Sustainability Reporting during the Crisis—What Was Disclosed by Companies in Response to the COVID-19 Pandemic Based on Evidence from Poland

Abstract

:1. Introduction

2. Literature Review

- Whether and in what context information on the COVID-19 pandemic was disclosed in the letters from the top management?

- Whether in the analyzed reports there were separate sections/chapters dedicated exclusively to issues related to the pandemic and, if so, what they covered?

- Whether and how the impact of the pandemic on the economic conditions and business activity of companies was described and whether specific changes were disclosed in the business strategies to respond to the pandemic?

- Whether and how the impact of the pandemic on companies’ environmental performance was described and whether any environmental activities to respond to the pandemic were disclosed?

- Whether and how the impact of the pandemic on the safety and well-being of employees was described and whether any activities to improve it were disclosed?

- Whether and how the impact of the pandemic on the companies’ community and stakeholder engagement was described and whether any activities in this area were disclosed that addressed issues related to the pandemic?

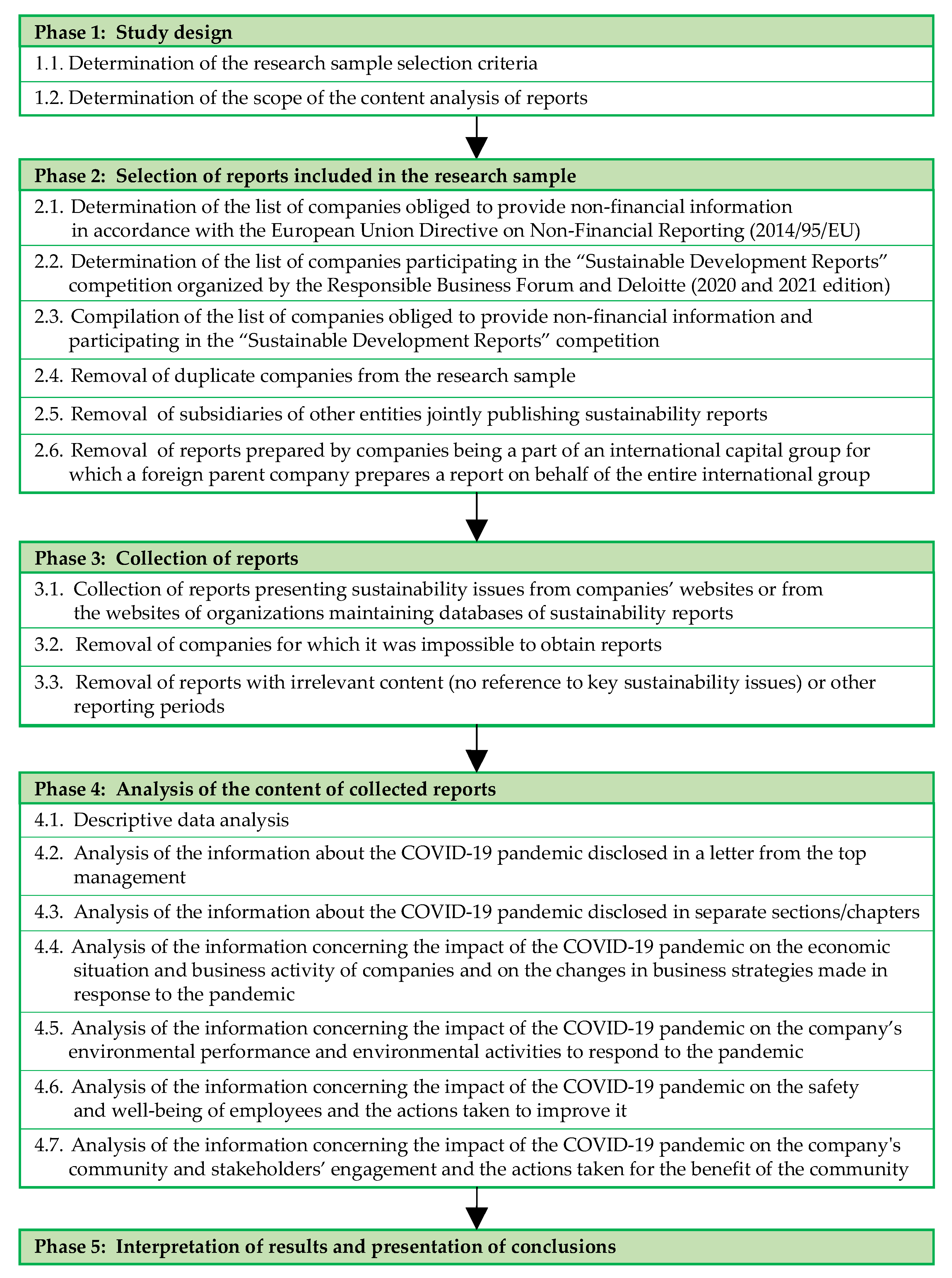

3. Materials and Methods

- Phase 1: Study design,

- Phase 2: Selection of reports included in the research sample,

- Phase 3: Collection of reports,

- Phase 4: Analysis of the content of collected reports, and

- Phase 5: Interpretation of results and presentation of conclusions.

3.1. Study Design

3.2. Selection of Reports Included in the Research Sample

3.3. Collection of Reports

3.4. Analysis of the Content of Collected Reports

4. Results and Discussion

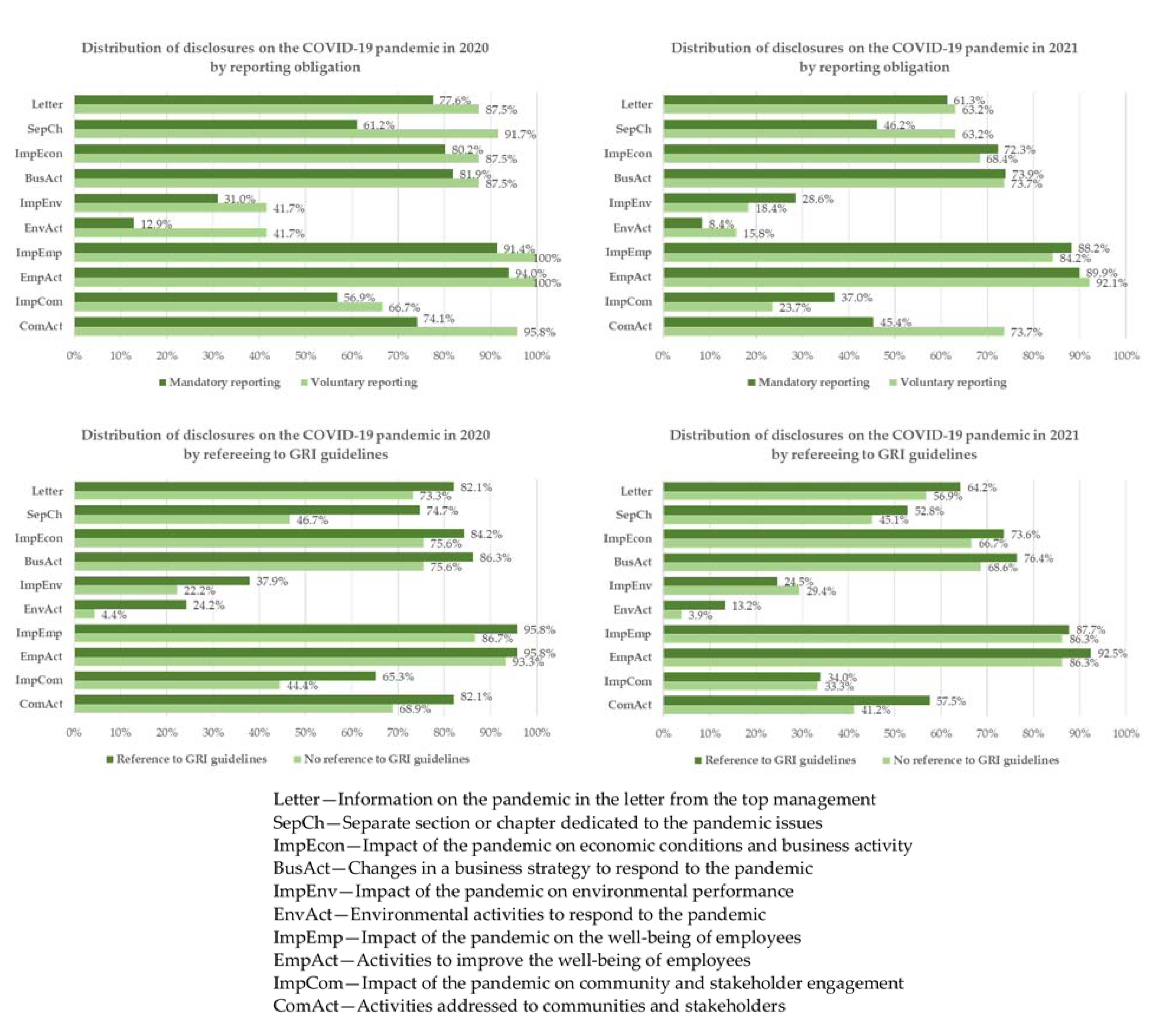

4.1. Descriptive Analysis of Disclosures on the COVID-19 Pandemic in the Analyzed Sustainability Reports

- Statements on the pandemic in the letter from the top management (Letter);

- Separate section/chapter dedicated to pandemic issues (SepCh);

- Impact of the pandemic on economic conditions and business activity (ImpEcon);

- Changes in the business strategy to respond to the pandemic (BusAct);

- Impact of the pandemic on environmental performance (ImpEnv);

- Environmental activities to respond to the pandemic (EnvAct);

- Impact of the pandemic on the well-being of employees (ImpEmp);

- Activities to improve the safety and well-being of employees (EmpAct);

- Impact of the pandemic on community and stakeholder engagement (ImpCom);

- Activities addressed to communities and stakeholders (ComAct).

