Role of Digital Inclusive Finance for High-Quality Business Development: A Study of China’s “Five Development Concept” Policy

Abstract

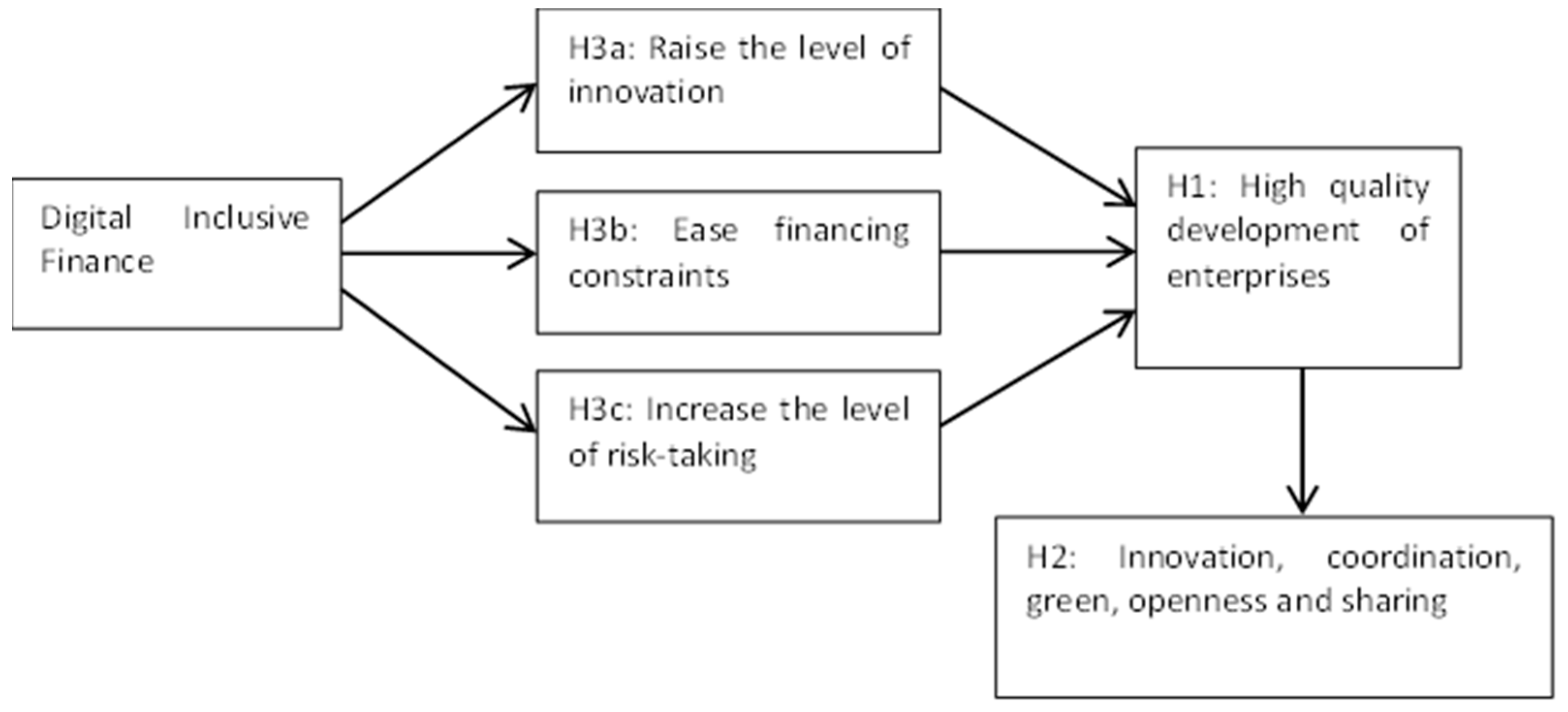

:1. Introduction

2. Theoretical Analysis and Research Hypothesis

- (i)

- The total effect of digital inclusive finance on the growth of high-quality businesses

- (ii)

- Based on the decomposition effect of the “Five Development Concept”

- (iii)

- Channels for influencing the high-quality growth of enterprises through digital inclusive finance

3. Research Design

- (i)

- Sample and data

- (ii)

- Empirical model

- (iii)

- Variable description

- (iv)

- Descriptive statistics

4. Analysis of the Empirical Results

- (i)

- Baseline regression results and the impact of three main facets of digital finance

- (ii)

- The impact of digital inclusive finance on the high-quality growth of firms under the “Five Development Concept”

- (iii)

- Heterogeneity analysis

- (iv)

- Robustness test

- (v)

- Endogenous problems

5. Mechanism Analysis

6. Conclusions, Implications, and Limitations

- (i)

- Research conclusions

- (ii)

- Policy implications

- (iii)

- Research limitations

Author Contributions

Funding

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Zhang, T. Research on the theoretical interpretation and measurement methods of high-quality development. Res. Quant. Econ. Tech. Econ. 2020, 37, 23–43. [Google Scholar]

