Effect of Green Intellectual Capital Practices on the Competitive Advantage of Companies: Evidence from Polish Companies

Abstract

:1. Introduction

- -

- Which green human capital practices are key to the competitiveness of organizations in the Polish reality?

- -

- Which green organizational capital practices are key to improve the competitiveness of the organization?

- -

- Which green relational capital practices develop the competitive advantage of enterprises?

- -

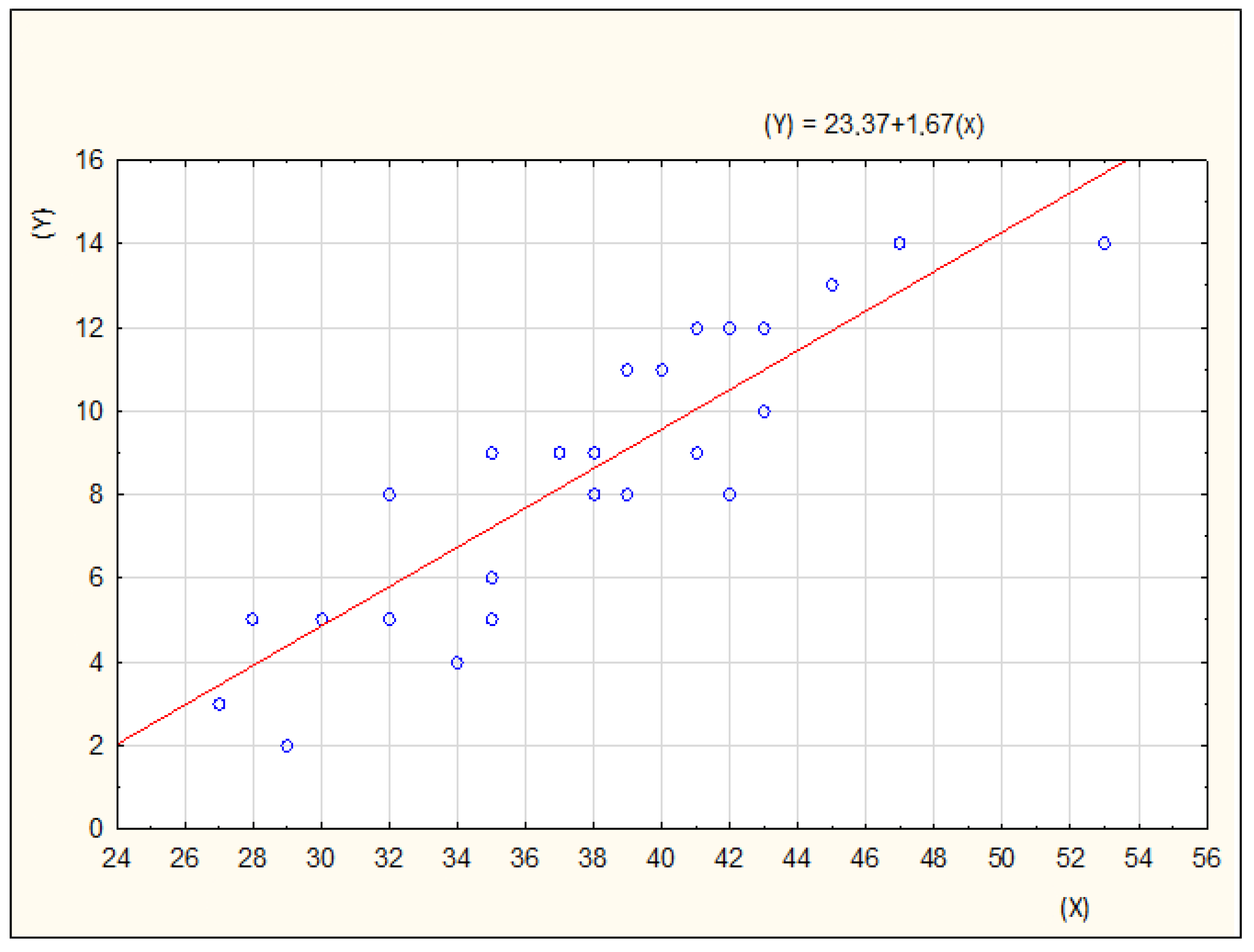

- Is there a relationship between the evaluation of the impact of GIC practices on the competitiveness of the organization and their implementation?

- -

- Is there a difference in the evaluation of the impact of GIC practices on company competitiveness and regarding their implementation depending on the form of company capital ownership?

