Islamic Law, Islamic Finance, and Sustainable Development Goals: A Systematic Literature Review

Abstract

:1. Introduction

2. Sustainability from the Perspective of Islamic Law and the UN

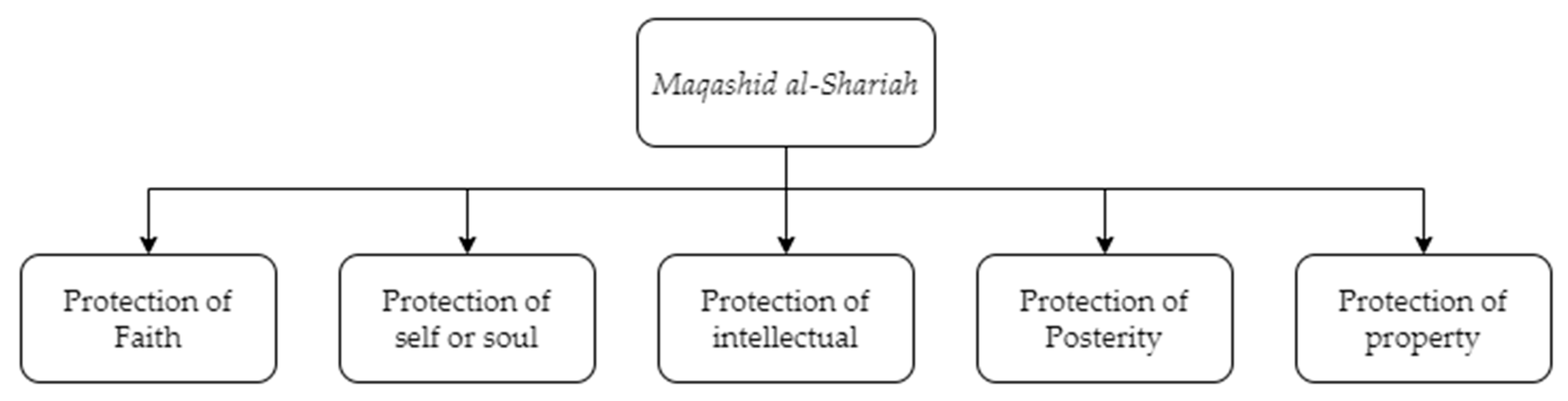

2.1. Islamic Law

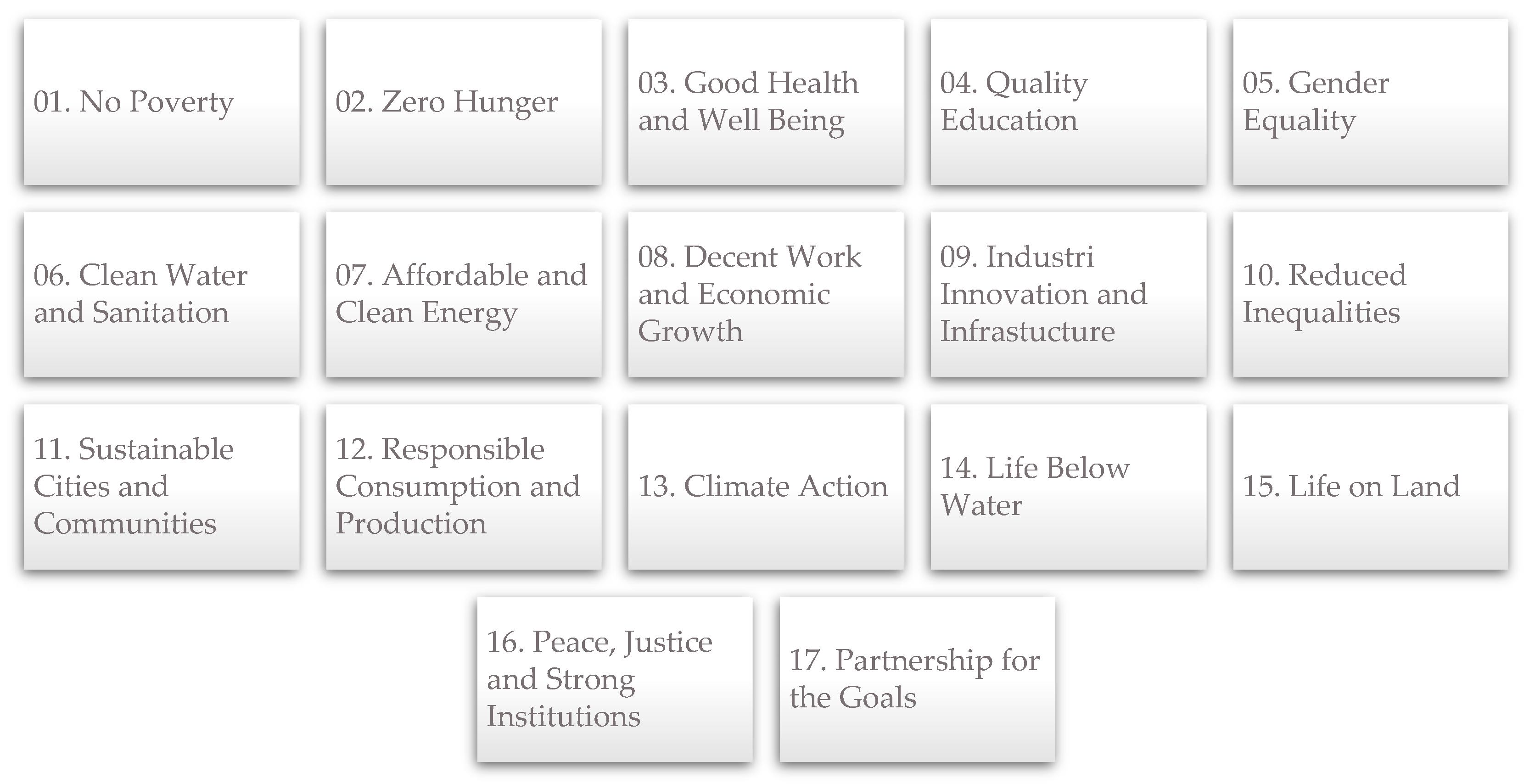

2.2. Sustainable Development Goals

3. Methodology

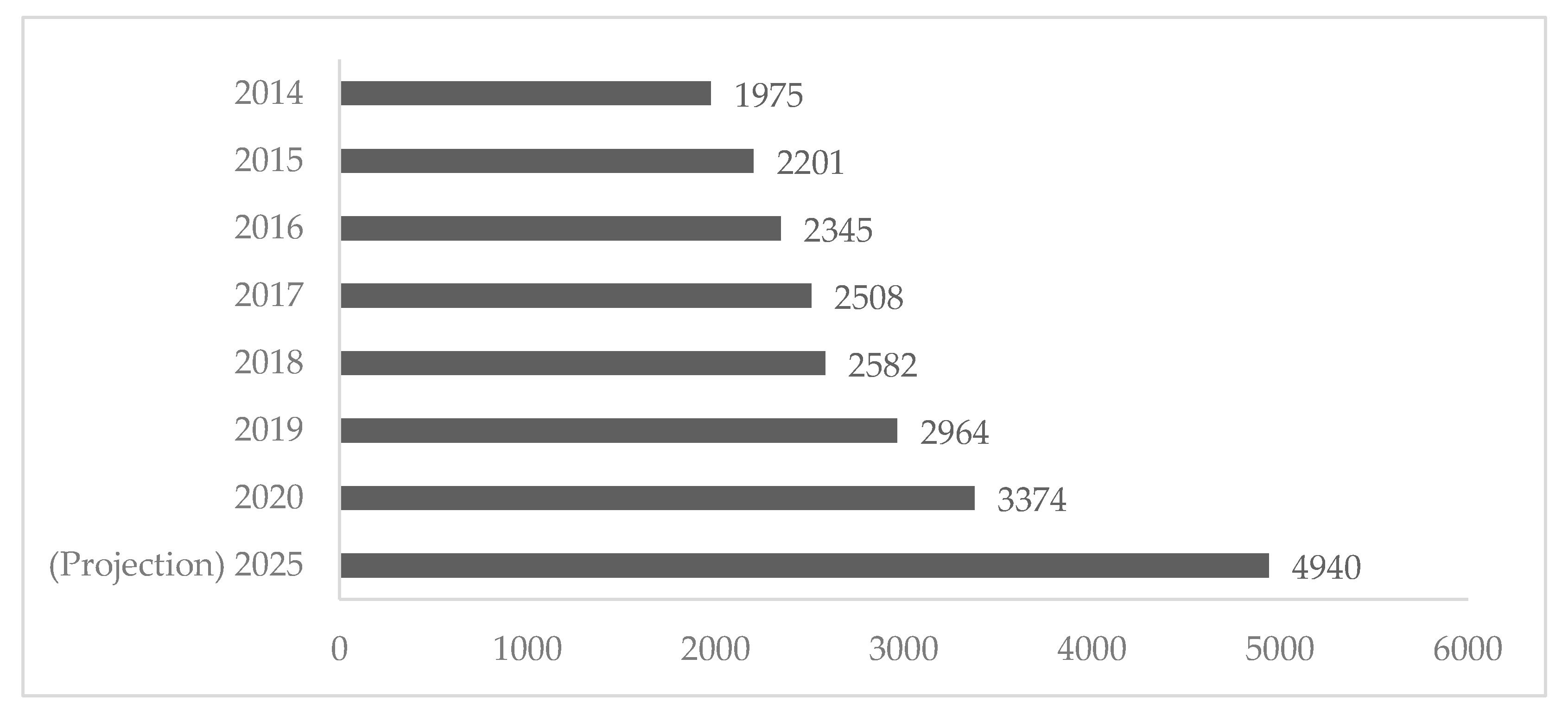

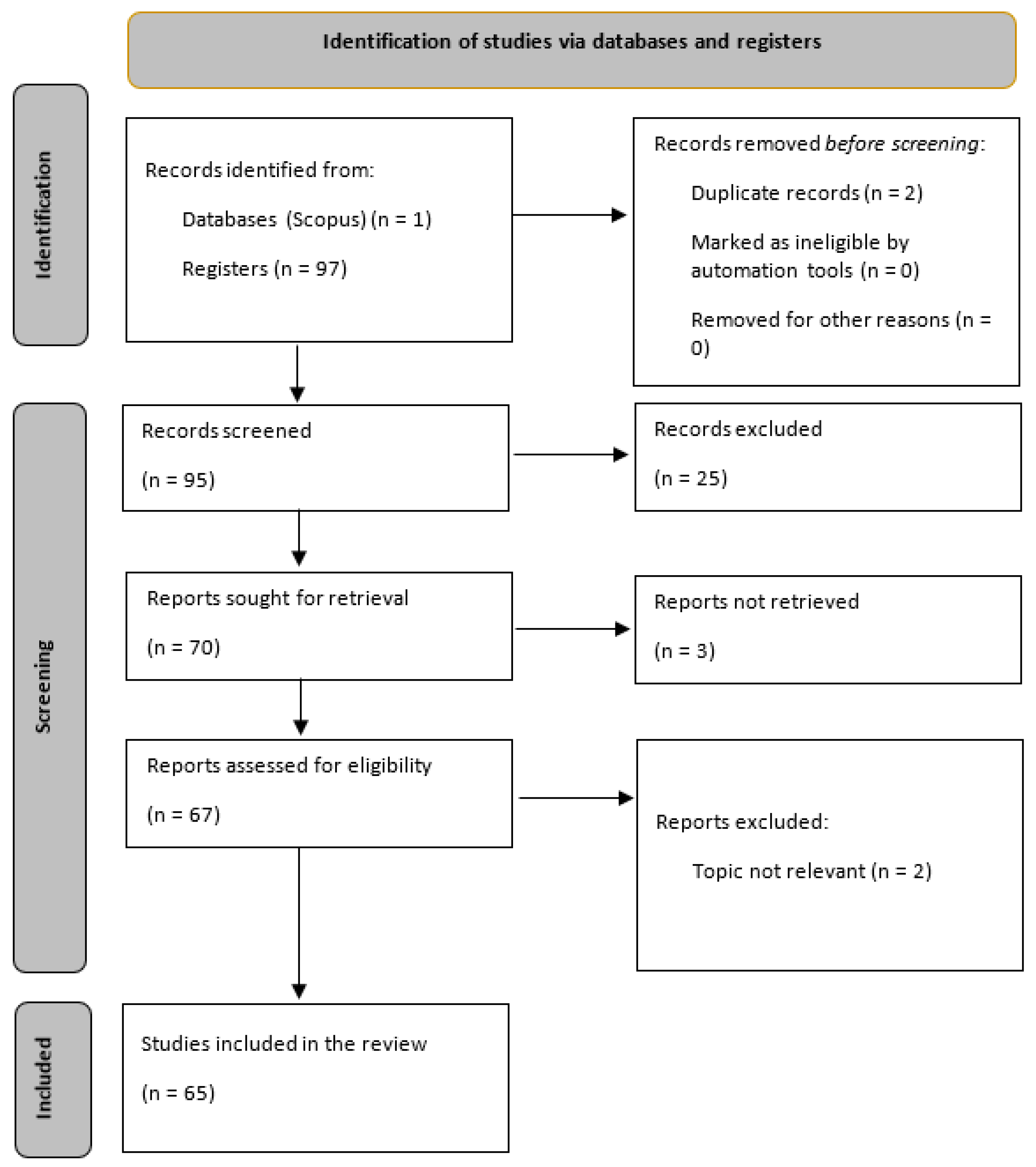

3.1. Search Stage

3.2. Implementation Stage

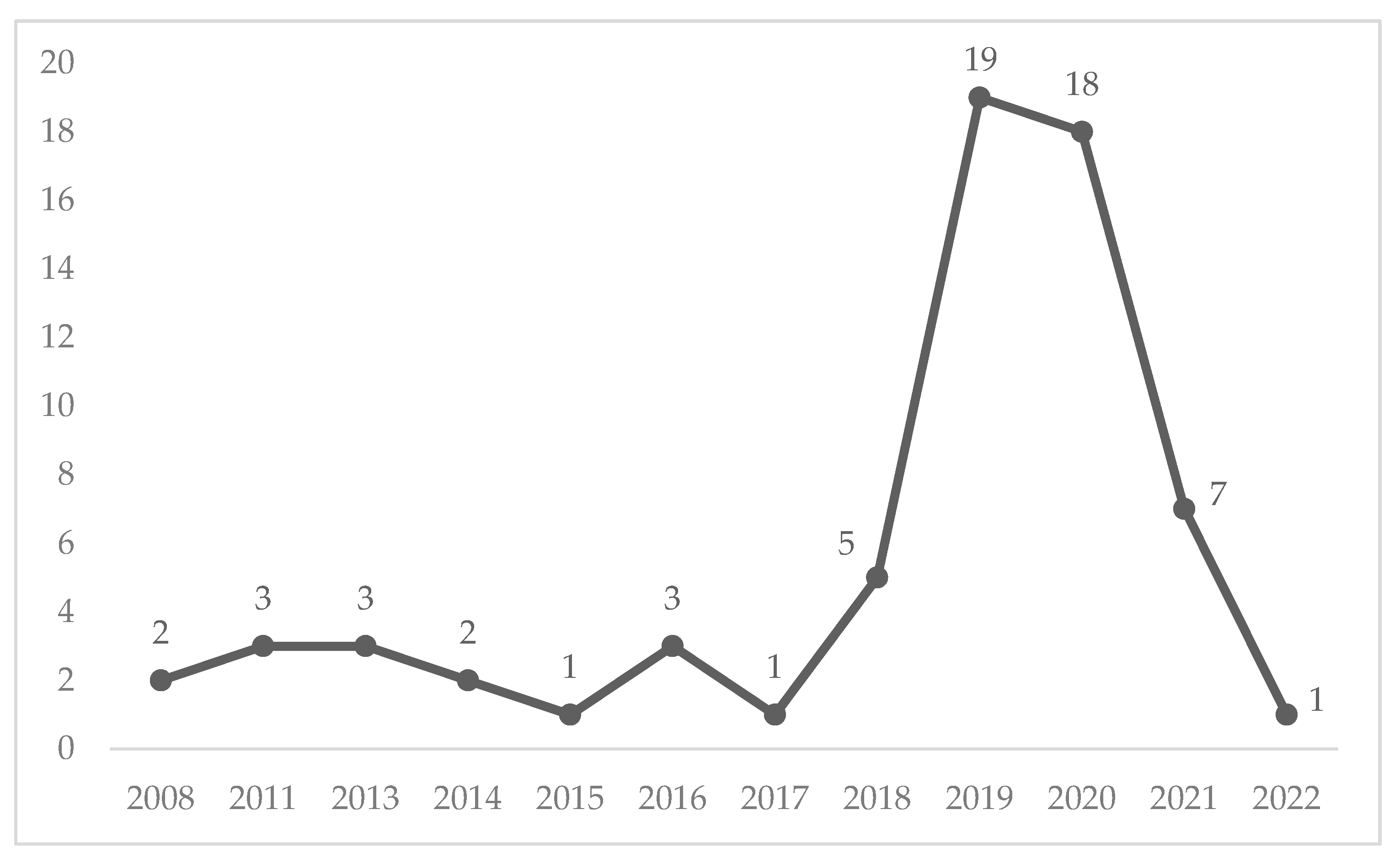

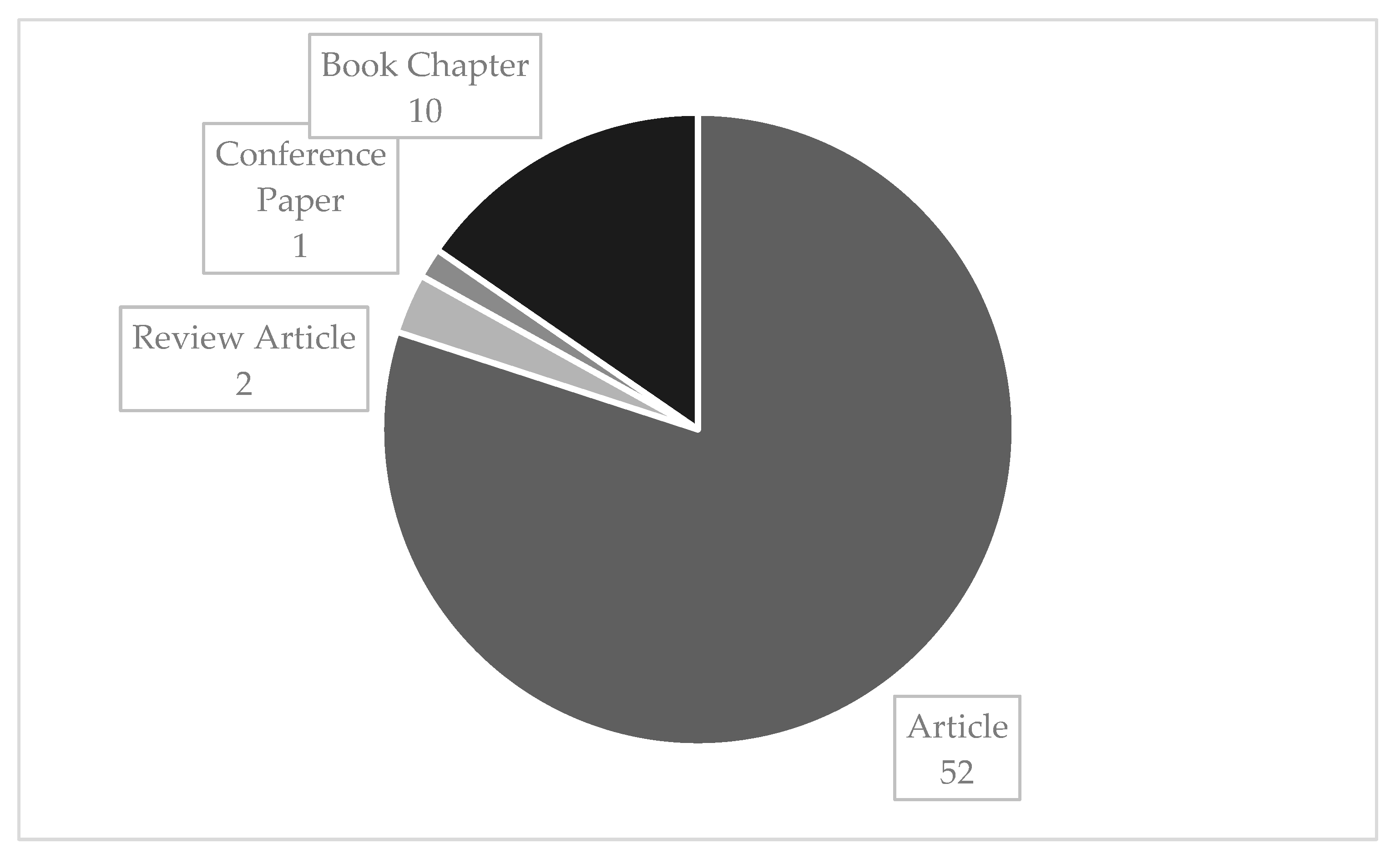

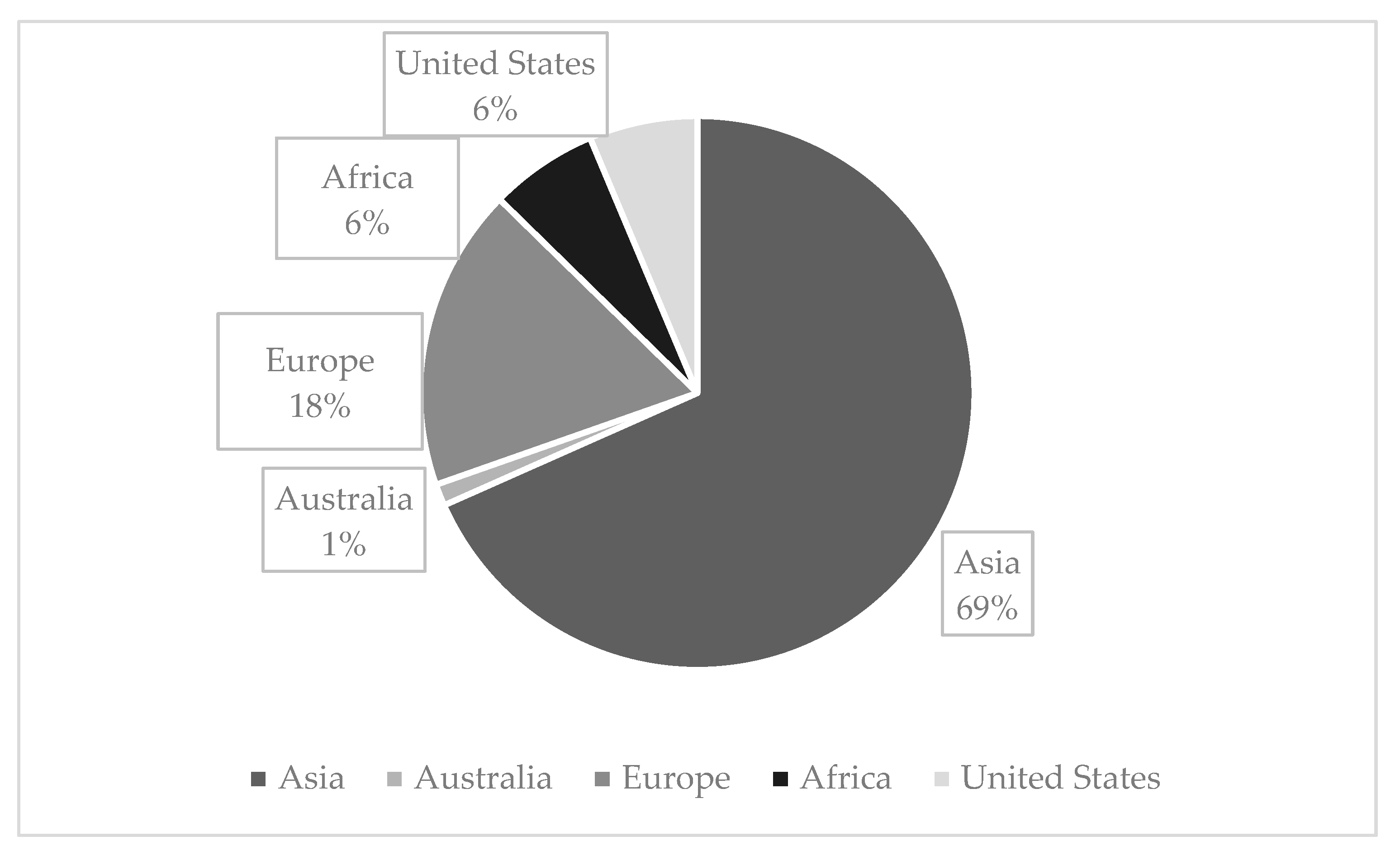

3.3. Data Extraction Results

4. Results and Discussion

4.1. Islamic Finance Sustainability in General

4.2. Compliance with Shariah

4.3. Consumer Behavior

4.4. Financial Technology

4.5. Green Banking

4.6. Halal Industry

4.7. Human Resources and Education

4.8. Islamic Corporate Governance

4.9. Philanthropy, Corporate Social Responsibility, and Ethics in the Financial Industry

4.10. Islamic Finance Innovation

4.11. Women Emporement

5. Summary of Findings

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Ghlamallah, E.; Alexakis, C.; Dowling, M.; Piepenbrink, A. The Topics of Islamic Economics and Finance Research. Int. Rev. Econ. Financ. 2021, 75, 145–160. [Google Scholar] [CrossRef]