- Huang, S.; Xiao, H.; Wang, X. On high-quality development of state-owned enterprises. China Ind. Econ. 2018, 19–41. [Google Scholar] [CrossRef]

- Dwivedi, R.; Alrasheedi, M.; Dwivedi, P.; Starešinić, B. Leveraging financial inclusion through technology-enabled services innovation: A case of economic development in India. Int. J. E-Serv. Mob. Appl. (IJESMA) 2022, 14, 1–13. [Google Scholar]

- Tang, S.; Wu, X.; Zhu, J. Digital finance and corporate technology innovation-structural characteristics, mechanism identification and differences in effects under financial regulation. Manag. World 2020, 36, 52–66+9. [Google Scholar]

- Li, S.-L.; Cui, S.-L.; Lai, X.-B. Can digital finance enhance the value of listed firms?—Theoretical mechanism analysis and empirical test. Mod. Financ. Econ. (J. Tianjin Univ. Financ. Econ.) 2020, 40, 83–95. [Google Scholar]

- Liang, B.; Zhang, J. Can China’s inclusive financial innovation ease the financing constraints of SMEs. China Sci. Technol. Forum 2018, 94–105. [Google Scholar] [CrossRef]

- Liu, Y.Q. Research on the impact of digital finance on SMEs’ technological innovation. Technol. Econ. Manag. Res. 2022, 51–56. [Google Scholar]

- Hu, B.; Cheng, X. Financial technology, digital inclusive finance and national financial competitiveness. J. Wuhan Univ. (Philos. Soc. Sci. Ed.) 2020, 73, 130–141. [Google Scholar]

- Zhou, L.; Feng, D.; Yi, X. Digital inclusive finance and urban-rural income gap: “digital dividend” or “digital divide”. Economist 2020, 99–108. [Google Scholar]

- He, Z.; Zhang, X.; Wan, G. Digital finance, digital divide and multidimensional poverty. Stat. Res. 2020, 37, 79–89. [Google Scholar]

- Labaye, E.; Remes, J. Digital technologies and the global economy, s productivity imperative. Commun. Strateg. 2015, 1, 47–64. [Google Scholar]

- Mou, X.; Sheng, Z.; Zhao, T. The impact of China’s digital finance development on the optimization and upgrading of industrial structure. Econ. Issues 2022, 10–20. [Google Scholar]

- Nie, X.; Jiang, P.; Zheng, X.; Wu, Q. Research on digital finance and regional technology innovation level. Financ. Res. 2021, 132–150. [Google Scholar]

- Teng, L.; Ma, D. Can digital finance promote high-quality development? Stat. Res. 2020, 37, 80–92. [Google Scholar]

- Thathsarani, U.; Wei, J.; Samaraweera, G. Financial Inclusion’s Role in Economic Growth and Human Capital in South Asia: An Econometric Approach. Sustainability 2021, 13, 4303. [Google Scholar] [CrossRef]

- Feng, S.; Chong, Y.; Yu, H.; Ye, X.; Li, G. Digital financial development and ecological footprint: Evidence from green-biased technology innovation and environmental inclusion. J. Clean. Prod. 2022, 380, 135069. [Google Scholar] [CrossRef]

- Wang, H.; Guo, J. Impacts of digital inclusive finance on CO2 emissions from a spatial perspective: Evidence from 272 cities in China. J. Clean. Prod. 2022, 355, 131618. [Google Scholar] [CrossRef]

- Xiong, M.; Li, W.; Jenny, C.; Wang, P. Financial Inclusion through Digitalization: Improving Emerging Drivers of Industrial Pollution—Evidence from China. Sustainability 2023, 15, 10203. [Google Scholar] [CrossRef]

- Yin, Z.C.; Gong, X.; Guo, P.Y.; Wu, T. What drives entrepreneurship in digital economy? Evid. China. Econ. Model. 2019, 82, 66–73. [Google Scholar] [CrossRef]

- Mapanje, O.; Karuaihe, S.; Machethe, C.; Amis, M. Financing Sustainable Agriculture in Sub-Saharan Africa: A Review of the Role of Financial Technologies. Sustainability 2023, 15, 4587. [Google Scholar] [CrossRef]

- Liu, J.H.; Zhou, K.; Zhang, Y.; Wang, Q. Digital inclusive finance, enterprise life cycle and technological innovation. Stat. Decis. Mak. 2022, 38, 130–134. [Google Scholar]

- Liu, L.; Yang, H.R. Digital finance, financing constraints and SMEs’ technological innovation-an empirical study based on NSSB data. East China Econ. Manag. 2022, 36, 15–23. [Google Scholar]

- Yao, Z.; Sun, X. Digital inclusive finance, financing constraints and corporate financial performance. Wuhan Financ. 2022, 42–52. [Google Scholar]

- Ma, L.; Du, S. Can digital finance enhance corporate risk-taking. Economist 2021, 65–74. [Google Scholar] [CrossRef]

- Wang, Y.; Xu, X. Tax reduction and high-quality economic development-micro evidence from small and micro enterprises. Tax. Res. 2019, 16–21. [Google Scholar]

