Accounting for ‘ESG’ under Disruptions: A Systematic Literature Network Analysis

Abstract

:1. Introduction

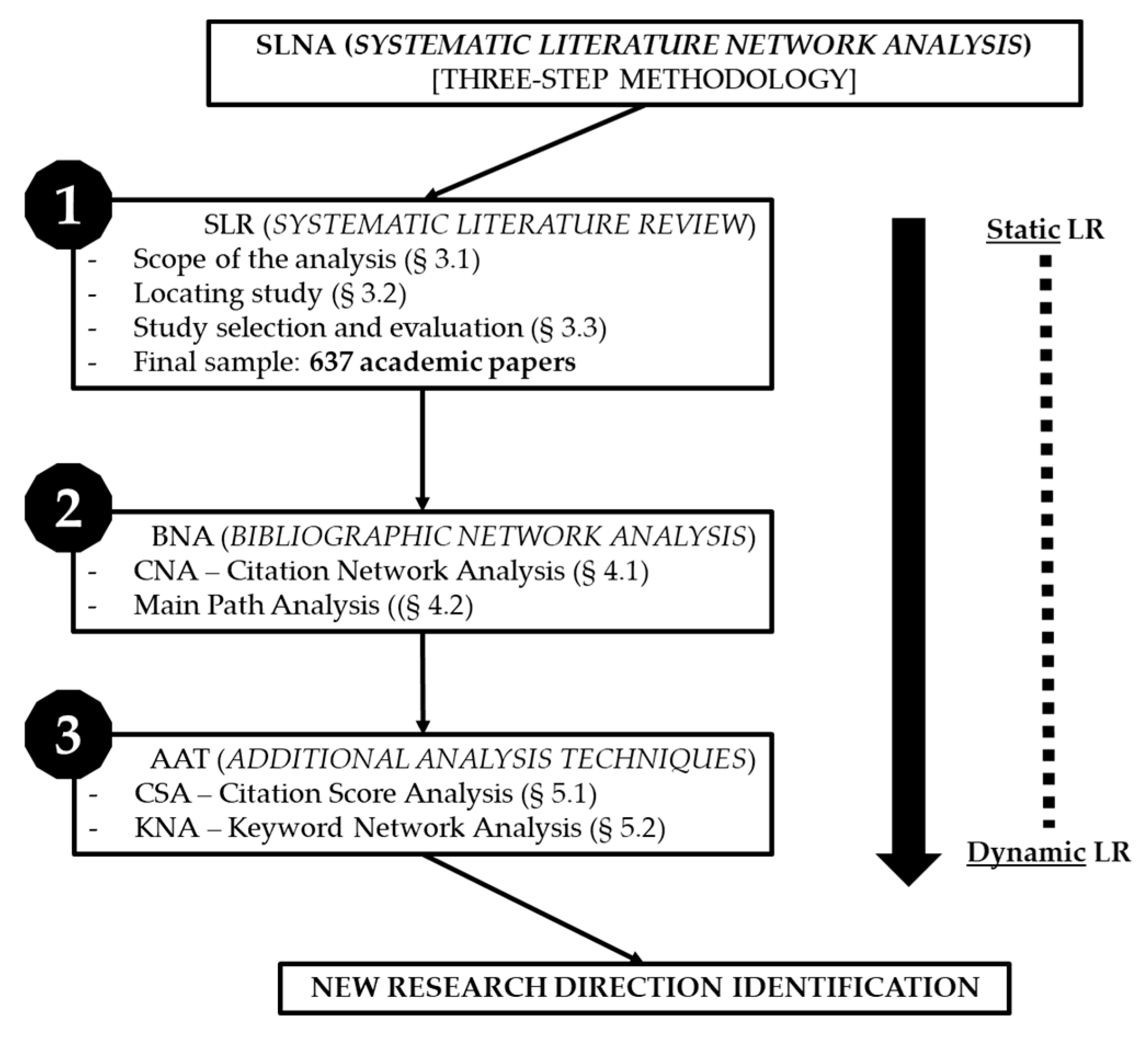

2. Methodology

- SLR—Systematic Literature Review: the first step regards the determination of the scope and boundaries of the extant literature, selecting, evaluating and isolating the most relevant articles to be used for the mentioned purposes. In essence, locating studies by means of keywords, time, type of documents and language is the first activity carried out. Locating studies through this procedure allows the researcher to extract the necessary data more objectively than would be the case with other review methodologies, in line with its principles of inclusivity, transparency, explanatory and heuristic nature;

- BNA—Bibliographic Network Analysis: the second step begins once the papers have been selected via the previous step, and it is characterised by analyses on citation network(s). In fact, citation network analysis (CNA) agglomerates the selected articles in clusters on the basis of their content, highlighting those that have contributed the most to the development of the research field. Based on the assumption that research works belonging to the same field cite one another, the citation flows resulting from the CNA are then partitioned into ‘paths’, among which the main path is identified. The latter would essentially constitute the backbone of the research tradition, and its constituent papers can be considered as the main reference points for possible trends in recent research [20];

- AAT—Additional Analysis Techniques: the third step can be separated into two further phases, which are:I. CSA—Citation Score Analysis: this identifies those seminal articles—not located in the above-mentioned citation network—that have also had a large chronological number of citations in Scopus;II. KNA—Keyword Network Analysis: based on the identification of co-occurrences among author-chosen keywords (that might, as a result, represent an appropriate proxy of the underlying research themes), this provides evidence with potential patterns and trends in the research field under analysis.

- –

- VOSviewer: this software allows a preliminary test to be carried out via network visualization and the co-occurrence keyword network analysis. It is also used to create the input file for Pajek;

- –

- Pajek: this program is necessary for conducting a social network analysis on the various citation networks in order to extract the main path(s) in research;

- –

- Sci2 Tool: this modular toolset allows temporal, geospatial, topical and network analysis to be performed, and was specifically applied in this study for the computation of the burst detection algorithm (whose utility will be explained in the related section);

- –

- GIMP: this software is used in combination with the previous one in order to better visualize the results;

- –

- Scopus analytics: a specific section of Scopus database, which also allows us to execute preliminary tests on the selected paper sample as well as to corroborate, integrate or confute results deriving from the application of the other above-mentioned tools.

3. First Step of SLNA Application: Systematic Literature Review (SLR)

3.1. Scope of the Analysis

3.2. Locating Study

- –

- Crisis OR pandemic OR ‘COVID-19’ OR ‘COVID-19’ OR COVID OR coronavirus OR ‘disruptive event’ OR ‘disruptive events’ OR disruptive OR disruption;

- –

- Accounting OR reporting OR disclosure;

- –

- Esg OR ‘non-financial’ OR ‘non financial’ OR ‘nonfinancial’ OR sustainability.

3.3. Study Selection and Evaluation

- –

- Studies published in a language other than English can be excluded (which, in this case, equalled 23);

- –

- The type of academic paper can be targeted: for instance, limiting the search to ‘articles’, ‘books’ and ‘reviews’ could be more appropriate in that they clearly contain citations, allowing for the achievement of ideal results (in so doing, another six documents were excluded);

- –

- The major research areas are reported. Hence, after having carefully assessed their pertinence to the research focus, the following might generally be included (for studies pertaining to accounting): ‘business, management and accounting’, ‘social sciences’ and ‘economics, econometrics and finance’ (this filter led to 114 documents being excluded).