4.2. Information Related to the COVID-19 Pandemic Disclosed in Letters from Top Management

4.3. Chapters and Sections in the Analyzed Sustainability Reports Dedicated to COVID-19 Pandemic Issues

4.4. Disclosures on the Impact of the COVID-19 Outbreak on Economic Conditions and Business Activity of Companies, and Changes in Business Strategies to Respond to the Pandemic

4.5. Disclosures on the Impact of the COVID-19 Outbreak on Companies’ Environmental Performance and Environmental Activities to Respond to the Pandemic

4.6. Disclosures on the Impact of the COVID-19 Pandemic on the Safety and Well-Being of Employees and Activities to Improve It

4.7. Disclosures on the Impact of the COVID-19 Pandemic on the Companies’ Community and Stakeholder Engagement and on the Activities concerning Social Involvement

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Company Name | Sustainability Impact | Activity Type | Report Type | Reporting Period | Reporting Obligation | REFERENCE to GRI Guidelines |

|---|---|---|---|---|---|---|

| AC SA | Group 2: Industrial | Manufacturer of gas installations, electronics and wiring harnesses for cars | Non-financial Statement (2020) Non-financial Statement (2021) | 2020–2021 | Yes | No |

| Ambra SA | Group 1: Basic materials and needs | Producer, importer and distributor of wines and other alcohols | Non-financial Report (2020) Non-financial Report (2021) | 07.2019–06.2022 | Yes | No |

| Amica SA | Group 4: Other services and light manufacturing | Manufacturer of household appliances | Non-financial Statement (2020) Non-financial Statement (2021) | 2020–2021 | Yes | Yes |

| ArcelorMittal Poland | Group 1: Basic materials and needs | Producer of steel and coke | Sustainability Report (2020) Sustainability Report (2021) | 2020–2021 | No | Yes |

| Arctic Paper SA | Group 1: Basic materials and needs | Producer of paper | CSR Report (2020) Sustainability Report (2021) | 2020–2021 | Yes | Yes |

| ASBISc Enterprises | Group 4: Other services and light manufacturing | Distributor of IT products | Non-financial Report (2020) Non-financial Report (2021) | 2020–2021 | Yes | No |

| Bank Gospodarstwa Krajowego | Group 1: Basic materials and needs | Banking and financial services company | Sustainability Report (2020) Sustainability Report (2021) | 2020–2021 | No | Yes |

| Carlsberg Polska | Group 1: Basic materials and needs | Beer producer | Sustainability Report (2020) ESG Report (2021) | 2020–2021 | Yes | Yes |

| CEMEX | Group 2: Industrial | Producer of cement, ready-mix concrete and aggregates | Integrated Report (2020) Sustainability Report (2021) | 2020–2021 | No | Yes |

| Credit Agricole Bank Polska SA | Group 1: Basic materials and needs | Banking and financial services company | CSR Report (2020) CSR Report (2021) | 2020–2021 | No | Yes |

| Emitel | Group 3: Transport, infrastructure and tourism | Operator of terrestrial radio and television infrastructure in Poland | CSR Report (2020) ESG Report (2021) | 2020–2021 | No | Yes |

| Fiberhost | Group 3: Transport, infrastructure and tourism | Construction, maintenance and management of open fiber optic networks, and provision of telecommunications services | CSR Report (2021) | 2021 | No | No |

| Firma Oponiarska “Dębica” SA | Group 2: Industrial | Tire manufacturer | Non-financial Statement (2020) Non-financial Statement (2021) | 2020–2021 | Yes | Yes |

| Fundacja Dorastaj z nami | Group 4: Other services and light manufacturing | Foundation supporting children of public service representatives who died or were injured in the performance of their duties | Sustainability Report (2021) | 2021 | No | Yes |

| Gdańsk Transport Company | Group 3: Transport, infrastructure and tourism | Operator of A1 Motorway | Sustainability Report (2020) Sustainability Report (2021) | 2020–2021 | No | Yes |

| GK Action SA | Group 4: Other services and light manufacturing | Wholesale company (Manufacturer and distributor in the areas of ICT, smart home and PV solutions) | Non-financial Statement (2020) Non-financial Statement (2021) | 2020–2021 | Yes | No |

| GK Agora | Group 3: Transport, infrastructure and tourism | Media company | CSR Report (2020) CSR Report (2021) | 2020–2021 | Yes | Yes |

| GK Alior Bank | Group 1: Basic materials and needs | Banking and financial services company | Non-financial Report (2020) Non-financial Report (2021) | 2020–2021 | Yes | No |

| GK Arteria SA | Group 3: Transport, infrastructure and tourism | Group of companies offering comprehensive solutions in the area of outsourcing contact center services, marketing as well as sales and logistics support | Non-financial Statement (2021) | 2021 | Yes | No |

| GK Bank Ochrony Środowiska SA | Group 1: Basic materials and needs | Banking and financial services company | Non-financial Statement (2020) ESG Report (2021) | 2020–2021 | Yes | Yes |

| GK Banku Handlowego w Warszawie SA | Group 1: Basic materials and needs | Banking and financial services company | Non-financial Report (2020) Non-financial Report(2021) | 2020–2021 | Yes | Yes |

| GK Banku Pekao SA | Group 1: Basic materials and needs | Banking and financial services company | Non-financial Report (2020) Non-financial Report (2021) | 2020–2021 | Yes | Yes |

| GK Best | Group 1: Basic materials and needs | leaders in the debt collection industry | Non-financial Report (2020) Non-financial Report (2021) | 2020–2021 | Yes | Yes |

| GK Bioton SA | Group 2: Industrial | Biotechnology company providing solutions for diabetes care | Non-financial Statement (2020) Non-financial Statement (2021) | 2020–2021 | Yes | Yes |

| GK BNP Paribas Bank Polska | Group 1: Basic materials and needs | Banking and financial services company | CSR Report (2020) ESG Report (2021) | 2020–2021 | Yes | Yes |

| GK Boryszew | Group 2: Industrial | Manufacturer of components for cars, steel products and industrial chemical, and non-ferrous metals processing | Non-financial Report (2020) Non-financial Report (2021) | 2020–2021 | Yes | Yes |

| GK Bumech | Group 1: Basic materials and needs | Mining hard coal, providing services in the field of drilling underground workings and production, service and repair of mining equipment and machinery | Non-financial Statement (2020) Non-financial Statement (2021) | 2020–2021 | Yes | No |

| GK CD Projekt | Group 3: Transport, infrastructure and tourism | Production and publishing of video games and related products | Sustainability Report (2021) | 2021 | Yes | Yes |

| GK CDRL SA | Group 1: Basic materials and needs | Production and sale of clothing | Non-financial Report (2020) Non-financial Report (2021) | 2020–2021 | Yes | Yes |

| GK Cognor | Group 1: Basic materials and needs | Producer of raw steel (semi-finished, billet) and metallurgical final products | Integrated Report (2020) Integrated Report (2021) | 2020–2021 | Yes | Yes |

| GK Columbus Energy | Group 1: Basic materials and needs | Provider of services on the modern energy market (photovoltaics, heat pumps, energy storage or electric vehicle chargers) | Sustainability Report (2021) | 2021 | No | Yes |

| GK Comp | Group 3: Transport, infrastructure and tourism | Group consisting of technology companies specializing in IT, network and cryptography security solutions as well as solutions for trade and services | Non-financial Report (2020) Non-financial Report (2021) | 2020–2021 | Yes | Yes |

| GK Decora | Group 4: Other services and light manufacturing | Production and distribution of interior decoration articles | Sustainability Report (2019–2020) Sustainability Report (2021) | 2019–2021 | Yes | Yes |

| GK Dekpol | Group 2: Industrial | Construction, real estate development and production of accessories for construction machines | Non-financial Report (2020) Non-financial Report (2021) | 2020–2021 | Yes | Yes |

| GK Delko SA | Group 4: Other services and light manufacturing | Wholesale and retail trade in hygienic, chemical and food products | Non-financial Report (2020) Non-financial Report (2021) | 2020–2021 | Yes | No |

| GK Dino Polska SA | Group 4: Other services and light manufacturing | Chain of supermarkets | Non-financial Statement (2020) Non-financial Statement (2021) | 2020–2021 | Yes | No |

| GK Elektrotim | Group 2: Industrial | Contractor of electrical and power installations and networks, automation systems for construction, industry and energy | Non-financial Statement (2020) Non-financial Statement (2021) | 2020–2021 | Yes | No |

| GK Enea | Group 1: Basic materials and needs | Energy sector company | Non-financial Statement (2020) Non-financial Statement (2021) | 2020–2021 | Yes | Yes |

| GK Enel-Med | Group 4: Other services and light manufacturing | Private operator of medical services | Non-financial Report (2020) Non-financial Report (2021) | 2020–2021 | Yes | No |

| GK Fabryka Farb i Lakierów Śnieżka SA | Group 2: Industrial | Manufacturer of paints and varnishes | Non-financial Statement (2020) Non-financial Statement (2021) | 2020–2021 | Yes | No |

| GK Fabryki Mebli “Forte” | Group 4: Other services and light manufacturing | Furniture manufacturer | Non-financial Report (2020) Non-financial Report (2021) | 2020–2021 | Yes | No |

| GK Fasing SA | Group 2: Industrial | Manufacturing of industrial chains | Non-financial Report (2020) Non-financial Report (2021) | 2020–2021 | Yes | No |

| GK Gaz System | Group 1: Basic materials and needs | Transmission Gas Pipeline Operator | Sustainability Report (2020) Sustainability Report (2021) | 2020–2021 | No | Yes |

| GK Gobarto | Group 1: Basic materials and needs | Slaughter, cutting and distribution of meat | Non-financial Report (2020) Non-financial Report (2021) | 2020–2021 | Yes | Yes |

| GK Hydrotor | Group 2: Industrial | Manufacturing of power hydraulics | Non-financial Report (2019–2020) Non-financial Report (2021) | 2019–2021 | Yes | No |

| GK Immobile | Group 2: Industrial | Group operating in electromechanical industry, hotel industry, construction investments, industrial construction, real estate rental and clothing industry | Non-financial Report (2020) Non-financial Report (2021) | 2020–2021 | Yes | No |

| GK ING Bank Śląski SA | Group 1: Basic materials and needs | Universal bank | Integrated Report (2020) Integrated Report (2021) | 2020–2021 | Yes | Yes |

| GK Inter Cars | Group 2: Industrial | Wholesale of parts and accessories for motor vehicles | Sustainability Report (2020) Sustainability Report (2021) | 2020–2021 | Yes | Yes |

| GK Komputronik | Group 4: Other services and light manufacturing | Retail sale of computers, peripherals and software | Non-financial Report (2020/2021) Non-financial Report (2021/2022) | 04.2020–03.2022 | Yes | No |

| GK Lentex | Group 2: Industrial | Manufacturing of floor coverings and nonwovens | Non-financial Report (2020) Non-financial Report (2021) | 2020–2021 | Yes | No |

| GK Lubawa | Group 1: Basic materials and needs | Production, processing and sale of fabrics and knitted fabrics | Sustainability Report (2020) Sustainability Report (2021) | 2020–2021 | Yes | Yes |

| GK Lubelski Węgiel Bogdanka | Group 1: Basic materials and needs | Coal mining company | Integrated Report (2020) Integrated Report (2021) | 2020–2021 | Yes | Yes |

| GK LUG SA | Group 2: Industrial | Manufacturing of professional lighting systems | Non-financial Report (2020) Non-financial Report (2021) | 2020–2021 | No | No |

| GK Mangata Holding | Group 2: Industrial | Manufacturing of automotive industry components, fasteners, industrial valves and automation | Non-financial Report (2020) Non-financial Report (2021) | 2020–2021 | Yes | No |

| GK Mercator Medical SA | Group 4: Other services and light manufacturing | Manufacturing of disposable personal protective equipment for medical purposes and surgical drapes | Non-financial Report (2020) Non-financial Report (2021) | 2020–2021 | Yes | No |

