Are Firms More Willing to Seek Green Technology Innovation in the Context of Economic Policy Uncertainty? —Evidence from China

Abstract

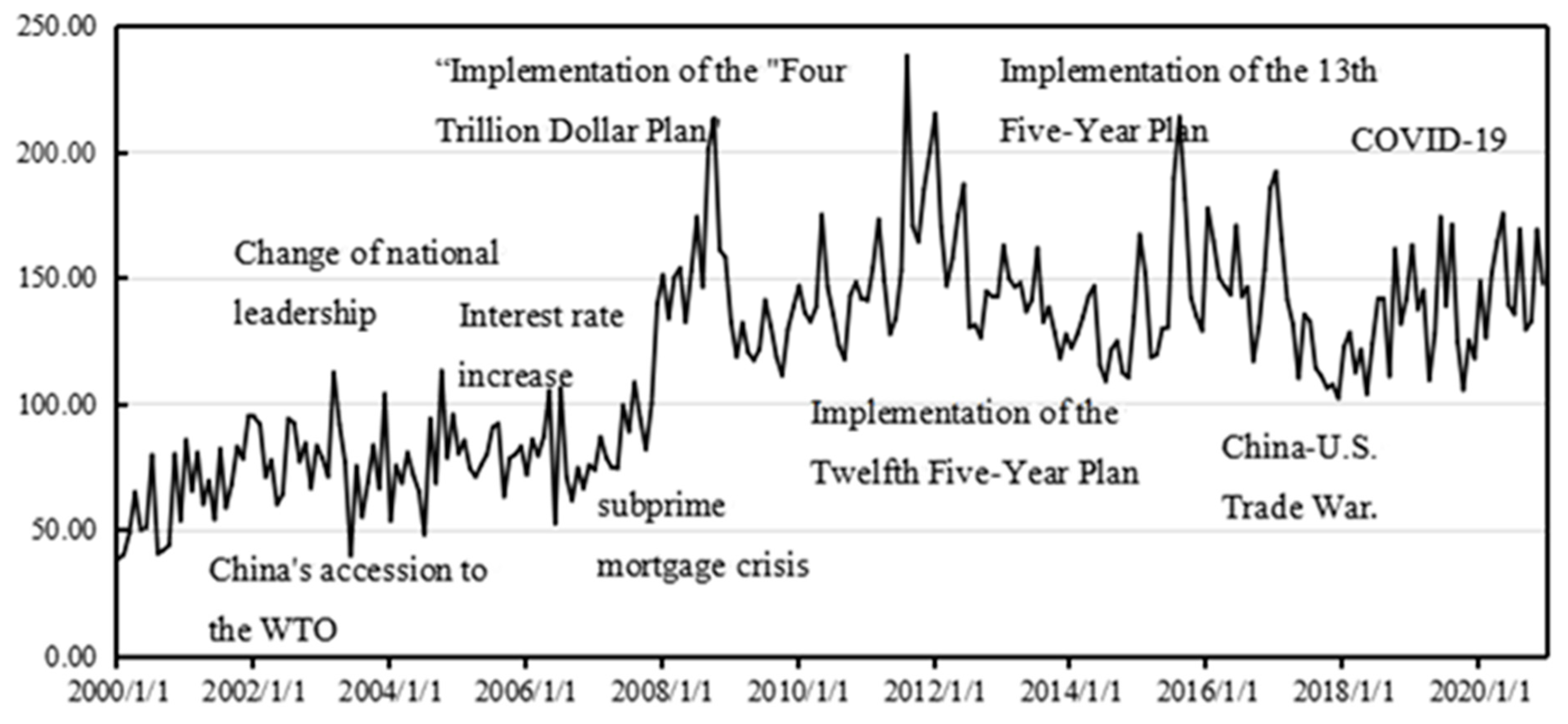

:1. Introduction

2. Theoretical Analysis and Research Hypothesis

2.1. Economic Policy Uncertainty and Corporate Green Technological Innovation

2.2. External Financing Constraint Mechanism

2.3. Management Risk Preference Mechanism

3. Research Design and Data Sources

3.1. Sample Selection, Data Processing, and Data Sources

3.2. Variable Definitions

- (1)

- Dependent variable: Enterprise green technology innovation. Since patent application indicates that the corresponding technology has reached maturity and is ready for use, this paper employs the proportion of green patents applied by enterprises in the current year to all patents applied by enterprises in the current year (IPC) as the primary measurement index of enterprises’ green technology innovation level. In order to avoid the conclusion bias caused by measurement error, the robustness test presented in this paper uses both the number of enterprise green patent applications (GreenPat_1) and the number of enterprise green patent grants (GreenPat_2) to measure the level of enterprise green technology innovation. Considering that the patent data are missing, explicitly assigning the value of 0 would result in right-biased characteristics of the data; therefore, the missing value of the original data is assigned to 0 based on adding one and logarithmic processing.

- (2)

- Explanatory variable: Economic policy uncertainty. Most existing studies use the economic policy uncertainty index calculated by Baker et al. (2016) using the South China Morning Post as the core explanatory variable [41]. Since the South China Morning Post is based in Hong Kong, and the index from a single newspaper is not sufficiently convincing, it has limitations. In contrast, the Chinese index by Huang and Luk (2020) compensates for the shortcomings of Baker et al. (2016). This paper measures economic policy uncertainty using the index calculated by Huang and Luk (2020), constructed by (1) selecting 10 newspapers such as Beijing Youth Daily, Guangzhou Daily, Jiefang Daily, People’s Daily (Overseas Edition), Shanghai Morning Post, etc., which are circulated in major mainland China cities, as text-mining sources from the 114 newspapers in the Wisers’ News database; (2) filtering and tagging keywords in news reports; (3) dividing the number of tagged articles by the total number of articles in the same month for the monthly index; (4) averaging monthly data to obtain yearly data, dividing by 100 for the final economic policy uncertainty index (See Table 1).

- (3)

- Control variables. This study selects control variables from the micro-enterprise, meso industry, and macro-national levels, drawing on the relevant literature on economic policy uncertainty. At the micro-firm level, the control variables include the following: (1) firm size: firms with substantial assets usually have sufficient capital and social resources for green innovation projects [22]; (2) gearing ratio (lev): firms with higher financial leverage usually exhibit excellent environmental performance [65]; (3) operating income growth rate (growth): firms with better operating income growth prospects typically demonstrate superior environmental performance [66]; (4) equity concentration (top5): higher firm equity concentration is more likely to weaken firms’ innovation capabilities [67]; (5) return on assets (Roa): firms with more substantial return on assets are more likely to engage in green innovation activities; (6) board size (Board): a higher proportion of board members helps cultivate CSR [68]; (7) fixed asset investment completion (fixed): the cost of machinery and equipment purchased by firms can usually be deducted from the sales of final products, which can increase the incentives for firms to purchase green equipment [69]; (8) corporate cash flow (Cash): corporate cash flow supports firms’ green innovation activities [70]. The industry-level control variable is local government industrial support (gov): with sufficient local government support, firms can obtain more resources for technological innovation [71]. The macro-level control variable is the purchasing managers’ index (PMI): the PMI is closely related to firms’ inventory investment fluctuation, which to some extent affects firms’ innovation behavioral decisions [72]. All variables are defined in Table 2.

