1. Introduction

During the past decades, the world economy has witnessed a series of crises. One notable instance is the onset of the global financial crisis in 2008, which triggered a synchronized deceleration in economic activity across the globe. Moreover, the outbreak of the COVID-19 epidemic at the end of 2019 intensified the vulnerability of a global economic downswing, bringing a high degree of uncertainty and a huge devastating impact on global economic development. It was even declared by the World Health Organization as a global health disaster.

To withstand external shocks and cope with economic recessions, governments worldwide have implemented a series of fiscal and monetary measures. For instance, the Chinese government executed a “four trillion” fiscal stimulus strategy, complemented by credit expansion [

1]. Responding to the central government’s directive, local governments at various tiers implemented a high-density investment approach accompanied by elevated debt levels, leading to a sharp increase in the number of local government financing platforms (LGFPs) and an unanticipated expansion of local debt magnitude. These massive and diverse forms of local government debt served as a safeguard for public investment during China’s rapid economic growth phase, emerging as a pivotal driving force behind the “growth miracle” of the Chinese economy. However, concurrently, the risks associated with these debts have accumulated. They transmit to the real economy through complex financial channels, which has a serious impact on the stability of the external business environment of enterprises and has become a major hidden danger hindering the development of China’s economy [

2,

3].

Up to this point, a significant amount of literature has been dedicated to the expansion of government debt. However, the majority of these analyses have been conducted at the macro level [

4,

5]. For instance, the investigation by Mao et al. (2023) [

6] reveals that the competitive economic growth objectives set by local governments serve as an endogenous root cause for the surge in urban debt in China. In addition, Cai and Song (2022) [

7] confirm that the role of China’s local government debt in fostering regional economic growth is notably significant. Moreover, this promotion exhibits a substantial spatial spillover effect, with the central region experiencing the most pronounced impact on economic growth, followed by the eastern region, while the western region remains largely unaffected. Interestingly, similar outcomes are also reported by Yang et al. (2022) [

8]. Furthermore, as revealed by Tang (2022) [

9], the debt levels of local governments in China have exceeded a reasonable threshold, and the expansion of debt has demonstrated a pronounced crowding-out effect on the real economy. While these macro-level studies offer a comprehensive depiction of overarching trends, they may not fully elucidate the intricacies that distinguish individual firms [

10].

To the best of our knowledge, there has been limited research conducted at the micro level concerning government debt, with a predominant focus on its implications for corporate innovation and pollution. For example, as illustrated by Fan et al. (2022) [

11], government debt escalation elevates the cost of capital for firms, thereby constraining their capacity to engage in research and development (R&D) initiatives. Notably, firms with financial constraints are more vulnerable to the adverse effects of government debt expansion. Similar findings are reported by Chen et al. (2022) [

12]. Their research indicates that the escalation of local debt levels not only weakens firms’ capabilities for green innovation but also generates larger financial risks. In addition, Zhou et al. (2023) [

13] observed that the proliferation of local government debt amplifies the financing constraints faced by firms. This, in turn, accentuates the level of pollution attributable to firms, particularly those located in areas characterized by weaker financial resilience and lower governance quality. Moreover, Xie et al. (2023) [

14] confirmed a substantial positive correlation between local government debt and the pollution emissions of firms. They further ascertain that this is realized through the means of increased investments in fixed assets and a reduction in firms’ R&D expenditures.

As is well known, enterprises serve as the fundamental constituents of the real economy, and the structure of their investments constitutes a crucial factor for the healthy development of enterprises, especially when faced with a highly turbulent external market environment and challenging conditions of deteriorating external financing. The significance of investment decision-making is particularly underscored in such circumstances [

15,

16]. It is worth noting that although a limited number of scholars have explored the ramifications of government debt on firms from an investment perspective, their investigations have primarily delved into the specific investment practices of firms [

17], with less emphasis on the structural aspects of investment. However, emerging markets typically exhibit institutional imperfections and regulatory gaps compared to developed markets, which may incentivize non-financial firms to pursue speculative financial investments over long-term productive investments [

18]. In particular, the trend of economic virtualization has emerged in China at this stage. Many non-financial enterprises have not increased their financial investments due to the liquidity of financial assets but rather as a result of pursuing short-term benefits without due consideration, exacerbating the operational risks faced by these firms [

19]. Therefore, it is crucial to delve deeply into the micro-level analysis to ascertain whether the investment decisions of non-financial firms are influenced by the expansion of government debt, and if so, what form of bias may arise in their investment patterns. These studies hold significant relevance, particularly in the context of the ongoing deceleration in China’s real economy and the growing trend of aggressive financialization among non-financial firms. They also carry important implications for policymakers and corporate management.

