The Influencing Factors of the Carbon Trading Price: A Case of China against a “Double Carbon” Background

Abstract

:1. Introduction

1.1. Research Background

1.2. Research Significance

1.3. Research Content and Innovation

2. Literature Review

2.1. Theoretical Basis of Carbon Trading and Trading Prices

2.1.1. Externality Theory

2.1.2. Emission Trading Theory

2.2. Formation Mechanism of the CTP

2.2.1. Carbon Total Emission Trading Mechanism

2.2.2. Carbon Emission Offsetting Mechanism

2.2.3. Carbon Financial Mechanism

2.2.4. Carbon Tax Mechanism

2.3. The Influencing Factors of the CTP

2.3.1. Macroeconomic Factors

2.3.2. Energy Price Factors

2.3.3. Policy Factors

2.3.4. Environmental Factors

2.4. Literature Reviews

3. Theoretical Hypothesis of the Effects of the Factors on the CTP

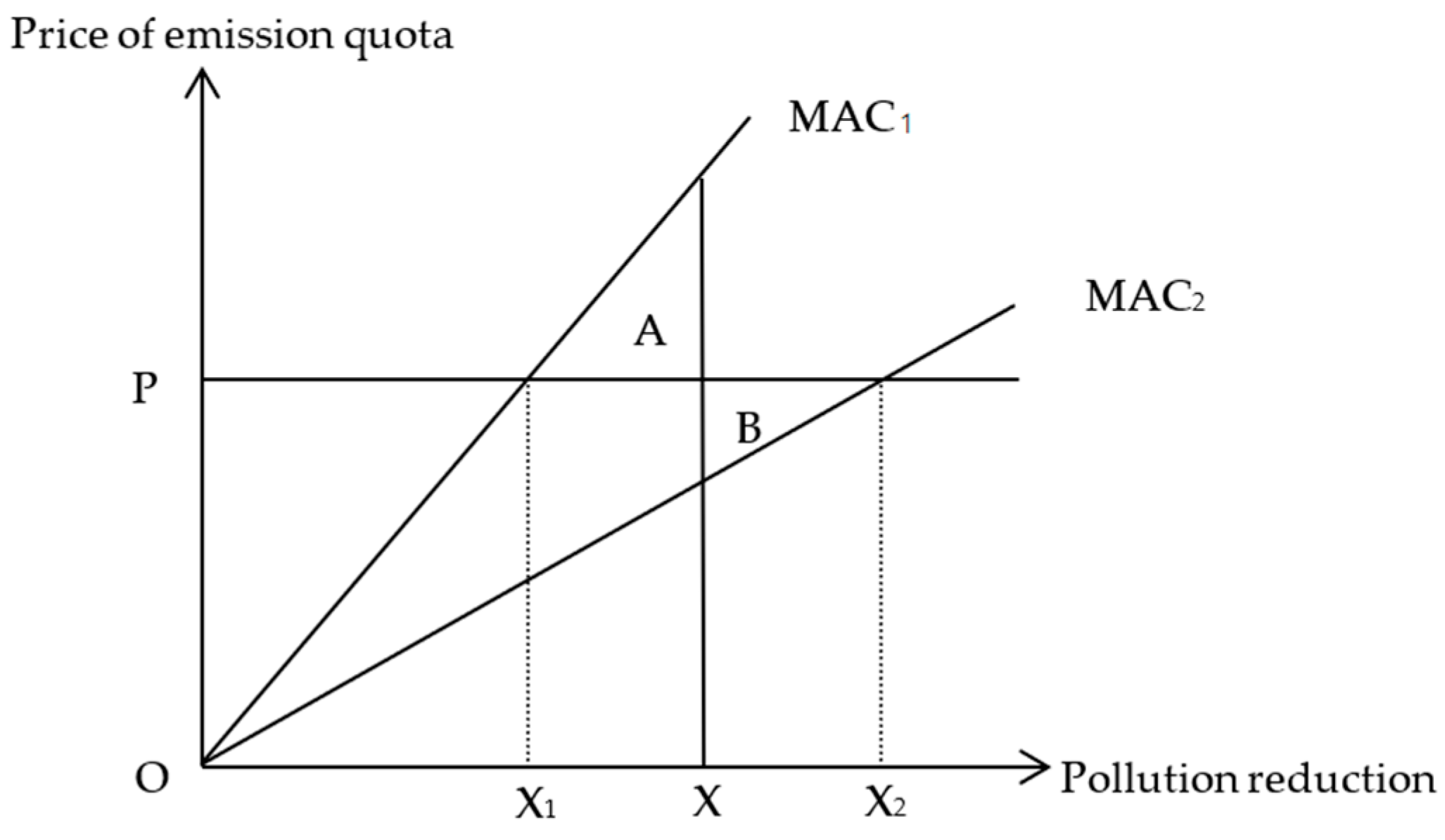

