1. Introduction

Corruption in business, accounting for 5% of the costs of conducting business in Asia [

1], is a sensitive but salient issue in the progress of economic marketization, which has been regarded as a major obstacle to fulfilling sustainability goals [

2,

3], including sustainable production, sustainable employment, and environmental sustainability. In the last decade, a large body of firms have been reported to be involved in corruption in China, including some global giants, and this corruption not only causes inequality and inefficiency in the market, but it also implies lurking crises for firms’ reputations and legitimacy. Bribery by firms has been found to have a close relationship with firm performance, although there are competing theories in the literature about the economic effects of bribery (i.e., grease vs. sand in the wheel) [

4]. To understand the driving forces of corrupt activities, scholars have mainly focused on external factors, including policy initiatives [

5], social norms [

6], government intervention [

7], and cultural and institutional drivers [

1,

8,

9]. However, the external viewpoint provides only restricted insights into how the levels of firms’ bribery activities vary in a certain environment. Recently, the internal corporate governance structure has been found to be related to the motivations of corporate corruption. For instance, Ramdani and Van Witteloostuijn [

10] examined the effect of the separation of ownership and control and the equity share of the largest shareholder on firm bribery activity. The executive compensation structure is known to be pivotal in corporate governance, and Feng and Johansson [

11] presented empirical evidence of the association between firm corruption and top executive compensation in Chinese listed state-owned enterprises. However, less research has investigated the influence of the executive pay structure on firm bribery activities, while top managers are the firm’s key decision-makers and the executors of bribery activities [

10].

The high wages and bonuses of chief executive officers (CEOs) have attracted wide attention from society. Although some commentators have questioned the justification of high levels of CEO pay from an ethical perspective [

12], others have provided evidence that the pyramid compensation structure creates tournament-like incentives among executives and is justified by higher productivity [

13]. The issue of pay disparity across top management team (TMT) members has also drawn attention from organization theorists for its significant role in corporate governance, and it has been found to be associated with various strategic outcomes, including innovation [

14], social performance [

15], new market entry [

16], and firm performance [

17]. In this study, we investigated the effects of managerial pay disparity on the tendency to engage in bribery. Tournament theory suggests that, within an organization, the hierarchical compensation structure creates incentives for executives to outperform their peers in an effort to win promotions and rewards [

16,

18]. From another perspective, social comparison theory states that when individuals compare their compensation to their fellows and find that the reward for their efforts is lower than that for their fellows, the ensuing perceived inequality will harm employee relations and morale and will lead to counterproductive activities [

16,

19]. Bribery is regarded as an action intended to acquire extra support and benefits from governmental officials and business partners, and it is thought to create both benefits (i.e., performance improvement) and costs (i.e., reputational damage and legal sanctions) for both the firm and the executives who commit it. In this context, both the tournament-like incentives and the perception of inequality derived from pay disparity will be connected to bribery activity.

Furthermore, tournament theory and social comparison theory are both highly focused on the similarity among contestants. Contestants are prone to compete more within a homogeneous group than in a heterogeneous one [

20], and social comparisons between top executives are strengthened by their similarity in a variety of attributes [

21]. On this basis, we suggest that demographic diversity among top managers will mitigate the unethical consequences of pay disparity. Additionally, we argue that the opportunities to win the tournament by being elected CEO will determine the incentives of pay disparity for TMT members, and we posit that CEO–TMT similarity will predict the potential for insider succession. We further posit that CEO–TMT demographic similarity will strengthen the relationship between pay disparity and bribery activities. Using a sample of Chinese listed firms, we propose that pay disparity will be positively associated with bribery, and this relationship will be mitigated by TMT demographic diversity and strengthened by CEO–TMT similarity. These hypotheses are generally verified by this study’s empirical results. Furthermore, when we decompose pay disparity into its vertical and horizontal components, we find that the effect of pay disparity on bribery is derived mainly from the vertical component.

This study contributes to the literature in multiple ways. First, in the literature on the antecedents of corrupt behavior by firms, most previous studies focused on external institutional and industrial factors, including formal and informal rules [

22], government anti-corruption campaigns [

23], and industrial competition [

24]. Very few studies considered the black box of how internal governance mechanisms affect firm bribery activity, with the exception of Dela Rama [

25], who studied how corporate governance reforms in Philippine institutions impacted corrupt behaviors, and Feng and Johansson [

11], who examined the relationship between executives’ underpayment and corrupt behaviors in China’s state sector. Our current study reveals how executives’ incentives, derived from their pay structure, influence bribery activity. The findings enrich the literature on corruption by extending our knowledge on the antecedents of corruption.

Furthermore, this study adds to the literature on executive compensation. Top executives’ compensation has been highlighted for its role in addressing the agency problem between principals and executives. For instance, equity-based compensation is widely adopted as a solution to agency problems, but it incentivizes CEOs to conceal bad news and choose suboptimal strategies [

26]. Thus, CEOs are penalized for fraud, and the lower the CEO compensation is, the more severe the fraud is that the firm commits [

27]. Recent studies have come to realize the implications of pay disparity among TMT members for numerous strategic outcomes, including divestiture [

28], innovation [

29], new market entry [

16], and firm performance [

30]. In addition to the types of market strategies that firms adopt in competition, this study reveals the impact that pay disparity has on a nonmarket strategy and its ethical implications. We extend the body of research on managerial pay gaps by examining their effects on engagement in unethical activities. Pay disparity within TMTs is not related merely to production efficiencies and strategic choices; it also may have a side effect for firms.

