How Does Corporate ESG Performance Affect Financial Irregularities?

Abstract

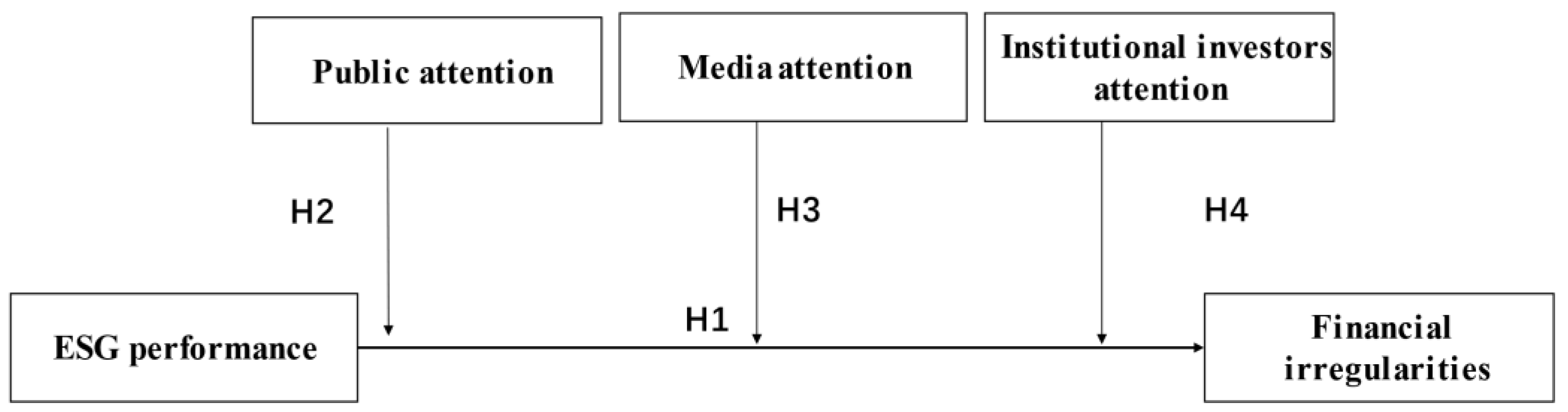

:1. Introduction

2. Theoretical Review and Hypotheses

2.1. Impact of ESG Performance on Corporate Financial Irregularities

2.2. Moderating the Effect of Public Attention

2.3. Moderating the Effect of Media Attention

2.4. Moderating the Effect of Institutional Investor Attention

3. Research Design

3.1. Data and Samples

3.2. Definition of Variables

3.2.1. Dependent Variable

3.2.2. Independent Variable

3.2.3. Moderating Variables

3.2.4. Control Variables

3.3. Model Design

4. Empirical Analysis Results

4.1. Descriptive Statistics

4.2. Correlation Analysis

4.3. Regression Results Analysis

4.4. Robustness Test

5. Discussion and Conclusions

5.1. Discussion

5.2. Conclusions

5.3. Implications

5.4. Limitations and Future Prospects

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Smaili, N.; Labelle, R. Preventing and Detecting Accounting Irregularities: The Role of Corporate Governance; SSRN: Rochester, NY, USA, 2009. [Google Scholar] [CrossRef]

- Aggarwal, R.; Hu, M.; Yang, J. Fraud, market reaction, and the role of institutional investors in Chinese listed firms. J. Portf. Manag. Spec. China Issue 2015, 41, 92–109. [Google Scholar] [CrossRef]

- Carmichael, J.J.; Eaton, S.E. Security risks, fake degrees, and other fraud: A topic modelling approach. In Fake Degrees and Fraudulent Credentials in Higher Education; Ethics and Integrity in Educational Contexts; Eaton, S.E., Carmichael, J.J., Pethrick, H., Eds.; Springer: Cham, Switzerland, 2023; Volume 5, pp. 227–250. [Google Scholar] [CrossRef]

- Johnson, W.C.; Xie, W.; Yi, S. Corporate fraud and the value of reputations in the product market. J. Corp. Financ. 2014, 25, 16–39. [Google Scholar] [CrossRef]