2. Theoretical Background and Hypotheses Development

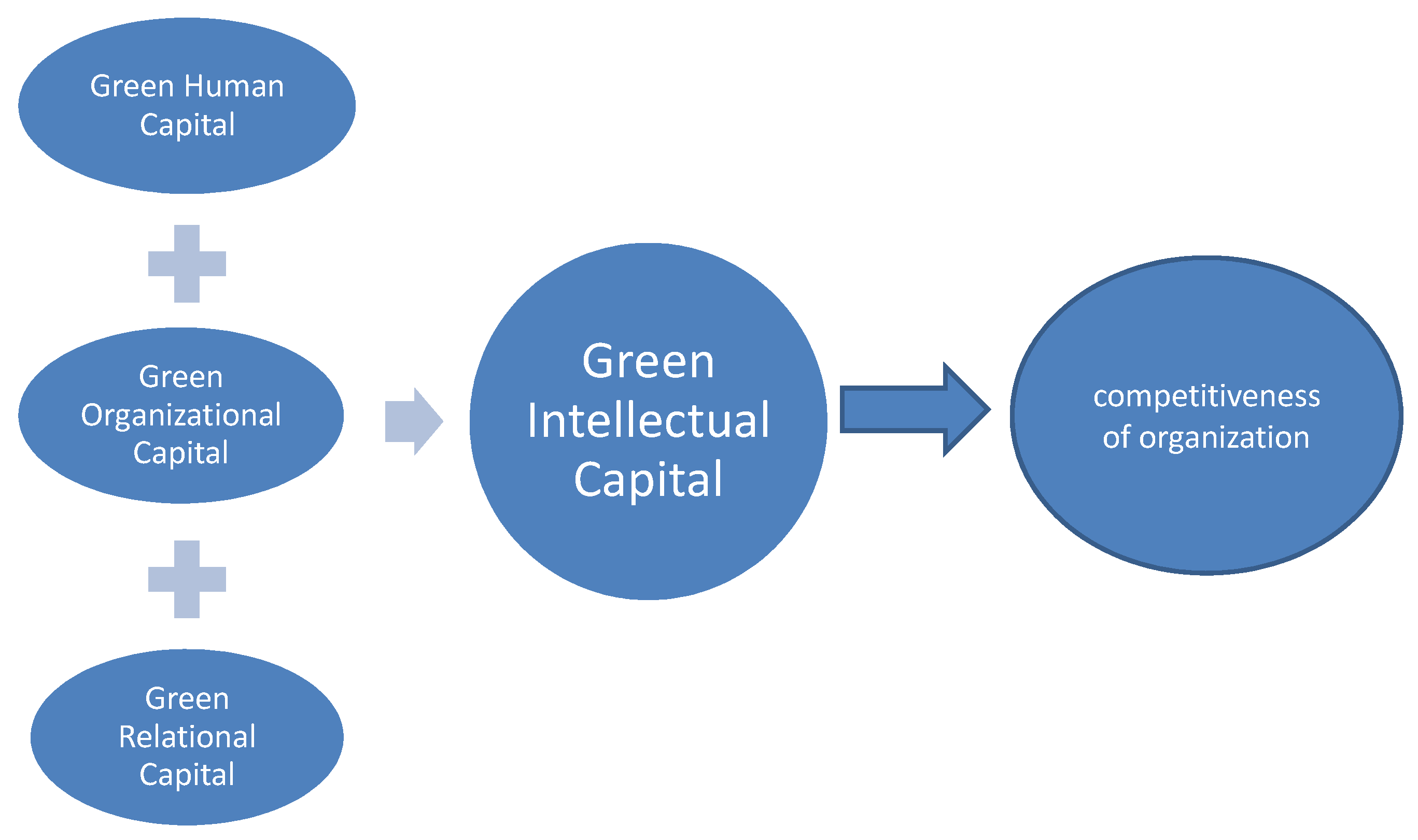

2.1. Definition and Classification of Intellectual Capital

2.2. Intellectual Capital and Company Performance

2.3. Specificity of Green Intellectual Capital

- -

- Green human capital (GHC);

- -

- Green organizational capital (GOC), also referred to as structural;

- -

- Green relational capital (GRC).

3. Materials and Methods

- -

- Green human capital (practices 1–12);

- -

- Green organizational capital (practices 13–23);

- -

- Green relational capital (practices 24–30).

4. Results

- -

- Financial bonuses for pro-environmental achievements (practice 2), the average impact of which was 2.90.

- -

- Implementationof a business model based on green innovation (practice 19), the average impact of which was assessed at 2.73;

- -

- Investing in environmental training for employees (practice 1), the average impact of which was 2.71;

- -

- Implementation of the system of environmental management (practice 14), with an impact average of 2.65;

- -

- Inclusion of environmental goals in company strategy (practice 13), with an impact average of 2.61.

- -

- Promoting ecological image on the labor market (practice 11)—average impact of 1.51;

- -

- Using ecological competence as a criterion for evaluating candidates applying for a job (practice 12), with an impact average of 1.55;

- -

- Taking into account pro-ecological attitudes and behaviors in the organization’s ethical code (practice 10)—average impact of 1.74;

- -

- Supporting sharing ecological knowledge (practice 9)—average impact of 1.75;

- -

- Charitable support for environmental initiatives (practice 30), the mean impact of which was at the level of 1.77.

- -

- Awarding financial bonuses for pro-environmental achievements (95%);

- -

- Investing in environmental training for employees (90%);

- -

- Informing employees about their contribution to the company’s achievements in the area of ecological efficiency (74.7%);

- -

- Implementing an environmental management system (71.3%);

- -

- Having an environmental knowledge management system (69.3%);

- -

- Including ecological goals in the company’s strategy (68%).

5. Discussion

6. Conclusions

- -

- Measuring the level of expenditure regarding the formation of individual GIC components;

- -

- Analyzing sub-indices for individual GIC components (i.e., environmental trainings, ecological initiatives, ecological patents, suppliers following the principles of eco-development);

- -

- Drafting GIC-related reports for internal and external stakeholders.