| GK Mercor SA | Group 4: Other services and light manufacturing | Producer of passive fire protection systems | Non-financial Report (2020) Non-financial Report (2021) | 04.2020–03.2022 | Yes | No |

| GK Mirbud | Group 2: Industrial | Construction company | Non-financial Report (2020) Non-financial Report (2021) | 2020–2021 | Yes | Yes |

| GK Monnari Trade SA | Group 1: Basic materials and needs | Designing and sale of women’s clothing | Non-financial Report (2020) Non-financial Report (2021) | 2020–2021 | Yes | Yes |

| GK Mostostal Warszawa | Group 2: Industrial | Construction company | Non-financial Statement (2020) Non-financial Statement (2021) | 2020–2021 | Yes | Yes |

| GK Newag | Group 2: Industrial | Production, maintenance, and modernization of railway rolling stock | Non-financial Report (2020) Non-financial Report (2021) | 2020–2021 | Yes | No |

| GK Orange Polska | Group 3: Transport, infrastructure and tourism | Telecommunications service provider | Integrated Report (2020) Integrated Report (2021) | 2020–2021 | No | Yes |

| GK OT Logistics | Group 3: Transport, infrastructure and tourism | Transport and logistics services | Non-financial Statement (2020) Non-financial Statement (2021) | 2020–2021 | Yes | No |

| GK Otmuchów | Group 1: Basic materials and needs | Food industry of confectioneries | Non-financial Statement (2020) | 2020 | Yes | No |

| GK Pamapol | Group 1: Basic materials and needs | Meat and vegetable processing | Non-financial Report (2020) Non-financial Report (2021) | 2020–2021 | Yes | Yes |

| GK PCC Rokita | Group 2: Industrial | Manufacturing of specialized chemical products and industrial formulations | Non-financial Statement (2020) Non-financial Statement (2021) | 2020–2021 | Yes | No |

| GK PGE | Group 1: Basic materials and needs | Energy sector company | Non-financial Report (2020) Non-financial Report (2021) | 2020–2021 | Yes | Yes |

| GK PKN Orlen SA | Group 1: Basic materials and needs | Integrated, multi-utility company providing energy and fuel | Non-financial Report (2020) Non-financial Report (2021) | 2020–2021 | Yes | Yes |

| GK PKO BP SA | Group 1: Basic materials and needs | Banking and financial services company | Non-financial Statement (2020) Non-financial Statement (2021) | 2020–2021 | Yes | Yes |

| GK Polimex Mostostal | Group 2: Industrial | Engineering and industrial construction company | Non-financial Report (2020) Non-financial Report (2021) | 2020–2021 | Yes | Yes |

| GK Polsat Plus | Group 3: Transport, infrastructure and tourism | Provider of integrated media and telecommunications services | CSR Report (2020) Sustainability Report (2021) | 2020–2021 | Yes | Yes |

| GK Polski Holding Nieruchomości SA | Group 3: Transport, infrastructure and tourism | Real estate management and investment project implementation | Non-financial Report (2020) Non-financial Report (2021) | 2020–2021 | Yes | No |

| GK Protektor | Group 1: Basic materials and needs | Manufacturer and distributor of footwear | Non-financial Statement (2020) Non-financial Statement (2021) | 2020–2021 | Yes | No |

| GK PZU | Group 1: Basic materials and needs | Insurance company | Non-financial Report (2020) Integrated Report (2021) | 2020–2021 | Yes | Yes |

| GK Rafamet | Group 2: Industrial | Manufacturing of special-purpose machine tools for wheelset machining | Non-financial Statement (2020) Non-financial Statement (2021) | 2020–2021 | Yes | No |

| GK Rainbow Tours | Group 4: Other services and light manufacturing | Tour operator | Non-financial Report (2020) Non-financial Report (2021) | 2020–2021 | Yes | Yes |

| GK Relpol SA | Group 2: Industrial | Manufacturing of relays and control equipment | Non-financial Statement (2020) Non-financial Statement (2021) | 2020–2021 | Yes | Yes |

| GK ROBYG SA | Group 3: Transport, infrastructure and tourism | Real estate developer | ESG Report (2021) | 2021 | No | Yes |

| GK Seco/Warwick SA | Group 2: Industrial | Manufacturing of solutions for heat treatment of metals | Non-financial Statement (2020) Non-financial Statement (2021) | 2020–2021 | Yes | Yes |

| GK Solar Company SA | Group 1: Basic materials and needs | Designing and production of original collections of women’s clothing and clothing accessories | Non-financial Statement (2020) Non-financial Statement (2021) | 2020–2021 | Yes | No |

| GK Stalprofil SA | Group 4: Other services and light manufacturing | Distribution of steel and metallurgical products | Non-financial Report (2020) Non-financial Report (2021) | 2020–2021 | Yes | No |

| GK SuperDrob | Group 1: Basic materials and needs | Production and sale of poultry products | Sustainability Report (2020–2021) | 2020–2021 | No | Yes |

| GK Tarczyński SA | Group 1: Basic materials and needs | Production, processing and preservation of meat | Non-financial Statement (2020) Non-financial Statement (2021) | 2020–2021 | Yes | Yes |

| GK Tauron Polska Energia SA | Group 1: Basic materials and needs | Energy holding company | Non-financial Report (2020) Non-financial Report (2021) | 2020–2021 | Yes | Yes |

| GK TIM | Group 4: Other services and light manufacturing | Wholesale distributor of electrotechnical goods | Non-financial Statement (2020) Integrated Report (2021) | 2020–2021 | Yes | Yes |

| GK Torpol | Group 2: Industrial | Construction, modernization and repairs of railway infrastructure | Sustainability Report (2020) Sustainability Report (2021) | 2020–2021 | Yes | Yes |

| GK Unibep | Group 2: Industrial | Construction company | Sustainability Report (2020) Sustainability Report (2021) | 2020–2021 | Yes | Yes |

| GK Voxel SA | Group 4: Other services and light manufacturing | Highly specialized medical diagnostic services | Non-financial Report (2021) | 2021 | Yes | No |

| GK VRG SA | Group 1: Basic materials and needs | Designing and distributing fashion collections for men and women, as well as jewelry and watches | Non-financial Report (2020) Non-financial Report (2021) | 2020–2021 | Yes | No |

| GK WASKO SA | Group 3: Transport, infrastructure and tourism | Information and communication technologies | Non-financial Statement (2020) Non-financial Statement (2021) | 2020–2021 | Yes | No |

| GK Wojas | Group 1: Basic materials and needs | Leather footwear manufacturing | Non-financial Report (2020) Non-financial Report (2021) | 2020–2021 | Yes | Yes |

| GK Zakłady Magnezytowe Ropczyce | Group 1: Basic materials and needs | Manufacturing of high-quality basic and aluminosilicate refractory materials | Non-financial Statement (2020) Non-financial Statement (2021) | 2020–2021 | Yes | Yes |

| GK ZE PAK SA | Group 1: Basic materials and needs | Electricity production | Non-financial Statement (2020) Non-financial Statement (2021) | 2020–2021 | Yes | Yes |

| GK ZUE | Group 3: Transport, infrastructure and tourism | Transport and railway infrastructure construction | Non-financial Statement (2020) Non-financial Statement (2021) | 2020–2021 | Yes | No |

| Globe Trade Centre | Group 3: Transport, infrastructure and tourism | Real estate developer | ESG Report (2020) ESG Report (2021) | 2020–2021 | No | Yes |

| Grupa 7R | Group 3: Transport, infrastructure and tourism | Rental of warehouse space | ESG Report (2021) | 2021 | No | Yes |

| Grupa AB | Group 4: Other services and light manufacturing | Chain of specialized shops offering consumer electronics and home appliances | Non-financial Report (07.2019–06.2020) Non-financial Report (07.2020–06.2021) Non-financial Report (07.2021–06.2022) | 07.2019–06.2022 | Yes | No |

| Grupa Allegro EU SA | Group 4: Other services and light manufacturing | Trading platform | ESG Report (2021) | 2021 | No | Yes |

| Grupa Alumetal | Group 1: Basic materials and needs | Producer of primary and secondary aluminum casting alloys | Non-financial Statement (2020) Non-financial Statement (2021) | 2020–2021 | Yes | No |

| Grupa Apator | Group 4: Other services and light manufacturing | Group of manufacturers and distributors of measuring devices and systems, as well as suppliers of solutions supporting the operation of electricity, water and gas networks | Non-financial Report (2020) Non-financial Report (2021) | 2020–2021 | Yes | Yes |

| Grupa Asseco Poland | Group 3: Transport, infrastructure and tourism | Software company | Non-financial Report (2020) Non-financial Report (2021) | 2020–2021 | Yes | Yes |

| Grupa Auto Partner SA | Group 2: Industrial | Importer and distributor of spare parts for cars, vans and motorcycles | Non-financial Report (2020) Non-financial Report (2021) | 2020–2021 | Yes | Yes |

| Grupa Azoty SA | Group 2: Industrial | Fertilizer and chemical industry company | Integrated Report (2020) Integrated Report (2021) | 2020–2021 | Yes | Yes |

| Grupa Banku Milennium | Group 1: Basic materials and needs | Banking and financial services company | Non-financial Report (2020) ESG Report (2021) | 2020–2021 | Yes | Yes |

| Grupa Benefit Systems | Group 4: Other services and light manufacturing | Healthy lifestyle, physical recreation, culture and entertainment, and adapted cafeteria programs | Non-financial Report (2020) Non-financial Report (2021) | 2020–2021 | Yes | Yes |

| Grupa Budimex | Group 2: Industrial | Construction company | Integrated Report (2020) Integrated Report (2021) | 2020–2021 | Yes | Yes |

| Grupa CCC | Group 4: Other services and light manufacturing | Retail sale of footwear | Non-financial Report (01.2020–01.2021) Sustainability Report (02.2021–01.2022) | 2020–2021 | No | Yes |

| Grupa Ciech | Group 2: Industrial | Chemical industry company | Non-financial Report (2020) Non-financial Report (2021) | 2020–2021 | Yes | Yes |

| Grupa Comarch | Group 3: Transport, infrastructure and tourism | Producer of innovative IT systems for key sectors of the economy both in Poland and abroad | Non-financial Report (2020) Non-financial Report (2021) | 2020–2021 | Yes | No |

| Grupa Echo Investment | Group 3: Transport, infrastructure and tourism | Real estate developer | Sustainability Report (2020) Sustainability Report (2021) | 2020–2021 | No | Yes |

| Grupa EMC Instytut Medyczny SA | Group 4: Other services and light manufacturing | Health care services (the owner of hospitals and clinics on the market of private medical services) | Non-financial Statement (2020) Non-financial Statement (2021) | 2020–2021 | Yes | No |

