1. Introduction

The achievement of the 17 Sustainable Development Goals (SDGs) requires the creation and offering of financial products that are aligned with sustainability issues [

1]. These primarily encompass environmental, social, and governance (ESG) concerns. In order to make this possible, financial eco-innovations play a pivotal role [

2]. Consequently, various financial mechanisms have been designed to diversify the portfolio of sustainable products [

3]. Among these mechanisms, debt-based products, particularly fixed-income bonds, have played a crucial role in the design of financial instruments focused on ESG concerns [

2]. In the realm of ESG, the social aspect has garnered significant interest, with its development being further driven by the COVID-19 pandemic [

4].

As one of the leading sustainable financial innovations boosted in recent years, social bonds play a pivotal role in facilitating access to capital for projects that contribute to socioeconomic advancement, affordable housing and infrastructure, access to essential services, employment generation, and food security [

5]. Moreover, social bonds display an exceptional opportunity to address gender equity challenges by directly financing critical issues affecting women, such as clean water, social housing, gender equality, and access to education and facilities, as well as supporting the operation and growth of women-led businesses, among others [

6].

Related to sustainable financial mechanisms, on the environmental side, green bonds were developed with the main purpose of financing or refinancing projects with positive environmental impact [

7]. Likewise, the green loan is an innovation designed for enterprises, banks, and governments in order to boost cleaner and greener production [

8,

9,

10] as well as for financing green projects [

11]. On the other hand, from a social perspective, social bonds are exclusively applied to finance or re-finance projects with a social focus [

12].

At this point, it is important to note that, from a market perspective, social bonds and impact bonds are not the same. While the former are financial mechanisms of fixed income, the latter are not bonds, in the traditional sense, given that they do not offer a fixed rate of return. Instead, these offer a pay-for-success, also called payment-by-results, whereby the cash flows depend on achieving specific predefined social objectives. Hence, in the worst scenario, investors may not recover 100% of the capital invested, while in social bonds, investment recovery is not dependent upon achievement [

13,

14].

It is worth mentioning that, in order to provide guidelines to all market players, particularly issuers and investors, the International Capital Market Association (ICMA) developed the Social Bond Principles (SBP), which are voluntary guidelines that issuers should follow for issuing this financial mechanism [

12]. The SBP seeks to support issuers in financing socially sound projects that achieve greater benefits [

15]. As a consequence, issuances of this financial mechanism have mainly been driven by the COVID-19 pandemic worldwide. Furthermore, social bonds could help understand how capital asset allocation can contribute to sustainable development [

16]. Thus, this financial mechanism changes the relationship between issuers and investors focusing on accelerating organizational change to advance social impact with financial return [

6].

Additionally, with a broader application and considering that there is often a need to finance projects with environmental and social impacts, proceeds of sustainability bonds and sustainability-linked bonds could be used for financing projects with mixed impact, i.e., social and environmental [

17,

18,

19,

20]. In this way, both social, green, sustainability-linked bonds, and sustainable bonds allow issuers to diversify financial sources and investors to combine economic return with social and environmental benefits. For the social bonds case, there is a strong connection between SDGs and ESG concerns, which can directly be observed in SDGs 1 (no poverty), 2 (zero hunger), 3 (good health and well being), 4 (quality education), 5 (gender equality), 6 (clean water and sanitation), 8 (decent work), 10 (reduced inequalities), 12 (responsible consumption), and 16 (peace and justice). Thus, sustainable finance’s increased financial resources suggest innovative ways to address social issues like gender inequality. In this scenario, investors include social bonds in the investment portfolio design to reduce the gender gap, i.e., inequalities that persist between women and men [

6].

In 2008, when there was an extremely challenging and volatile market environment and financial markets were entering a crisis, the International Finance Corporation (IFC) issued one of the first social bonds of USD 1 billion. The proceeds exclusively financed eligible projects selected from IFC’s global investment portfolio, including those that address the socioeconomic consequences [

5]. This issuance attracted several investors worldwide that exceeded the order book by 3.4x. It marked the largest bond issued under the IFC’s Social Bond Program [

5].

In the specific case of gender social bonds, they are a subset of social bonds that help to address gender issues. Thus, they are fixed-income securities allocated for new or existing projects that support women’s advancement, empowerment, and equality [

21]. With this purpose, capital markets play a pivotal role in leading gender equality. From the issuers’ perspective, these offer an opportunity to prove leadership in forward-moving gender equality [

6]. In this way, UN Women and the Luxembourg Stock Exchange joined forces in order to encourage greater capital allocations toward tackling the economic and social inequalities that continue between women and men across the globe by means of gender social bonds [

22]. However, capital flows are insufficient to close the gap between women and men. Indeed, this issue continues after the COVID-19 pandemic [

23]. Considering a specific context, issuances of sustainable financial mechanisms have been growing in the Latin American (Latam) market.

However, a few studies have been conducted to analyze how this market has evolved. For example, ref. [

24] analyzed the development of the green bonds market for Latam. Among the main findings, this study found that USD 26 billion has been issued from 2014 to 2021. Brazil, Chile, and Mexico are the most active countries, and the main sectors are sovereign, renewable energy, and development banks. During this same period, the study conducted by ref. [

25] on green bonds for the renewable energy sector, USD 9.9 billion have been issued, particularly in transmission and distribution, wind, solar, and bioenergy subsectors.

Likewise, Brazil, Mexico, and Peru are the leading countries. Ref. [

26] analyzed the incentives and barriers to expanding the green bonds market in Latam. The main findings are based on economic benefits, pricing, external review, reporting, and asset selection.

On the other hand, sustainability bonds, which are becoming more relevant in the Latam markets [

18], have been issued USD 9.7 billion by June 2021 [

27]. In addition, ref. [

28] found that the economic growth of the countries in the Latam region that are issuing green, social, and sustainability bonds is significantly related to the sovereign green issuance, the ratio of Private Credit/GDP, and the Rule of Law Index.

As can be observed from different viewpoints, both professional and academic, relevant studies on sustainable financial mechanisms have been conducted. However, regardless of all the advances that have been made, we identified a knowledge gap in the study of the evolution and development of the social bonds market from a gender perspective, particularly in the Latam region, which plays a pivotal role in the social scene worldwide.

To the best of our knowledge, no study in the current literature has provided an in-depth analysis of the characteristics of this financial mechanism. Particularly, there has been no analysis of characteristics and determinants that help to promote successful gender social bonds initiatives, which face higher capital constraints for raising financial resources, particularly in the Latam region. To help bridge the identified knowledge gap, this study aims at examining the overall state of the gender social bonds in the Latam market in order to contribute to a better understanding of how this financial mechanism could help to boost the social development of the region. In this way, it is the first study carried out on gender social bonds worldwide.

