Non-Monotonic Relationship between Corporate Governance and Banks’ Operating Performance—The Moderating Role of CEO Duality: Evidence from Selected Countries

Abstract

:1. Introduction

2. Theoretical Framework and Hypotheses Development

3. Data and Methodology

3.1. Sample

3.2. Variables

3.3. Model for the Non-Monotonic Relationship between CG and Operating Performance

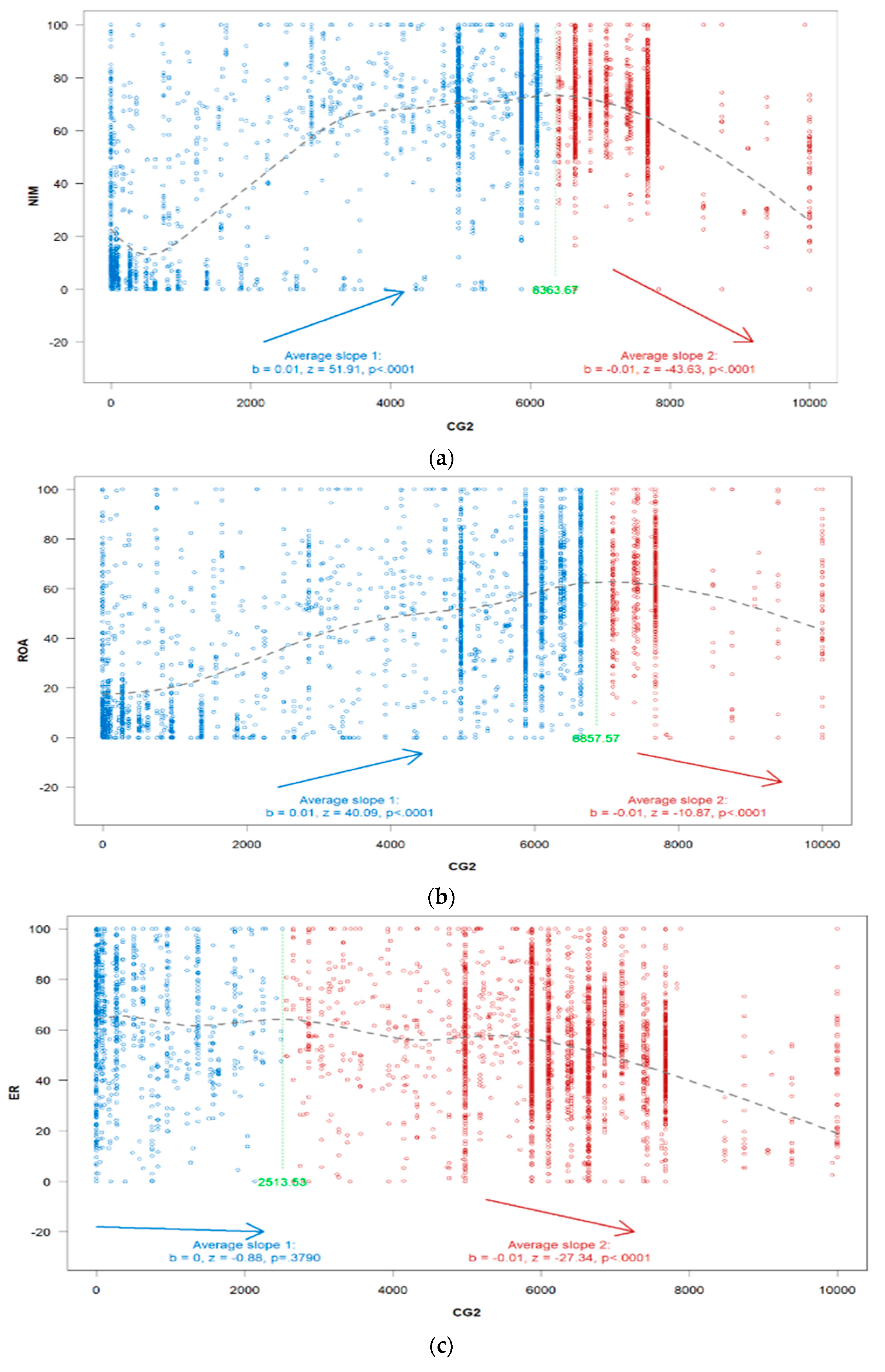

4. Two-Line Approach and the Robin Hood Algorithm

- Our study refers to the predictor hypothesized to have a U-shaped effect as CG2, and the dependent variable as NIM.

- To test if the effect of CG2 is U-shaped (or inverted U-shaped) on performance, the two-line test procedure conducted the following:

- Run a quadratic regression of the form Performance = aCG + bCG2

- The results were a = 0.022 and b = −0. With these values, one obtains the implied slope (a + 2bCG2) at the lowest observed value of CG (CGmin = 0). If that slope is negative at that point, the two-line test considers a U shape; if it is positive, an inverted-U shape. Here the quadratic implies a slope of 0.022 at the lowest CG value of CG = 0, which was positive; thus, it tested for an inverted-U shape.