3.3. Sample Selection, Data Processing, and Data Sources

4. Empirical Analysis

4.1. Descriptive Statistical Analysis and Correlation Analysis

4.2. Benchmark Regression Estimation Results

4.3. Endogeneity Treatment and Robustness Tests

4.3.1. Robustness Tests

- (1)

- Replacement of firms’ green technology innovation indicators. Although the benchmark regression indicates a reluctance among firms to pursue green technological innovation under economic policy uncertainty, the drop in the ratio-type green innovation indicator (IPC) might stem from an increase in current-year patent applications rather than a decrease in green patents filed. To alleviate the potential bias in measuring firms’ green innovation, this study draws on Popp’s methodology (2006) [76], using the number of green patents granted (GreenPat_1). Additionally, recognizing that enterprise green innovation includes both strategic and substantive elements, and that non-substantive “green” behavior may affect benchmark regression results, this paper employs the number of green patents granted (GreenPat_2) to gauge enterprise green innovation levels. Columns (1) and (2) in Table 6 confirm that the estimated coefficient of economic policy uncertainty (epu) remains significantly negative at the 1% level, even with the revised green innovation measurement, underscoring the robustness of the benchmark regression’s conclusions.

- (2)

- Replacement of econometric estimation methods. The overall green innovation of enterprises (IPC) represents a restricted dependent variable with a substantial number of “0” values and a range within [0,1]. The conventional econometric model is inadequate to handle estimation results from data with truncated characteristics. To address this issue, we employ the Tobit model to conduct further robustness testing. The estimation results in column (3) of Table 6 demonstrate that the estimated coefficient of economic policy uncertainty (epu) remains significantly negative at the 1% level. This finding indicates that the conclusion drawn from the benchmark regression remains unchanged.

- (3)

- Replacement of the economic policy uncertainty index. To ensure that the estimated impact of the benchmark regression is independent of how economic policy uncertainty is measured, this paper reevaluates economic uncertainty using the monthly economic policy uncertainty index (epu_robust) calculated by Huang and Luk (2020) [39] with the annual geometric mean treatment applied. The estimation results in column (4) of Table 6 indicate that the estimated coefficient on economic policy uncertainty (epu_robust) is significantly negative at the 10 percent significance level, confirming that the conclusions drawn from the baseline regression remain unchanged.

- (4)

- Lagging the explanatory variables by 1 period. Recognizing the time lag between the external transmission of policy and firms’ perception of policy uncertainty, the explanatory variables are lagged by 1 period to investigate the dynamic impact of firms’ green technology innovation under the influence of economic policy uncertainty. The estimation results in column (5) of Table 6 demonstrate that economic policy uncertainty (epu_lag) with a 1-period lag is significantly negative at the 10% statistical level, confirming that the conclusions drawn from the baseline regression remain unchanged.

- (5)

- Control variables lagged by 1 period. Since the control variables selected in this study may also have time-lagged effects on enterprises’ green technological innovation, which could potentially confound the estimation results of the baseline regression, we apply a one-period lag to all control variables to reassess the impact of economic policy uncertainty on enterprises’ green technological innovation. The estimation results in column (6) of Table 6 reveal that economic policy uncertainty (epu) remains significantly negative at the 1% statistical level, further confirming the consistency of conclusions drawn from the benchmark regression.

4.3.2. Endogenous Treatment

- (1)

- Bidirectional causal endogeneity. With China’s local development model shifting from “competition for growth” to “competition for innovation” in recent years [77], the performance of firms’ green innovation activities can prompt local governments to introduce targeted and biased policies, leading to fluctuations in economic policy uncertainty. Additionally, the performance of enterprises’ green innovation activities may prompt local governments to implement specific policies, influencing economic policy uncertainty in return. This creates a bidirectional causal endogenous problem between economic policy uncertainty and enterprises’ green technological innovation. To address the potential error in baseline regression estimation results due to bidirectional causal endogeneity, this study adopts the approach of Yu et al. (2021) by using the U.S. economic policy uncertainty index (epu_IV) calculated by Baker et al. (2016) as an instrumental variable for two-stage least squares (2sls) estimation [41,78]. The selection of this instrumental variable is based on the usual correlation between China’s economic policy uncertainty and that of the U.S. in the context of economic globalization. However, U.S. economic policy uncertainty does not directly impact firms’ green technological innovations. The green innovation behaviors of China’s micro firms have limited influence on U.S. economic policy uncertainty [79]. Therefore, using U.S. economic policy uncertainty as the instrumental variable generally satisfies the requirements of relevance and exogeneity.

- (2)

- The problem of endogeneity due to omitted variables. Economic policy uncertainty influences corporate green innovation decisions, with corporate executives’ personal experience and management structure characteristics playing a significant role [80]. Ignoring these factors in the benchmark regression may lead to an endogeneity problem caused by omitted variables. To enhance the robustness of the benchmark regression, this study employs CEO green experience (Green) and managerial power (Dual) as measurement variables for corporate executives’ personal experience and managerial and structural characteristics, respectively, and includes them in model (1) for re-regression. The CEO’s green experience is represented as a “0–1” variable, where 1 indicates that the CEO has received green education or been involved in green work, while 0 indicates otherwise. Managerial power is represented as a “0–1” variable, where a value of 1 indicates that the chairman of the board of directors and general manager are the same person, while 0 indicates otherwise.

- (3)

- Endogeneity due to control error in enterprise green technology innovation trend. In the baseline regression, this paper includes industry and city fixed effects to mitigate the impact of enterprise green innovation shocks resulting from industry and regional differences. However, given the variation in enterprise green technology innovation trends among different industries and cities, individual fixed effects alone cannot effectively control the coefficient bias caused by trend errors. To address this endogeneity problem, the paper further introduces “enterprise-industry” joint fixed effects and “enterprise-city” joint fixed effects.

4.4. Mechanism Analysis

4.5. Heterogeneity Analysis

- (1)

- Enterprise ownership structure. Compared to privately listed firms, SOEs, due to their strong government connections, have more advantages in obtaining bank loans and biased policy support. They are slightly less sensitive to policy’s negative impacts [83], fostering a greater willingness to undertake high-cost, long-term green technological innovation. In this paper, the research sample is divided into two groups based on the ownership structure of enterprises, utilizing model (1) for sub-sample regression. The results in columns (1) and (2) of Table 9 indicate that, when differentiating by ownership structure, the negative effect of economic policy uncertainty (epu) on green technology innovation is more significant among non-state-owned firms and not significant among state-owned firms. In a context of high economic policy uncertainty, non-state-owned firms, lacking financial or biased policy support, are less likely to pursue green innovation activities.