- Li, J.; Zhang, Q.; Dong, J. Financial development, corporate diversification strategy and high-quality development. Econ. Manag. 2021, 43, 88–105. [Google Scholar]

- Shao, N. Management innovation for high-quality development of enterprises. Enterp. Manag. 2018, 8–12. [Google Scholar]

- Wang, Z. Promoting entrepreneurship in the new era to promote high-quality development of enterprises. Enterp. Manag. 2018, 6–10. [Google Scholar]

- Chen, L.; Fu, Y. Dynamic characteristics of technological innovation affecting the high-quality development of enterprises under financing constraints. China Soft Sci. 2019, 108–128. [Google Scholar]

- Li, C.; Shen, Y. Identification, measurement and prevention and control of risks in the new financial industry in the era of digital economy. Manag. World 2019, 35, 53–69. [Google Scholar]

- Zhang, C.; Zhong, C.; Yang, J. Research on the impact of digital finance on the high-quality development of real enterprises–empirical evidence based on Zhejiang. East China Econ. Manag. 2022, 36, 63–71. [Google Scholar]

- Song, J.; Zhang, J. The intrinsic connection and mechanism of action between digital finance and high-quality development of manufacturing enterprises. Bus. Econ. 2022, 41, 127–138. [Google Scholar]

- Li, X.; He, W.; Huo, Y.; Zhou, J. How digital innovation affects the high quality development of enterprises—The moderating role of digital finance level. J. Cap. Univ. Econ. Bus. 2022, 24, 80–95. [Google Scholar]

- He, L.; Cheng, T. The strategic choice of digital economy to promote high-quality economic development. Bus. Econ. Res. 2021, 189–192. [Google Scholar]

- Yang, Y.; Zhan, J.; Hu, Y. Research on the impact of digital inclusive finance on high-quality economic development. Sci. Technol. Dev. 2021, 17, 838–845. [Google Scholar]

- Dwivedi, P.; Alabdooli, J.I.; Dwivedi, R. Role of FinTech adoption for competitiveness and performance of the bank: A study of banking industry in UAE. Int. J. Glob. Bus. Compet. 2021, 16, 130–138. [Google Scholar] [CrossRef]

- Xie, P.; Zou, C.; Liu, H. The underlying theory of Internet finance. Financ. Res. 2015, 1–12. [Google Scholar]

- Qian, S.; Zhou, Y. Financial development, technological progress and industrial upgrading. Stat. Res. 2011, 28, 68–74. [Google Scholar]

- He, J.; Wei, T.; Ni, C. What can digital finance do to alleviate the difficulties of SME financing? Wuhan Financ. 2021, 29–36+45. [Google Scholar]

- Guo, F.; Wang, J.Y.; Wang, F.; Kong, T.; Zhang, X.; Cheng, Z.Y. Measuring the development of digital inclusive finance in China: Indexing and spatial characteristics. Econ. Q. 2020, 19, 1401–1418. [Google Scholar]

- Li, X. Leading high-quality development of manufacturing industry with new development concept. People’s Forum-Acad. Front. 2021, 51–59. [Google Scholar]

- Seker, M. Importing, Exporting, and Innovation in Developing Countries. Rev. Int. Econ. 2012, 20, 299–314. [Google Scholar] [CrossRef] [Green Version]

- Ozili, P.K. Impact of Digital Finance on Financial Inclusion and Stability. Borsa Istanb. Rev. 2018, 18, 329–340. [Google Scholar] [CrossRef]

- Li, X.; Ran, G. How does digital financial development affect the quality of technological innovation? Mod. Econ. Explor. 2021, 69–77. [Google Scholar]

- Wang, X.; Anders, J. Financial inhibition and structural transformation of the economy. Econ. Res. 2013, 48, 54–67. [Google Scholar]

- Yi, X.; Liu, F. Financial development, technological innovation and industrial structural transformation—A framework for analysis of multisectoral endogenous growth theory. Manag. World 2015, 24–39+90. [Google Scholar]

- Zhang, C.; Dong, X. The dynamic impact of green credit on bank performance–and the moderating effect of Internet finance. Res. Financ. Econ. 2018, 33, 56–66. [Google Scholar]

- Liu, M.; Huang, X.; Sun, J. The impact mechanism of digital finance on green development. China Popul. -Resour. Environ. 2022, 32, 113–122. [Google Scholar]

- Fan, H.C.; Peng, Y.C.; Wang, H.H. Greening through finance? J. Dev. Econ. 2021, 152, 102683. [Google Scholar] [CrossRef]

- Jin, X.; Zhang, W. Digital finance and corporate cross-border mergers and acquisitions: A factual examination and mechanistic analysis. Econ. Sci. 2021, 56–72. [Google Scholar]

- Hausmann, R.; Klinger, B. Structural Transformation and Patterns of Comparative Advantage in the Product Space. Ssrn Electron. J. 2006, 65–77. [Google Scholar] [CrossRef] [Green Version]