- Estimated a spline (smoothed scatterplot) model, Performance = f (CG). See the gray dashed line in Figure 1a–c.

- Among the middle 80% of CG values (between the 10th and 90th percentile), the most extreme fitted Performance value was identified: performancemax = 73.369, which corresponds to CG2 = 6346.164.

- All CG values associated with a fitted performance within a standard error of performance max were identified: CGflat.

- The median CG value in CGflat was identified as 6411.041.

- An interrupted regression was estimated with that midpoint value as the breakpoint (with heteroskedasticity-robust standard errors (using ‘HC3’ by default, switching to ‘HC1’ if a NA is produced)).

- The resulting z-values (b/se) for the two slopes were z1 = 51.77 and z2 = 42.544.

- Using these z-values, we computed the following ratio, z1/(z1 + z2) = 0.549, which is the percentile of the CG2 value within CGflat used as the breakpoint for the final interrupted regression, whose results are depicted in Figure 1, CGc = 6363.672.

5. Results

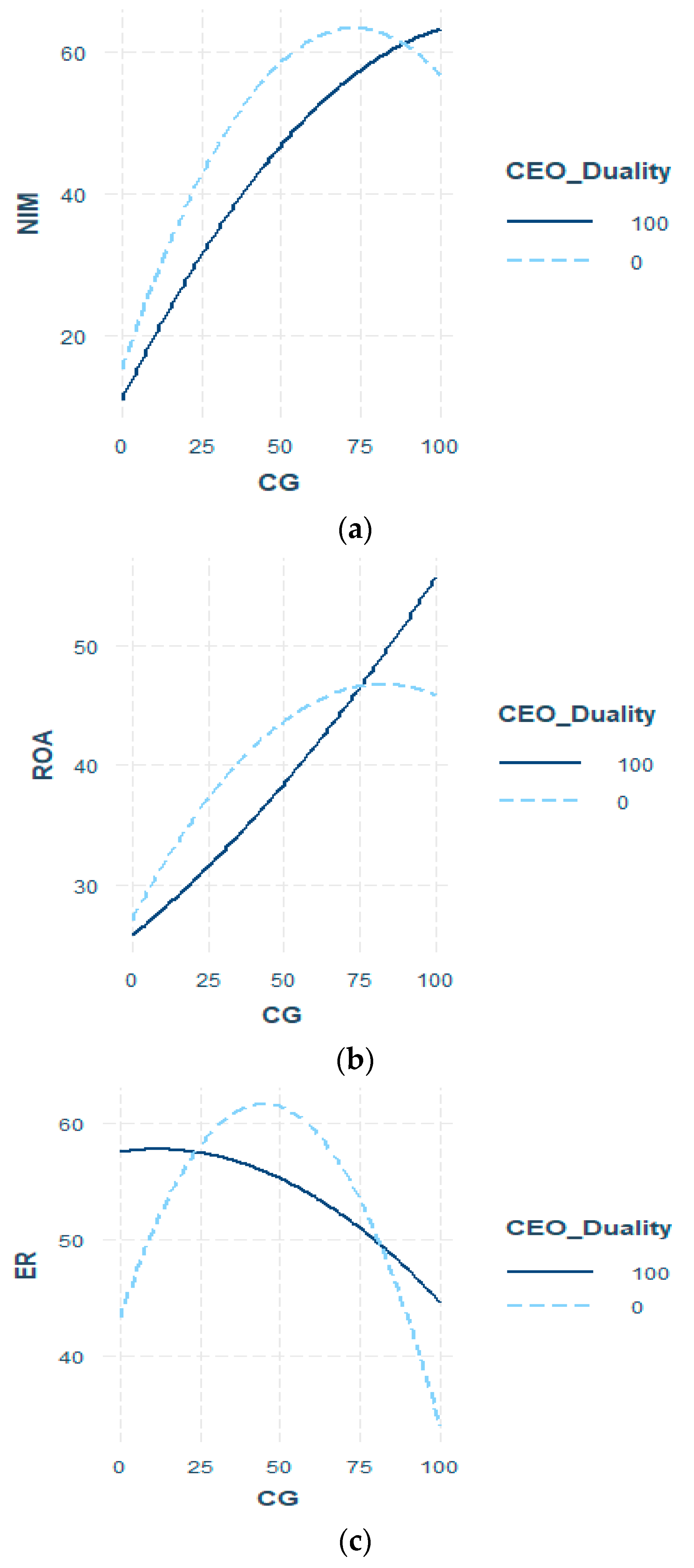

6. The Interaction Effect of CEO Duality

7. Discussion and Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Basel Committee on Banking Supervision. Principles for Sound Liquidity Risk Management and Supervision; Basel Committee on Banking Supervision: Basel, Switzerland, 2008. [Google Scholar]