4. Second Step of SLNA Application: Bibliographic Network Analysis (BNA)

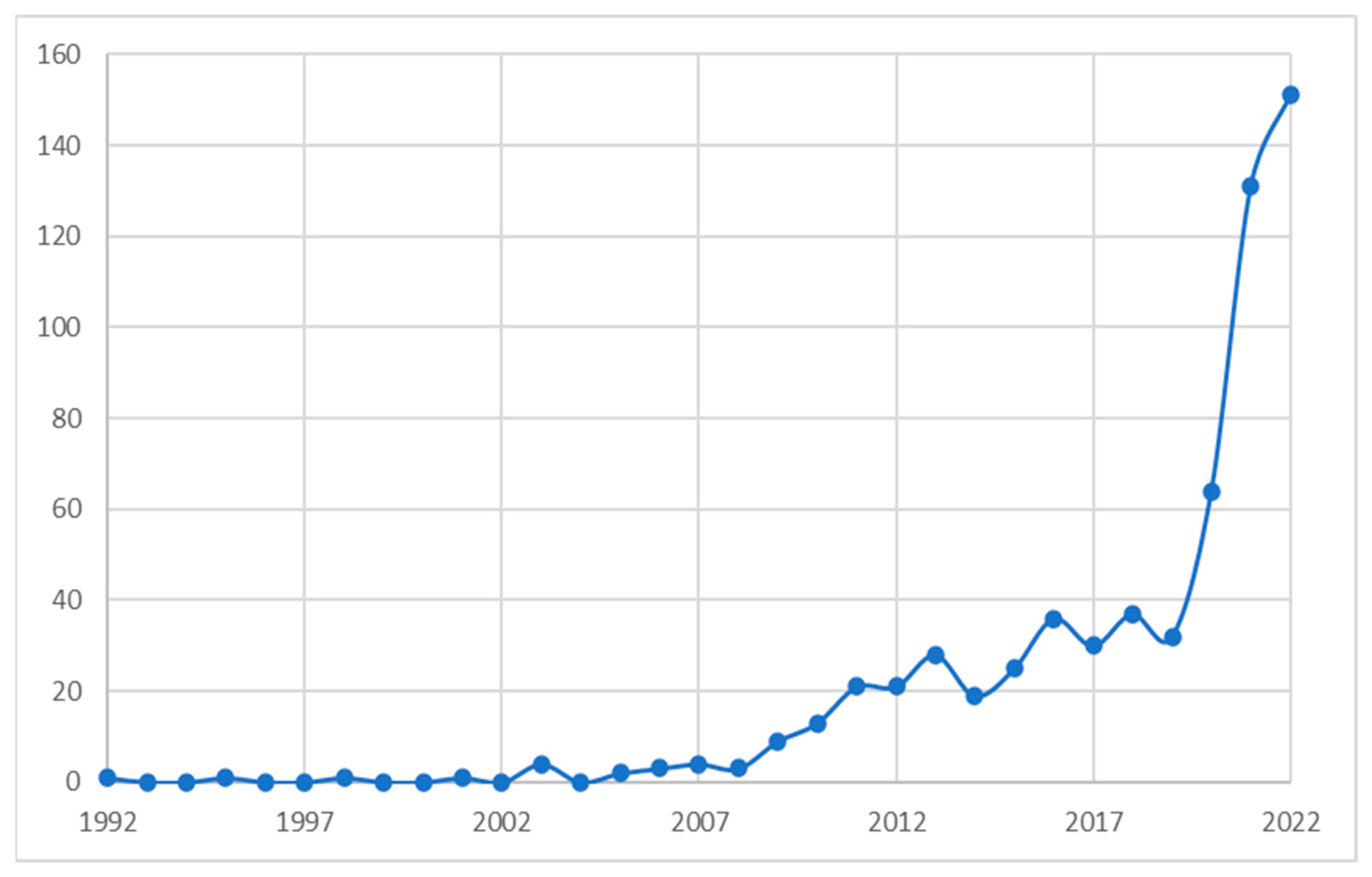

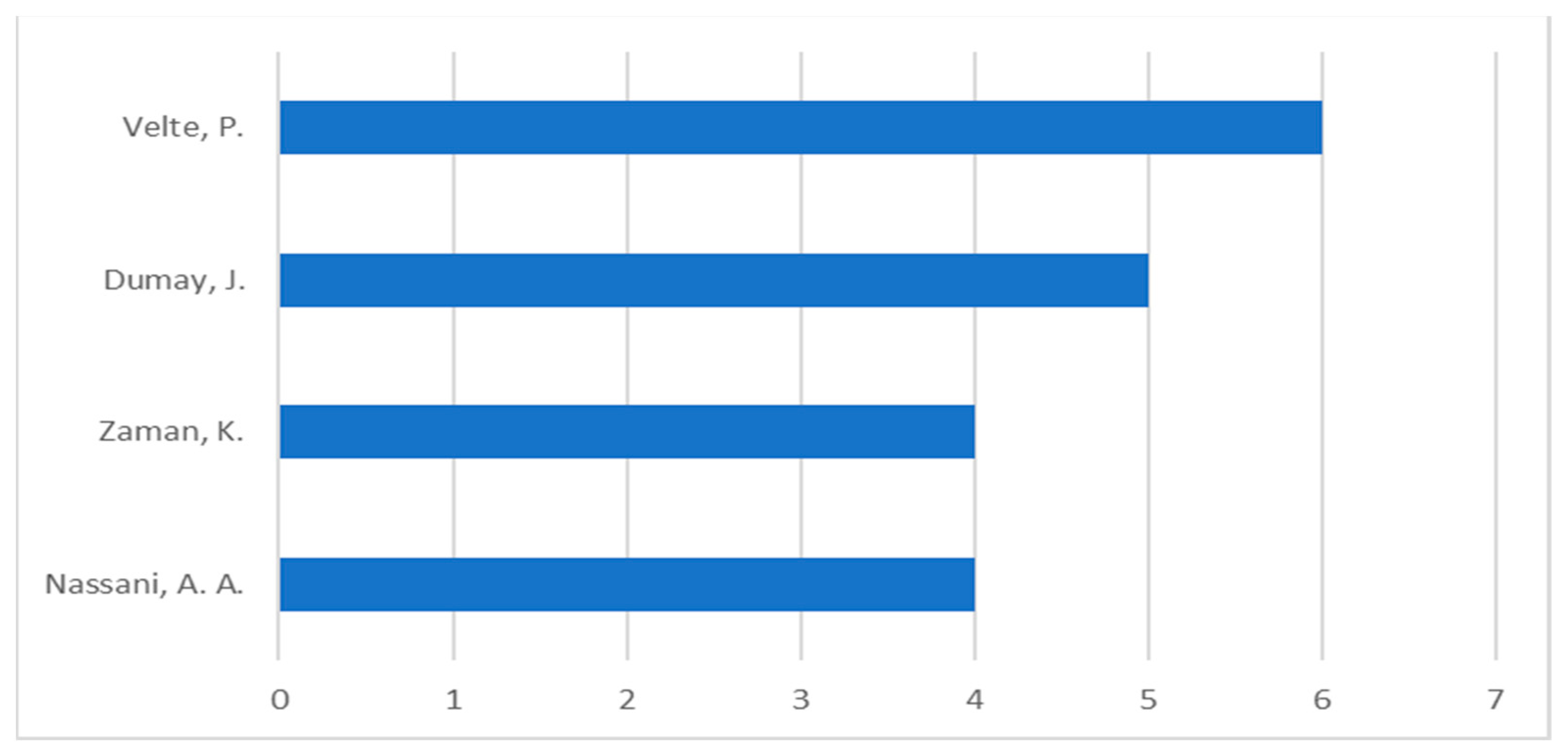

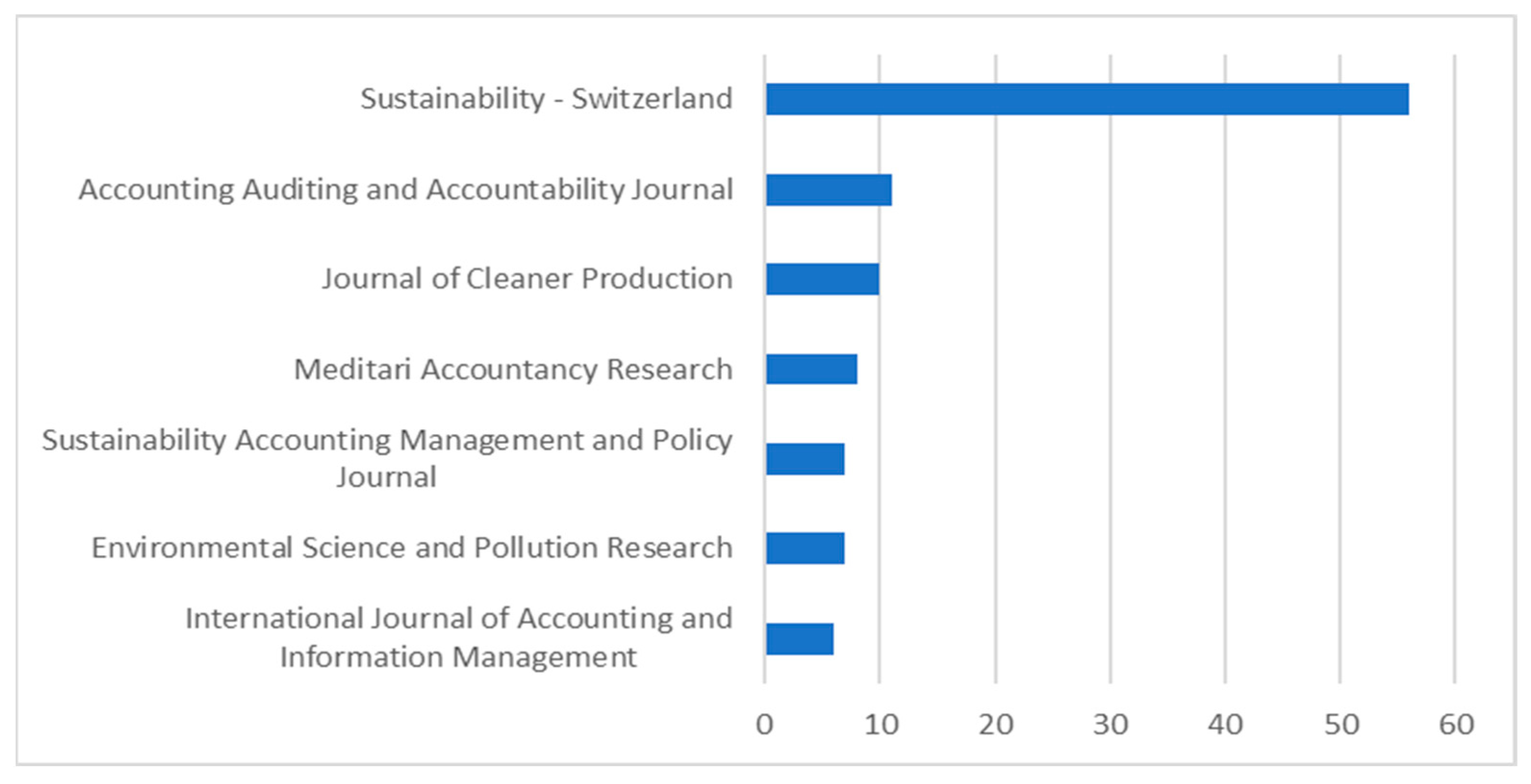

4.1. Sample Description and Static Analysis

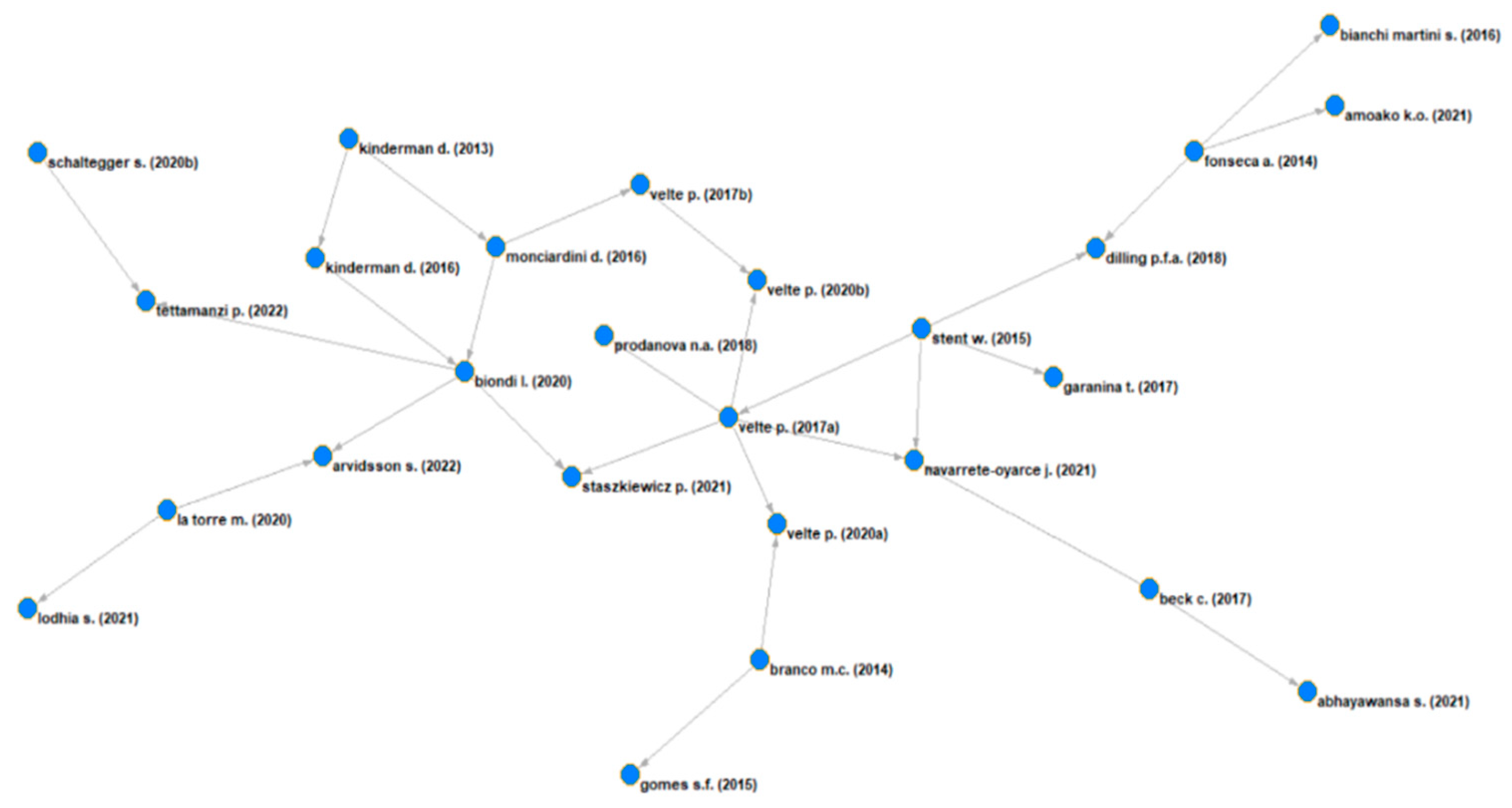

4.2. Dynamic Analysis, Main Path Identification and Study Discussion

- –

- The history of CSR in EU [41];

- –

- Sustainability in the mining sector [23];

- –

- Voluntary and regulatory measures in CSR private governance [42];

- –

- <IR> problems and compliance with EU Directives on non-financial and diversity disclosure [43];

- –

- Pandemic and accounting for non-financial issues [46];

- –

- EFRAG and International Financial Reporting Standards (IFRS) Foundation activities pertaining to sustainability disclosure [44].