Third, we advance arguments on the composition of top management. This study reveals that demographic diversity among top managers and the characteristics of the CEO–TMT interface can have moderating effects on the unethical consequences of pay disparities. In the literature, demographic diversity within TMTs is argued to be related to cognitive and expertise heterogeneities, and it therefore represents the capabilities for more thoughtful decision-making in innovation and reflects a broader collection of human and social capital [

31,

32]. In this study, which was based on social comparison theory and tournament theory, we explored the role of TMT diversity in corporate governance and uncovered an indirect mechanism through which TMT diversity relates to organizational outcomes. Demographic diversity among a firm’s top managers implies that the firm has heterogeneous human and social capital, and thus it mitigates the feeling of relative deprivation via pay disparity and relieves the tournament-like tension among the managers. Moreover, a growing body of research has underscored the notion that power is not equally distributed among TMT members, and the TMT is not treated as a single unit. Among these studies, the interface between the CEO and other TMT members was underscored [

33]. In this study, we argue that the CEO–TMT demographic interface can indicate the potential for insider succession, which in turn can affect succession tournaments within TMTs and can shed light on how pay disparity among TMT members influences unethical organizational behaviors.

2. Theoretical Foundation and Hypotheses

Corruption is regarded as an illegal act involving a specific exchange between public or private parties. The literature is divided on the consequences of corruption for firms, however. On one hand, bribery of government officials is pervasive in business practices seeking to achieve benefits for the firm through avoiding or reducing taxes, obtaining public procurement contracts, and circumventing regulations. More specifically, corruption can lower firms’ operating and transaction costs by reducing their payments for government taxes, license fees, and tariffs [

34], facilitating their entry into highly regulated economies [

35], motivating their short-term-oriented decisions [

36], achieving firm growth [

37], and promoting innovation [

38]—all of which are regarded as a “grease the wheel” scenario.

On the other hand, bribery practices also carry hidden costs for both executives and firms. First, bribery exposes firms to the risk of potentially substantial legal and legitimacy losses [

39], which then elicit financial and reputational damage if the bribery activities are recognized and reported publicly. Executives who are prosecuted for bribery may face fines and jail sentences, and this possibility introduces additional risks for their firms’ operations. Second, bribery divests investment in core competencies [

40], and when firms obtain advantages through paying bribes, the perceived importance of innovation and product development and of executives’ efforts toward them are reduced [

41], causing improvement in management to lose its priority status and investment in better growth opportunities to be limited [

36]. Third, firms that engage in bribery face a forced escalation of commitment to bribery activities, because once they participate in corruption, corrupt officials will expect them to provide the same payment or a higher one. Corrupt officials apply more red tape to such firms and raise the level of bureaucratic interference in order to gain more bribes [

42]. As a result, the bribing firms become worse off, but when they choose to stop or reduce their bribes below the amount that they paid previously, they are likely to face new problems with the corrupt officials. This viewpoint is described as the “sand in the wheel” scenario.

Business corruption is argued to result from flaws and deficiencies in institutions and supervisory systems. When government officials are empowered with great discretion in allocating critical resources, but they have no effective supervision and no substantial sanctions have been established to address their misbehaviors, they tend to seek rents of power to maximize their own interests. The weaknesses in financial and legal institutions, combined with the social networks in which top executives are situated, are the sources of corporate corruption [

43]. Moreover, scholars have argued that the divergence between the “grease” and “sand” viewpoints of corruption lies in the institutional field. Generally, in transitional economies, in which institutions tend to malfunction and serious bureaucratic red tape exists, corruption plays the role of “greasing the wheel” [

36,

38,

44]. In the early stages of marketization, the government adopts various market institutions, such as competitive public procurement, and market reform generates policy instability and institutional dynamics, all of which cannot alleviate corruption and in fact actually create new opportunities for it [

22], with the intensive market competition driving firms to engage in corruption in order to reduce their costs [

45].

In addition to the external viewpoint presented in the literature on corporate governance, a series of studies have revealed the effects that both the total amount and the structure of executives’ compensation exert on those individuals’ immoral and illegal acts, including their concealment of bad news [

26] and their engagement in environmental violations [

46]. The studies highlight the importance of equity-based long-term compensation. When executives adopt corruption to overcome regulatory barriers in an institutional environment and, in so doing, to achieve better firm performance, the incentives stemming from their compensation structure are closely related to their corrupt behaviors. For example, Feng and Johansson [

11] provided empirical evidence of a positive relationship between executive underpayment and corruption in state-owned companies in China. In fact, in addition to the levels and types of executive pay, the distribution of pay within the TMT has been identified by several studies to be correlated with a series of organizational behaviors and strategic outcomes, including workforce performance [

47], social performance [

15], new market entry [

16], R&D and innovation [

14], and firm performance [

17,

48]. Prior studies on pay disparity were mainly based on tournament theory and social comparison theory. Modern organizations adopt a pyramid structure within which CEOs are paid the highest wages, followed by TMT members and then by middle managers. Tournament theory argues that the hierarchical compensation structure creates incentives for executives to outperform their colleagues. Therefore, the hierarchical pay structure is considered effective in incentivizing individuals to make greater efforts, and a high degree of pay disparity is related to higher levels of firm performance [

21]. On the other hand, when individuals compare their compensation to that of their fellows, if they find that the ratio of their output to input is lower than that of their fellows, their organizational commitment will drop and they will tend to reduce their efforts (inputs), which ultimately will lead to a diseconomy of pay disparity and will impose social comparison costs on the firm. Social comparison costs include less cooperative behaviors within work teams [

49], increased employee turnover [

50], and reduced workforce performance [

30,

51].