- Basel Committee on Banking Supervision. Enhancing Corporate Governance for Banking Organisations; Basel Committee on Banking Supervision: Basel, Switzerland, 2006. [Google Scholar]

- Jensen, M.C.; Meckling, W.H. Rights and Production Functions: An Application to Labor-Managed Firms and Codetermination. J. Bus. 1979, 52, 469. [Google Scholar] [CrossRef]

- Hart, O. Corporate Governance: Some Theory and Implications. Econ. J. 1995, 105, 678–689. [Google Scholar] [CrossRef]

- Naceur, S.B.; Omran, M. The Effects of Bank Regulations, Competition, and Financial Reforms on Banks’ Performance. Emerg. Mark. Rev. 2011, 12, 1–20. [Google Scholar] [CrossRef]

- Rodriguez-Fernandez, M.; Fernandez-Alonso, S.; Rodriguez-Rodriguez, J. Board Characteristics and Firm Performance in Spain. Corp. Gov. Int. J. Bus. Soc. 2014, 14, 485–503. [Google Scholar] [CrossRef]

- Wang, Y.-Y. Relationship between Gastrointestinal Flora and Chronic Atrophic Gastritis. World Chin. J. Dig. 2016, 24, 1526. [Google Scholar] [CrossRef]

- OECD. OECD Corporate Governance Factbook; OECD: Paris, France, 2021. [Google Scholar]

- Jesover, F.; Kirkpatrick, G. The Revised OECD Principles of Corporate Governance and Their Relevance to Non-OECD Countries. Corp. Gov. 2005, 13, 127–136. [Google Scholar] [CrossRef]

- Abu-Tapanjeh, A.M. Corporate Governance from the Islamic Perspective: A Comparative Analysis with OECD Principles. Crit. Perspect. Account. 2009, 20, 556–567. [Google Scholar] [CrossRef]

- Chen, V.Z.; Li, J.; Shapiro, D.M. Are OECD-Prescribed “Good Corporate Governance Practices” Really Good in an Emerging Economy? Asia Pac. J. Manag. 2010, 28, 115–138. [Google Scholar] [CrossRef]

- Levine, R. The Corporate Governance of Banks; World Bank Publications: Washington, DC, USA, 2004. [Google Scholar]

- Craig Nichols, D.; Wahlen, J.M.; Wieland, M.M. Publicly Traded versus Privately Held: Implications for Conditional Conservatism in Bank Accounting. Rev. Account. Stud. 2008, 14, 88–122. [Google Scholar] [CrossRef]

- Bamber, L.S.; Jiang, J.; Wang, I.Y. What’s My Style? The Influence of Top Managers on Voluntary Corporate Financial Disclosure. Account. Rev. 2010, 85, 1131–1162. [Google Scholar] [CrossRef] [Green Version]

- Beltratti, A.; Stulz, R.M. The Credit Crisis around the Globe: Why Did Some Banks Perform Better? J. Financ. Econ. 2012, 105, 1–17. [Google Scholar] [CrossRef]

- Peni, E.; Vähämaa, S. Did Good Corporate Governance Improve Bank Performance during the Financial Crisis? J. Financ. Serv. Res. 2011, 41, 19–35. [Google Scholar] [CrossRef]

- Erkens, D.H.; Hung, M.; Matos, P. Corporate Governance in the 2007–2008 Financial Crisis: Evidence from Financial Institutions Worldwide. J. Corp. Finance 2012, 18, 389–411. [Google Scholar] [CrossRef]

- Chen, C.J.P.; Jaggi, B. Association between Independent Non-Executive Directors, Family Control and Financial Disclosures in Hong Kong. J. Account. Public Policy 2000, 19, 285–310. [Google Scholar] [CrossRef]

- Abobakr, M.G. Corporate Governance and Banks Performance: Evidence from Egypt. Asian Econ. Financ. Rev. 2017, 7, 1326–1343. [Google Scholar] [CrossRef] [Green Version]

- Claessens, S.; Yurtoglu, B.B. Corporate Governance in Emerging Markets: A Survey. Emerg. Mark. Rev. 2013, 15, 1–33. [Google Scholar] [CrossRef]

- Staikouras, P.K.; Staikouras, C.K.; Agoraki, M.-E.K. The Effect of Board Size and Composition on European Bank Performance. Eur. J. Law Econ. 2007, 23, 1–27. [Google Scholar] [CrossRef]

- De Andres, P.; Vallelado, E. Corporate Governance in Banking: The Role of the Board of Directors. J. Bank. Finance 2008, 32, 2570–2580. [Google Scholar] [CrossRef] [Green Version]

- Salim, R.; Arjomandi, A.; Seufert, J.H. Does Corporate Governance Affect Australian Banks’ Performance? J. Int. Financ. Mark. Inst. Money 2016, 43, 113–125. [Google Scholar] [CrossRef] [Green Version]