- Ahmed, H. Contribution of Islamic Finance To the 2030 Agenda for Sustainable Development. In Proceedings of the High-level Conference on Financing for Development and the Means of Implementation of the 2030 Agenda for Sustainable Development, Doha, Qatar, 18–19 November 2017. [Google Scholar]

- Paltrinieri, A.; Dreassi, A.; Migliavacca, M.; Piserà, S. Islamic Finance Development and Banking ESG Scores: Evidence from a Cross-Country Analysis. Res. Int. Bus. Financ. 2020, 51, 101100. [Google Scholar] [CrossRef]

- Refinitiv. Islamic Finance Development Report 2021; Refinitiv: New York, NY, USA, 2021. [Google Scholar]

- Azmat, S.; Kabir Hassan, M.; Ali, H.; Sohel Azad, A.S.M. Religiosity, Neglected Risk and Asset Returns: Theory and Evidence from Islamic Finance Industry. J. Int. Financ. Mark. Inst. Money 2021, 74, 101294. [Google Scholar] [CrossRef]

- Abduh, M. The Role of Islamic Social Finance in Achieving Sdg Number 2: End Hunger, Achieve Food Security and Improved Nutrition and Promote Sustainable Agriculture. Al Shajarah J. Int. Inst. Islam. Thought Civiliz. ISTAC 2019, 2019, 185–206. [Google Scholar]

- Alhammadi, S. Analyzing the Role of Islamic Finance in Kuwait Regarding Sustainable Economic Development in COVID-19 Era. Sustainability 2022, 14, 701. [Google Scholar] [CrossRef]

- Ul-Hassan, M.; Usman, M. Building the Entrepreneurship through Non-Banking Institution: An Empirical Study on the Contribution of GEAR for Economic Development in Islamic Way. Middle East J. Sci. Res. 2013, 15, 1353–1362. [Google Scholar] [CrossRef]

