate PIT, while higher levels of social solidarity and more education increase the chances of being reluctant about it. The element of novelty of these analyses comes from three aspects. First, there are still relatively few studies dedicated to the determinants of preferences for a flat tax in any given country. Second, very little is known about the Romanians’ fiscal preferences. Third, it clearly sets social solidarity as a central determinant of attitudes towards the flat tax in a complex multivariate explanatory model.

There are also potential limitations that come with this investigation of public opinion on flat-rate PIT in Romania. A first one is due to the scarcity of previous studies on the topic. The literature review is almost entirely focused on the determinants of preferences for progressive income taxation. In the development of the theoretical argument, flat tax and progressive taxation were regarded as opposite alternatives, a solution that allowed the mirroring of expectations. This deliberately ignored regressive taxation as a third alternative, on the basis that it had never been a topic of debate in Romania and in the region. A second limitation comes from the clearly suboptimal timing of RES survey data collection. Data were collected eight years after the adoption of the flat rate in Romania and in the final phases of a hard economic crisis, which put a particularly high emphasis on solidarity in public discourse. However, it also provided a proper framework to analyse the formation of fiscal preferences in a time of crisis.

Future research on flat tax support in Romania might focus on a wider range of possible determinants, using dedicated instruments. With survey data collected repeatedly at specific points in time, a more clear-cut perspective could be provided on medium-term or long-term trends in public opinion on flat-rate PIT and the impact of societal crises on it. Taxes should reflect the will of the citizens; therefore, regular social data on their fiscal preferences and what shapes those preferences are very much needed to properly assess the prospects of Romania for keeping the flat tax or just moving away from it.

{kind=link}