- Linck, J.; Netter, J.; Yang, T. The Determinants of Board Structure. J. Financ. Econ. 2008, 87, 308–328. [Google Scholar] [CrossRef]

- Francis, B.; Hasan, I.; Wu, Q. Professors in the Boardroom and Their Impact on Corporate Governance and Firm Performance. Financ. Manag. 2015, 44, 547–581. [Google Scholar] [CrossRef] [Green Version]

- de Andres, P.; Azofra, V.; Lopez, F. Corporate Boards in OECD Countries: Size, Composition, Functioning and Effectiveness. Corp. Gov. 2005, 13, 197–210. [Google Scholar] [CrossRef]

- Tosun, O.K.; Senbet, L.W. Does Internal Board Monitoring Affect Debt Maturity? Rev. Quant. Financ. Account. 2019, 54, 205–245. [Google Scholar] [CrossRef] [Green Version]

- Pi, L.; Timme, S.G. Corporate Control and Bank Efficiency. J. Bank. Finance 1993, 17, 515–530. [Google Scholar] [CrossRef]

- Bai, G.; Elyasiani, E. Bank Stability and Managerial Compensation. J. Bank. Finance 2013, 37, 799–813. [Google Scholar] [CrossRef]

- Finkelstein, S.; D’aveni, R.A. CEO duality as a Double-Edged Sword: How Boards of Directors Balance Entrenchment Avoidance and Unity of Command. Acad. Manag. J. 1994, 37, 1079–1108. [Google Scholar] [CrossRef]

- Donaldson, L.; Davis, J.H. Stewardship Theory or Agency Theory: CEO Governance and Shareholder Returns. Aust. J. Manag. 1991, 16, 49–64. [Google Scholar] [CrossRef] [Green Version]

- Boyd, B.K. CEO Duality and Firm Performance: A Contingency Model. Strateg. Manag. J. 1995, 16, 301–312. [Google Scholar] [CrossRef]

- Larcker, D.F.; Tayan, B. Chairman and CEO: The Controversy Over Board Leadership Structure. Available online: https://ssrn.com/abstract=2800244 (accessed on 30 March 2021).

- Tang, T.Y.H. Privatization, Tunneling, and Tax Avoidance in Chinese SOEs. Asian Rev. Account. 2016, 24, 274–294. [Google Scholar] [CrossRef]

- Smith, C.W.; Stulz, R.M. The Determinants of Firms’ Hedging Policies. J. Financ. Quant. Anal. 1985, 20, 391. [Google Scholar] [CrossRef]

- Byrd, J.; Fraser, D.R.; Scott Lee, D.; Tartaroglu, S. Are Two Heads Better than One? Evidence from the Thrift Crisis. J. Bank. Finance 2012, 36, 957–967. [Google Scholar] [CrossRef] [Green Version]

- Berger, A.N.; Imbierowicz, B.; Rauch, C. The Role of Corporate Governance in Bank Failures during the Recent Financial Crisis. SSRN Electron. J. 2012. [Google Scholar] [CrossRef] [Green Version]

- Simpson, W.G.; Gleason, A.E. Board Structure, Ownership, and Financial Distress in Banking Firms. Int. Rev. Econ. Finance 1999, 8, 281–292. [Google Scholar] [CrossRef]

- Mollah, S.; Liljeblom, E. Governance and Bank Characteristics in the Credit and Sovereign Debt Crises What Is Different? SSRN Electron. J. 2016. [Google Scholar] [CrossRef]

- Li, M.; Roberts, H. Does Mandated Independence Improve Firm Performance? Evidence from New Zealand. Pac. Account. Rev. 2018, 30, 92–109. [Google Scholar] [CrossRef]

- De Haan, J.; Vlahu, R. Corporate Governance of Banks: A Survey. J. Econ. Surv. 2015, 30, 228–277. [Google Scholar] [CrossRef] [Green Version]

- Škare, M.; Hasić, T. Corporate Governance, Firm Performance, and Economic Growth—Theoretical Analysis. J. Bus. Econ. Manag. 2016, 17, 35–51. [Google Scholar] [CrossRef] [Green Version]

- Allam, B.S. The Impact of Board Characteristics and Ownership Identity on Agency Costs and Firm Performance: UK Evidence. Corp. Gov. Int. J. Bus. Soc. 2018, 18, 1147–1176. [Google Scholar] [CrossRef]

- Lu, J.; Boateng, A. Board Composition, Monitoring and Credit Risk: Evidence from the UK Banking Industry. Rev. Quant. Finance Account. 2017, 51, 1107–1128. [Google Scholar] [CrossRef] [Green Version]

- Aebi, V.; Sabato, G.; Schmid, M. Risk Management, Corporate Governance, and Bank Performance in the Financial Crisis. J. Bank. Finance 2012, 36, 3213–3226. [Google Scholar] [CrossRef]