- Gomber, P.; Kauffman, R.J.; Parker, C. On the Fintech Revolution: Interpreting the Forces of Innovation, Disruption, and Transformationin Financial Services. J. Manag. Inf. Syst. 2018, 35, 220–265. [Google Scholar] [CrossRef]

- Lee, I.; Shin, Y.J. Fintech: Ecosystem, Business Models, Investment Decisions, and Challenges. Bus. Horiz. 2018, 61, 35–46. [Google Scholar] [CrossRef]

- Jin, X.; Zhang, W. Does digital finance development promote Chinese firms’ exports?—Theoretical mechanisms and Chinese evidence. Nankai Econ. Res. 2022, 81–99. [Google Scholar]

- Chen, C.; Xu, W. Theoretical connotation of people-centered high-quality development. Macroecon. Manag. 2020, 15–20. [Google Scholar]

- Yang, Z.-H.; Lei, L.-H.; Liao, D.-S. Does R&D manipulation inhibit high-quality development of listed companies? Syst. Eng. 2020, 38, 19–32. [Google Scholar]

- Zhao, X. Influence and insight of profit distribution criteria on enterprise development: The case of Anqi Yeast Co. Fisc. Superv. 2010, 55–56. [Google Scholar]

- Brown, J.R.; Peterson, B.C. Cash Holdings and R&D Smoothing. J. Corp. Financ. 2011, 17, 694–709. [Google Scholar]

- Xiong, X.L. Research on the mechanism of high-quality development of agriculture-related science and technology-based enterprises—Based on the perspective of rural industrial revitalization. Sci. Technol. Dev. 2021, 17, 143–152. [Google Scholar]

- Chang, Y.; Zeng, Y.; Huang, S. Cash holdings, R&D investment and high quality development of enterprises–analysis based on mediating effect and panel threshold model. East China Econ. Manag. 2022, 36, 58–67. [Google Scholar]

- Myers, S.C.; Majluf, N.S. Corporate Financing and Investment Decisions When Firms Have Information That Investors Do Not Have. J. Financ. Econ. 1984, 13, 187–221. [Google Scholar] [CrossRef] [Green Version]

- Kaplan, S.N.; Zingales, L. Do Investment-cash Flow Sensitivities Provide Useful Measures of Financing Constraints? Q. J. Econ. 1997, 112, 169–215. [Google Scholar] [CrossRef] [Green Version]

- Love, I. Financial Development and Financial Constraints: International Evidence from the Structural Investment Model. Rev. Financ. Stud. 2003, 16, 765–791. [Google Scholar] [CrossRef] [Green Version]

- Huang, H. Formation and Challenges of Digital Financial Ecosystem—Experience from China. Economist 2018, 80–85. [Google Scholar]

- Zhou, Z.; Luo, J.; Li, X. Private enterprise identity and risk-taking level. Manag. World 2019, 35, 193–208. [Google Scholar]

- Jensen, M.C.; Meckling, W.H. Theory of the Firm: Managerial Behavior, Agency Costs, and Capital Structure. J. Financ. Econ. 1976, 76, 323–339. [Google Scholar]

- Yu, M.G.; Li, W.G.; Pan, H.B. Managerial overconfidence and corporate risk-taking. Financ. Res. 2013, 149–163. [Google Scholar]

- He, Y.; Yu, W.; Yang, M. CEOs’ composite career experience, corporate risk-taking and firm value. China Ind. Econ. 2019, 155–173. [Google Scholar]

- Nakano, M.; Nguyen, P. Board Size and Corporate Risk Taking: Further Evidence from Japan. Corp. Gov. Int. Rev. 2012, 20, 369–387. [Google Scholar] [CrossRef] [Green Version]

- Demertzis, M.; Silvia, M.; Wolff, G.B. Capital Markets Union and the Fintech Opportunity. J. Financ. Regul. 2018, 4, 157–165. [Google Scholar] [CrossRef] [Green Version]

- Yu, X.L.; Shangguan, Y.W.; Yu, W.G.; Li, Q. Pension contribution rate, capital-skill complementarity and total factor productivity of firms. China Ind. Econ. 2019, 96–114. [Google Scholar]

- Wen, Z.; Ye, B. Mediation effect analysis: Methodology and model development. Adv. Psychol. Sci. 2014, 22, 731–745. [Google Scholar] [CrossRef]

- Hadlock, C.J.; Pierce, R.J. New Evidence on Measuring Financial Constraints: Moving Beyond the KZ Index. Rev. Financ. Stud. 2010, 23, 1909–1940. [Google Scholar] [CrossRef]

- Jiang, F.; Shi, B.; Ma, Y. Financial experience of information publishers and corporate financing constraints. Econ. Res. 2016, 51, 83–97. [Google Scholar]

- Zhang, X.; Liu, B.; Wang, T.; Li, C. Credit rent-seeking, financing constraints and firm innovation. Econ. Res. 2017, 52, 161–174. [Google Scholar]