7. Limitations and Future Research

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

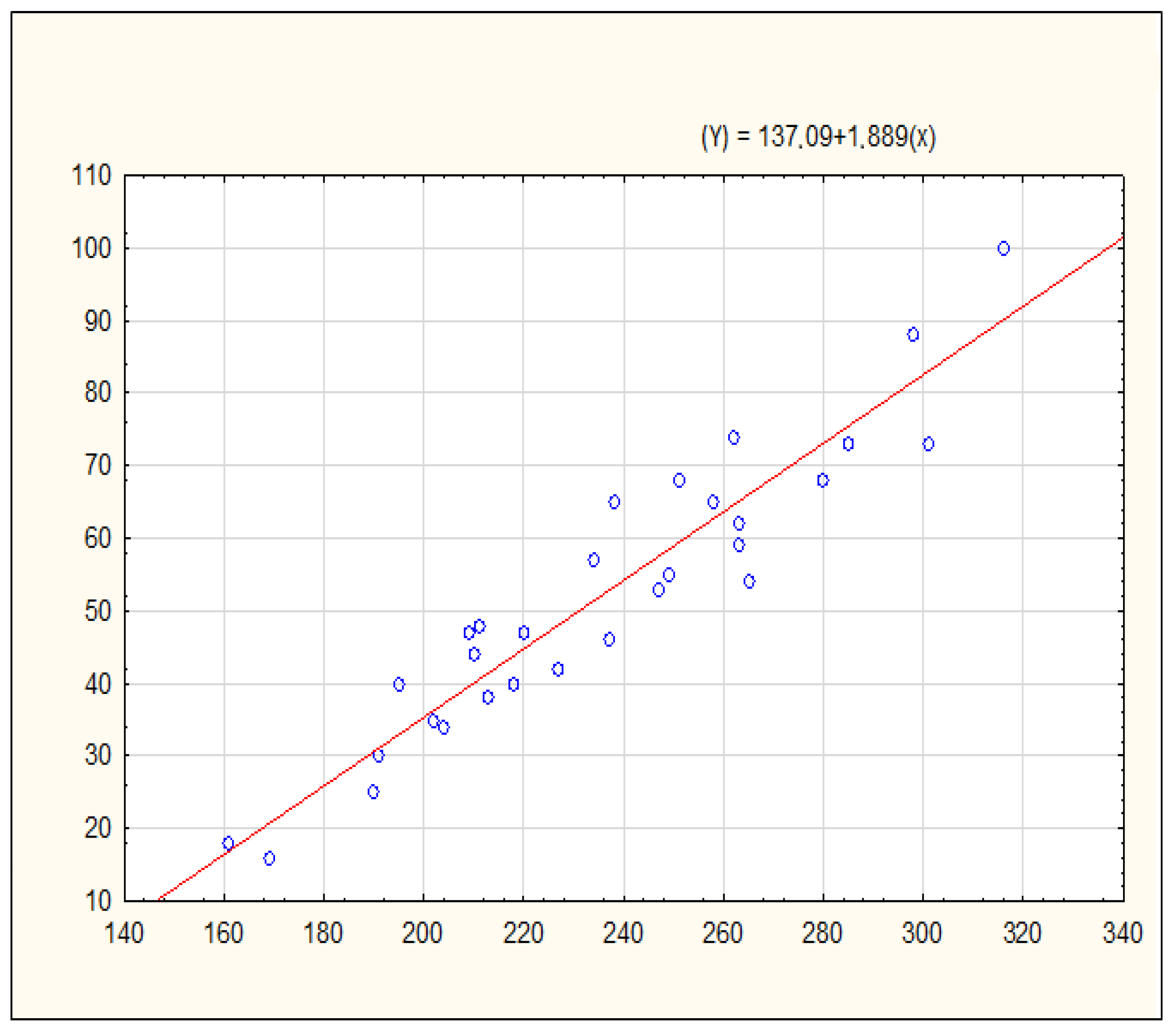

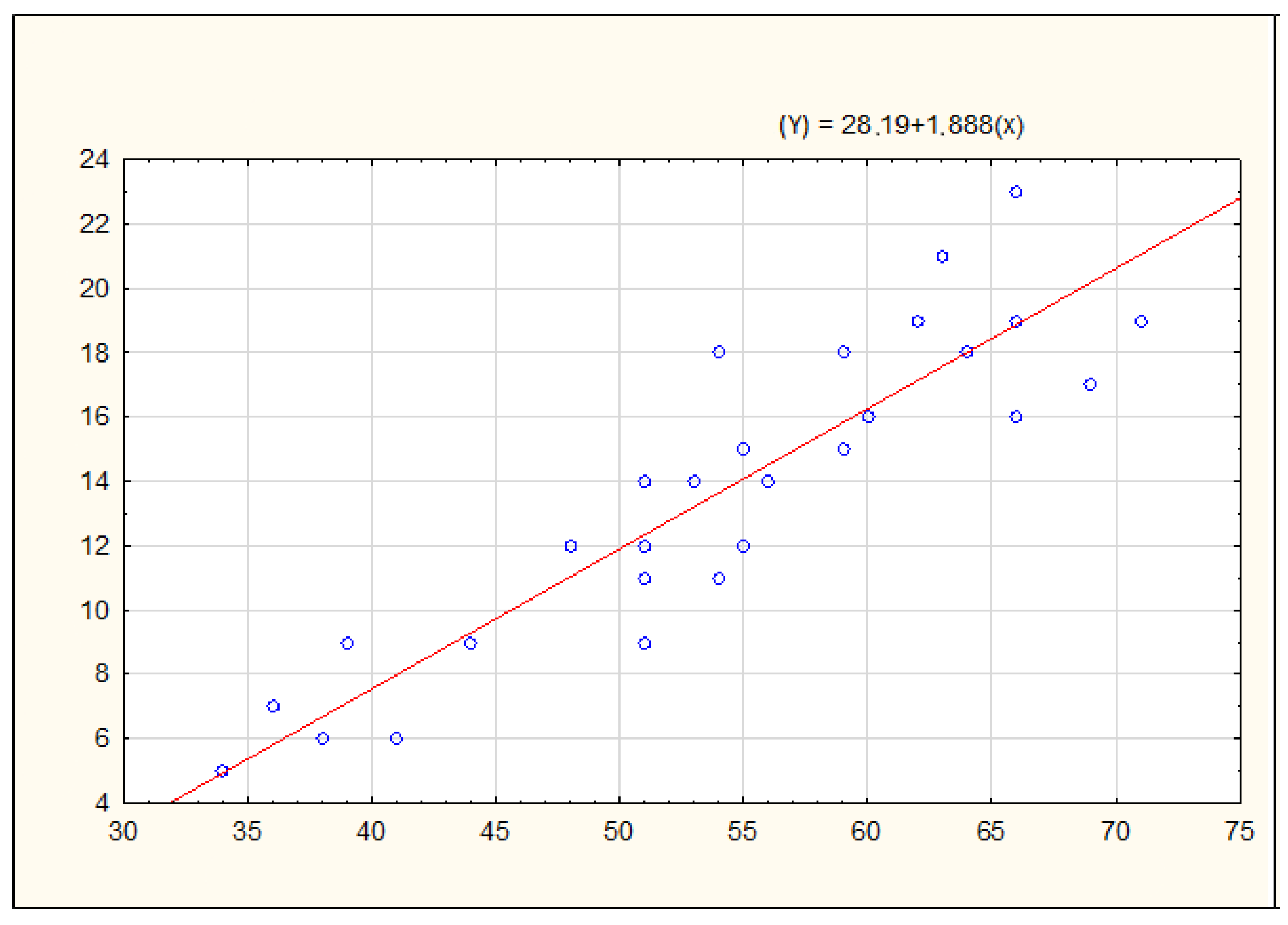

| Practice No. | Companies with Polish capital | Companies with Foreign Capital | Companies with Mixed Capital | |||

|---|---|---|---|---|---|---|

| Aggregate Evaluation of Practices’ Impact on the Competitiveness of the Organization (X) | Number of Enterprises Performing the Practices (Y) | Aggregate Evaluation of Practices’ Impact on the Competitiveness of the Organization (X) | Number of Enterprises Performing the Practices (Y) | Aggregate Evaluation of Practices’ Impact on the Competitiveness of the Organization (X) | Number of Enterprises Performing the Practices (Y) | |

| 1 | 298 | 88 | 63 | 21 | 45 | 13 |

| 2 | 316 | 100 | 66 | 23 | 53 | 14 |

| 3 | 247 | 53 | 53 | 14 | 43 | 10 |

| 4 | 227 | 42 | 44 | 9 | 34 | 4 |

| 5 | 204 | 34 | 51 | 12 | 38 | 8 |

| 6 | 234 | 57 | 53 | 14 | 35 | 9 |

| 7 | 238 | 65 | 54 | 18 | 37 | 9 |

| 8 | 262 | 74 | 59 | 18 | 39 | 11 |

| 9 | 191 | 30 | 36 | 7 | 35 | 6 |

| 10 | 190 | 25 | 41 | 6 | 30 | 5 |

| 11 | 161 | 18 | 38 | 6 | 27 | 3 |

| 12 | 169 | 16 | 34 | 5 | 29 | 2 |

| 13 | 280 | 68 | 64 | 18 | 47 | 14 |

| 14 | 285 | 73 | 71 | 19 | 41 | 9 |

| 15 | 237 | 46 | 66 | 16 | 32 | 8 |

| 16 | 251 | 68 | 62 | 19 | 41 | 12 |

| 17 | 258 | 65 | 66 | 19 | 38 | 8 |

| 18 | 213 | 38 | 39 | 9 | 32 | 5 |

| 19 | 218 | 40 | 51 | 11 | 38 | 8 |

| 20 | 249 | 55 | 54 | 11 | 38 | 9 |

| 21 | 220 | 47 | 48 | 12 | 32 | 8 |

| 22 | 301 | 73 | 69 | 17 | 40 | 11 |

| 23 | 263 | 59 | 59 | 15 | 43 | 12 |

| 24 | 263 | 62 | 60 | 16 | 42 | 12 |

| 25 | 210 | 44 | 55 | 12 | 35 | 5 |

| 26 | 202 | 35 | 51 | 9 | 42 | 8 |

| 27 | 211 | 48 | 55 | 15 | 28 | 5 |

| 28 | 209 | 47 | 51 | 14 | 30 | 5 |

| 29 | 265 | 54 | 56 | 14 | 39 | 8 |

| 30 | 195 | 40 | 41 | 6 | 30 | 5 |

References

- Mubarik, S.; Naghavi, N.; Mubarik, M.F. Governance-led intellectual capital disclosure: Empirical evidence from Pakistan. Humanit. Soc. Sci. Lett. 2019, 7, 141–155. [Google Scholar] [CrossRef]

