Most corporate funding has been concentrated in a small number of scalable modern cooking businesses [

22]. It is estimated that in 2020, there existed 450–500 fully dedicated manufacturers and distributors in the cookstove operations chain globally, with around ten percent of enterprises collectively responsible for over forty percent of stove sales. Very few businesses have reached sales volumes that enable economies of scale [

6]. Sector financiers themselves consider only 10–20 companies investible and scalable [

22]. CCA confirmed this in 2020 when it found that six companies accounted for eighty-two percent of revenue, while seven companies raised more than ninety percent of total investment. Four of the seven were also among the eight companies that received ninety percent of investment capital in 2019 [

32].

The focus of most investment in a small number of late-growth-stage companies relative to the number of companies operating in the sector highlights two issues. First, the multiple barriers to investment as expressed by financiers and companies alike. Second, a very small proportion of enterprises (according to the above figures, five percent or less of active clean cooking businesses) survive past the proof of concept stage of the innovation cycle. The latter, combined with the declining volume of public funding, especially in the form of grants, suggests poor effectiveness of public finance in two major respects. In the first instance, limited sustained innovation funding at the beginning of the business growth cycle, where risks are highest and the private sector most reluctant to invest. In the second instance, limited use of public financiers’ expansive mandates to mitigate risk for private capital.

4.1. A Broad Spectrum of Investment Barriers

From the perspective of potential investors in enterprises that provide clean cooking solutions, financiers cite a lack of proven, viable business models; lack of investible pipeline; potential investees’ lack of profitability (compounded by very limited publicly available data) and lack of operational history; and poor consumer affordability as the greatest barriers to scale [

22]. Financiers’ overall risk aversion may be underscored by business models in the sector evolving too rapidly to enable investors to suitably assess risk [

6]. In the adjacent LMD sector, financiers cite LMDs’ lack of a strong funding pitch, lack of financial literacy and poor data collection as key pain points in a company’s early growth stages [

9,

28].

For their part, clean cooking companies rank consumers’ lack of ability and willingness to pay for solutions, poor access to finance and lack of financial support as the greatest obstacles to scale. Specific fundraising challenges include a perception that funders have a low-risk appetite; the shortage of early-stage grant capital; the high cost of debt and short loan tenors; lack of working capital; the length of funder due diligence processes; lack of energy know-how among local financiers; and a shortage of equity. In summary, no single issue dominates clean cooking companies’ fundraising challenges. It is a broad spectrum that spans the entire innovation chain [

22].

Together, these barriers are borne out in the difficulty clean cooking companies have in securing finance at all stages of their development in the context of an overall huge shortfall. However, even if sufficient volumes of finance were available, questions remain as to whether it is allocated at the early stages of the clean cooking innovation cycle in such a manner that anticipates risks later in the cycle, seeks to help mitigate them and ensures a healthy pipeline of viable businesses for later stage investment. Further, it is important to consider whether the institutions that supply finance are organised in such a way to be able to effectively deploy it and enable businesses that require finance to efficiently access it. To answer these questions, it is useful to examine in more detail the nature and flows of finance through the clean cooking enterprise value chain, with a focus on the early, innovative stages of a business’s lifecycle.

4.2. Surviving Proof of Concept

A sustainable clean cooking sector depends on a critical mass of businesses moving through the early stages of the innovation cycle to commercial operation and, ultimately, maturity. However, it can take many years to bring an innovative idea to market, with energy technologies typically operating within highly regulated environments. Importantly, conventional drivers of technology push through the innovation cycle from RD&D, as well as market pull from end-use consumer demand, can be reinforced or inhibited by feedback between different stages of the cycle and by the influence of framework conditions, such as government policy and the availability of risk capital [

36]. Further, just as critical as a technology or business model’s progression through the innovation cycle, concerned as it is with problem-solving of a technical or marketing nature, are the bridges between the various stages of the cycle. These are associated with mobilising interest, resources (including financial resources) and market constituents and are geared towards satisfying the various stakeholders of the technology or business model at each stage, without whom its value is not recognised [

37].