- (2)

- Enterprise size. The impact of economic policy uncertainty on green technological innovation varies among enterprises of different sizes. Faced with economic policy uncertainty, large firms often invest in risky opportunities while hedging their bets. Small firms, constrained by capital flows, tend to act “conservatively,” receiving government subsidies and shelving high-cost, high-uncertainty projects like green innovation [84]. In this paper, the research sample is divided into two groups: those with enterprise sizes greater than the median of 22.309 form a larger group, and the rest form a smaller group. This grouping is based on model (1) regression. The results in columns (3) and (4) of Table 9 indicate that economic policy uncertainty’s negative effect on green technology innovation is more pronounced among smaller firms and less so among larger ones. Under high uncertainty, smaller firms tend to be more “conservative” and avoid green innovation.

- (3)

- Enterprise industry type. The demand for green technology innovation varies across industries; thus, the influence of economic policy uncertainty on firms’ innovation varies too. Referencing Zhou (2021) [85] and using the “Guidelines for the Classification of Listed Companies in China (2012 Revision),” firms are grouped into labor-intensive, capital-intensive, and technology-intensive categories, and then analyzed using model (1). Table 9, columns (5)~(7), reveal that the negative impact of economic policy uncertainty on green innovation is more pronounced in labor-intensive and capital-intensive industries, but not in technology-intensive ones. This indicates that under high uncertainty, labor- and capital-intensive firms often delay green innovation, while technology-intensive firms remain unaffected.

- (4)

- Degree of industry competition. Robinson et al. (2012) [86] demonstrated that in an uncertain environment, firms considering the benefits and costs of delaying innovation see a gradual increase in waiting costs. Thus, under fierce industry competition, firms are more likely to enhance R&D investment to preserve competitiveness, possibly lessening the negative impact of economic policy uncertainty on green innovation. Using the Herfindahl Index (HHI) based on Spiegel’s (2021) method (, where Xi denotes firm size, N denotes the number of firms in the industry, and Xi/X reflects the market share of the ith firm) [87], the study samples are divided into low- and high-competition groups, based on a 0.159 median. Regression is conducted on model (1), post-grouping. Table 10, columns (1) and (2), indicate that the negative effect of economic policy uncertainty on green innovation is pronounced in low-competition firms but not in high-competition ones. This highlights that intensifying industry competition can alleviate the adverse effects of uncertainty on green innovation.

- (5)

- Regional property rights protection. The influence of economic policy uncertainty on green technological innovation varies with regional property rights protection levels. High input costs and the long-term nature of green innovation require effective intellectual property rights (IPR) protection to encourage firms. Following Grimaldi et al. (2021) [88], regional IPR is measured using the arithmetic average of intellectual property infringements per capita and lawyers per capita. The sample is split into two groups by the median IPP of 0.744: those above are the high IPP group, and the rest are treated as another group. Regression on these groups reveals (Table 10, columns (3) and (4)) a significantly milder negative effect of economic policy uncertainty on green innovation in areas with strong property rights protection, confirmed by a statistically significant Fisher combination test.

- (6)

- Degree of enterprise pollution. The cost of emissions varies across firms due to differences in pollution and energy consumption related to their products. For heavily polluting firms, their characteristics of high pollution and emissions lead to increased environmental taxes and charges. (According to the “Listed Companies Environmental Verification Industry Classification and Management List” (Environmental Affairs Office Letter [2008] No. 373), the industries that heavily polluting enterprises belong to include coal mining and washing; oil and natural gas mining; ferrous and non-ferrous metal mining and processing; non-metallic mining and processing; textile, leather, fur, feather products, and footwear; paper and paper products; petroleum refining; chemical raw materials and products manufacturing; pharmaceutical manufacturing; chemical fiber manufacturing; rubber and plastic products; non-metallic mineral products; ferrous and non-ferrous metal smelting and rolling processing; and thermal power.) Therefore, irrespective of economic policy uncertainty, green technological innovation becomes a favored means of avoiding harsh environmental penalties. (This includes purchasing green equipment as a form of innovation.) For non-heavily polluting firms, their relatively light pollution emissions do not result in serious environmental costs. In the face of economic policy uncertainty, these firms often reduce their green technology innovation projects to minimize business risks. The estimation results in columns (5) to (6) of Table 10 show that economic policy uncertainty (epu) has a more pronounced negative effect on green technology innovation in non-heavily polluted firms and a less significant impact in heavily polluted firms. Fischer’s combined between-groups coefficient test also reveals that this difference is statistically significant. The influence of economic policy uncertainty on green innovation activities is confirmed, considering the differences in pollution levels among enterprises.

5. Discussion

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Rasmussen, K.D.; Wenzel, H.; Bangs, C.; Petavratzi, E.; Liu, G. Platinum demand and potential bottlenecks in the global green transition: A dynamic material flow analysis. Environ. Sci. Technol. 2019, 53, 11541–11551. [Google Scholar] [CrossRef] [PubMed]

- Hickel, J.; Kallis, G. Is green growth possible? New Political Econ. 2020, 25, 469–486. [Google Scholar] [CrossRef]

- Schiederig, T.; Tietze, F.; Herstatt, C. Green innovation in technology and innovation management—An exploratory literature review. RD Manag. 2012, 42, 180–192. [Google Scholar] [CrossRef]

- Rennings, K. Redefining innovation—Eco-innovation research and the contribution from ecological economics. Ecol. Econ. 2000, 32, 319–332. [Google Scholar] [CrossRef]

- Qi, G.Y.; Shen, L.Y.; Zeng, S.X.; Jorge, O.J. The drivers for contractors’ green innovation: An industry perspective. J. Clean. Prod. 2010, 18, 1358–1365. [Google Scholar] [CrossRef]

- Chen, C.T.; Lin, C.T.; Huang, S.F. A fuzzy approach for supplier evaluation and selection in supply chain management. Int. J. Prod. Econ. 2006, 102, 289–301. [Google Scholar] [CrossRef]

- Tseng, M.L.; Chiu, A.S.F. Evaluating firm’s green supply chain management in linguistic preferences. J. Clean. Prod. 2013, 40, 22–31. [Google Scholar] [CrossRef]

- Tan, Y.; Zhu, Z. The effect of ESG rating events on corporate green innovation in China: The mediating role of financial constraints and managers’ environmental awareness. Technol. Soc. 2022, 68, 101906. [Google Scholar] [CrossRef]

- Bosetti, V.; Carraro, C.; Duval, R.; Tavoni, M. What should we expect from innovation? A model-based assessment of the environmental and mitigation cost implications of climate-related R&D. Energy Econ. 2011, 33, 1313–1320. [Google Scholar]

- Vanhaverbeke, W.; Van de Vrande, V.; Chesbrough, H. Understanding the advantages of open innovation practices in corporate venturing in terms of real options. Creat. Innov. Manag. 2008, 17, 251–258. [Google Scholar] [CrossRef]