5. Third Step of SLNA Application: Additional Analysis Techniques (AAT)

5.1. Citation Score Analysis (CSA)

5.1.1. Main Path Content Integration and CSA ‘New’ Topical Research Areas

5.1.2. Remarks on CSA Results

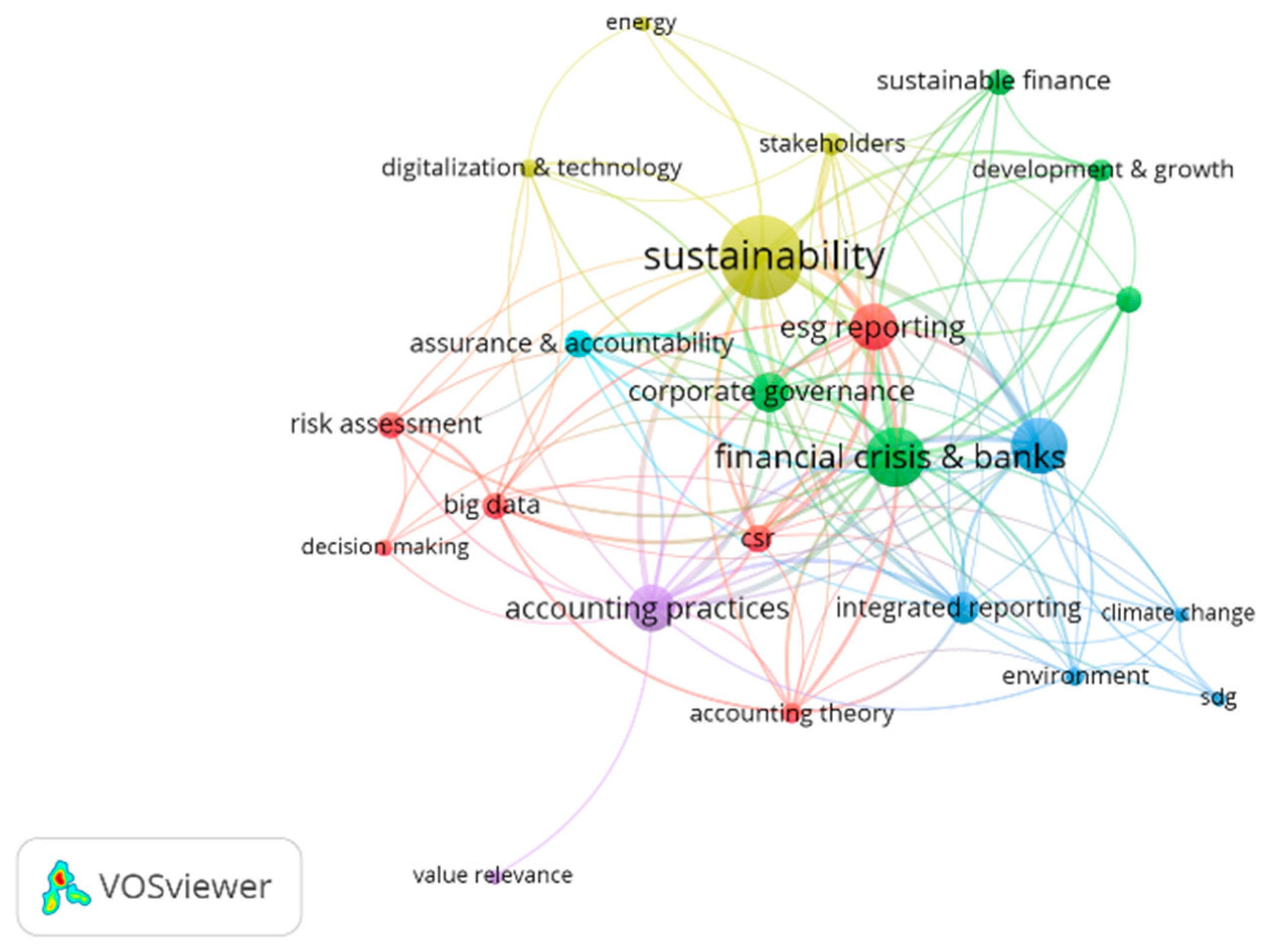

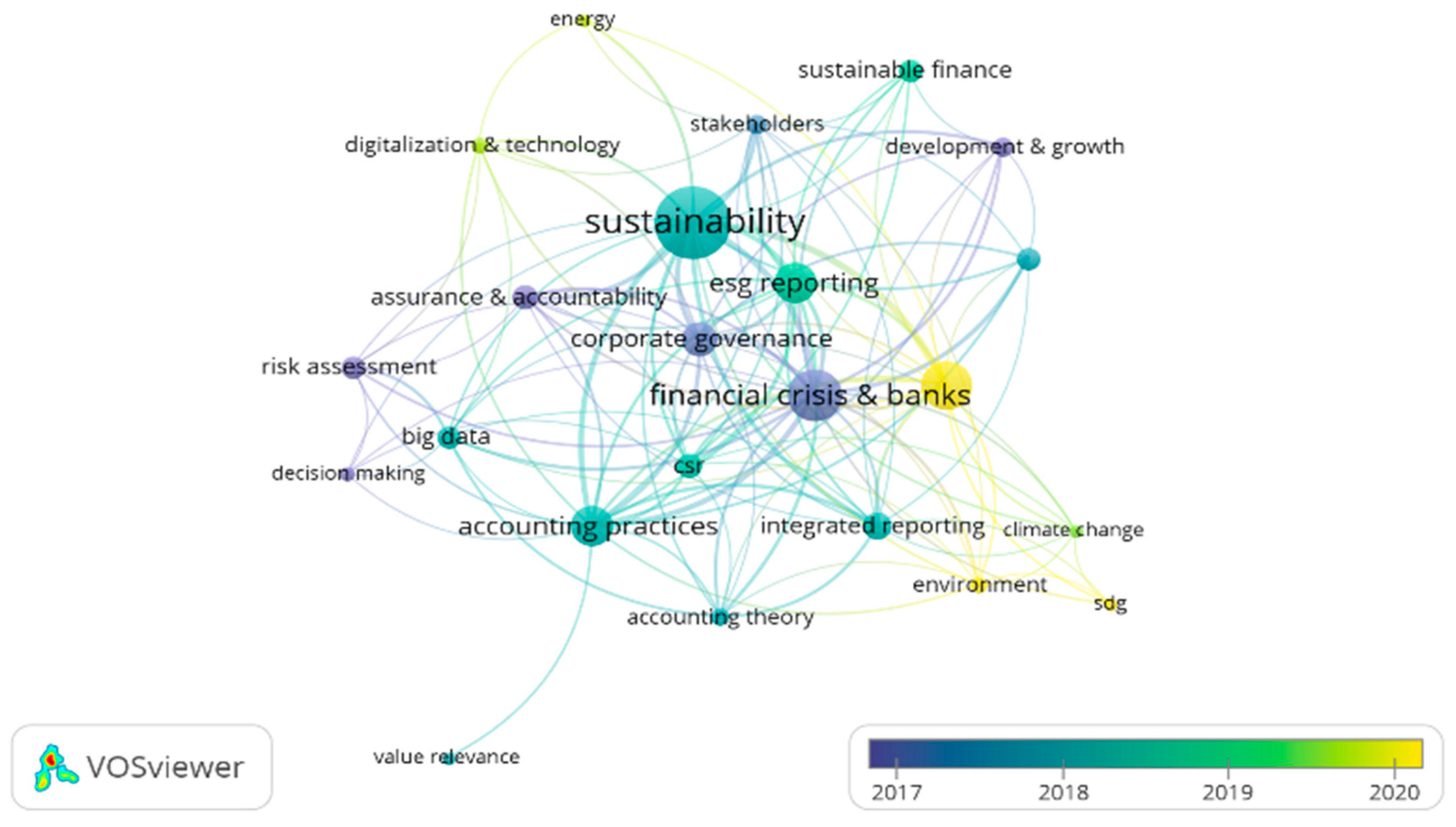

5.2. Keyword Network Analysis (KNA)

5.2.1. Co-Occurrence Analysis of Authors’ Keywords

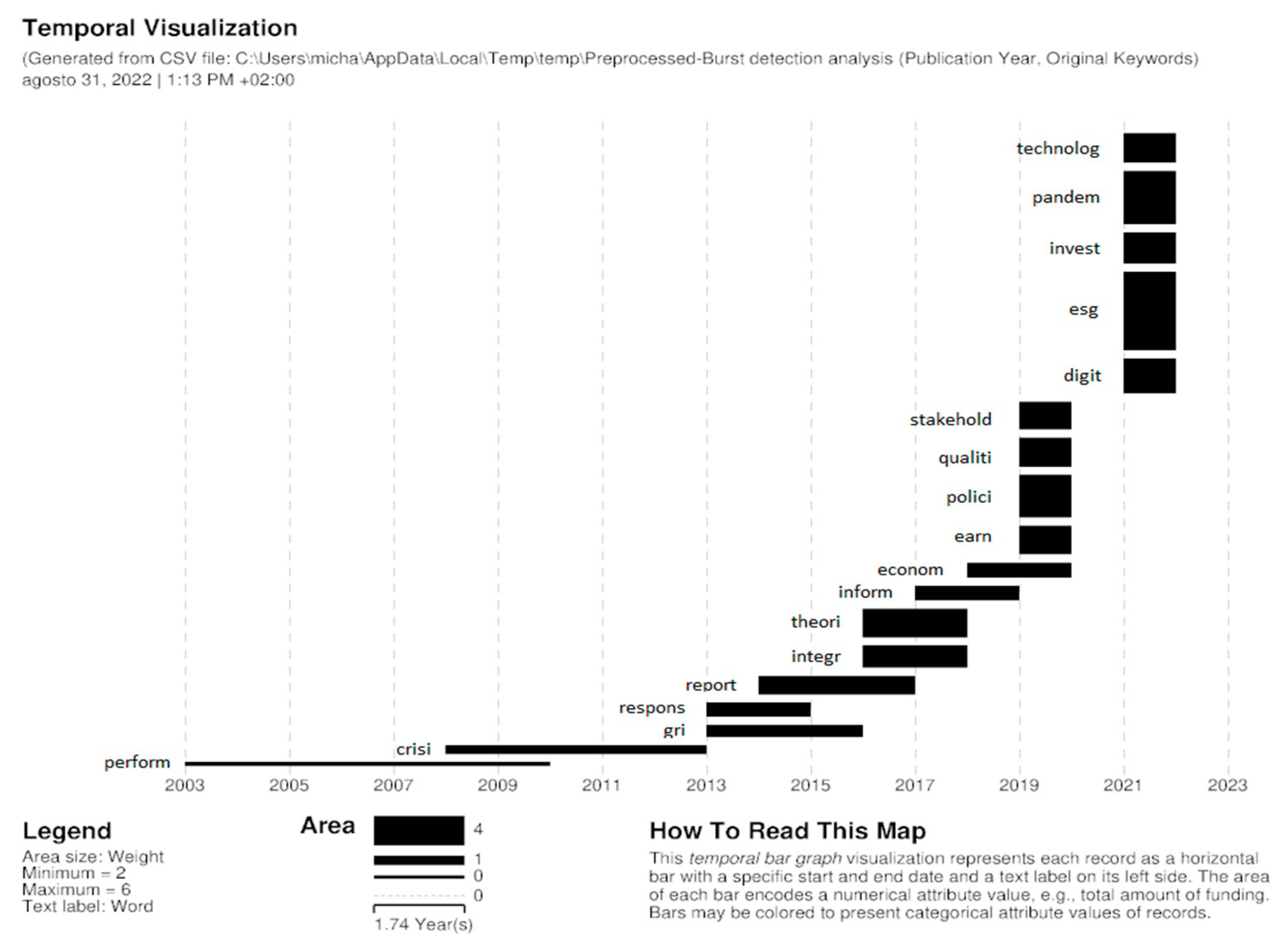

5.2.2. Kleinberg’s Burst Detection Algorithm

6. Identifying New Research Directions

7. Discussion and Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Arvidsson, S.; Dumay, J. Corporate ESG reporting quantity, quality and performance: Where to now for environmental policy and practice? Bus. Strategy Environ. 2022, 31, 1091–1110. [Google Scholar] [CrossRef]