3.1. Effect of Environmental Factors on the CTP

3.2. Effect of Energy Price Factors on the CTP

3.3. Effect of Macroeconomic Factors on the CTP

3.4. Construction of the Basic Model

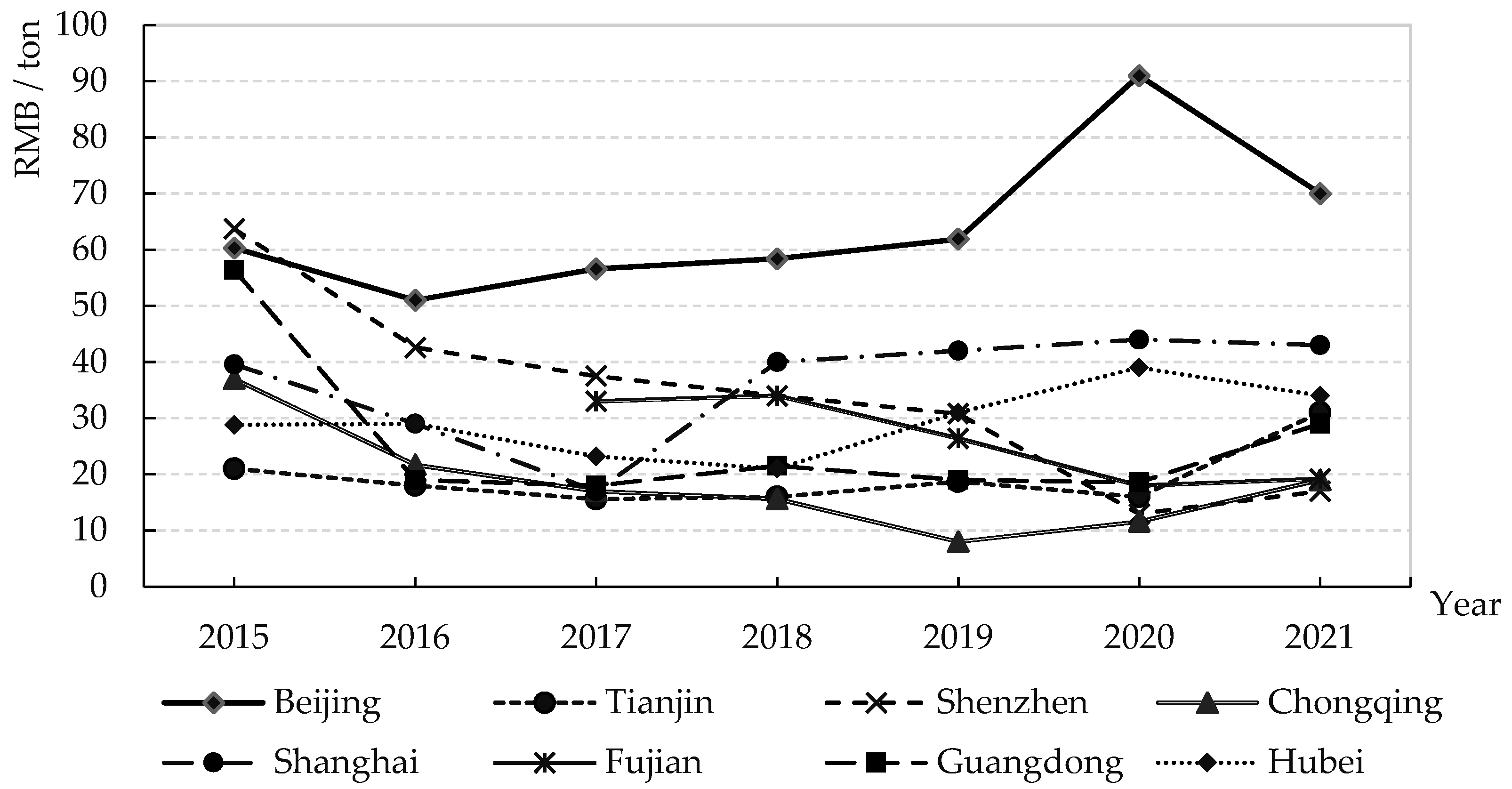

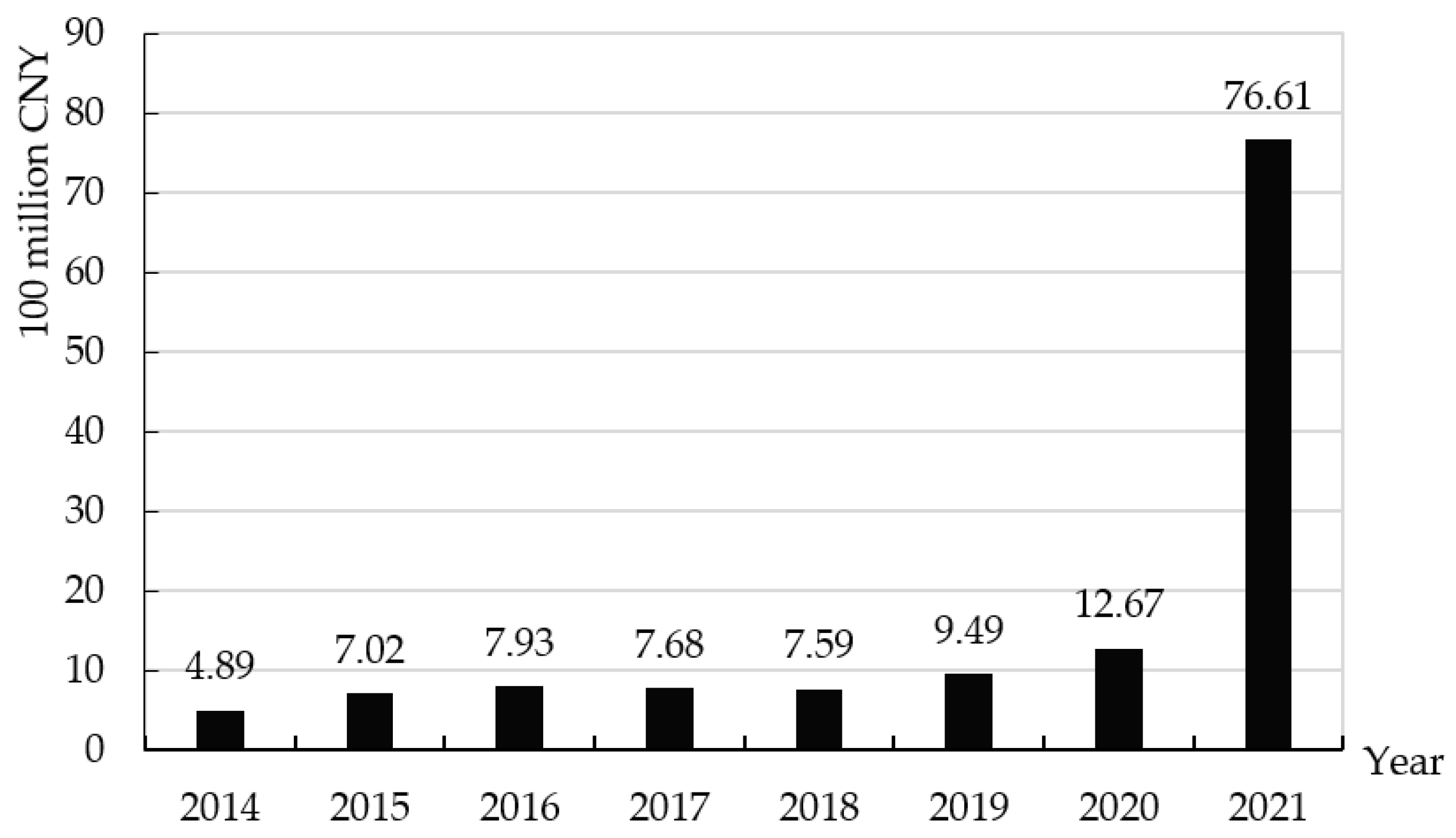

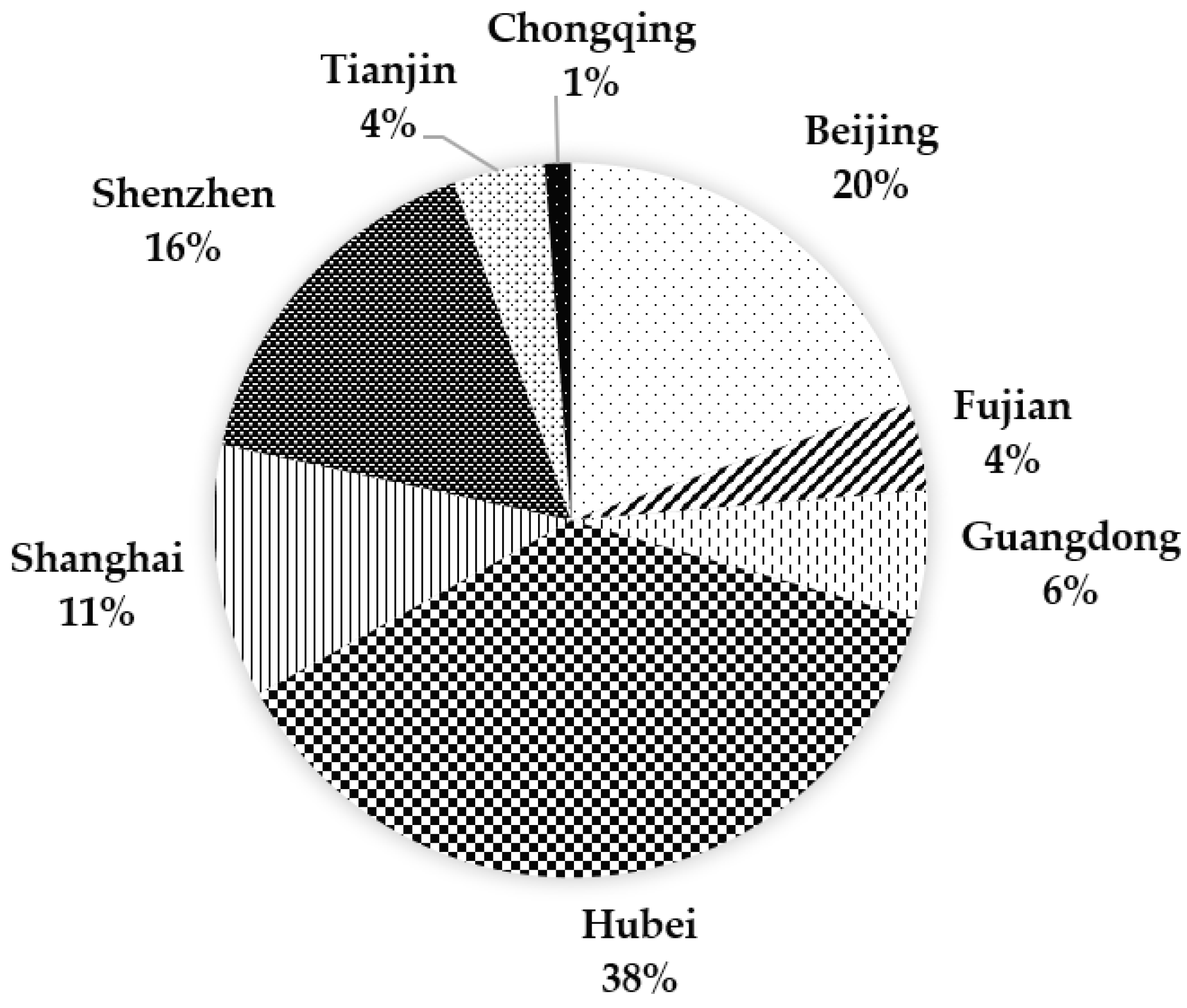

4. China Carbon Emission Trading Market Status

4.1. Development Progress

4.2. Status Analysis

5. Empirical Analysis of the Influencing Factors of the CTP

5.1. Variable Selection and Data Sources

5.1.1. Variable Selection

5.1.2. Data Source

5.2. Model Construction

5.2.1. Empirical Model Setting

5.2.2. Descriptive Statistics of Variables

5.2.3. Correlation Analysis of Variables

5.3. Empirical Test

5.3.1. Cross-Section Correlation Test Result

5.3.2. Panel Unit Root Test Results and Cointegration Test Results