- Kang, W.; Lee, K.; Ratti, R.A. Economic policy uncertainty and firm-level investment. J. Macroecon. 2014, 39, 42–53. [Google Scholar] [CrossRef]

- Aastveit, K.A.; Natvik, G.J.; Sola, S. Economic uncertainty and the influence of monetary policy. J. Int. Money Financ. 2017, 76, 50–67. [Google Scholar] [CrossRef]

- Cerda, R.; Silva, A.; Valente, J.T. Impact of economic uncertainty in a small open economy: The case of Chile. Appl. Econ. 2018, 50, 2894–2908. [Google Scholar] [CrossRef]

- Song, W.; Yu, H. Green innovation strategy and green innovation: The roles of green creativity and green organizational identity. Corp. Soc. Responsib. Environ. Manag. 2018, 25, 135–150. [Google Scholar] [CrossRef]

- Padilla-Lozano, C.P.; Collazzo, P. Corporate social responsibility, green innovation and competitiveness–causality in manufacturing. Compet. Rev. Int. Bus. J. 2021, 32, 21–39. [Google Scholar] [CrossRef]

- Tang, M.; Walsh, G.; Lerner, D.; Fitza, M.A.; Li, Q. Green innovation, managerial concern and firm performance: An empirical study. Bus. Strategy Environ. 2018, 27, 39–51. [Google Scholar] [CrossRef]

- Aghion, P.; Dechezleprêtre, A.; Hemous, D.; Martin, R.; Van Reenen, J. Carbon taxes, path dependency, and directed technical change: Evidence from the auto industry. J. Political Econ. 2016, 124, 1–51. [Google Scholar] [CrossRef]

- Esposito De Falco, S.; Renzi, A. The role of sunk cost and slack resources in innovation: A conceptual reading in an entrepreneurial perspective. Entrep. Res. J. 2015, 5, 167–179. [Google Scholar] [CrossRef]

- Wang, K.H.; Liu, L.; Zhong, Y.; Lobonţ, O.R. Economic policy uncertainty and carbon emission trading market: A China’s perspective. Energy Econ. 2022, 115, 106342. [Google Scholar] [CrossRef]

- Xu, Z. Economic policy uncertainty, cost of capital, and corporate innovation. J. Bank. Financ. 2020, 111, 105698. [Google Scholar] [CrossRef]

- Eder, J.; Trippl, M. Innovation in the periphery: Compensation and exploitation strategies. Growth Change 2019, 50, 1511–1531. [Google Scholar] [CrossRef]

- Lin, W.L.; Cheah, J.H.; Azali, M.; Ho, J.A.; Yip, N. Does firm size matter? Evidence on the impact of the green innovation strategy on corporate financial performance in the automotive sector. J. Clean. Prod. 2019, 229, 974–988. [Google Scholar] [CrossRef]

- Ding, X.; Appolloni, A.; Shahzad, M. Environmental administrative penalty, corporate environmental disclosures and the cost of debt. J. Clean. Prod. 2022, 332, 129919. [Google Scholar] [CrossRef]

- Van Vo, L.; Le, H.T.T. Strategic growth option, uncertainty, and R&D investment. Int. Rev. Financ. Anal. 2017, 51, 16–24. [Google Scholar]

- Friedlingstein, P.; O’sullivan, M.; Jones, M.W.; Andrew, R.M.; Hauck, J.; Olsen, A.; Peters, G.P.; Peters, W.; Pongratz, J.; Sitch, S.; et al. Global carbon budget 2020. Earth Syst. Sci. Data Discuss. 2020, 2020, 3269–3340. [Google Scholar] [CrossRef]

- Moore, A. Measuring economic uncertainty and its effects. Econ. Rec. 2017, 93, 550–575. [Google Scholar] [CrossRef]

- Sha, Y.; Kang, C.; Wang, Z. Economic policy uncertainty and mergers and acquisitions: Evidence from China. Econ. Model. 2020, 89, 590–600. [Google Scholar] [CrossRef]

- Li, Y.; Tong, Y.; Ye, F.; Song, J. The choice of the government green subsidy scheme: Innovation subsidy vs. product subsidy. Int. J. Prod. Res. 2020, 58, 4932–4946. [Google Scholar] [CrossRef]

- He, F.; Ma, Y.; Zhang, X. How does economic policy uncertainty affect corporate Innovation?—Evidence from China listed companies. Int. Rev. Econ. Financ. 2020, 67, 225–239. [Google Scholar] [CrossRef]

- Cui, X.; Wang, C.; Sensoy, A.; Liao, J.; Xie, X. Economic policy uncertainty and green innovation: Evidence from China. Econ. Model. 2023, 118, 106104. [Google Scholar] [CrossRef]

- Dunn, S.P.; Pressman, S. The Economic Contributions of John Kenneth Galbraith. Rev. Political Econ. 2005, 17, 161–209. [Google Scholar] [CrossRef]

- Morris, J.; Reilly, J.; Paltsev, S.; Sokolov, A.; Cox, K. Representing socio-economic uncertainty in human system models. Earth’s Future 2022, 10, e2021EF002239. [Google Scholar] [CrossRef]

- Caggiano, G.; Castelnuovo, E.; Figueres, J.M. Economic policy uncertainty and unemployment in the United States: A nonlinear approach. Econ. Lett. 2017, 151, 31–34. [Google Scholar] [CrossRef]

- Ashraf, B.N.; Shen, Y. Economic policy uncertainty and banks’ loan pricing. J. Financ. Stab. 2019, 44, 100695. [Google Scholar] [CrossRef]

- Ma, H.; Hao, D. Economic policy uncertainty, financial development, and financial constraints: Evidence from China. Int. Rev. Econ. Financ. 2022, 79, 368–386. [Google Scholar] [CrossRef]

- Wang, C.; Zheng, C.; Hu, C.; Luo, Y.; Liang, M. Resources sustainability and energy transition in China: Asymmetric role of digital trade and policy uncertainty using QARDL. Resour. Policy 2023, 85, 103845. [Google Scholar] [CrossRef]

- Wang, C.W.; Lee, C.C.; Chen, M.C. The effects of economic policy uncertainty and country governance on banks’ liquidity creation: International evidence. Pac.-Basin Financ. J. 2022, 71, 101708. [Google Scholar] [CrossRef]

- Gulen, H.; Ion, M. Policy uncertainty and corporate investment. Rev. Financ. Stud. 2016, 29, 523–564. [Google Scholar] [CrossRef]

- Huang, Y.; Luk, P. Measuring economic policy uncertainty in China. China Econ. Rev. 2020, 59, 101367. [Google Scholar] [CrossRef]

- Manela, A.; Moreira, A. News implied volatility and disaster concerns. J. Financ. Econ. 2017, 123, 137–162. [Google Scholar] [CrossRef]

- Baker, S.R.; Bloom, N.; Davis, S.J. Measuring economic policy uncertainty. Q. J. Econ. 2016, 131, 1593–1636. [Google Scholar] [CrossRef]