- Dusuki, A.W. Understanding the Objectives of Islamic Banking: A Survey of Stakeholders’ Perspectives. Int. J. Islam. Middle East. Financ. Manag. 2008, 1, 132–148. [Google Scholar] [CrossRef] [Green Version]

- Ali, S.N. Big Data, Islamic Finance, and Sustainable Development Goals. J. King Abdulaziz Univ. Islam. Econ. 2020, 33, 83–90. [Google Scholar] [CrossRef]

- Ayub, M. Issues in Theory and Practice of Islamic Finance and the Reform Agenda. J. King Abdulaziz Univ. Islam. Econ. 2020, 33, 81–92. [Google Scholar] [CrossRef]

- Imronudin, I.; Hussain, J. Sustainable Supply Chain Finance Process in Delivering Financing for SMEs: The Case of Indonesia. Int. J. Supply Chain Manag. 2020, 9, 867–878. [Google Scholar]

- Jan, A.; Marimuthu, M.; Mohd, M.P.b.; Isa, M. The Nexus of Sustainability Practices and Financial Performance: From the Perspective of Islamic Banking. J. Clean. Prod. 2019, 228, 703–717. [Google Scholar] [CrossRef]

- Karake-Shalhoub, Z. Private Equity, Islamic Finance, and Sovereign Wealth Funds in the MENA Region. Thunderbird Int. Bus. Rev. 2008, 50, 359–368. [Google Scholar] [CrossRef]

- Khan, T. Reforming Islamic Finance for Achieving Sustainable Development Goals. J. King Abdulaziz Univ. Islam. Econ. 2019, 32, 3–21. [Google Scholar] [CrossRef]