5.4. Dynamic Heterogeneous Panel PMG Model Results

6. Conclusions and Recommendations

6.1. Conclusions

6.1.1. Effect of Industrial Sector on the CTP

6.1.2. Effect of Energy Price on the CTP

6.1.3. Effect of Air Quality on the CTP

6.2. Policy Recommendations

6.3. Research Deficiencies

Author Contributions

Funding

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Key Term | Abbreviations |

|---|---|

| Carbon trading price | CTP |

| Air quality index | AQI |

| Bohai-Rim steam-coal price index | BSPI |

| Liquefied natural gas index | LNGI |

| Shanghai stock exchange industrial index | SSEII |

| China carbon emission trade exchange | CCETE |

| European Union | EU |

| Carbon dioxide | CO2 |

| Emissions trading system | ETS |

| EU emission allowance | EUA |

| secondary certified emission reductions | sCERs |

| China Carbon Emissions Database | CEADs |

References

- Song, X.; Zhang, W.; Ge, Z.; Huang, S.; Huang, Y.; Xiong, S. A Study of the Influencing Factors on the Carbon Emission Trading Price in China Based on the Improved Gray Relational Analysis Model. Sustainability 2022, 14, 8002. [Google Scholar] [CrossRef]

- NDRC, China 2050 High Renewable Energy Penetration Scenario and Roadmap Study. Available online: https://www.efchina.org/Attachments/Report/report-20150420 (accessed on 6 October 2022).

- Statement by H.E. Xi Jinping, President of the People’s Republic of China, At the General Debate of the 75th Session of the United Nations General Assembly, Chinadaily 22 September 2020. Available online: https://language.chinadaily.com.cn/a/202009/23/WS5f6a9cc2a31024ad0ba7b25f.html (accessed on 23 September 2020).