- Davis, S.J. An Index of Global Economic Policy Uncertainty; National Bureau of Economic Research: Cambridge, MA, USA, 2016. [Google Scholar]

- Bond, S.; Van Reenen, J. Microeconometric models of investment and employment. Handb. Econom. 2007, 6, 4417–4498. [Google Scholar]

- Courchane, M.; Nickerson, D.; Sullivan, R. Investment in internet banking as a real option: Theory and tests. J. Multinatl. Financ. Manag. 2002, 12, 347–363. [Google Scholar] [CrossRef]

- Sánchez-Sellero, P.; Bataineh, M.J. How R&D cooperation, R&D expenditures, public funds and R&D intensity affect green innovation? Technol. Anal. Strateg. Manag. 2022, 34, 1095–1108. [Google Scholar]

- Wang, P.; Bu, H.; Liu, F. Internal control and enterprise green innovation. Energies 2022, 15, 2193. [Google Scholar] [CrossRef]

- Munawar, S.; Yousaf, H.Q.; Ahmed, M.; Rehman, S. Effects of green human resource management on green innovation through green human capital, environmental knowledge, and managerial environmental concern. J. Hosp. Tour. Manag. 2022, 52, 141–150. [Google Scholar] [CrossRef]

- Zhou, C.; Yang, J. Factors that Impact Consumers’ Expenditure on Electric Vehicles: A Case Study from China. In Proceedings of the 2021 International Conference on Financial Management and Economic Transition (FMET 2021), Guangzhou, China, 27–29 August 2021; Atlantis Press: Amsterdam, The Netherlands, 2021; pp. 384–389. [Google Scholar]

- Chen, Z.; He, Z.; Liu, C. The financing of local government in China: Stimulus loan wanes and shadow banking waxes. J. Financ. Econ. 2020, 137, 42–71. [Google Scholar] [CrossRef]

- Xiang, X.; Liu, C.; Yang, M. Who is financing corporate green innovation? Int. Rev. Econ. Financ. 2022, 78, 321–337. [Google Scholar] [CrossRef]

- Chay, J.B.; Suh, J. Payout policy and cash-flow uncertainty. J. Financ. Econ. 2009, 93, 88–107. [Google Scholar] [CrossRef]

- Beladi, H.; Deng, J.; Hu, M. Cash flow uncertainty, financial constraints and R&D investment. Int. Rev. Financ. Anal. 2021, 76, 101785. [Google Scholar]

- Bofondi, M.; Carpinelli, L.; Sette, E. Credit supply during a sovereign debt crisis. Bank of Italy Temi di Discussione (Working Paper) No 2013, 909. J. Eur. Econ. Assoc. 2018, 16, 696–729. [Google Scholar] [CrossRef]

- Makosa, L.; Jie, S.; Bonga, W.G.; Jachi, M.; Sitsha, L. Does economic policy uncertainty aggravate financial constraints? S. Afr. J. Account. Res. 2021, 35, 151–166. [Google Scholar] [CrossRef]

- Von Neumann, J.; Morgenstern, O. Theory of Games and Economic Behavior, 2nd ed.; Princeton University Press: Princeton, NJ, USA, 1947. [Google Scholar]

- Hambrick, D.C.; Mason, P.A. Upper echelons: The organization as a reflection of its top managers. Acad. Manag. Rev. 1984, 9, 193–206. [Google Scholar] [CrossRef]

- Mata, R.; Frey, R.; Richter, D.; Schupp, J.; Hertwig, R. Risk preference: A view from psychology. J. Econ. Perspect. 2018, 32, 155–172. [Google Scholar] [CrossRef] [PubMed]

- Roper, S.; Tapinos, E. Taking risks in the face of uncertainty: An exploratory analysis of green innovation. Technol. Forecast. Soc. Change 2016, 112, 357–363. [Google Scholar] [CrossRef]

- Ivanov, D.; Dolgui, A. The shortage economy and its implications for supply chain and operations management. Int. J. Prod. Res. 2022, 60, 7141–7154. [Google Scholar] [CrossRef]

- Gholipour, H.F.; Nunkoo, R.; Foroughi, B.; Daronkola, H.K. Economic policy uncertainty, consumer confidence in major economies and outbound tourism to African countries. Tour. Econ. 2022, 28, 979–994. [Google Scholar] [CrossRef]

- Krol, R. Economic policy uncertainty and exchange rate volatility. Int. Financ. 2014, 17, 241–256. [Google Scholar] [CrossRef]

- Yoder, C.Y.; Mancha, R.; Agrawal, N. Culture-related factors affect sunk cost bias. Behav. Dev. Bull. 2014, 19, 105. [Google Scholar] [CrossRef]

- Zhang, Y.; Ye, J. The impact of risk preference of top management team on re-innovation behavior after innovation failure. J. Intell. Fuzzy Syst. 2021, 40, 11051–11061. [Google Scholar] [CrossRef]

- Zhang, S.; Wu, Z.; Wang, Y.; Hao, Y. Fostering green development with green finance: An empirical study on the environmental effect of green credit policy in China. J. Environ. Manag. 2021, 296, 113159. [Google Scholar] [CrossRef] [PubMed]

- Modi, S.B.; Cantor, D.E. How coopetition influences environmental performance: Role of financial slack, leverage, and leanness. Prod. Oper. Manag. 2021, 30, 2046–2068. [Google Scholar] [CrossRef]

- Ben-Amar, W.; McIlkenny, P. Board effectiveness and the voluntary disclosure of climate change information. Bus. Strategy Environ. 2015, 24, 704–719. [Google Scholar] [CrossRef]

- Xu, X.L.; Chen, H.H.; Li, Y.; Chen, Q.X. The role of equity balance and executive stock ownership in the innovation efficiency of renewable energy enterprises. J. Renew. Sustain. Energy 2019, 11, 055901. [Google Scholar] [CrossRef]

- Ben Rejeb, W.; Berraies, S.; Talbi, D. The contribution of board of directors’ roles to ambidextrous innovation: Do board’s gender diversity and independence matter? Eur. J. Innov. Manag. 2020, 23, 40–66. [Google Scholar] [CrossRef]

- Ivus, O.; Jose, M.; Sharma, R. R&D tax credit and innovation: Evidence from private firms in India. Res. Policy 2021, 50, 104128. [Google Scholar]

- Dyck, A.; Lins, K.V.; Roth, L.; Wagner, H.F. Do institutional investors drive corporate social responsibility? International evidence. J. Financ. Econ. 2019, 131, 693–714. [Google Scholar] [CrossRef]

- Caleb, H.T.; Yim, C.K.B.; Yin, E.; Wan, F.; Jiao, H. R&D activities and innovation performance of MNE subsidiaries: The moderating effects of government support and entry mode. Technol. Forecast. Soc. Change 2021, 166, 120603. [Google Scholar]