Commercialisation of new technology, defined as the process of moving a technology from laboratory to market acceptance and use, thereby becoming part of mainstream economic activity, is expensive and time-consuming [

11]. By way of example, it is possible to summarise the progress of a solar photovoltaic (PV) technology through the innovation cycle into four phases. Phase 1, comprising fundamental research and new concept development, requires continuous, long-term (minimum 10 years) funding, which is largely provided by a host research institution backed by government funding. Typically, strategic industry investors have little interest in funding innovation at this stage, as intellectual property arising from it has little or no value. The demonstration and evaluation of new concepts during phase 2 continue to require medium-to-long-term funding and, as the work becomes more applied in nature, is more reliant on capital-intensive facilities. Intellectual property arising out of this phase is still of minimal value, resulting in difficulty in attracting private investors. Therefore, public grant funding is essential to help advance technologies through this phase. The development of commercially relevant technology during phase 3 is highly innovative and generates the most intellectual property, which is typically jointly owned by the developers. Strategic industry involvement is essential to ensure that research outcomes are commercially relevant and preferably lead to pilot production. Government funding that fosters collaboration between research institutions and industry is valued in this phase. Lastly, phase 4 of a PV technology’s development, as it moves to large-scale manufacturing, involves minimal innovation and intellectual property creation. However, the high capital intensity of this phase can raise significant financing challenges [

38].

Similarly, business model innovation is a process that occurs over time. It entails a set of deliberate actions that are undertaken by managers and entrepreneurs to change the components and architecture of a business model in an innovative way with the aim of gaining a strategic advantage [

39].

Against this background, it is instructive to highlight the role of public finance in pushing new technologies and business models through the critical, early stages of the clean cooking innovation cycle and, by extension, creating viable opportunities for later-stage private investment.

Early-stage funding is important to support technology development, proof of concept and pilot demonstration. While some founder equity may be available at this stage, accelerating energy innovation hinges critically on public investment and institutions for RD&D [

40]. This reflects long timeframes to commercialisation, a commensurate lack of value in intellectual property and, therefore, a relative lack of interest from private sector strategic and financial investors. As concepts are proven, early-stage private investors (for example, strategic industry investors, angel investors and early-stage venture capital) demonstrate an increased willingness to invest in new ventures, especially as intellectual property begins to emerge as an asset. At this stage, greater scope for public and private sector co-funding emerges. Once a technology or business model is more developed and risks are retired, the capital intensity required to scale increases. Consequently, while early-stage technology and business model innovation can be supported by relatively modest amounts of capital from the public sector and equity investors, the substantial amounts of capital required to scale mean that all but the most highly capitalised companies must seek significant amounts of finance, often from multiple sources. In blended finance structures, this can include government-backed financial instruments to increase confidence among, and encourage the participation of, private sector investors. Blended finance is the use of catalytic capital from public or philanthropic sources to increase private sector investment in developing countries to realise the SDGs [

41].