| Grupa Energa | Group 1: Basic materials and needs | Energy sector company | Non-financial Report (2020) Non-financial Report (2021) | 2020–2021 | Yes | Yes |

| Grupa Eneris | Group 1: Basic materials and needs | Company specializing in environmental protection: waste and raw material management, water and sewage management and renewable energy | Sustainability Report (2019–2020) | 2019–2020 | No | Yes |

| Grupa Erbud | Group 2: Industrial | Construction company | Integrated Report (2020) | 2020 | Yes | Yes |

| Grupa Ergo Hestia | Group 1: Basic materials and needs | Insurance company | Sustainability Report (2020) Sustainability Report (2021) | 2020–2021 | No | Yes |

| Grupa Eurocash | Group 1: Basic materials and needs | Wholesale distributor of FMCG products | CSR Report (2020) CSR Report (2021) | 2020–2021 | Yes | Yes |

| Grupa Famur | Group 1: Basic materials and needs | Manufacturer of machines and systems used in underground mining and supplier of related aftermarket services | Non-financial Statement (2020) Integrated Report (2021) | 2020–2021 | Yes | Yes |

| Grupa Introl | Group 2: Industrial | Installing industrial machinery, equipment and fittings | Non-financial Statement (2021) | 2021 | Yes | No |

| Grupa Kęty SA | Group 1: Basic materials and needs | Aluminum processing | Non-financial Statement (2020) Non-financial Statement (2021) | 2020–2021 | Yes | Yes |

| Grupa KGHM Polska Miedź SA | Group 1: Basic materials and needs | Production of copper and silver | Integrated Report (2020) Integrated Report (2021) | 2020–2021 | Yes | Yes |

| Grupa KOM-EKO | Group 1: Basic materials and needs | Waste disposal and cleaning | ESG Report (2021) | 2021 | No | No |

| Grupa Kruk | Group 1: Basic materials and needs | Debt collection and management of receivables | Non-financial Statement (2020) Sustainability Report (2021) | 2020–2021 | Yes | Yes |

| Grupa Makarony Polskie | Group 1: Basic materials and needs | Production of pasta | Non-financial Statement (2020) Non-financial Statement (2021) | 2020–2021 | Yes | No |

| Grupa Mostostal Zabrze | Group 2: Industrial | Industrial construction | Non-financial Statement (2020) Non-financial Statement (2021) | 2020–2021 | Yes | Yes |

| Grupa Neuca | Group 4: Other services and light manufacturing | Wholesale of pharmaceutical and medical products | Non-financial Report (2020) Non-financial Report (2021) | 2020–2021 | Yes | No |

| Grupa OEX | Group 4: Other services and light manufacturing | Retail and e-commerce services | Non-financial Report (2020) Non-financial Report (2021) | 2020–2021 | Yes | No |

| Grupa Pekabex | Group 2: Industrial | Designing, production and assembly of facility structures based on prefabrication technology | Integrated Report (2020) Integrated Report (2021) | 2020–2021 | Yes | Yes |

| Grupa PKP Cargo | Group 3: Transport, infrastructure and tourism | Railway freight carrier | Non-financial Statement (2020) Non-financial Statement (2021) | 2020–2021 | Yes | Yes |

| Grupa Rafako SA | Group 2: Industrial | Manufacturing of technological solutions related to power generation and environment protection | Non-financial Report (2020) Non-financial Report (2021) | 2020–2021 | Yes | Yes |

| Grupa Sygnity | Group 3: Transport, infrastructure and tourism | IT company | Non-financial Report (2020) Non-financial Report (2021) | 10.2019–09.2021 | Yes | No |

| Grupa Trakcja | Group 2: Industrial | Construction and modernizing of railway and road infrastructure | Non-financial Report (2020) Non-financial Report (2021) | 2020–2021 | Yes | No |

| Grupa UNIMOT | Group 1: Basic materials and needs | Wholesale of liquid and gas fuels | ESG Report (2021) | 2021 | No | Yes |

| Grupa VELUX | Group 4: Other services and light manufacturing | Roof windows manufacturing | Sustainability Report (2020–2021) | 2020–2021 | No | Yes |

| Grupa Zamet | Group 1: Basic materials and needs | Equipment for metallurgical and mining industry and large-size steel structures | Non-financial Report (2021) | 2021 | Yes | No |

| Grupa Żabka | Group 4: Other services and light manufacturing | Convenience stores | CSR Report (2021) | 2021 | No | Yes |

| Grupa Żywiec SA | Group 1: Basic materials and needs | Beer producer | Non-financial Report (2020) Non-financial Report (2021) | 2020–2021 | No | Yes |

| Jeronimo Martins Polska | Group 4: Other services and light manufacturing | Chain of supermarkets | Sustainability Report (2020) Sustainability Report (2021) | 2020–2021 | No | Yes |

| JSW SA | Group 1: Basic materials and needs | Coal mining company | Sustainability Report (2020) Integrated Report (2021) | 2020–2021 | Yes | Yes |

| Kaufland Polska | Group 4: Other services and light manufacturing | Hypermarket chain | Sustainability Report (2020–2021) | 2020–2021 | No | Yes |

| Kompania Piwowarska | Group 1: Basic materials and needs | Brewing group | Sustainability Report (2020) Sustainability Report (2021) | 2020–2021 | No | Yes |

| Korporacja KGL SA | Group 3: Transport, infrastructure and tourism | Manufacturing of plastic food packaging and production tools | Non-financial Statement (2020) Non-financial Statement (2021) | 2020–2021 | Yes | No |

| KPPD Szczecinek SA | Group 1: Basic materials and needs | Acquisition and production of wood and wood-based products | Non-financial Report (2020) Non-financial Report (2021) | 2020–2021 | Yes | Yes |

| Leroy Merlin Polska | Group 4: Other services and light manufacturing | Home improvement and gardening retailer | CSR Report (2021) | 2021 | No | Yes |

| Lidl Polska | Group 4: Other services and light manufacturing | Discount retailer chain | Sustainability Report (2019–2021) | 03.2019–02.2021 | No | Yes |

| LPP SA | Group 1: Basic materials and needs | Designing, production and distribution of clothing | Integrated Report (2020) Sustainability Report (2021) | 02.2020–01.2022 | Yes | Yes |

| mBank SA | Group 1: Basic materials and needs | Universal bank | Integrated Report (2020) Integrated Report (2021) | 2020–2021 | Yes | Yes |

| McDonald’s Polska | Group 4: Other services and light manufacturing | Fast food chain | ESG Report (2021) | 2021 | No | Yes |

| Odlewnie Polskie SA | Group 1: Basic materials and needs | Manufacturing of ADI cast iron and nodular cast iron | Non-financial Statement (2020) Non-financial Statement (2021) | 2020–2021 | Yes | No |

| PKP Energetyka | Group 1: Basic materials and needs | Electricity distributor to railway network and other business customers | ESG Report (2021) | 2021 | No | Yes |

| Raben | Group 3: Transport, infrastructure and tourism | Logistics company | Sustainability Report (2020) Sustainability Report (2021) | 2020–2021 | No | Yes |

| Rawlplug SA | Group 2: Industrial | Manufacturing of tools, fasteners and fixings | Sustainability Report (2020) Sustainability Report (2021) | 2020–2021 | Yes | Yes |

| Sanok Rubber Company SA | Group 2: Industrial | Rubber products and rubber compounds manufacturing | Non-financial Report (2020) Non-financial Report (2021) | 2020–2021 | Yes | Yes |

| Santander Bank Polska SA | Group 1: Basic materials and needs | Universal bank | ESG Report (2020) ESG Report (2021) | 2020–2021 | Yes | Yes |

| Solaris Bus & Coach Sp. Z o.o. | Group 2: Industrial | Bus and trolleybus manufacturer | Sustainability Report (2020) Sustainability Report (2021) | 2020–2021 | No | Yes |

| T-Mobile Polska | Group 3: Transport, infrastructure and tourism | Mobile network operator | Sustainability Report (2021) | 2021 | No | Yes |

| Totalizator Sportowy | Group 4: Other services and light manufacturing | Number games and cash lotteries | Integrated Report (2021) | 2021 | No | Yes |

| Vantage Development | Group 3: Transport, infrastructure and tourism | Real estate developer | ESG Report (2021) | 2021 | No | Yes |

| VGL Solid Group | Group 3: Transport, infrastructure and tourism | Truck transportation and services in logistics | CSR Report (2021) | 2021 | No | No |

| Wawel SA | Group 1: Basic materials and needs | Confectionery manufacturing | Non-financial Report (2020) Non-financial Report (2021) | 2020–2021 | Yes | No |

| Wielton SA | Group 2: Industrial | Manufacturing of semi-trailers, trailers and car bodies | Non-financial Report (2020) Non-financial Report (2021) | 2020–2021 | Yes | Yes |

| Wirtualna Polska Holding SA | Group 3: Transport, infrastructure and tourism | e-commerce, advertising and media activities | Non-financial Statement (2020) Non-financial Statement (2021) | 2020–2021 | Yes | Yes |

| Zarząd Transportu Metropolitalnego | Group 3: Transport, infrastructure and tourism | Collective public transport | CSR Report (2020) | 2020 | No | Yes |

References

- Clemente-Suárez, V.J.; Navarro-Jiménez, E.; Moreno-Luna, L.; Saavedra-Serrano, M.C.; Jimenez, M.; Simón, J.A.; Tornero-Aguilera, J.F. The Impact of the COVID-19 Pandemic on Social, Health, and Economy. Sustainability 2021, 13, 6314. [Google Scholar] [CrossRef]

- Nicola, M.; Alsafi, Z.; Sohrabi, C.; Kerwan, A.; Al-Jabir, A.; Iosifidis, C.; Agha, M.; Agha, R. The socio-economic implications of the coronavirus pandemic (COVID-19): A review. Int. J. Surg. 2020, 78, 185–193. [Google Scholar] [CrossRef]

- Gujski, M.; Raciborski, F.; Jankowski, M.; Nowicka, P.M.; Rakocy, K.; Pinkas, J. Epidemiological analysis of the first 1389 cases of COVID-19 in Poland: A preliminary report. Med. Sci. Monit. 2020, 26, e924702. [Google Scholar] [CrossRef] [PubMed]

- Akhtaruzzaman, M.; Boubaker, S.; Umar, Z. COVID-19 media coverage and ESG leader indices. Financ. Res. Lett. 2022, 45, 102170. [Google Scholar] [CrossRef]

- Chowdhury, M.T.; Sarkar, A.; Paul, S.K.; Moktadir, M.A. A case study on strategies to deal with the impacts of COVID-19 pandemic in the food and beverage industry. Oper. Manag. Res. 2022, 15, 166–178. [Google Scholar] [CrossRef]

- Chudziński, P.; Cyfert, S.; Dyduch, W.; Koubaa, S.; Zastempowski, M. Strategic and entrepreneurial abilities: Surviving the crisis across countries during the COVID-19 pandemic. PLoS ONE 2023, 18, e0285045. [Google Scholar] [CrossRef]