- Sadaf, R.; Olah, J.; Popp, J.; Mate, D. Cases: A cross-country perspective. Sustainability 2018, 3, 588. [Google Scholar] [CrossRef] [Green Version]

- Zhou, Y.; Makridis, C. Financial Misconduct and Changes in the Employee Satisfaction; SSRN: Rochester, NY, USA, 2019. [Google Scholar] [CrossRef]

- Li, P.; Yang, Z. Accounting fraud and prevention in listed companies in China. Int. J. Front. Sociol. 2019, 1, 23–31. [Google Scholar]

- Albuquerque, R.; Koskinen, Y.; Zhang, C. Corporate social responsibility and firm risk. Manag. Sci. 2019, 65, 4451–4469. [Google Scholar] [CrossRef] [Green Version]

- Hoepner, A.G.F.; Oikonomou, I.; Sautner, Z.; Starks, L.T.; Zhou, X. ESG Shareholder Engagement and Downside Risk; Finance Working Paper No. 671/2020; European Corporate Governance Institute: Brussels, Belgium, 2020. [Google Scholar] [CrossRef]

- Hong, H.; Liskovich, I. Crime, Punishment and the Halo Effect of Corporate Social Responsibility; NBER Working Paper, 21215; National Bureau of Economic Research: Cambridge, MA, USA, 2015. [Google Scholar] [CrossRef]

- Luan, X.; Wang, X. Open innovation, enterprise value and the mediating effect of ESG. Bus. Process Manag. J. 2023, 29, 489–504. [Google Scholar] [CrossRef]

- El Ghoul, S.; Guedhami, O.; Kwok, C.C.Y.; Mishra, D.R. Does corporate social responsibility affect the cost of capital? J. Bank. Financ. 2011, 35, 2388–2406. [Google Scholar] [CrossRef]

- Sharfman, M.P.; Fernando, C.S. Environmental risk management and the cost of capital. Strateg. Manag. J. 2008, 29, 569–592. [Google Scholar] [CrossRef]

- Cooper, E.; Uzun, H. Corporate social responsibility and bankruptcy. Stud. Econ. Financ. 2019, 36, 130–153. [Google Scholar] [CrossRef]

- Lin, K.C.; Dong, X. Corporate social responsibility engagement of financial distressed firms and their bankruptcy likelihood. Adv. Account. 2018, 43, 32–45. [Google Scholar] [CrossRef]

- Boubaker, S.; Cellier, A.; Manita, R.; Saeed, A. Does corporate social responsibility reduce financial distress risk? Econ. Model. 2020, 91, 835–851. [Google Scholar] [CrossRef]

- Akisik, O.; Gal, G. The impact of corporate social responsibility and internal controls on stakeholders’ view of the firm and Finance performance. Sustain. Account. Manag. Policy J. 2017, 8, 246–280. [Google Scholar] [CrossRef]

- Zhu, Y.; Sun, Y. The impact of coupling interaction of internal control and CSR on corporate performance: Based on the perspective (2017) of stakeholder. Procedia Eng. 2017, 174, 449–455. [Google Scholar]

- Harasheh, M.; Provasi, R. A need for assurance: Do internal control systems integrate environmental, social, and governance factors? Corp. Soc. Responsib. Environ. Manag. 2023, 30, 384–401. [Google Scholar] [CrossRef]

- Cek, K.; Eyupoglu, S. Does environmental, social and governance performance influence economic performance? J. Bus. Econ. Manag. 2023, 21, 1165–1184. [Google Scholar] [CrossRef]

- Aboud, A.; Diab, A. The financial and market consequences of environmental, social and governance ratings, The implications of recent political volatility in Egypt, Sustainability Accounting. Manag. Policy J. 2019, 10, 498–520. [Google Scholar] [CrossRef] [Green Version]

- Ruan, L.; Liu, H. Environmental, Social, Governance Activities and Firm Performance: Evidence from China. Sustainability 2021, 13, 767. [Google Scholar] [CrossRef]

