1. Introduction

Globally speaking, sustainable development is currently at a turning point. More and more nations recognize the necessity of reasonably limiting carbon emissions within a particular range as greenhouse gas emissions have reached record highs and rapid economic development is placing pressure on the ecological environment. In 2020, China committed to pursuing the goals of a carbon peak in 2030 and carbon neutrality in 2060. An eco-friendly, low-carbon lifestyle is promoted through the dual-carbon plan. The growth of green finance is crucial to promote the achievement of this goal. The report by the Communist Party of China’s 20th National Congress places a strong emphasis on the necessity of fostering low-carbon, environmentally friendly economic and social development as well as reasonable economic and qualitative growth. Providing financial services to businesses engaged in environmental improvement, addressing climate change, and boosting low carbon growth through resource efficiency are the strategies at the heart of green finance. The development of green finance can directly or indirectly influence high-quality economic development. In the 14th five-year plan, it is highlighted that a green and low-carbon modern economic system should be developed together with sustainable development goals. One of the key methods to carry out this philosophy is green finance. The green finance sector in China has grown rapidly in recent years, supporting the capital need and ensuring the best use of resources in linked industries. Also, in the framework of the dual-carbon goal, green finance’s diversity and policy, along with the financial instruments created from it during the development process, are significant ways to reach the target of “3060”. Currently, one of the most important research areas is how to successfully link carbon emission reduction, green finance, and high-quality economic development.

Green finance has evolved into a tool for implementing green policies that is being studied by academics both domestically and internationally. Given that environmental protection and sustainable development are still significant global hot topics, research on green finance can help financial institutions allocate resources judiciously to support high-quality economic development. This research can also offer useful research recommendations for policymakers during the implementation process. In addition to being one of the core components of China’s “3060” target, the growth of green finance can also be advantageous in several ways: (1) it promotes the growth of the green economy and directs funding toward green, low-carbon, and other industries. (2) To achieve the objective of sustainable development, it assists in preserving the environment, improving the quality of the environment, and fostering resource efficiency. (3) It aids in lowering carbon emissions and reduces the risks associated with climatic conditions. (4) It helps Chinese enterprises become more inventive and competitive internationally, enhancing China’s global competitiveness in the “low-carbon economy” sector. (5) It offers a new strategy to support the growth of green businesses.

In summary, the development of green finance is crucial in a number of ways. To fully realize the goal of a high-quality economy and sustainable development, it can effectively distribute funding to low-carbon and green industries and encourage businesses to innovate in green technology [

1], and it can advocate for lowering carbon dioxide emissions and energy efficiency [

2]. Green financing accounts for a sizable share of the carbon market, and its growth can aid initiatives to cut carbon emissions. Businesses may effectively reduce carbon emissions and support high-quality economic development while implementing green finance by developing green technology. The underlying assumption of this article is that green finance can both directly and indirectly support the high-quality growth of regional economies. This indirect support comes from the decrease in carbon emissions. Using panel data from 30 Chinese provinces, cities, and autonomous regions from 2008 to 2019, this study builds a two-way fixed effect model to investigate how green funding affects the high-quality expansion of local economies. The mechanism is then studied using an intermediary effect model. First, this paper analyzes the research context and significance of the study, then moves on to the research issue of how green finance affects high-quality economic development in the context of double carbon, which explains the innovative content of the paper. Second, the relevant literature on domestic and international green finance is outlined, and the theories of green finance, the impact of green finance on reducing carbon emissions, and green finance’s role in fostering high-quality economic growth are all explored. Third, given the Cobb–Douglas production function and environmental Kuznets curve, the influence mechanism of green finance is analyzed, and on this basis, relevant assumptions are put forward. Finally, this paper builds a two-way fixed effect model, introduces provincial panel data for empirical test, and verifies the hypothesis through a robustness test, heterogeneity analysis, intermediary mechanism, and spatial measurement test, and finally draws a conclusion and puts forward policy suggestions.

This paper introduces the following innovations. (1) Index measurement: This study uses the entropy weight TOPSIS rule to measure the economic high-quality development levels of 30 provinces, cities, and autonomous areas of China from 2008 to 2019. It also uses the green credit ratio to calculate the level of regional green development as well as the CEADs China carbon accounting data to compute the intensity of China’s carbon emissions. (2) Model: This paper tests the impact of green finance on the high-quality economic development through the two-way fixed benefit model and analyzes the provinces, cities, and autonomous regions in China by using the Moran index and spatial econometric model to test the spatial spillover effect of green finance development. (3) Impact mechanism: This study examines how green financing indirectly influences high-quality economic development in China using the intermediary effect model.