- Grondys, K.; Ślusarczyk, O.; Hussain, H.I.; Androniceanu, A. Risk Assessment of the SME Sector Operations during the COVID-19 Pandemic. Int. J. Environ. Res. Public Health 2021, 18, 4183. [Google Scholar] [CrossRef] [PubMed]

- Milewska, B. The Impact of the COVID-19 Pandemic on Supply Chains in the Example of Polish Clothing Companies in the Context of Sustainable Development. Sustainability 2022, 14, 1899. [Google Scholar] [CrossRef]

- Veselovská, L. Supply chain disruptions in the context of early stages of the global COVID-19 outbreak. Probl. Perspect. Manag. 2020, 18, 490–500. [Google Scholar] [CrossRef]

- Nowacki, K.; Grabowska, S.; Łakomy, K. Activities of employers and OHS services during the developing COVID-19 epidemic in Poland. Saf. Sci. 2020, 131, 104935. [Google Scholar] [CrossRef] [PubMed]

- Buk, H.; Wiercioch, M. The use of IT systems in financial and accounting services for enterprises in the conditions of the COVID-19 pandemic. Procedia Comput. Sci. 2021, 192, 4112–4119. [Google Scholar] [CrossRef]

- Saputra, N.; Sasanti, N.; Alamsjah, F.; Sadeli, F. Strategic role of digital capability on business agility during COVID-19 era. Procedia Comput. Sci. 2022, 197, 326–335. [Google Scholar] [CrossRef] [PubMed]

- Khan, S.A.R.; Waqas, M.; Honggang, X.; Ahmad, N.; Yu, Z. Adoption of innovative strategies to mitigate supply chain disruption: COVID-19 pandemic. Oper. Manag. Res. 2022, 15, 1115–1133. [Google Scholar] [CrossRef]

- Urbaniec, M.; Małkowska, A.; Włodarkiewicz-Klimek, H. The Impact of Technological Developments on Remote Working: Insights from the Polish Managers’ Perspective. Sustainability 2022, 14, 552. [Google Scholar] [CrossRef]

- Liu, H.; Yi, X.; Yin, L. The impact of operating flexibility on firms’ performance during the COVID-19 outbreak: Evidence from China. Finance Res. Lett. 2021, 38, 101808. [Google Scholar] [CrossRef] [PubMed]

- Trabucco, M.; de Giovanni, P. Achieving Resilience and Business Sustainability during COVID-19: The Role of Lean Supply Chain Practices and Digitalization. Sustainability 2021, 13, 12369. [Google Scholar] [CrossRef]

- Markovic, S.; Koporcic, N.; Arslanagic-Kalajdzic, M.; Kadic-Maglajlic, S.; Bagherzadeh, M.; Islam, N. Business-to-business open innovation: COVID-19 lessons for small and medium-sized enterprises from emerging markets. Technol. Forecast. Soc. Change 2021, 170, 120883. [Google Scholar] [CrossRef]

- Atayah, O.F.; Dhiaf, M.M.; Najaf, K.; Frederico, G.F. Impact of COVID-19 on financial performance of logistics firms: Evidence from G-20 countries. J. Glob. Oper. Strateg. Sourc. 2021, 15, 172–196. [Google Scholar] [CrossRef]

- Golubeva, O. Firms’ performance during the COVID-19 outbreak: International evidence from 13 countries. Corp. Gov. 2021, 21, 1011–1027. [Google Scholar] [CrossRef]

- Hu, S.; Zhang, Y. COVID-19 pandemic and firm performance: Cross-country evidence. Int. Rev. Econ. 2021, 74, 365–372. [Google Scholar] [CrossRef]

- Almustafa, H.; Nguyen, Q.K.; Liu, J.; Dang, V.C. The impact of COVID-19 on firm risk and performance in MENA countries: Does national governance quality matter? PLoS ONE 2023, 18, e0281148. [Google Scholar] [CrossRef] [PubMed]

- Milewski, D.; Milewska, B. The Energy Efficiency of the Last Mile in the E-Commerce Distribution in the Context the COVID-19 Pandemic. Energies 2021, 14, 7863. [Google Scholar] [CrossRef]

- Zhang, T.; Gerlowski, D.; Acs, Z. Working from home: Small business performance and the COVID-19 pandemic. Small Bus. Econ. 2022, 58, 611–636. [Google Scholar] [CrossRef]

- Amore, M.D.; Pelucco, V.; Quarato, F. Family ownership during the COVID-19 pandemic. J. Bank. Financ. 2022, 135, 106385. [Google Scholar] [CrossRef] [PubMed]

- Klymenko, O.; Lillebrygfjeld Halse, L. Sustainability practices during COVID-19: An institutional perspective. Int. J. Logist. Manag. 2021, 33, 1315–1335. [Google Scholar] [CrossRef]

- Carroll, A.B. Corporate Social Responsibility (CSR) and the COVID-19 Pandemic: Organizational and Managerial Implications. J. Strategy Manag. 2021, 14, 315–330. [Google Scholar] [CrossRef]

- Zyznarska-Dworczak, B. Sustainability Accounting in Times of the COVID-19 Pandemic. In Corporate Sustainability in Times of Virus Crises. Accounting, Finance, Sustainability, Governance & Fraud: Theory and Application; Çalıyurt, K.T., Ed.; Springer: Singapore, 2023; pp. 107–119. [Google Scholar] [CrossRef]

- EFRAG Draft European Sustainability Reporting Standards. Apendix VI. Acronyms and Glossary of Terms. PTF-ESRS. April 2022. Available online: https://www.efrag.org/lab6 (accessed on 12 June 2023).

- Basiago, A.D. Economic, social, and environmental sustainability in development theory and urban planning Practice. Environmentalist 1998, 19, 145–161. [Google Scholar] [CrossRef]

- Mensah, J. Sustainable development: Meaning, history, principles, pillars, and implications for human action: Literature review. Cogent Soc. Sci. 2019, 5, 1653531. [Google Scholar] [CrossRef]

- Ben-Eli, M. Sustainability: Definition and five core principles, a system perspective. Sustain. Sci. 2018, 13, 1337–1343. [Google Scholar] [CrossRef]

- Olawumi, T.O.; Chan, D.W.M. A scientometric review of global research on sustainability and sustainable development. J. Clean. Prod. 2018, 183, 231–250. [Google Scholar] [CrossRef]

- Sartori, S.; da Silva, F.L.; de Souza Campos, L.M. Sustainability and sustainable development: A taxonomy in the field of literature. Ambiente Soc. 2014, 17, 1–22. [Google Scholar] [CrossRef]

- World Commission on Environment and Development (WCED). Report Our Common Future; United Nations: New York, NY, USA, 1987; Available online: https://sustainabledevelopment.un.org/content/documents/5987our-common-future.pdf (accessed on 16 August 2023).

- Diesendorf, M. Sustainability and Sustainable Development. In Sustainability: The Corporate Challenge of the 21st Century; Dunphy, D., Benveniste, J., Griffiths, A., Sutton, P., Eds.; Allen & Unwin: Sydney, Australia, 2000; pp. 19–37. [Google Scholar]

- Gray, R. Is accounting for sustainability actually accounting for sustainability … and how would we know? An exploration of narratives of organisations and the planet. Account. Organ. Soc. 2010, 35, 47–62. [Google Scholar] [CrossRef]

- European Parliament, Council of the European Union. Directive (EU) 2022/2464 of the European Parliament and of the Council of 14 December 2022 Amending Regulation (EU) No 537/2014, Directive 2004/109/EC, Directive 2006/43/EC and Directive 2013/34/EU, as Regards Corporate Sustainability Reporting; European Parliament, Council of the European Union: Brussels, Belgium, 2022.

- Janik, A.; Ryszko, A.; Szafraniec, M. Greenhouse Gases and Circular Economy Issues in Sustainability Reports from the Energy Sector in the European Union. Energies 2020, 13, 5993. [Google Scholar] [CrossRef]

- Van der Lugt, C.; van de Wijs, P.P.; Petrovics, D. Carrots & Sticks: Sustainability Reporting Policy: Global Trends in Disclosure as the ESG Agenda Goes Mainstream. Global Reporting Initiative (GRI), the University of Stellenbosch Business School (USB). 2020. Available online: https://research.vu.nl/ws/portalfiles/portal/111479833/carrots_and_sticks_2020_interactive.pdf (accessed on 10 June 2023).

- Global Reporting Initiative. Consolidated Set of GRI Sustainability Reporting Standards 2020; Global Reporting Initiative, Global Sustainability Standards Board: Amsterdam, The Netherlands, 2020. [Google Scholar]

- United Nations Global Compact. UN Global Compact Policy on Communicating Progress; United Nations Global Compact: New York, NY, USA, 2013. [Google Scholar]

- Sustainability Accounting Standards Board. SASB Standards. Available online: https://sasb.org/standards/download/ (accessed on 10 June 2023).

- European Parliament, Council of the European Union. Directive 2014/95/EU of the European Parliament and of the Council of 22 October 2014 Amending Directive 2013/34/EU as Regards Disclosure of Non-Financial and Diversity Information by Certain Large Undertakings and Groups; European Parliament, Council of the European Union: Brussels, Belgium, 2014.

- European Parliament, Council of the European Union. Regulation (EU) 2019/2088 of the European Parliament and of the Council of 27 November 2019 on Sustainability-Related Disclosures in the Financial Services Sector; European Parliament, Council of the European Union: Brussels, Belgium, 2019.