- Bigoni, M.; Mohammed, S. Critique is unsustainable: A polemic. Crit. Perspect. Account. 2023, 102555. [Google Scholar] [CrossRef]

- Saxena, A.; Singh, R.; Gehlot, A.; Akram, S.; Twala, B.; Singh, A.; Montero, E.; Priyadarshi, N. Technologies Empowered Environmental, Social and Governance (ESG): An Industry 4.0 Landscape. Sustainability 2023, 15, 309. [Google Scholar] [CrossRef]

- García-Sánchez, I.-M.; Raimo, N.; Amor-Esteban, V.; Vitolla, F. Board committees and non-financial information assurance services. J. Manag. Gov. 2021, 27, 1–42. [Google Scholar] [CrossRef]

- Tregidga, H.; Laine, M. On crisis and emergency: Is it time to rethink long-term environmental accounting? Crit. Perspect. Account. 2022, 82, 102311. [Google Scholar] [CrossRef]

- Schaltegger, S. Unsustainability as a key source of epi- and pandemics: Conclusions for sustainability and ecosystems accounting. J. Account. Organ. Change 2020, 16, 613–619. [Google Scholar] [CrossRef]

- Pekar, J.; Magee, A.; Prker, E.; Moshiri, N.; Izhikevich, K.; Havens, J.; Gangavarapu, K.; Serrano, L.; Crits-Christoph, A.; Matteson, N.; et al. The molecular epidemiology of multiple zoonotic origins of SARS-CoV-2. Science 2022, 377, 960–966. [Google Scholar] [CrossRef]

- Worobey, M.; Levy, J.I.; Serrano, L.M.; Crits-Christoph, A.; Pekar, J.E.; Goldstein, S.A.; Rasmussen, A.L.; Kraemer, M.U.G.; Newman, C.; Koopmans, M.P.G.; et al. The Huanan Seafood Wholesale Market in Wuhan was the early epicenter of the COVID-19 pandemic. Science 2022, 377, 951–959. [Google Scholar] [CrossRef]

- Rüger, M.; Maertens, S.U. The Content Scope of Airline Sustainability Reporting According to the GRI Standards—An Assessment for Europe’s Five Largest Airline Groups. Adm. Sci. 2022, 13, 10. [Google Scholar] [CrossRef]

- Vinnari, E.; Vinnari, M. Making the invisibles visible: Including animals in sustainability (and) accounting. Crit. Perspect. Account. 2022, 82, 102324. [Google Scholar] [CrossRef]

- Jayasuriya, D.D.; Sims, A. From the abacus to enterprise resource planning: Is blockchain the next big accounting tool? Account. Audit. Account. J. 2023, 36, 24–62. [Google Scholar] [CrossRef]

- Molinari, M.; de Villiers, C. Qualitative Accounting Research in the Time of COVID-19 Changes, Challenges and Opportunities. Pac. Account. Rev. 2021, 33, 568–577. [Google Scholar] [CrossRef]

- Colicchia, C.; Strozzi, F. Supply chain risk management: A new methodology for a systematic literature review. Supply Chain Manag. Int. J. 2012, 17, 403–418. [Google Scholar] [CrossRef]

- Massaro, M.; Dumay, J.; Guthrie, J. On the shoulders of giants: Undertaking a structured literature review in accounting. Account. Audit. Account. J. 2016, 29, 767–801. [Google Scholar] [CrossRef]

- Dawson, S.; Gasevi, C.; Siemens, G.; Joksimovic, S. Current State and Future Trends: A Citation Network Analysis of the Learning Analytics Field. In Proceedings of the Fourth International Conference on Learning Analytics and Knowledge; Association For Computing Machinery: New York, NY, USA, 2014; pp. 231–240. [Google Scholar]

- Strozzi, F.; Colicchia, C.; Creazza, A.; Noè, C. Literature Review on the ‘Smart Factory’ Concept Using Bibliometric Tools. Int. J. Prod. Res. 2017, 55, 6572–6591. [Google Scholar] [CrossRef]

- Afeltra, G.; Alerasoul, A.; Usman, B. Board of Directors and Corporate Social Reporting: A Systematic Literature Network Analysis. Account. Eur. 2021, 19, 48–77. [Google Scholar] [CrossRef]

- Zhao, D.; Strotmann, A. Analysis and Visualization of Citation Networks. Synth. Lect. Inf. Concepts Retr. Serv. 2015, 7, 1–207. [Google Scholar] [CrossRef]

- Kim, S.; Colicchia, C.; Menachof, D. Ethical Sourcing: An Analysis of the Literature and Implications for Future Research. J. Bus. Ethics 2018, 152, 1033–1052. [Google Scholar] [CrossRef] [Green Version]

- De Nooy, W.; Mrvar, A.; Batagelj, V. Exploratory Social Network Analysis with Pajek: Revised and Expanded Second Edition, Structural Analysis. In The Social Sciences; Cambridge University Press: Cambridge, UK, 2011. [Google Scholar]

- Minutiello, V.; Tettamanzi, P. The quality of nonfinancial voluntary disclosure: A systematic literature network analysis on sustainability reporting and integrated reporting. Corp. Soc. Responsib. Environ. Manag. 2021, 29, 1–18. [Google Scholar] [CrossRef]

- Hummon, N.P.; Doreian, P. Connectivity in a Citation Network: The Development of DNA Theory. Soc. Netw. 1989, 11, 39–63. [Google Scholar] [CrossRef]

- Fonseca, A.; McAllister, M.L.; Fitzpatrick, P. Sustainability reporting among mining corporations: A constructive critique of the GRI approach. J. Clean. Prod. 2014, 84, 70–83. [Google Scholar] [CrossRef]

- Bianchi Martini, S.; Corvino, A.; Doni, F. Investigating the respect of human rights within CSR reporting. Evidence from the European oil and gas sector. Int. J. Bus. Res. 2016, 16, 135–151. [Google Scholar] [CrossRef]

- Amoako, K.O.; Amoako, I.O.; Tuffour, J.; Marfo, E.O. Formal and informal sustainability reporting: An insight from a mining company’s subsidiary in Ghana. J. Financ. Rep. Account. 2022, 20, 897–925. [Google Scholar] [CrossRef]

- Dilling, P.F.; Harris, P. Reporting on long-term value creation by Canadian companies: A longitudinal assessment. J. Clean. Prod. 2018, 191, 350–360. [Google Scholar] [CrossRef]

- Stent, W.; Dowler, T. Early assessments of the gap between integrated reporting and current corporate reporting. Meditari Account. Res. 2015, 23, 92–117. [Google Scholar] [CrossRef]

- Garanina, T.; Dumay, J. Forward-looking intellectual capital disclosure in IPOs: Implications for intellectual capital and integrated reporting. J. Intellect. Cap. 2016, 18, 128–148. [Google Scholar] [CrossRef]

- Navarrete-Oyarce, J.; Gallegos, J.; Moraga-Flores, H.; Gallizo, J. Integrated Reporting as an Academic Research Concept in the Area of Business. Sustainability 2021, 13, 7741. [Google Scholar] [CrossRef]

- Beck, C.; Dumay, J.; Frost, G.R. In Pursuit of a ‘Single Source of Truth’: From Threatened Legitimacy to Integrated Reporting. J. Bus. Ethics 2017, 141, 191–205. [Google Scholar] [CrossRef]

- Abhayawansa, S.; Adams, C. Towards a conceptual framework for non-financial reporting inclusive of pandemic and climate risk reporting. Meditari Account. Res. 2022, 30, 710–738. [Google Scholar] [CrossRef]

- Velte, P.; Stawinoga, M. IR: The current state of empirical research, limitations and future research implication. J. Manag. Control 2017, 28, 275–320. [Google Scholar] [CrossRef]

- Prodanova, N.; Plaskova, N.; Sitnikova, V. Corporate Reporting of the Future: On the Path towards New through the Analysis of Today. Eurasian J. Anal. Chem. 2018, 13, 296–303. [Google Scholar]

- Gomes, S.F.; Eugénio, T.C.P.; Branco, M.C. Sustainability reporting and assurance in Portugal. Corp. Gov. 2015, 15, 281–292. [Google Scholar] [CrossRef]

- Branco, M.C.; Delgado, C.; Gomes, S.F.; Eugénio, T.C.P. Factors influencing the assurance of sustainability reports in the context of the economic crisis in Portugal. Manag. Audit. J. 2014, 29, 237–252. [Google Scholar] [CrossRef]

- Velte, P. Institutional ownership, environmental, social, and governance performance and disclosure—A review on empirical quantitative research. Probl. Perspect. Manag. 2020, 18, 282–305. [Google Scholar] [CrossRef]

- Staszkiewicz, P.; Werner, A. Reporting and Disclosure of Investments in Sustainable Development. Sustainability 2021, 13, 908. [Google Scholar] [CrossRef]

