Can the Digital Economy Improve the Level of High-Quality Financial Development? Evidence from China

Abstract

:1. Introduction

- In optimizing the financial industry’s market structure, the integration of the digital economy and the financial system has created a new financial industry—digital finance. Digital finance has forced banks to undergo digital transformation. Banks will form an inclusive financial industry while providing a more transparent information disclosure mechanism for the capital market and optimizing financial market structure [13].

- In terms of improving the financial industry’s business philosophy, the high penetration rate of the digital economy blurs the boundaries between financial institutions, effectively solves the problems of information asymmetry and high transaction costs faced by banks and enterprises, and improves resource utilization efficiency [14]. Ultimately, it promotes the financial industry to shift to a greener, shared, and intelligent development approach [15,16].

- In improving the financial industry’s innovation capacity, digital resource investment will promote innovation in the financial industry by influencing information sharing and value creation [17,18]. Meanwhile, in an era where data and information are becoming companies’ central capital, companies will proactively use the digital economy for technological innovation, improving the financial industry’s ability to innovate [19].

- In order to improve the financial industry’s service level in the digital age, companies will need to enhance their products and services and improve customer satisfaction in response to the changing digital competitive environment, thus improving the financial industry’s service levels [20].

2. Methods and Data

2.1. Model Construction

2.2. Main Variables

2.2.1. Explained Variable

- Construction of the indicator system

- Measurements

2.2.2. Core Explanatory Variable

2.2.3. Control Variables

- The number of employees (ne). The efficient and high-quality services of financial institution employees can improve the level of operation and management of financial institutions and further enhance the operational efficiency and value of the financial industry [38]. The mobility of financial institution employees also affects the level of regional financial aggregation and, thus, the level of high-quality financial development, so the number of financial institution employees is used as an indicator.

- The industrial structure (is). Industrial structure is an essential factor affecting the level of financial development [39]. In this paper, the ratio of total regional output value of the financial sector to total regional output value of the tertiary sector is used to express this.

- The level of government regulation (gr). Only in countries with high governmental capacity can a low level of resistance to financial development lead to an effective increase in credit market development [40]. This paper uses fiscal spending as a share of GDP in each provincial region to reflect the local level of government regulation.

- The degree of openness (do). Establishing a pilot free trade zone can improve the efficiency of financial services to the real economy, which is essential for high-quality financial development [41]. This measurement is the presence or absence of a pilot free trade zone in each provincial-level region. That is, regions with a pilot free trade zone have a value of 1, and regions without a pilot free trade zone have a value of 0.

- The level of economic development (ep). Financial development is facilitated by increased demand for credit resulting from economic development and increased investment opportunities [42]. We choose the GDP per capita of each provincial-level region to reflect the level of economic development of each provincial-level region.

