1. Introduction

The sustainable development concept has made a significant adjustment to the activities of large national and international business structures [

1]. Many business actors implement CSR as a commitment from the company to behave ethically and play a role in economic development while improving the quality of life of its employees and their families, as well as the local and the wider community [

2]. According to Alexander Dahlsrud, CSR can be defined as a set of policies adopted voluntarily by companies to provide adequate contributions to society, to preserve the environment, and to maintain beneficial relationships with certain groups with interest [

3]. CSR could create long-term relationships that are beneficial and reliable between the parties involved in it [

4].

In developed countries, CSR is not positioned as a legal responsibility, but rather as a voluntary activity and is more focused on social or charitable activities. As in the United States, CSR is defined within the framework of a philanthropic model (voluntary driven) in which profit-generating companies donate a certain portion of their profits to charitable causes in the form of grants or donations [

5]. In Europe, CSR is focused on an operational model in which business actors are expected to act and be socially responsible.

Meanwhile, in developing countries where poverty is still an issue, CSR is positioned as a legal responsibility and is focused more on encouraging economic growth through community empowerment.

A number of studies have been conducted in several countries that still struggle with poverty to see the position and focus of CSR implementation. In India, the authorities enacted a regulation that requires large companies to spend 2% (two percent) of their net profit on priority issues such as poverty alleviation, improvement of public facilities, and environmental sustainability [

6]. In Africa, where unemployment and poverty are still an issue, the focus of CSR rests on how to help African communities and institutions, especially local communities, in encouraging economic growth and development [

7]. Just as in India and Africa, CSR in Indonesia falls under legal responsibility and is focused more on encouraging economic growth in the context of poverty alleviation, job creation, and boosting the business capacity of micro, small, and medium enterprises (MSMEs). The government stipulates that companies fall within certain categories, such as LLCs engaged in the sector of natural resources and state-owned enterprises (SOEs), and are required to perform social and environmental responsibilities. Setting CSR as a legal responsibility is a current phenomenon around the developing world today, as an effort made by the government to pursue a unique combination of hard and soft laws aimed at sharing the responsibility for providing and maintaining a welfare state with the business actors [

8].

CSR as a legal responsibility is one of the four interrelated aspects of CSR as a responsibility, which consist of economic responsibility, ethical responsibility, philanthropic responsibility, and legal responsibility. Archie B. Carroll developed this social responsibility concept in 1979 [

9]. Apart from being an economic, ethical, philanthropic, and legal responsibility, CSR can also create business continuity within the company. This is in line with Elkington’s opinion, which believes that if companies want to be sustainable, it must pay attention to the “3Ps”, which in addition to pursuing profit must also pay attention to and be involved in fulfilling the welfare of society (people) and actively contribute to preserving the environment (planet) [

9]. Many companies have re-arranged certain schemes to implement the “3Ps” so that the companies are not only concerned with the profit of the business sector itself, with the hope of maintaining the business in both the medium and long term [

10].

Raising awareness and insight concerning CSR initiatives has encouraged CSR to become a competitive strategy among companies [

11]. The use of CSR as the strategy in determining organizational goals is considered crucial to boost the corporate image and profitability by recognizing the need and significance of CSR in order to create business sustainability [

12]. Business continuity achieved through the implementation of CSR can have an impact on both the implementing subjects and the implementing objects of CSR. Companies, as the implementing subjects of CSR, will benefit from business continuity by preserving resources and obtaining a positive image from the society. While the implementing objects, such as MSMEs, will benefit from business continuity through the provision of financial aid, product promotion, soft skills development, and training in management by the companies implementing CSR.

CSR that has an impact on the implementing subjects is viewed as having an internal dimension, while CSR that has an impact on the implementing objects is viewed as having an external dimension. The external dimension of CSR refers to the behavior of organizational social responsibility towards parties outside the company, while the internal dimension refers to the behavior of organizational social responsibility towards parties within the company, in this case, its employees or its subsidiaries. CSR can be implemented not only by companies in the form of LLCs or SOEs but also by other forms of business entities, such as cooperatives. However, the current various applicable regulations in Indonesia only accommodate the implementation of CSR by companies in the form of LLCs and SOEs and rather more focus on the external dimension of CSR implementation by empowering the community to create sustainable businesses in smaller business entities.

Cooperatives’ role in the CSR implementation in Indonesia is only viewed as the implementing objects by the large companies in the form of LLCs and SOEs, but they are not encouraged to implement the CSR itself, which is known as CoopSR. As a result, even though cooperatives are the type of companies that are directly committed to sustainable development because it has two main characteristics, namely economic and social [

13], they become dependent on CSR programs and cannot play a more active role in sustainable development. The economic characteristics of cooperatives can be seen from the main purpose of cooperatives themselves, that is to generate economic results (surplus) to be distributed among their members according to patronage, whereas their social characteristics can be seen from their particular economic benefits, one of which is to serve the less fortunate [

14]. Furthermore, there is a strategic plan for cooperatives until 2030 called “A People-Centred Path for a Second Cooperative Decade” that consists of four pillars, one of which is the contribution of cooperatives to sustainable development [

15].

This article aims to analyze the contribution of CSR to sustainable development and the response of regulations concerning social responsibility in Indonesia toward creating sustainable businesses. This article also aims to analyze the institutional nature of cooperatives and establish a policy model for implementing CSR and CoopSR to create a sustainable business in cooperatives. Finally, this article also aims to determine the characteristics of CSR performed by cooperatives based on their identity, thus generally to find the fundamental differences between such CSR and the CSR performed by the companies.

3. Literature Review

CSR is the commitment of business actors to sustainable economic development by taking into account the balance between the economic, social, and environmental aspects of their businesses [

16]. Howard Rothmann Bowen first introduced modern CSR in 1953 through the publication of the book titled “Social Responsibility of the Businessmen” [

17]. Formerly, CSR was known merely as a social responsibility and the word corporate did not yet exist because the company’s influence and dominance over the business world were not yet significant. Social responsibility is defined as the obligation of businesses to pursue those policies, to make those decisions, or to follow those lines of action, which are desirable in terms of the objectives, and values of our society [

18].

In its development, the definition of CSR has varied greatly from time to time. Previously, CSR was limitedly defined as a voluntary company activity, and as defined by John Elkington, CSR is a voluntary action that businesses can take over and above compliance with minimum requirements [

19]. CSR refers to a company’s orientation and attitude to integrate social and environmental concerns into its strategy voluntarily, and at the same time, to ensure the company’s economic realization [

20]. However, presently, apart from being defined as a philanthropic responsibility, CSR is also defined as an economic, ethical, and legal responsibility, as stated by Archie B. Carroll.

CSR as a concept is a form of implementing sustainable development. This is in line with its definition according to the World Business Council for Sustainable Development (WBCSD), which states that CSR is an ongoing commitment by the business world to act ethically and contribute to the economic development of the local community or society, along with improving the standard of living of its employees and their whole family. Meanwhile, the International Organization for Standardization in the ISO 26000 Social Responsibility Guidance Standard defines CSR as the responsibility of an organization for the impact of decisions that are manifested in the form of transparent and ethical behavior that is in line with sustainable development and community welfare.

Fortunately, sustainable development has become a universal concept to be the basis of development programs in any country throughout the world [

21]. Sustainable development is a concept that aims to provide long-term global life through wiser use and management of the economy and natural resources while respecting the lives of people and other living things. According to Pim Martens, simple sustainable development is to meet the basic needs of humanity without committing violence against the natural systems of life on Earth [

22]. The essence of sustainable development is a development that meets the needs of the present without compromising the ability of future generations to meet their own needs [

23].

The term sustainable development first appeared in 1980 in the World Conservation Strategy from the International Union for the Conservation of Nature (IUCN), then in 1981, Lester R. Brown used it in the book titled “Building a Sustainable Society” [

24]. Furthermore, in 1992, a UN conference called the “Earth Summit” was held, which resulted in the “Rio Declaration” containing 27 points of guidance for countries in the world to implement sustainable development [

25]. Five years later, in 1997, the principles of the Rio de Janeiro declaration were adopted in the Kyoto Protocol and a list of sustainable development goals was made by the United Nations in the 2030 Agenda [

13]. All of those sustainable development agendas have one common essence it trying to emphasize, that economic, social, and environmental development are an integral and inseparable part of sustainable development itself.

John Elkington introduced the concept of a sustainable company in his book titled “Cannibals with Forks: The Triple Bottom Line of 21st Century Business in 1997” [

26]. There are three keys to a sustainable company that cannot be separated from one another, namely economic, social, and environmental aspects [

26]. To achieve sustainability, a company must effectively balance the creation of economic value with its concern for social and environmental issues [

27]. This triple-bottom-line framework introduced by John Elkington has been embraced by a wider audience [

28] and implemented in the CSR program.