- Duque-Grisales, E.; Aguilera-Caracuel, J. Environmental, Social and Governance (ESG) Scores and Financial Performance of Multilatinas: Moderating Effects of Geographic International Diversification and Financial Slack. J. Bus. Ethics 2021, 168, 315–334. [Google Scholar] [CrossRef]

- Pu, G. A non-linear assessment of ESG and firm performance relationship, evidence from China. Econ. Res.-Ekon. Istraživanja 2023, 36, 2113336. [Google Scholar] [CrossRef]

- Yuan, X.; Li, Z.; Xu, J.; Shang, L. ESG disclosure and corporate financial irregularities: Evidence from Chinese listed firms. J. Clean. Prod. 2022, 332, 129992. [Google Scholar] [CrossRef]

- Xue, J.; He, Y.; Liu, M.; Tang, Y.; Xu, H. Incentives for corporate environmental information disclosure in China: Public media pressure, local government supervision and interactive effects. Sustainability 2021, 13, 10016. [Google Scholar] [CrossRef]

- Yao, S.; Pan, Y.; Sensoy, A.; Uddin, G.S.; Cheng, F. Green credit policy and firm performance: What we learn from China. Energy Econ. 2021, 101, 105415. [Google Scholar] [CrossRef]

- Zhang, Z.; Chen, H. Media coverage and impression management in corporate social responsibility reports: Evidence from China. Sustain. Account. Manag. Policy J. 2020, 11, 863–886. [Google Scholar] [CrossRef]

- Chen, W.; Chu, Z.; Gu, W. Assessing the role of public attention in China’s wastewater treatment: A spatial perspective. Technol. Forecast. Soc. Chang. 2021, 171, 120984. [Google Scholar]

- Qi, B.; Yang, R.; Tian, A. Evidence from China. Rev. Quant. Financ. Account. 2014, 42, 571–597. [Google Scholar] [CrossRef]

- Saleh, M.; Zulkifli, N.; Muhamad, R. Corporate social responsibility disclosure and its relation on institutional ownership, evidence from public listed companies in Malaysia. Manag. Audit. J. 2010, 25, 591–613. [Google Scholar] [CrossRef] [Green Version]

- Amiram, D.; Owens, E.; Rozenbaum, O. Do information releases increase or decrease information asymmetry? New evidence from analyst forecast announcement. J. Account. Econ. 2016, 62, 121–138. [Google Scholar] [CrossRef]

- Godfrey, P.C. The relationship between corporate philanthropy and shareholder wealth: A risk management perspective. Acad. Manag. Rev. 2005, 30, 18378878. [Google Scholar] [CrossRef] [Green Version]

- Chang, K.; Kim, I.; Li, Y. The heterogeneous impact of corporate social responsibility activities that target different stakeholders. J. Bus. Ethics 2014, 125, 211–234. [Google Scholar] [CrossRef]

- Chakraborty, A.; Gao, L.S.; Sheikh, S. Managerial risk taking incentives, Corporate social responsibility and firm risk. J. Econ. Bus. 2019, 101, 58–72. [Google Scholar] [CrossRef]

- Hong, H.; Kacperczyk, M. The price of sin, the effects of social norms on markets. J. Financ. Econ. 2009, 93, 15–36. [Google Scholar] [CrossRef]

- Cheng, J.; Liu, Y. The effects of public attention on the environmental performance of high-polluting firms, based on big data from web search in China. J. Clean. Prod. 2018, 186, 335–341. [Google Scholar] [CrossRef]

- Gu, Y.; Ho, K.C.; Cheng, Y.; Gozgor, G. Public environmental concern, CEO turnover, and green investment, Evidence from a quasi-natural experiment in China. Energy Econ. 2021, 100, 105379. [Google Scholar] [CrossRef]

- Yong, Z.; Anqi, L.A.; Lin, R.; Hu, Y. A study on the relationship between technical independent directors and enterprise innovation under media Attention. J. Financ. Account. 2021, 9, 258–267. [Google Scholar] [CrossRef]

- Billings, M.B.; Cedergren, M.C. Strategic silence, insider selling and litigation risk. J. Account. Econ. 2015, 59, 119–142. [Google Scholar] [CrossRef] [Green Version]