The establishment of the model in this paper considers the spatial factors. In addition to looking at how green finance directly affects the high-quality development of the economy, this paper also looked at how those effects have changed because of the inclusion of spatial factors. Based on theoretical construction and empirical analysis, this paper explores the influence of green finance in high-quality economic development and strengthens the theoretical case for encouraging the government and relevant financial institutions to develop green finance to promote the high-quality economic development.

The following is the organization of this paper.

Section 2 reviews the existing literature. In

Section 3, various presumptions are made and a theoretical analysis of the relationship between green finance, carbon emission reduction, and high-quality economic development is presented.

Section 4 demonstrates an empirical evaluation of green finance’s effects on carbon emission reduction and high-quality economic development.

Section 5 presents empirical results, a robustness test, intermediary mechanism, and spatial measurement test. The paper is concluded in

Section 6, which also offers suggestions for future research and policy.

3. Theoretical Analysis

The relationship among green finance, carbon emission, and economic development is complex. The Cobb–Douglas production function is used as the basis of establishing the model, and the influence of green finance on high-quality economic development is analyzed theoretically. This study investigates the function of green finance in enhancing environmental quality, i.e., reducing carbon emissions, and supports high-quality economic development. It introduces the environmental Kuznets curve hypothesis.

3.1. Extended Cobb–Douglas Production Function

According to the Cobb–Douglas production function, economic growth is influenced by a variety of factors, including the amount of labor and fixed assets, a broad technical level (including management level, labor quality, introduction of contemporary technology, etc.), and other factors. Energy use, production, and pollutant emission are intimately connected. The production function is given by

where

Y denotes economic output,

denotes the level of technology,

denotes capital,

denotes the energy consumption in production,

denotes labor, and

denotes the error term.

,

, and

are the elasticity coefficients of capital stock, energy consumption, and labor force, respectively. The technical level of Cobb–Douglas production function is limited, that is, when

, the return to scale remains unchanged.

When the technical level is given, the link between energy consumption (

) and environmental pollutant emission (

) is

[

60], and

is a constant, then Formula (1) can be deformed as:

This paper offers a theoretical analysis based on Equation (2). The development of green finance can also pool idle funds and savings in the social economy and effectively transform them into green investments, improve capital stock and green technology level, and play a beneficial role in promoting economic development under the direction of governmental policies and financial institutions.

The main distinction between green finance and conventional finance is the emphasis on resource and environmental preservation in the former. Green finance will guide capital, workforce, and other resource elements into green industries through green financial instruments; it will also provide resource support for green environmental protection enterprises after thoroughly investigating the economic benefits of the environment. The effective and rational allocation of resources will be realized with the continuous transfer of resources from traditional “double-high” enterprises to environment-friendly enterprises. The proportion of traditional industrial output will gradually decrease, the output of green industries will gradually increase, and the industrial structure will be optimized.

Last but not least, the study above enables us to conclude that green finance may successfully direct financial and technological resources to flow towards green enterprises. However, traditional industries that have lost the support of resources must change their traditional business and carry out technological innovation in order to adapt to the trend of green development to survive in the market. Under this condition of inclined resources, green enterprises supported by resources make rational use of resources, improving their own technical level, and realizing technological progress. The modernization of the industrial structure has gained new momentum. In this situation, the market will observe an increase in innovation-driven businesses, which is very beneficial for economic growth. We present the following hypothesis:

Hypothesis 1. Green finance has a direct and positive role in promoting economic development.