Sustainable development and CSR are two things that are integral and inseparable. The three important aspects of sustainable development; namely economic, social, and environmental; are another form of the triple bottom line concept; namely profit, people, and planet; which forms the basis of CSR. The concept of the triple bottom line requires that, in addition to seeking profits, companies must also be socially responsible and take into account their impact on the environment. Those three concepts of the triple bottom line must work synergistically and continuously in order to create a good corporate climate so that the companies’ existence is guaranteed by a positive image or reputation obtained from consumers and society.

The implementation of the triple bottom line model is indicated by economic growth, environmental services, and social improvement, which overlapped with one another. Firstly, economic growth and environmental services overlap with the efficiency of economic and resources. Secondly, economic growth and social improvement overlap with socioeconomic growth. Thirdly, environmental service and social improvement overlap with social–environmental improvement. All of these indicators support each other and intersect to achieve sustainable business activities.

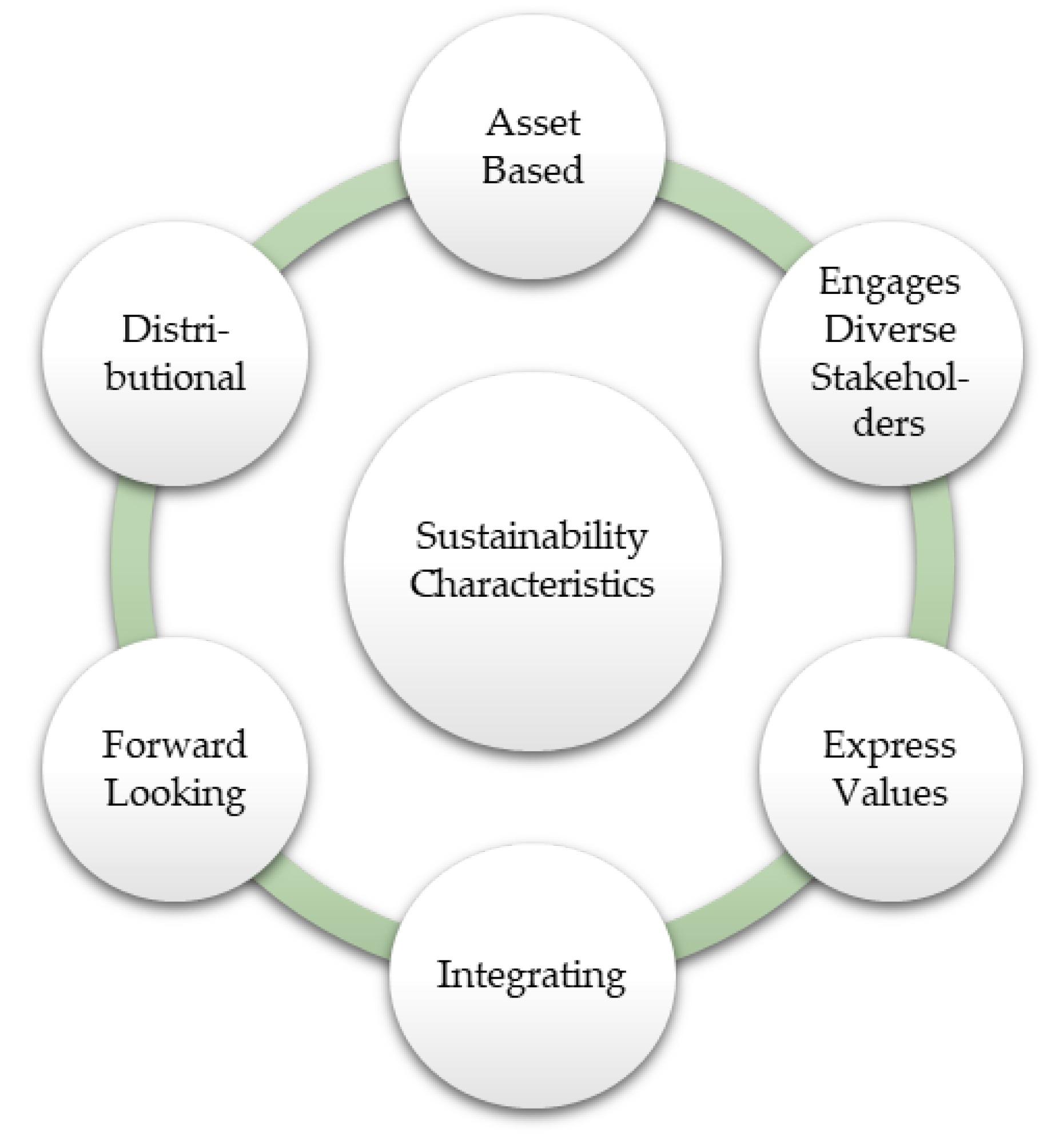

Figure 1 shows six main characteristics in the definition of sustainability, namely asset-based, engages diverse stakeholders, express values, integrating, forward looking, and distributional [

29].

First, asset-based, starting by taking into account the existing assets and then emphasizing their deficiencies. Second, engages diverse stakeholders, by involving stakeholders from various groups based on the principles of mutual respect, cooperation, flexibility, and openness. Third, express values, by expressing values that have been formally adopted by local residents. Fourth, integrating, by explaining the relationship between issues. Fifth, forward looking, by focusing on long-term future changes. Sixth, distributional, by working with an appropriate distribution of resources and welfare, not only for the current generation but also for future generations.

With the existence of CSR as one of the implementations of sustainable development and as a form of the triple bottom-line concept, companies must also prioritize sustainability in addition to profitability. The company should not solely be a self-centered profit-seeking entity, but its actions should also form an integral part of the economy, society, and environment in which it exists [

30]. The concept of sustainability in CSR is closely related to acceptability. To be able to conduct business in the long term, companies must be sustainable and accepted by their societies.

CSR is also related closely to the goal of achieving sustainable economic activity itself, due to the use of sustainable development concepts that will have long-term effects for the company itself. Companies that combine social issues and business activities are more likely to gain competitive advantages that create value for the business, their chosen customers, and society [

31]. CSR will bring improvements to what has been carried out and will also positively impact the company’s image in the eyes of society in the future, which will serve as an investment concept to develop the capacity of the community as a whole for the sake of sustainable development (sustainability) that can improve the quality of life of the community [

32].

4. Results and Discussions

4.1. Cooperatives and Social Responsibility for Sustainable Development in Indonesia

Cooperatives, according to the International Cooperative Alliance (ICA), are autonomous associations of persons united voluntarily to meet common economic, social, and cultural needs and aspirations through mutually owned and democratically controlled enterprises. In Indonesia, cooperatives are narrowly defined only as legal entities, specifically as business entities, consisting of individuals or cooperative legal entities with activities based on cooperative principles as well as a people’s economic movement based on the principle of kinship, as stipulated in Article 1 Number (1) of Law No. 25 of 1992 concerning Cooperatives (Indonesian Cooperative Law).

The number of cooperatives in Indonesia is one of the largest in the world. Based on data from the Ministry of Cooperatives and Small and Medium Enterprises of the Republic of Indonesia in 2021, the number of active cooperatives is up to 127,846 units. Such a large number is also followed by a growth in terms of the number of members.

Table 1 below shows that in Indonesia, the number of cooperative members has increased significantly in the last five years, and it has increased almost by around 2,000,000–3,000,000 members per year. The most significant increase occurred in 2020, where there was an increase of almost 3,000,000 to 25,098,807 members compared to 2019, which only had 22,463,738 members. In 2021, the number of cooperative members nationally reached 27,100,372 members. The data below also show that the cooperatives in Indonesia have a considerable amount of capital, both from their own capital and other external sources of funds, which in 2021 reached IDR 196.27 trillion. It followed by an increase in the total assets of IDR 250.98 trillion and in the total revenue of IDR 182.35 trillion in the same year.

Cooperatives are business entities that are most compatible with the economic system in Indonesia. The 1945 Indonesian Constitution stipulates that the Indonesian economy must be structured as a common effort based on the principle of kinship and organized based on economic democracy. The constitutional message incorporated in the 1945 Indonesian Constitution shows that the intention of the constitution is indeed a certain economic system, which is not a capitalistic economy (based on individualism), but an economic system based on common effort and the principle of kinship [

34], which in concert form a cooperative [

35].