- Kong, G.W.; Kong, D.M.; Wang, M. Evidence from China. Singap. Econ. Rev. 2020, 65, 577–600. [Google Scholar] [CrossRef]

- Wu, W.; Liang, Z.; Zhang, Q. Effects of corporate environmental responsibility strength and concern on innovation Performance: The Moderating Role of Firm Visibility. Corp. Soc. Responsib. Environ. Manag. 2020, 27, 1487–1497. [Google Scholar] [CrossRef]

- Eisenhardt, K. Agency theory: An assessment and review. Acad. Manag. Rev. 1989, 14, 57–74. [Google Scholar] [CrossRef]

- Sparkes, R.; Cowton, C.J. The maturing of socially responsible investment: A review of the developing link with corporate social responsibility. J. Bus. Ethics 2004, 52, 45–57. [Google Scholar] [CrossRef]

- Dyck, A.; Lins, K.; Roth, L.; Wagner, H. Do institutional investors drive corporate social responsibility? International evidence. J. Financ. Econ. 2019, 131, 693–714. [Google Scholar] [CrossRef]

- He, J.; Huang, J.; Zhaom, S. Internalizing governance externalities: The role of institutional cross-ownership. J. Financ. Econ. 2019, 134, 400–418. [Google Scholar] [CrossRef]

- Lewis, B.W.; Walls, J.L.; Tang, Q. Gender diversity, Board Independence, Environment Committe and Greenhouse Gas Disclosure. Br. Account. Rev. 2015, 47, 409–424. [Google Scholar] [CrossRef]

- Ramalingegowda, S.; Utke, S.; Yu, Y. Common institutional ownership and earnings management. Contemp. Account. Res. 2021, 38, 208–241. [Google Scholar] [CrossRef]

- Jiang, P.; Ma, Y.; Shi, B. Common ownership and stock price crash risk: Evidence from China. Aust. Econ. Pap. 2022, 61, 876–912. [Google Scholar] [CrossRef]

- Di Tommaso, C.; Thornton, J. Do ESG scores effect bank risk taking and value? Evidence from European banks. Corp. Soc. Responsib. Environ. Manag. 2020, 27, 2286–2298. [Google Scholar] [CrossRef]

- Qiu, M.Y.; Yin, H. An analysis of enterprises’ financing cost with ESG performance under the background of ecological civilization construction. J. Quant. Econ. 2019, 36, 108–123. [Google Scholar]

- Bloomberg. Behind the Bloomberg ESG Disclosure Score. 2016. Available online: http://framework-llc.com/bloomberg-esg-disclosure-scores-behind-the-terminal/ (accessed on 4 December 2022).

- He, X.; Shi, J. The effect of air pollution on Chinese green bond market: The mediation role of public concern. J. Environ. Manag. 2022, 325, 116522. [Google Scholar] [CrossRef]

- Luo, Y.; Xiong, G.; Mardani, A. Environmental information disclosure and corporate innovation: The “Inverted U-shaped” regulating effect of media attention. J. Bus. Res. 2022, 146, 453–463. [Google Scholar] [CrossRef]

- Su, W.; Fan, Y.H. Impact of media attention on environmental performance in China. Environ. Chall. 2021, 4, 100133. [Google Scholar] [CrossRef]

- Liu, C.; Wang, X. Media and institutional investors focus on the impact on corporate sustainability performance. Sustainability 2022, 14, 13878. [Google Scholar] [CrossRef]

- Zhang, C.; Jin, S.Y. What drives sustainable development of enterprises? Focusing on ESG management and green technology innovation. Sustainability 2022, 14, 11695. [Google Scholar] [CrossRef]