- Nobanee, H.; Ellili, N. Corporate Sustainability Disclosure in Annual Reports: Evidence from UAE Banks: Islamic versus Conventional. Renew. Sustain. Energy Rev. 2016, 55, 1336–1341. [Google Scholar] [CrossRef]

- Razimi, M.S.A. The Prospect and Challenges of Islamic Banking and Finance in Nigeria: A Conceptual Approach. Res. J. Appl. Sci. 2016, 11, 1362–1371. [Google Scholar]

- Smolo, E.; Musa, A.M. The (Mis)Use of Al-Hilah (Legal Trick) and Al-Makhraj (Legal Exit) in Islamic Finance. J. Islam. Account. Bus. Res. 2020, 11, 2169–2182. [Google Scholar] [CrossRef]

- Al Madani, H.; Alotaibi, K.O.; Alhammadi, S. The Role of Sukuk in Achieving Sustainable Development: Evidence from the Islamic Development Bank. Banks Bank Syst. 2020, 15, 36–48. [Google Scholar] [CrossRef]

- Hussain, H.I.; Anwar, N.A.M.; Razimi, M.S.A. A Generalised Regression Neural Network Model of Financing Imbalance: Shari’ah Compliance as the Roadmap for Sustainability of Capital Markets. J. Intell. Fuzzy Syst. 2020, 39, 5387–5395. [Google Scholar] [CrossRef]

- Mahadi, N.F.; Mohd Zain, N.R.; Engku Ali, E.R.A. Leading towards Impactful Islamic Social Finance: Malaysian Experience with the Value-Based Intermediation Approach. Al Shajarah J. Int. Inst. Islam. Thought Civiliz. ISTAC 2019, 2019, 69–87. [Google Scholar]

- Abdullah, R. Al-Tawhid in Relation to the Economic Order of Microfinance Institutions. Humanomics 2014, 30, 325–348. [Google Scholar] [CrossRef]