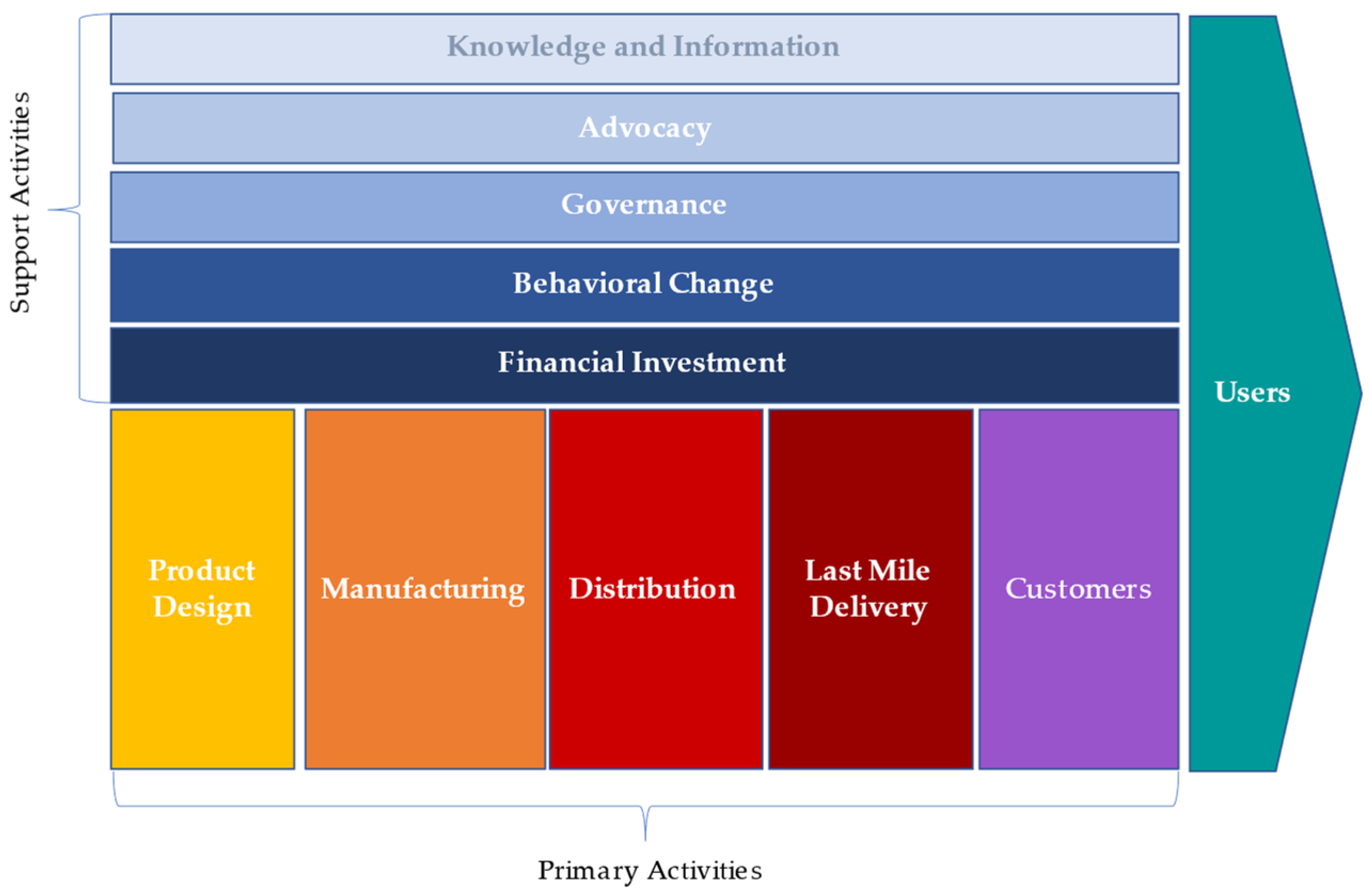

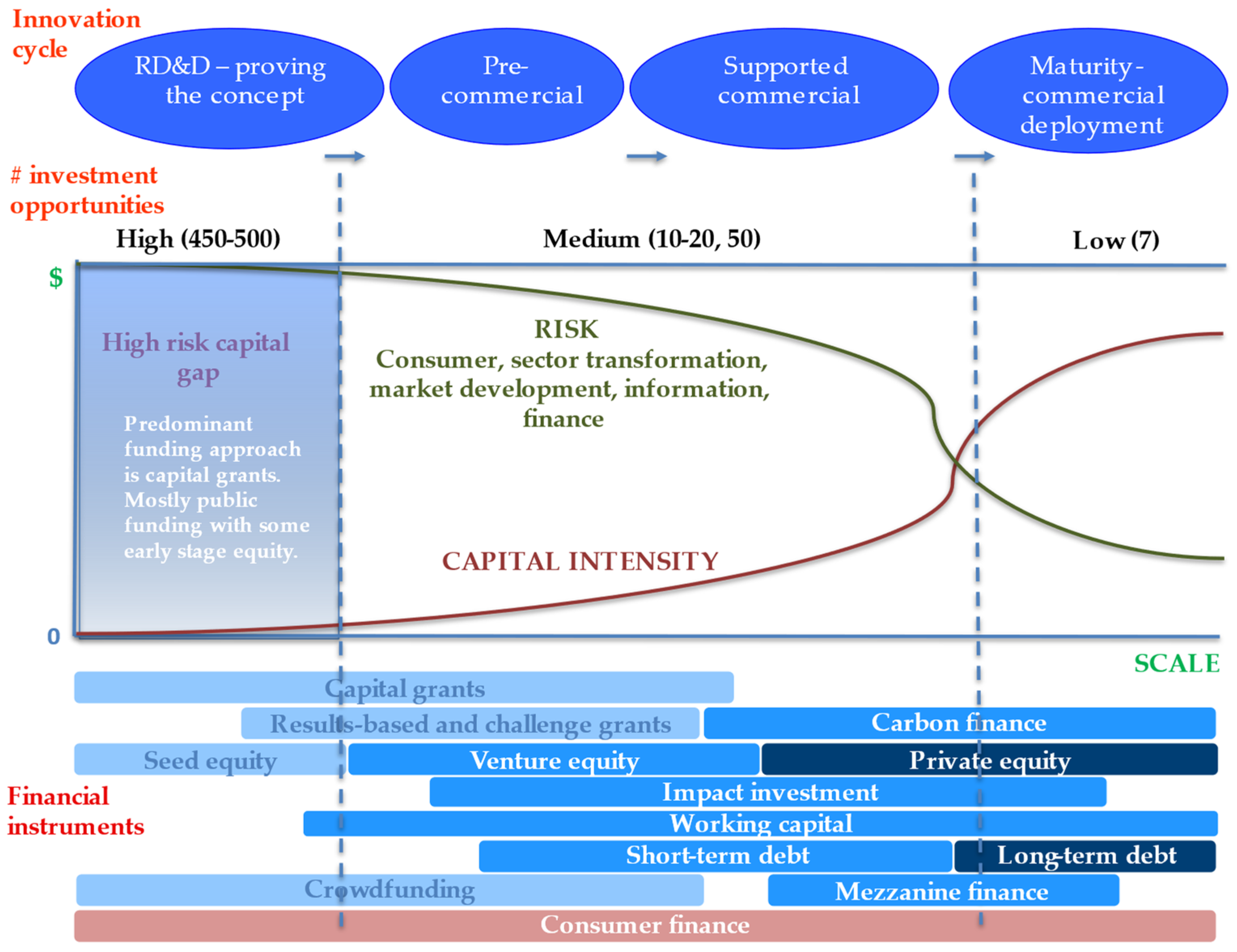

Applying these dynamics to the clean cooking sector,

Figure 5 shows a stylised progression of a clean cooking company through its innovation cycle following a typical S-curve. This is overlaid with considerations of consumer, sector transformation, market development, information and finance risk, and the financial instruments currently most used in the sector.

The data show a relatively high number of enterprises, and by extension, investment opportunities at the beginning of the cycle, where risks associated with new ventures are highest and, therefore, where clean cooking funders that seek a return are most reluctant to commit funding. In 2019–2020 combined, almost nine out of every ten dollars going into clean cooking companies sought some return on investment [

32].

This is reflected in financiers’ risk perceptions. Viewed through an equity investment lens, most are interested in funding enterprises in their early or late growth stage, followed by mature and then seed companies [

22]. Risk aversion has also driven existing investors towards familiar investees rather than high-potential new ventures [

6]. Similarly, in the LMD sector, start-up capital and small working capital loans can be difficult to secure in the early stages of company growth, creating a funding “valley of death”. These companies are often unsophisticated, struggle to identify suitable funders and are unable to communicate their value proposition using language that resonates with investors [

9,

28].