2.1. Pay Disparity and Bribery

Pay disparity derives mainly from the pay-for-performance scheme and hierarchical compensation structure. A hierarchical compensation structure incentivizes individual executives to compete for promotions and rewards [

15,

16]. The CEO is paid the highest, followed by other TMT members. This pyramid structure stimulates executives’ efforts to gain a promotion by outperforming their executive peers. Prior empirical studies have provided evidence that financial incentives motivate individuals to undertake risk-taking activities, such as acquisitions [

52], and these studies have identified a positive link between executive pay dispersion and firm performance [

53]. To outperform their peers, executives tend to commit undesirable and immoral behaviors, including cooperating less with other employees [

54], undertaking less social responsibility [

15], and raising the cost of equity [

55]. Weaknesses and flaws in regulations and supervisory systems create opportunities for corporate managers to bypass bureaucratic regulations by bribing officials. When pay disparity imposes immense pressure on executives to enhance their performance, they are tempted to take higher risks to boost their performance by adopting corrupt activities, and this strategy takes advantage of the weakness in the regulatory and supervisory systems. In particular, performers struggling with low ability or challenging tasks may choose risky and illicit activities to achieve a successful outcome [

53]. In a deficient and flawed institutional environment, managers resort to bribing government officials to achieve better performance that will earn them rewards and promotions, even though they and the firm may face the costs of potential legal and reputational risks in the long run [

10].

According to social comparison theory, non-CEO executives may also perceive an inequality resulting from being compared with their peers of similar status. When individuals find that their efforts lead to less reward, and they take reactive measures to rebalance this situation, the result may be the addition of “social comparison costs” to firms [

19,

28]. A large pay inequality creates employees’ feelings of deprivation and resentment, impairs their relationships and cooperation, discourages them from making continuous efforts and remaining committed to organizational goals [

56], increases worker turnover [

57], fosters deception [

49], promotes a tendency of divestiture [

28], and reduces employee efforts and lowers firm performance [

53]. Pay inequality hurts executives’ morale and reduces their efforts [

58], thus eliciting their misconduct through taking shortcuts in carrying out their duties. Furthermore, studies on criminology have revealed that interpersonal discrimination increases the risk of crime [

59]. In addition, the relationship between social discrimination and delinquency is mediated by negative emotions, such as feelings of anger and depression [

60]. Certain specific goals in business, such as winning government licenses, contracts, subsidies, and tax cuts, can be achieved via a shortcut by paying bribes. Whenever executives sense inequality and deprivation in comparing themselves with their peers, they tend to make less effort and to become more likely to commit unethical activities.

Hence, bribery is likely to be committed more often in firms with larger pay disparities within the top management team.

H1. Pay disparity within the TMT will have a positive relationship with engagement in bribery.

2.2. Top Executives’ Demographic Diversity

The pay disparity between CEOs and non-CEO executives induces succession tournaments among non-CEO managers, and these tournaments can lead to risk-taking activities and unfavorable outcomes [

61]. According to tournament theory, differences among actors are a significant factor influencing their tournament behavior and relative rank [

62]. Contestants are most prone to compete when they are within a relatively homogeneous group [

20], and those who do not differ in their abilities suffer the most intense rivalries. If the members are aware that a successful promotion will be related to certain capabilities and characteristics and they believe that they have less opportunity to win, they will reduce their overall efforts [

63]. Demographic characteristics are significant indicators of executives’ backgrounds, experience, and capabilities, and demographic diversity implies cognitive and expertise heterogeneity and represents the potential for more thoughtful decision-making [

64], whereas a more intense tournament is formed among managers with similar demographic characteristics. Hence, in the top management teams that feature a high level of demographic diversity, pay disparity is less likely to give rise to tournament competition among the top executives.

On the other hand, according to equity theory, social comparisons occur more frequently among peers with similar characteristics and status. A core proposition in social comparison theory states that individuals tend to compare themselves to those with whom they share common characteristics [

65]. Furthermore, it is argued that individuals desire to obtain what similar others possess, and comparisons with similar others lead to feelings of relative deprivation. Social comparisons between top executives are strengthened by similarity in a variety of attributes, such as age, gender, and ethnicity [

21]. In contrast, when higher pay is attributed to executives’ specific attributes that are related to outstanding performance, the result is a lowered perception of deprivation and inequality. Therefore, a high pay disparity between executives and others with similar demographic attributes will raise intense feelings of relative deprivation and thus will lead to more unethical behaviors.

H2. Demographic diversity within a TMT will mitigate the relationship between pay disparity and firm bribery.