This paper contributes to the previous research in the following ways. First, an in-depth scientometric analysis is carried out in order to have a better understanding of social bonds. This analysis allows us to have a better understanding of the knowledge frontier in sustainable financial mechanisms, particularly social bonds. Likewise, research areas, trending topics, and evolution in this arena are examined. Second, we provide insight into the role of the social bonds market in Latam. In this way, to better understand gender social bonds, the most representative issuances in terms of volume issued are examined. Also, analyses at the country level and the type of issuers are carried out. This analysis allows key market players to have a more comprehensive knowledge of how issuers have used proceeds. Third, it also adds to the literature by discussing and analyzing the advantages of social bonds in the context of sustainable finance. Therefore, this study provides significant new evidence and further insights into this novel financial mechanism.

The results are valuable for policy makers in the design of public social policies. Hence, it suggests that decision makers on designing strategies for promoting social-friendly policies that contribute to issuing more gender social bonds in the capital markets. In addition, the study presents the potential for further research in both qualitative and quantitative approaches.

This paper is organized as follows. After this introduction,

Section 2 provides the theoretical background on social bonds.

Section 3 describes the data and methods.

Section 4 analyzes the results. Finally, in

Section 5, the conclusions, contributions, and further research are presented.

3. Literature Review

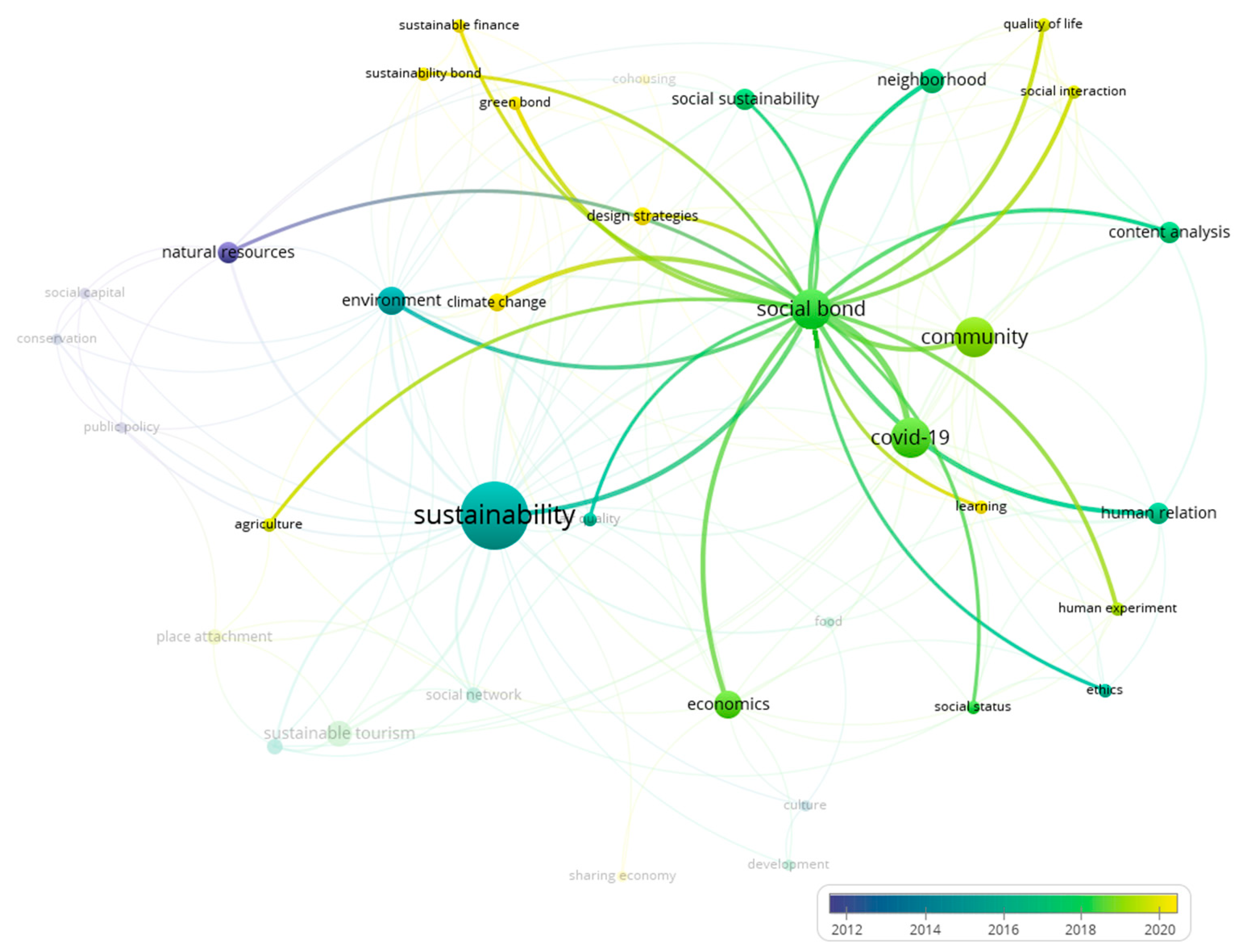

This study undertook a comprehensive and holistic scientometric review of the leading studies about social bonds. Given their stronger academic status than other academic databases, in order to conduct this study, the research papers used were obtained from Scopus and WoS. The following keywords were used in both: social bonds and sustainability. Thus, the search equation used in both databases was TITLE-ABS-KEY (“social bond*” AND sustainability). After this search, all the research papers were downloaded and indexed into Mendeley for further analysis. Scopus reported 46 studies, while Web of Science 44 mostly are in Scopus. Almost these studies have been published as articles, book chapters, and conference papers in open access. Given that a few studies have been conducted on this topic, Google Scholar was also used. This finding makes a suitable signal of the relevance of this research topic.

Based on the results obtained from Scopus, we selected keywords as a criterion to evaluate relevance. Specifically, we include only those with two or more keywords co-occurrences. Thus,

Figure 1 depicts in a network the most relevant keywords obtained after refining the search. It allows observing a diversity of terms among which, at least directly, it is possible to observe sustainable finance and social concerns as the most important topics studied in the social bonds arena. In this context, two well-defined research development trends are identified in the scientific literature.

This first and one of the most important branches of the literature seeks to explain why sustainable financial mechanisms play a crucial role in reaching the SDGs. Based on this issue, [

34] found that capital markets in Asian economies need to make a transition to tap by growing interest in sustainable investing among investors worldwide. Therefore, sustainable financial mechanisms should have market conditions that allow for attracting investors, namely, information availability, unblocking regulatory obstacles, and reducing distortions. According to ref. [

35], proceeds of social, green, and sustainability bonds allow issuers to finance projects, assets, or businesses that include environmental, social, or economic outcomes. It confirms the relevance of sustainable financial mechanisms, particularly social bonds, for reaching the SDGs. Comparing the green bonds with the social bonds market, the latter is growing, mainly driven by the COVID-19 pandemic outbreak. These have become of increasing interest to investors looking to achieve both positive social outcomes and financial returns [

5].