- Jones, T.M.; Harrison, J.S.; Felps, W. How applying instrumental stakeholder theory can provide sustainable competitive advantage. Acad. Manag. Rev. 2018, 43, 371–391. [Google Scholar] [CrossRef] [Green Version]

- Rupcic, N. Organizational learning in stakeholder relations. Learn. Organ. 2019, 26, 219–231. [Google Scholar] [CrossRef]

- Paillé, P.; Chen, Y.; Boiral, O.; Jin, J. The impact of human resource management on environmental performance: An employee-level study. J. Bus. Ethics 2014, 121, 451–466. [Google Scholar] [CrossRef]

- Chen, Y.S. The Positive Effect of Green Intellectual Capital on Competitive Advantages of Firms. J. Bus. Ethic 2008, 77, 271–286. [Google Scholar] [CrossRef]

- Yusoff, Y.M.; Omar, M.K.; Zaman, M.D.K. Practice of green intellectual capital. Evidence from Malaysian manufacturing sector 1st International Postgraduate Conference on Mechanical Engineering (IPCME2018). In IOP Conference Series: Materials Science and Engineering; IOP Publishing: Bristol, UK, 2019; Volume 469, p. 012008. [Google Scholar] [CrossRef]

- Rezaei, S.; Izadi, M.; Jokar, I. The relationship between green intellectual capital and competitive advantages. Int. Bus. Manag. 2016, 10, 4743–4748. [Google Scholar] [CrossRef]

- Yong, J.Y.; Yusliza, M.-Y.; Ramayah, Y.; Olawole Fawehinmi, O. Nexus between green intellectual capital and green human resource management. J. Clean. Prod. 2019, 215, 364–374. [Google Scholar] [CrossRef]

- Yusliza, M.-Y.; Yong, J.Y.; Tanveer, M.I.; Ramayah, T.; Faezah, J.N.; Muhammad, Z. A structural model of the impact of green intellectual capital on sustainable performance. J. Clean. Prod. 2020, 249, 119334. [Google Scholar] [CrossRef]

- Yadiati, W.; Nissa, N.; Paulus, S.; Suharman, H.; Meiryani, M. The role of green intellectual capital and organizational reputation in influencing environmental performance. Int. J. Energy Econ. Policy 2019, 9, 261–268. [Google Scholar] [CrossRef] [Green Version]

- Malik, S.Y.; Cao, Y.; Mughal, Y.H.; Kundi, G.M.; Mughal, M.H.; Ramayah, T. Pathways towards sustainability in organizations: Empirical evidence on the role of green human resource management practices and green intellectual capital. Sustainability 2020, 12, 3228. [Google Scholar] [CrossRef] [Green Version]

- Lev, B. Intangibles: Management, Measurement, and Reporting; The Brookings Institution: Washington, DC, USA, 2001. [Google Scholar]

- Hall, R. The Strategic analysis of intangible resources. Strateg. Manag. J. 1992, 13, 135–144. [Google Scholar] [CrossRef]

- Stewart, T. The New Wealth of Organizations; Doubleday: New York, NY, USA, 1997. [Google Scholar]

- Roos, J.; Roos, G.; Dragonetti, N.C.; Edvinsson, L. Intellectual Capital: Navigating in the New Business Landscape; Macmillan Business: London, UK, 1997. [Google Scholar]

- Klein, D.A.; Prusak, L. Characterising Intellectual Capital; Ernst & Young: Cambridge, UK, 1994. [Google Scholar]

- Sullivan, P.H. Value-Driven Intellectual Capital: How to Convert Intangible Corporate Assets into Market Value; John Wiley & Sons: Toronto, ON, Canada, 2000. [Google Scholar]

- Edvinsson, L.; Malone, M.S. Intellectual Capital: Realizing Your Company’s True Value by Finding Its Hidden Brainpower; Harper Business: New York, NY, USA, 1997. [Google Scholar]

- Chaharbaghi, K.; Cripps, S. Intellectualcapital: Direction, not blind faith. J. Intellect. Cap. 2006, 7, 29–32. [Google Scholar] [CrossRef]

- Youndt, M.A.; Subramaniam, M.; Snell, S. Intellectual Capital profiles. An examination of investments and returns. J. Manag. Stud. 2004, 16, 337–361. [Google Scholar] [CrossRef]

- Holton, E.E.; Yamkovenko, B. Strategic intellectual capital development: A defining paradigm for HRD? Hum. Resour. Dev. Rev. 2008, 7, 270–291. [Google Scholar] [CrossRef]

- Tayles, M.; Pike, R.; Sofian, S. Intellectual capital, management accounting practices and corporate performance. Account. Audit. Account. J. 2007, 20, 522–548. [Google Scholar] [CrossRef]

- Yang, C.C.; Lin, C.Y.Y. Does intellectual capital mediate the relationship between HRM and organizational performance? Perspective of a healthcare industry in Taiwan. Int. J. Hum. Resour. Manag. 2009, 20, 1965–1984. [Google Scholar] [CrossRef]

- Zerenler, M.; Gozlu, S. Impact of intellectual capital on exportation performance: Research on the Turkish automotive supplier. J. Transnatl. Manag. 2008, 13, 318–341. [Google Scholar] [CrossRef]

- Walsh, K.; Enz, C.; Canina, L. The impact of strategic orientation on intellectual capital investments in customer service firms. J. Serv. Res. 2008, 10, 300–317. [Google Scholar] [CrossRef]

- Ahmed, S.S.; Guozhu, J.; Mubarik, S.; Khan, M.; Khan, E. Intellectual capital and business performance: The role of dimensions of absorptive capacity. J. Intellect. Cap. 2019, 21, 23–39. [Google Scholar] [CrossRef]

- Sumedrea, S. Intellectual Capital and Firm Performance: A Dynamic Relationship in Crisis Time. Procedia Econ. Financ. 2013, 6, 137–144. [Google Scholar] [CrossRef] [Green Version]

- Guthrie, J.; Abeysekera, I. Human capital reporting in a developing nation. Br. Account. Rev. 2004, 36, 251–268. [Google Scholar]

- Muda, S.; Rahman, R.C.A. SMEs Performance: Does Intellectual Capital Matter? Int. J. Adm. Gov. 2015, 1, 5–10. [Google Scholar]

- Egbu, C.O. Managing knowledge and intellectual capital for improved organizational innovations in the construction industry: An examination of critical success factors. Engineering. Constr. Archit. Manag. 2004, 11, 301–315. [Google Scholar] [CrossRef]

- Wagner, M. Environmental management activities and sustainable HRM in German manufacturing firms–incidence, determinants, and outcomes. Ger. J. Hum. Resour. Manag. 2011, 25, 157–177. [Google Scholar] [CrossRef]

- Cinquini, L.; Passetti, E.; Tenucci, A.; Frey, M. Analyzing intellectual capital information in sustainability reports: Some empirical evidence. J. Intellect. Cap. 2012, 13, 531–561. [Google Scholar] [CrossRef]