2.3. Variable Measures and Data Description

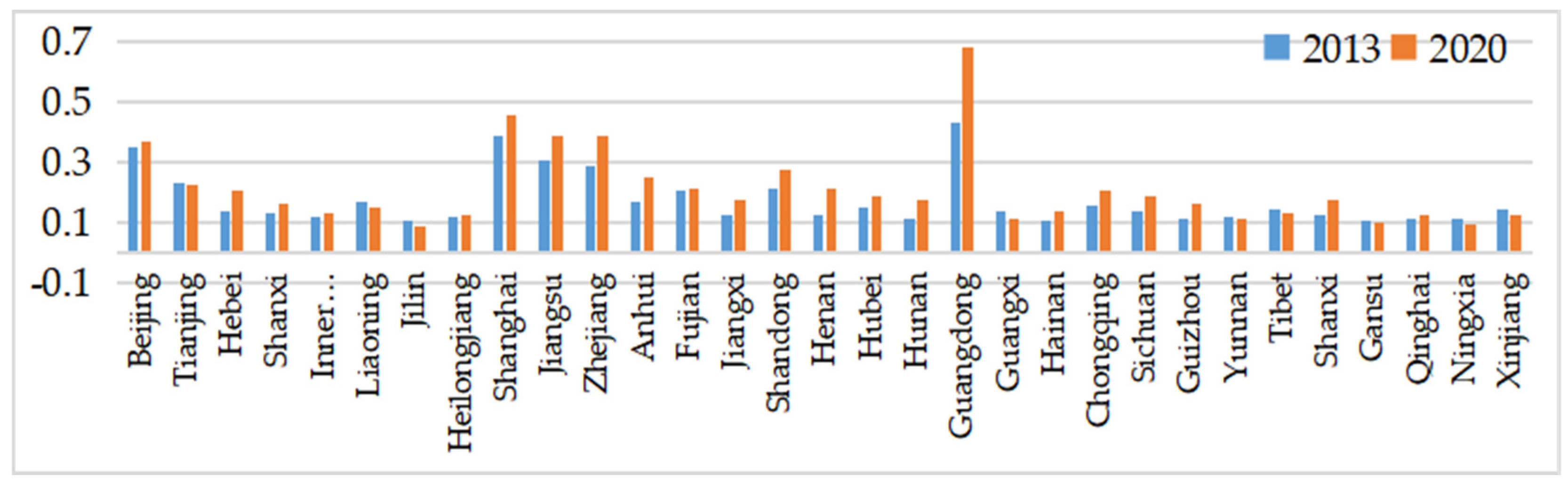

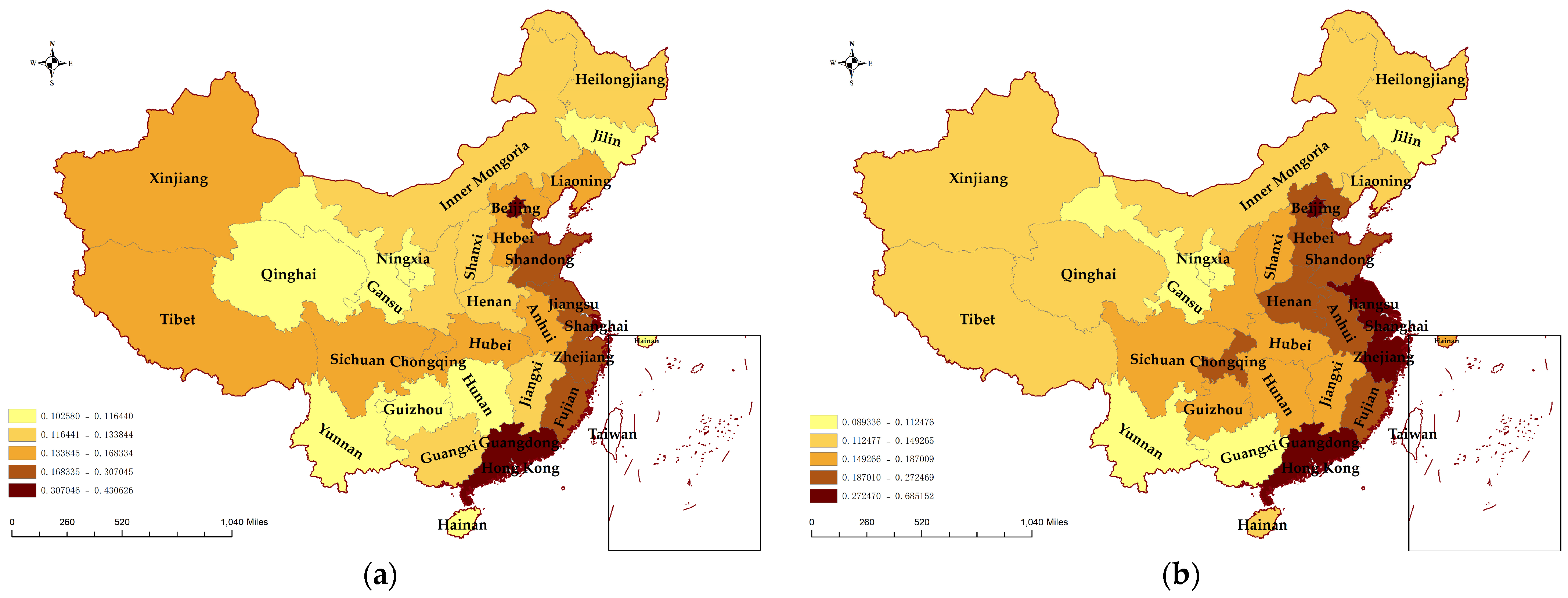

3. Analyzing the Spatial Pattern of High-Quality Financial Development

4. Empirical Results

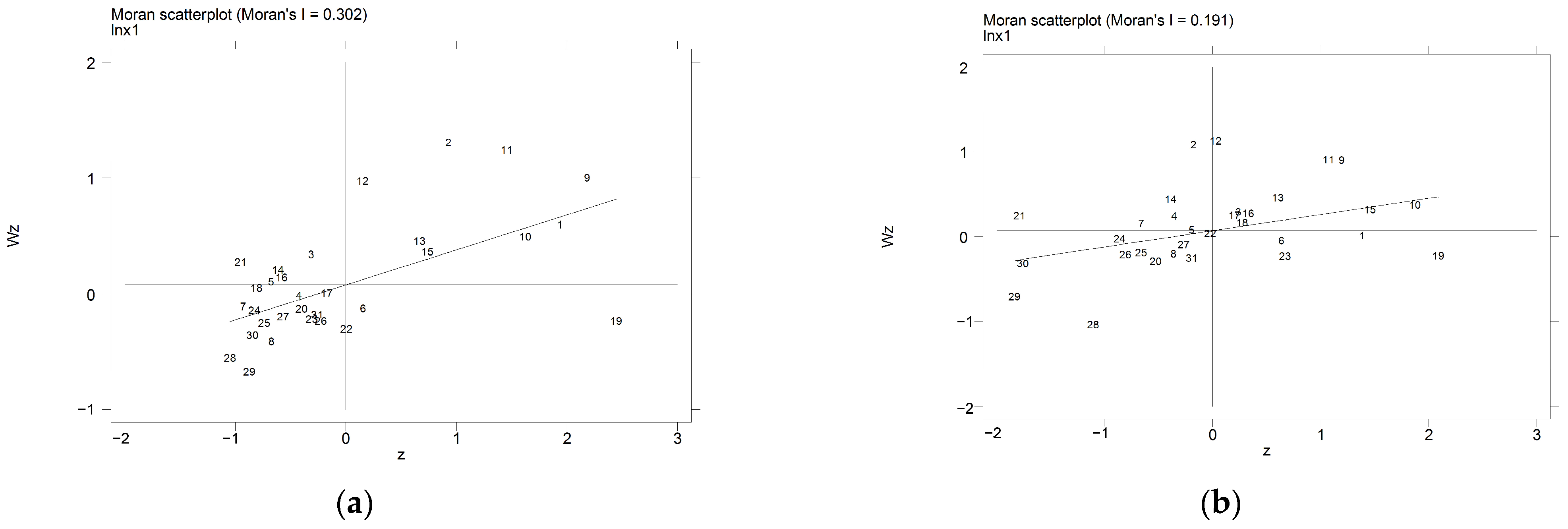

4.1. Exploratory Space Analysis

- The global autocorrelation test

- The local autocorrelation test

4.2. Model Selection

4.3. Baseline Regression Results

4.4. Decomposition of Spillover Effects

4.5. Heterogeneity Test

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Huang, X.; Binqing, C.; Yalin, L. Evaluation index system and measurement of high-quality development in China. Rev. Cercet. Interv. Soc. 2020, 68, 163. [Google Scholar] [CrossRef]

- Jin, B. Study on the “high-quality development” economics. China Ind. Econ. 2018, 1, 163–180. [Google Scholar]

- Sun, Z.; Lu, C. Xi Jinping’s Outlook on High Quality Development of the Financial Industry in the New Era. Financ. Econ. Res. 2020, 6, 3–21. [Google Scholar]

- Liu, Y.; Liu, M.; Wang, G.; Zhao, L.; An, P. Effect of environmental regulation on high-quality economic development in China—An empirical analysis based on dynamic spatial durbin model. Environ. Sci. Pollut. Res. 2021, 28, 54661–54678. [Google Scholar] [CrossRef]

- Wang, R.; Wang, F. Exploring the role of green finance and energy development towards high-quality economic development: Application of spatial Durbin model and intermediary effect model. Int. J. Environ. Res. Public Health 2022, 19, 8875. [Google Scholar] [CrossRef]