3.2. Environmental Kuznets Curve Theory

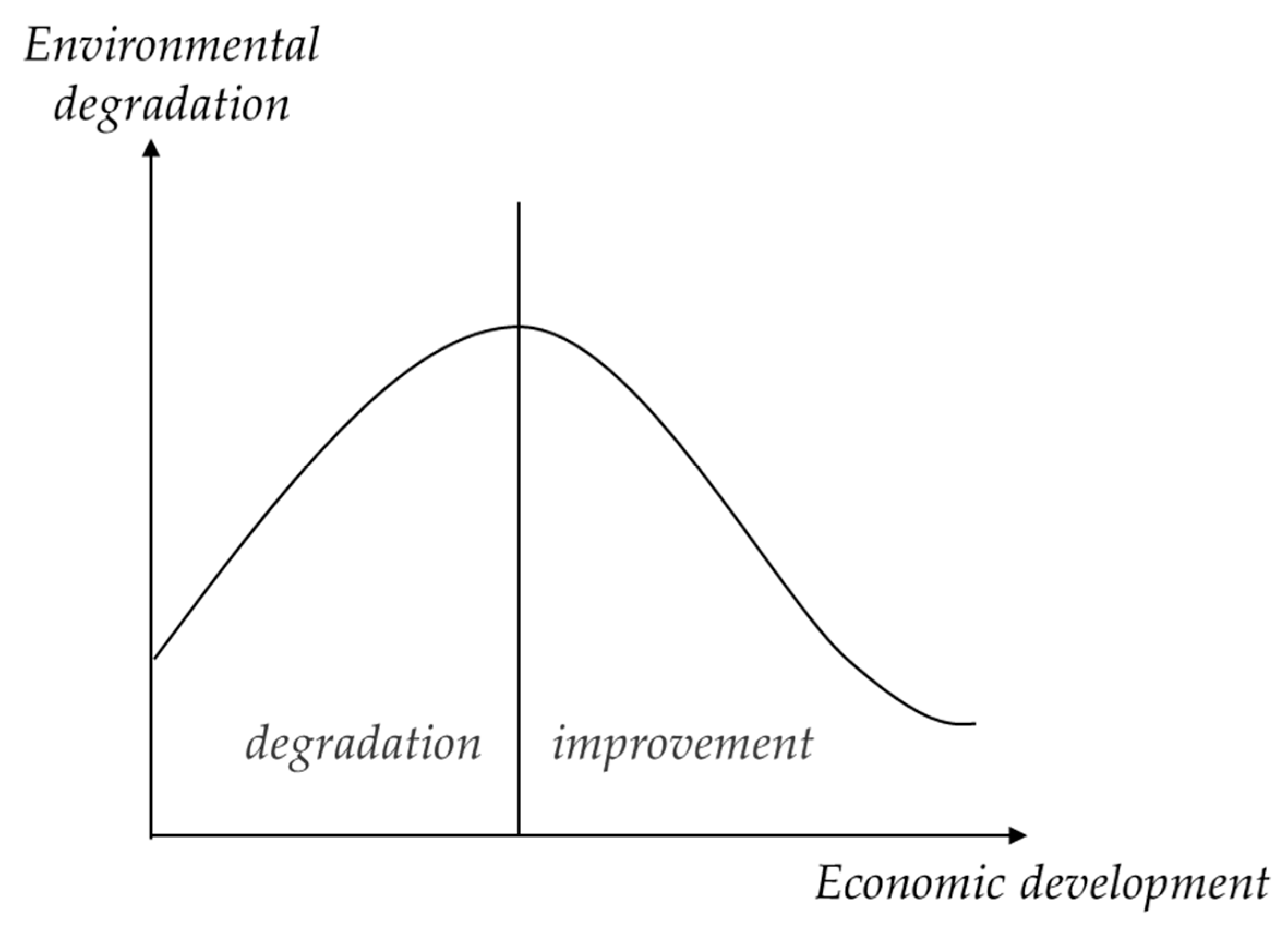

Grossman and Krueger conducted the first empirical investigation of the relationship between environmental quality and per capita income in the early 1990s to address the concern that the fall of free trade would have a negative influence on the environment. They held that a country’s environmental quality was higher and its pollution levels were lower when its economic development was in its early stages, and that as per capita income continuously climbed, so did the level of environmental pollution. They believed that, as per capita income rose, the level of environmental pollution would fall decrease and the environment would get cleaner once the nation’s economy had advanced to a certain point and passed a crucial threshold. When there is a significant combined effect, it is referred to as the environmental Kuznets curve [

61]. The graph of environmental Kuznets curve is shown in

Figure 1. The significance of environmental pollution caused by economic growth in China is illustrated by the inverted U-shaped environmental Kuznets curve, as well as the correlation between environmental pollution caused by the economic development model and the change in per capita income.

The emergence of green finance may directly affect carbon emissions. In contrast to currently used command-based environmental regulation and incentive-based environmental regulation, green bonds contain both the characteristics of market-based environmental regulation and the resource allocation function of the financial sector. Their focus is on encouraging the best distribution of financial resources among economic and environmental agencies. To effectively allocate resources in the market and support the green development of industries, which has an impact on economic growth, by shifting talent, technology, capital, and other resources away from traditional sectors with high energy consumption and high pollution to environmentally friendly green industries with low energy consumption and high production, green finance can fulfill its duty as a resource-oriented industry.

On the other hand, in the new phase of China’s economic and social transition to a green economy, the government would fully support the growth of green financing. Relevant government departments heavily subsidize green bonds as part of government policy, making green bonds in China far more affordable to finance than comparable bonds. These elements work together to lower the cost of borrowing for businesses using green bonds. Therefore, green bonds can aid in easing the financial constraints faced by businesses while increasing their investment in environmental protection to lower carbon emissions.

In conclusion, given that the total amount of regional financial capital is known, green bonds on the one hand help direct more social funds toward the green industry sector, improving the effectiveness of green development; on the other hand, increased green bond financing will result in less money being allocated to other pollution projects, preventing the growth of heavily polluting industries, lowering unexpected output, and improving green total factor productivity.