- Velte, P.; Stawinoga, M. Do chief sustainability officers and CSR committees influence CSR-related outcomes? A structured literature review based on empirical-quantitative research findings. J. Manag. Control. 2020, 31, 333–377. [Google Scholar] [CrossRef]

- Velte, P. Does board composition have an impact on CSR reporting? Probl. Perspect. Manag. 2017, 15, 19–35. [Google Scholar] [CrossRef] [Green Version]

- Monciardini, D. The ‘Coalition of the Unlikely’ Driving the EU Regulatory Process of Non-Financial Reporting. Soc. Environ. Account. J. 2016, 36, 76–89. [Google Scholar] [CrossRef] [Green Version]

- Kinderman, D. Corporate Social Responsibility in the EU, 1993-2013: Institutional Ambiguity, Economic Crises, Business Legitimacy and Bureaucratic Politics. JCMS J. Common Mark. Stud. 2013, 51, 701–720. [Google Scholar] [CrossRef] [Green Version]

- Kinderman, D. Time for a reality check: Is business willing to support a smart mix of complementary regulation in private governance? Policy Soc. 2016, 35, 29–42. [Google Scholar] [CrossRef] [Green Version]

- Biondi, L.; Dumay, J.; Monciardini, D. Using the IIR framework to comply with EU directive 2014/95/EU: Can we afford another reporting facade? Meditari Account. Res. 2020, 28, 5. [Google Scholar]

- Tettamanzi, P.; Venturini, G.; Murgolo, M. Sustainability and Financial Accounting: A Critical Review on the ESG Dynamics. Environ. Sci. Pollut. Res. 2022, 29, 16758–16761. [Google Scholar] [CrossRef] [PubMed]

- La Torre, M.; Sabelfeld, S.; Blomkvist, M.; Dumay, J. Rebuilidng trust: Sustainaiblity and non-financial reporting and the EU regulation. Meditari Account. Res. 2020, 28, 701–725. [Google Scholar] [CrossRef]

- Lodhia, S.; Sharma, U.; Low, M. Creating value: Sustainability and accounting for non-financial matters in the pre- and post-corona environment. Meditari Account. Res. 2021, 29, 185–196. [Google Scholar] [CrossRef]

- DeSimone, S.; D’Onza, G.; Sarens, G. Correlates of internal audit function involvement in sustainability audits. J. Manag. Gov. 2021, 25, 561–591. [Google Scholar] [CrossRef]

- Schneider, F.; Kallis, G.; Martinez-Alier, J. Crisis or opportunity? Economic degrowth for social equity and ecological sustainability. Introduction to this Special Issue. J. Clean. Prod. 2010, 18, 511–518. [Google Scholar] [CrossRef]

- Allan, J.D.; Abell, R.; Hogan, Z.; Revenga, C.; Taylor, B.W.; Welcomme, R.L.; Winemiller, K. Overfishing of Inland Waters. Bioscience 2005, 55, 1041–1051. [Google Scholar] [CrossRef] [Green Version]

- Lozano, R.; Huisingh, D. Inter-linking issues and dimensions in sustainability reporting. J. Clean. Prod. 2011, 19, 99–107. [Google Scholar] [CrossRef]

- Ntim, C.; Lindop, S.; Thomas, D. Corporate Governance and Risk Reporting in South Africa: A Study of Corporate Risk Disclosures in the Pre- and Post-2007/2008 Global Financial Crisis Periods. Int. Rev. Financ. Anal. 2013, 30, 363–383. [Google Scholar] [CrossRef]

- Krausmann, F.; Lauk, C.; Haas, W.; Wiedenhofer, D. From resource extraction to outflows of wastes and emissions: The socioeconomic metabolism of the global economy, 1900–2015. Glob. Environ. Chang. 2018, 52, 131–140. [Google Scholar] [CrossRef]

- Jones, M.J.; Solomon, J.F. Problematising accounting for biodiversity. Account. Audit. Account. J. 2013, 26, 668–687. [Google Scholar] [CrossRef]

- Calzadilla, A.; Rehdanz, K.; Tol, R.S. The economic impact of more sustainable water use in agriculture: A computable general equilibrium analysis. J. Hydrol. 2010, 384, 292–305. [Google Scholar] [CrossRef]

- Patel, A.; Arora, N.; Mehtani, J.; Pruthi, V.; Pruthi, P.A. Assessment of fuel properties on the basis of fatty acid profiles of oleaginous yeast for potential biodiesel production. Renew. Sustain. Energy Rev. 2017, 77, 604–616. [Google Scholar] [CrossRef] [Green Version]

- Abu-Rayash, A.; Dincer, I. Analysis of mobility trends during the COVID-19 coronavirus pandemic: Exploring the impacts on global aviation and travel in selected cities. Energy Res. Soc. Sci. 2020, 68, 101693. [Google Scholar] [CrossRef] [PubMed]

- Amicarelli, V.; Bux, C. Food waste in Italian households during the COVID-19 pandemic: A self-reporting approach. Food Secur. 2021, 13, 25–37. [Google Scholar] [CrossRef]

- Tomczyk, S.; Rahn, M.; Schmidt, S. Social Distancing and Stigma: Association Between Compliance with Behavioral Recommendations, Risk Perception, and Stigmatizing Attitudes During the COVID-19 Outbreak. Front. Psychol. 2020, 11, 1821. [Google Scholar] [CrossRef]

- Hausberg, J.P.; Liere-Netheler, K.; Packmohr, S.; Pakura, S.; Vogelsang, K. Research streams on digital transformation from a holistic business perspective: A systematic literature review and citation network analysis. J. Bus. Econ. 2019, 89, 931–963. [Google Scholar] [CrossRef] [Green Version]

- Sun, S.; Xie, Z.; Yu, K.; Jiang, B.; Zheng, S.; Pan, X. COVID-19 and healthcare system in China: Challenges and progression for a sustainable future. Glob. Health 2021, 17, 1–8. [Google Scholar] [CrossRef]

- Langemeyer, J.; Madrid-Lopez, C.; Beltran, A.; Mendez, G. Urban Agriculture—A Necessary Pathway towards Urban Resilience and Global Sustainability? Landsc. Urban Plan. 2021, 210, 104055. [Google Scholar] [CrossRef]

- Adedoyin, F.F.; Agboola, P.O.; Ozturk, I.; Bekun, F.V.; Agboola, M.O. Environmental consequences of economic complexities in the EU amidst a booming tourism industry: Accounting for the role of brexit and other crisis events. J. Clean. Prod. 2021, 305, 127117. [Google Scholar] [CrossRef]

- Chen, S.; Kharrazi, A.; Liang, S.; Fath, B.D.; Lenzen, M.; Yan, J. Advanced approaches and applications of energy footprints toward the promotion of global sustainability. Appl. Energy 2020, 261, 114415. [Google Scholar] [CrossRef]

- Nikas, A.; Gambhir, A.; Trutnevyte, E.; Koasidis, K.; Lund, H.; Thellufsen, J.; Mayer, D.; Zachmann, G.; Miguel, L.; Ferreras-Alonso, N.; et al. Perspective of comprehensive and comprehensible multi-model energy and climate science in Europe. Energy 2021, 215, 119153. [Google Scholar] [CrossRef]

- Adams, C.; Abhayawansa, S. Connecting the COVID-19 Pandemic, Environmental, Social and Governance (ESG) Investing and Calls for ‘Harmonisation’ of Sustainability Reporting. Crit. Perspect. Account. 2022, 82, 102309. [Google Scholar] [CrossRef]

- Bernal-Delgado, E.; García-Armesto, S.; Oliva, J.; Sánchez Martínez, F.; Repullo, J.; Peña-Longobardo, L.; Ridao-López, M.; Hernández-Quevedo, C. Spain: Health System Review; Health Systems in Transition; World Health Organization: Geneva, Switzerland, 2018. [Google Scholar]

- Cho, C.H.; Senn, J.; Sobkowiak, M. Sustainability at stake during COVID-19: Exploring the role of accounting in addressing environmental crises. Crit. Perspect. Account. 2022, 82, 102327. [Google Scholar] [CrossRef]

- Parmentola, A.; Petrillo, A.; Tutore, I.; De Felice, F. Is blockchain able to enhance environmental sustainability? A systematic review and research agenda from the perspective of Sustainable Development Goals (SDGs). Bus. Strat. Environ. 2022, 31, 194–217. [Google Scholar] [CrossRef]

- Naeem, M.A.; Karim, S.; Nor, S.M.; Ismail, R. Sustainable corporate governance and gender diversity on corporate boards: Evidence from COVID-19. Econ. Res. 2022, 35, 5824–5842. [Google Scholar] [CrossRef]

- Van Eck, N.J.; Waltman, L. Software survey: VOSviewer, a computer program for bibliometric mapping. Scientometrics 2010, 84, 523–538. [Google Scholar] [CrossRef] [Green Version]

- Kleinberg, J. Burst and Hierarchical Structure in Streams. Data Min. Knowl. Discov. 2003, 7, 373–397. [Google Scholar] [CrossRef]