- Scarpa, F.; Torelli, R.; Fiandrino, S. Business engagement for the SDGs in COVID-19 time: An Italian perspective. Sustain. Account. Manag. Policy J. 2023, 14, 152–178. [Google Scholar] [CrossRef]

- Yadav, H.; Kar, A.K.; Kashiramka, S. How does entrepreneurial orientation and SDG orientation of CEOs evolve before and during a pandemic. J. Enterp. Inf. Manag. 2021, 35, 160–178. [Google Scholar] [CrossRef]

- Aguinis, H.; Villamor, I.; Gabriel, K.P. Understanding employee responses to COVID-19: A behavioural corporate social responsibility perspective. Manag. Res. 2020, 18, 421–438. [Google Scholar] [CrossRef]

- El Khoury, R.; Nasrallah, N.; Harb, E.; Hussainey, K. Exploring the performance of responsible companies in G20 during the COVID-19 outbreak. J. Clean. Prod. 2022, 354, 131693. [Google Scholar] [CrossRef]

- Huang, W.; Chen, S.; Nguyen, L.T. Corporate Social Responsibility and Organizational Resilience to COVID-19 Crisis: An Empirical Study of Chinese Firms. Sustainability 2020, 12, 8970. [Google Scholar] [CrossRef]

- Cardillo, G.; Bendinelli, E.; Torluccio, G. COVID-19, ESG investing, and the resilience of more sustainable stocks: Evidence from European firms. Bus. Strat. Environ. 2022, 32, 602–623. [Google Scholar] [CrossRef] [PubMed]

- Bose, S.; Shams, S.; Ali, M.J.; Mihret, D. COVID-19 Impact, Sustainability Performance and Firm Value: International Evidence. Account. Financ. 2022, 62, 597–643. [Google Scholar] [CrossRef]

- Yoo, S.; Keeley, A.R.; Managi, S. Does sustainability activities performance matter during financial crises? Investigating the case of COVID-19. Energy Policy 2021, 155, 112330. [Google Scholar] [CrossRef] [PubMed]

- Qiu, S.C.; Jiang, J.; Liu, X.; Chen, M.-H.; Yuan, X. Can corporate social responsibility protect firm value during the COVID-19 pandemic? Int. J. Hosp. Manag. 2021, 93, 102759. [Google Scholar] [CrossRef] [PubMed]

- Bae, K.H.; El Ghoul, S.; Gong, Z.J.; Guedhami, O. Does CSR matter in times of crisis? Evidence from the COVID-19 pandemic. J. Corp. Financ. 2021, 67, 101876. [Google Scholar] [CrossRef]

- Demers, E.; Hendrikse, J.; Joos, P.; Lev, B. ESG Did Not Immunize Stocks during the COVID-19 Crisis, but Investments in Intangible Assets Did. J. Bus. Financ. Account. 2021, 48, 433–462. [Google Scholar] [CrossRef] [PubMed]

- Mohd Zam, Z.; Yusoff, H.; Ismail, R.F.; Fauzi, H. Sustainability reporting as strategic crisis response mechanism: An innovative approach. Corp. Gov. Organ. Behav. Rev. 2023, 7, 259–271. [Google Scholar] [CrossRef]

- Wenzel, M.; Stanske, S.; Lieberman, M.B. Strategic responses to crisis. Strateg. Manag. J. 2020, 42, 231–488. [Google Scholar] [CrossRef]

- Zharfpeykan, R.; Ng, F. COVID-19 and sustainability reporting: What are the roles of reporting frameworks in a crisis? Pacific Account. Rev. 2021, 33, 189–198. [Google Scholar] [CrossRef]

- Krivačić, D.; Janković, S. Sustainability Reporting During the Pandemic: Current State and Expectations for the Future. J. Account. Manag. 2021, 11, 51–64. [Google Scholar]

- Schwartz, M.S.; Kay, A. The COVID-19 global crisis and corporate social responsibility. Asian J. Bus. Ethics 2023, 12, 101–124. [Google Scholar] [CrossRef]

- MacGregor-Pelikánová, R.; Němečková, T.; MacGregor, R.K. CSR Statements in International and Czech Luxury Fashion Industry at the Onset and during the COVID-19 Pandemic—Slowing Down the Fast Fashion Business? Sustainability 2021, 13, 3715. [Google Scholar] [CrossRef]

- Zyznarska-Dworczak, B.; Rudžionienė, K. Corporate COVID-19-Related Risk Disclosure in the Electricity Sector: Evidence of Public Companies from Central and Eastern Europe. Energies 2022, 15, 5810. [Google Scholar] [CrossRef]

- Brand, F.S.; Blaese, R.; Weber, G.; Winistoerfer, H. Changes in Corporate Responsibility Management during COVID-19 Crisis and Their Effects on Business Resilience: An Empirical Study of Swiss and German Companies. Sustainability 2022, 14, 4144. [Google Scholar] [CrossRef]

- Nicolò, G.; Aversano, N.; Sannino, G.; Tartaglia Polcini, P. Investigating Web-Based Sustainability Reporting in Italian Public Universities in the Era of COVID-19. Sustainability 2021, 13, 3468. [Google Scholar] [CrossRef]

- García-Sánchez, I.-M.; García-Sánchez, A. Corporate Social Responsibility during COVID-19 Pandemic. J. Open Innov. Technol. Mark. Complex. 2020, 6, 126. [Google Scholar] [CrossRef]

- Alkayed, H.; Yousef, I.; Hussainey, K.; Shehadeh, E. The impact of COVID-19 on sustainability reporting: A perspective from the US financial institutions. J. Appl. Account. Res. 2023, in press. [CrossRef]

- Vinod, M.S.; Umesh, P.; Sivakumar, N. Impact of COVID-19 on corporate social responsibility in India–a mixed methods approach. Int. J. Organ. Anal. 2023, 31, 168–195. [Google Scholar] [CrossRef]

- Albitar, K.; Al-Shaer, H.; Elmarzouky, M. Do assurance and assurance providers enhance COVID-related disclosures in CSR reports? An examination in the UK context. Int. J. Account. Inf. Manag. 2021, 29, 410–428. [Google Scholar] [CrossRef]

- Elmarzouky, M.; Albitar, K.; Hussainey, K. COVID-19 and performance disclosure: Does governance matter? Int. J. Account. Inf. Manag. 2021, 29, 776–792. [Google Scholar] [CrossRef]

- Poursoleyman, E.; Mansourfar, G.; Nazari, J.; Homayoun, S. Corporate social responsibility and COVID-19: Prior reporting experience and assurance. Bus. Ethics Environ. Responsib. 2022, 1–31, in press. [Google Scholar] [CrossRef]

- Phang, S.Y.; Adrian, C.; Garg, M.; Pham, A.V.; Truong, C. COVID-19 pandemic resilience: An analysis of firm valuation and disclosure of sustainability practices of listed firms. Manag. Audit. J. 2023, 8, 85–128. [Google Scholar] [CrossRef]

- Hoang, T.H.V.; Pham, L.; Lahiani, A.; Segbotangni, E.A. Does ESG Disclosure Transparency Mitigate the COVID-19 Pandemic Shock? An Empirical Analysis of Listed Firms in the UK. J. Innov. Econ. Manag. 2023, 2, 75–106. [Google Scholar] [CrossRef]

- Giannopoulos, G.; Kihle Fagernes, R.V.; Elmarzouky, M.; Afzal Hossain, K.A.B.M. The ESG Disclosure and the Financial Performance of Norwegian Listed Firms. J. Risk Financ. Manag. 2022, 15, 237. [Google Scholar] [CrossRef]

- Jastrzębska, E. Corporate Social Responsibility in Poland during the COVID-19 Pandemic and UN Sustainable Development Goals. Ann. Univ. Mariae Curie-Skłodowska Sect. H Oeconomia 2021, 55, 51–64. [Google Scholar] [CrossRef]

- GRI Sector Program—List of Prioritized Sectors. Revision 3. Approved by the GSSB on 19 October 2021. Available online: https://www.globalreporting.org/media/mqznr5mz/gri-sector-program-list-of-prioritized-sectors.pdf (accessed on 12 June 2023).

- Point, S. A User’s Guide for Interpreting the CEO Letter to Shareholders. In Handbook of Top Management Teams; Bournois, F., Duval-Hamel, J., Roussillon, S., Scaringella, J.L., Eds.; Palgrave Macmillan: London, UK, 2010; pp. 663–673. [Google Scholar] [CrossRef]

- Manuel, T.; Herron, T.L. An ethical perspective of business CSR and the COVID-19 pandemic. Soc. Bus. Rev. 2020, 15, 235–253. [Google Scholar] [CrossRef]

- Di Carlo, E. The Real Entity Theory and the Primary Interest of the Firm: Equilibrium Theory, Stakeholder Theory and Common Good Theory. In Accountability, Ethics and Sustainability of Organizations. Accounting, Finance, Sustainability, Governance & Fraud: Theory and Application; Brunelli, S., di Carlo, E., Eds.; Springer: Cham, Switzerland, 2020; pp. 3–21. [Google Scholar] [CrossRef]

- La Torre, M.; Sabelfeld, S.; Blomkvist, M.; Dumay, J. Rebuilding trust: Sustainability and non-financial reporting and the European Union regulation. Meditari Account. Res. 2020, 28, 701–725. [Google Scholar] [CrossRef]

- Singhania, M.; Saini, N. Institutional framework of ESG disclosures: Comparative analysis of developed and developing countries. J. Sustain. Financ. Investig. 2023, 13, 516–559. [Google Scholar] [CrossRef]

- Adams, C.A.; Abhayawansa, S. Connecting the COVID-19 pandemic, environmental, social and governance (ESG) investing and calls for ‘harmonisation’ of sustainability reporting. Crit. Perspect. Account. 2022, 82, 102309. [Google Scholar] [CrossRef]

- Lee, S. Corporate social responsibility and COVID-19: Research implications. Tour. Econ. 2020, 28, 863–869. [Google Scholar] [CrossRef]

| Example Statements | Company Name (Reporting Year) |

|---|---|

| “Every day we learned new practices and worked intensively on unprecedented solutions to ensure the safety of our crew.” | ArcelorMittal Poland (2020) |

| “Due to the great commitment and discipline of employees, we introduced all new products for the 2020 season on time. During the difficult time of the pandemic, we took care not only of the safety of employees, but also of their mental health and well-being.” | Carlsberg Polska (2020) |

| “We reacted to the immediate challenges of the COVID-19 pandemic by focusing on three priorities: (1) protecting the health and safety of our employees and their families, our contractors, customers and suppliers, and the communities in which we operate; (2) continuing to serve our customers both safely and reliably by leveraging our digital technologies; and (3) strengthening our liquidity position through various bold actions.” | CEMEX (2020) |

| “Due to the consistency, diligence and talent of our team, we took care of the safety of customers and employees, while striving to achieve the assumed goals.” | GK BNP Paribas Bank Polska (2020) |

| “The priority for us was the protection of the health of our employees and the safety of our customers.” | GK ING Bank Śląski SA (2020) |

| “In accordance with our core value, which is innovation, in a few months we have developed, tested and implemented proprietary solutions that ensure effective surface and air sterilization, commonly used to fight the SARS-CoV-2 virus.” | GK LUG SA (2020) |

| “The pandemic year showed us that there is strength in the group, and a committed and well-coordinated crew is always a determinant of success.” | GK Zakłady Magnezytowe Ropczyce (2020) |

| “The ongoing pandemic makes us act with an increased sense of responsibility—for our employees, subcontractors and contractors.” | GK ZUE (2020) |

| “The COVID-19 pandemic has taken its toll on the lives of all of us in the past year, and I am proud that in this extremely difficult time we have passed the test of continuing our business effectively and we have confirmed that social responsibility is integral to our strategy regardless of the circumstances. Our business model has proven resilient in the face of the turmoil caused by the pandemic that hit the economy.” | Globe Trade Centre (2020) |

| “The pandemic period was a difficult time for our teams, but also for business partners, customers and owners. We emerged victorious from this trial.” | Grupa Apator (2020) |

| “The restrictions related to the COVID-19 pandemic introduced last year, as well as the solutions we implemented to increase the energy efficiency of the operation of our showrooms, resulted in a reduction in the energy consumption rate.” | Grupa CCC (2020) |