2.3. The CEO–TMT Demographic Interface

In terms of tournament theory and social comparison theory, CEO–TMT demographic similarity has a significant effect on the relationship between pay disparity and firm bribery. The opportunity to win the tournament by being elected CEO determines the degree of tournament-like incentives from pay disparity for TMT members. For example, larger pay disparities are required to incentivize participants when they are faced with a greater number of competitors, because the larger number of contestants reduces each participant’s chances of winning the tournament [

66]. In addition, the TMT members’ perception of the opportunities to win the tournament is affected by the current CEO’s characteristics. Scholars suggest that firms tend to repeat their criteria in electing CEOs, and thus the more similar a non-CEO executive’s demographic characteristics are to those of the current CEO, the more the non-CEO perceives that he/she could be promoted. In other words, when the current CEO is similar to the TMT members, the likelihood increases that the next CEO will be elected from insiders, and thus a lower pay disparity is needed to form a tournament among TMT members [

21]. Demographic characteristics represent a variety of elements of human and social capital that relate to executives’ performance and promotion [

67]. Therefore, we argue that the more similar a CEO’s demographic characteristics are to those of the other TMT members, the stronger the incentive will be for a certain level of pay disparity to prompt TMT members to engage in bribery.

Social comparisons are made more frequently among people with similar characteristics. Individuals tend to want what similar others have, and, consequently, feelings of deprivation may result from comparisons with similar others. Furthermore, a CEO who is noticeably different from the members of the TMT is less likely to be seen by them as a social comparison target and therefore is less likely to prompt the TMT members to perceive relative deprivation [

21]. Studies have shown that the potential for insider succession is predicted by the current CEO’s characteristics, because the criteria in electing CEOs tend to be repeated. High succession potential will induce TMT members to compare their pay to that of the CEO, and thus they will experience more relative deprivation from a high pay disparity, which in turn will lead to less commitment to organizational goals and more unethical behaviors. Therefore, we anticipate that the relationship between pay disparity and firm bribery will be strengthened by CEO–TMT demographic similarity.

H3. Demographic similarity in the CEO–TMT interface will strengthen the relationship between pay disparity within the TMT and the firm’s bribery.

3. Sample Selection and Measurement

The study’s sample consisted of Chinese firms listed on the Shanghai and Shenzhen A-share stock markets from 2009 to 2016. Data on firm-specific information were obtained from the China Stock Market and Accounting Research (CSMAR) database and firms’ annual reports. Consistent with prior studies, (1) the special treatment (ST) and particular transfer (PT) listed companies were eliminated because they operate in abnormal conditions; (2) the firms that had been listed in the stock market for less than three years were excluded to avoid the “window-dressing” effect that can occur in the early stages of going public; (3) the firm-year observations with missing values were dropped to ensure validity; and (4) the top and bottom 1% of the distribution of each financial variable were winsorized to control for the potential effect of extreme data. Finally, we obtained 6366 firm-year observations.

3.1. Pay Disparity

In accordance with prior studies on top executive pay in China [

27,

68], we measured top executive pay by the sum of salaries, stipends, and bonuses. Stock options are rare in our sampled firms, of which approximately 6% reported stock options, and our results are robust when removing these observations. First, we constructed a measure of

Overall Pay Disparity, which was operationalized as the coefficient of variation in the pay of CEOs and the other four highest-paid TMT members divided by the averaged pay, following Siegel and Hambrick [

30]. Second, because pay disparity is argued to be decomposed into vertical and horizontal pay disparity components, we measured them separately.

Vertical Pay Disparity was measured by subtracting the average TMT member’s total pay from the CEO’s total pay and taking the natural logarithm to alleviate skewness [

66].

Horizontal Pay Disparity has been defined as the standard deviation of the total pay of TMT members except the CEO divided by the average of their total pay [

15]. In line with the TMT literature, in this study, TMT members were characterized as the four highest-paid top managers excluding the CEO.

3.2. Bribery Expenditure

Most of the extant literature on corruption has relied on subjective perception indices, but due to the illicit and sensitive nature of corruption, subjective survey data may suffer from a significant bias. In this study, bribery expenditures were measured as abnormal entertainment and travel expenses, on the basis of the accounting data disclosed in firms’ annual reports, as was proposed by Cai et al. [

69]. The entertainment and travel expenses were disclosed in the annual reports of Chinese firms as a standard expenditure item. In Chinese firms, this accounting item includes expenditures on normal business activities, such as funding business trips and entertaining clients, partners, and suppliers, and bribery to government officials and other parties [

69,

70].

To rule out normal entertainment expenditures, we regressed entertainment and travel expenses on a set of variables including total assets, total sales, marketing expenses divided by total sales, capital intensity, and the average compensation of the four highest-paid executives based on Cai, Fang, and Xu [

69], which are important determinants of normal entertainment expenses and managerial excesses. The residual of this model was adopted as a proxy for abnormal entertainment expenses that are ascribed to bribery activities. This approach has been verified in a set of prior studies [

55,

70], which proposes a measure of bribery expenditure based on objective data instead of on managers’ subjective evaluations and reports. For example, based on this method, Xu, Zhou, and Du [

70] find that low-performing firms have an increased probability to engage in bribery.

3.3. CEO–TMT Demographic Diversity

A top management team’s demographic diversity was measured in terms of three primary characteristics of the four highest-paid non-CEO top managers, namely their gender, age, and educational background, in accordance with prior studies [

33]. Gender was captured by a binary variable; the educational level was assigned a value from 5 to 1, according to the educational degree that a manager held (PhD, Master’s, or Bachelor’s degree, diploma from junior college, or technical secondary school and below).