- Lu, W.; Wu, H.; Wang, L. The optimal environmental regulation policy combination for high-quality economic development based on spatial Durbin and threshold regression models. Environ. Dev. Sustain. 2022, 1–27. [Google Scholar] [CrossRef]

- Chen, S. Effect of green investment on high-quality economic development in china under the new era. Front. Econ. Manag. 2021, 2, 369–376. [Google Scholar]

- Chi, M.; Guo, Q.; Mi, L.; Wang, G.; Song, W. Spatial distribution of agricultural eco-efficiency and agriculture high-quality development in China. Land 2022, 11, 722. [Google Scholar] [CrossRef]

- Yao, W.; Sun, Z. The Impact of the Digital Economy on High-Quality Development of Agriculture: A China Case Study. Sustainability 2023, 15, 5745. [Google Scholar] [CrossRef]

- Wang, M.; Yu, D.; Chen, H.; Li, Y. Comprehensive Measurement, Spatiotemporal Evolution, and Spatial Correlation Analysis of High-Quality Development in the Manufacturing Industry. Sustainability 2022, 14, 5807. [Google Scholar] [CrossRef]

- Wu, Y.; Zhang, S. Research on the evolution of high-quality development of China’s provincial foreign trade. Sci. Program. 2022, 2022, 3102157. [Google Scholar] [CrossRef]

- Zhang, W.; Zhao, S.; Wan, X.; Yao, Y. Study on the effect of digital economy on high-quality economic development in China. PLoS ONE 2021, 16, e0257365. [Google Scholar] [CrossRef]

- Wang, W.; Zhang, Y. Financial Structure, Industrial Structure Upgrading and Economic Growth—The Perspective of Technological Progress Based on Different Characteristics. Economist 2022, 2, 118–128. [Google Scholar]

- Laguna de Paz, J.C. Some implications of the new global digital economy for financial regulation and supervision. J. Bank. Regul. 2022, 1–10. [Google Scholar] [CrossRef]

- Awan, U.; Shamim, S.; Khan, Z.; Zia, N.U.; Shariq, S.M.; Khan, M.N. Big data analytics capability and decision-making: The role of data-driven insight on circular economy performance. Technol. Forecast. Soc. Chang. 2021, 168, 120766. [Google Scholar] [CrossRef]

- Tian, X.; Zhang, Y.; Qu, G. The Impact of digital economy on the efficiency of green financial investment in China’s provinces. Int. J. Environ. Res. Public Health 2022, 19, 8884. [Google Scholar] [CrossRef]

- Chen, X.; Yan, D.; Chen, W. Can the digital economy promote FinTech development? Growth Chang. 2022, 53, 221–247. [Google Scholar] [CrossRef]

- Wang, J.; Xie, Z.; Li, J.; Yang, D. Learning from institutional diversity to innovate: A study of Chinese exporters in digital industries. Int. J. Technol. Manag. 2021, 87, 384–411. [Google Scholar] [CrossRef]

- Vicente-Saez, R.; Gustafsson, R.; Martinez-Fuentes, C. Opening up science for a sustainable world: An expansive normative structure of open science in the digital era. Sci. Public Policy 2021, 48, 799–813. [Google Scholar] [CrossRef]

- Liu, M.; Jiang, W. Empirical Research on the Influence Mechanisms of Digital Resources Input on Service Innovation in China’s Finance Industry. Sustainability 2022, 14, 7143. [Google Scholar] [CrossRef]

- Ding, C.; Liu, C.; Zheng, C.; Li, F. Digital economy, technological innovation and high-quality economic development: Based on spatial effect and mediation effect. Sustainability 2022, 14, 216. [Google Scholar] [CrossRef]

- Shen, W.; Xia, W.; Li, S. Dynamic coupling trajectory and spatial-temporal characteristics of high-quality economic development and the digital economy. Sustainability 2022, 14, 4543. [Google Scholar] [CrossRef]

- Tang, L.; Lu, B.; Tian, T. Spatial correlation network and regional differences for the development of digital economy in China. Entropy 2021, 23, 1575. [Google Scholar] [CrossRef] [PubMed]

- Chang, X.; Li, J. Effects of the Digital Economy on Carbon Emissions in China: A Spatial Durbin Econometric Analysis. Sustainability 2022, 14, 16624. [Google Scholar] [CrossRef]