- Hussain, H.I.; Grabara, J.; Razimi, M.S.A.; Sharif, S.P. Sustainability of Leverage Levels in Response to Shocks in Equity Prices: Islamic Finance as a Socially Responsible Investment. Sustainability 2019, 11, 3260. [Google Scholar] [CrossRef] [Green Version]

- Ali, Q.; Parveen, S.; Senin, A.A.; Zaini, M.Z. Islamic Bankers’ Green Behaviour for the Growth of Green Banking in Malaysia. Int. J. Environ. Sustain. Dev. 2020, 19, 393–411. [Google Scholar] [CrossRef]

- Aassouli, D.; Ebrahim, M.-S.; Basiruddin, R. Can UGITs Promote Liquidity Management and Sustainable Development? ISRA Int. J. Islam. Financ. 2018, 10, 126–142. [Google Scholar] [CrossRef]

- Mohd Nor, S. Islamic Social Bank: An Adaptation of Islamic Banking? J. Pengur. 2016, 46, 43–52. [Google Scholar] [CrossRef]

- Aust, V.; Morais, A.I.; Pinto, I. How Does Foreign Direct Investment Contribute to Sustainable Development Goals? Evidence from African Countries. J. Clean. Prod. 2019, 245, 118823. [Google Scholar] [CrossRef]

- Ogunmakinde, O.E.; Egbelakin, T.; Sher, W. Contributions of the Circular Economy to the UN Sustainable Development Goals through Sustainable Construction. Resour. Conserv. Recycl. 2021, 178, 106023. [Google Scholar] [CrossRef]

- Hummel, D.; Hashmi, A.T. The Possibilities of Community Redevelopment with Islamic Finance. J. Islam. Account. Bus. Res. 2019, 10, 259–273. [Google Scholar] [CrossRef]

- Ghafar, A.; Tohirin, A. Islamic Law and Finance. Humanomics 2010, 26, 178–199. [Google Scholar] [CrossRef] [Green Version]

- Shinkafi, A.A.; Ali, N.A.; Choudhury, M. Contemporary Islamic Economic Studies on Maqasid Shari’ah: A Systematic Literature Review. Humanomics 2017, 33, 315–334. [Google Scholar] [CrossRef]

- Dusuki, A.W.; Bouheraoua, S. The Framework of Maqasid Al-Shari’ah and Its Implication for Islamic Finance. ICR J. 2011, 2, 316–336. [Google Scholar] [CrossRef]

- Arsad, S.; Ahmad, R.; Fisol, W.N.M.; Said, R.; Haji-Othman, Y. Maqasid Shariah in Corporate Social Responsibility of Shari’ah Compliant Companies. Res. J. Financ. Account. 2015, 6, 239–247. [Google Scholar]

- Esen, M.F. A Statistical Framework on Identification of Maqasid Al-Shariah Variables for Socio-Economic Development Index. J. Bus. Stud. Q. 2015, 7, 18. [Google Scholar]

- Ascarya, S.R.; Sukmana, R. Measuring the Islamicity of Islamic Bank in Indonesia and Other Countries Based on Shari’ah Objectives. In Proceedings of the 11th Islamic Conference on Islamic Economics and Finance, Kuala Lumpur, Malaysia, 11–13 October 2016. [Google Scholar]

- Chapra, M. The Islamic Vision of Development in the Light of the Maqasid Al-Shari’ah (Research Paper). Occas. Pap. 2008, 235, 1–55. [Google Scholar]

- United Nations. Transforming Our World: The 2030 Agenda for Sustainable Development; United Nations: San Francisco, CA, USA, 2015. [Google Scholar]

- Sharma, H.B.; Vanapalli, K.R.; Samal, B.; Cheela, V.R.S.; Dubey, B.K.; Bhattacharya, J. Circular Economy Approach in Solid Waste Management System to Achieve UN-SDGs: Solutions for Post-COVID Recovery. Sci. Total Environ. 2021, 800, 149605. [Google Scholar] [CrossRef]

- Siddaway, A.P.; Wood, A.M.; Hedges, L.V. How to Do a Systematic Review: A Best Practice Guide for Conducting and Reporting Narrative Reviews, Meta-Analyses, and Meta-Syntheses. Annu. Rev. Psychol. 2018, 70, 747–770. [Google Scholar] [CrossRef]

- Jafari, J.; Scott, N. Muslim World and Its Tourisms. Ann. Tour. Res. 2014, 44, 1–19. [Google Scholar] [CrossRef] [Green Version]

- Iskandar, A.; Possumah, B.T.; Aqbar, K.; Yunta, A.H.D. Islamic Philanthropy and Poverty Reduction in Indonesia: The Role of Integrated Islamic Social and Commercial Finance Institutions. Al Ihkam J. Huk. Dan Pranata Sos. 2021, 16, 274–301. [Google Scholar] [CrossRef]

- Hassana, S.H.M.; Bahari, Z.; Aziz, A.H.A.; Doktoralina, C.M. Sustainable Development of Endowment (Waqf) Properties. Int. J. Innov. Creat. Chang. 2020, 13, 1135–1150. [Google Scholar]

- Ibrahim, F.; Frisdiantara, C.; Wekke, I.S. Differentiation Strategy of Islamic Micro Finance Institutions in Malang. J. Eng. Appl. Sci. 2017, 12, 3865–3869. [Google Scholar] [CrossRef]

- Haji-Othman, Y.; Yusuff, M.S.S.; Moawad, A.M.K. Analyzing Zakat as a Social Finance Instrument to Help Achieve the Sustainable Development Goals in Kedah|Análisis Del Zakat Como Instrumento de Financiación Social Para Contribuir a La Consecución de Los Objetivos de Desarrollo Sostenible En Kedah. Stud. Appl. Econ. 2021, 39. [Google Scholar] [CrossRef]

- Chong, F.H.L. Enhancing Trust through Digital Islamic Finance and Blockchain Technology. Qual. Res. Financ. Mark. 2021, 13, 328–341. [Google Scholar] [CrossRef]

- Zain, N.S.; Muhamad, Z.S. An Exploratory Study on Musharakah SRI Sukuk for the Development of Waqf Properties/Assets in Malaysia. Qual. Res. Financ. Mark. 2020, 12, 301–314. [Google Scholar] [CrossRef]

- Thaker, M.A.B.M.T.; Thaker, H.B.M.T.; Pitchay, A.B.A.; Amin, M.F.B.; Khaliq, A. Bin Leveraging the Potential of Islamic Banking and Finance for Small Businesses. In Investment In Startups And Small Business Financing; WSPC: Singapore, 2021. [Google Scholar]

- Muneeza, A. Short-Term Sharīʿah-Compliant Islamic Liquidity Management Instruments to Sustain Islamic Banking: The Case of Maldives. J. Islam. Account. Bus. Res. 2020, 11, 428–439. [Google Scholar] [CrossRef]

- Adewale, A.S.; Zubaedy, A.A.G. Islamic Finance Instruments as Alternative Financing to Sustainable Higher Education in Nigeria. Glob. J. Al Thaqafah 2019, 9, 35–48. [Google Scholar] [CrossRef]

- Choudhury, M.A.; Hossain, M.S.; Mohammad, M.T. Islamic Finance Instruments for Promoting Long-Run Investment in the Light of the Well-Being Criterion (Maslaha). J. Islam. Account. Bus. Res. 2019, 10, 315–339. [Google Scholar] [CrossRef]

- Oseni, U.A.; Hassan, M.K.; Ali, S.N. Judicial Support for the Islamic Financial Services Industry: Towards Reform-Oriented Interpretive Approaches. Arab. Law Q. 2020, 35, 421–443. [Google Scholar] [CrossRef]