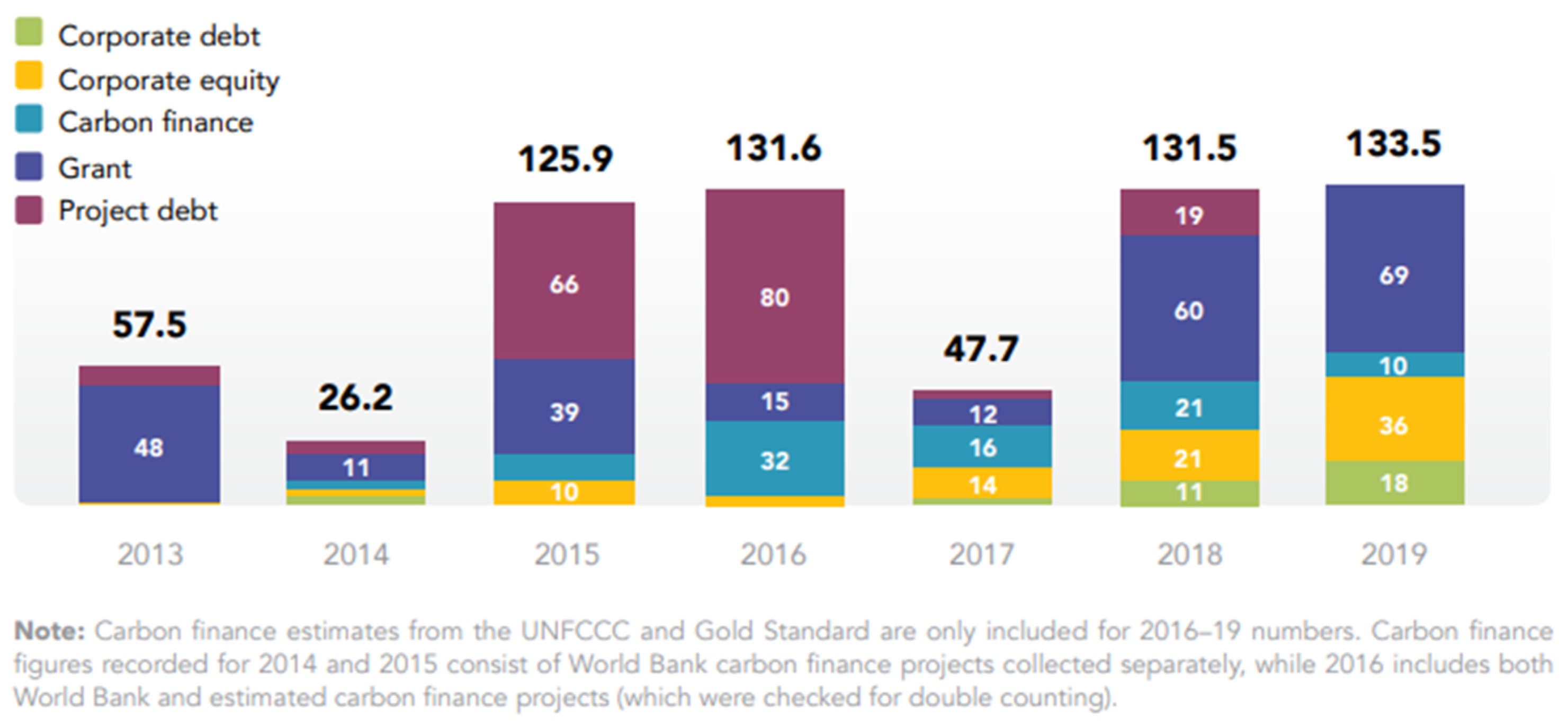

Critically, the risk aversion of private financiers in the early stages of business growth has not been met with a commensurate assumption of risk and volume of targeted public finance to help push promising new ventures through this essential stage of the innovation cycle. On the contrary, there is a dearth of RD&D funding to support the development of new clean cooking technology, ventures and pilot demonstration activity. This is underscored by the diminishing role of grants in funding clean cooking enterprises, where grants have traditionally been the financial instrument most likely to support RD&D. In 2020, grants represented the smallest amounts of capital flowing to clean cooking companies, with an average of USD 400,000 per company. Further, the number of companies reporting having received grants declined from thirty-six in 2014 to nineteen in 2020 [

32]. These data suggest an increasing concentration of grants into fewer companies over time, while the amount of grant funding per company has also declined. From the point of view of the innovation cycle, the implication is that ever fewer companies are receiving the early-stage capital required to test new ideas and prove business models as a precursor to private investment and scale.