- Francis, J.R.; Stokes, D.J. Audit Prices, Product Differentiation, and Scale Economies: Further Evidence from the Australian Market. J. Account. Res. 1986, 24, 383–393. [Google Scholar] [CrossRef]

- Tsui, J.S.L.; Jaggi, B.; Gul, F.A. CEO Domination, Growth Opportunities, and Their Impact on Audit Fees. J. Account. Audit. Finance 2001, 16, 189–208. [Google Scholar] [CrossRef]

- Huafang, X.; Jianguo, Y. Ownership Structure, Board Composition and Corporate Voluntary Disclosure. Manag. Audit. J. 2007, 22, 604–619. [Google Scholar] [CrossRef]

- Bliss, M.A.; Muniandy, B.; Majid, A. CEO Duality, Audit Committee Effectiveness and Audit Risks. Manag. Audit. J. 2007, 22, 716–728. [Google Scholar] [CrossRef]

- Mashayekhi, B.; Bazaz, M.S. Corporate Governance and Firm Performance in Iran. J. Contemp. Account. Econ. 2008, 4, 156–172. [Google Scholar] [CrossRef]

- Onal, M.M.; Ashton, J.K. Is the Journey More Important than the Destination? EU Accession and Corporate Governance and Performance of Banks. JCMS J. Common Mark. Stud. 2021, 59, 1516–1535. [Google Scholar] [CrossRef]

- Khan, I.; Wang, M. Evaluating Corporate Performance and Bank Productivity in China: The Moderating Role of Independent Directors. Sustainability 2021, 13, 3193. [Google Scholar] [CrossRef]

- Boachie, C. Corporate Governance and Financial Performance of Banks in Ghana: The Moderating Role of Ownership Structure. Int. J. Emerg. Mark. 2021, 18, 607–632. [Google Scholar] [CrossRef]

- Khan, I.; Zahid, S.N. The Impact of Shari’ah and Corporate Governance on Islamic Banks Performance: Evidence from Asia. Int. J. Islam. Middle East. Finance Manag. 2020, 13, 483–501. [Google Scholar] [CrossRef]

- Ajili, H.; Bouri, A. Corporate Governance Quality of Islamic Banks: Measurement and Effect on Financial Performance. Int. J. Islam. Middle East. Finance Manag. 2018, 11, 470–487. [Google Scholar] [CrossRef]

- Gangi, F.; Meles, A.; D’Angelo, E.; Daniele, L.M. Sustainable Development and Corporate Governance in the Financial System: Are Environmentally Friendly Banks Less Risky? Corp. Soc. Responsib. Environ. Manag. 2018, 26, 529–547. [Google Scholar] [CrossRef]

- Bachiller, P.; Garcia-Lacalle, J. Corporate Governance in Spanish Savings Banks and Its Relationship with Financial and Social Performance. Manag. Decis. 2018, 56, 828–848. [Google Scholar] [CrossRef] [Green Version]

- Tarchouna, A.; Jarraya, B.; Bouri, A. How to Explain Non-Performing Loans by Many Corporate Governance Variables Simultaneously? A Corporate Governance Index Is Built to US Commercial Banks. Res. Int. Bus. Finance 2017, 42, 645–657. [Google Scholar] [CrossRef]

- Greene, W.H. Econometric Analysis; Pearson Education India: Delhi, India, 2003. [Google Scholar]

- Yermack, D. Higher Market Valuation of Companies with a Small Board of Directors. J. Financ. Econ. 1996, 40, 185–211. [Google Scholar] [CrossRef]

- Hermalin, B.E.; Weisbach, M.S. The Effects of Board Composition and Direct Incentives on Firm Performance. Financ. Manag. 1991, 20, 101–112. [Google Scholar] [CrossRef]

- Caprio, G.; Laeven, L.; Levine, R. Governance and Bank Valuation. J. Financ. Intermediation 2007, 16, 584–617. [Google Scholar] [CrossRef] [Green Version]

- Adams, R.B.; Mehran, H. Corporate Performance, Board Structure and its Determinants in the Banking Industry. In Proceedings of the EFA 2005 Moscow Meetings, Moscow, Russia, 24–27 August 2005; Available online: https://ssrn.com/abstract=302593 (accessed on 8 March 2023).

- Bhagat, S.; Black, B.S. The Non-Correlation between Board Independence and Long-Term Firm Performance. SSRN Electron. J. 1998. [Google Scholar] [CrossRef]

- Watson, R. Financial Leverage and Corporate Governance; Oxford University Press: Oxford, UK, 2013. [Google Scholar] [CrossRef]

- Abdallah, A.A.-N.; Ismail, A.K. Corporate Governance Practices, Ownership Structure, and Corporate Performance in the GCC Countries. J. Int. Financ. Mark. Inst. Money 2017, 46, 98–115. [Google Scholar] [CrossRef]

- Brown, L.D.; Caylor, M.L. Corporate Governance and Firm Operating Performance. Rev. Quant. Finance Account. 2008, 32, 129–144. [Google Scholar] [CrossRef]