- Wang, L.; Yin, K.; Cao, Y.; Li, X. A new grey relational analysis model based on the characteristic of inscribed core (IC-GRA) and its application on seven-pilot carbon trading markets of China. Int. J. Environ. Res. Public Health 2019, 16, 99. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Sun, W.; Zhang, J. Carbon price prediction based on ensemble empirical mode decomposition and extreme learning machine optimized by improved bat algorithm considering energy price factors. Energies 2020, 13, 3471. [Google Scholar] [CrossRef]

- Zhao, B.; Sun, L.; Gao, S. Effects of Government Regulations on Under-Reporting of Carbon Emission Transfers by Enterprises in Supply Chains. Sustainability 2022, 14, 9269. [Google Scholar] [CrossRef]

- Komarova, A. State Regulation of Energy Transition and Economic Development. Energies 2022, 15, 4304. [Google Scholar] [CrossRef]

- Ji, C.; Li, X.; Hu, Y.; Wang, X.Y.; Tang, B.J. Research on carbon price in emissions trading scheme: A bibliometric analysis. Nat. Hazards 2019, 99, 1381–1396. [Google Scholar] [CrossRef]

- Zeng, S.; Zhang, H.; Qu, Y.; Zeng, B. Study on price fluctuation and influencing factors of regional carbon emission trading in China under the background of high-quality economic development. Int. Energy J. 2021, 21, 201–211. [Google Scholar]

- Ellerman, A.; Buchner, B. The European Union emissions trading scheme: Origins, allocation, and early results. Rev. Environ. Econ. Policy 2007, 1, 66–87. [Google Scholar] [CrossRef]

- Zhu, H.; Tang, Y.; Peng, C.; Yu, K. The heterogeneous response of the stock market to emission allowance price: Evidence from quantile regression. Carbon Manag. 2018, 9, 277–289. [Google Scholar] [CrossRef]

- Conrad, C.; Rittler, D.; Rotfuss, W. Modeling and explaining the dynamics of european union allowance prices at high-frequency. Energy Econ. 2012, 34, 316–326. [Google Scholar] [CrossRef] [Green Version]

- Jiang, C.; Yue, Y. Sensitivity analysis of key factors influencing carbon prices under the EU ETS. Pol. J. Environ. Stud. 2021, 30, 3645–3658. [Google Scholar] [CrossRef]

- Sun, W.; Sun, C.; Li, Z. A Hybrid Carbon Price Forecasting Model with External and Internal Influencing Factors Considered Comprehensively: A Case Study from China. Pol. J. Environ. Stud. 2020, 29, 3305–3316. [Google Scholar] [CrossRef]

- Yang, J.; Dong, H.; Shackman, J.D.; Yuan, J. Construction of a carbon price benchmark in China—Analysis of eight pilot markets. Environ. Sci. Pollut. Res. 2022, 29, 41309–41328. [Google Scholar] [CrossRef] [PubMed]

- Lamphiere, M.; Blackledge, J.; Kearney, D. Carbon Futures Trading and Short-Term Price Prediction: An Analysis Using the Fractal Market Hypothesis and Evolutionary Computing. Mathematics 2021, 9, 1005. [Google Scholar] [CrossRef]

- Jiang, Y.; Wu, Z. Regression analysis of the factors affecting the carbon pricing in China. Environ. Sustain. Dev. 2021, 46, 77–83. [Google Scholar] [CrossRef]

- Yan, Z.; Cui, C. How Natural Gas Infrastructure Affects Carbon Emission Indicators in Guangdong Province? Sustainability 2022, 14, 8104. [Google Scholar] [CrossRef]

- Yang, X.; Zhang, C.; Yang, Y.; Wu, Y.; Yun, P.; Wagan, Z.A. China’s Carbon Pricing Based on Heterogeneous Tail Distribution. Sustainability 2020, 12, 2754. [Google Scholar] [CrossRef] [Green Version]

- Huang, S. Three Theoretical Pillars to Support ESG. Financ. Account. Mon. 2021, 19, 3–10. [Google Scholar] [CrossRef]

- Shi, D.; Zhang, C.; Zhou, B.; Yang, L. The True Impacts of and Influencing Factors Relating to Carbon Emissions Rights Trading: A Comprehensive Literature Review. Chin. J. Urban Environ. Stud. 2018, 6, 1850016. [Google Scholar] [CrossRef]

- Zhao, S. The essence of Coase theorem and its academic disputes. Economist 2004, 4, 92–96. [Google Scholar] [CrossRef]

- Wu, Q.; Wang, Y. How does carbon emission price stimulate enterprises’ total factor productivity? Insights from China’s emission trading scheme pilots. Energy Econ. 2022, 109, 105990. [Google Scholar] [CrossRef]

- Chen, S.; Huang, M.; Bin, H. Institutional Optimization of Sustainable Development of National Carbon Trading Market under Dual Carbon Target. Financ. Minds 2021, 4, 88–101,142–143. Available online: https://oversea.cnki.net/kns/detail/detail.aspx?FileName=CJZK202104006&DbName=CJFQ2021 (accessed on 20 May 2022).