- Janicka, M.; Sainóg, A. The ESG Reporting of EU Public Companies. Does the Company’s Capitalisation Matter. Sustainability 2022, 14, 4279. [Google Scholar] [CrossRef]

- Faccia, A.; Manni, F.; Capitanio, F. Mandatory ESG Reporting and XBRL Taxonomies Combination: ESG Ratings and Income Statement, a Sustainable Value-Added Disclosure. Sustainability 2021, 13, 8876. [Google Scholar] [CrossRef]

- Koch, R. The 80/20 Principle: The Secret of Achieving More with Less; Nicholas Brealey Pub: London, UK, 2000. [Google Scholar]

- Andreassen, N. Sustainability Reporting Guidelines—Safety Issues of Oil Companies. Eur. J. Sustain. Dev. 2017, 6, 377–387. [Google Scholar] [CrossRef] [Green Version]

- Bhimavarapu, V.M.; Rastogi, S.; Kanoujiya, J. Ownership concentration and its influence on transparency and disclosures of banks in India. Corp. Gov. Int. J. Bus. Soc. 2023, 23, 18–42. [Google Scholar] [CrossRef]

- Carter, C.; Easton, P. Sustainable Supply Chain Management: Evolution and Future Directions. Int. J. Phys. Distrib. Logist. Manag. 2011, 41, 46–62. [Google Scholar] [CrossRef]

- Del Baldo, M. The implementation of integrating reporting in SMEs: Insights from a pioneering experience in Italy. Meditari Account. Res. 2017, 25, 505–532. [Google Scholar] [CrossRef]

- Waltman, L.; van Eck, N.J.; Noyons, E.C.M. A unified approach to mapping and clustering of bibliometric networks. J. Informetr. 2010, 4, 629–635. [Google Scholar] [CrossRef] [Green Version]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| N° | Authors (Year) | Type of Paper | Main Topic |

|---|---|---|---|

| 1 | Fonseca et al., 2014 [23] | Critique | Sustainability in mining sector |

| 2 | Bianchi Martini et al., 2016 [24] | Empirical analysis | Human rights, CSR and reporting |

| 3 | Amoako et al., 2021 [25] | Empirical analysis (case study) | Informal reporting for ESG |

| 4 | Dilling & Harris, 2018 [26] | Empirical analysis (longitudinal assessment) | Long-term value creation reporting |

| 5 | Stent & Dowler, 2015 [27] | Empirical analysis | Gap between IR and corporate reporting |

| 6 | Garanina & Dumay, 2016 [28] | Empirical analysis | IR, IC disclosure research and IPO prospectus |

| 7 | Navarrete-Oyarce et al., 2021 [29] | Literature review | IR as academic topic in business |

| 8 | Beck et al., 2017 [30] | Empirical analysis (case study) | IR as single source of truth |

| 9 | Abhayawansa & Adams, 2021 [31] | Empirical analysis | Pandemic and climate change risk disclosure evaluation |

| 10 | Velte & Stawinoga, 2017 [32] | Literature review | Overview on IR as of 2016/17 |

| 11 | Prodanova et al., 2018 [33] | Empirical analysis | Implementation of IR in Russia |

| 12 | Gomes et al., 2015 [34] | Empirical analysis | Sustainability reporting assurance (SRA) |

| 13 | Branco et al., 2014 [35] | Empirical analysis | SRA engagement and factors |

| 14 | Velte, 2020 [36] | Literature review | Institutional ownership role in ESG performance/disclosure |

| 15 | Staszkiewicz & Werner, 2021 [37] | Empirical analysis and review | Measuring sustainability framework |

| 16 | Velte & Stawinoga, 2020 [38] | Literature review | CSR committees and CSO impacts on CSR performance |

| 17 | Velte, 2017 [39] | Literature review | Influence of board composition on the quality of CSR reporting |

| 18 | Monciardini, 2016 [40] | Empirical study | EU directive on NFR process |

| 19 | Kinderman, 2013 [41] | Critique | EU CSR History |

| 20 | Kinderman, 2016 [42] | Critique | Voluntary and regulatory measures in CSR private governance |

| 21 | Biondi et al., 2020 [43] | Critique | IR problems and compliance with EU NFI and diversity |

| 22 | Tettamanzi et al., 2022 [44] | Critique | EFRAG vs IFRS on sustainability disclosure |

| 23 | Schaltegger, 2020 [6] | Literature review | Sources of epidemics and impact on accounting and reporting |

| 24 | La Torre et al., 2020 [45] | Literature review | Accountability and EU directive on NFR |

| 25 | Lodhia et al., 2021 [46] | Critique | Pandemic and accounting for non-financial issues |

| 26 | Arvidsson & Dumay, 2022 [1] | Empirical study | Trends in ESG reporting: quality and corporate ESG performance |

| Rank | Title | Author(s) | Journal | Pub. Year | GCS | Main Path |

|---|---|---|---|---|---|---|

| 1 | Crisis or Opportunity? Economic Degrowth for Social Equity and Ecological Sustainability. | Schneider, Kallis & Martinez-Alier [48] | Journal of Cleaner Production | 2010 | 521 | |

| 2 | Overfishing of Inland Waters | Allan et al. [49] | BioScience | 2005 | 452 | |

| 3 | Inter-Linking Issues and Dimensions in Sustainability Reporting | Lozano & Huisingh [50] | Journal of Cleaner Production | 2011 | 324 | |

| 4 | Corporate Governance and Risk Reporting in South Africa: A Study of Corporate Risk Disclosures in The Pre- and Post-2007/2008 Global Financial Crisis Periods | Ntim, Lindop & Thomas [51] | International Review of Financial Analysis | 2013 | 169 | |

| 5 | Sustainability Reporting Among Mining Corporations: A Constructive Critique of the GRI Approach | Fonseca, McAllister & Fitzpatrick [23] | Journal of Cleaner Production | 2014 | 136 | x |

| 6 | From Resource Extraction to Outflows of Wastes and Emissions: The Socioeconomic Metabolism of the Global Economy, 1900–2015 | Krausmann et al. [52] | Global Environmental Change | 2018 | 117 | |

| 7 | Problematising Accounting for Biodiversity | Jones & Solomon [53] | Accounting, Auditing and Accountability Journal | 2013 | 116 | |

| 8 | The Economic Impact of More Sustainable Water Use in Agriculture: A Computable General Equilibrium Analysis | Calzadilla, Rehdanz & Tol [54] | Journal of Hydrology | 2010 | 116 | |

| 9 | Integrated Reporting: The Current State of Empirical Research, Limitations and Future Research Implications | Velte & Stawinoga [32] | Journal of Management Control | 2017 | 114 | x |

| 10 | Assessment of Fuel Properties on the Basis of Fatty Acid Profiles of Oleaginous Yeast for Potential Biodiesel Production | Patel et al. [55] | Renewable and Sustainable Energy Reviews | 2017 | 112 |

| Rank | Title | Author(s) | Journal | Pub. Year | GLCS | Main Path |

|---|---|---|---|---|---|---|

| 1 | Analysis of Mobility Trends During the COVID-19 Pandemic: Exploring the Impacts on Global Aviation and Travel in Selected Cities | Abu-Rayash & Dincer [56] | Energy Research and Social Science | 2020 | 92 | |

| 2 | Food Waste in Italian Households during the COVID-19 Pandemic: A Self-Reporting Approach | Amicarelli & Bux [57] | Food Security | 2021 | 47 | |

| 3 | Social Distancing and Stigma: Association Between Compliance with Behavioral Recommendations, Risk Perception, and Stigmatizing Attitudes during the COVID-19 Outbreak | Tomczyk, Rahn & Schmidt [58] | Frontiers in Psychology | 2020 | 45 | |

| 4 | Research Streams on Digital Transformation from a Holistic Business Perspective: A Systematic Literature Review and Citation Network Analysis | Hausberg et al. [59] | Journal of Business Economics | 2019 | 44 | |

| 5 | COVID-19 and Healthcare System in China: Challenges and Progression for a Sustainable Future | Sun et al. [60] | Globalization and Health | 2021 | 39 | |

| 6 | Urban Agriculture—A Necessary Pathway towards Urban Resilience and Global Sustainability? | Langemeyer et al. [61] | Landscape and Urban Planning | 2021 | 39 | |

| 7 | Environmental Consequences of Economic Complexities in the EU amidst a Booming Tourism Industry: Accounting for the Role of Brexit and other Crisis Events | Adedoyin et al. [62] | Journal of Cleaner Production | 2021 | 35 | |

| 8 | Advanced Approaches and Applications of Energy Footprints toward the Promotion of Global Sustainability | Chen et al. [63] | Applied Energy | 2020 | 31 | |

| 9 | Perspective of Comprehensive and Comprehensible Multi-Model Energy and Climate Science in Europe | Nikas et al. [64] | Energy Research and Social Science | 2021 | 30 | |