Aside from company-level RD&D, several structured clean cooking RD&D programs exist or have existed but, with some exceptions, these have tended to be time-limited and focused on cookstoves, as distinct from the full range of modern cooking solutions [

6,

22]. A promising development is a planned innovation fund under the auspices of Pillar 2 of ESMAP’s USD 500 million Clean Cooking Fund. The innovation fund is envisaged to support “technological, business, policy, and financing innovations closely aligned with country and regional investment projects” and “co-financing of pilots and technology transfer for projects” [

42]. Notwithstanding these initiatives, current sector-wide clean cooking RD&D efforts are said to lack focus [

9].

Exacerbating the diminishing share of innovation funding is evidence that the sector’s traditional reliance on grant-based funding and subsidies does not in fact reduce the risk of debt or equity financing for private financiers, which are concerned with the profitability of businesses net of any grants they receive. Poorly designed grants and subsidies are at best unsuccessful and, in a worst-case scenario, can distort markets and sustain enterprises with sub-optimal business models [

9,

25].

The very small proportion of clean cooking businesses that become investible and scalable in the eyes of financiers bears this out. This speaks to an overall failure of early-stage funding for the sector to properly target key risks to business and sector growth [

6]. It, in turn, contributes to an incomplete supply-side financing value chain and an inefficient process of financial resource aggregation and transfer to clean cooking solutions providers. These companies’ ability to access commercial finance depends on their ability to demonstrate profitability in both the short and long term. This, in turn, arguably requires sustained public investment in innovation to put meritorious ideas on a path to success and, crucially, attract follow-on private sector funding.

4.3. Expanding Public Finance for Innovation and Risk Mitigation

In 2009, developed countries agreed to jointly mobilise USD 100 billion each year by 2020 to support developing countries in taking climate action. They reaffirmed and extended this commitment through 2025 under the auspices of the 2015 Paris Climate Agreement [

43]. However, the annual goal has never been met [

44]. Further, while the public sector can potentially play a powerful role in catalysing private sector finance by reducing constraints and underwriting risk, the volume of private capital mobilised through public climate finance did not exceed USD 15 billion in any year (2016–2020) for which comparable data are available [

45,

46]. As is widely acknowledged, public finance alone will not achieve the world’s emissions reduction targets and by implication, the SDGs that were established to help do so [

26]. Rather, the role of public finance should be to make judicious, targeted investments to prove a climate-friendly business or project’s investment readiness, catalyse co-investment and ultimately promote self-sustaining private finance markets.

Private investment in clean cooking markets can be leveraged through more and better targeted public funding for innovation to help nurture more companies through proof of concept and thereby improve the investment pipeline for later-stage commercial financiers. In this regard, an analogy may be drawn with decades-long public funding for the development of solar PV technology and the impact of that funding on PV deployment.

The cost of PV modules has declined ninety-nine percent since 1980. R&D and improvements in cell efficiency are the major contributing factors, accounting for almost a quarter of the decline between 1980 and 2012 [

47]. As a result, the cost of electricity from utility-scale PV fell eighty-five percent in the decade to 2020 and it is now the lowest cost source of electricity generation in history [

48,

49]. Annual investment in off-grid solar companies, whose consumer profile overlaps significantly with that of people without clean cooking access, was between USD 300 and 350 million between 2016 and 2020 [

50]. Investment into the off-grid solar sector in 2014 was USD 74.5 million, a similar amount to that seen in clean cooking companies in 2020 [

32].