According to ref. [

36], the total market cumulative for social bonds by 31 December 2022, was USD 653.6 billion, in which 772 issuers, 49 countries, and 42 currencies participated. Regarding social premium, which is defined as the yield differential between social bonds and otherwise identical conventional bonds (vanilla bonds) [

37], ref. [

38] found that a sample of social bonds showed at least 8bp in South Korea. However, it decreased significantly after the outbreak of COVID-19. This trend is also characterized by encouraging gender equity challenges, mainly by providing direct financing for critical issues such as the operation and expansion of women-led businesses and closing gaps in access to clean water and education [

6]. On the other side, ref. [

37] found that, in a sample of 64 social bonds aligned with the ICMA, a social premium is significantly explained by differences in liquidity and volatility, which are, respectively, negatively and positively correlated with the yield differential. Also, the analysis of the fixed effects proves the existence of a significant and positive premium of 1.242 bps. However, they argued that social premium deserves further research as the market becomes more developed. In this way, social bonds offer a great opportunity to tackle social concerns.

Connecting with the first, the second research development trend focuses on social concerns. For example, ref. [

39] highlighted the benefits and characteristics of social bonds in affordable housing, education, food security, access to healthcare, and gender inequality. Also, based on social bonds, this study proposed a framework for evaluating human rights factors in impact investing. For this purpose, it suggested reforms to the social bonds market in order to increase investor assessment, external assurance, and impact-maximizing leverage.

On the other hand, ref. [

40] examined the real-world application of social bonds in the real estate sector in Sweden. This study’s findings revealed notable variations in the criteria, motivations, and practices related to social bonds among different market participants, with pronounced differences observed between investors and issuers.

Furthermore, the study highlights that a standardized framework for social bonds is currently underdeveloped, and the social bond market is still in its nascent stages, with anticipated changes in policies and standards in the coming years.

On the other hand, considering an educational perspective, ref. [

41] argued that financing the higher education sector is lacking and requires new financial mechanisms as well as financing models. In this way, the study proposed three innovative approaches for issuing social bonds in this sector. First, it assumes that a bank or other financial institution issues on behalf of a university. The second approach involves a university issuing social bonds in partnership with the state. The third approach entails creating a platform to finance long-term educational programs, potentially with the involvement of a prominent company that implements large-scale socioeconomic projects. This platform is expected to have a significant social and economic impact, aligning with promoting a just transition. Also, this trend is characterized by encouraging the just transition. This concept is based on the idea that a green economy cannot be achieved without addressing the social risks faced by communities.

Although the transition to a net-zero economy is anticipated to yield numerous economic benefits, such as the creation of roughly 18 million new green jobs on a global scale, it is also expected to result in approximately six million job losses within the coal and petroleum industries by 2030 [

42]. Although just transition has mainly been on energy transitions, other areas have recently gained increasing attention, such as food systems, bioeconomy, employment, and gender inequalities [

43,

44]. For example, ref. [

35] proposed that the just transition concept could involve subsidizing polluting companies to invest in cleaner technologies or funding retraining programs to support displaced workers as polluting industries are phased out.

As can be observed, these studies highlight the relevance of social bonds in the sustainability market. Hence, the present study aimed to fill the knowledge gap by examining the overall state of the gender social bonds market in the Latam market.

4. Results

This section provides a comprehensive analysis of the main characteristics of the gender social bonds market in Latam, including the most significant issuances regarding the amount issued and main characteristics. All calculations are based on the current dollar value according to transactions for each year. As mentioned above, the dataset is mainly gathered from Refinitiv Thomson Reuters Eikon and Bloomberg, which comprised observations of issuances, including the information on issuers, amount, number of deals, type of issuers, currency, use of the proceeds, maturity, among other. Also, issuers were classified into different categories, namely, financial corporations, development banks, or supranational banks.

Table 1 shows the main elements of the gender social bonds market in Latam.

4.1. Country Summary

As shown in

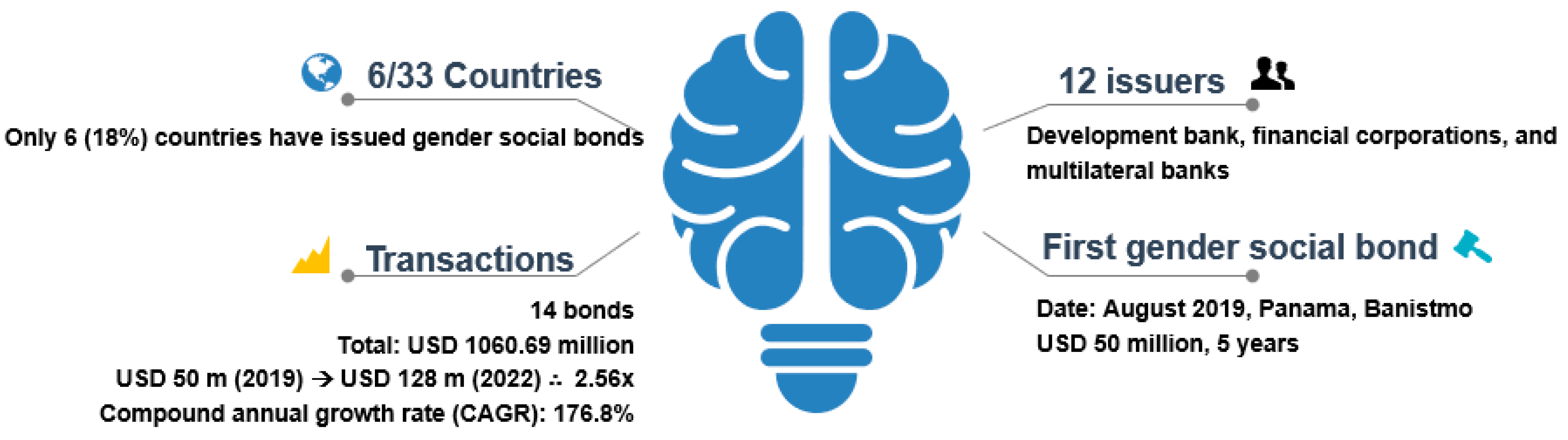

Table 1, the analysis of the gender social bonds market in Latam discloses that this type of social bond is limited to six countries, with 14 bonds and 12 issuers, for a total cumulative of USD 1060.69 million. Mexico is the leader, accounting for 58.9% of the total amount issued. Colombia follows with 18.9%, while Ecuador ranks third with 9.4%. The remaining three countries jointly represent an average share of approximately 5%. The issuance made by the multilateral bank—Inter-American Development Bank (IDB) Invest—was assigned to Mexico because it was there that the issuance was made. Notably, all issuances featured a second-party opinion (SPO), providing enhanced clarity and transparency for market players.

Brazil is an outstanding country that has established itself as a leader in the green bonds market. However, in the social bonds market, none has a gender focus. It is expected that considering the knowledge of other countries, its capital market, and experience in issuing thematic bonds, Brazil may become a key player in this segment of gender social bonds in the medium term, especially in the financial sector in the design of financial products with a gender approach.

In order to complement

Table 1,

Figure 2 shows the main elements of the gender social bonds market in Latam. Although countries in the region have shown outstanding commitment to helping achieve the gender-related SDGs, only six countries have issued social bonds with a gender focus. Considering all the above, only 18% of Latam countries have issued gender social bonds, while in the green bonds market, this participation exceeds double, reaching 48% [

36]. This may be because the green bonds market started in 2014, five years earlier than the gender social bonds market, intending to offer solutions to climate change-related issues, while the first gender social bond was issued in 2019. This was issued by Banistmo in Panama in order to enable access to financing for small and medium-sized enterprises (SMEs) led by women.