- Wang, J.; Luo, X.; Zhu, J. Does the digital economy contribute to carbon emissions reduction? A city-level spatial analysis in China. Chin. J. Popul. Resour. Environ. 2022, 20, 105–114. [Google Scholar] [CrossRef]

- Zhang, W.; Liu, X.; Wang, D.; Zhou, J. Digital economy and carbon emission performance: Evidence at China’s city level. Energy Policy 2022, 165, 112927. [Google Scholar] [CrossRef]

- Yi, M.; Liu, Y.; Sheng, M.S.; Wen, L. Effects of digital economy on carbon emission reduction: New evidence from China. Energy Policy 2022, 171, 113271. [Google Scholar] [CrossRef]

- Zhao, S.; Peng, D.; Wen, H.; Song, H.J.S. Does the digital economy promote upgrading the industrial structure of Chinese cities? Sustainability 2022, 14, 10235. [Google Scholar] [CrossRef]

- Guan, H.; Guo, B.; Zhang, J.J.S. Study on the impact of the digital economy on the upgrading of industrial structures—Empirical analysis based on cities in China. Sustainability 2022, 14, 11378. [Google Scholar] [CrossRef]

- Gao, Y.; Xu, Y.; Ji, C.; Zhong, Y. The Measurement and Characteristics of China’s Financial Industry High-quality Development. J. Quant. Tech. Econ. 2020, 10, 63–82. [Google Scholar]

- Elhorst, J.P. Spatial Econometrics: From Cross-Sectional Data to Spatial Panels; Springer: Berlin/Heidelberg, Germany, 2014; Volume 479. [Google Scholar]

- Liu, J. Research on the Evaluation of High-Quality Financial Development in The Yangtze River Economic Belt. Master’s Thesis, Chongqing Technology and Business University, Chongqing, China, 2020. [Google Scholar]

- Stavytskyy, A.; Kharlamova, G.; Stoica, E.A. The analysis of the digital economy and society index in the EU. TalTech J. Eur. Stud. 2019, 9, 245–261. [Google Scholar] [CrossRef]

- Sidorov, A.; Senchenko, P. Regional digital economy: Assessment of development levels. Mathematics 2020, 8, 2143. [Google Scholar] [CrossRef]

- Yang, S.; He, J. Analysis of Digital Economy Development Based on AHP-Entropy Weight Method. J. Sens. 2022, 2022, 7642682. [Google Scholar] [CrossRef]

- Li, K.; Kim, D.J.; Lang, K.R.; Kauffman, R.J.; Naldi, M. How should we understand the digital economy in Asia? Critical assessment and research agenda. Electron. Commer. Res. Appl. 2020, 44, 101004. [Google Scholar] [CrossRef]

- Li, Z.; Liu, Y. Research on the spatial distribution pattern and influencing factors of digital economy development in China. IEEE Access 2021, 9, 63094–63106. [Google Scholar] [CrossRef]

- Athanassopoulos, A.D. Service quality and operating efficiency synergies for management control in the provision of financial services: Evidence from Greek bank branches. Eur. J. Oper. Res. 1997, 98, 300–313. [Google Scholar] [CrossRef]

- Shi, S. Mechanism Analysis of the Effects of Economic Growth on Financial Development: An Empirical Analysis Based on China’s County Data. Financ. Trade Res. 2011, 2, 107–112. [Google Scholar]

- Becerra, O.; Cavallo, E.; Scartascini, C. The politics of financial development: The role of interest groups and government capabilities. J. Bank. Financ. 2012, 36, 626–643. [Google Scholar] [CrossRef]

- Wang, L.; Liu, Z.; Shi, H. The Impact of the Pilot Free Trade Zone on Regional Financial Development. China World Econ. 2022, 30, 154–184. [Google Scholar] [CrossRef]

- Santoli, S. The Theory of Economic Development. An Inquiry into Profits, Capital, Credit, Interest and the Business Cycle; JSTOR: New York, NY, USA, 1964. [Google Scholar]