As clean cooking companies move through the early stages of the innovation cycle, their RD&D efforts need not be limited to technology development and business model improvement. On the contrary, an approach that prioritises the practical and strategic needs of end users should be adopted to create the greatest potential for sustained adoption of solutions. The energy-related needs and concerns of the world’s poorest people, and therefore those most likely to experience cooking poverty, are rarely integrated into energy innovation efforts, are understudied and are poorly understood [

51]. Research efforts should therefore be channeled to better understand end-use consumer preferences and other demand-side barriers. For example, a wide variety of customer segments exist for cookstoves based on characteristics and price points and it is critical that RD&D efforts aim to develop and foster solutions that consumers find useful and attractive. Notably, research has found that consumer-facing subsidies to incentivise adoption often do not match consumers’ needs and preferences, which are better understood by cooking companies themselves. As a result, policies that use indirect subsidies to support company RD&D, manufacturing and marketing tend to be more successful than blanket consumer-facing subsidies in creating sustained adoption [

9].

To the extent that fledgling companies do not secure the finance necessary to develop their business models to viability, they will not contribute to a later pipeline of potential investees; these are precisely the issues cited by financiers as the greatest barriers to scale. As a result, public finance has a critical role to play in supporting RD&D and innovation, whether related to technology development, business model improvement or consumers, that are necessary to nurture promising new ideas through to bankability and scale. This is entirely consistent with SDG7.a’s target to enhance international cooperation to facilitate access to clean energy research and technology, while progress could be assessed by reference to indicator SDG7.a.1, which measures international financial flows to developing countries in support of clean energy research and development [

13]. While competition and the attractiveness of growing clean cooking markets will of itself incentivise RD&D investment, greater strategic engagement in the RD&D process by public funders will arguably accelerate a business’s progress through this crucial phase of the innovation cycle [

9].

Beyond innovation funding, public financiers are uniquely placed to promote new financing solutions and co-funding efforts, especially through assuming greater risk and anchoring blended finance structures.

Clean cooking companies that have endured through the difficult, early stages of their business growth encounter a range of obstacles that prevent them from becoming one of the handful of businesses that have attracted significant funding to scale. Part of the reason for this is a lack of catalytic public finance for businesses in their growth stages, as well as a lack of structure around co-funding and risk sharing among public and private funders.

In June 2019, SEforALL convened a set of charrettes in Amsterdam, Netherlands, to identify impactful but pragmatic solutions to accelerate progress on SDG7. One of four charrettes was grounded in the question: “What is required to create a sustainable, investable, private sector-led market for fuels for clean cooking?” Twenty-seven experts from developed and developing countries, who represented organisations spanning the full value chain, were invited to participate in this “Clean Cooking Charrette”. They were asked, collectively, to bring forth solutions with the potential to disrupt the sector’s status quo and enable transformative progress towards the achievement of universal access to clean fuels and technology for cooking by 2030 [

12].

One such solution was a proposal to create a Clean Cooking Market Catalyst (CCMC) that seeks to address the fragmentation and inefficiency of current donor-funded programs and projects by aligning providers of public finance on a common vision and approach to prove the viability of, and to scale, the clean cooking market. The CCMC was envisioned as a USD 1 billion, grant-funded platform that would offer a suite of financial products across the development and finance continuum of clean cooking, enabling quick decision-making and a high risk tolerance. With a prioritisation on “clean” fuels, the platform would offer equity for 15–20 select companies languishing in the “valley of death”, to demonstrate scalability and create confidence in the sector; a catalytic finance window to foster innovative business models and technology solutions; an RBF window that would pay for verified social, health and gender impacts of deployed solutions; and a debt fund for consumer finance and company working capital, with a possible guarantee window [

12].

In its emphasis on a greater assumption of risk by public funders, the CCMC concept aligns with the IEA’s assertion that concessional finance provided by public financiers has a key role to play in helping to de-risk commercial participation [

3]. It is also consistent with MECS and Energy 4 Impact’s recommendation to expand the availability of concessionary, first loss capital to catalyse commercial debt at later stages of clean cooking company growth and that of the GDC to create new or adapted debt mechanisms to free up companies’ working capital [

22,

28].

As is the case with innovation, public funding, including through DFIs, has a unique role to play in anchoring blended finance funds and facilities, as well as assuming early-stage risk, by fulfilling the promise of public funders’ typically expansive funding mandates.