Among the most active countries, Mexico and Colombia lead in terms of volume (77.7%), number of bonds (60%), and issuers (58%). On the other hand, although the total issued in Latam does not represent a significant portion of the total issued globally in terms of volume (less than 1%), this region is the leader in issuing social gender bonds, as confirmed [

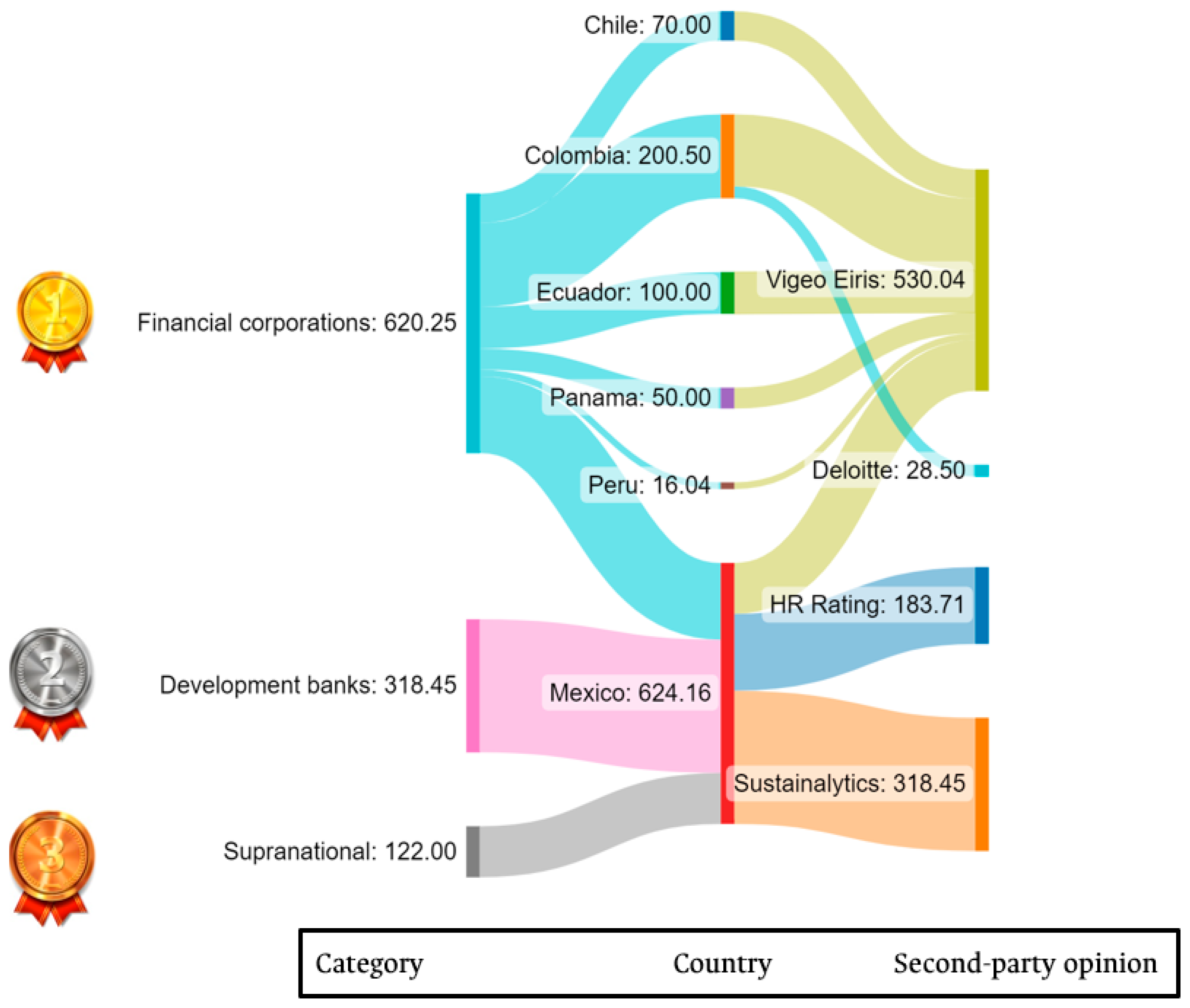

21]. To achieve this, the role of supranational banks has been fundamental, particularly IDB Invest, which supported USD 470 m allocated in eight issuances. Not only has it participated in issuing gender social bonds, but it has also played a role in structuring the issues and, on some occasions, with purchase mandates. Also, with 83% of all issuers, financial corporations have played a pivotal role in developing this type of social bond.

4.2. Market Evolution

Although the social bonds market began in 2016 with the issuance of Banco del Estado de Chile, it was not until 2019 that the first issuance of a gender social bond, which was issued by Banistmo—Panama subsidiary of Grupo Bancolombia—as shown in

Figure 2. Banistmo is the second-largest bank by loans and deposits, with a market share of about 14% [

45]. Undoubtedly, this issuance represents a milestone in the region, indicating that financial corporations can link growth strategies and market instruments with a gender-focus lens. Thus, this issuance addresses the gap identified in the lack of financial instruments for boosting women-led businesses.

In this way, with the proceeds of USD 50 million raised from the issuance, it was possible to finance 311 SMEs led by women in different sectors, such as commerce, services, and agribusiness, promoting gender equality (SDG 5), decent work and economic growth (SDG 8), industry, innovation, and infrastructure (SDG 9) [

46]. Furthermore, although the issuance had a five-year term, the loans offered had a maximum term of three years, and the refinancing of loans did not exceed 10% of the total amount issued. With this strategy, over the next five years, Banistmo expects to achieve an average annual growth of approximately 6% in the portfolio of SMEs led by women [

47].

This is one of the cases where the supranational banks, particularly IDB Invest, played a fundamental role in guiding the process of issuing this type of bond. It participated as lead manager and underwriter of the issuance. Likewise, in order to have a second-party opinion on the use of proceeds, Vigeo Eiris, a consulting firm, indicated after an evaluation process that the gender social bond is aligned with the four main components of the Social Bond Principles described by ICMA [

48].