Following prior studies [

71], for interval data (age and educational background), we employed the coefficient of variation (the standard deviation divided by the mean) to obtain a scale-invariant measure of diversity. For the categorical variables (gender), Blau’s index of heterogeneity (

) was used, where

is the proportion of group members in a gender category and

i is the number of different categories represented in the team (

i = 2 in this study). To calculate the overall TMT demographic diversity measure, we normalized these variables and then aggregated them together into a composite variable.

3.4. CEO–TMT Demographic Interface

The CEO–TMT demographic interface variable refers to a CEO’s similarity to the rest of the TMT in terms of his/her demographic characteristics [

33]: age, gender, and educational background. Age and educational level were continuous variables, and the similarity between the CEO and the TMT was calculated using the distance formula:

where

Xi represents the age or educational level of CEO

i,

Xj represents the age or educational level of each non-CEO executive

j, and

n is the number of TMT members. To convert this into a similarity measure, this variable was reversed.

Next, CEO–TMT gender similarity was measured by the proportion of TMT members who had the same gender as the CEO. To obtain the overall CEO–TMT similarity measure, we aggregated the three components into a composite variable after standardization.

3.5. Controls

To exclude the potential influence of other factors and mitigate endogeneity problems, this study controlled for a set of variables from various levels, including the board of directors, the firm, the industry, and the region where the firm was located.

Marketization index. Corporate corruption is closely tied to the flaws and deficiencies in governmental regulations. The level of regional marketization reflects the firm’s development in the business institutional environment, and has been broadly adopted in prior studies. This variable was compiled by the National Economic Research Institute (NERI), which features the progress of the transition toward a market-based economy in 31 provinces and special administrative regions in such aspects as government intervention, market competition, the development of product and factor markets, and the strength of the legal environment. There were a total of 23 indicators in these categories. The scale of each indicator ranged from 0 to 10.

Competition. Industry competition was gauged using the Herfindahl–Hirschman Index (HHI), which indicates the extent of industry concentration and is widely adopted as a proxy for competition. It is tightly connected with executives’ compensation [

72]. The HHI for an industry equals the sum of each firm’s squared market shares, of which the maximum value is 1.

Firm age and

firm size. Firm age is associated with the firm’s level of legitimacy and the experience of dealing with government authorities, and firm size determines its bargaining power with the government and is related to executives’ compensation [

73]. Firm age was measured as the number of years for which a company had been listed in the Chinese stock market. Firm size was calculated as the natural log of the total amount of assets.

Firm performance. Firm performance is a critical determinant of executives’ pay [

74] and is associated with firms’ bribery activities [

8]. Firm performance was captured by ROA and Tobin’s Q on an annual basis to control for financial and market performance, respectively. In accordance with prior studies, these variables were adjusted by the average in the industry.

Leverage. Financial leverage shows how much of a firm’s capital is in the form of liability, which is associated with executives’ compensation [

75] and the firm’s performance. It was coded as the ratio of the amount of total debt divided by the amount of the total assets.

Growth. The variable for a firm’s growth measured the growth rate of sales revenue and was associated with executives’ compensation. The growth rate was calculated as the difference between a firm’s sales in the current and previous years divided by the sales of the current year.

Cash flow. The operating cash flow ratio was calculated as the operating cash flows divided by total assets and is related to executives’ compensation and bribery.

Ownership. In China, firms’ government background has a significant influence on their executives’ compensation and strategic outcomes, due to the pursuit of social welfare. Whether a firm was owned and controlled by the government was captured by a dummy variable.

Management expense. The amount of management expense captures firms’ agency costs, which affect firms’ engagement in bribery [

10].

Additionally, the board of directors is responsible for top executives’ compensation plans and firms’ tactics to deal with government officials. To control for the characteristics of the board of directors, the board size, independence, and CEO–chairman duality were included. Board size was gauged as the number of board members. Independence was operationalized as the proportion of independent members on the board. CEO–chairman duality was a dummy variable, which was set to a value of 1 for CEOs who chaired the board of directors and 0 otherwise. Furthermore, because firms’ dependence on the government and the pressure of performance imposed on top executives vary between industries, in terms of the Industry Classification Guidance of Listed Companies issued in China, industrial binary variables were controlled for in the regressions. Moreover, to exclude year-specific heterogeneity, dummy variables were included to control for each year. These variables and definitions are summarized in

Table 1.

4. Model and Results

In

Table 1 and

Table 2, descriptive statistics and correlation coefficients are reported. The maximum VIF value of all of the variables was 2.12, which ensured that the results were free from multicollinearity bias. The generalized least squares (GLS) regression method adapted for panel data was deployed to address the potential autocorrelation problem, and a yearly lag between the dependent and independent variables was employed to better capture the causal effect, for which the model was set as Equation (1). The results are shown in

Table 3. Model 1 included only the control variables, and it showed that marketization imposed a significant and negative effect on firm bribery.

Notes: Pay Disparity denotes overall pay disparity, vertical pay disparity, and horizontal pay disparity, respectively; control variables were CEO duality, board size, board independence, firm age, firm size, leverage, growth, ROA, Tobin’s Q, cash flow, HHI, ownership, management expenses, and year and industry dummies.