- Sveiby, K.E. The New Organisational Wealth, Managing and Measuring Knowledge Based Assets; Berrett-Koehler Publisher: San Francisco, CA, USA, 1997. [Google Scholar]

- Mention, A.L.; Bontis, N. Intellectual capital and performance within the banking sector of Luxembourg and Belgium. J. Intellect. Cap. 2013, 14, 286–309. [Google Scholar] [CrossRef]

- Tseng, C.; Goo, Y.J. Intellectual capital and corporate value in an emerging economy. Empirical study of Taiwanese manufacturers. RD Manag. 2005, 35, 187–202. [Google Scholar]

- Cohen, W.M.; Levinthal, D.A. Absorptive capacity: A new perspective on learning and innovation. Adm. Sci. Q. 1990, 35, 128–152. [Google Scholar] [CrossRef]

- Jansen, J.J.; Van Den Bosch, F.A.; Volberda, H.W. Managing potential and realized absorptive capacity: How do organizational antecedents matter? Acad. Manag. J. 2005, 48, 999–1015. [Google Scholar] [CrossRef] [Green Version]

- Komnenic, B.; Pokrajčić, D. Intellectual capital and corporate performance of MNCs in Serbia. J. Intellect. Cap. 2012, 13, 106–119. [Google Scholar] [CrossRef]

- Yahya, N.A.; Arshad, R.; Kamaluddin, A. Measuring green intellectual capital in Malaysian environmentally sensitive companies. Int. J. Bus. Manag. Studies 2014, 1, 92–96. [Google Scholar]

- Bontis, N. Managing organizational knowledge by diagnosing intellectual capital: Framing and advancing the state of the field. Int. J. Technol. Manag. 1999, 18, 433–462. [Google Scholar] [CrossRef]

- Ortiz, B.; Donate, M.J.; Guadamillas, F. Inter-organizational social capital as an antecedent of a firm’s knowledge identification capability and external knowledge acquisition. J. Knowl. Manag. 2018, 22, 1332–1357. [Google Scholar] [CrossRef]

- Pal, K.; Soriya, S. IC performance of Indian pharmaceutical and textile industry. J. Intellect. Cap. 2012, 13, 120–137. [Google Scholar] [CrossRef]

- Maditinos, D.; Chatzoudes, D.; Tsairidis, C.; Theriou, G. The impact of intellectual capital on firms’ market value and financial performance. J. Intellect. Cap. 2011, 12, 132–151. [Google Scholar] [CrossRef] [Green Version]

- Riahi-Belkaoui, A. Intellectual capital and firm performance of US multinational firms. J. Intellect. Cap. 2003, 4, 215–226. [Google Scholar] [CrossRef]

- Wang, J.C. Investigating market value and intellectual capital for S&P 500. J. Intellect. Cap. 2008, 9, 546–563. [Google Scholar]

- Tan, H.P.; Plowman, D.; Hancock, P. Intellectual capital and financial returns ofcompanies. J. Intellect. Cap. 2007, 8, 76–95. [Google Scholar] [CrossRef]

- Chang, C.; Lin, M.J. Enhancing green competitive advantage through environmental commitment and green intangible assets: In the information and electronics industry of Taiwan. In Proceedings of the PICMET 2010 Technology Management for Global Economic Growth, Phuket, Thailand, 18–22 July 2010; pp. 1–8. [Google Scholar]

- Sharabati, A.A.; Jawad, S.N.; Bontis, N. Intellectual capital and business performance in the pharmaceutical sector of Jordan. Manag. Decis. 2010, 48, 105–131. [Google Scholar] [CrossRef]

- Zeghal, D.; Maaloul, A. Analyzing value added as an indicator of intellectual capital and its consequences on company performance. J. Intellect. Cap. 2010, 11, 39–60. [Google Scholar] [CrossRef] [Green Version]

- Clarke, M.; Seng, D.; Whiting, R.H. Intellectual capital and firm performance in Australia. J. Intellect. Cap. 2011, 12, 505–530. [Google Scholar] [CrossRef] [Green Version]

- Narwal, K.P.; Deep, R. The Relationship between Intellectual Capital and Financial Performance: An Empirical Study of Indian Pharmaceutical Industry. MERC Glob. Int. J. Manag. 2014, 2, 151–169. [Google Scholar]

- Wang, Z.; Wang, N.; Liang, H. Knowledge sharing, intellectual capital and firm performance. Manag. Decis. 2014, 52, 230–258. [Google Scholar] [CrossRef] [Green Version]

- Syahcharia, D.H.; Sahbanb, M.A. The Impact of Intellectual Capital and Knowledge Management on Competitive Advantage. Int. J. Innov. Creat. Chang. 2019, 10, 261–272. [Google Scholar]

- Firer, S.; Williams, S.M. Intellectual capital and traditional measures of corporate performance. J. Intellect. Cap. 2003, 4, 348–360. [Google Scholar] [CrossRef]

- Kujansivu, P.; Lonnqvist, A. How do investments in intellectual capital create profits? Int. J. Learn. Intellect. Cap. 2007, 4, 256–275. [Google Scholar] [CrossRef]

- Kamath, G.B. Intellectual capital and corporate performance in Indian pharmaceutical industry. J. Intellect. Cap. 2008, 9, 684–704. [Google Scholar] [CrossRef]

- Chan, K.H. Impact of intellectual capital on organisational performance: An empirical study of companies in the Hang Seng Index (part 2). Learn. Organ. 2009, 16, 22–39. [Google Scholar] [CrossRef]

- Chan, K.H. Impact of intellectual capital on organisational performance: An empirical study of companies in the Hang Seng Index (part 1). Learn. Organ. 2009, 16, 4–21. [Google Scholar] [CrossRef]

- Ghosh, S.; Mondal, A. Indian software and pharmaceutical sector IC and financial performance. J. Intellect. Cap. 2009, 10, 1469–1930. [Google Scholar] [CrossRef]

- Mehralian, G.; Rajabzadeh, A.; Sadeh, M.R.; Rasekh, H.R. Intellectual capital and corporate performance in Iranian pharmaceutical industry. J. Intellect. Cap. 2012, 13, 138–158. [Google Scholar] [CrossRef]

- Sambasivan, M.; Bah, S.M.; Jo-Ann, H. Making the Case for Operating Green: Impact of Environmental Proactivity on Multiple Performance Outcomes of Malaysian Firms. J. Clean. Prod. 2013, 42, 69–82. [Google Scholar] [CrossRef]

- Januškaite, V.; Užiene, L. Intellectual Capital as a Factor of Sustainable Regional Competitiveness. Sustainability 2018, 10, 4848. [Google Scholar] [CrossRef] [Green Version]

- Liu, C. Developing green intellectual capital in companies by AHP. In Proceedings of the 2010 8th International Conference on Supply Chain Management and Information, Hong Kong, China, 6–9 October 2010; pp. 1–5. [Google Scholar]

- Villena, V.H.; Revilla, E.; Choi, T.Y. The dark side of buyer-supplier relationships: A social capital perspective. J. Oper. Manag. 2011, 29, 561–576. [Google Scholar] [CrossRef]

- Porter, M. Competitive Strategy: Technique for Analyzing Industries and Competitors; The Free Press: New York, NY, USA, 1998. [Google Scholar]