- Allah Pitchay, A.B.; Mohd Thas Thaker, M.A.B.; Azhar, Z.; Mydin, A.A.; Mohd Thas Thaker, H.B. Factors Persuade Individuals’ Behavioral Intention to Opt for Islamic Bank Services: Malaysian Depositors’ Perspective. J. Islam. Mark. 2020, 11, 234–250. [Google Scholar] [CrossRef]

- Rosman, R.; Haron, R.; Othman, N.B.M. The Impact of ZakĀt Contribution on the Financial Performance of Islamic Banks in Malaysia. Al Shajarah J. Int. Inst. Islam. Thought Civiliz. ISTAC 2019, 2019, 1–21. [Google Scholar]

- Zain, N.R.M.; Mahadi, N.F.; Noor, A.M. The Potential in Reviving Waqf through Crowdfunding Technology: The Case Study of Thailand. Al Shajarah J. Int. Inst. Islam. Thought Civiliz. ISTAC 2019, 2019, 89–106. [Google Scholar]

- Aziz, M.R.A.; Harun, M.S.; Noor, M.N.M. Preliminary Study on Talent Enhancement Programme for Building Capacities and Talent in Islamic Finance. J. Eng. Appl. Sci. 2018, 13, 2073–2076. [Google Scholar] [CrossRef]

- Manaf, U.A.; Markom, R.; Mohd Ali, H.; Abdul Rahim Merican, R.M.; Hassim, J.Z.; Mohamad, N. The Development of Islamic Finance Alternative Dispute Resolution Framework in Malaysia. Int. Bus. Manag. 2014, 8, 68372. [Google Scholar] [CrossRef]

- Akoum, I.; Haron, A. Islamic Banking: Towards a Model of Corporate Governance. J. Glob. Bus. Adv. 2011, 4, 317–335. [Google Scholar] [CrossRef]

- Mirghani, M.; Mohammed, M.; Bhuiyan, A.B.; Siwar, C. Islamic Microcredit and Poverty Alleviation in the Muslim World: Prospects and Challenges. Aust. J. Basic Appl. Sci. 2011, 5, 620–626. [Google Scholar]

- Jan, A.A.; Lai, F.-W.; Tahir, M. Developing an Islamic Corporate Governance Framework to Examine Sustainability Performance in Islamic Banks and Financial Institutions. J. Clean. Prod. 2021, 315, 128099. [Google Scholar] [CrossRef]

- Tariq, F.; Umar, S. Arming the Other Half: Attaining Sustainability through Women with Microfinance. WIT Trans. Ecol. Environ. 2011, 155, 811–819. [Google Scholar] [CrossRef] [Green Version]

- Mustapha, Z.; Kunhibava, S.B.; Muneeza, A. Legal and Sharīʿah Non-Compliance Risks in Nigerian Islamic Finance Industry: A Review of the Literature. Int. J. Law Manag. 2021, 63, 275–299. [Google Scholar] [CrossRef]

- Abdullahi, S.I. Zakah as Tool for Social Cause Marketing and Corporate Charity: A Conceptual Study. J. Islam. Mark. 2019, 10, 191–207. [Google Scholar] [CrossRef]

- Atif, M.; Hassan, M.K.; Rabbani, M.R.; Khan, S. Islamic FinTech: The Digital Transformation Bringing Sustainability to Islamic Finance. In COVID-19 and Islamic Social Finance; Routledge: Abingdon, UK, 2021. [Google Scholar]

- Budalamah, L.H.; El-Kholei, A.O.; Al-Jayyousi, O.R. Harnessing Value-Based Financing for Achieving Sdgs: Social Innovation Model for Arab Municipalities. Arab. Gulf J. Sci. Res. 2019, 37, 1–19. [Google Scholar] [CrossRef]

- Ercanbrack, J.G. Islamic Financial Law and the Law of the United Arab Emirates: Disjuncture and the Necessity for Reform. Arab Law Q. 2019, 33, 152–178. [Google Scholar] [CrossRef]

- Alshaleel, M.K. Islamic Finance, Sustainable Development and Developing Countries: Linkages and Potential. In Corporate Social Responsibility in Developing and Emerging Markets: Institutions, Actors and Sustainable Development; Cambridge University Press: Cambridge, UK, 2019. [Google Scholar]

- Farooq, M.O. Islamic Finance and Debt Culture: Treading the Conventional Path? Int. J. Soc. Econ. 2015, 42, 1168–1195. [Google Scholar] [CrossRef]

- Yesuf, A.J.; Aassouli, D. Exploring Synergies and Performance Evaluation between Islamic Funds and Socially Responsible Investment (SRIs) in Light of the Sustainable Development Goals (SDGs). Heliyon 2020, 6, e04562. [Google Scholar] [CrossRef]

- Martín, J.C.; Orden-Cruz, C.; Zergane, S. Islamic Finance and Halal Tourism: An Unexplored Bridge for Smart Specialization. Sustainability 2020, 12, 5736. [Google Scholar] [CrossRef]

- Ray, R.; Kamal, R. Can South–South Cooperation Compete? The Development Bank of Latin America and the Islamic Development Bank. Dev. Chang. 2019, 50, 191–220. [Google Scholar] [CrossRef]

- Mohseni-Cheraghlou, A. Global Governance: Is There a Role for Islamic Economics and Finance? In Global Governance and Muslim Organizations; Palgrave Macmillan: London, UK, 2019. [Google Scholar]

- Nobi, K.; Singh, M. The Conceptual Framework of Sustainable Islamic Finance with Special Reference to Shariah Index in India. World Rev. Sci. Technol. Sustain. Dev. 2020, 16, 241–256. [Google Scholar] [CrossRef]

- Jawadi, F.; Jawadi, N.; Sener, P. The Convergence of Ethical Investment Business Models and Their Reliance on the Conventional US Investment Market. Appl. Econ. 2020, 52, 6265–6276. [Google Scholar] [CrossRef]

- Al Hallaq, S.S.; Ajlouni, M.M.; Al-Douri, A.S. The Role of Stock Market in Influencing Firms’ Investments in Jordan. Int. J. Ethics Syst. 2019, 35, 90–118. [Google Scholar] [CrossRef]

- Franzoni, S.; Allali, A.A. Principles of Islamic Finance and Principles of Corporate Social Responsibility: What Convergence? Sustainability 2018, 10, 637. [Google Scholar] [CrossRef] [Green Version]

- Piratti, M.; Cattelan, V. Islamic Green Finance: A New Path to Environmental Protection and Sustainable Development. In Islamic Social Finance: Entrepreneurship, Cooperation and the Sharing Economy; Routledge: London, UK, 2018. [Google Scholar]

- Alblooshi, F.S.A.K. FinTech in the United Arab Emirates: A General Introduction to the Main Aspects of Financial Technology. In Entrepreneurial Rise in the Middle East and North Africa: The Influence of Quadruple Helix on Technological Innovation; Emerald Publishing Ltd.: Bingley, UK, 2022. [Google Scholar]

- Khan, M.M. Developing a Conceptual Framework to Appraise the Corporate Social Responsibility Performance of Islamic Banking and Finance Institutions. Account. Public Interes. 2013, 13, 191–207. [Google Scholar] [CrossRef]

- Shaukat, M.; Madbouly, A. Assessing the Entrepreneurial Ecosystem of Oman and Discovering the Innate Suitability of Islamic Finance. In Contributions to Management Science; Springer: Berlin/Heidelberg, Germany, 2019. [Google Scholar]

- Kamal, R.; Ray, R. A Connected and Sustainable Future—Comparing Lessons from Southern-Led Regional Banks and Networks, Caf and the Islamic Development Bank Compared. In Southern-Led Development Finance: Solutions from the Global South; Palgrave Macmillan: London, UK, 2020. [Google Scholar]

- Maqbool, A. Islamic Systems Finance; McGraw Hill: Singapore, 2018; ISBN 9781351174817. [Google Scholar]

- Smyth, M. Islamic Finance in an Almost Postcrisis and Postrevolutionary World: As in Politics, All Islamic Finance Is Local. In Contemporary Islamic Finance: Innovations, Applications, and Best Practices; John Wiley & Sons Inc.: Hoboken, NJ, USA, 2013. [Google Scholar]

- Azman, S.M.M.S.; Ali, E.R.A.E. Islamic Social Finance and the Imperative for Social Impact Measurement. Al Shajarah J. Int. Inst. Islam. Thought Civiliz. ISTAC 2019, 2019, 43–68. [Google Scholar]

- Omar Farooq, M. Exploitation, Profit and the Riba-Interest Reductionism. Int. J. Islam. Middle East. Financ. Manag. 2012, 5, 292–320. [Google Scholar] [CrossRef]

- Murugiah, S. Sukuk Industry Could Benefit from Blockchain Technology, Says S&P Global Ratings. Available online: https://www.theedgemarkets.com/article/sukuk-industry-could-benefit-blockchain-technology-says-sp-global-ratings (accessed on 22 February 2022).