As business entities based on common effort and the principle of kinship, cooperatives in Indonesia are viewed as small-scale business entities originating from the people, by the people, and for the people. Cooperatives may also be recognized in the form of a gathering place for MSMEs, meaning that the cooperatives’ members consist of several MSMEs. In Indonesia, most business actors are considered MSMEs. Based on data from Statistics Indonesia (BPS), out of 59,693,791 business units in Indonesia, 99.89 percent of them consist of MSMEs [

36]. Large corporations often use such cooperatives as the implementing object of philanthropic programs or community empowerment. One of the philanthropic or empowerment programs aimed at cooperatives is CSR performed by LLCs and SOEs. Although CSR is a very broad concept with no clear boundaries [

37], it can be interpreted as a comprehensive idea that considers economic, social, and environmental issues and, at the same time, protects the interests of all stakeholders by requiring greater transparency so that one of the implementations of CSR can be for the empowerment of cooperatives [

30].

The implementation of CSR can be divided into six models, namely, cause promotion, caused-related marketing, corporate social marketing, corporate philanthropy, community volunteering, socially responsible business practices, as shown in

Figure 2 below [

5].

The first model, cause promotion, is a program in the form of contributing funds or fundraising to increase awareness of certain social issues. The second model is caused-related marketing, a program in which a company contributes by setting aside a fraction of a percent of revenue as a donation for certain social issues or certain products. The third model, corporate social marketing, is a model in which the company assists the development and implementation of campaigns with a focus on changing certain behaviors that have a negative influence. Fourth, corporate philanthropy is a company initiative program making a direct contribution to charity. The fifth model, community volunteering, is a program to provide assistance and encouragement to employees and business partners to voluntarily become involved and assist the local community. Lastly, socially responsible business practices is an initiative in which the company adopts and implements certain business practices and investments that are shown to improve community quality and protect the environment.

From those six models above, the model relevant to empower the cooperatives is the socially responsible business practices model. The improvement of the community’s quality in the socially responsible business practices model includes its employees, suppliers, distributors, and non-profit organizations serving as partners of the company, MSMEs, and society in general. Cooperatives are included in the criteria for MSMEs originating from the communities in the society. Actions taken by the companies implementing CSR with socially responsible business practices models for cooperatives can be in the form of cooperation that can support the development of cooperatives. In addition, companies can also create new business opportunities and increase the capacity of cooperatives through their resources.

The CSR practices conducted in Indonesia are generally divided into three models: grants, environmental restoration, and community development. The implementation of CSR in the form of grants is a program that is given free of charge without expecting reciprocity from the recipient. The program can be in the form of educational aid such as scholarships, improvement of health facilities or capacity, natural disaster aid, charity, and development of public facilities or infrastructure. CSR in the form of environmental restoration is conducted by a series of company obligations to assume responsibility for survivors whose rights to a good and healthy environment have been violated. Companies whose business activities pollute the environment are required to carry out the environmental restoration. The program can be in the form of post-exploitation environmental restoration, tree planting, and environmental cleaning, such as rivers and beach cleaning. Furthermore, CSR in the form of community development is a productive and sustainable program. In community development, there is a collaboration of common interests between the company and the community; those are participation, productivity, and sustainability. The implementation of community development aims to increase the capacity of micro and small businesses, as well as cooperatives, by providing financial aid, promoting products, increasing soft skills, and providing training in management. The CSR program in the form of community development is the most widely implemented CSR program for the reason that it is directly more profitable from the perspective of the company implementing CSR.

In Indonesia, since the applicable laws only require the LLCs engaging in natural resources and SOEs to perform CSR, CSR is generally performed by such companies. However, the authors believe that all stakeholders, including cooperatives, should also be encouraged to perform CSR as one of the efforts to create sustainable development. Even though it has practically been performed by some cooperatives, the number is still insignificant and it is not performed in compliance with the values and principles of cooperatives.

The authors believe that cooperatives in Indonesia need to be encouraged to participate in sustainable development. As hybrid organizations, cooperatives have dual characteristics, namely as a company and an association of members [

38]. Not only are they positioned as associations of ordinary members, but they are also positioned as collectivities due to common needs and goals among the members [

39]. With these dual characteristics, cooperatives serve as both economic and social entities to meet the interests of their members.

Cooperatives are social capital-based organizations and their social foundation has been recognized as the main comparative advantage compared to other business entities [

40]. As an organization based on social capital, it serves as a hybrid entity that combines the characteristics of ordinary business and non-profit organizations. The combination of characteristics between business and not-for-profit leads to a different cooperative management orientation compared to the typical mono-identity of business and non-profit entities [

41].

In terms of the sustainable development agenda, the authors believe that cooperatives cannot be separated from the attempts to solve present social issues, since cooperatives are directly committed to sustainable development by having both economic and social characteristics [

42]. Their economic characteristics can be seen from their main purpose, which is to achieve economic results (surplus) distributed among their members according to patronage, while their social characteristics can be seen from their economic benefits, one of which is to serve the less fortunate [

14]. Those characteristics cause the cooperatives to be business entities that must create sustainable business and development. Cooperatives can be sustainable if they become economically viable businesses that fully implement the seven cooperative principles and maintain or regenerate the ecosystem in which the cooperative exists. The cooperatives’ business model is based on ethics, values, and principles that put the needs and aspirations of their members above the simple goal of maximizing profits. Through community empowerment and concern for people’s welfare, the cooperatives have nurtured a long-term vision for sustainable economic growth, social development, and environmental responsibility.

Furthermore, the first blueprint revision of “A People-Centred Path for a Second Cooperative Decade” consists of a cooperative strategic plan until 2030. There are several pillars or strategic plans for cooperatives going forward, including the promotion of cooperative identity; the growth of the cooperative movement; cooperation between cooperatives; and the contribution of cooperatives to sustainable development [

15]. One of the pillars of cooperatives going forward is the contribution of cooperatives to sustainable development, by encouraging cooperatives to be able to apply sustainable principles covering the triple bottom line (economic, social, and environmental) in order to achieve the United Nations (UN) sustainable development agenda in 2030.

4.2. Legal Perspective to Solve Issues in Corporate Social Responsibility Regulations

Implementation of the CSR program is intended to achieve sustainable development in the economic system. CSR was for a long time initially restricted to economics, business management, sociology, and (in part) political science [

43]. A large amount of research was therefore dedicated to the relationship between CSR and firm performance [

44]. It was not until recently that these issues have become more popular in law and legal studies [

45]. CSR is a subject that has links with many areas of law, including corporate law and corporate governance [

46]. Such a legal dimension of CSR states that every organization that implements CSR must be based on certain legal standards and criteria [

47].