- Chen, M.; Cheng, S.; Hwang, Y. An empirical investigation of the relationship between intellectual capital and firms’ market value and financial performance. J. Intellect. Cap. 2005, 6, 159–176. [Google Scholar] [CrossRef]

- Barney, J. Firm resources and Sustained Competitive Advantage. J. Manag. 1991, 17, 99–120. [Google Scholar] [CrossRef]

- Nivlouei, F.B.; Khass, E.D. The Role of Green Intellectual Capital Management in Acquiring Green Competitive Advantage for Companies. Int. J. Manag. Res. Dev. 2014, 4, 41–58. [Google Scholar]

- Sidik, M.H.J.; Yadiati, W.; Hoyoung Lee, H.; Nadeem Khalid, N. The Dynamic Association of Energy, Environmental Management Accounting and Green Intellectual Capital with Corporate Environmental Performance and Competitive Advantages. Int. J. Energy Econ. Policy 2019, 9, 379–386. [Google Scholar] [CrossRef] [Green Version]

- Susandya, A.A.; Kumalasari, P.D.; Manuari, I.A.R. The Role of Green Intellectual Capital on Competitive Advantage: Evidence from Balinese Financial Institution. Int. J. Dyn. Econ. Bus. 2019, 3, 227–242. [Google Scholar] [CrossRef]

- Zhang, X.; Shen, L. Green strategy for gaining competitive advantage in housing development: A China study. J. Clean. Prod. 2011, 19, 157–167. [Google Scholar] [CrossRef]

- Crassous, T.; Gassmann, J. Gaining Competitive Advantage through Green Marketing. 2011, pp. 1–73. Available online: https://www.diva-portal.org/smash/get/diva2:536912/fulltext01.pdf (accessed on 16 September 2022).

- Papadasa, K.-K.; Avlonitisb, G.J.; Carriganc, M.; Pihad, L. The interplay of strategic and internal green marketing orientation on competitive advantage. J. Bus. Res. 2019, 104, 632–643. [Google Scholar] [CrossRef]

- Li, J.; Sun, X.; Li, G. Relationships among green brand, brand equity and firm performance: Empirical evidence from China. Transform. Bus. Econ. 2018, 17, 221–236. [Google Scholar]

- Lin, Y.-H.; Chen, Y.-S. Determinants of green competitive advantage: The roles of green knowledge sharing, green dynamic capabilities, and green service innovation. Qual. Quant. 2016, 51, 1663–1685. [Google Scholar] [CrossRef]

- Qiu, L.; Jie, X.; Wang, Y.; Zhao, M. Green product innovation, green dynamic capability, and competitive advantage: Evidence from Chinese manufacturing enterprises. Corp. Soc. Responsib. Environ. Manag. 2020, 27, 146–165. [Google Scholar] [CrossRef]

- Porter, M.E.; Claas van der Linde, C. Green and Competitive: Ending the Stalemate, Harvard Business Review, September–October 1995. Available online: https://hbr.org/1995/09/green-and-competitive-ending-the-stalemate (accessed on 11 October 2022).

- Yahya, N.A.; Arshad, R.; Kamaluddin, A.; Rahman, R.A. Green Intellectual Capital and Firm Competitive Advantage: Evidence from Malaysian Manufacturing Firms. J. Soc. Sci. Res. 2019, 5, 463–471. [Google Scholar]

- Jirawuttinunt, S.; Limsuwan, K. The effect of Green Human Resource Management on Performance of Certified ISO 14000 Businesses in Thailand UTCC. Int. J. Bus. Econ. 2019, 11, 168–185. [Google Scholar]

- NR, E.; Yurniwati, Y. Green Intellectual Capital and Financial Performance of Manufacturing Companies in Indonesia. Adv. Econ. Bus. Manag. Res. 2018, 57, 57–62. [Google Scholar]

| Green Intellectual Capital Components | Practice No. | Practice |

|---|---|---|

| Green Human Capital | 1 | The company invests in environmental training for employees |

| 2 | The company awards financial bonuses for pro-environmental achievements | |

| 3 | The company provides flexible working hours in order to undertake pro-ecological activities | |

| 4 | The company evaluates employees’ ecological competences | |

| 5 | The company uses public praise/awards/certificates for environmental activities | |

| 6 | Responsibility for the environment is included in the job instructions | |

| 7 | The company encourages its employees to be involved in waste reduction and pollution prevention | |

| 8 | The company informs employees about their contribution to the company’s achievements in the area of ecological efficiency | |

| 9 | The company supports sharing ecological knowledge | |

| 10 | The organization’s ethical code considers pro-ecological attitudes and behaviors | |

| 11 | The company promotes its ecological image on the labor market | |

| 12 | The company uses ecological competence as a criterion for evaluating candidates applying for a job | |

| Green Organizational Capital | 13 | The company includes ecological goals in the company’s strategy |

| 14 | The company has implemented an environmental management system | |

| 15 | Ecological values are put into the company’s mission | |

| 16 | The organization conducts environmental audits | |

| 17 | The organization implements a proactive environmental strategy | |

| 18 | The organization implements a reactive environmental strategy | |

| 19 | The organization implements a business model based on green innovation | |

| 20 | The company improves green corporate culture | |

| 21 | The company runs an environmental analysis of the product lifecycle | |

| 22 | The company has an environmental knowledge management system | |

| 23 | The organization has created a department responsible for implementing the environmental strategy | |

| Green Relational Capital | 24 | The company shares information related to environmental aspects with key customers to improve green practices within the supply chain |

| 25 | The company cooperates with key suppliers in the implementation of environmental initiatives | |

| 26 | The company applies green marketing | |

| 27 | The company cooperates only with partners who respect ecological standards | |

| 28 | The company prepares environmental reports | |

| 29 | The company cares about its green image | |

| 30 | The company is involved in charity work for environmental initiatives |

| Criterion | Number of Enterprises | Percentage |

|---|---|---|

| Employment number: | ||

| 50–249 employees | 87 | 58.0 |

| 250–499 employees | 23 | 15.3 |

| 500–749 employees | 32 | 21.3 |

| Over 500 employees | 8 | 5.3 |

| Industry experience: | ||

| Up to 5 years | 11 | 7.3 |

| 5–7 years | 23 | 15.3 |

| 7–9 years | 47 | 31.3 |

| Over 9 years | 69 | 46.0 |

| Scope of operations: | ||

| International | 79 | 52.6 |

| European | 33 | 22.0 |

| National | 27 | 18.0 |

| Regional | 6 | 4.0 |

| Local | 5 | 3.4 |

| Capital structure | ||

| Polish | 101 | 67.3 |

| Foreign | 28 | 18.6 |

| Mixed | 21 | 14.0 |

| Practice No. | Aggregate Assessment of Impact (Points) | Mean Impact of Practice (Points) | Median (Points) | Modal Value (Points) | Standard Deviation (Points) | Asymmetry (Points) | Kurtosis (Points) |