- Kunhibava, S.; Mustapha, Z.; Muneeza, A.; Sa’ad, A.A.; Karim, M.E. Ṣukūk on Blockchain: A Legal, Regulatory and Sharī’ah Review. ISRA Int. J. Islam. Financ. 2021, 13, 118–135. [Google Scholar] [CrossRef]

- Fanani, A.; Kuncoro, A.W.; Husni, A.B.M.; Wijayanti, E.A. The Contribution of Waqf on Poverty Alleviation through Digital Platforms: A Case of Indonesia. Shirkah J. Econ. Bus. 2021, 6, 246–261. [Google Scholar] [CrossRef]

- Junaidi, J. Halal-Friendly Tourism and Factors Influencing Halal Tourism. Manag. Sci. Lett. 2020, 10, 1755–1762. [Google Scholar] [CrossRef]

- Kovjanic, G. Islamic Tourism as a Factor of the Middle East Regional Development. Turizam 2014, 18, 33–43. [Google Scholar] [CrossRef] [Green Version]

- Gilat, A. “The Courage to Express Myself”: Muslim Women’s Narrative of Self-Empowerment and Personal Development through University Studies. Int. J. Educ. Dev. 2015, 45, 54–64. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Journal and Proceeding Name | No. of Articles |

|---|---|

| Accounting and the Public Interest | 1 |

| Advanced Strategies in Entrepreneurship, Education and Ecology | 1 |

| Al-Ihkam: Jurnal Hukum dan Pranata Sosial | 1 |

| Al-Shajarah 2019 (Special Issue Islamic Banking and Finance 2019) | 5 |

| Applied Economics | 1 |

| Arab Gulf Journal of Scientific Research | 1 |

| Arab Law Quarterly | 2 |

| Australian Journal of Basic and Applied Sciences | 1 |

| Banks and Bank Systems | 1 |

| Contemporary Islamic Finance: Innovations, Applications, and Best Practices | 1 |

| Corporate Social Responsibility in Developing and Emerging Markets: Institutions, Actors and Sustainable Development | 1 |

| Development and Change | 1 |

| Global Governance and Muslim Organizations | 2 |

| Estudios de Economia Aplicada | 1 |

| Global Journal Al-Thaqafah | 1 |

| Globalization and Development | 1 |

| Heliyon | 1 |

| Humanomics | 1 |

| International Business Management | 1 |

| International Journal of Environment and Sustainable Development | 1 |

| International Journal of Ethics and Systems | 1 |

| International Journal of Innovation, Creativity and Change | 1 |

| International Journal of Islamic and Middle Eastern Finance and Management | 1 |

| International Journal of Law and Management | 1 |

| International Journal of Social Economics | 1 |

| Investment In Startups And Small Business Financing | 1 |

| International Journal of Supply Chain Management | 1 |

| ISRA International Journal of Islamic Finance | 1 |

| Journal for Global Business Advancement | 1 |

| Journal of Cleaner Production | 2 |

| Journal of Engineering and Applied Sciences | 2 |

| Journal of Intelligent and Fuzzy Systems | 1 |

| Journal of Islamic Accounting and Business Research | 4 |

| Journal of Islamic Marketing | 2 |

| Journal of King Abdulaziz University, Islamic Economics | 3 |

| Jurnal Pengurusan | 1 |

| Middle East Journal of Scientific Research | 1 |

| Qualitative Research in Financial Markets | 2 |

| Renewable and Sustainable Energy Reviews | 1 |

| Research Journal of Applied Sciences | 1 |

| Southern-Led Development Finance: Solutions from the Global South | 1 |

| Sustainability | 4 |

| Sustainable Innovation and Impact | 1 |

| Thunderbird International Business Review | 1 |

| WIT Transactions on Ecology and the Environment | 1 |

| World Review of Science, Technology and Sustainable Development | 1 |

| Total | 65 |

| Country | No. Publications | Contributions |

|---|---|---|

| Kuwait | 2 | Islamic finance prioritizes human welfare and Maqasid al-Shariah sustainable development that avoids wealth gaps [7]. |

| Through the service of the Sukuk program, Islamic finance is in line with Maqasid al-Shariah which provides overall human welfare [19]. | ||

| Indonesia | 4 | The Islamic Banking Industry prioritizes social welfare objectives in banking services compared to commercial purposes [41]. |

| Islamic banking prioritizes funding in activities that are in accordance with Shariah [12]. | ||

| The waqf program provides social welfare development [42]. | ||

| Microfinance Islamic institutions require differentiation innovation to build marketing through human resources with an educational background in Islamic finance [43]. | ||

| Malaysia | 27 | The Islamic banking industry prioritizes social welfare objectives in banking services compared to commercial purposes [41]. |

| The Islamic banking industry in Malaysia positively impacts green banking growth [24]. | ||

| Zakat helps achieve SDGs in Kedah through funding related to SDGs [44]. | ||

| Blockchain technology can help the transparency of financial transactions in Islamic fintech [45]. | ||

| The Musyarakah-based Sukuk model helps to develop waqf assets that help humanity and social welfare [46]. | ||

| Investment in private equity that does not use a conventional leverage system is a good place to invest and is in accordance with Shariah, e.g., investing in startup companies [14]. | ||

| Islamic finance plays an important role in small financing because it prioritizes social welfare goals [47]. | ||

| The waqf program provides social welfare development [42]. | ||

| Amendments to Shariah-based regulations are important for Islamic financial practices [48]. | ||

| Sustainability practices in Islamic banking have a positive relationship with banking performance, management, and stakeholders [13]. | ||

| Sukuk, waqf, and zakat can help fund higher education in Nigeria [49]. | ||

| The relationship between Islamic financial financing programs and welfare sustainability through long-run investment is empirical [50]. | ||

| Compliant firms tend to be more financially sustainable [35]. | ||

| There is a lack of judicial support related to problems of Islamic financial practices [51]. | ||

| The unleveraged green investment trust (UGIT) model supports environmental sustainability and stability in Islamic financial institutions [25]. | ||

| There are factors outside of religion that encourage consumers to choose Islamic financial services [52]. | ||

| Companies that comply with Shariah principles prioritize financing prudence as an effort to resolve financial imbalances [20]. | ||

| Islamic finance has social benefits with a value-based intermediation (VBI) approach [21]. | ||

| Zakat, waqf, and ṣadaqah play a role in social development [53]. | ||

| Waqf innovations that are useful in social welfare can be achieved digitally through crowdfunding platform technology [54]. | ||

| Talent programs and human resource training are indispensable in the Islamic finance industry [55]. | ||

| Opportunities in the field of Islamic finance have great investment opportunities [17]. | ||

| Islamic social banks can play a role in reducing poverty and bringing conformity closer to Islamic principles [17]. | ||

| Alternative dispute resolution institutions in Malaysia complement the needs of Islamic law in Malaysia [56]. | ||

| There needs to be a corporate governance structure that handles profit/loss-sharing issues handled by banks [57]. | ||