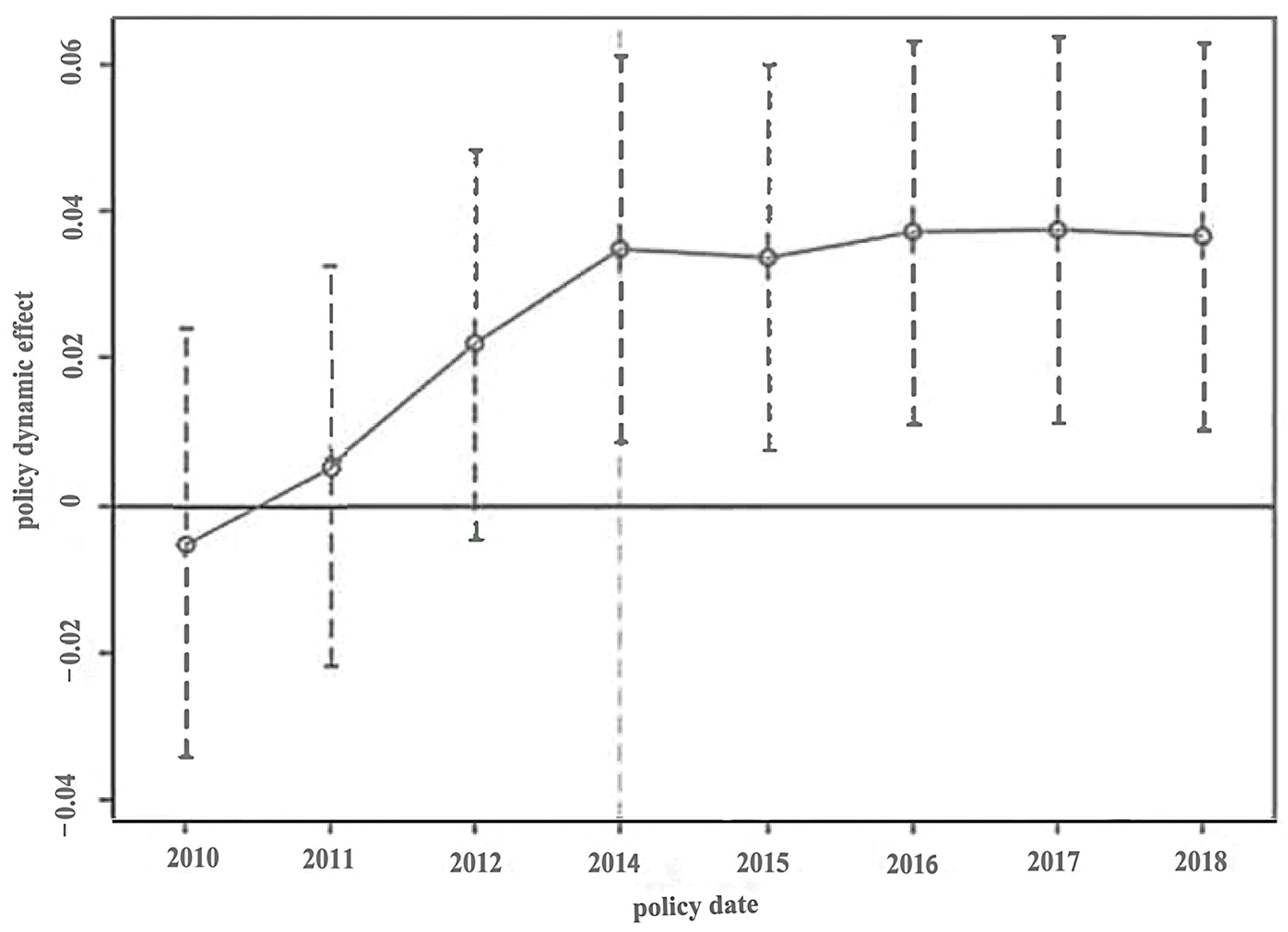

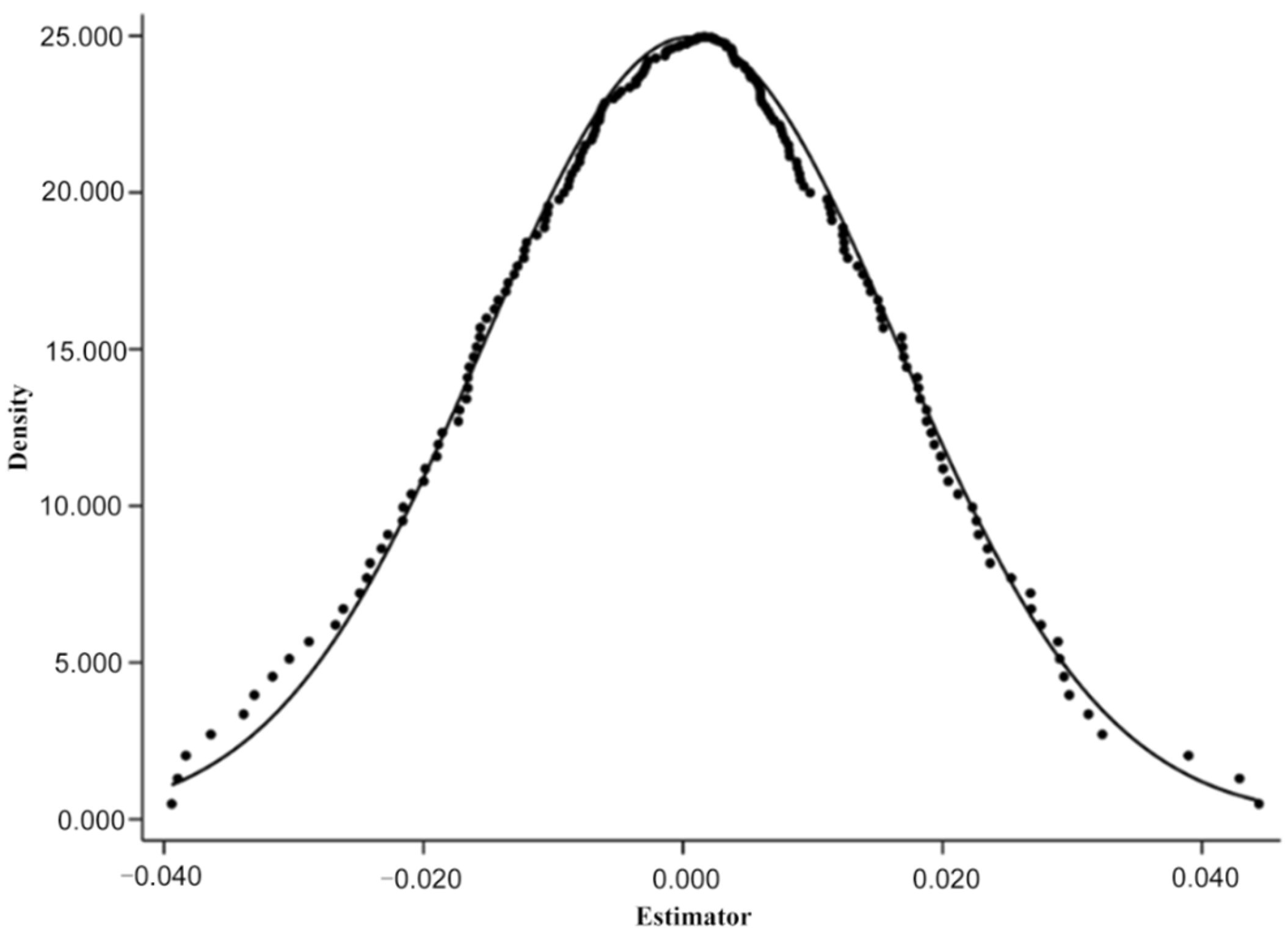

This study investigates the impact of LGD on the investment arrangement of non-financial corporations in China. We employed a two-way fixed effects model to identify the causal relationship between LGD and the investment structure of non-financial firms. Additionally, to alleviate endogeneity, we utilized a double difference model for quasi-natural experiments. The results indicate that the expansion of LGD exacerbates the inclination of non-financial firms toward financialization. Importantly, we observed that effectively managing the magnitude of local debt results in non-financial firms decreasing their financial investment and increasing their bias towards real investment. Moreover, we find this result to be robust through various robustness tests, such as parallel trend tests, modified model settings, the substitution of explanatory variables, and placebo tests. Notably, our further analysis demonstrates that the increase in LGD leads to a bias in the investment structure of non-SOEs and highly constrained financing firms towards financial investment, while SOEs and low-constrained financing firms are not affected.

This paper’s main findings are summarized below. First, although a large number of studies have examined the impact of LGD from the macro level, we analyze the impact of LGD on the investment structure of enterprises from the micro level, which enriches and expands the study of the microeconomic effects of LGD governance. This study is particularly timely, given China’s accelerating pace of capital market opening. Additionally, the “over-financialization” of non-financial enterprises has led to the “exit from real to virtual” investment structure. As such, this paper offers valuable insights to policymakers to clarify the impact of LGD governance on correcting the bias of corporate investment structures. Second, while some literature has explored the “crowding out” [

20,

21,

22] and “crowding in” [

1,

23] effects of LGD on corporate investment, there is no consensus on this issue [