|---|---|---|---|---|---|---|---|

| 1 | 406 | 2.71 | 3 | 3 | 1.256 | 0.078 | −1.018 |

| 2 | 435 | 2.90 | 3 | 3 | 1.151 | −0.150 | −0.891 |

| 3 | 343 | 2.29 | 2 | 1 | 1.244 | 0.477 | −0.935 |

| 4 | 305 | 2.03 | 2 | 1 | 1.255 | 0.947 | −0.314 |

| 5 | 293 | 1.95 | 1 | 1 | 1.228 | 0.950 | −0.350 |

| 6 | 322 | 2.15 | 2 | 1 | 1.228 | 0.553 | −1.027 |

| 7 | 329 | 2.19 | 2 | 1 | 1.224 | 0.579 | −0.905 |

| 8 | 360 | 2.40 | 2 | 1 | 1.210 | 0.387 | −0.908 |

| 9 | 262 | 1.75 | 1 | 1 | 1.100 | 1.285 | 0.614 |

| 10 | 261 | 1.74 | 1 | 1 | 1.065 | 1.214 | 0.321 |

| 11 | 226 | 1.51 | 1 | 1 | 0.925 | 1.862 | 2.785 |

| 12 | 232 | 1.55 | 1 | 1 | 0.924 | 1.802 | 2.940 |

| 13 | 391 | 2.61 | 3 | 3 | 1.269 | 0.017 | −1.192 |

| 14 | 397 | 2.65 | 3 | 1 | 1.352 | 0.023 | −1.429 |

| 15 | 335 | 2.23 | 2 | 1 | 1.318 | 0.540 | −1.171 |

| 16 | 354 | 2.36 | 2 | 1 | 1.265 | 0.320 | −1.250 |

| 17 | 362 | 2.41 | 2 | 1 | 1.391 | 0.439 | −1.154 |

| 18 | 284 | 1.89 | 1 | 1 | 1.238 | 1.131 | 0.013 |

| 19 | 410 | 2.73 | 3 | 4 | 1.359 | -0.040 | −1.400 |

| 20 | 307 | 2.05 | 1 | 1 | 1.266 | 0.817 | −0.680 |

| 21 | 441 | 2.94 | 3 | 4 | 1.399 | 0.587 | −1.056 |

| 22 | 300 | 2.00 | 1 | 1 | 1.259 | 0.901 | −0.466 |

| 23 | 365 | 2.43 | 2.5 | 1 | 1.223 | 0.145 | −1.340 |

| 24 | 365 | 2.43 | 2 | 1 | 1.318 | 0.351 | −1.142 |

| 25 | 300 | 2.00 | 1 | 1 | 1.295 | 0.864 | −0.713 |

| 26 | 295 | 1.97 | 1 | 1 | 1.308 | 0.993 | −0.432 |

| 27 | 294 | 1.96 | 1 | 1 | 1.164 | 0.778 | −0.772 |

| 28 | 290 | 1.93 | 1 | 1 | 1.145 | 0.893 | −0.413 |

| 29 | 360 | 2.40 | 2 | 1 | 1.447 | 0.418 | −1.361 |

| 30 | 266 | 1.77 | 1 | 1 | 1.112 | 1.113 | −0.089 |

| Green Intellectual Capital Components | Practice No. | Mean Impact of Practice (Points) | Mean Impact of Component (Points) |