As shown in

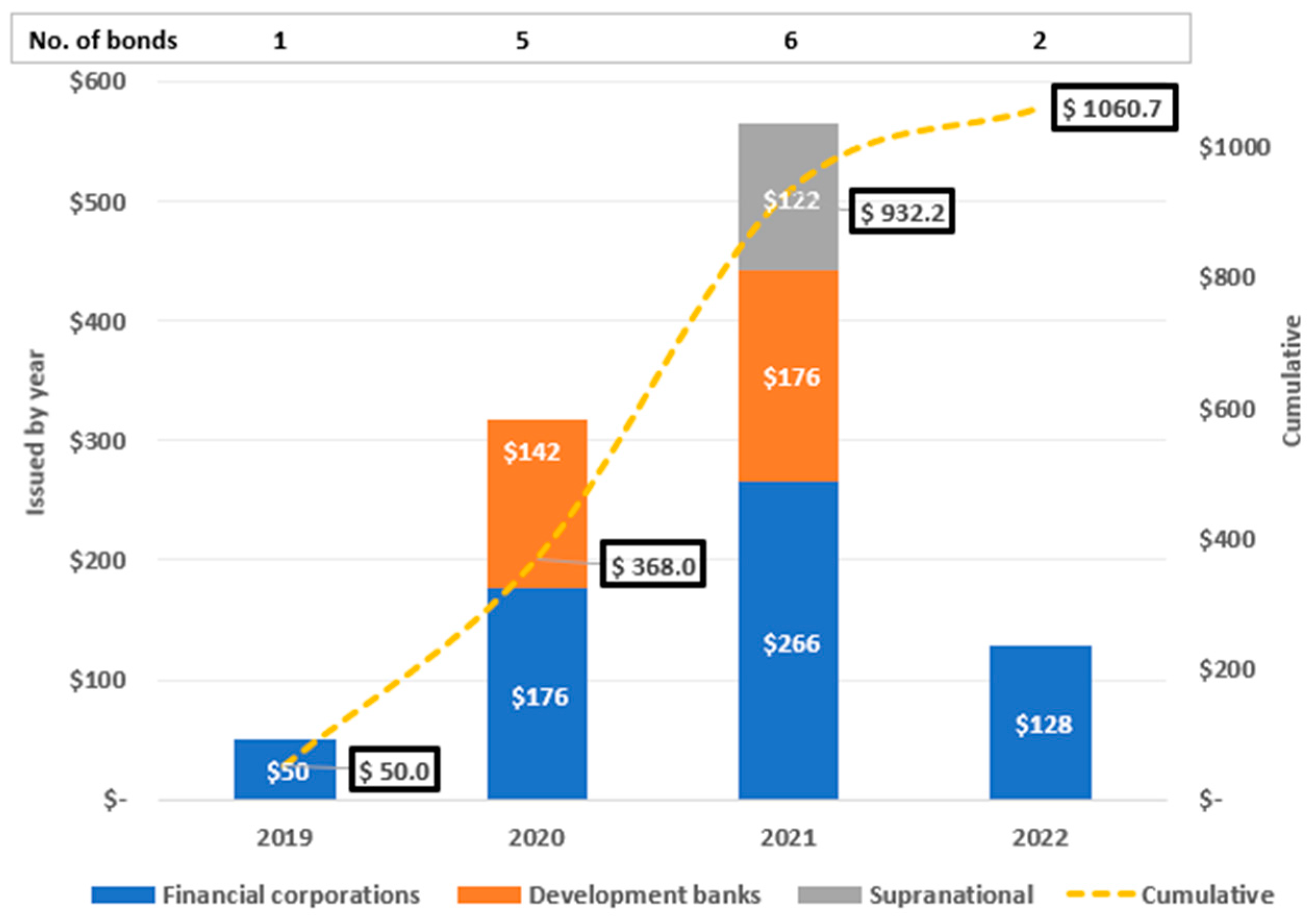

Figure 3, between 2019 and 2021, the market showed a positive trend in this financial mechanism, which had significant issuances during 2020 and 2021 due mainly to the COVID-19 pandemic. Thus, while in 2019 USD 50 million was issued, in 2020 and 2021, the market increased by 6.35x and 11.28x compared with 2020. This is also reflected in the number of issuances. It is also important to highlight the commitment of financial corporations. From 2019 to 2022, they had gender social bond issuances.

While one gender social bond was issued in 2019, five and six bonds were issued in 2020 and 2021, respectively. Thus, the pandemic caused the social bonds market to increase and both the green and sustainable bond markets to slow down from their previous pace. However, by 2022 fiscal, political, and macroeconomic uncertainty in the region limited not only the issuance of gender social bonds but also the entire fixed-income market.

4.3. Issuers Profiles

According to the data presented in

Table 1, Mexico, Colombia, and Chile, countries that lead the sustainable bonds market, especially green ones, also emerge as leaders in the gender social bonds market, with financial corporations being the primary issuers, as shown in

Figure 4. This suggests that the banking sector is actively aligning its product portfolio with sustainability factors.

Regarding development bank issuances, which rank second in the region, the initial offerings from a regional entity of this nature were carried out in Mexico. In 2020, FIRA (Trusts Established in Relation to Agriculture) issued USD 142 million and USD 176.4 million in 2021 (approx), reaching an accumulated of USD 318.4 million. The first one, which was supported by IDB, achieved a bid-to-cover ratio of 4.0x, which demonstrated great market demand for this type of bond. This significant response may have incentivized the issuer to proceed with a second issuance in the following year. Proceeds were used to finance projects led by women related to agricultural, fishing, forestry, agri-food, and rural sectors. Also, they are framed in three categories: (1) financial inclusion, (2), labor and productive initiatives, and (3) entrepreneurships [

49]. According to the annual reports published by FIRA, with proceeds raised by the first issuance, 7812 credits were delivered for 10,007 women. Regarding the second issuance, 6020 credits and 7384 women [

49,

50]. Mexico is the only country in which a development bank has issued social gender bonds.

Despite the active role of development banks in issuing social bonds, there remains a significant market gap for gender-focused social bonds. Out of the 30 issuances made between 2018 and 2022, only two had a gender focus and were issued by the same country and issuer, as previously mentioned.

This indicates a suitable opportunity for development banks to enhance their participation as key players in closing the financing gap for gender-focused initiatives. Thus, as market, political, economic, and fiscal conditions improve, development banks are expected to gain greater relevance in this space, given their extensive scope and potential impact in promoting gender equality through financing.

On the other hand, supranational entities, such as IDB Invest and IFC, have outstanding importance, not only for helping to structure the issuance but also for acting as investors or issuers, as it happens in the green and sustainability-linked bonds market [

24]. They have mainly participated in the issuances of Banistmo (Panama), the first gender bond issued in the region, Davivienda (Colombia), the first gender bond issued in Colombia, and Caja Arequipa (Peru), which is also the first issue of subordinated bonds made by an entity of this type in Peru [

51].

Regarding the supranational category, IDB Invest is the sole active entity with one bond issuance of USD 122 million in 2021. This highlights the various roles assumed by IDB Invest in fostering and expanding this market, including acting as lead manager, issuer, and investor. A scrutiny of supranational entities’ social bond issuances reveals that the most prolific entities are Corporacion Andina de Fomento (eight bonds), Banco Centroamericano de Integración Económica (five bonds), and IDB Invest (one bond). In sum, these entities have issued 14 social bonds from 2019 to 2022 representing around 8% of the total amount issued in the social bonds market in Latam. It is important to highlight that only one bond with a gender focus has been issued within the supranational category. This indicates that more measures need to be taken by these entities to address the existing gender financing gaps. Supranational entities must make significant efforts to promote gender-focused social bond issuances. This will enable them to be more impactful in advancing gender equality through financial inclusion.

On the other hand, a notable advancement in the realm of sustainable finance is the universal adoption of second-party opinions (SPOs) for gender social bond issuances in Latam, as shown in

Figure 4.