| 10 | Rebuilding Trust: Sustainability and Non-Financial Reporting and the European Union Regulation | La Torre et al. [45] | Meditari Accountancy Research | 2020 | 30 | x |

| Rank | Title | Author(s) | Journal | Pub. Year | INCEX | Main Path |

|---|---|---|---|---|---|---|

| 1 | Crisis or Opportunity? Economic Degrowth for Social Equity and Ecological Sustainability. Introduction to this Special Issue | Schneider, Kallis & Martinez-Alier [48] | Journal of Cleaner Production | 2010 | 40.1 | |

| 2 | Analysis of Mobility Trends during the COVID-19 Coronavirus Pandemic: Exploring the Impacts on Global Aviation and Travel in Selected Cities | Abu-Rayash & Dincer [56] | Energy Research and Social Science | 2020 | 30.7 | |

| 3 | Inter-Linking Issues and Dimensions in Sustainability Reporting | Lozano & Huisingh [50] | Journal of Cleaner Production | 2011 | 27.0 | |

| 4 | Overfishing of Inland Waters | Allan et al. [49] | BioScience | 2005 | 25.1 | |

| 5 | Connecting the COVID-19 Pandemic, Environmental, Social and Governance (ESG) Investing and Calls for ‘Harmonisation’ of Sustainability Reporting | Adams & Abhayawansa [65] | Critical Perspective on Accounting | 2022 | 25.0 | |

| 6 | Food Waste In Italian Households During The COVID-19 Pandemic: A Self-Reporting Approach | Amicarelli & Bux [57] | Food Security | 2021 | 23.5 | |

| 7 | From Resource Extraction to Outflows of Wastes and Emissions: the Socioeconomic Metabolism of the Global Economy, 1900–2015 | Krausmann et al. [52] | Global Environmental Change | 2018 | 23.4 | |

| 8 | Spain: Health System Review | Bernal-Delgado Et al. [66] | Health Systems in Transition | 2018 | 20.4 | |

| 9 | COVID-19 and Healthcare System in China: Challenges and Progression for a Sustainable Future | Sun et al. [60] | Globalization and Health | 2021 | 19.5 | |

| 10 | Urban Agriculture—A Necessary Pathway towards Urban Resilience and Global Sustainability? | Langemeyer et al. [61] | Landscape and Urban Planning | 2021 | 19.5 |

| Keyword | Avg. Pub. Year |

|---|---|

| Cluster 1 | |

| Accounting practices | 2018.24 |

| Accounting theory | 2018.00 |

| Assurance and accountability | 2017.00 |

| Decision making | 2016.88 |

| ESG reporting | 2018.67 |

| Risk assessment | 2015.38 |

| Value relevance | 2018.00 |

| Cluster 2 | |

| Corporate governance | 2017.19 |

| CSR | 2018.44 |

| Development and growth | 2016.42 |

| Financial crisis and banks | 2017.16 |

| Performance measurement | 2017.94 |

| Stakeholders | 2017.50 |

| Sustainable finance | 2018.69 |

| Cluster 3 | |

| Climate change | 2019.43 |

| COVID-19 | 2021.02 |

| Environment | 2020.40 |

| Integrated reporting | 2018.17 |

| SDG | 2021.17 |

| Sustainability | 2018.19 |

| Cluster 4 | |

| Digitalization and technology | 2019.60 |

| Big data | 2018.19 |

| Energy | 2019.71 |

| N° | Topic Gap | Description | References |

|---|---|---|---|

| 1 | Non-financial reporting (NFR) process, EU context and directives, and Green Taxonomy | - Longitudinal and cross-national studies, with different subjects (both corporations, entities and small/medium enterprises). - Interviews and case studies. - SEM-PLS studies and regression technique analysis for panel data. - Ground theory and computer-aided qualitative analysis data software (CAQDAS) implementation. | Lozano & Huisingh, 2011 [50] La Torre et al., 2020 [45] Amoako et al., 2021 [25] Abhayawansa & Adams, 2021 [31] Staszkiewicz & Werner, 2021 [37] Arvidsson & Dumay, 2022 [1] |

| 2 | <IR>, GRI and SDGs achievement: the COVID-19 pandemic and climate change | - Need for a determined framework or several contextual frameworks for ‘good’ ESG reporting practices and their quality assessment. - Gap analysis and systems thinking approach. - Need for a determination of what, how and why decisions were made throughout the COVID-19 pandemic period, helping a forward-looking perspective to emerge. - Further investigation into the concept of sustainability reporting. | Stent & Dowler, 2015 [27] Garanina & Dumay, 2016 [28] Adams & Abhayawansa, 2022 [65] Tregidga & Laine, 2022 [5] Rüger & Maertens, 2023 [9] |

| 3 | Risk disclosure evaluation/assessment, long-term value creation and forward-looking information | - Qualitative studies (surveys, case studies, interviews, and experimental studies). - Two-stage methodology (content analysis combined with market data regression analysis). - Action research. | Dilling & Harris, 2018 [26] Cho et al., 2022 [67] |

| 4 | Sustainability reporting assurance (SRA) | - Qualitative studies (surveys, case studies, interviews, and experimental studies). - In-depth analysis and bivariate/multivariate non-parametric statics. - Action research. | Branco et al., 2014 [35] Gomes et al., 2015 [34] |

| 5 | Voluntary and regulatory measures in CSR private and corporate governance | - Empirical studies on choice determinants and impacts on performance. - Interviews and case studies. - SEM-PLS studies and regression technique analysis. | Ntim et al., 2013 [51] Velte, 2020 [36] Naeem et al., 2022 [69] |

| 6 | Economic degrowth, harmonisation and long-term environmental accounting role in addressing crises | - Qualitative studies (both archival and interviews). - Interpretivist approach by publicly available secondary data sources. - Generalised method of moment (GMM) model and pooled ordinary least squares (pooled-OLS) regression. | Biondi et al., 2020 [43] Adedoyin et al., 2021 [62] Bigoni & Mohammed, 2023 [2] |

| 7 | Energy, transportation, tourism and other industry disruptions | - Assessment model for specific sector in smart city extension. - Energy footprint measurement. - Life cycle assessment (LCA) from a whole-supply-chain perspective. - Multi-model framework and collective science approach. | Abu-Rayash & Dincer, 2020 [56] Chen et al., 2020 [63] Nikas et al., 2021 [64] |

| 8 | Ecosystems, biodiversity and accounting for animals | - Cross-field research among management, governance and business researchers and natural science departments. - Framework problematising biodiversity. - Examination of reporting and valuation models in a real-life context to test predictability. | Jones & Solomon, 2013 [53] Schaltegger, 2020 [6] Vinnari & Vinnari, 2022 [10] |

| 9 | Food, water and waste management | - Cross-field research among management, governance and business researchers and natural science departments. - GTAP-W model and the concept of maximum allowable water withdrawal (MAWW) extension. - Assessment of the development of material flows through the global economy. - Food diary and Sankey diagram. - Focused literature reviews. | Allan et al., 2005 [49] Calzadilla et al., 2010 [54] Krausmann et al., 2018 [52] Amicarelli & Bux, 2021 [57] Langemeyer et al., 2021 [61] |

| 10 | Health care systems and safety disruptions | - Examination of reporting and valuation models in a real-life context to test predictability. - SEM-PLS studies and regression technique analysis for panel data. - Multinomial logistic regression model. | Bernal-Delgado et al., 2018 [66] Sun et al., 2021 [60] |

| 11 | Blockchain and digital transformation influences on sustainability | - Gephi analysis and cluster. - Preferred Reporting Items for Systematic Review and Meta-Analyses (PRISMA) protocol implementation. - Focused literature reviews. | Hausberg et al., 2019 [59] Parmentola et al., 2022 [68] Saxena et al., 2023 [3] |

| 12 | Sustainable corporate governance and diversity: socio-economic crises and psychological consequences | - Cross-field research among management, governance and business researchers and sociology or psychology departments. - Sociodemographic and psychosocial predictor testing. - Compromise and/or latent conflicts between the environment and the social in ESG dynamics. | Tomczyk et al., 2020 [58] Lodhia et al., 2021 [46] |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Comoli, M.; Tettamanzi, P.; Murgolo, M. Accounting for ‘ESG’ under Disruptions: A Systematic Literature Network Analysis. Sustainability 2023, 15, 6633. https://doi.org/10.3390/su15086633

Comoli M, Tettamanzi P, Murgolo M. Accounting for ‘ESG’ under Disruptions: A Systematic Literature Network Analysis. Sustainability. 2023; 15(8):6633. https://doi.org/10.3390/su15086633

Chicago/Turabian StyleComoli, Maurizio, Patrizia Tettamanzi, and Michael Murgolo. 2023. "Accounting for ‘ESG’ under Disruptions: A Systematic Literature Network Analysis" Sustainability 15, no. 8: 6633. https://doi.org/10.3390/su15086633