- Faccio, M.; Marchica, M.T.; Mura, R. Large Shareholder Diversification and Corporate Risk-Taking. Rev. Financ. Stud. 2011, 24, 3601–3641. [Google Scholar] [CrossRef] [Green Version]

- Li, K.; Griffin, D.; Yue, H.; Zhao, L. How Does Culture Influence Corporate Risk-taking? J. Corp. Financ. 2013, 23, 1–22. [Google Scholar] [CrossRef]

{kind=link}

| Variable Category | Variable Name | Variables Symbol | Variable Definition |

|---|---|---|---|

| Explained variables | High-quality development of enterprises | Qua | Quantification and summation of the enterprise quality development index through a five-point scale |

| Ratio of R&D investment to enterprise’s operating revenue for the year | g_RD | Innovation dimension | |

| Social Responsibility | g_SR | Coordination, green dimension | |

| R&D Expenditure | g_RDS | Open dimension | |

| Shareholdings of the second to tenth largest shareholders | g_CG | Shared dimension | |

| Explanatory variables | Digital Inclusive Finance | Index | “Peking University Digital Inclusive Finance Index” |

| Breadth of coverage | coverage | ||

| Depth of use | usage | ||

| Degree of digitization | digiti | ||

| Tool Variables | Internet development level | Int | “Statistical Report on the Development Status of the Internet in China” |

| Control variables | Enterprise size | size | Total assets are taken as logarithm |

| Gearing ratio | lev | Total liabilities/total assets | |

| Operating income growth rate | growth | (Operating income for the current year—operating income for the same period of the previous year)/operating income for the same period of the previous year | |

| Asset turnover ratio | asst | Operating income/total assets ending balance | |

| Return on Net Assets | roe | Net income/shareholders’ equity balance | |

| Return on Assets | roa | Total profit/total assets | |

| Board Size | bod | Number of directors (including chairman) | |

| Tobin’s q-value | tobinq | Enterprise market value/replacement cost | |

| Business Age | age | 2022—date of company establishment | |

| Nature of company ownership | soe | Divided by whether a company is a state-owned enterprise—state-owned enterprise is 1, non-state-owned enterprise is 0 | |

| Year | year | 2011–2018 | |

| Industry | ind | Translated into category variables, the classification criteria follow the industry classification codes issued by the SEC | |

| City | city | Translated to category variables, mainland China cities above prefecture level |