It is important to highlight that SPOs aim to validate the framework by confirming that the targets and metrics employed to measure the results are science-based, ambitious, and consistent with the Social Bonds Principles described by ICMA [

52]. The SPOs serve as an independent assurance mechanism, providing an expert evaluation of the issuer’s environmental and social objectives, as well as its alignment with international standards. As such, SPOs play a vital role in developing the gender social bonds market, enabling greater accountability, transparency, and credibility for issuers and investors alike. In this way, bonds with a lack of an SPOs process may have a higher susceptibility to washing, underscoring the importance of external validation in assessing sustainability-related credentials [

53].

The phenomenon of washing in the green bonds market is called greenwashing, which can be extrapolated to the social bonds market as socialwashing. This refers to the misrepresentation of the social impact of an investment or project, which could lead to a lack of credibility and trust in the market. Thus, the possible existence of washing in the thematic bonds market highlights the need for vigilance and caution in these emerging markets to avoid the potential risks of washing.

Similarly, SPOs can reduce information asymmetry by giving greater prominence to ESG performance and disclosure [

54]. The market highly values this process, as evidenced by a study conducted by [

53], which found that green bonds with an SPO have a lower yield spread, between six and nine basis points.

In the Latam region, the prevalence of these opinions, primarily supplied by leading firms such as Vigeo Eiris and Sustainalytics, as shown in

Figure 4, underscores the industry’s commitment to responsible investment practices. This represents a significant milestone in developing gender-focused social bonds and marks a shift towards greater integrity and responsibility in the sustainable finance arena.

4.4. Transaction Profile

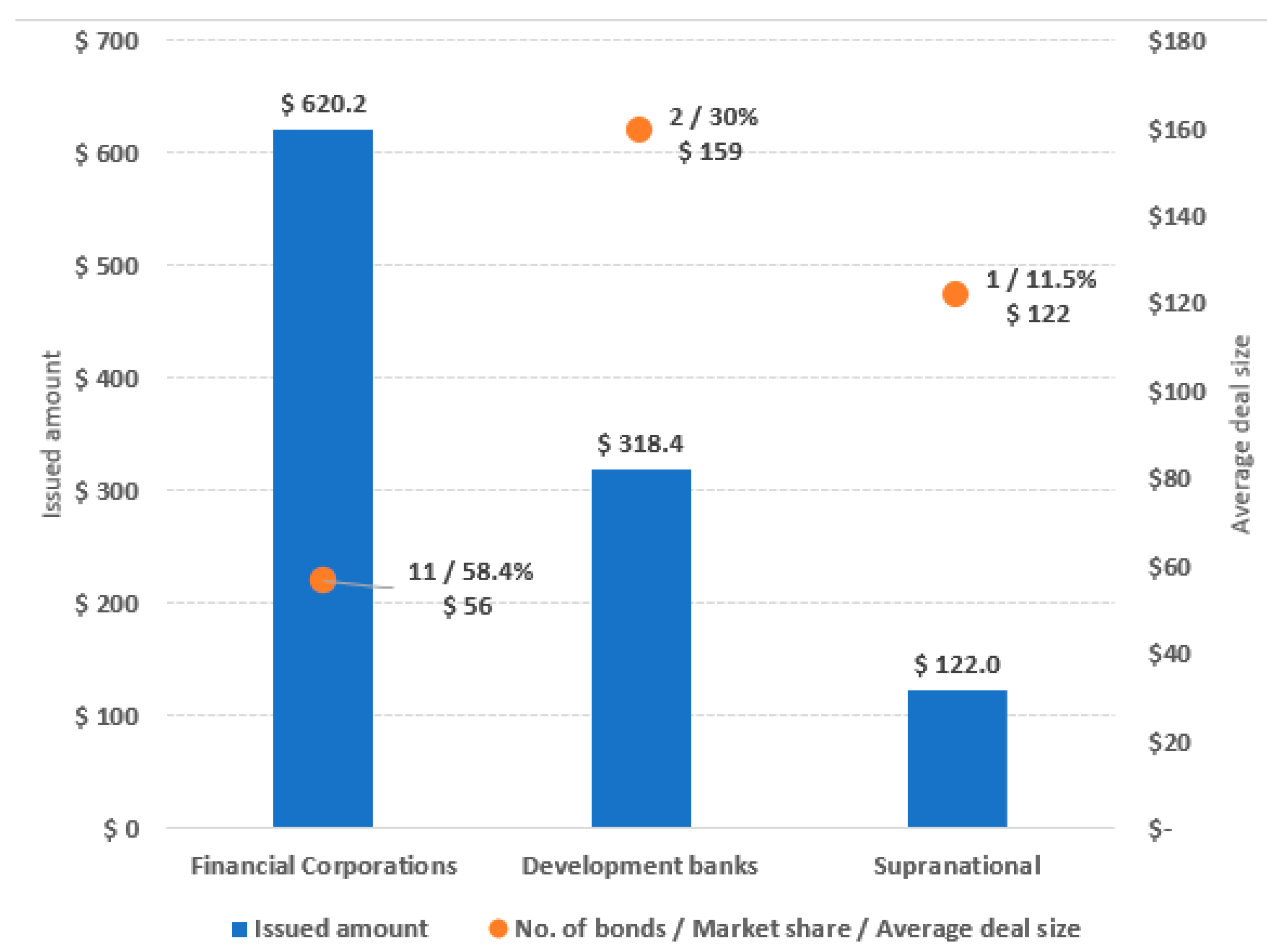

In light of the growing interest in sustainability-focused financial mechanisms, women-led businesses have made remarkable strides in recent years, particularly in the wake of the COVID-19 pandemic. As a result, financial corporations have taken the lead in developing social financial products, resulting in a significant upswing in the issuance of social gender bonds in the Latam market. To 2022, these issuances totaled USD 619.8 million across six countries and 11 issuances, accounting for a substantial market share of 58.4%, as shown in

Figure 5. The issuances are mainly concentrated in Colombia (4), Chile (2), Mexico (2), Ecuador (1), Panama (1), and Peru (1). Although Ecuador only has one issue for USD 100 million, which Banco Pichincha made, this is one of the largest by amount in the financial corporations’ category. This was subscribed in equal parts between the IDB Invest and the IFC and had an AAA credit rating by BankWatchRatings.

Colombia plays a strategic role in the gender social bonds market. This can be attributed to the strong commitment of the Colombian banking sector, led by Asobancaria, to promoting sustainable finance. Thus, a noteworthy proportion of gender social bonds issuances in Colombia has been facilitated by non-traditional financial institutions, such as BancoW, Bancamia, and Mibanco, which possess substantial market knowledge and focus on underserved communities at the base of the social and economic pyramid.

By leveraging this expertise, these entities have expanded their product offerings to populations lacking access to financial services. As a result, their contributions to the gender social bonds market have promoted greater financial inclusion.

On the other hand, Mexico stands out in the development bank category, with a total of USD 318.4 million in social bonds issuances, all of which were issued by a single entity, FIRA, one of the most prominent development banks, as mentioned above. Despite having only two issuances in 2020 and 2021, which were placed through the local debt market, FIRA’s average issuance size of USD 159 million is substantial compared to other regional issuers.