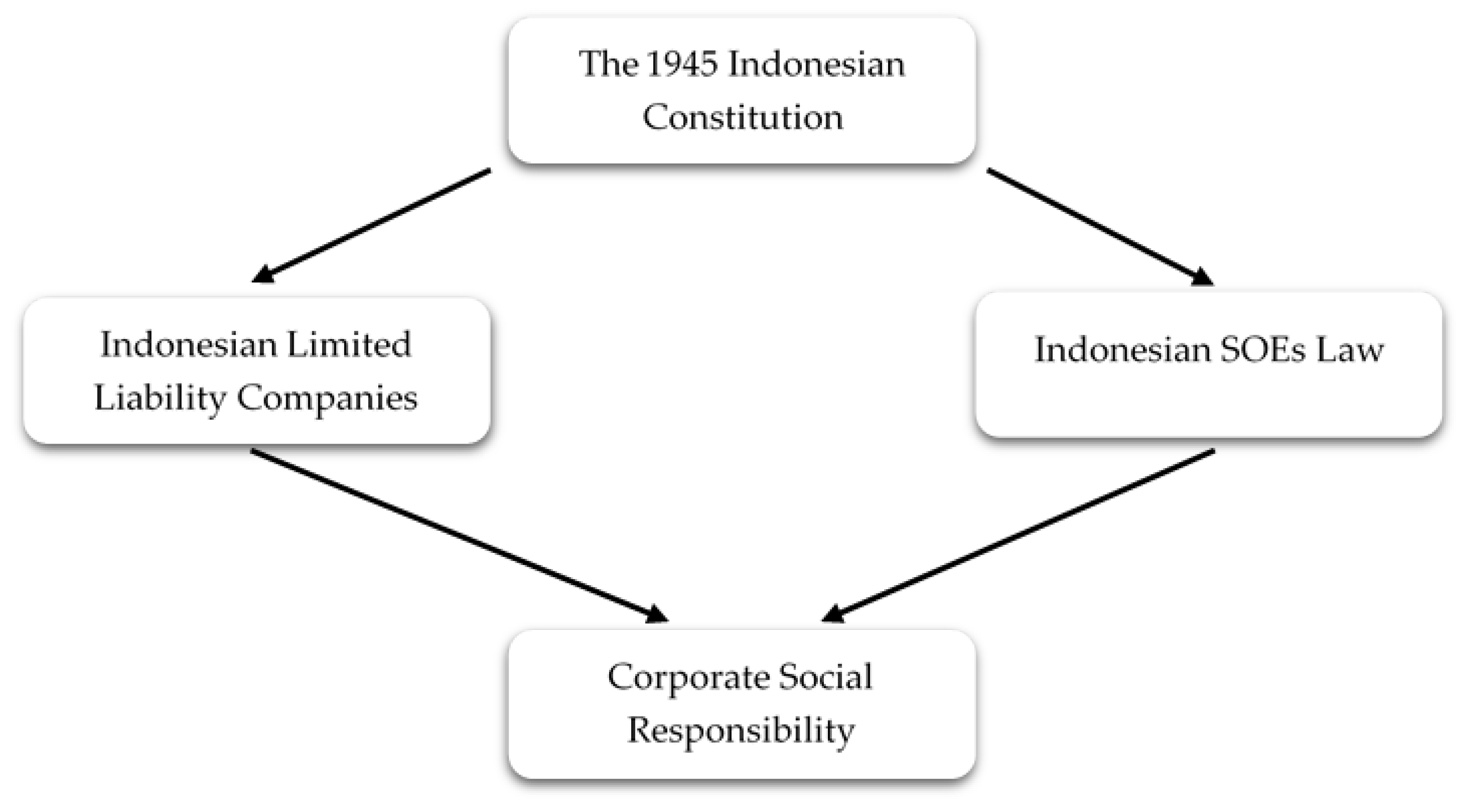

In Indonesia, the sustainable development policy as the main basis of CSR regulations is stipulated in the 1945 Indonesian Constitution. Article 33 paragraph (4) of the 1945 Indonesian Constitution mandates that the national economy is organized based on economic democracy with the principles of togetherness, efficiency with justice, sustainability, environmental insight, and independence, as well as by maintaining a balance of progress and national economic unity. The principles of sustainability and environmental insight in the 1945 Indonesian Constitution serve as a basis from which the implementation of the economy in Indonesia must accomplish sustainable development.

The legal framework for CSR as a form of sustainable development in the economy is not specifically stipulated in one area of law, but is spread over several regulations instead, as shown in

Figure 3. CSR are stipulated in regulations concerning the company according to the type of company. For LLCs, it is specified in Law No. 40 of 2007 on Limited Liability Companies (Indonesian Limited Liability Companies Law) and its implementing regulation, Government Regulation No. 47 of 2012 on Social and Environmental Responsibility of Limited Liability Companies. For SOEs, CSR implementation is specified in Law No. 19 of 2003 on State-Owned Enterprises (Indonesian SOEs Law) and its implementing regulation, namely the Minister of State-Owned Enterprises Regulation No. PER-02/MBU/04/2020 of 2020 on Partnership Programs and Community Development Programs for State-Owned Enterprises.

CSR performed by LLCs in Indonesia is known as social and environmental responsibility, which is the company’s commitment to participate in sustainable economic development in order to improve the quality of life and the environment that is beneficial for the company itself, the local community, and society in general. The purpose of doing so is intended to support the creation of a harmonious and balanced relationship of the company in accordance with the environment, values, norms, and culture of the local community.

In principle, LLCs in various fields are able to perform social and environmental responsibility. However, only the company having business in the field of and/or related to natural resources is obliged to perform such responsibility. It also must be budgeted for and calculated as the company’s costs that are carried out with due observance of decency and fairness. It is performed by the Board of Directors based on the company’s annual plan once it secures approval from the Board of Commissioners or the General Meeting of Shareholders (GMS), in accordance with the company’s articles of association. It must also be included in the company’s annual report and accounted for at the GMS. Should the company having business in the field of and/or related to natural resources fails to perform its obligation to conduct social and environmental responsibility, it will be subject to sanctions in accordance with the applicable laws and regulations.

Furthermore, CSR performed by SOEs in Indonesia is known as Partnership Program and Community Development Program, as specified in Indonesian SOEs Law and its implementing regulations. Pursuant to Article 88 Paragraph (1) of Indonesian SOEs Law, SOEs may set aside a portion of their net profits to foster small businesses or cooperatives as well as developing communities around the SOEs. The partnership program is implemented by SOEs to improve the ability of small businesses, including cooperatives, to become resilient and independent, while the environmental development program is implemented to empower the social circumstances of the community.

SOEs in the form of public companies and LLCs are required to perform partnership and environmental development programs. The source of funds for implementing such a program comes from the provision of a portion of the net profit of the SOEs and/or the budget that is calculated as SOEs’ expenses. The amount of funds allocated is a maximum of 4% of the previous year’s projected net profit, which is determined at the time of ratification of the annual report.

Partnership and community development programs are projected toward small businesses, cooperatives, or communities in the form of loans to finance working capital and/or the purchase of fixed assets in order to increase production and sales. It is also conducted in the form of coaching through education, training, apprenticeship, marketing, promotion, and other matters related to increasing the productivity of small businesses and cooperatives. A special unit formed within SOEs named the partnership and environmental development program unit implements this program.

As previously mentioned, cooperatives are viewed as objects of CSR implemented by LLCs and SOEs, both in terms of implementations and regulations. Regulations concerning CSR, derived from the sustainable development provisions in the 1945 Indonesian Constitution, are explicitly mentioned in the relevant regulations concerning business entities. As for the cooperative, its regulation, namely Indonesian Cooperative Law, does not specify obligations regarding social and environmental responsibility. Thus, the authors believe, this is the main reason cooperatives do not perform such social and environmental responsibility.

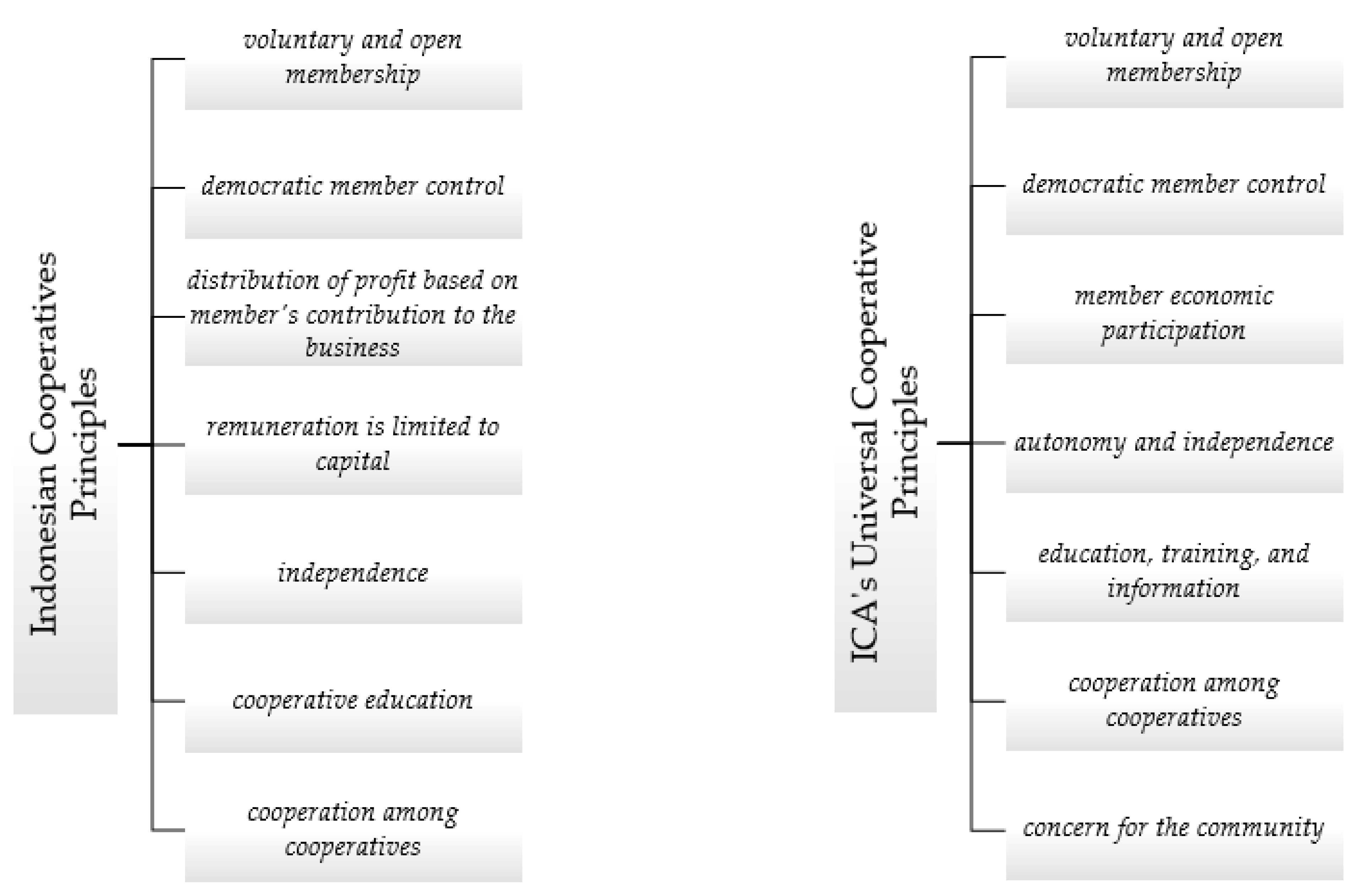

Indonesian Cooperative Law does not mention anything regarding concern for the community as the value and principle of cooperatives. According to ICA, cooperatives have universal values that consist of self-help, self-responsibility, democracy, equality, equity, and solidarity. Cooperative members also believe in ethical values, including honesty, openness, social responsibility, and caring for others as a tradition of their founders. Their values that are directly related to sustainable development are social responsibility and caring for others.