- Schweizer, D.; Walker, T.J.; Zhang, A. Cross-Border Acquisitions by Chinese Enterprises: The Benefits and Disadvantages of Political Connections. SSRN Electron. J. 2018. [Google Scholar] [CrossRef] [Green Version]

- Zeqiraj, V.; Hammoudeh, S.; Iskenderoglu, O.; Tiwari, A.K. Banking Sector Performance and Economic Growth: Evidence from Southeast European Countries. Post-Communist Econ. 2019, 32, 1–18. [Google Scholar] [CrossRef]

- Zeqiraj, V.; Sohag, K.; Hammoudeh, S. Financial Inclusion in Developing Countries: Do Quality Institutions Matter? J. Int. Financ. Mark. Inst. Money 2022, 81, 101677. [Google Scholar] [CrossRef]

- Zeqiraj, V.; Mrasori, F.; Iskenderoglu, O.; Sohag, K. Dynamic Impact of Banking Performance on Financial Stability: Fresh Evidence from Southeastern Europe. J. Cent. Bank. Theory Pract. 2021, 10, 165–181. [Google Scholar] [CrossRef]

- Simonsohn, U. Two Lines: A Valid Alternative to the Invalid Testing of U-Shaped Relationships with Quadratic Regressions. Adv. Methods Pract. Psychol. Sci. 2018, 1, 538–555. [Google Scholar] [CrossRef] [Green Version]

- Kumar, A.; Gupta, J.; Das, N. Revisiting the Influence of Corporate Sustainability Practices on Corporate Financial Performance: An Evidence from the Global Energy Sector. Bus. Strategy Environ. 2022, 31, 3231–3253. [Google Scholar] [CrossRef]

- Gompers, P.; Ishii, J.; Metrick, A. Corporate Governance and Equity Prices. Q. J. Econ. 2003, 118, 107–156. [Google Scholar] [CrossRef] [Green Version]

- Bhagat, S.; Bolton, B. Corporate Governance and Firm Performance. J. Corp. Finance 2008, 14, 257–273. [Google Scholar] [CrossRef]

- Nollet, J.; Filis, G.; Mitrokostas, E. Corporate Social Responsibility and Financial Performance: A Non-Linear and Disaggregated Approach. Econ. Model. 2016, 52, 400–407. [Google Scholar] [CrossRef] [Green Version]

{kind=link}

{kind=link}

| Author(s) | Dependent Variables | Governance (Control) and Dummy Variables | Data | Methods | Results |

|---|---|---|---|---|---|

| Onal and Asthon [51] | ROA, ROE, and NIM | Board size, Board independence, Board Structure, Gender diversity, Nationality diversity, CEO Duality, and Foreign Ownership | The data comprise 211 banks from an estimated total of 2241 banks, including major banks, functioning in EU member and candidate states from 2000 to 2015. | Fixed Effect Model | Significant Negative Impact |

| Khan and Wang [52] | ROA | Bank size and financial leverage | The data consist of 17 commercial banks (CBs) in China from 2008 to 2019. | GMM | Significant and Positive |

| Boachie [53] | ROA | Audit committee size, Non-executive director, CEO duality, Board size, and Board ownership | The data include 23 Ghanaian banks that were active between 2006 and 2018. | Multiple regression method | Significant and Positive |

| Khan and Zahid [54] | ROA, ROE, and Tobin’s Q | CGI, Board Size, Board education, Board independence, Board activity and ownership structure | The data include 79 Islamic banks from 19 countries, totaling 553 entities with year-to-year observations from 2010 to 2016. | Panel random effects regression | Significant and Positive |

| Ajili and Bouri [55] | ROA, ROE, and Tobin’s Q | Board of directors, Audit committee and Shariah Supervisory Board indices | A sample consists 44 IBs operating in the GCC from 2010 to 2014. | Multiple regression models | Insignificant |

| Gangi et al. [56] | ENV Score and Z-Score | Board size, Board independence, Board diversity, CEO power and CEO compensation | The data include a sample of 142 banks from 35 countries from 2011 to 2015. | Heckman’s two-stage model | Significant and Positive |

| Bachiller and Garcia-Lacalle [57] | ROA | Total assets, no. of employees, and no. of branches | The data contain 45 SBs that were operating in Spain in 2009. | Structural Equation Model (SEM)- PLS | Insignificant |

| Tarchouna et al. [58] | Non-performing Loans | Board size, Board independence, CEO duality, and ownership structure | The sample comprise 184 US commercial banks from the years 2000 to 2013. | PCA and GMM dynamic panel data methods | Small banks are characterized by a sound CG system as opposed to medium and large banks |