24]. More importantly, financial investment, another important component of corporate investment structures, has not been explored thoroughly. To address this gap in the literature, this paper aims to construct a first-order differential index of investment that considers both the real investments and financial investments of non-financial enterprises, which not only can better identify the influence of LGD on the bias of corporate investment structures but also incorporates financial investment into the research framework of this paper. In addition, to guarantee the strength and dependability of the outcomes, this paper employs a difference–in-differences model to mitigate the endogeneity problem.

It is essential to maintain logical connections between these sections. The paper is structured as follows: firstly,

Section 2 provides an overview of the policy context of the study. Following this,

Section 3 introduces the theoretical analysis and research hypotheses. In

Section 4, our data and empirical strategy are presented.

Section 5 reports and discusses the empirical results, and the final section,

Section 6, focuses on the research mechanism and heterogeneity. The last part concludes our work with a discussion of its implications.

2. Background

Following the implementation of the tax-sharing reform in 1994, local governments in China have been faced with a significant challenge concerning the misalignment between their duty, expenditure responsibilities, and available financial resources [

2]. Consequently, there is often a substantial funding gap in the process of economic construction, particularly in the realm of infrastructure construction. This predicament, characterized by an “upward concentration of financial resources” and a “downward concentration of duty”, has compelled local governments to resort to borrowing from formal and informal channels [

25], either directly or indirectly. In response to the challenge of insufficient funds in the face of rapid economic development, they have commonly established financing platforms to issue debt financing and obtain mortgage loans from banks.