- Broadstock, D.C.; Matousek, R.; Meyer, M.; Tzeremes, N.G. Does corporate social responsibility impact firms’ innovation capacity? The indirect link between environmental & social governance implementation and innovation performance. J. Bus. Res. 2020, 119, 99–110. [Google Scholar]

- Bonaime, A.; Gulen, H.; Ion, M. Does policy uncertainty affect mergers and acquisitions? J. Financ. Econ. 2018, 129, 531–558. [Google Scholar] [CrossRef]

- Ley, M.; Stucki, T.; Woerter, M. The impact of energy prices on green innovation. Energy J. 2016, 37, 75. [Google Scholar] [CrossRef]

- Keele, L.; Stevenson, R.T.; Elwert, F. The causal interpretation of estimated associations in regression models. Political Sci. Res. Methods 2020, 8, 1–13. [Google Scholar] [CrossRef]

- Popp, D. International innovation and diffusion of air pollution control technologies: The effects of NOX and SO2 regulation in the US, Japan, and Germany. J. Environ. Econ. Manag. 2006, 51, 46–71. [Google Scholar] [CrossRef]

- Bian, Y.; Song, K.; Bai, J. Impact of Chinese market segmentation on regional collaborative governance of environmental pollution: A new approach to complex system theory. Growth Change 2021, 52, 283–309. [Google Scholar] [CrossRef]

- Yu, J.; Shi, X.; Guo, D.; Yang, L. Economic policy uncertainty (EPU) and firm carbon emissions: Evidence using a China provincial EPU index. Energy Econ. 2021, 94, 105071. [Google Scholar] [CrossRef]

- Wang, Y.; Chen, C.R.; Huang, Y.S. Economic policy uncertainty and corporate investment: Evidence from China. Pac.-Basin Financ. J. 2014, 26, 227–243. [Google Scholar] [CrossRef]

- Al-Matari, E.M. Do characteristics of the board of directors and top executives have an effect on corporate performance among the financial sector? Evidence using stock. Corp. Gov. Int. J. Bus. Soc. 2020, 20, 16–43. [Google Scholar] [CrossRef]

- Hadlock, C.J.; Pierce, J.R. New evidence on measuring financial constraints: Moving beyond the KZ index. Rev. Financ. Stud. 2010, 23, 1909–1940. [Google Scholar] [CrossRef]

- Zhou, B.; Li, Y.M.; Sun, F.C.; Zhou, Z.G. Executive compensation incentives, risk level and corporate innovation. Emerg. Mark. Rev. 2021, 47, 100798. [Google Scholar] [CrossRef]

- Lin, J.Y.; Cai, F.; Li, Z. Competition, policy burdens, and state-owned enterprise reform. Am. Econ. Rev. 1998, 88, 422–427. [Google Scholar]

- Otchere, I.; Senbet, L.W.; Zhu, P. Does political connection distort competition and encourage corporate risk taking? International evidence. J. Empir. Financ. 2020, 55, 21–42. [Google Scholar] [CrossRef]

- Zhou, C. How does capital intensity affect the relationship between outward FDI and productivity? Micro-evidence from Chinese manufacturing firms. Emerg. Mark. Financ. Trade 2021, 57, 4004–4019. [Google Scholar] [CrossRef]

- Robinson DK, R.; Le Masson, P.; Weil, B. Waiting games: Innovation impasses in situations of high uncertainty. Technol. Anal. Strateg. Manag. 2012, 24, 543–547. [Google Scholar] [CrossRef]

- Spiegel, Y. The Herfindahl-Hirschman Index and the Distribution of Social Surplus. J. Ind. Econ. 2021, 69, 561–594. [Google Scholar] [CrossRef]

- Grimaldi, M.; Greco, M.; Cricelli, L. A framework of intellectual property protection strategies and open innovation. J. Bus. Res. 2021, 123, 156–164. [Google Scholar] [CrossRef]

- Ren, X.; Xia, X.; Taghizadeh-Hesary, F. Uncertainty of uncertainty and corporate green innovation—Evidence from China. Econ. Anal. Policy 2023, 78, 634–647. [Google Scholar] [CrossRef]

- Cheng, Z.; Masron, T.A. Economic policy uncertainty and corporate digital transformation: Evidence from China. Appl. Econ. 2023, 55, 4625–4641. [Google Scholar] [CrossRef]

- Lou, Z.; Chen, S.; Yin, W.; Zhang, C.; Yu, X. Economic policy uncertainty and firm innovation: Evidence from a risk-taking perspective. Int. Rev. Econ. Financ. 2022, 77, 78–96. [Google Scholar] [CrossRef]

- Guan, J.; Xu, H.; Huo, D.; Hua, Y.; Wang, Y. Economic policy uncertainty and corporate innovation: Evidence from China. Pac.-Basin Financ. J. 2021, 67, 101542. [Google Scholar] [CrossRef]

- Shi, J.; Zhang, M. Investor Sentiment, Corporate Investment, and Firm Performance. In Proceedings of the 2010 3rd International Conference on Information Management, Innovation Management and Industrial Engineering, Kunming, China, 26–28 November 2010; IEEE: New York, NY, USA, 2010; Volume 1, pp. 251–254. [Google Scholar]

- William, M.; Fengrong, W. Economic policy uncertainty and industry innovation: Cross country evidence. Q. Rev. Econ. Financ. 2022, 84, 208–228. [Google Scholar] [CrossRef]

- Peng, X.Y.; Zou, X.Y.; Zhao, X.X.; Chang, C.P. How does economic policy uncertainty affect green innovation? Technol. Econ. Dev. Econ. 2023, 29, 114–140. [Google Scholar] [CrossRef]

- Yang, X.; Mao, S.; Sun, L.; Feng, C.; Xia, Y. The Effect of Economic Policy Uncertainty on Green Technology Innovation: Evidence from China’s Enterprises. Sustainability 2022, 14, 11522. [Google Scholar] [CrossRef]

{kind=link}

| Form | English Keywords |

|---|---|

| Economic | Economic/Economy/Financial |

| Uncertainty | Uncertainty/Uncertain Volatile Unstable/Unclear Unpredictable |

| Policy | Policy/measures Politics Government/Authority President Prime minister Reform Regulation Fiscal Tax People’s Bank of China/PBOC Deficit Interest rate |

| Type | Symbols | Variable Name | Measurement Methods |

|---|---|---|---|

| Dependent variable | IPC | Green technology innovation | Proportion of green patents applied for by enterprises in the same year to all patents applied for by enterprises in the same year |

| Independent variable | epu | Economic policy uncertainty | Ten representative newspapers in mainland China are selected as texts to calculate monthly economic policy uncertainty, and the arithmetic mean of the monthly economic policy uncertainty index is converted into an annual index and divided by 100 |

| Control variables | Roa | Return on equity | (Net profit of the enterprise for the year + interest expense + income tax) divided by average total assets |

| lev | Debt-to-Asset Ratio | Total liabilities of the enterprise at the end of the year divided by total assets of the enterprise at the end of the year | |

| growth | Revenue growth rate | Current year’s operating income divided by last year’s operating income-1 | |