| Variable | US | INDIA | JAPAN | AUSTRALIA | ALL |

|---|---|---|---|---|---|

| OBS. | 2790/279 | 250/25 | 740/74 | 450/45 | 4230 |

| NIM | 72.512 | 54.837 | 7.369 | 28.837 | 55.425 |

| ROA | 58.882 | 41.786 | 10.944 | 44.252 | 47.929 |

| ER | 54.434 | 32.631 | 72.786 | 18.868 | 52.572 |

| CG | 75.973 | 38.193 | 21.635 | 94.087 | 66.161 |

| CEO_Duality | 32.294 | 24 | 59.054 | 0 | 33.050 |

| TBQ | 46.158 | 37.226 | 9.822 | 55.312 | 40.247 |

| LEV | 17.592 | 32.253 | 25.131 | 85.651 | 27.017 |

| Earnings | 0.415 | 28.724 | 44.407 | 6.895 | 10.474 |

| GDP | 49.792 | 55.9 | 55.006 | 55.214 | 51.642 |

| Inflation Rate | 1.885 | 5.877 | 0.54 | 1.867 | 1.884 |

| Variable | Observations | Mean | Median | Maximum | Minimum | Std. Dev. |

|---|---|---|---|---|---|---|

| NIM | 4230 | 55.425 | 63.966 | 100.000 | 0.000 | 30.020 |

| ROA | 4230 | 47.929 | 51.761 | 100.000 | 0.000 | 28.808 |

| ER | 4230 | 52.572 | 53.066 | 100.000 | 0.000 | 26.239 |

| CG | 4230 | 66.161 | 76.661 | 100.000 | 0.000 | 28.418 |

| CEO_DUALITY | 4230 | 33.050 | 0.000 | 100.000 | 0.000 | 47.045 |

| TBQ | 4230 | 40.247 | 37.151 | 100.000 | 0.000 | 28.304 |

| LEV | 4230 | 27.017 | 17.544 | 100.000 | 0.000 | 27.451 |

| EARNINGS | 4230 | 10.474 | 0.113 | 100.000 | 0.000 | 23.760 |

| GDP | 4230 | 51.642 | 55.275 | 100.000 | 0.000 | 32.187 |

| INFLATION RATE | 4230 | 1.884 | 1.622 | 10.018 | −0.233 | 1.590 |

| Variables | NIM | ROA | TBQ | CEO_ DUALITY | CG | ER | GDP | INFLATION_RATE | EARNINGS | LEV |

|---|---|---|---|---|---|---|---|---|---|---|

| NIM | 1 | |||||||||

| ----- | ||||||||||

| ROA | 0.361648 | 1 | ||||||||

| 0 | ----- | |||||||||

| TBQ | 0.405129 | 0.21931 | 1 | |||||||

| 0 | 0 | ----- | ||||||||

| CEO_ DUALITY | −0.1383 | −0.10169 | −0.11084 | 1 | ||||||

| 0 | 0 | 0 | ----- | |||||||

| CG | 0.488476 | 0.303733 | 0.27445 | −0.24567 | 1 | |||||

| 0 | 0 | 0 | 0 | ----- | ||||||

| ER | −0.1104 | −0.30266 | −0.25837 | 0.142959 | −0.32763 | 1 | ||||

| 0 | 0 | 0 | 0 | 0 | ----- | |||||

| GDP | −0.13587 | 0.05574 | −0.01357 | −0.04946 | 0.093529 | −0.10619 | 1 | |||

| 0 | 0.0003 | 0.0075 | 0.0013 | 0 | 0 | ----- | ||||

| INFLATION_ RATE | 0.207586 | 0.276484 | 0.144352 | −0.09624 | 0.072858 | −0.28504 | 0.173376 | 1 | ||

| 0 | 0 | 0 | 0 | 0 | 0 | 0 | ----- | |||

| EARNINGS | −0.2353 | −0.18439 | −0.29771 | 0.095477 | −0.15565 | 0.029692 | 0.09473 | −0.11571 | 1 | |

| 0 | 0 | 0 | 0 | 0 | 0.0535 | 0 | 0 | ----- | ||

| LEV | −0.39236 | −0.14756 | 0.107295 | −0.17817 | 0.200804 | −0.382 | −0.02664 | −0.0447 | 0.162474 | 1 |

| 0 | 0 | 0 | 0 | 0 | 0 | 0.0332 | 0.0401 | 0 | ----- |

| Dependent Variable | |||

|---|---|---|---|

| NIM | ROA | ER | |

| (1) | (2) | (3) | |

| CG | 1.233 *** | 0.417 *** | 0.466 *** |

| (0.047) | (0.040) | (0.047) | |

| TBQ | 0.130 *** | 0.507 *** | −0.334 *** |

| (0.010) | (0.012) | (0.012) | |

| LEV | −0.490 *** | −0.214 *** | −0.237 *** |

| (0.011) | (0.011) | (0.012) | |

| Earnings | −0.290 *** | −0.066 *** | −0.121 *** |

| (0.015) | (0.011) | (0.016) | |

| GDP | −0.142 *** | −0.003 | −0.019 * |

| (0.009) | (0.009) | (0.010) | |

| Inflation_Rate | 2.546 *** | 3.272 *** | −3.425 *** |

| (0.220) | (0.206) | (0.237) | |

| I((CG2)) | −0.008 *** | −0.002 *** | −0.006 *** |

| (0.0004) | (0.0004) | (0.0005) | |