Local government financing platforms are usually financial institutions or investment and construction companies funded or controlled by local governments. The main objective of these platforms is to raise funds for local governments to support local infrastructure construction and project financing needs. These financing platforms are typically established under the direct control of the local government, with the platform’s leadership appointed and directly led by the local government. Furthermore, these platforms benefit from guarantees or implicit guarantee commitments provided by the local government to facilitate their financing activities [

26]. More importantly, local government financing platforms will directly participate in local infrastructure investment and contribute to overall economic construction.

However, with the dramatic expansion of the LGD scale of financing platforms, some local government debt risks are increasingly accumulating, which reduces the quality of economic growth and may even induce a widespread financial crisis. In light of these concerns, the central government has shifted its policy orientation towards local government financing platforms from encouragement to a more stringent approach aimed at tightening control. This change in direction is driven by the goal of strengthening local government debt management and promoting the sustainable and healthy development of the national economy. In 2014, the State Council promulgated “Document No. 43”, known as the “Opinions of the State Council on Strengthening the Management of LGD”, which explicitly prohibits local governments from providing guarantees for financing platform companies. Instead, it advocates for measures such as the replacement of local government bonds and the regulation of urban investment bonds to address the potential risks associated with local government debts [

27]. The implementation of this document signifies a gradual control and management of the extensively expanded local government debt, ultimately aiming to establish a sustainable local debt model by effectively controlling the scale of LGD.