4.4. Improving Data and Knowledge Sharing among Financiers

Closely related to investment barriers concerning investees and pipeline are poor data availability and knowledge sharing among clean cooking funders. Siloed, fragmented data on markets, enterprises and customers are some of the biggest obstacles to attracting capital to the sector. With incomplete data, financiers are less effectively able to define markets, develop investment strategies, conduct due diligence and close investments [

22,

28]. When looked at through the lens of the business growth cycle, scarce data means that financiers have less visibility into which clean cooking solutions are working and, therefore, to target resources to promote the scale-up of demonstrably successful strategies. Specifically, a dearth of rigorous, context-specific evidence on the success of different business models acts as a barrier to growth for clean cooking enterprises, particularly in their early stages [

9]. ESMAP notes that most sector data come from academic journals, with very little from non-journal sources, such as international organisations, non-government organisations and the private sector. The effect is that the results of much valuable fieldwork are not finding their way into the synthesis of evidence [

25].

In contrast, improved collaboration and sharing of market-oriented data among funders can help them, in aggregate, form a more complete picture of potential investees and a truly integrated view of the sector. This should in turn result in better investment decision-making and a more efficient process of financial resource aggregation and transfer to businesses.

Sector financiers are overwhelmingly in favour of greater data sharing and knowledge exchange. More than eighty percent of clean cooking funders want an online data portal as a collaborative effort with other stakeholders [

22]. Similarly, the LMD sector calls for greater collaboration among funders through improved data sharing, for example, through the creation of an investment portal, as well as investment readiness and data tools to increase LMD companies’ visibility and help them showcase their performance [

28].

Notwithstanding the demand, to date, no attempt has been made to create a dynamic, open-access portal as a repository of sector data. However, the idea was foreshadowed by the SEforALL Clean Cooking Charrette participants, who envisaged a platform that would provide accurate and timely data to help drive informed decisions by investors, enterprises and governments to allocate resources and funding to viable and scalable clean cooking solutions. The platform would optimise existing data while making it more accessible and usable, for example, through the visualisation of MTF household survey data. Additional data would be collected and evidence derived on the impacts of cooking practices on health, climate and gender equality, with transparency around measurement and metrics. Consumer preference data would also be captured, as would data on next-generation solutions to identify and test the scalability of promising ideas and business models [

12].

The demand from sector stakeholders for a data portal need not be met by creating a whole new infrastructure. Rather, existing platforms conceived of and sponsored by public international institutions with an interest in climate and energy could be leveraged to achieve the same objective. For example, the Climate Investment Platform (CIP) or the Global Atlas for Renewable Energy could incorporate a clean cooking data window. The CIP was jointly announced by the United Nations Development Programme (UNDP), the International Renewable Energy Agency (IRENA) and SEforALL in coordination with the Green Climate Fund (GCF) at the UN Secretary-General’s Climate Action Summit in September 2019. It convenes governments, financial institutions, project developers and the private sector to increase financing for climate action and help countries reach their climate goals, with its first focus being the clean energy transition [

52]. IRENA’s Global Atlas for Renewable Energy, informed by data from over fifty international research institutions, is an online platform intended to assist policymakers and investors to find renewable energy resource maps for locations across the world. It aims to close the gap between countries that have access to the necessary data and expertise to evaluate the potential for renewable energy deployment in their countries and those that do not [

53]. Cross-sectoral collaboration on clean cooking data capture and sharing through, for example, the CIP or the Global Atlas for Renewable Energy would have the benefit of better integrating clean cooking with broader energy transition and related investment initiatives.

DFIs also have the motivation and resources to play a key role in knowledge sharing by facilitating the development of best-case practices, as well as investing in rigorous monitoring and evaluation of different business models and strategies with the objective of generating adaptable evidence that could be made freely available [

9]. In this regard, Pillar 2 of ESMAP’s USD 500 million Clean Cooking Fund is a global platform for knowledge, innovation and policy coordination. This is intended to incorporate a “knowledge platform for publishing and sharing analytical products, promoting cross-country learning and exchange, and taking stock of knowledge gaps and opportunities” [

42]. A logical extension of this concept could include dynamic data of the kind envisaged at the Clean Cooking Charrette.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}