It allowed for reaching a market share of 30% in the gender social bonds market of Latam, as shown in

Figure 5. Notably, both bonds had a three-year tenor and a bid-to-cover oversubscribed upper three times, indicating strong investors’ interest.

The IDB Invest played a crucial role in the first issuance as a lead manager and contributor to the development of the reference framework, highlighting its commitment to promoting sustainable financing practices in the region. Regarding the supranational category, only one issuance has been carried out. In this case, IDB Invest went from being structured and buying to being an issuer. The issuance of USD 122 million in 2021 represented a milestone as it is the first supranational to issue a social bond with a gender focus, which directly impacts SDG 5. Additionally, it was the largest issue of this entity in the Institutional Stock Market (BIVA—Mexico) [

55]. All of the above confirms that IDB Invest has had a multipurpose role in this market.

In terms of tenors, unlike the vanilla fixed-income and most green bonds, most issuances, comprising 71% of the total amount issued, have maturities of three years or less. This segment represents 64% of the gender social bonds issued, primarily focusing on the Chilean, Mexican, and Colombian markets. This high level of participation can be attributed to the nascent nature of this market, where investors and issuers are still familiarizing themselves with the intricate dynamics and key characteristics. Consequently, carefulness prevails regarding exposure to risks associated with these issuances.

Additionally, factors such as political changes, macroeconomic complexities, elevated interest rates, and limited market incentives contribute to the preference for shorter tenors rather than longer-term commitments. Nonetheless, approximately 18% of the total amount issued features tenors ranging from three to six years, while the remaining 11% extends between six and eight years, as shown in

Table 2. Notably, Caja Arequipa (Peru) deserves attention for boasting the most extended maturity in this segment, with an eight-year gender social bond.

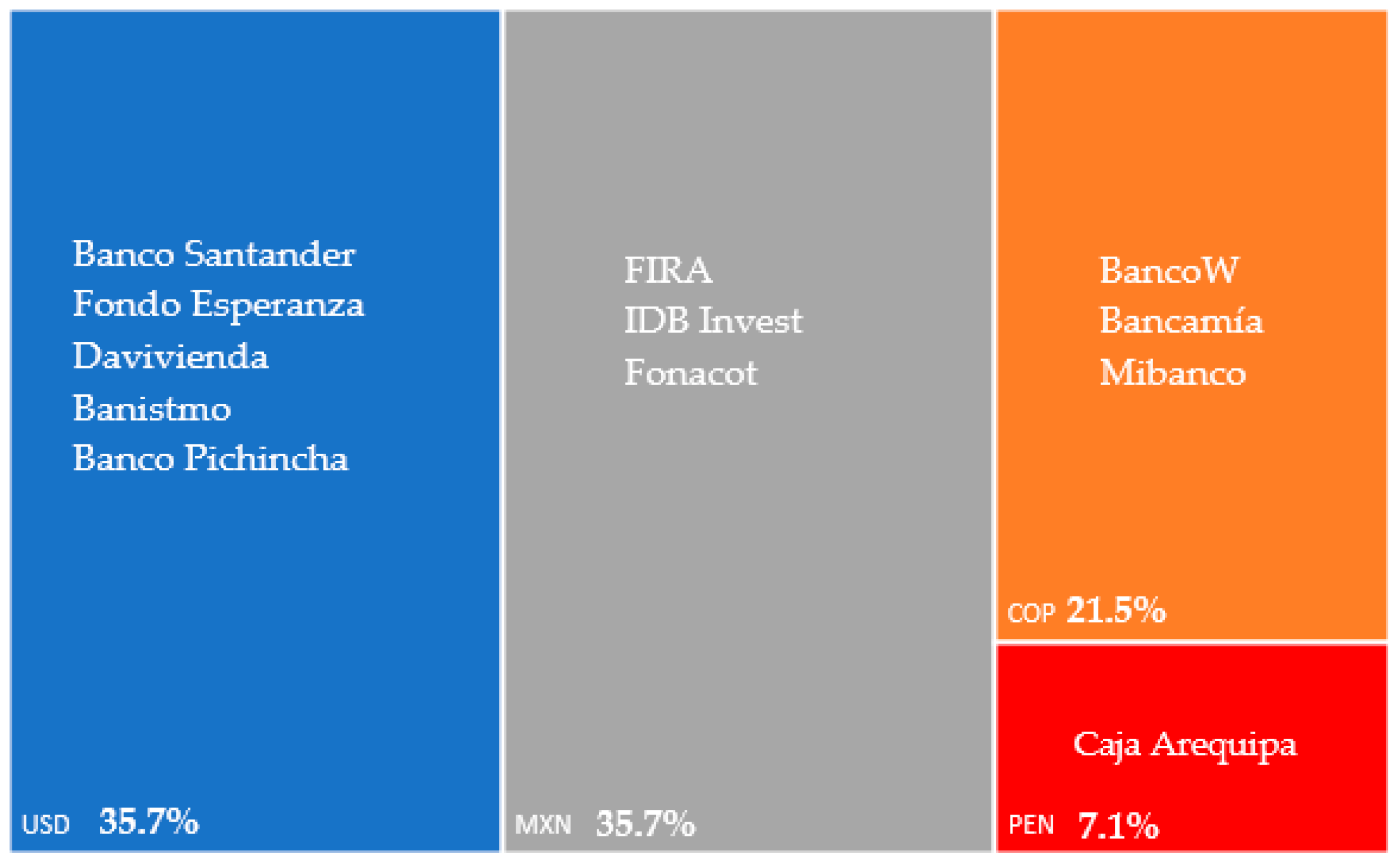

4.5. Currencies

While the gender social bond market is still developing, only three issuances have been denominated in a currency other than the local, 21.4% of the total. On one side, Banco Santander in Chile raised USD 50 million worth with a three-year tenor in 2020. Although it was issued as a sustainable bond, dedicated to refinancing or financing new loans for Chilean small and medium-sized enterprises (SMEs) led by women [

56], the bond falls under the category of a gender-focused social bond for the purpose of this research; the key market participants also endorse this categorization [

21]. Also, according to the SPO carried out by Vigeo Eiris, the issuance was aligned with the assessed elements of the Social Bond Principles [

57].

Furthermore, leveraged by its international presence, the issuance was conducted in US dollars as part of Banco Santander’s global financing strategy. This approach facilitated the participation of international investors and further solidified the bank’s leadership in ESG concerns and sustainability indices, including Dow Jones, MSCI, FTSE4Good, and S&P IPSA ESG [

56].

On the other hand, through the structuring and subscription made by IDB Invest, Davivienda successfully issued USD 100 million worth with a 7-year tenor. The primary objective of this issuance was to allow financing for SMEs led by women and facilitate the acquisition of social interest housing dedicated to women. This landmark transaction holds significant market and financial implications, both regionally and globally, as it represents the world’s pioneering issuance of a gender social bond incorporating target-linked incentives.