This paper presents the following hypothesis based on the analysis previously mentioned:

Hypothesis 2. Green finance helps to increase carbon productivity, fostering high-quality economic development.

6. Conclusions and Recommendations

6.1. Conclusions

Based on panel data from the provinces from 2008 to 2019, this study develops a two-way fixed effect model for theoretical analysis and empirical testing of the role of green finance on high-quality economic development. By analyzing the research results, the following conclusions are drawn:

First, green finance directly promotes the improvement of China’s high-quality economic development level. After replacing variables, it can be seen that the result is robust and credible. Green finance promotes the high-quality economic development of the region by integrating idle funds in the market into green investment, guiding people to carry out green consumption and playing a resource-oriented role. Various institutions have actively responded to the green finance policy and developed diversified green financial products, with green credit and green bonds performing particularly well in the market. Heterogeneity analysis demonstrates that, whereas the central and western regions do not have a significant positive impact on high-quality economic development, the eastern region experiences a more positive promotion of green finance. With a focus on technologically intensive industries like new energy, the eastern area offers advanced development advantages and a high degree of green financing development.

Green finance can support the enhancement of carbon productivity and further support the high-quality economic development. The growth of the green finance industry is advantageous for upholding environmental regulations, fostering low-carbon development, creating a green recycling industry system, effectively fostering green technology innovation, enhancing the capacity to reduce pollution and carbon, and quickening the conversion of traditional and alternative energy sources. By encouraging the coordinated growth of industries, raising the technical level of energy conservation and emission reduction, promote the high-quality growth of the regional economy.

Overall, under three spatial weight matrices, the development level of green financing has a positive spatial spillover effect on the level of high-quality economic development. The growth of green finance in these provinces has the potential to not only contribute significantly to the high-quality development of the local economy, but also to that of the nearby provinces. The promotion effect is amplified by geographic distance.

6.2. Recommendations

6.2.1. Vigorously Support the Development of Green Finance

Environmental protection and the idea of being “green” are receiving more and more attention from the general public. Therefore, economic agents need to integrate sustainable development into their strategies to help solve environmental problems [

70]. The government should actively encourage the promotion of green finance, introduce pertinent green finance development policies, direct investment into green industries, enhance the system for green consumption, and direct green consumption. We should also enhance the legal framework pertaining to green finance in China, provide a productive and reliable green financial development market, and adopt pertinent incentive measures. The government should also monitor how statistics and information about green financing are disclosed in different provinces, localities, or publicly traded banks and businesses.

6.2.2. Financial Institutions Actively Cooperate with Development

Financial institutions must actively support the government’s plans for policies and actions. The guiding role of the government cannot be separated from the growth of green finance; nevertheless, it also requires the support of assisting enterprises in the financial sector. Financial institutions need to keep their business systems up to date in order for financial products to develop more quickly, meet the demands of a shift to a green economy, and create a system of varied green financial products. At the moment, green credit makes up more than 90% of China’s green credit products, demonstrating that our green finance still suffers from issues, including a monolithic structure and a lack of innovation, which financial institutions must urgently address.

6.2.3. Attach Importance to Regional Differences and Develop Green Finance

When it comes to green finance development, different regions started at different times, which results in varying degrees of progress. The central and western regions must perform well in the fundamental tasks of developing green finance, such as system development and extending financing options. They must also utilize the benefits of talent capital, green technology, and capital in developed areas, amplify the radiation effect in central areas, make up for the shortcomings of economic development in surrounding areas, and encourage regional coordinated development.

6.2.4. Strengthen the Development Role of Green Finance in Low-Carbon Production

The role of green finance in fostering high-quality economic growth must be enhanced, and the interaction of such growth with environmental protection must be fostered. To achieve competitive advantages from sustainable development, businesses should actively change their financing strategies, increase the proportion of green financial financing, and fully utilize green bonds. On the other hand, we should increase tax incentives and investment scale in green and low-carbon fields and encourage market players to actively participate in green development to enhance public awareness of environmental issues.

6.3. Limitations

This study examines the relationship between green finance, carbon emission reduction, and high-quality economic development in China. It does so by calculating the interest expense ratio of green finance, developing an index system for high-quality economic development, using the method of carbon productivity to measure the effect of carbon emission reduction, establishing an econometric model, and obtaining hypothetical results. However, it is very challenging to evaluate the development level of green funding in more depth given the dearth of trustworthy data measuring indicators and the fact that the provincial data used in this study only covers the years 2008 through 2019. Another factor that may be lacking for high-quality economic development is a consistent and well-defined index system and measuring technique. In future research, we should improve the theoretical model derivation and data comprehensiveness.

{kind=link}