| “The actions, efforts and management methods we have taken are another expression of our responsibility for employees, partners and customers, as well as the local communities of which we are a part.” | Grupa Echo Investment (2020) |

| “The pandemic made us realize the importance of our social responsibility and of the need to ensure an uninterrupted food supply chain while maintaining the maximum sanitary regime.” | Grupa Eurocash (2020) |

| “Despite the pandemic, we did not slow down. In terms of the long-term outlook, we continued to advance key investments.” | Grupa KGHM Polska Miedź SA (2020) |

| “The priority was the safety of our employees in the first place, and then supporting the continuity of critical processes in our clients’ organizations.” | Grupa Sygnity (2020) |

| “The year 2020 had its heroes. For us, these are our employees. Despite the understandable fears arising from the pandemic, tens of thousands of exceptional people showed up for work in our stores and distribution centers every day. It is their dedication, sense of mission and understanding of the situation that has allowed millions of customers to safely shop in their favorite chain stores.” | Jeronimo Martins Polska (2020) |

| “It is worth noting that thanks to the generosity of the convalescent miners and the plasma they donated, it was possible to effectively treat the most severe cases of COVID-19 in the most difficult period of the pandemic.” | JSW SA (2020) |

| “Even in such difficult conditions, we have risen to the occasion, providing customers with uninterrupted, safe and comfortable access to food products, safe and stable working conditions for employees, and the support needed at this time for entities involved in the fight against the pandemic.” | Kaufland Polska (2020) |

| “No matter what the future holds, we will stay on course, maintaining an ethical and responsible approach to employees, customers, suppliers, business partners and other stakeholders, and taking care of the natural environment.” | Kompania Piwowarska/2020 |

| “The pandemic was an impulse that accelerated the implementation of innovative solutions and made us react positively to many challenges.” | Raben (2020) |

| “We managed to overcome all the challenges related to the pandemic. It would not have been possible without my team, which showed 100% commitment, 100% responsibility, 100% perseverance.” | Rawlplug SA (2020) |

| “In the past year, we focused on protecting our customers from falling out of the financial market due to financial distress caused by COVID-19. We developed Good Practices for Vulnerable Customer Service, an information website for customers with credit repayment problems and resources for advisors.” | Santander Bank Polska SA (2020) |

| “I would like to thank our employees for their exceptional, responsible attitude during the ongoing pandemic, for their commitment and loyalty, which allowed us to function without significant interruptions in our daily activities.” | Wawel SA (2020) |

| “Our priority was to adapt production plants to operate in accordance with the sanitary regime while increasing their efficiency and ensuring maximum work comfort for our employees and partners.” | Wielton SA (2020) |

| “In this special, pandemic year, our priority was to ensure the continuity of services to our users and customers and guarantee safe conditions for employees.” | Wirtualna Polska Holding SA (2020) |

| “The COVID-19 pandemic was a practical verification of what kind of organization we are. Many times we have shown responsibility and full commitment to what we do. At the same time, this situation has shown that our digital transformation and continuous optimization of operations bring measurable social benefits” | Zarząd Transportu Metropolitalnego (2020) |

| “Employees have always been important to us, which is why during the pandemic we took care of such an organization of work that ensured their safety, health and support.” | Grupa VELUX (2020–2021) |

| “The last year was a period of revival of commercial activities, which was possible thanks to the gradual stabilization of the situation related to the COVID-19 pandemic, and as a result, the restoration of supply chains and opening up to most markets.” | GK Fasing SA (2021) |

| “We are involved in solving the most important social problems through financial and material support in the fight against COVID-19.” | GK PZU (2021) |

| “We introduced a vaccination program which included a cash reward for fully vaccinated employees and an additional reward for those receiving a booster dose.” | GK Stalprofil SA (2021) |

| “We undertook social activities, making targeted donations for the purchase of equipment for foundations and medical facilities. The solutions introduced due to the pandemic in the field of customer service will stay with us for years, including the rapid digitization of processes.” | GK Tauron Polska Energia SA (2021) |

| “Another year of the pandemic showed that we were able to adapt even to such a difficult, long-term and complicated situation, which is undoubtedly due to our professional crew.” | Grupa Trakcja (2021) |

| “The pandemic has accelerated changes in the way our consumers buy our products. We constantly adapt to these changes, investing in our brands, adjusting our route to the market, introducing innovations in developing segments and developing the skills of our team to meet the changing expectations of customers.” | Grupa Żywiec SA (2021) |

| “We would like to thank all employees and associates for their responsible approach to the solutions proposed by the Management Board in these very limiting restrictions.” | Korporacja KGL SA (2021) |

| Examples of Titles | Company Name (Reporting Year) |

|---|---|

| Activities during the COVID-19 pandemic | GK Cognor (2020 & 2021); GK Pamapol (2020); Grupa Energa (2020 & 2021); Grupa Banku Milennium (2020); Grupa Famur (2020); Grupa KOM-EKO (2021); Grupa Kruk (2020); Kaufland Polska (2020–2021); McDonald’s Polska (2021); Wielton SA (2020) |

| Challenges related to COVID-19 | Solaris Bus & Coach Sp. z o.o. (2020) |

| Commitment to preventing the effects of the COVID-19 pandemic | Grupa UNIMOT (2021) |

| Counteracting the effects of the COVID-19 pandemic | GK ING Bank Śląski SA (2020) |

| COVID-19 and activities in the area of occupational health and safety | GK Unibep (2020) |

| [Company Name] during the COVID-19 pandemic | Grupa Eurocash (2020); GK LUG SA (2020); GK Tauron Polska Energia SA (2021); Grupa Azoty SA (2020 & 2021); Grupa Żabka (2021); LPP SA (2020) |

| How we change for the client during the COVID-19 Health of employees during a pandemic | Grupa Echo Investment (2020) |

| Impact of the COVID-19 pandemic on our operations | Wirtualna Polska Holding SA (2020) |

| Impact of the COVID-19 pandemic on the operations of [Company Name] | Amica SA (2021); ArcelorMittal Poland (2020); Bank Gospodarstwa Krajowego (2020); Firma Oponiarska “Dębica” SA (2020 & 2021); GK BNP Paribas Bank Polska (2020); GK Enea (2020 & 2021); GK ZUE (2020 & 2021); Grupa Famur (2021); Grupa KGHM Polska Miedź SA (2020 & 2021); Grupa PKP Cargo (2020); mBank SA (2020) |

| Impact of the COVID-19 pandemic on non-financial aspects | GK Fasing SA (2020); GK Torpol (2021) |

| Impact of restrictions resulting from the pandemic on the Rawlplug development | Rawlplug SA (2020) |

| Information on the threat of COVID-19 | GK Rafamet (2020 & 2021) |

| Occupational health and safety during the COVID-19 pandemic | Grupa Benefit Systems (2020); GK Fabryki Mebli “Forte” (2020 & 2021); GK Lubelski Węgiel Bogdanka (2020); GK LUG SA (2021); GK Mercor SA (2020 & 2021); Grupa KOM-EKO (2021); Grupa Pekabex (2020 & 2021); GK Polski Holding Nieruchomości SA (2020 & 2021); GK PZU (2021); GK Relpol SA (2020 & 2021) |

| Organization of work during COVID-19 | GK Gaz System (2020) |

| Our engagement during the pandemic—Managing the COVID-19 situation in 2020 Ensuring security during the COVID-19 pandemic | Santander Bank Polska SA (2020) |

| Our response to COVID-19 | CEMEX (2020); GK Inter Cars (2020) |

| Preventing the COVID-19 pandemic in the work environment Support for local communities during the COVID-19 pandemic | CEMEX (2021) |

| PZU faced with the COVID-19 pandemic | GK PZU (2020) |

| Reliable in the face of the pandemic | Grupa Eneris (2020) |

| Response to the COVID-19 pandemic | Kompania Piwowarska (2020 & 2021); Raben (2020 & 2021) |

| Responsibility during the pandemic | Jeronimo Martins Polska (2020) |

| Responsibility of the ENEA Group in the context of the COVID-19 epidemic | GK Enea (2020) |

| Safety of employees during the COVID-19 pandemic | GK ING Bank Śląski SA (2020) |

| Safety during the pandemic | GK Gaz System (2021) |

| Situation of the Rainbow Tours in connection with the pandemic caused by the SARS-CoV-2 coronavirus | GK Rainbow Tours (2020) |

| Support activities related to the COVID-19 epidemic | GK Solar Company SA (2020) |

| Support during the COVID-19 pandemic | Grupa VELUX (2020–2021) |

| Support of the public during the COVID-19 pandemic | Grupa KGHM Polska Miedź SA (2020 & 2021) |

| Support to customers during the COVID-19 pandemic | GK BNP Paribas Bank Polska (2020 & 2021); Santander Bank Polska SA (2021) |

| TAURON Group against the greatest global challenges—the coronavirus pandemic Responsibility towards the client in the era of the SARS-CoV-2 pandemic | GK Tauron Polska Energia SA (2020) |

| TAURON Group in the era of the coronavirus pandemic | GK Tauron Polska Energia SA (2021) |

| The COVID-19 pandemic | GK Seco/Warwick SA (2020 & 2021) |

| The fight against the pandemic | Carlsberg Polska (2020 & 2021) |

| The impact of the COVID-19 | GK Solar Company SA (2021); GK Orange Polska (2020) |

| The pandemic and the safety of our employees The pandemic and the safety of our customers The pandemic and social support from ROBYG | GK ROBYG SA (2021) |

| We support the fight against the coronavirus | Grupa OEX (2020) |

| Example Information on the Changes in Business Strategies | Company Name (Reporting Year) |

|---|---|

| Minimizing the threats related to the spread of the COVID-19 pandemic as a key area of the updated business strategy | Wielton SA (2020 & 2021) |

| Introduction of flexible management, especially in the area of logistics and inventory management, and cooperation with new suppliers to maintain an undisturbed flow of production and timely deliveries | GK Fabryki Mebli “Forte”; GK Zakłady Magnezytowe Ropczyce (2020); Solaris Bus & Coach Sp. z o.o. (2020 & 2021); Grupa Żywiec SA (2020) |

| Revision of the business strategy to accelerate the technological, logistics and sales transformation, integration of physical sales and e-commerce channels, building an omnichannel organization | LPP SA (2020); Grupa CCC (2021) |

| Optimization of sales activities and reconstruction of the franchise network and showroom network, modernization and relocation of showrooms to more favorable locations (outside shopping malls) | GK CDRL SA (2021); GK Monnari Trade SA (2020 & 2021) |

| Introduction of new products and services in response to the needs arising during the pandemic (e.g., new offices equipped with modern air purification technologies; touchless devices and systems, washing machines with functions that eliminate viruses and bacteria; home delivery and collection of purchases from the store; insurance against SARS-CoV-2 infection). | Grupa Echo Investment (2020 & 2021); Amica SA (2020); Grupa Żabka (2021); GK PZU (2020) |