- Akinwande, M.O.; Dikko, H.G.; Samson, A. Variance inflation factor: As a condition for the inclusion of suppressor variable (s) in regression analysis. Open J. Stat. 2015, 5, 754. [Google Scholar] [CrossRef]

- Han, F.; Sui, F. Effect of global Moran’s I and space-time permutation scanning method in Shanghai metro traffic based on ecological transportation system. Ekoloji 2019, 28, 4741–4749. [Google Scholar]

- Yin, H.; Wang, P. Transnational infection and spatial dependence of stock investor sentiment: Based on panel data from seven countries such as China and US. J. Ind. Eng. Eng. Manag. 2020, 34, 224–232. [Google Scholar]

- LeSage, J.P. An introduction to spatial econometrics. Rev. D’économie Ind. 2008, 123, 19–44. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

| Level 1 | Level 2 | Level 3 |

|---|---|---|

| Market Structure | Financial Market Size | Social financing scale increments |

| Financial Market Efficiency | The incremental social financing scale/GDP | |

| The proportion of direct financing in the total social financing scale | ||

| Year-end loan balances of financial institutions | ||

| Innovation Capacity | Financial Innovations | R&D expenditure/GDP |

| The proportion of financial funding for science and technology promotion | ||

| The ratio of total revenue and number of high-tech enterprises | ||

| Business Philosophy | Green Finance | Financial support for green development funds accounted for |

| Investment in environmental pollution control/GDP | ||

| Financial Openness | Import and export volume/GDP | |

| Service Level | Financial Information Services | Number of financial information service business units |

| Risk Prevention | Financial Risk Prevention | Non-performing loan rate of financial institutions |

| Level 1 | Level 2 | Level 3 |

|---|---|---|

| Digital Industrialization | Communications | Total telecommunications businesses |

| Cell phone penetration rate | ||

| Long-distance fiber optic cable line length | ||

| Internet broadband access ports | ||

| Express business volume | ||

| Cell phone exchange capacity | ||

| Internet and Related Services | Number of Ipv4 addresses | |

| Total number of CN domain names | ||

| Software and Information Technology Services | Software business revenue | |

| Information technology service revenue | ||

| Electronic Information Manufacturing | Revenue from main businesses | |

| Industry Digitization | Industrial Digitalization | Operating income |

| Digital Innovation | Expenditures on the introduction of technology | |

| Expenditures on technical transformation | ||

| Digital Governance | E-commerce Development Level | E-commerce procurement volume |

| The proportion of enterprises using e-commerce | ||

| Number of employees in the information transmission, software and information technology services sector |

| Variable | Symbol | Obs. | Mean | Sd. | Min. | Max. |

|---|---|---|---|---|---|---|

| The level of high-quality financial development | lnHQF | 248 | −1.803 | 0.478 | −2.836 | −0.378 |

| The digital economy | lnDE | 248 | −2.514 | 0.810 | −4.506 | −0.278 |

| The number of employees | lnne | 248 | 2.786 | 0.903 | −0.108 | 4.557 |

| The industrial structure | lnis | 248 | −1.952 | 0.238 | −2.723 | −1.343 |

| The level of government regulation | lngr | 248 | −1.384 | 0.471 | −2.13 | 0.321 |

| The degree of openness | do | 248 | 10.899 | 0.412 | 10.05 | 12.013 |

| The level of economic development | lnep | 248 | −1.803 | 0.478 | −2.836 | −0.378 |

| Unstandardized Coefficients | Standardized Coefficients | Collinearity Statistics | ||||||