| Variables | N | Mean | sd | Min | p50 | Max |

|---|---|---|---|---|---|---|

| Qua | 20,115 | 12.03 | 3.160 | 5 | 12 | 19 |

| g_RD | 20,115 | 3.020 | 1.420 | 1 | 3 | 5 |

| g_SR | 20,115 | 3.010 | 1.410 | 1 | 3 | 5 |

| g_RDS | 20,115 | 3.020 | 1.410 | 1 | 3 | 5 |

| g_CG | 20,115 | 2.990 | 1.410 | 1 | 3 | 5 |

| Index | 20,115 | 192.1 | 64.80 | 48.38 | 200.0 | 291.4 |

| coverage | 20,115 | 191.4 | 61.03 | 44.26 | 201.8 | 290.3 |

| usage | 20,115 | 189.8 | 70.19 | 50.93 | 186.6 | 320.5 |

| digiti | 20,115 | 199.0 | 81.95 | 19.20 | 230.4 | 324.7 |

| size | 20,115 | 22.06 | 1.310 | 19.49 | 21.89 | 26.06 |

| lev | 20,115 | 0.420 | 0.220 | 0.0500 | 0.410 | 0.950 |

| growth | 20,089 | 0.200 | 0.480 | −0.580 | 0.110 | 3.330 |

| asst | 20,105 | 0.620 | 0.440 | 0.0600 | 0.520 | 2.600 |

| roa | 20,115 | 0.0600 | 0.0600 | −0.240 | 0.0500 | 0.240 |

| roe | 19,997 | 0.0600 | 0.130 | −0.720 | 0.0700 | 0.330 |

| bod | 20,114 | 8.620 | 1.700 | 5 | 9 | 15 |

| tobinq | 19,276 | 2.080 | 1.400 | 0.890 | 1.620 | 9.380 |

| age | 20,112 | 23.82 | 5.170 | 13 | 24 | 37 |

| (1) Qua | (2) Qua | (3) Qua | (4) Qua | (5) Qua | |

|---|---|---|---|---|---|

| Index | 0.0194 *** | 0.0187 *** | |||

| (4.3680) | (4.1916) | ||||

| coverage | 0.0160 *** | ||||

| (4.0756) | |||||

| usage | 0.0060 ** | ||||

| (2.2056) | |||||

| digiti | 0.0017 | ||||

| (1.1627) | |||||

| size | −0.1606 *** | −0.1618 *** | −0.1610 *** | −0.1614 *** | |

| (−6.9237) | (−6.9766) | (−6.9381) | (−6.9559) | ||

| lev | −0.3167 ** | −0.3160 ** | −0.3109 ** | −0.3071 ** | |

| (−2.3597) | (−2.3545) | (−2.3161) | (−2.2875) | ||

| growth | 0.4640 *** | 0.4622 *** | 0.4664 *** | 0.4660 *** | |

| (10.8460) | (10.8008) | (10.8989) | (10.8898) | ||

| asst | −0.6247 *** | −0.6273 *** | −0.6240 *** | −0.6246 *** | |

| (−10.6056) | (−10.6487) | (−10.5892) | (−10.5981) | ||

| roa | 1.8101 *** | 1.7781 ** | 1.8349 *** | 1.8395 *** | |

| (2.5997) | (2.5533) | (2.6345) | (2.6406) | ||

| roe | −0.4630 | −0.4557 | −0.4749 | −0.4717 | |

| (−1.4337) | (−1.4110) | (−1.4701) | (−1.4602) | ||

| bod | 0.0356 *** | 0.0359 *** | 0.0357 *** | 0.0356 *** | |

| (2.7265) | (2.7550) | (2.7370) | (2.7292) | ||

| tobinq | 0.0351 * | 0.0342 * | 0.0358 * | 0.0358 * | |

| (1.9063) | (1.8537) | (1.9384) | (1.9416) | ||

| age | 0.0026 | 0.0024 | 0.0025 | 0.0024 | |

| (0.5961) | (0.5403) | (0.5750) | (0.5552) | ||

| Year FE | YES | YES | YES | YES | YES |

| City FE | YES | YES | YES | YES | YES |

| Ind FE | YES | YES | YES | YES | YES |

| adjust. | 0.2485 | 0.2635 | 0.2635 | 0.2630 | 0.2629 |

| F | 19.0795 *** | 40.4856 *** | 40.3877 *** | 39.1890 *** | 38.8304 *** |

| N | 20,113 | 19,159 | 19,159 | 19,159 | 19,159 |

| (1) Innovation | (2) Coordinated, Greenness | (3) Openness | (4) Share | |

|---|---|---|---|---|

| Index | 0.0102 *** | 0.0010 | 0.0072 *** | 0.0003 |

| (5.3081) | (0.5153) | (3.7216) | (0.1343) | |

| size | −0.1103 *** | −0.3622 *** | 0.3572 *** | −0.0463 *** |

| (−11.0089) | (−34.2333) | (35.3511) | (−4.2200) | |

| lev | −0.0234 | 0.2383 *** | 0.3457 *** | −0.8855 *** |

| (−0.4037) | (3.8932) | (5.9147) | (−13.9531) | |

| growth | 0.0126 | 0.1444 *** | 0.0477 ** | 0.2654 *** |

| (0.6842) | (7.3990) | (2.5600) | (13.1192) | |

| asst | −0.5139 *** | −0.1233 *** | 0.1888 *** | −0.1817 *** |

| (−20.2021) | (−4.5887) | (7.3601) | (−6.5235) | |

| roa | −0.6408 ** | −0.0788 | 0.6803 ** | 1.8501 *** |

| (−2.1309) | (−0.2482) | (2.2432) | (5.6192) | |

| roe | 0.2447 * | −0.2741 * | −0.1044 | −0.3359 ** |

| (1.7547) | (−1.8611) | (−0.7425) | (−2.1999) | |

| bod | −0.0062 | −0.0050 | −0.0051 | 0.0527 *** |

| (−1.1030) | (−0.8442) | (−0.8979) | (8.5380) | |

| tobinq | 0.0880 *** | −0.0618 *** | 0.0996 *** | −0.0909 *** |

| (11.0559) | (−7.3534) | (12.3990) | (−10.4311) | |

| age | 0.0117 *** | −0.0013 | 0.0214 *** | −0.0293 *** |

| (6.1738) | (−0.6585) | (11.2525) | (−14.1642) | |

| Year FE | YES | YES | YES | YES |

| City FE | YES | YES | YES | YES |

| Ind FE | YES | YES | YES | YES |

| adjust. | 0.3231 | 0.2427 | 0.3030 | 0.1846 |

| F | 109.0781 *** | 169.2017 *** | 246.0786 *** | 114.0710 *** |

| N | 19159 | 19159 | 19159 | 19159 |

| (1) State-Owned Enterprises Qua | (2) Non-State Enterprises Qua | (3) Big Growth Qua | (4) Small Growth Qua | (5) Large Scale Qua | (6) Small Scale Qua | |

|---|---|---|---|---|---|---|

| Index | 0.0122 * | 0.0218 *** | 0.0294 *** | 0.0095 | 0.0183 *** | 0.0216 *** |

| (1.7208) | (3.9735) | (4.5461) | (1.4719) | (2.9590) | (3.4275) | |

| lev | 0.3514 | −0.7583 *** | −0.2904 | −0.1435 | −0.5157 *** | −0.3393 * |

| (1.5363) | (−4.5399) | (−1.4145) | (−0.7703) | (−2.6717) | (−1.8844) | |

| asst | −0.8373 *** | −0.2315 *** | −0.5281 *** | −0.4753 *** | −0.4507 *** | −0.6976 *** |