Hypothesis 1 predicted a positive relationship between pay disparity and bribery, and Model 2 showed a positive and significant coefficient of Overall Pay Disparity (β > 0 and p < 0.05) and thus provided support for this relationship. Hypothesis 2 proposed that demographic diversity among members of the TMT would have a negative moderating effect on the relationship between pay disparity and bribery. In Model 3, the interaction term of Pay Disparity × TMT Diversity carried a negative and significant coefficient (β < 0 and p < 0.01), thus supporting Hypothesis 2. Finally, in Hypothesis 3, we proposed that CEO–TMT demographic similarity would have a positive moderating effect on the relationship between pay disparity and firm bribery. In Model 4, the interaction of Pay Disparity × CEO–TMT Similarity was both positive and significant, lending support to Hypothesis 3. The interaction terms were added together in Model 5, which showed that the results remained stable.

Moreover, in

Table 4, pay disparity is represented by two components: vertical pay disparity and horizontal pay disparity. In Model 1,

Vertical Pay Disparity had a positive and significant coefficient (β > 0 and

p < 0.01), which was consistent with Hypothesis 1, but

Horizontal Pay Disparity had a nonsignificant coefficient. In Model 2, the coefficient of the interaction term

Vertical Pay Disparity ×

TMT Diversity was statistically significant and negative, lending support to Hypothesis 2. In Model 3, the coefficient of the interaction term between

Horizontal Pay Disparity and

TMT Diversity was not significant. When both interaction terms were added together in Model 4, the results held. In addition, the coefficient of the interaction term

Vertical Pay Disparity ×

CEO–TMT Similarity was statistically significant and positive, which was consistent with Hypothesis 3, although the coefficient of the interaction term between

Horizontal Pay Disparity and

CEO–TMT Similarity was not significant. In summary, vertical pay disparity offered further evidence to support Hypotheses 1, 2, and 3, but horizontal pay disparity did not.

Executive compensation may be endogenously determined by firms’ strategic outcomes and unobservable factors, which leads to an endogeneity issue. We simultaneously ran Equation (1)—the determinants of bribery—with Equation (2), which specified certain determinants of pay dispersion. These determinants were

firm size, growth opportunities,

uncertainty,

competition, CEO pay, capital intensity, and

averaged pay disparity at the industrial level. Firm size is a fundamental determinant of top executive compensation. Firms with high growth potential are inclined to employ powerful incentives to attract high-quality top managers. When a firm is faced with high uncertainty, high pay dispersion is needed to motivate top managers to cope with the adverse effects of uncertainty, which is calculated as the standard deviation of the ROA for the past five years. When firms are involved in fierce competition, top executives need to be better incentivized by compensation schemes. Pay for the CEO is a benchmark that determines the degree of pay disparity of other executives. A higher level of capital intensity may lead to higher risks in financial returns and higher production efficiencies, which are related to top executive compensation. Capital intensity is measured by the ratio of total assets to sales. Furthermore, the level of disparity within a firm can be influenced by that of its peer firms in the same industry. Hence, we controlled for the industry-averaged pay disparities.

Note: In Equation (2), Pay Disparity refers to overall, vertical, and horizontal pay disparity; industrial pay disparity is either the industry-averaged overall, vertical, or horizontal pay disparity, according to the dependent variable. The instruments for the interaction terms were created based on Equation (2).

Table 5 and

Table 6 provide the estimates of simultaneous equations using two-stage least-squares (2SLS), which remain qualitatively similar to what we report above. Both the overall pay disparity and the vertical pay disparity had significantly positive coefficients, in which the moderating effects of

TMT Diversity and

CEO–TMT Similarity were shown to be statistically significant. Furthermore, the estimators of

Horizontal Pay Disparity and its interaction term with

TMT Diversity and

CEO–TMT Similarity provided no remarkable support to our hypotheses. Finally, a Hausman test showed no significant difference between the instrumented and non-instrumented estimations.

In addition to the results reported above, we conducted several robustness checks to further test the hypotheses.

First, we used an alternative measure of vertical pay disparity, the ratio of the CEO’s compensation to the non-CEO executives’ average compensation, and we gauged the horizontal pay disparity by the Gini coefficient of the non-CEO executives’ compensation. As is shown in

Table 7, our results were robust across the alternative measures.

Second, when President Xi Jinping and the new generation of leadership came to power in 2012, a fierce anti-corruption campaign was started [

76,

77]. In 2012, the Eight Austerity Rules were approved, forbidding conspicuous perks and confining administrative power within an institutional domain, which greatly strengthened law enforcement, curbed officials’ abuse of power, and limited the government’s excessive intervention in the economy. We further tested whether our results changed before and after the anti-corruption campaign started in 2012. The results are reported in

Table 8 based on the divided samples according to the year of 2012, from which it is shown that the results remain consistent with what was reported above, except that the association between vertical pay disparity and bribery was slightly weakened after 2012.

Third, some prior studies suggested that the system general method of moment (GMM) estimators is effective in controlling for heteroscedasticity and addressing endogeneity concerns [

16]. Our results from applying the GMM were similar to those that we report above.