| Top5 | Equity concentration | Proportion of shares held by the top five shareholders of the enterprise at the end of the year | |

| Cash | Corporate cash flow | Cash flows from operating activities of the enterprise for the year divided by total assets of the enterprise | |

| Size | Company size | Total assets of the enterprise at the end of the year in natural logarithms | |

| Board | Board size | Number of people on the board of directors of the company | |

| fixed | Fixed Asset Investment Completion | Total company purchases of machinery and equipment, computer equipment, land, utilities, and repairs | |

| gov | Local government industry support | If the industry in which the enterprise is engaged is a key support industry in the local five-year plan, the value will be assigned as 1; otherwise, it will be defined as 0 | |

| pmi | purchasing managers’ index | Conversion of the arithmetic average of monthly PMI indices published by the National Bureau of Statistics into annual values |

| VarName | Obs | Mean | SD | Min | Median | Max |

|---|---|---|---|---|---|---|

| IPC | 13,625 | 0.047 | 0.142 | 0.000 | 0.000 | 1.000 |

| epu | 13,625 | 1.430 | 0.131 | 1.250 | 1.409 | 1.657 |

| Size | 13,625 | 22.448 | 1.406 | 19.226 | 22.309 | 27.784 |

| Roa | 13,625 | 0.036 | 0.060 | −0.263 | 0.031 | 0.226 |

| Cash | 13,625 | 0.047 | 0.074 | −0.213 | 0.047 | 0.256 |

| Board | 13,625 | 8.997 | 1.834 | 5.000 | 9.000 | 15.000 |

| fixed | 13,625 | 0.249 | 0.186 | 0.000 | 0.211 | 0.971 |

| Growth | 13,625 | 0.002 | 0.006 | −0.007 | 0.001 | 0.049 |

| top5 | 13,625 | 0.501 | 0.154 | 0.008 | 0.498 | 0.959 |

| lev | 13,625 | 0.500 | 0.203 | 0.007 | 0.509 | 2.529 |

| gov | 13,625 | 0.405 | 0.491 | 0.000 | 0.000 | 1.000 |

| pmi | 13,625 | 0.509 | 0.013 | 0.495 | 0.508 | 0.536 |

| FC | 13,625 | 3.805 | 0.258 | 2.344 | 3.816 | 4.83 |

| Risk_Preference | 13,625 | 0.109 | 0.577 | −2.467 | 0.124 | 3.199 |

| IPC | epu | Size | Roa | Cash | Board | fixed | Growth | top5 | lev | gov | pmi | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| IPC | 1 | |||||||||||

| epu | −0.026 *** | 1 | ||||||||||

| Size | 0.071 *** | −0.080 *** | 1 | |||||||||

| Roa | 0.005 | 0.0110 | 0.070 *** | 1 | ||||||||

| Cash | 0.01 | −0.019 ** | 0.049 *** | 0.371 *** | 1 | |||||||

| Board | 0.046 *** | 0.033 *** | 0.246 *** | 0.028 *** | 0.073 *** | 1 | ||||||

| fixed | 0.035 *** | 0.022 ** | 0.032 *** | −0.101 *** | 0.259 *** | 0.158 *** | 1 | |||||

| Growth | −0.009 | 0.006 | 0.050 *** | 0.165 *** | 0.0110 | −0.021 ** | −0.063 *** | 1 | ||||

| top5 | −0.012 | 0.002 | 0.322 *** | 0.158 *** | 0.108 *** | 0.126 *** | 0.077 *** | 0.094 *** | 1 | |||

| lev | 0.036 *** | 0.006 | 0.378 *** | −0.373 *** | −0.178 *** | 0.109 *** | 0.01 | 0.045 *** | 0.059 *** | 1 | ||

| gov | 0.064 *** | 0.033 *** | −0.033 *** | 0.046 *** | 0.047 *** | 0.035 *** | 0.146 *** | −0.011 | −0.0120 | −0.099 *** | 1 | |

| pmi | 0.002 | −0.415 *** | −0.141 *** | 0.095 *** | 0.009 | 0.038 *** | 0.035 *** | 0.075 *** | −0.002 | 0.017 ** | −0.037 *** | 1 |

| Variables | (1) | (2) | (3) | (4) | (5) | (6) |

|---|---|---|---|---|---|---|

| IPC | IPC | IPC | IPC | IPC | IPC | |

| epu | −0.028 *** | −0.031 *** | −0.030 *** | −0.025 *** | −0.025 *** | −0.027 *** |