- Zhu, R.; Long, L.; Gong, Y. Emission Trading System, Carbon Market Efficiency, and Corporate Innovations. Int. J. Environ. Res. Public Health 2022, 19, 9683. [Google Scholar] [CrossRef] [PubMed]

- Liu, L.; Zhang, Y.; Zhou, Q. Some Suggestions on the Carbon Taxation in China from the Perspective of Coordination of Policy. Tax. Res. 2022, 3, 121–126. [Google Scholar] [CrossRef]

- Green, J.F. Does carbon pricing reduce emissions? A review of ex-post analyses. Environ. Res. Lett. 2021, 16, 043004. [Google Scholar] [CrossRef]

- Peng, X.; Zhong, Y. Research on influencing factors and strategies of carbon emission trading price. Prices Mon. 2021, 12, 25–31. [Google Scholar] [CrossRef]

- Wu, H.; Zhang, Z. Price characteristics and its causes in China’s carbon market: Level, equilibrium and stability. World For. Res. 2021, 34, 123–128. [Google Scholar] [CrossRef]

- Fan, Y.; Wang, X. Which Sectors Should Be Included in the ETS in the Context of a Unified Carbon Market in China? Energy Environ. 2014, 25, 613–634. [Google Scholar] [CrossRef]

- Zhang, X.; Zhang, D.; Yu, R. Theory and Practice of China’s National Carbon Emissions Trading System. J. Manag. World 2021, 37, 80–95. [Google Scholar] [CrossRef]

- Zhang, J.; Liang, Z.; Matsumoto, T.; Zhang, T. Environmental and Economic Implication of Implementation Scale of Sewage Sludge Recycling Systems Considering Carbon Trading Price. Sustainability 2022, 14, 8684. [Google Scholar] [CrossRef]

- Li, L.; Ye, F.; Li, Y.; Chang, C. How will the Chinese Certified Emission Reduction scheme save cost for the national carbon trading system? J. Environ. Manag. 2019, 244, 99–109. [Google Scholar] [CrossRef] [PubMed]

- Li, Y.; Lv, Y. Research Progress of China’s Carbon Trading System. J. Shanghai Lixin Univ. Account. Financ. 2019, 3, 42–52. [Google Scholar] [CrossRef]

- Ji, C.; Hu, Y.; Tang, B.; Qu, S. Price drivers in the carbon emissions trading scheme: Evidence from Chinese emissions trading scheme pilots. J. Clean. Prod. 2021, 278, 123469. [Google Scholar] [CrossRef]

- Liu, C.; Luan, W.; Guo, G. Research on the Impact Mechanism of Green Finance Development on Carbon Rights Trading and Carbon Emissions. Trade Fair Econ. 2022, 7, 133–136. [Google Scholar] [CrossRef]

- Xie, C.; Li, J.; Xu, E. Construction of carbon pricing system based on carbon market and carbon tax. Int. Financ. 2021, 5, 20–31. [Google Scholar] [CrossRef]

- Jiang, J. Analysis of Carbon Pricing Mechanism and Proposals on the Improvement of China’s Carbon Market under Carbon Neutralization. Price Theory Pract. 2022, 2, 26–30,90. [Google Scholar] [CrossRef]

- Dutta, A.A. Impact of carbon emission trading on the European Union biodiesel feedstock market. Biomass Bioenergy 2019, 128, 105328. [Google Scholar] [CrossRef]

- Wang, H. International Experience, China Development and Prospect of Carbon Market Construction. Int. Financ. 2021, 12, 23–33. [Google Scholar] [CrossRef]

- Santos, L.; Steininger, K.; Cordeiro, M.C.; Vogel, J. Current Status and Future Perspectives of Carbon Pricing Research in Austria. Sustainability 2022, 14, 9684. [Google Scholar] [CrossRef]

- Ji, C.; Hu, Y.; Tang, B. Research on carbon market price mechanism and influencing factors: A literature review. Nat. Hazards 2018, 92, 761–782. [Google Scholar] [CrossRef]

- Li, Y.; Song, J. Research on the application of GA-ELM Model in carbon trading price—An example of Beijing. Pol. J. Environ. Stud. 2022, 31, 149–161. [Google Scholar] [CrossRef]

- Wang, Z.; Hu, Y. An empirical analysis of the factors affecting the carbon price in China. J. Ind. Technol. Econ. 2018, 2, 128–136. Available online: https://oversea.cnki.net/kns/detail/detail.aspx?FileName=GHZJ201802016&DbName=CJFQ2018 (accessed on 20 May 2022).