|---|---|---|---|

| Green Human Capital | 1 | 2.71 | 2.1 |

| 2 | 2.90 | ||

| 3 | 2.29 | ||

| 4 | 2.03 | ||

| 5 | 1.95 | ||

| 6 | 2.15 | ||

| 7 | 2.19 | ||

| 8 | 2.40 | ||

| 9 | 1.75 | ||

| 10 | 1.74 | ||

| 11 | 1.51 | ||

| 12 | 1.55 | ||

| Green Organizational Capital | 13 | 2.61 | 2.4 |

| 14 | 2.65 | ||

| 15 | 2.23 | ||

| 16 | 2.36 | ||

| 17 | 2.41 | ||

| 18 | 1.89 | ||

| 19 | 2.73 | ||

| 20 | 2.05 | ||

| 21 | 2.94 | ||

| 22 | 2.00 | ||

| 23 | 2.43 | ||

| Green Relational Capital | 24 | 2.43 | 2.1 |

| 25 | 2.00 | ||

| 26 | 1.97 | ||

| 27 | 1.96 | ||

| 28 | 1.93 | ||

| 29 | 2.40 | ||

| 30 | 1.77 |

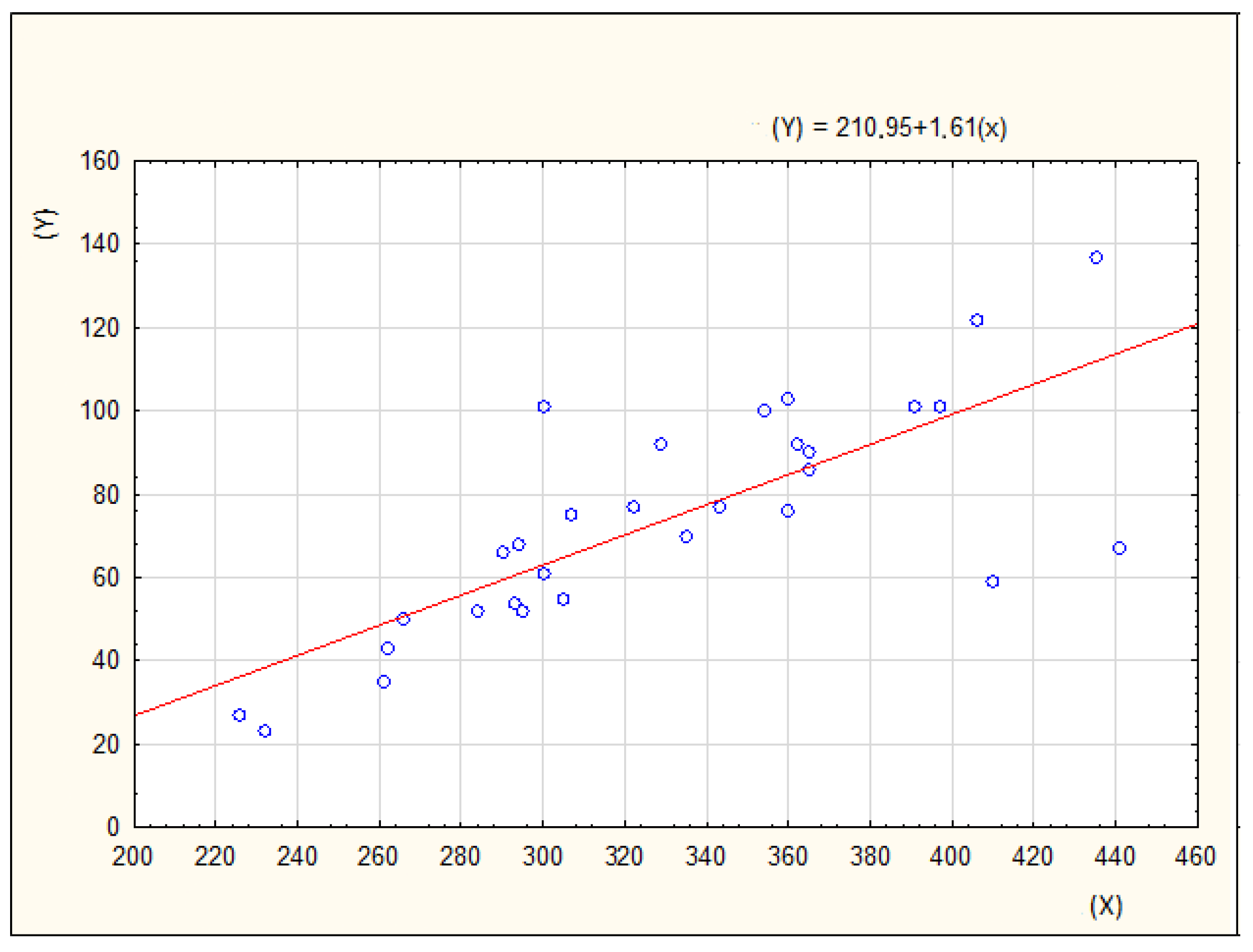

| Practice No. | Aggregate Evaluation of Practices’ Impact on the Competitiveness of the Organization (Variable X) | Number of Enterprises Pursuing the Practices (Variable Y) | Percentage of Enterprises Pursuing the Practices (%) |

|---|---|---|---|

| 1 | 406 | 135 | 90 |

| 2 | 435 | 141 | 95 |

| 3 | 343 | 81 | 54 |

| 4 | 305 | 59 | 39.3 |

| 5 | 293 | 56 | 37.3 |

| 6 | 322 | 78 | 52 |

| 7 | 329 | 95 | 63.3 |

| 8 | 360 | 112 | 74.7 |

| 9 | 262 | 49 | 32.7 |

| 10 | 261 | 37 | 24.7 |

| 11 | 226 | 29 | 19.3 |

| 12 | 232 | 25 | 16.7 |

| 13 | 391 | 102 | 68 |

| 14 | 397 | 107 | 71.3 |

| 15 | 335 | 73 | 48.7 |

| 16 | 354 | 105 | 70 |

| 17 | 362 | 88 | 58.7 |

| 18 | 284 | 51 | 34 |

| 19 | 410 | 52 | 34.7 |

| 20 | 307 | 74 | 49.3 |

| 21 | 441 | 66 | 44 |

| 22 | 300 | 104 | 69.3 |

| 23 | 365 | 89 | 59.3 |

| 24 | 365 | 87 | 58 |

| 25 | 300 | 63 | 42 |

| 26 | 295 | 50 | 33.3 |

| 27 | 294 | 70 | 46.7 |

| 28 | 290 | 60 | 40 |

| 29 | 360 | 73 | 48.7 |

| 30 | 266 | 39 | 26 |

| Practice No. | Evaluation of GIC Practices Impact on the Competitiveness of Organizations on a Scale of 1–5 | Implementation of GIC Practices (Data Shown in %) | ||||

|---|---|---|---|---|---|---|

| Companies with Polish Capital | Companies with Foreign Capital | Companies with Mixed Capital | Companies with Polish Capital | Companies with Foreign Capital | Companies with Mixed Capital | |

| 1 | 2.7 | 2.7 | 2.7 | 79.3 | 91.3 | 81.3 |

| 2 | 2.9 | 2.9 | 3.3 | 90.1 | 100.0 | 87.5 |

| 3 | 2.2 | 2.3 | 2.5 | 47.7 | 60.9 | 62.5 |

| 4 | 2.1 | 1.9 | 2.1 | 37.8 | 31.1 | 25.0 |

| 5 | 1.8 | 2.2 | 2.3 | 30.6 | 52.2 | 50.0 |

| 6 | 2.1 | 2.3 | 2.1 | 51.4 | 43.5 | 56.3 |

| 7 | 2.1 | 2.3 | 2.3 | 58.6 | 60.9 | 56.3 |

| 8 | 2.4 | 2.6 | 2.4 | 66.7 | 78.3 | 68.8 |

| 9 | 1.7 | 1.6 | 2.1 | 27.0 | 30.4 | 37.5 |

| 10 | 1.7 | 1.8 | 1.9 | 22.5 | 26.1 | 31.3 |

| 11 | 1.5 | 1.7 | 1.7 | 16.2 | 26.1 | 18.8 |

| 12 | 1.5 | 1.5 | 1.9 | 14.4 | 21.8 | 12.5 |

| 13 | 2.5 | 2.8 | 2.9 | 61.3 | 78.3 | 87.5 |

| 12 | 2.6 | 3.1 | 2.4 | 65.8 | 82.6 | 56.3 |

| 15 | 2.1 | 2.9 | 2.0 | 41.4 | 69.6 | 50.0 |

| 16 | 2.3 | 2.7 | 2.5 | 61.3 | 82.6 | 75.0 |

| 17 | 1.3 | 2.9 | 2.4 | 58.6 | 82.6 | 50.0 |

| 18 | 1.9 | 1.7 | 1.9 | 34.2 | 31.1 | 31.3 |

| 19 | 2.0 | 2.2 | 2.5 | 36.0 | 47.8 | 50.0 |

| 20 | 2.2 | 2.4 | 2.4 | 49.6 | 47.8 | 56.3 |

| 21 | 2.0 | 2.1 | 2.1 | 42.3 | 52.2 | 50.0 |

| 22 | 2.7 | 3.0 | 2.5 | 65.8 | 73.9 | 68.8 |

| 23 | 2.4 | 2.6 | 2.6 | 53.2 | 65.2 | 75.0 |

| 24 | 2.4 | 2.6 | 2.7 | 55.9 | 69.6 | 75.0 |

| 25 | 1.9 | 2.4 | 2.7 | 39.6 | 31.1 | 31.3 |

| 26 | 1.8 | 2.2 | 2.7 | 31.5 | 65.2 | 50.0 |

| 27 | 1.9 | 2.4 | 1.7 | 43.2 | 60.9 | 31.3 |

| 28 | 1.9 | 2.2 | 1.8 | 42.3 | 60.9 | 31.3 |

| 29 | 2.4 | 2.4 | 2.3 | 48.7 | 26.1 | 50.0 |

| 30 | 1.8 | 1.8 | 1.7 | 36.0 | 28.4 | 31.3 |

| Arithmetic mean | 2.1 | 2.3 | 2.3 | 46.9 | 57.6 | 51.3 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Bombiak, E. Effect of Green Intellectual Capital Practices on the Competitive Advantage of Companies: Evidence from Polish Companies. Sustainability 2023, 15, 4050. https://doi.org/10.3390/su15054050

Bombiak E. Effect of Green Intellectual Capital Practices on the Competitive Advantage of Companies: Evidence from Polish Companies. Sustainability. 2023; 15(5):4050. https://doi.org/10.3390/su15054050

Chicago/Turabian StyleBombiak, Edyta. 2023. "Effect of Green Intellectual Capital Practices on the Competitive Advantage of Companies: Evidence from Polish Companies" Sustainability 15, no. 5: 4050. https://doi.org/10.3390/su15054050