5. Discussion

Prior studies on corporate bribery behavior have focused mainly on the business environment. This study revealed the antecedents of bribery, which developed from incentives deriving from the compensation structure among top executives, and also as a social comparison cost when pay disparity among TMT members gave rise to corruptive misconduct, thus eliciting potential costs in the long run. Although, compared with principals, managers tend to avoid engagement in illegal misbehaviors in order to protect their favorable career reputations [

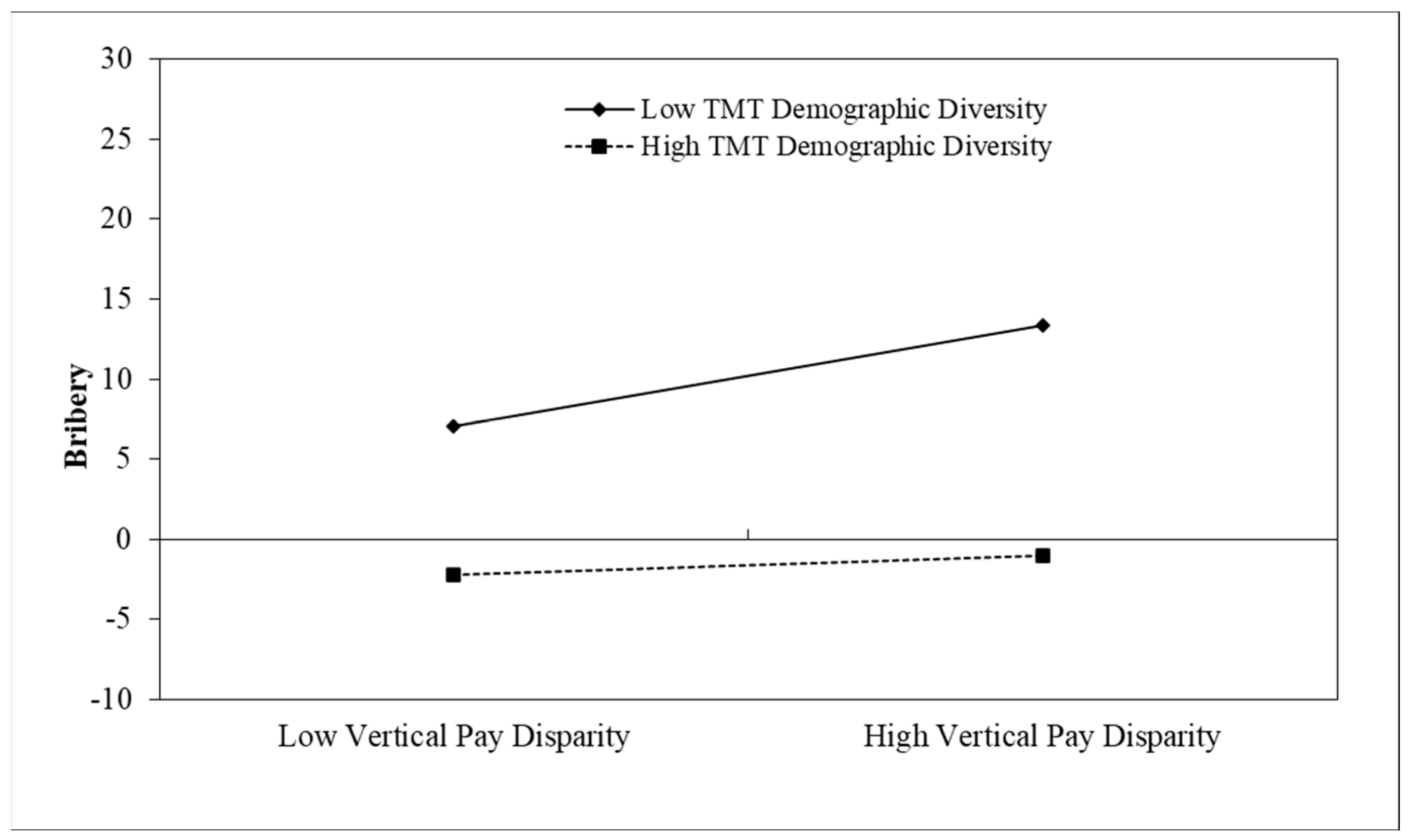

10], corporate governance devices can exert a significant influence on managers’ bribery activities. The relationship between TMT pay disparity and firm bribery was corroborated by estimations using measures of overall and vertical pay disparities within TMTs, whereas the effect of a horizontal pay disparity was not significant. Therefore, it shows that this effect was mainly derived from the vertical pay disparity. Moreover, using the tournament theory and the social comparison theory, we argued and subsequently found empirically that demographic diversity in TMTs could mitigate this effect of vertical pay disparity in promoting bribery and that CEO–TMT demographic similarities exacerbated it. These findings are delineated in

Figure 1 and

Figure 2.

This study also contributes to the research on top executive compensation. In the literature, compensation incentive schemes have been argued to play a critical role in corporate governance. The level and structure of top executives’ compensation have been found to be related to a set of organizational outcomes. Although, relative to firm owners, managers tend to avoid engaging in unethical activities out of concern for their reputations [

10], a set of compensation schemes, including equity-based compensation and pay for performance, are effective at bridging the separation between firm ownership and control and are likely to incentivize executives to misbehave. For instance, top management incentive compensation increases the likelihood that they will misrepresent finances [

78], and stock-based compensation motivates managers to make costly efforts but also induces them to conceal negative news and to choose suboptimal policies [

26]. Moreover, if the top manager owns the firm, the likelihood that the firm will engage in bribery increases [

10]. Incentive compensation is designed to induce top executives to be more involved in pursuing organizational goals, but as a side effect, it also can elicit short-term unethical misconduct among managers who are under immense pressure to perform. Moreover, the distribution of pay within the TMT is closely linked with firm performance [

15,

17,

47,

53] and a series of strategic outcomes [

14,

16]. Within the pyramid structure of an organization, individuals tend to compare their pay with that of peer referents, and they are rewarded with increased pay, favorable prestige, promotions, and higher status if they win the competition with their peers, thus giving them financial incentives to outperform these peers. Under the tremendous pressure derived from a vertical pay disparity, managers tend to engage in bribery, which provides a shortcut to acquiring resources and privileges, circumventing regulatory barriers, and thus promoting performance. Although a hierarchical compensation structure may increase executives’ efforts to improve firm performance, our study suggests that such a structure could also incentivize top executives to engage in unethical behaviors.