- Chu, W.; Chai, S.; Chen, X.; Du, M. Does the Impact of Carbon Price Determinants Change with the Different Quantiles of Carbon Prices? Evidence from China ETS Pilots. Sustainability 2020, 12, 5581. [Google Scholar] [CrossRef]

- Zhu, B.; Tang, J.; Wang, P.; Zhang, L. Exploring the drivers of carbon market risk: A meta regression analysis. J. Clean. Prod. 2022, 352, 131538. [Google Scholar] [CrossRef]

- Zhou, K.; Li, Y. Influencing factors and fluctuation characteristics of China’s carbon emission trading price. Phys. A Stat. Mech. Its Appl. 2019, 524, 459–474. [Google Scholar] [CrossRef]

- Kanamura, T. Role of carbon swap trading and energy prices in price correlations and volatilities between carbon markets. Energy Econ. 2016, 54, 204–212. [Google Scholar] [CrossRef]

- Zhu, B.; Ye, S.; Han, D.; Wang, P.; He, K.; Wei, Y.; Xie, R. A multiscale analysis for carbon price drivers. Energy Econ. 2019, 78, 202–216. [Google Scholar] [CrossRef]

- Li, Y. An empirical study on the external influencing factors of carbon emission trading pricing. Price Theory Pract. 2020, 6, 146–149. [Google Scholar] [CrossRef]

- Lin, B.; Xu, B. A non-parametric analysis of the driving factors of China’s carbon prices. Energy Econ. 2021, 104, 105684. [Google Scholar] [CrossRef]

- Zhang, J.; Wang, Z.; Lei, Y. The Enlightenment of the EU Carbon Market Experience to the Construction of China’s Carbon Market Chinese Full Text. Price Theory Pract. 2020, 1, 32–36,170. [Google Scholar] [CrossRef]

- Peng, W.; Chen, S. Analysis and Forecast of Carbon Trading Price in China’s Carbon Emission Pilot Market. J. Technol. Econ. 2020, 3, 102–110. [Google Scholar]

- Zhang, S.; Ji, H.; Tian, M.; Wang, B. High-dimensional nonlinear dependence and risk spillovers analysis between China’s carbon market and its major influence factors. Ann. Oper. Res. 2022, JUNE, 1–30. [Google Scholar] [CrossRef] [PubMed]

- Bredin, D.; Muckley, C. An emerging equilibrium in the EU emissions trading scheme. Energy Econ. 2011, 33, 353–362. [Google Scholar] [CrossRef]

- Lovcha, Y.; Perez-Laborda, A.; Sikora, I. The determinants of CO2 prices in the EU emission trading system. Appl. Energy 2022, 305, 117903. [Google Scholar] [CrossRef]

- Alberola, E.; Chevallier, J.; Chèze, B.T. Price drivers and structural breaks in European carbon prices 2005–2007. Energy Policy 2008, 36, 787–797. [Google Scholar] [CrossRef]

- Mansanet-Bataller, M.; Pardo, A.; Valor, E. CO2 prices, energy and weather. Energy J. 2007, 28, 73–92. [Google Scholar] [CrossRef]

- Ali, M.; Tursoy, T.; Samour, A.; Moyo, D.; Konneh, A. Testing the impact of the gold price, oil price, and renewable energy on carbon emissions in South Africa: Novel evidence from bootstrap ARDL and NARDL approaches. Resour. Policy 2022, 79, 102984. [Google Scholar] [CrossRef]

- Zhang, J.; Xu, Y. Research on the Price Fluctuation and Risk Formation Mechanism of Carbon Emission Rights in China Based on a GARCH Model. Sustainability 2020, 12, 4249. [Google Scholar] [CrossRef]

- Wu, Q.; Tambunlertchai, K.; Pornchaiwiseskul, P. Examining the Impact and Influencing Channels of Carbon Emission Trading Pilot Markets in China. Sustainability 2021, 13, 5664. [Google Scholar] [CrossRef]

- Chen, Y.; Sun, Y.; Wang, C. Influencing Factors of Companies’ Behavior for Mitigation: A Discussion within the Context of Emission Trading Scheme. Sustainability 2018, 10, 414. [Google Scholar] [CrossRef]

| Variable Category | Variable Name | Variable Abbreviation | Data Sources |

|---|---|---|---|

| the explained variable | |||

| PRICE | CTP of Beijing | BEIJING | http://www.tanpaifang.coc/ (accessed on 12 April 2022) |

| CTP of Shenzhen | SHENZHEN | ||

| CTP of Shanghai | SHANGHAI | ||

| CTP of Hubei | HUBEI | ||

| CTP of Guangdong | GUANGDONG | ||

| explanatory variables | |||

| macroeconomic factor | SSEII | IND | wind |

| nonclean energy price factor | BSPI | COAL | |

| clean energy price factor | LNGI | GAS | |

| environmental factor | AQI | AQI | https://www.mee.gov.cn/ (accessed on 12 April 2022). |