Social responsibility as a cooperative value serves as a commitment to contribute to sustainable development that lies beyond the boundaries of cooperatives as an economic entity. It causes cooperatives to make continuous improvements to the conditions around their environment. Negative consequences in society resulting from or stemming from the actions or operations of cooperatives must be reversed. In addition, cooperatives must also be responsible for contributing to the welfare of society and the environment.

Caring for others as a cooperative value serves as an obligation to its members, each of its units, and its movement as a whole to act in either such a way as not to cause harm or inconvenience to others, now or in the future. It reflects the tolerance of the parties involved in the cooperative towards other people. It is a basic value to be practiced in cooperatives to create good relations between their members and the public outside of the cooperatives.

Those cooperative values, particularly social responsibility and caring for others, need to be incorporated into the applicable laws and regulations in Indonesia so that cooperatives can play a more active role in sustainable development. Those are very important for cooperatives to conduct their operational activities. Hence, to make cooperatives conduct social and environmental responsibilities, the basis for such responsibilities shall be created in the form of cooperative values. Furthermore, the legal issue of why the cooperatives in Indonesia are not encouraged to perform social and environmental responsibilities is because there are fundamental differences between the cooperative principles stipulated in the Indonesian Cooperative Law with the universal cooperative principles issued by the ICA, as shown in

Figure 4.

The principle of universal cooperatives that does not exist in the Indonesian Cooperative Law is the principle of concern for the community, which means that cooperatives operate for the sustainable development of their communities through policies approved by their members. This principle is a combination of two elements of cooperative values, self-help and self-responsibility, as well as the ethical values of honesty, openness, social responsibility, and concern for others. It arises because of the cooperatives’ existence and roots in the community where they conduct their business activities. The scope of the principle of concern for the community includes concern for the cooperative movement for sustainable economic, environmental, and social development that benefits the community and cooperative members.

It is necessary to amend the regulation concerning the cooperative principle in Indonesian Cooperative Law so that it accommodates the principle of concern for the community. Cooperative principles are important to adapt to universal development because they are one unit and cannot be separated in cooperative existence. Its principle is the essence of the basic work of cooperatives as business entities and is a characteristic and identity of cooperatives that distinguishes them from other business entities. By implementing all of these principles, cooperatives manifest themselves as business entities as well as people’s economic movements that are social in nature and participate in sustainable development.

4.3. CSR and CoopSR Implementation Policy Strategy in Creating a Sustainable Business in Cooperatives

CSR is the implementation of the triple bottom line concept to create development and a sustainable company. The concept of the triple bottom line consisting of profit, people, and planet is a derivative of the concept of sustainable development and is a key dimension of the concept of a sustainable company. The concept of the triple bottom line was introduced due to the awareness of the business world that companies are no longer faced with responsibilities that are based on a single bottom line, namely corporate value, which is reflected only in its financial condition, but also the responsibilities to pay attention to social and environmental aspects [

2]. Companies that run their businesses are not justified in pursuing profit alone (profit), but they must also be involved in fulfilling the welfare of society (people) and actively participate in preserving the environment (planet).

The regulation and implementation of CSR in Indonesia are currently more supportive for LLCs and SOEs, while it has not been regulated and directed for other forms of companies such as cooperatives. Cooperatives are only positioned as objects of CSR programs just as with MSMEs. In principle, cooperatives as the implementing objects of the CSR itself have a certain advantage, since they can develop their business with the help of the CSR program. On the other hand, CSR performed by cooperatives also needs to be regulated and directed, specifically concerning social and environmental responsibility where cooperatives have also contributed to environmental pollution [

48] and must play a role in sustainable development so that the business continues to exist.

The strategy that can be implemented to optimize the current implementation of CSR, especially to create a sustainable business in cooperatives, is to combine CSR in the form of community development and CSR performed by cooperatives. CSR, which is currently being performed by LLCs and SOEs, has been directed to develop cooperative businesses in the form of community development. Contrariwise, these companies also perform other CSR programs such as grants and environmental restoration, which are usually conducted separately from the community development program. Therefore, it is necessary to encourage the implementation of grants and restoration to involve parties in community development, one of which is cooperatives. In addition, community development programs for cooperative development can be performed by providing financial aid, promoting products, increasing soft skills, and providing training in management.

The next strategy, besides encouraging the implementation of CSR by LLCs and SOEs in the form of community development, is also needed to encourage cooperatives to perform social and environmental responsibility, better known as CoopSR. The social responsibility practices have been performed by every type of company and in many ways [

49], including by cooperatives. The term CoopSR was first introduced by Develtere [

50] and Harris [

51] in 2005. CoopSR is the application of cooperative values and principles in cooperative strategies with a focus on sustainable entrepreneurship in cooperatives [

52]. In Indonesia, the term CoopSR is still not well known by either cooperative management or society in general. Even though several large-scale cooperatives have already performed social responsibility, their implementation does not refer to the values and principles that exist in cooperatives.

The problem of not implementing CoopSR in Indonesia is caused by inadequate regulations. There are no cooperative values and principles regarding social responsibility in Indonesian Cooperative Law, despite the importance of the social responsibility performed by the companies, including cooperatives, to boost the organizational performance and develop corporate governance [