Notably, the issuer stands to benefit from the Women Entrepreneurs (We-Fi) program, offered by IDB Invest, which presents an opportunity to receive an annual bonus of up to US 60,000 for five years, with a potential cumulative amount of up to US 300,000. This financial incentive is contingent upon successfully expanding the SMEs Women’s loan portfolio from 20% to 27%, equivalent to approximately 6500 loans [

58]. Such strategic growth in the portfolio would signify a substantial commitment to supporting gender-inclusive lending practices and further advancing sustainable financial initiatives.

Finally, with Fundación Microfinanzas BBVA as its largest shareholder holding a 51% stake, Fondo Esperanza successfully issued USD 20 million in bonds, with a subscription of USD 10 million from the IFC. These allocated resources were explicitly intended to support a significantly vulnerable population of over 100,000 entrepreneurs, predominantly comprising women, who find themselves exposed to heightened susceptibility to the adverse effects of the pandemic.

In sum, the issuances have predominantly occurred in the US dollar (35.7%) and the Mexican peso (35.7%), followed by the Colombian peso (21.5%), and to a lesser extent, the Sol Peruvian (7.1%), as shown in

Figure 6.

5. Discussion

Gender social bonds have emerged as a powerful financial mechanism within the sustainable finance landscape, focusing on promoting gender equality and addressing the gender gap. This study analyzed the gender social bonds, a subset of social bonds, in Latam. As a market that emerged in the region in 2019, this bond has been the catalyst for different initiatives to promote, through the development of financial products, the SDGs related to equity, mainly SDG 5—gender equality, SDG 8—decent work and economic growth, SDG 9—industry, innovation, and infrastructure, and SDG 10—reduced inequalities. In this way, this research is useful for policy makers, issuers, regulators, and investors in their efforts to align the SGDs.

The issuance of this financial mechanism has reached an impressive milestone, totaling USD 1 billion. This significant figure underscores the increasing interest and commitment to addressing gender-related challenges. The market has witnessed participation from 12 issuers, who have executed 14 issuances across six countries. This involvement highlights the growing recognition of the importance of gender-focused financing initiatives. Regarding countries, Panama stands as the pioneer in issuing gender social bonds, with the first bond issued in 2019. This groundbreaking step demonstrated the country’s commitment to fostering gender equality through innovative financial instruments. By volume issued, Mexico, Colombia, and Ecuador lead the ranking of countries with the highest activity.

An important aspect to highlight, despite Brazil’s prominence in the sustainable debt market, it has yet to embrace gender social bonds. Encouraging Brazil’s active participation could significantly enhance the market’s impact and extend its reach to new horizons. As the market continues to evolve, more countries are expected to embrace gender social bonds. This growing trend reflects the broader commitment to closing the gender gap and fostering inclusive economic development. By encouraging diverse issuers to enter the market, gender social bonds can generate substantial impact and promote financial inclusion, ensuring previously underserved communities access to necessary resources.

Within this market, the financial sector has played a prominent role, accounting for 58.4% of the total volume of issuances. This demonstrates the sector’s recognition of the importance of integrating gender considerations into their financing strategies.

Additionally, given the nascent stage of the market and the ongoing learning process for investors and issuers, social gender bonds tend to have a concentration in three-year maturities. Moreover, the dominant currencies in these issuances are the USD and MXN, each representing 35.7% of the market.

On the other hand, the Bank IDB has played a vital role in elevating the relevance of the gender social bonds market. Actively engaged as a structurer, issuer, and investor, the IDB has effectively promoted the adoption of gender-focused financing across Latam. Its active involvement has increased regional significance and contributed to the global recognition of gender social bonds as essential in advancing gender equality in Latam.

6. Conclusions

This study examines the overall state of the gender social bonds in the Latam market in order to contribute to boosting the understanding of this financial mechanism. The findings of this research underline the substantial progress made in the gender social bonds market in Latam, which reached USD 1 billion, signaling its potential to drive sustainable finance and foster gender equality.

With increasing participation, active involvement by influential institutions like the IDB and the IFC, and the expansion of issuers that used proceeds for developing gender financial mechanisms, gender social bonds can create a lasting impact by closing the gender gap and promoting inclusive economic growth. As this market continues to grow, it will have a pivotal role in realizing a more equitable and sustainable future for all. Similarly, developing social taxonomies will enable investors, regulators, and issuers to gain the implications and scope of finance with a social focus. This will contribute to improved clarity and transparency, fostering informed decision making, and driving further progress in socially oriented financial initiatives.

Given the increasing interest in this bond, the current challenge of issuers and investors lies in harnessing social bonds as a financial avenue to support projects and companies with a social focus. These initiatives should not only address the socioeconomic impact resulting from health crises, gender gaps, inequalities, and other challenges but also establish social finance as a normalized and inclusive financial concept. This means embracing social finance as an integral part of the financial sector, free from any labeling.

In sum, gender social bonds serve as a dynamic catalyst for propelling gender equality and women’s empowerment endeavors, simultaneously addressing a multitude of gender-related challenges. In the pursuit of achieving the Sustainable Development Goals (SDGs), these innovative financial mechanisms play a pivotal role in channeling financial resources towards organizations that strategically advocate gender equality.

6.1. Policy Recommendations

While the global market for gender-focused social bonds keeps growing, there is still a requirement for more public policy tools and incentives to encourage the issuance of such bonds not only at large firms but also at small and medium. By implementing these measures, investors will open up broader market prospects for incorporating these socially conscious instruments into their investment portfolios. Investing with a gender focus is being incorporated mainly by private equity and index funds investors. Likewise, it will allow financial product development with a social focus. This thoughtful strategy empowers investors to mitigate risks proficiently, create portfolio diversity, and actively contribute to accomplishing gender-related goals outlined by the SDGs, particularly SGD 5. Only seven years away from the goal of reaching it [

22], gender social bonds offer a promising solution for helping achievement; for this reason, it is essential to boost this financial mechanism.

6.2. Further Research

The fast growth of issuances of sustainable financial mechanisms, mainly in the fixed-income arena, and the scarcity of related studies in the Latam region confirm social bonds as a recent field of study. This underscores the need for further research to fully explore its potential and opportunities. Conducting comprehensive studies on these topics would expand the knowledge frontier surrounding this type of bond, fostering a deeper understanding of its potential and implications. In this way, further research may include:

Analyzing key aspects of social bonds, such as social premiums and the evolution of social financing products.

Examining the dynamic correlations between social bonds and different asset classes.

Determining the impact of social bonds on COVID-19 pandemic consequences.

Analyzing the social bonds market issuances focused on education, housing, rural, employment, and health.

Examining the impact of social bonds on firm performance.

Analyzing how asset managers include gender social bonds in investment portfolios.

Finally, gender social bonds emerge as an innovative financial mechanism for fostering prosperity and raising living standards, rightfully occupying a central position within the realm of financial mechanisms. As highlighted by [

59] in the social finance context, the widening horizons of social bonds demonstrate their capability to generate not only social impact but also financial value. Consequently, placing a priority on advancing gender social bonds becomes essential from both practical and research perspectives. This emphasis can significantly contribute to addressing gender disparities, promoting social inclusivity, and driving sustainable development in the broader context of financial markets and social progress. Therefore, boosting gender social bonds, from practical and research perspectives, should be a priority for market players.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}