| Constant | 27.266 *** | 10.845 *** | 82.184 *** |

| (1.385) | (1.075) | (1.278) | |

| Observations | 4230 | 4230 | 4230 |

| R2 | 0.658 | 0.597 | 0.476 |

| F Statistic (df = 7; 4222) 1160.100 *** 893.557 *** 547.413 *** | |||

| Dependent Variable | |||

|---|---|---|---|

| NIM | ROA | ER | |

| (1) | (2) | (3) | |

| CG | 0.956 *** | 0.415 *** | 0.485 *** |

| (0.044) | (0.040) | (0.047) | |

| TBQ | 0.184 *** | 0.505 *** | −0.333 *** |

| (0.011) | (0.012) | (0.012) | |

| LEV | −0.465 *** | −0.216 *** | −0.234 *** |

| (0.012) | (0.011) | (0.012) | |

| Earnings | −0.256 *** | −0.066 *** | −0.122 *** |

| (0.014) | (0.011) | (0.015) | |

| GDP | −0.158 *** | −0.003 | −0.020 * |

| (0.009) | (0.009) | (0.010) | |

| Inflation_Rate | 2.957 *** | 3.257 *** | −3.354 *** |

| (0.181) | (0.208) | (0.238) | |

| I((CG2)) | −0.006 *** | −0.002 *** | −0.006 *** |

| (0.0004) | (0.0004) | (0.0005) | |

| CEO_Duality | −0.050 *** | −0.004 | 0.017 ** |

| (0.006) | (0.006) | (0.007) | |

| Constant | 33.220 *** | 11.164 *** | 80.770 *** |

| (1.267) | (1.169) | (1.350) | |

| Observations | 4230 | 4230 | 4230 |

| R2 | 0.639 | 0.594 | 0.482 |

| F Statistic (df = 8; 4221) 934.856 *** 771.953 *** 490.385 *** | |||

| Dependent Variable | |||

|---|---|---|---|

| NIM | ROA | ER | |

| (1) | (2) | (3) | |

| CG | 1.325 *** | 0.476 *** | 0.815 *** |

| (0.072) | (0.057) | (0.065) | |

| TBQ | 0.131 *** | 0.506 *** | −0.327 *** |

| (0.010) | (0.012) | (0.012) | |

| LEV | −0.483 *** | −0.197 *** | −0.214 *** |

| (0.011) | (0.011) | (0.013) | |

| Earnings | −0.265 *** | −0.056 *** | −0.100 *** |

| (0.015) | (0.011) | (0.015) | |

| GDP | −0.137 *** | 0.001 | −0.007 |

| (0.009) | (0.009) | (0.010) | |

| Inflation_Rate | 2.261 *** | 3.195 *** | −3.471 *** |

| (0.215) | (0.214) | (0.229) | |

| I((CG2)) | −0.009 *** | −0.003 *** | −0.009 *** |

| (0.001) | (0.001) | (0.001) | |

| CEO_Duality | −0.043 * | −0.013 | 0.142 *** |

| (0.025) | (0.017) | (0.020) | |

| I((CG2) * CEO_Duality) | 0.0001 *** | 0.00004 *** | 0.0001 *** |

| (0.00001) | (0.00001) | (0.00001) | |

| CG:CEO_Duality | −0.004 *** | −0.003 *** | −0.008 *** |

| (0.001) | (0.001) | (0.001) | |

| Constant | 30.031 *** | 10.865 *** | 72.256 *** |

| (2.342) | (1.608) | (1.892) | |

| Observations | 4230 | 4230 | 4230 |

| R2 | 0.681 | 0.608 | 0.503 |

| F Statistic (df = 10; 4219) 899.145 *** 653.295 *** 426.860 *** | |||

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Enam, M.; Shajar, S.N.; Das, N. Non-Monotonic Relationship between Corporate Governance and Banks’ Operating Performance—The Moderating Role of CEO Duality: Evidence from Selected Countries. Sustainability 2023, 15, 5643. https://doi.org/10.3390/su15075643

Enam M, Shajar SN, Das N. Non-Monotonic Relationship between Corporate Governance and Banks’ Operating Performance—The Moderating Role of CEO Duality: Evidence from Selected Countries. Sustainability. 2023; 15(7):5643. https://doi.org/10.3390/su15075643

Chicago/Turabian StyleEnam, Marghoob, Syed Noorul Shajar, and Niladri Das. 2023. "Non-Monotonic Relationship between Corporate Governance and Banks’ Operating Performance—The Moderating Role of CEO Duality: Evidence from Selected Countries" Sustainability 15, no. 7: 5643. https://doi.org/10.3390/su15075643