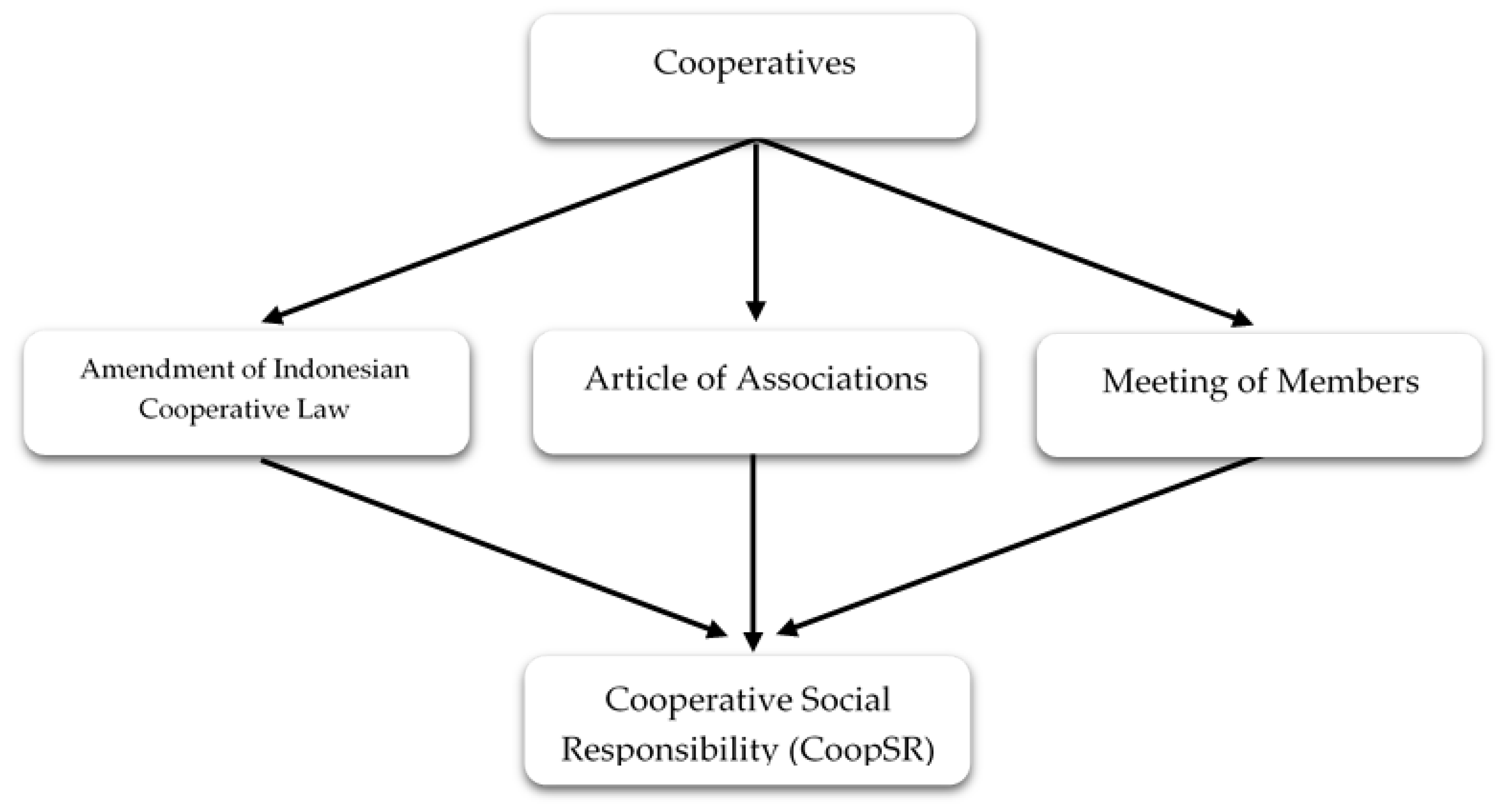

53]. Therefore, in order to encourage the implementation of CoopSR by cooperatives in Indonesia, it is necessary to amend the current Indonesian Cooperative Law. In addition, the policy strategy so that CoopSR is implemented can also be accommodated in the cooperatives’ articles of association and decided in its general meeting of members, as shown in

Figure 5.

First, in order to implement CoopSR, an amendment to the Indonesian Cooperative Law is required. The current regulation is considered ancient and outdated since it was enacted in 1992. Many new things in cooperative businesses have not been accommodated, one of which is related to the development of cooperatives’ values and principles. In 2022, the Indonesian Cooperative Law has been amended through the enactment of Government Regulation in Lieu of Law No. 2 of 2022 on Job Creation. However, such government regulation does not touch the basic things that exist in cooperatives today, namely the values and principles of the cooperatives.

Among the external factors, legal means play a vital role in contributing to the success of every business throughout the world, including in CSR implementation by various business entities [

54]. Reform of the regulation related to cooperatives needs to include the values that exist in cooperatives. The values underlying cooperative activities can consist of self-help, self-responsibility, democracy, equality, equity, solidarity, honesty, openness, social responsibility, and caring for others. The values of cooperatives that are directly related to CoopSR as a form of sustainable development are social responsibility and caring for others.

As previously explained, there are differences in cooperative principles in Indonesian Cooperative Law with universal cooperative principles, since Indonesian Cooperative Law does not stipulate principles regarding concern for the community, even though it is the basis of CoopSR implementation by cooperatives. In addition, there are differences between the principle of independence and the principle of autonomy and independence as stipulated by the ICA, as well as the differences between the principle of education in Indonesian Cooperative Law with the principle of education, training, and information issued by ICA. Regulations need to be updated to accommodate the development of cooperative principles, one of which is related to concern for the community.

Secondly, the strategy to enable the performance of CoopSR by cooperatives is to include such a commitment in the articles of association, as a must-have book for companies that serve as a direction for the companies themselves [

55]. The articles of association also serve as a guideline, which contains rules for all members to conduct any activities. It contains all general rules relating to the company’s day-to-day operations that will regulate the relationship between the company and its members so that it can run the company in a more orderly manner.

According to Articles 7 and 8 of the Indonesian Cooperative Law, each cooperative is required to have an article of association in the phase of formation that is incorporated into its deed of establishment. The article of association shall include at least a list of founders’ names; name and place of domicile; aims and objectives as well as business activities; provision regarding membership; meeting of the members; management; capital; period of establishment; the distribution of the remaining business profit; and sanctions. From such requirements, it can be inferred that the Indonesian Cooperative Law has not encouraged social and environmental responsibility or CoopSR to be a material content of the cooperatives’ articles of association. Cooperatives are also not yet encouraged to create CoopSR reports, while it has been practiced by cooperatives in other countries. Therefore, the authors believe that it is necessary to amend the current Indonesian Cooperative Law in relation to the content requirement of the cooperatives’ articles of association so that it contains material related to CoopSR, and the cooperatives shall be encouraged to implement CoopSR in order to achieve a sustainable business for the cooperative itself.

Thirdly, all members of the cooperative who have a voice at the meeting of members shall discuss and approve the CoopSR program and implementation. Cooperatives’ members as the most important stakeholders of the cooperatives must be involved in CoopSR, where such involvement by a group of stakeholders could present a positive relationship between the construction of CSR and the company’s reputation [

53]. The meeting of members is a cooperative organizational body that holds the highest authority in the cooperative. It shall convene a meeting at least once a year. There are two types of meetings, namely ordinary meetings of the members that are held in a normal situation, and extraordinary meetings that are held if circumstances require an immediate decision from all members.

The meeting of members will discuss and determine various matters, including the articles of association; general policy on the organizational management; election, appointment, and dismissal of the management and commissioners; annual plan, cooperative income and expenditure budget plans, and ratification of financial reports; validation of the accountability of duty performed by the management; distribution of remaining business profit; and merger, consolidation, division, and dissolution of cooperatives.

As mentioned above, a meeting of members determines, among other things, the general policy of organizational management and annual plans. These two things can be a means of reference in implementing CoopSR in cooperatives. CoopSR needs to be included in general policies and annual plans of the cooperatives in the future to support the implementation of CoopSR. The members must be mutually aware and agree to the determination of CoopSR at the meeting so that its implementation can be optimal. In addition to those three strategies, to enable the implementation of CoopSR by the cooperatives, it is no less vital to incorporate it into the principles of corporate governance of the cooperatives. The inclusion of CoopSR into the cooperatives regulations itself, that is its corporate governance, serves as information to the public about the nature of the organization and the cooperatives’ commitment to implement CoopSR. By including certain goals in its corporate governance, then the moral strength of the organization in performing certain things does not need to be questioned anymore [

56]. Cooperatives that include CoopSR in their corporate governance principles have more responsibility to ensure their programs are implemented according to the goals they desire to achieve.

The principles of corporate governance in cooperatives are different from such principles in general. Such principles in the companies in general are known as Good Corporate Governance (GCG), while in the cooperatives are referred to as Good Cooperative Governance (GCoopG), as shown in

Table 2.

The differences between GCoopG and GCG can be seen in several ways, one of which is the basic pillars, main focus, and goals of the governance. The most essential thing to note in CoopSR so that it can be included in GCoopG is the basic pillars. In general, there are four pillars in GCoopG, which consist of teaming, accountable empowerment, strategic leadership, and democracy [

57]. Meanwhile, from the authors’ perspectives, another essential pillar that needs to exist in GCoopG and is directly related to CoopSR is sustainability. The implementation of CoopSR must be in accordance with the pillars in GCoopG and be one of the priority programs that the cooperative desires to achieve.

Firstly, CoopSR in cooperatives must be based on the results of cooperation to achieve common goals as the pillars of GCoopG, namely teaming. Cooperative management must be able to organize and manage the continuity of CoopSR implementation together with all stakeholders. The management and all stakeholders including members of the cooperative are one unit that can work together effectively as a team. This cooperation could determine what will be done and the goals to be achieved in CoopSR.

Secondly, CoopSR must be based on accountable empowerment, which means that the governance of its implementation must create success in fully empowering members while still paying attention to the responsibilities of members. Empowerment in CoopSR is needed to increase the business capacity and ability of members so that they can indirectly develop the cooperative itself. Accountability is needed so that in empowering CoopSR, there are clear objectives and roles for each stakeholder.

Thirdly, CoopSR must be based on strategic leadership, where the governance of its implementation must be able to successfully prepare and direct cooperatives in general in achieving their goals. The essence of CoopSR, which is based on strategic leadership, is how its implementation can meet the needs and aspirations of cooperative members, distinguish CoopSR from other companies’ CSR, and the kind of goals that the CoopSR desired to achieve. Cooperative management is obliged to determine the direction or goals of CoopSR, while at the same time facilitating such achievement.

Fourthly, CoopSR must be based on democracy, where the governance of its implementation must successfully practice, protect, promote, and preserve democratic management in cooperatives. Democracy in cooperatives is not only narrowly defined or practiced in decision-making, but also in providing opportunities for all members to participate fully in CoopSR. Cooperative members as the holder of the highest sovereignty in cooperatives must be given equal opportunity to contribute to CoopSR without receiving different treatment between one another.