7. Conclusions

In recent years, the rapid expansion of LGD in China has been a notable trend. However, the associated risks and potential economic ramifications stemming from this phenomenon have yet to receive comprehensive recognition [

58,

59]. The surge in local government debt has further exacerbated an existing imbalance between China’s financial sector and the trajectory of real economic development. Particularly, the observed shift towards an “exit from real to virtual” within the real economy’s developmental trajectory has become a significant concern. This phenomenon is discernible at both the macro and micro levels. On a macroscopic scale, there is a noticeable decline in the efficacy of financial services in catering to tangible economic activities. This is coupled with a concerning occurrence of funds becoming dormant within the financial system [

60]. At the micro level, enterprises are increasingly diverting their funds away from real investments, instead channeling substantial amounts into financial products. This transition of investment of firms from tangible to intangible activities severely hampers the advancement of the real economy. This development has elicited considerable attention from both governmental bodies and the academic community. In the current economic climate, particularly within the context of the post-pandemic era and the ongoing economic downturn, comprehending the underlying drivers behind this financialization of enterprises assumes heightened significance.

Consequently, it becomes imperative to explore strategies for controlling the burgeoning scale of LGD, guiding the rechanneling of funds into tangible economic sectors and thereby fostering the steady and sustainable growth of the real economy. Addressing these issues becomes a pivotal step in navigating the economic challenges ahead and establishing a more balanced and resilient economic trajectory. In view of this, we propose some recommendations for the effective management of local government debt in China.

Firstly, it is advisable to optimize the debt financing structure of local governments and rigorously enforce debt management practices. Drawing from the regression results in this paper, it is evident that local debt governance can improve the corporate investment structure. Therefore, local governments should comprehensively consider the influence of debt financing on corporate investment structures and actively promote the optimization of debt financing structures. This can be achieved through the adoption of innovative financing instruments, such as infrastructure funds and equity financing, thereby mitigating the adverse effects suffered by firms as a result of the conventional debt financing approach employed by local governments. Simultaneously, it is imperative for local governments to bolster their debt management protocols to guarantee the rational allocation and repayment of debt. Furthermore, establishing a robust risk-monitoring mechanism is essential for identifying potential debt risks, thereby preventing the debt from becoming an onerous burden on firms. This approach ultimately safeguards the stability of corporate investment structures.

Secondly, it is imperative to foster the growth of non-state-owned firms. The regression results indicate variations in the influence of local government debt on firms based on their ownership properties, necessitating the implementation of tailored support policies. Compared with state-owned firms, non-state-owned firms often encounter competitive disadvantages in the marketplace. Therefore, for non-state-owned firms, the government may contemplate initiatives such as tax incentives, reducing financing entry barriers, and extending loan guarantees to help these firms overcome the distress caused by local government debt financing. Such actions would contribute to optimizing corporate investment structures and fostering the sustainable development of non-state-owned firms, thereby promoting shared prosperity.

Lastly, it is imperative to advocate for the development of financial markets and the introduction of innovative financing mechanisms. The government should proactively undertake initiatives to promote the development and innovation of financial markets, while also ensuring firms have access to a diverse array of financing avenues. In particular, the government can incentivize financial institutions to introduce novel financing instruments, such as supply chain finance and microfinance, to meet the financing requirements of diverse firms. This approach will effectively enhance the financing capabilities of firms, fortify their production and market competitiveness, and mitigate the potential adverse effects of local government debt.

There are some limitations to this study. First and foremost, it is worth noting that an appropriate level of government debt can promote economic development, while excessive government debt will accumulate a large amount of debt risk, leading to a shift in corporate investment structures towards financial investment. Hence, the pursuit of an optimal debt balance point is a noteworthy avenue for future exploration. Secondly, we used the data of the listed companies to investigate the influence of local government debt on the firms’ investment structures. Extending the applicability of these findings to non-listed companies represents an area for further in-depth examination. Thirdly, it is important to acknowledge that this study primarily approached the subject from the perspective of non-financial firms and did not consider the impact of local government debt on financial institutions. As such, future research could be directed toward investigating the impact of local government debt on financial institutions.

{kind=link}

{kind=link}