| (−3.700) | (−4.112) | (−3.922) | (−3.417) | (−3.496) | (−2.680) | |

| Size | 0.007 *** | 0.007 *** | 0.006 *** | |||

| (3.123) | (3.139) | (2.969) | ||||

| Roa | −0.002 | −0.003 | −0.002 | |||

| (−0.082) | (−0.120) | (−0.066) | ||||

| Cash | −0.029 * | −0.029 * | −0.030 * | |||

| (−1.797) | (−1.783) | (−1.805) | ||||

| Board | 0.001 | 0.001 | 0.001 | |||

| (0.963) | (0.929) | (0.954) | ||||

| fixed | 0.019 | 0.019 | 0.019 | |||

| (1.170) | (1.128) | (1.135) | ||||

| Growth | −0.020 | −0.021 | −0.016 | |||

| (−0.166) | (−0.169) | (−0.127) | ||||

| top5 | −0.040 ** | −0.040 ** | −0.040 ** | |||

| (−2.115) | (−2.091) | (−2.084) | ||||

| lev | −0.003 | −0.002 | −0.002 | |||

| (−0.242) | (−0.232) | (−0.182) | ||||

| gov | 0.005 | 0.005 | ||||

| (1.267) | (1.251) | |||||

| pmi | −0.029 | |||||

| (−0.247) | ||||||

| _cons | 0.087 *** | 0.091 *** | 0.089 *** | −0.056 | −0.058 | −0.036 |

| (7.739) | (8.446) | (8.225) | (−1.123) | (−1.159) | (−0.382) | |

| Firm fixed effect | No | YES | YES | YES | YES | YES |

| Industry fixed effect | YES | YES | YES | YES | YES | YES |

| Urban fixed effect | No | No | YES | YES | YES | YES |

| Time Trend Control | YES | YES | YES | YES | YES | YES |

| N | 13,625 | 13,625 | 13,625 | 13,625 | 13,625 | 13,625 |

| Adjust R2 | 0.0665 | 0.3851 | 0.3879 | 0.3891 | 0.3892 | 0.3892 |

| Variables | (1) | (2) | (3) | (4) | (5) | (6) |

|---|---|---|---|---|---|---|

| GreenPat_1 | GreenPat_2 | IPC | IPC | IPC | IPC | |

| epu | −0.369 *** | −0.594 *** | −0.029 *** | −0.035 *** | ||

| (−5.41) | (−9.30) | (−3.08) | (−4.07) | |||

| epu_robust | −0.232 * | |||||

| (−17.74) | ||||||

| epu_lag | −0.014 * | |||||

| (−1.79) | ||||||

| Intercept, control variables | YES | YES | YES | YES | YES | YES |

| Firm fixed effect | YES | YES | NO | YES | YES | YES |

| Industry fixed effect | YES | YES | NO | YES | YES | YES |

| Urban fixed effect | YES | YES | NO | YES | YES | YES |

| Time trend control | YES | YES | YES | YES | YES | YES |

| N | 13,559 | 13,559 | 13,625 | 13,559 | 12,258 | 12,258 |

| Adjust R2 | 0.1089 | 0.0825 | 0.0773 | 0.3890 | 0.3981 | 0.4003 |

| Variables | (1) | (2) | (3) | (4) | (5) |

|---|---|---|---|---|---|

| epu | IPC | IPC | IPC | IPC | |

| epu | −0.205 *** | −0.020 * | −0.030 *** | −0.030 *** | |

| (−5.86) | (−1.81) | (−3.88) | (−3.79) | ||

| epu_IV | 0.001 *** | ||||

| (30.92) | |||||

| Green | 0.023 * | ||||

| (1.74) | |||||

| Dual | −0.002 | ||||

| (−0.35) | |||||

| Intercept, control variables | YES | YES | YES | YES | YES |

| Cragg–Donald Wald F-value | 956.3 | ||||

| Anderson canon. corr. LM statistic | 889.16 | ||||

| Firm fixed effect | YES | YES | YES | YES | YES |

| Industry fixed effect | YES | YES | YES | YES | YES |

| Urban fixed effect | YES | YES | YES | YES | YES |

| Joint firm–industry fixed effects | NO | NO | NO | YES | NO |

| Joint firm–city fixed effects | NO | NO | NO | NO | YES |

| Time Trend Control | YES | YES | YES | YES | YES |

| N | 13,625 | 13,625 | 13,625 | 13,559 | 13,559 |

| Adjust R2 | 0.1485 | 0.0825 | 0.0775 | 0.1205 | 0.1166 |

| Panel A: Results of the Analysis of Mechanisms | |||||

|---|---|---|---|---|---|

| Variables | (1) | (2) | (3) | (4) | |

| FC | Risk_Preference | IPC | IPC | ||

| epu | 0.349 *** | −0.434 *** | −0.036 *** | −0.030 *** | |

| (34.22) | (−12.97) | (−3.35) | (−2.61) | ||

| FC | −0.017 * | ||||

| (−1.65) | |||||

| Risk_Preference | 0.006 ** | ||||

| (2.12) | |||||

| Intercept, control variables | YES | YES | YES | YES | |

| Firm fixed effect | YES | YES | YES | YES | |

| Industry fixed effect | YES | YES | YES | YES | |

| Urban fixed effect | YES | YES | YES | YES | |

| Time trend control | YES | YES | YES | YES | |

| N | 13,522 | 13,482 | 13,522 | 13,482 | |

| Adjust R2 | 0.8355 | 0.6092 | 0.3867 | 0.3195 | |

| Panel B: Mediation effect test | |||||

| Z-Value | Sobel | Aroian | Goodman | ||

| FC | 10.286 *** | 10.283 *** | 10.290 *** | ||

| Risk_Preference | 2.094 ** | 2.089 ** | 2.099 ** | ||

| Variables | (1) | (2) | (3) | (4) | (5) | (6) | (7) |

|---|---|---|---|---|---|---|---|

| State-Owned Enterprise | Non-State-Owned Enterprise | Larger Scale | Smaller Scale | Labor-Intensive | Capital-Intensive | Technology-Intensive | |

| IPC | IPC | IPC | IPC | IPC | IPC | IPC | |

| epu | −0.010 | −0.038 *** | −0.017 | −0.035 ** | −0.038 ** | −0.033 * | −0.016 |

| (−0.72) | (−2.62) | (−1.23) | (−2.19) | (−2.18) | (−1.74) | (−0.94) | |

| Intercept, control variables | YES | YES | YES | YES | YES | YES | YES |

| Firm fixed effect | YES | YES | YES | YES | YES | YES | YES |

| Industry fixed effect | YES | YES | YES | YES | YES | YES | YES |

| Urban fixed effect | YES | YES | YES | YES | YES | YES | YES |

| Time trend control | YES | YES | YES | YES | YES | YES | YES |

| N | 5563 | 7789 | 6737 | 6733 | 4637 | 4217 | 4642 |

| Adjust R2 | 0.4780 | 0.3452 | 0.4611 | 0.3847 | 0.2841 | 0.4081 | 0.4800 |

| Between-group coefficient test p-value | 0.09 * | 0.02 ** | 0.02 ** | ||||

| Variables | (1) | (2) | (3) | (4) | (5) | (6) |

|---|---|---|---|---|---|---|

| High Industry Competition | Low Industry Competition | High-IPP | Low-IPP | Heavy-Polluting | Non-Heavy-Polluting | |

| IPC | IPC | IPC | IPC | IPC | IPC | |

| epu | −0.022 | −0.041 *** | −0.023 * | −0.028 * | −0.028 | −0.028 ** |

| (−1.58) | (−2.66) | (−1.67) | (−1.85) | (−1.36) | (−2.59) | |

| Intercept, control variables | YES | YES | YES | YES | YES | YES |

| Firm fixed effect | YES | YES | YES | YES | YES | YES |

| Industry fixed effect | YES | YES | YES | YES | YES | YES |

| Urban fixed effect | YES | YES | YES | YES | YES | YES |

| Time trend control | YES | YES | YES | YES | YES | YES |

| N | YES | YES | YES | YES | YES | YES |

| Adjust R2 | 8001 | 5473 | 6899 | 6605 | 4738 | 8791 |

| Between-group coefficient test p-value | 0.01 *** | 0.05 ** | 0.01 *** | |||

| Intercept, control variables | 0.4297 | 0.3708 | 0.4540 | 0.3856 | 0.3504 | 0.4328 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Chen, M.; Hu, X.; Zhang, J.; Xu, Z.; Yang, G.; Sun, Z. Are Firms More Willing to Seek Green Technology Innovation in the Context of Economic Policy Uncertainty? —Evidence from China. Sustainability 2023, 15, 14188. https://doi.org/10.3390/su151914188

Chen M, Hu X, Zhang J, Xu Z, Yang G, Sun Z. Are Firms More Willing to Seek Green Technology Innovation in the Context of Economic Policy Uncertainty? —Evidence from China. Sustainability. 2023; 15(19):14188. https://doi.org/10.3390/su151914188

Chicago/Turabian StyleChen, Mo, Xuhua Hu, Jijian Zhang, Zhe Xu, Guang Yang, and Zenan Sun. 2023. "Are Firms More Willing to Seek Green Technology Innovation in the Context of Economic Policy Uncertainty? —Evidence from China" Sustainability 15, no. 19: 14188. https://doi.org/10.3390/su151914188