Fifthly, CoopSR must be based on sustainability, where the governance of its implementation must be able to create both present and future sustainability. Sustainability that is created from CoopSR implementation must be in a broad sense, where it does not only create sustainability for cooperatives themselves, but also all surrounding stakeholders, including, the most crucial one, the cooperative members. By creating sustainability for members’ businesses due to the implementation of CoopSR, it can indirectly create stronger sustainability for the cooperatives.

4.4. Regulating Cooperative Social Responsibility in Accordance with the Cooperatives’ Identity

The CSR dimension that has developed into legal responsibility has consequences that program implementers must comply with the prevailing laws and regulations enacted by the government as basic guidelines in which they operate [

58]. Laws and regulations stipulate certain criteria and standards so that the implementation of CSR can run well and in accordance with the desired objectives. Furthermore, laws and regulations could also be a stimulus for CSR to be performed by various stakeholders, which is by imposing certain consequences such as sanctions for the entities that are not performing the CSR.

Laws serve the function in the economic development that refers to the development of legal theory, which places the law functions as not only limited to guaranteeing legal certainty and order, but also more than that, as a means of social engineering or a means of social reform and development [

59]. In terms of the function of law as a means of social engineering, the law is defined in a broader sense, not only as a whole principle and as rules governing human life in society, but also includes institutions and processes that embody the enactment of these rules in reality [

60].

Laws that serve a function as a means of economic development in society must not only stipulate the content of principles and rules, but also institutions and processes so that the laws can be implemented. In terms of the content, the things that must be considered are identity, values, principles, or characteristics attached to the matter being regulated. The same goes with the regulation concerning CoopSR, which is performed by cooperatives that have their unique characteristics compared to other business entities. Thus, organizational identification within cooperatives is necessary to regulate CoopSR as a process of combining perceptions of the organization [

61].

Universal cooperatives’ identities cannot be separated from three main things, namely definitions, values, and principles that exist in cooperatives. The ICA defines a cooperative as an autonomous association of persons united voluntarily to meet their economic, social, and cultural needs and aspirations through a mutually owned and democratically controlled enterprise. From the ICA’s definition of cooperatives, there are two main elements of cooperatives’ identity. First, cooperatives as autonomous associations of people try to meet social, economic, and cultural needs and aspirations. Second, cooperatives as business entities are democratically controlled and mutually owned.

Cooperatives’ identity can also be seen from the values that exist in cooperatives. As has been previously discussed, there are no cooperative values in the Indonesian legal system. However, there are universal cooperative values that consist of self-help, self-responsibility, democracy, equality, equity, and solidarity. Furthermore, there are ethical values that consist of honesty, openness, social responsibility, and caring for others. The values that exist in the cooperative are very crucial as the basis or spirit of the cooperative to perform its various activities.

Moreover, the cooperatives’ identities can also be seen from the principles that serve as a reference in cooperatives’ operations. In the universal values, there are seven cooperative principles, consisting of voluntary and open membership; democratic member control; member economic participation; autonomy and independence; education, training, and information; cooperation among cooperatives; and concern for the community. It has also been explained in the previous discussion that there are differences between the cooperative principles in Indonesia with the universal cooperative principles, in which there is no principle of concern for the community in the cooperative principles in Indonesia.

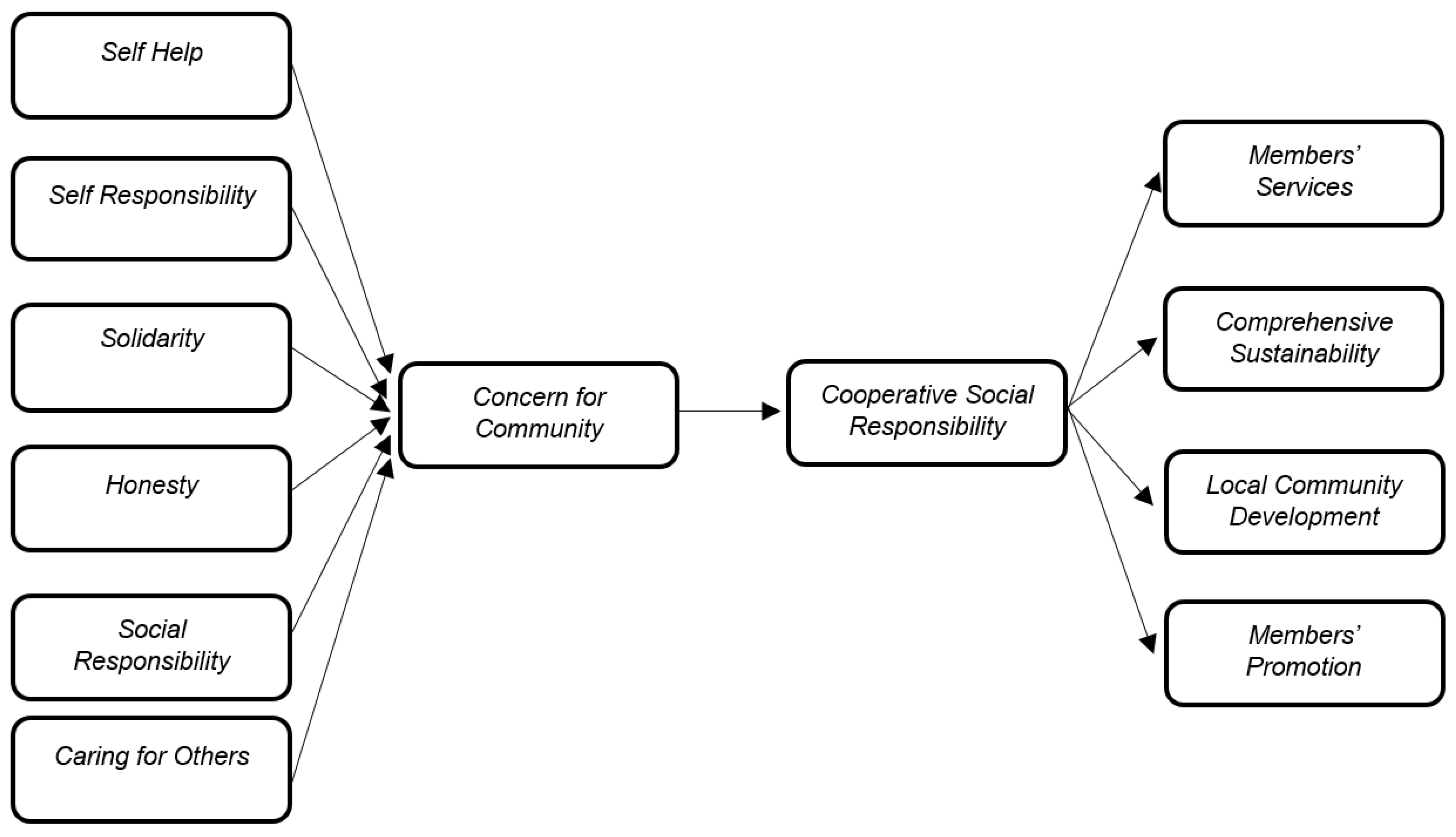

Based on the cooperatives’ identities mentioned above, it can be specified that the cooperative values of social responsibility and caring for others, as well as the cooperative principle of concern for the community, are directly related to CoopSR. Each of the values and principles that exist in cooperatives has a relationship with one another. Since CoopSR is naturally a technical program, it is directly related to the principles, in this case the principle of concern for the community. Apart from being based on the values of social responsibility and caring for others, this principle also comes from the values of self-help, self-responsibility, solidarity, and honesty.

The principle of concern for community, which comes from the values of self-help, self-responsibility, solidarity, honesty, social responsibility, and caring for others, is the basis for determining CoopSR in cooperatives. From the authors’ perspectives, there are at least four characteristics of CoopSR that shall exist in cooperatives based on their identity. Those are services to the members, comprehensive sustainability, local community development, and promotion of the members, as shown in

Figure 6.

The first characteristic that distinguishes CoopSR from CSR performed by other companies is that it must be performed in order to provide services to the members. The CoopSR program that is aimed at members could increase the loyalty and benefits of members, so that it is indirectly beneficial for cooperatives. The loyalty of members is crucial to the cooperatives since it measures how well the cooperatives run their businesses. Having CoopSR implementation focus on providing the services to members is a fundamental thing that distinguishes CoopSR and CSR from other companies that do not involve shareholders as the priority of the program. Providing services to the members in CoopSR is based on the values of self-help and self-responsibility, where cooperatives and their members must be able to improve their own conditions and self-responsibility.