| Variable | Mean | Std. Dev. | Minimum | Maximum | Observations |

|---|---|---|---|---|---|

| PRICE | 34.861 | 19.871 | 3.030 | 107.260 | 6035 |

| BEIJING | 65.274 | 18.647 | 24.000 | 107.260 | 1207 |

| SHENZHEN | 21.248 | 11.182 | 3.030 | 56.240 | 1207 |

| SHANGHAI | 37.844 | 4.580 | 24.750 | 49.500 | 1207 |

| HUBEI | 26.188 | 8.383 | 11.560 | 53.850 | 1207 |

| GUANGDONG | 23.751 | 9.627 | 11.050 | 47.800 | 1207 |

| IND | 31.521 | 2.945 | 24.644 | 37.154 | 6035 |

| GAS | 40.582 | 11.558 | 24.932 | 76.350 | 6035 |

| COAL | 5.887 | 0.539 | 5.260 | 8.480 | 6035 |

| AQI | 0.595 | 0.164 | 0.040 | 7.890 | 6035 |

| PRICE | IND | GAS | COAL | AQI | |

|---|---|---|---|---|---|

| PRICE | 1.000 | ||||

| IND | 0.002 | 1.000 | |||

| GAS | −0.045 *** | 0.243 *** | 1.000 | ||

| COAL | 0.020 | 0.526 *** | 0.591 *** | 1.000 | |

| AQI | 0.024 * | −0.131 *** | −0.026 ** | −0.091 *** | 1.000 |

| Variable | VIF | VIF |

|---|---|---|

| IND | 1.410 | 0.710 |

| GAS | 1.554 | 0.644 |

| COAL | 2.022 | 0.495 |

| AQI | 1.019 | 0.982 |

| Mean VIF | 1.501 |

| Method | CD | P |

|---|---|---|

| PesaranCSD | 10.357 | 0.000 |

| FreesCSD | 0.972 | 0.000 |

| Variable | Statistic | P | D_Variable | Statistic | P |

| PRICE | −9.368 | 0.000 | D.PRICE | −63.424 | 0.000 |

| IND | −80.533 | 0.000 | D.IND | −53.069 | 0.000 |

| GAS | −4.301 | 0.988 | D.GAS | −54.677 | 0.000 |

| COAL | 0.784 | 1.000 | D.COAL | −54.946 | 0.000 |

| AQI | −53.310 | 0.000 | D.AQI | −88.200 | 0.000 |

| Variable | Shanghai | Beijing | Guangdong | Shenzhen | Hubei |

|---|---|---|---|---|---|

| ECM | 0.943 *** | 0.951 *** | 0.999 *** | 0.799 *** | 0.995 *** |

| (98.77) | (106.53) | (521.37) | (46.05) | (321.70) | |

| IND | 0.083 ** | −0.030 | 0.078 * | 0.048 | 0.076 * |

| (2.03) | (−0.44) | (1.92) | (0.66) | (1.86)) | |

| D.GAS | 0.005 | 0.245 ** | 0.002 | −0.004 | −0.028 |

| (0.17) | (2.27) | (0.19) | (−0.03) | (−1.60) | |

| D.COAL | −0.730 | 4.925 | 0.043 | −1.438 | 0.208 |

| (−0.66) | (1.23) | (0.10) | (−0.29) | (0.32) | |

| AQI | −0.124 | 0.138 | 0.414 | −0.982 | 0.142 |

| (−0.65) | (0.09) | (1.62) | (−0.42) | (1.25) | |

| _CONS | 1.769 *** | 6.187 ** | −0.377 | 5.153 ** | −0.081 |

| (2.94) | (2.38) | (−1.63) | (1.97) | (−0.25) | |

| obs | 1207 | 1207 | 1207 | 1207 | 1207 |

| Variable | Statistic | Z |

|---|---|---|

| Long-term parameter | ||

| IND | 0.073 * | 1.80 |

| (1.80) | ||

| D.GAS | −0.015 | −1.63 |

| (−1.63) | ||

| D_COAL | 0.079 | 0.24 |

| (0.24) | ||

| AQI | −0.054 | −0.57 |

| (−0.57) | ||

| Short-term parameter | ||

| ECM | 0.937 *** | 25.70 |

| (25.70) | ||

| IND | 0.051 ** | 2.40 |

| (2.40) | ||

| D.GAS | 0.044 | 0.87 |

| (0.87) | ||

| D.COAL | 0.602 | 0.54 |

| (0.54) | ||

| AQI | −0.082 | −0.34 |

| (−0.34) | ||

| _CONS | 2.530 * | 1.88 |

| (1.88) | ||

| Log likelihood | −12,559.350 | |

| OBS | 6035 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Zeng, S.; Fu, Q.; Yang, D.; Tian, Y.; Yu, Y. The Influencing Factors of the Carbon Trading Price: A Case of China against a “Double Carbon” Background. Sustainability 2023, 15, 2203. https://doi.org/10.3390/su15032203

Zeng S, Fu Q, Yang D, Tian Y, Yu Y. The Influencing Factors of the Carbon Trading Price: A Case of China against a “Double Carbon” Background. Sustainability. 2023; 15(3):2203. https://doi.org/10.3390/su15032203

Chicago/Turabian StyleZeng, Shaolong, Qinyi Fu, Danni Yang, Yihua Tian, and Yang Yu. 2023. "The Influencing Factors of the Carbon Trading Price: A Case of China against a “Double Carbon” Background" Sustainability 15, no. 3: 2203. https://doi.org/10.3390/su15032203