| (−8.8161) | (−3.0455) | (−6.3484) | (−5.4890) | (−5.4984) | (−7.7873) | |

| roe | 0.8838 * | −1.2763 *** | 0.0083 | −0.1764 | 0.5986 | −1.5003 *** |

| (1.9207) | (−2.8033) | (0.0141) | (−0.4307) | (1.3017) | (−3.2457) | |

| roa | −0.4418 | 2.1976 ** | 1.1867 | 0.9254 | −2.2117 ** | 3.9712 *** |

| (−0.3757) | (2.4331) | (1.0114) | (0.9983) | (−2.0130) | (4.1578) | |

| bod | 0.0253 | 0.0600 *** | 0.0371 * | 0.0562 *** | 0.0055 | 0.0986 *** |

| (1.2217) | (3.4948) | (1.9494) | (3.0140) | (0.3220) | (4.7899) | |

| tobinq | 0.0137 | 0.0545 *** | 0.0457 * | 0.0396 | 0.0290 | 0.0703 *** |

| (0.3626) | (2.6332) | (1.6466) | (1.5302) | (0.7488) | (3.3665) | |

| age | −0.0007 | −0.0024 | 0.0170 *** | 0.0073 | −0.0014 | 0.0073 |

| (−0.0787) | (−0.4659) | (2.6776) | (1.1370) | (−0.2318) | (1.1098) | |

| size | −0.2311 *** | 0.0628 ** | −0.1124 *** | −0.0956 *** | ||

| (−6.0681) | (2.0038) | (−3.3508) | (−2.7924) | |||

| growth | 0.3669 *** | 0.3738 *** | 0.4191 *** | 0.3311 *** | ||

| (4.9662) | (7.4444) | (7.3293) | (5.2038) | |||

| soe | −0.6753 *** | −0.6515 *** | −0.6978 *** | −0.7792 *** | ||

| (−8.4700) | (−8.6703) | (−9.6296) | (−9.4318) | |||

| adjust. | 0.3686 | 0.2712 | 0.2413 | 0.2931 | 0.3020 | 0.2985 |

| F | 15.4332 *** | 12.9770 *** | 23.6515 *** | 19.0586 *** | 25.6032 *** | 25.6239 *** |

| N | 7278 | 11,872 | 9489 | 9360 | 9606 | 9222 |

| (1) tfp | (2) tfp | (3) tfp | (4) tfp | (5) Qua | (6) Qua | |

|---|---|---|---|---|---|---|

| Index | 0.0006 *** | |||||

| (16.0964) | ||||||

| coverage | 0.0006 *** | |||||

| (15.6066) | ||||||

| usage | 0.0005 *** | |||||

| (14.9881) | ||||||

| digiti | 0.0005 *** | |||||

| (15.7555) | ||||||

| dum | 0.4246 *** | |||||

| (9.4366) | ||||||

| L.Index | 0.0083 *** | |||||

| (22.1650) | ||||||

| size | 0.0057 ** | 0.0062 ** | 0.0080 *** | 0.0054 * | −0.2652 *** | −0.3013 *** |

| (1.9912) | (2.1791) | (2.8112) | (1.8793) | (−11.9492) | (−13.1115) | |

| lev | −0.1098 *** | −0.1129 *** | −0.1079 *** | −0.1122 *** | 0.3687 *** | 0.3635 ** |

| (−6.5565) | (−6.7523) | (−6.4288) | (−6.6922) | (2.6634) | (2.4804) | |

| growth | 0.0540 *** | 0.0543 *** | 0.0539 *** | 0.0551 *** | 0.5349 *** | 0.5158 *** |

| (7.7488) | (7.7848) | (7.7146) | (7.8986) | (12.0733) | (10.9419) | |

| asst | 0.3335 *** | 0.3340 *** | 0.3311 *** | 0.3340 *** | −0.5679 *** | −0.6404 *** |

| (48.3671) | (48.5225) | (47.9680) | (48.1214) | (−9.6894) | (−10.1460) | |

| roe | −0.4110 *** | −0.4196 *** | −0.4050 *** | −0.3969 *** | −0.0062 | −0.1192 |

| (−9.2419) | (−9.4184) | (−9.1159) | (−8.9257) | (−0.0193) | (−0.3552) | |

| roa | 2.0376 *** | 2.0486 *** | 2.0073 *** | 2.0213 *** | 1.0273 | 1.0866 |

| (20.7608) | (20.8096) | (20.5142) | (20.6094) | (1.4340) | (1.4535) | |

| bod | 0.0080 *** | 0.0078 *** | 0.0075 *** | 0.0076 *** | −0.0265 ** | −0.0243 * |

| (4.9689) | (4.8561) | (4.6927) | (4.7562) | (−1.9819) | (−1.7200) | |

| tobinq | 0.0055 *** | 0.0052 ** | 0.0081 *** | 0.0046 ** | −0.1372 *** | −0.1206 *** |