The second characteristic is that it must be performed in order to create comprehensive sustainability in the cooperatives’ ecosystems. The purpose of having such comprehensive sustainability is that with the implementation of CoopSR, sustainability does not only have an impact on cooperatives, but also on cooperative movements, cooperative members, partners, and other parties. Sustainability in CoopSR must become a supply chain for all stakeholders involved in the cooperatives’ ecosystem. For instance, cooperatives are responsible for the costs of CoopSR, and their members or partners are directly responsible for implementing the program. The characteristic of comprehensive sustainability in CoopSR is based on the value of solidarity, which means the existence of mutual respect and mutual need for each other.

The third characteristic is that it must be performed to develop the local community where the cooperative operates. Focusing on the local community is very crucial for the cooperatives since they exist and root in the communities where they conduct their business activities. Cooperatives must be the prime stimulus in the local community empowerment, as in the context of cooperatives in Indonesia itself, the cooperatives exist and emerge from the rural areas. The values underlying the characteristics of CoopSR with a focus on local community empowerment are based on the values of social responsibility and caring for others. The value of social responsibility means that cooperatives must create continuous improvements to the conditions surrounding their environment. While the value of caring for others means that the cooperatives must create a good relationship with the society outside of the cooperatives.

The fourth characteristic that must exist in CoopSR is the promotion of members, which means that the CoopSR implementation should be a way to recruit new cooperative members, as much as possible. The promotion of members is also a part of the pillars of promoting cooperatives’ identity according to the strategic plan for cooperatives until 2030, called “A People-Centred Path for a Second Cooperative Decade”. The object of this fourth characteristic is the society that potentially joins the cooperatives, for instance, those who have the same businesses. The promotion of members in CoopSR is based on the value of honesty, where cooperatives must emphasize in conducting their activities, for example by emphasizing the importance of honesty in business transaction, measurable planning, reliable quality, and competitive prices, to build a good reputation in the society and make people interested in joining the cooperatives. To summarize,

Table 3 shows the comparison between CoopSR and CSR in terms of values, principles, and characteristics.

The thing that differentiates CSR performed by the cooperatives and other business entities is the four characteristics that exist in CoopSR. Apart from being a differentiator, these characteristics are in accordance with the identity of cooperatives and effective to develop the cooperatives and the parties involved in its future. Every type of cooperative could implement and refer to these characteristics, while still being adjusted according to the specific type or focus of the cooperatives’ business activity. For example, in one of the largest cooperatives in Indonesia,

Koperasi Peternakan Bandung Selatan Pangalengan, (hereinafter referred to as PX Cooperative). PX Cooperative is one of the largest dairy farmer cooperatives in Indonesia. Its total assets reached IDR 175 billion while consisting of 4304 farmer members in 2021 [

63]. It has performed its social responsibilities in terms of providing services to its members through one of its business units, PT Keluarga Pangalengan Bersama Sejahtera Asysyifa, which is engaged in the hospital sector. This business unit provides PX Cooperative’s members and their families with free health facilities. In another business unit, PT BPR Bandung Kidul, which is engaged in the finance sector, the members are given lower loan interest rates compared to other people who are not members of PX Cooperative.

In terms of comprehensive sustainability, PX Cooperative is empowering its members by implementing a corporate culture that prioritizes the interests of members and works in cooperation, so that all members receive equal welfare. PX Cooperative also cooperates with SOEs in providing capital loan for its members. PX Cooperative is also very concerned about the local community development, specifically surrounding their societies. This is because the word “Pangalengan” in the name of PX Cooperative is taken from the name of the area where PX cooperative is located. Thus, PX Cooperative performs social responsibility in the form of education assistance and contribution to regional development. As for member promotion, PX Cooperative is continuously able to invite farmers around their areas to become members. This promotion can be carried out through business and service units in the PX Cooperative, especially those directly related to farmers, such as feed management units, animal health units, and production units.

The characteristics of CoopSR can be incorporated into the existing cooperative arrangements in Indonesia. As explained in the previous analysis, in addition to the necessity to amend the Indonesian Cooperative Law to incorporate the cooperatives’ values and principles of concern for the community, it is mandatory to enact a specific chapter dedicated to the CoopSR. It shall contain, at the very least, characteristics of CoopSR, criteria for cooperatives that are required to perform CoopSR, the amount and source of fund allocated for it, duties and functions of the management, supervision and guidance, reporting mechanism, and sanctions.

The criteria for cooperatives that are required to perform CoopSR can be based on the Cooperatives Business Classification (Klasifikasi Usaha Koperasi/KUK) determined by the Ministry of Cooperatives and Small and Medium Enterprises of the Republic of Indonesia. KUK is the classification of cooperative businesses according to the number of their members, the amount of their capital, and/or the number of their assets. The suitable KUK criteria to perform CoopSR can be based on the number of their assets. There are four KUK criteria in terms of their assets. KUK I are cooperatives with maximum total assets of IDR 2.5 billion. KUK II are cooperatives with maximum total assets of IDR 2.5 billion to 100 billion. KUK III are cooperatives with maximum total assets of IDR 100 billion to 500 billion. Finally, KUK IV are cooperatives with total assets of more than IDR 500 billion. Thus, CoopSR can be required for large cooperatives, or cooperatives that are included in the KUK III and KUK IV categories. Further, it can also be required for cooperatives that have a direct impact on the environment in order to recover the environment.

The amount and source of funds allocated for the implementation of CoopSR also need to be regulated as a guideline for cooperatives who desire to implement it. It needs further research to be able to determine the specific amount the cooperatives should allocate for the cost of CoopSR. However, considering the cost of CSR performed by SOEs in Indonesia as explained previously, at most 4% of the projected net profit, it can be referred to determine the cooperatives’ allocation for CoopSR. It can be reduced even further to, for example, 2% of the projected net profit. The sources can be from the business profit or the Remaining Results of Operations, namely net profits come from the business result of cooperatives’ members, not from its business.

CoopSR implementation cannot be separated from the role of the cooperatives’ management. As a party that runs and controls the cooperative’s operations, the management ensures the cooperatives run CoopSR. Management structures or divisions specifically related to CoopSR may also be formed. It becomes crucial to ensure optimal conduct of budget planning, program planning, implementation, and evaluation of the implementation of CoopSR.

CoopSR has different characteristics from the other forms of social responsibility, as it requires supervision in its implementation. Both internal and external parties can conduct such supervision. The internal party can ensure that CoopSR implementation is according to its provisions, which can be carried out by the cooperatives’ supervisors. The cooperatives’ supervisors’ daily tasks include supervision and examination of the implementation of cooperative management and policies, which in this case are related to the CoopSR. While the external parties, an independent institution formed between the cooperative movement association and the Ministry of Cooperatives and Small and Medium Enterprises of the Republic of Indonesia, can monitor the CoopSR implementation. Apart from being the initiator of such independent institution establishment, both the cooperative movement association and the Ministry of Cooperatives and Small and Medium Enterprises of the Republic of Indonesia can also play a role in fostering cooperatives that wish to implement CoopSR.

Furthermore, it is also necessary to enact regulations on reporting mechanisms and sanctions should the cooperatives not perform the required CoopSR. The reporting mechanism can contain necessary information regarding the development, implementation, and position of cooperatives, as well as the impact of CoopSR activities. Such reports concerning CoopSR implementation can indirectly influence the sustainability of cooperatives since they gain a positive image in society. The frequency of the reports also needs to be stipulated, for instance an annual report simultaneously with the annual meeting of members. As for the sanction, it is necessary to determine the type of penalties that will be imposed for the cooperatives not implementing the required CoopSR, which can also be in the form of fines. The mechanism of sanction is crucial so that the cooperatives that are required to perform the mandatory CoopSR are more responsible and contribute optimally to the sustainable development.

Regulation concerning CSR in the Indonesian legal system, specifically in the Indonesian Cooperative Law, caused the CSR implementation to become a legal responsibility. The position of CoopSR as a legal responsibility is relevant to the current condition in Indonesia, since as a developing country, it is necessary for the private sector to be involved in an effort to alleviate poverty, to improve public facilities, to create a sustainable environment, and to develop the economy. As a legal responsibility, CoopSR will give rise to rights and obligations for cooperatives as its implementing subject. Cooperatives that meet certain criteria, such as the amount of their assets or the type of business activities they conducted (whether it has a direct impact to the environment), will be required to perform CoopSR as discussed previously in this article. The authors believe that as a legal responsibility, CoopSR will be able to encourage the cooperatives in Indonesia, which is the largest in the world in terms of the numbers, to directly contribute to the sustainable development that will eventually benefit both the economic growth of Indonesia in general and also the sustainability of the cooperative itself in particular.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}