|---|---|---|---|---|---|---|---|---|

| Model | B | Std. Error | Beta | t | Sig. | Tolerance | VIF | |

| 1 | (Constant) | 0.001 | 0.014 | 0.061 | 0.951 | |||

| lnDE | 0.487 | 0.052 | 0.510 | 9.413 | 0.000 | 0.224 | 4.468 | |

| lnne | 0.002 | 0.000 | 0.251 | 4.621 | 0.000 | 0.223 | 4.493 | |

| lnis | 0.278 | 0.095 | 0.092 | 2.941 | 0.004 | 0.670 | 1.492 | |

| lngr | 0.006 | 0.016 | 0.012 | 0.394 | 0.694 | 0.670 | 1.492 | |

| do | 0.000 | 0.007 | −0.002 | −0.055 | 0.956 | 0.757 | 1.321 | |

| lnep | 8.278 × 10−7 | 0.000 | 0.214 | 5.184 | 0.000 | 0.384 | 2.602 | |

| Year | lnDE | p-Value | LnHQF | p-Value |

|---|---|---|---|---|

| 2013 | 0.210 | 0.044 | 0.490 | 0.000 |

| 2014 | 0.229 | 0.033 | 0.537 | 0.000 |

| 2015 | 0.178 | 0.070 | 0.519 | 0.000 |

| 2016 | 0.203 | 0.049 | 0.496 | 0.000 |

| 2017 | 0.205 | 0.049 | 0.520 | 0.000 |

| 2018 | 0.477 | 0.000 | 0.470 | 0.000 |

| 2019 | 0.180 | 0.068 | 0.522 | 0.000 |

| 2020 | 0.390 | 0.002 | 0.435 | 0.001 |

| Value | p-Value | |

|---|---|---|

| LMlag | 40.836 *** | (0.000) |

| Robust LMlag | 20.489 *** | (0.000) |

| LMerror | 20.764 *** | (0.000) |

| Robust LMerror | 0.418 | (0.518) |

| Hausman test | 28.15 *** | |

| LR_spatial_lag | 26.75 *** | |

| LR_spatial_error | 35.71 *** | |

| Variables | Main Effects | Spatial Effects (Wx) |

|---|---|---|

| lnDE | 0.219 *** | 0.239 ** |

| (0.00) | (0.01) | |

| lnen | 0.136 *** | −0.328 *** |

| (0.00) | (0.00) | |

| lnis | 0.161 ** | 0.111 |

| (0.01) | (0.58) | |

| lngr | 0.188 *** | −0.545 *** |

| (0.00) | (0.01) | |

| do | 0.069 * | 0.077 |

| (0.07) | (0.46) | |

| lnep | 0.462 *** | −0.398 *** |

| (0.00) | (0.00) | |

| rho | 0.336 *** | |

| (0.00) | ||

| Observations | 248 | |

| R-squared | 0.765 | |

| Number of code | 31 | |

| Variables | Direct Effect | Spatial Spillover Effect | Total Effect |

|---|---|---|---|

| lnDE | 0.239 *** | 0.449 *** | 0.688 *** |

| (0.00) | (0.00) | (0.00) | |

| lnne | 0.117 *** | −0.413 *** | −0.296 ** |

| (0.00) | (0.00) | (0.03) | |

| lnis | 0.179 *** | 0.255 | 0.433 |

| (0.00) | (0.36) | (0.14) | |

| lngr | 0.154 ** | −0.704 ** | −0.550 |

| (0.02) | (0.02) | (0.10) | |

| do | 0.074 ** | 0.138 | 0.212 |

| (0.05) | (0.38) | (0.23) | |

| lnep | 0.446 *** | −0.349 * | 0.096 |

| (0.00) | (0.06) | (0.62) |

| Variables | Eastern Regions | Central and Western Regions | ||||

|---|---|---|---|---|---|---|

| Direct Effect | Spatial Spillover Effect | Total Effect | Direct Effect | Spatial Spillover Effect | Total Effect | |

| lnDE | 0.212 *** | 0.408 *** | 0.620 *** | −0.056 | −0.100 | −0.156 |

| (0.00) | (0.01) | (0.00) | (0.22) | (0.48) | (0.36) | |

| Controls | Yes | Yes | Yes | Yes | Yes | Yes |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Zhou, H.; Li, X.; Li, X. Can the Digital Economy Improve the Level of High-Quality Financial Development? Evidence from China. Sustainability 2023, 15, 7451. https://doi.org/10.3390/su15097451

Zhou H, Li X, Li X. Can the Digital Economy Improve the Level of High-Quality Financial Development? Evidence from China. Sustainability. 2023; 15(9):7451. https://doi.org/10.3390/su15097451

Chicago/Turabian StyleZhou, Hao, Xinyi Li, and Xiaoli Li. 2023. "Can the Digital Economy Improve the Level of High-Quality Financial Development? Evidence from China" Sustainability 15, no. 9: 7451. https://doi.org/10.3390/su15097451