| Change in the strategy aimed at expanding the business with protective products directly dedicated to the fight against the pandemic (e.g., textile hygienic and medical masks; disinfecting aerosols, disinfectants, virucides for surface disinfection, UV-C luminaires for surface and air sterilization; protective clothing, triage systems and tent systems) | GK Protektor (2020); Grupa Ciech (2020); Rawlplug SA (2020); Grupa Azoty SA (2020); GK Gaz System (2020); GK Lubawa (2020) |

| Continuation of the development of protective products indispensable during the pandemic (hygienic and medical masks, protective gloves) | GK Protektor (2021); GK Mercator Medical SA |

| Introduction of aggressive marketing and adjusting offers to the needs and capabilities of customers, including the launch of online webinars showing customers the applications of offered products | Rawlplug SA (2020) |

| Acceleration of digital transformation processes and intensive development of remote channels to protect customers and employees against a coronavirus infection and provide new services and products, including the development of online banking, new functions of mobile applications and expanding the use of chatbots | Credit Agricole Bank Polska SA (2020); GK Banku Pekao SA (2020); GK BNP Paribas Bank Polska (2020); GK PKO BP SA (2020); mBank SA (2020); Santander Bank Polska SA (2020) |

| Focus on accelerated digitalization and automation of processes (software robots) and implementation of new technological solutions to enable faster customer service and contact with contractors | GK Inter Cars (2020); Vantage Development (2021) |

| Use of virtual reality to enable an overview of offered products | Grupa Echo Investment (2020 & 2021) |

| Intensive development of the fast fiber-optic broadband internet as the leading technology | GK Orange Polska (2020 & 2021) |

| Activities in the area of e-commerce and development of digital marketing and online sales channels to keep customers and ensure safe shopping | GK CDRL SA (2020); GK Komputronik (2021); GK Wojas (2020); GK Mercator Medical SA (2020 & 2021) |

| Expanding channels to reach the customer and enabling remote contact with customers through the use of modern technologies and information systems, including chatbots | Grupa Kruk (2020); GK ROBYG SA (2021) |

| Development of the service support area based on remote channels | GK PGE (2020) |

| Development of a platform for communication between employees in dispersed work teams, including teleconferences and videoconferences, and ensuring the security of the IT structure and the confidentiality of business information | GK Relpol SA (2020); PKP Energetyka (2020) |

| Adjusting the public transport structure to real needs and restrictions (minimizing the occupancy on less loaded lines and increasing the rolling stock/the number of vehicles on lines serving the most heavily loaded routes) | Zarząd Transportu Metropolitalnego (2020) |

| Providing franchisees with financial, material and legal assistance to maintain the continuity of operation of stores and secure supplies, and to provide customers with the possibility of safe shopping | Grupa Żabka (2021) |

| Introduction of support solutions for customers (possibility of postponing the payment deadline, spreading payments into instalments, extending the loan period; assistance in submitting applications for financial subsidies under the government’s anti-crisis financial shield). | GK Banku Pekao SA (2020); GK ING Bank Śląski SA (2020); GK PZU (2020); mBank SA (2020); Santander Bank Polska SA (2020) |

| Implementation of a savings and reorganization scheme to reduce operating costs | Credit Agricole Bank Polska SA (2021); GK Relpol SA (2020); Grupa Alumetal (2020); GK Agora SA (2020) |

| Delaying or postponing the implementation of the business strategy, including postponing the launch of completed investments | GK Dino Polska SA (2020); GK Elektrotim (2020); Grupa Ciech (2020) |

| Revision of the assumed financial results communicated in previous years | GK Banku Pekao SA (2020); GK Elektrotim (2020); Grupa Zamet (2020) |

| Tightening of credit procedures and temporary limitation of sales on credit to B2B customers | GK Komputronik (2021) |

| Examples of the Impact of the COVID-19 Outbreak on Environmental Performance and Environmental Activities to Respond to the Pandemic | Company Name (Reporting Year) |

|---|---|

| Reduction in fuel and energy consumption and emissions due to the limitation of operating activities, working in the remote mode, limited in-person visits to customers, limited use of cars by employees and business trips | GK CDRL S.A. (2021); GK ENEL MED (2020 & 2021); GK ING Bank Śląski SA (2021); GK Mercator Medical SA (2020); GK ZUE (2021); Grupa Asseco Poland (2020); Grupa Kruk (2020); Grupa Neuca (2020); LPP SA (2020); Santander Bank Polska SA (2021 & 2021); Wawel SA (2020); Wielton SA (2020) |

| Reduction in energy consumption for administrative purposes due to the ongoing pandemic and the low occupancy rate of employees working in offices | GK PGE (2020); GK Polski Holding Nieruchomości SA (2020) |

| Reduction in electricity, heat and hot water consumption due to the remote working mode | GK Rainbow Tours (2021) |

| Decrease in the consumption of raw materials and components due to a lower production volume during the economic downturn caused by the pandemic | GK Mangata Holding (2020) |

| Reduction in paper consumption due to digitalization of processes and popularization of online systems during the pandemic | GK ENEL MED (2020 & 2021); GK PGE (2020); GK PZU (2020); GK ZUE (2021); Grupa Ergo Hestia (2020); Vantage Development (2021) |

| Reduction in waste generation due to the decreased number of purchasing processes | Grupa Asseco Poland (2020) |

| Increase in water consumption and the amount of sewage discharged due to extended opening hours of stores during the pandemic | Jeronimo Martins Polska (2020) |

| Increase in the use of detergents for disinfection of public transport vehicles | Zarząd Transportu Metropolitalnego (2020) |

| Increase in energy and fuel consumption in the second year of the pandemic after the easing of the hard lockdown and the economic recovery | GK Fasing SA (2021); GK PZU (2021) |

| Increase in energy consumption and greenhouse gas emissions due to the return to the operation of showrooms and to the bigger scale of operations | Grupa CCC (2021) |

| Increase in energy and water consumption for administrative purposes and more sewage discharged due to the return of employees from remote work | GK PGE (2021) |

| Increase in electricity consumption in 2021 compared to 2020 due to the increase in the production volume and the fact that employees were allowed to work in the hybrid mode | GK Mercator Medical SA (2021); Sanok Rubber Company SA (2021) |

| Increase in the consumption of raw materials and components due to higher production volumes being a result of the recovery of the market demand after a significant slowdown in 2020 | GK Mangata Holding (2021) |

| Increase in the amount of medical waste due to the specificity of offered services (medical tests) and the sanitary regime during the pandemic | GK Voxel SA (2021) |

| Increase in volatile emissions from disinfectants used to prevent and reduce the transmission of COVID-19 | GK PKN Orlen SA (2021) |

| Despite the COVID-19 pandemic, environmental projects were performed as planned without interruptions (e.g., the “CEMEX for the Planet” educational campaign; the implementation of the Recycled Claim Standard; the Eco Aware Production program). | CEMEX (2021); GK Lubawa (2020); LPP SA (2020) |

| Due to the COVID-19 pandemic, some assumptions of key environmental projects were modified (e.g., the “Forests Full of Energy” project; the forest planting program aimed to compensate for land used for stores, parking lots and other infrastructure) | GK PGE (2020); Leroy Merlin Polska (2021) |

| Due to the COVID-19 pandemic, some of the planned environmental activities were postponed or suspended (e.g., optimization of energy consumption; photovoltaic systems; installation of online emissions monitoring systems; adaptation to the requirements of the Best Available Techniques conclusions for large combustion plants) | GK Agora SA (2021); GK SuperDrob (2020–2021); Grupa Benefit Systems (2020); CEMEX (2020); GK Tauron Polska Energia SA (2020) |

| The pandemic time was used to improve energy efficiency (e.g., thermal modernization, upgrading of heat sources and replacement of lighting) and implement actions aiming to reduce electricity consumption and greenhouse gas emissions | GK LUG SA (2020); GK Orange Polska (2020); GK PZU (2020); Sanok Rubber Company SA (2020); Grupa CCC (2020); Grupa Neuca (2021) |

| Specific environmental solutions were implemented to respond to the challenges posed by the pandemic (e.g., production of biogas based on processing unsold beer; a free mobile application “ecoAPP” as a source of practical knowledge about waste management during the pandemic) | Grupa Żywiec SA (2021); Grupa KOM-EKO (2020) |

| Educational campaigns were organized (e.g., energy system transformation and proper municipal waste handling and disposal during the pandemic) | GK ING Bank Śląski SA (2020); Grupa Asseco Poland (2020); Grupa Eneris (2020) |

| Studies on environmental issues were carried out during the pandemic (e.g., “Changes in consumer attitudes in Poland in the era of COVID-19”; “Green transformation in the post-pandemic world”; “Environmental education of customers” to determine preferences and changes in the ecological lifestyle during the pandemic) | Grupa Kruk (2020); GK ING Bank Śląski SA (2020); GK ROBYG SA (2021) |

| Example Activities Improving the Safety and Well-Being of Employees | Company Name (Reporting Year) |

|---|---|

| Online recruitment process | GK Bank Handlowy w Warszawie SA (2020), GK Best (2020) |

| Reduction in the number of trainings conducted in contact with others and development of the online training offer | Ambra SA (2020), Amica SA (2020), Emitel (2020), GK Agora (2021), GK Best (2021), GK Polsat Plus (2021), Grupa Apator (2020) |

| Introduction of new ways of communication between employees using modern long-distance communication tools and the intranet; internal information portals | AC SA (2021), Arctic Paper SA (2021), Emitel (2020), GK PKO BP SA (2020), GK Mercator Medical SA, Grupa Apator (2020), Grupa Ciech (2020), Grupa Erbud (2020) |

| Introduction of different work systems (remote, stationary, rotation) and a shift work system (to limit physical contact) | GK PKO BP SA (2020), GK Mercor SA (2020), GK ROBYG SA (2021), |

| Equipping employees with individual and collective protection equipment | AC SA (2020), GK LUG SA (2020), GK Mercor SA (2020), GK PKO BP SA (2020), GK ROBYG SA (2021), Grupa Ciech (2020) |

| Introduction of changes in the workspace structure to keep distance between employees and reduce the number of people in a room, etc. | AC SA (2020), GK LUG SA (2020), GK Mercor SA (2020), GK PKO BP SA (2020), GK ROBYG SA (2021) |

| Introduction of body temperature measurements | GK LUG SA (2020), GK ROBYG SA (2021), Żabka (2021) |

| Introduction of ventilation, disinfection and/or ozonation of rooms, as well as disinfection of rooms, touched surfaces and communication routes | GK ENEL MED (2020), GK LUG SA (2020), GK PKO BP SA (2020), GK ROBYG SA (2021), Grupa Erbud (2020), Grupa Żabka (2021), JSW SA (2020) |