| (2.6188) | (2.4272) | (3.8442) | (2.1435) | (−7.3543) | (−6.4908) | |

| age | 0.0008 | 0.0008 * | 0.0008 | 0.0005 | 0.0088 ** | 0.0077 * |

| (1.5845) | (1.6663) | (1.5023) | (0.8967) | (2.0950) | (1.7571) | |

| adjust. | 0.3199 | 0.3191 | 0.3182 | 0.3194 | 0.0286 | 0.0568 |

| F | 446.1827 *** | 447.0367 *** | 440.9788 *** | 441.1898 *** | 51.7304 *** | 97.1343 *** |

| N | 11,564 | 11,564 | 11,564 | 11,564 | 17,772 | 16,021 |

| (1) Phase I | (2) Phase II | |

|---|---|---|

| Index | Qua | |

| Int | 2.4315 *** | |

| (0.029) | ||

| Index | 0.0016 ** | |

| (0.001) | ||

| size | 10.0561 *** | −0.2824 *** |

| (0.400) | (0.025) | |

| lev | −17.6110 *** | 0.6168 *** |

| (2.382) | (0.141) | |

| growth | 1.4046 * | 0.6167 *** |

| (0.832) | (0.048) | |

| asst | −5.0019 *** | −0.7079 *** |

| (0.926) | (0.054) | |

| roe | −13.6144 ** | 1.5898 *** |

| (6.118) | (0.356) | |

| roa | −56.8884 *** | −0.5156 |

| (13.043) | (0.762) | |

| bod | −3.7191 *** | 0.0586 *** |

| (0.240) | (0.014) | |

| tobinq | 4.6016 *** | −0.0164 |

| (0.315) | (0.019) | |

| age | −0.8334 *** | 0.0375 *** |

| (0.077) | (0.005) | |

| Constant | −113.2443 *** | 16.5545 *** |

| (8.524) | (0.496) | |

| N | 19,090 | 19,090 |

| adjust. | 0.331 | 0.021 |

| (1) | (2) | (3) | (4) | (5) | (6) | |

|---|---|---|---|---|---|---|

| RD | Qua | SA | Qua | Risk | Qua | |

| Index | 0.0019 | 0.0033 | 0.0000 | 0.0187 *** | −0.0028 | 0.0190 *** |

| (0.2736) | (0.7801) | (0.1034) | (4.1939) | (−0.0730) | (4.2501) | |

| RD | 0.2614 *** | |||||

| (51.0975) | ||||||

| SA | −0.4925 ** | |||||

| (−2.3450) | ||||||

| Risk | −0.0006 | |||||

| (−0.7017) | ||||||

| controls | YES | YES | YES | YES | YES | YES |

| adjust.R2 | 0.4620 | 0.4536 | 0.9964 | 0.2637 | 0.4595 | 0.2641 |

| F | 229.1684 *** | 316.7057 *** | 368,384.4473 *** | 37.3138 *** | 125.9624 *** | 37.0011 *** |

| N | 14,479 | 14,479 | 19,159 | 19,159 | 19,131 | 19,131 |

| Sobel | 13.13 *** | −4.270 *** | 3.248 *** | |||

| Goodman-1 | 13.13 *** | −4.251 *** | 3.223 *** | |||

| Goodman-2 | 13.14 *** | −4.290 *** | 3.273 *** | |||

| Explained Variables | Research Scholar | Research Conclusion | Mechanism Test | Heterogeneity Analysis |

|---|---|---|---|---|

| Total factor productivity | Li et al. (2021) [34] | U shaped | Yes Diversification strategy | Yes Scale; Property right; Investment efficient; R&D intensity; Innovation ability |

| Li et al. (2022) [33] | Positive | Yes Cost | Yes Property right; Survival span; Scale | |

| Labor productivity | Zhang et al. (2022) [31] | Positive | No | Yes Structure; Scale; Region |

| Entropy weight method | Song and Zhang (2022) [32] | Positive | Yes Financing constraints; Technological innovation; Maturity mismatch of investment and financing | Yes Region; Digital dimension; Property right |

| Uniform quantization and sum by quintile | This paper | Positive | Yes Innovation level; Financing constraint; Risk bearing level | Yes Property right; Growth; Scale |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Su, R.; Zheng, T.; Zhong, Y.; Zhong, W. Role of Digital Inclusive Finance for High-Quality Business Development: A Study of China’s “Five Development Concept” Policy. Sustainability 2023, 15, 12078. https://doi.org/10.3390/su151512078

Su R, Zheng T, Zhong Y, Zhong W. Role of Digital Inclusive Finance for High-Quality Business Development: A Study of China’s “Five Development Concept” Policy. Sustainability. 2023; 15(15):12078. https://doi.org/10.3390/su151512078

Chicago/Turabian StyleSu, Ruixin, Tong Zheng, Yuzhao Zhong, and Weizhou Zhong. 2023. "Role of Digital Inclusive Finance for High-Quality Business Development: A Study of China’s “Five Development Concept” Policy" Sustainability 15, no. 15: 12078. https://doi.org/10.3390/su151512078