| There is a need to modify financial services that are not in accordance with Shariah principles as the fulfillment of small financing [58]. | ||

| Pakistan | 4 | Increasing Islamic corporate governance in IBFIs helps improve social performance and sustainability [59]. |

| Islamic finance helps development through microfinance [60]. | ||

| Discussing the Islamic financial agenda in the framework of sustainable development is important [11]. | ||

| Microfinancing by Islamic finance institutions helps reduce poverty [8]. | ||

| Nigeria | 5 | There is a need for specific regulations related to governance and supervision of Shariah compliance in Islamic financial practices in Nigeria [61]. |

| Hilah principles are used in Islamic financial practices to avoid usury [18]. | ||

| Sustainability practices in Islamic banking have a positive relationship with banking performance, management, and stakeholders [13]. | ||

| Zakah is an Islamic financial instrument that helps promote consumption and social welfare [62]. | ||

| Sukuk, waqf, and zakat can help fund higher education in Nigeria [49]. | ||

| Saudi Arabia | 3 | Through the service of the Sukuk program, Islamic finance is in line with Maqasid al-Shariah, which provides overall human welfare [19]. |

| Islamic finance plays an important role in small financing because it prioritizes social welfare goals [47]. | ||

| Investment in private equity that does not use a conventional leverage system is a good place to invest and is in accordance with Shariah, e.g., investing in startup companies [14]. | ||

| United Kingdom | 7 | A strategy model in the development of Islamic fintech is presented [63]. |

| Islamic banking prioritizes funding in activities that are in accordance with Shariah [12]. | ||

| Waqf helps achieve SDGs as in Islamic law prioritizing social goals [64]. | ||

| The unleveraged green investment trust (UGIT) model supports environmental sustainability and stability in Islamic financial institutions [25]. | ||

| There are still gaps in Islamic law globally that vary across countries [65]. | ||

| Islamic finance is very much in line with the goals of the SDGs in terms of ideology and principles applied to financial instruments [66]. | ||

| Consumer credit considers the Islamic financial system related to debt to be biased and no different from conventional systems [67]. | ||

| Qatar | 4 | There is a lack of judicial support related to problems of Islamic financial practices [51]. |

| Islamic finance plays a role in reducing the financing gap that supports the achievement of SDGs [68]. | ||

| The use of blockchain can help the development of the halal industry by facilitating tracking the purchase of food raw materials [10]. | ||

| The unleveraged green investment trust (UGIT) model supports environmental sustainability and stability in Islamic financial institutions [25]. | ||

| Spain | 1 | Islamic finance is a driver of sustainable tourism [69]. |

| United States | 5 | There is a lack of judicial support related to problems of Islamic financial practices [51]. |

| Some respondents in the US community consider the risk-sharing system in Islamic finance to play a role in economic development [29]. | ||

| The Development Bank of Latin America (CAF) and the Islamic Development Bank (IsDB) play an important role in infrastructure development because of their emphasis on humanitarian and social welfare objectives [70]. | ||

| Islamic finance plays an important role in financial stability, promoting prosperity, reducing inequality, and improving environmental sustainability [71]. | ||

| Islamic finance helps development through microfinance [60]. | ||

| India | 3 | There is a need for diversification of special regulations for investment based on Islamic finance by the government [72]. |

| There is an empirical relationship between Islamic financing programs and welfare sustainability through long-term investment [50]. | ||

| A strategy model in the development of Islamic fintech is presented [63]. | ||

| Poland | 2 | Shariah conformity greatly affects financial imbalances because it relates to the prudence of funding selection [20]. |

| Compliant firms tend to be more financially sustainable [23]. | ||

| Brunei Darussalam | 3 | The Islamic banking industry in Malaysia has a positive impact on green banking growth [24]. |

| Islamic financial instruments, namely, waqf, zakat, and infaq, support social welfare, especially in fulfilling nutrition [6]. | ||

| The Al-Tawhidi concept can be used as an Islamic financial practice, along with contract and cash waqf as the source of funding in MFIs [22]. | ||

| France | 1 | Islamic finance investment and socially responsible investment (SRI) both have investment ethical values [73] |

| Jordan | 1 | Consideration of moral and material values provides more benefits in the investment industry [74]. |

| Italy | 2 | Islamic finance principles are the same as CSR principles [75]. |

| Islamic green finance contributes to sustainable environmental protection [76]. | ||

| United Arab Emirates | 2 | Islamic banking in the UAE has low-level CSR disclosures compared to conventional banking, but has no relationship with banking performance [16]. |

| Fintech helps Islamic finance in terms of Shariah compliance and helps sustainable development through green banking programs [77]. | ||

| Australia | 1 | CSR assessment of Islamic banking and finance institutions is not yet considered in accordance with Shariah [78]. |

| Oman | 1 | Islamic finance enhances the entrepreneurial ecosystem [79]. |

| Germany | 1 | Islamic green finance contributes to sustainable environmental protection [76]. |

| Undefined | 3 | There are financial imbalances in the Development Bank of Latin America (CAF) and the Islamic Development Bank (IsDB) as particular sources of funding [80]. |

| The Islamic investment model as a financing approach has a positive impact on humans and environmental sustainability [81]. | ||

| This research focuses on the Islamic political and financial environment [82]. |

| Topic | Objective of Islamic Law (Maqashid Al-Shariah) | Sustainable Development Goals (SDGs) | Related Articles |

|---|---|---|---|

| Islamic finance sustainability in general | Protection of faith, self or soul, intellect, posterity, and property | Goals: 01, 02, 03, 04, 05, 07, 08, 09, 10, 11, 12, 14, 16, and 17 | [6,7,8,9,10,11,12,13,14,15,16,17] |

| Compliance with Shariah | Protection of faith, self or soul, intellect, posterity, and property | Goals: 01, 02, 08, 09, 10, 11, and 17 | [18,19,20,21,22,23] |

| Consumer behavior | Protection of intellect and property | Goals: 08, 09, 11, and 16 | [29,52,67] |

| Financial technology | Protection of posterity and property | Goals: 01, 08, and 09 | [45,54] |

| Green banking | Protection of posterity | Goals: 01, 02, and 08 | [24,25] |

| halal industry | Protection of faith and posterity | Goals: 08, 09, 13, and 15 | [10,69] |

| Human resources and education | Protection of self or soul, intellect, and posterity | Goals: 04 and 10 | [55] |

| Islamic corporate governance | Protection of faith, intellect, posterity, and property | Goals: 01, 02, 11, and 16 | [48,51,56,61,83] |

| Philanthropy, corporate social responsibility, or ethics in the financial industry | Protection of self or soul, intellect, posterity, and property | Goals: 01, 02, 03, 04, 08, 09, 10, and 11 | [26,41,42,44,49,50,53,62,68,73,75,78,83] |

| Islamic finance innovation | Protection of faith, posterity, and property | Goals: 01, 02, 03, 04, 08, 09, 10, and 11 | [43,46,58,64,70,74] |

| Women empowerment | Protection of self or soul and intellect | Goals: 01, 05, 08, and 10 | [60] |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Harahap, B.; Risfandy, T.; Futri, I.N. Islamic Law, Islamic Finance, and Sustainable Development Goals: A Systematic Literature Review. Sustainability 2023, 15, 6626. https://doi.org/10.3390/su15086626

Harahap B, Risfandy T, Futri IN. Islamic Law, Islamic Finance, and Sustainable Development Goals: A Systematic Literature Review. Sustainability. 2023; 15(8):6626. https://doi.org/10.3390/su15086626

Chicago/Turabian StyleHarahap, Burhanudin, Tastaftiyan Risfandy, and Inas Nurfadia Futri. 2023. "Islamic Law, Islamic Finance, and Sustainable Development Goals: A Systematic Literature Review" Sustainability 15, no. 8: 6626. https://doi.org/10.3390/su15086626