Furthermore, this study enriches the literature on TMT composition. In the literature, demographic diversity has been argued to reflect cognitive and expertise heterogeneity and thus to represent potential for more thoughtful decision-making in innovation. Thus, such diversity indicates a sum of human and social capital for international expansion [

31] and for strategic change [

32], thereby leading to better firm performance. In this study, we found that diversity among top managers had another implication for organizational behavior—it played a role in tournaments and social comparisons. Based on tournament and social comparison theories, a promotion tournament is more intense among executives with similar characteristics, and executives tend to compare themselves with similar others, leading to strong feelings of relative deprivation. Demographic diversity among top managers in a firm implies heterogeneous human and social capital, mitigates feelings of relative deprivation due to pay disparity, and relieves the tension of tournament competition within the management team. In addition, in a stream of prior studies, the TMT was traditionally treated as a single unit, but a growing body of recent research has underscored that power is not equally distributed among TMT members. To resolve the drawback of unequal power, scholars have turned to the interface between the CEO and other TMT members, and it not only explains how the knowledge-related factions can be integrated to create beneficial outcomes [

33], but it also helps us to understand how pay disparities among TMT members are likely to influence organizations’ unethical behaviors. Similarity between a firm’s CEO and non-CEO TMT members implies the potential for insider succession and intensifies tournament thinking within the TMT, and this in turn was found to exacerbate the effect that pay disparity had on engaging in bribery.

This study holds certain implications for practice. Our findings can inform boards of directors in designing top management incentive schemes. Our results suggest a negative side effect of relative compensation among top managers, whereas several other studies have argued that a large pay disparity can motivate top managers to outperform others and consequently should increase productivity. This study’s findings imply that if an incentive compensation scheme is adopted to create incentives for executives, it can increase the risk of firms committing illicit and unethical behaviors in the short term because the scheme imposes immense pressure on executives and leads them to take shortcuts to enhance their performance. These illegal shortcuts can in turn elicit potential risks and costs in the long run and thus are harmful to shareholder interests. Furthermore, this study suggests counteractive measures to this problem, by highlighting that top managers’ demographic diversity and CEO–TMT dissimilarity are important for curbing the effects of pay disparity on corruption. When the TMT is composed of members with diverse demographic characteristics and the elected CEO is significantly different from non-CEO executives, the management team can tolerate higher levels of pay disparity and fewer negative consequences will result. These findings together inspire an effective scheme that would reward and promote executives on the basis of identifiable attributes, and such an approach could mitigate the promotion tournament and feelings of deprivation among top executives and thus weaken the negative aspects of a large pay gap within the TMT.

6. Conclusions

This study focused on the effects that pay disparity across top management teams exert on firm bribery. Investigating a sample of Chinese listed companies, we found that pay disparity played an important role in firm bribery. In an institutional field that is in an early stage of development, bribery is known to be effective in helping firms to achieve better outcomes in the short run, but it can also incur reputational, legal, and economic costs for the firms that engage in it. We proposed that pay disparity would impose pressures on executives to achieve better performance and also would create a perception of inequality, which then would increase the executives’ incentives to commit bribery.

This study had limitations. First, in line with prior studies on Chinese firms’ executive compensation [

11,

27,

68], we defined top executives’ compensation as aggregated cash pay, including basic salary, bonuses, and other benefits. In present-day China, fewer firms have executive stock option schemes compared to their counterparts in developed economies. However, the adoption of option-based compensation has already entered an early stage [

79], and the exclusion of long-term equity-based compensation would have led to a bias in our results. This should be considered in future works when data for option-based benefits are available. Second, with regard to measuring firms’ engagement in bribery, the sensitive nature of corruption made related information difficult to extract from managers’ subjective and voluntary disclosures. An increasing number of studies seek the use of an objective indicator from accounting information. We employed a procedure to extract the abnormal entertainment expenses as a proxy for bribery, which has been adopted in some prior studies, but the procedure has difficulty in precisely determining the normal expenses related to regular operations and relationship-building efforts. Future research should endeavor to improve the accuracy of the method in measuring bribery. Another limitation was that the findings were derived from sampled firms in a transitional economy, wherein bribery can be argued to have a positive effect on firms’ outcomes. As a result, caution should be exercised in applying our results to other contexts, although an examination of the present findings in other economies will be necessary and inspiring for future studies. Moreover, our findings may be subject to the uniqueness of China’s institutional environments. Reciprocal gift-giving and the

guanxi culture are deeply ingrained in the Chinese people, and, thus, bribery may be more acceptable, beneficial, and pervasive in China than in other contexts.

{kind=link}

{kind=link}