{kind=link}

| Variable Types | Variable Names | Variable Symbols | Measurement Methods |

|---|---|---|---|

| Dependent variable | Financial irregularities | VIO | Dummy variable: takes 1 if the firm has a reported financial violation; takes 0 otherwise |

| Independent variable | ESG performance | ESG | Bloomberg ESG total score |

| Moderating variables | Public attention | PA | Ln (median of the annual Web search volume index) |

| Media attention | MEDIA | Ln (total number of news articles with this company in the headline) | |

| Investor attention | INVEST | Institutional investors’ share of total equity | |

| Control variables | Corporate listing lifespan | AGE | Ln (current year-listing year) |

| Asset/liability ratio | LEV | Total liabilities/total assets | |

| Enterprise size | SIZE | Ln (book value of total assets at the end of the year) | |

| Nature of enterprise | STATE | State-owned enterprise = 1, Non-state-owned enterprise = 0 | |

| Return on assets | ROA | Net profit/average balance of total assets | |

| Current asset turnover | CAT | Sales revenue/average balance of current assets | |

| Capital intensity | CD | Ratio of total assets to operating income | |

| Industry | INDUSTRY | Dummy variable | |

| Year | YEAR | Dummy variable |

| Variables | N | Mean | sd | Min | Max |

|---|---|---|---|---|---|

| VIO | 1050 | 0.1410 | 0.3481 | 0 | 1 |

| ESG | 1050 | 22.9576 | 4.5361 | 12.81 | 43.39 |

| PA | 1050 | 7.188 | 0.591 | 5.464 | 9.093 |

| MEDIA | 1050 | 4.752 | 1.047 | 0 | 7.660 |

| INVEST | 1050 | 3.881 | 0.444 | 1.163 | 4.490 |

| ROA | 1049 | 0.0484 | 0.0542 | −0.317 | 0.270 |

| CAT | 1050 | 3.247 | 3.699 | 0.100 | 35.94 |

| LEV | 1050 | 0.485 | 0.174 | 0.0341 | 0.916 |

| CD | 1050 | 1.935 | 1.821 | 0.303 | 22.69 |

| AGE | 1050 | 2.944 | 0.269 | 2.303 | 3.584 |

| STATE | 1050 | 0.554 | 0.497 | 0 | 1 |

| SIZE | 1050 | 23.17 | 1.053 | 20.65 | 25.96 |

| VIO | ESG | PA | MEDIA | INVEST | AGE | ROA | CAT | STATE | SIZE | LEV | CD | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| VIO | 1 | |||||||||||

| ESG | −0.288 *** | 1 | ||||||||||

| PA | −0.101 *** | 0.111 *** | 1 | |||||||||

| MEDIA | −0.036 | 0.155 *** | 0.561 *** | 1 | ||||||||

| INVEST | −0.229 *** | 0.097 *** | 0.120 *** | 0.095 *** | 1 | |||||||

| AGE | −0.064 ** | 0.013 *** | −0.056 * | −0.164 *** | 0.037 | 1 | ||||||

| ROA | −0.085 *** | 0.002 | 0.056 * | 0.158 *** | 0.125 *** | −0.081 *** | 1 | |||||

| CAT | −0.063 ** | 0.124 *** | 0.006 | 0.049 | 0.168 *** | −0.094 *** | 0.052 * | 1 | ||||

| STATE | −0.022 | 0.031 | 0.124 *** | −0.017 | 0.281 *** | 0.046 | −0.206 *** | 0.025 | 1 | |||

| SIZE | −0.068 ** | 0.328 *** | 0.419 *** | 0.172 *** | 0.337 *** | 0.215 *** | −0.113 *** | 0.110 *** | 0.303 *** | 1 | ||

| LEV | 0.096 *** | 0.084 *** | −0.014 | 0.012 | 0.127 *** | 0.136 *** | −0.495 *** | 0.119 *** | 0.158 *** | 0.444 *** | 1 | |

| CD | 0.081 *** | −0.114 *** | −0.118 *** | −0.275 *** | −0.088 *** | 0.070 ** | −0.126 *** | −0.225 *** | 0.122 *** | −0.006 | −0.006 ** | 1 |

| Variables | Model (1) | Model (2) | Model (3) | Model (4) |

|---|---|---|---|---|

| ESG | −0.0177 *** | −0.0973 *** | −0.0450 *** | −0.0981 *** |

| (−6.7565) | (−3.1194) | (−3.6809) | (−5.3717) | |

| PA | −0.2539 ** | |||

| (−2.5580) | ||||

| PA × ESG | 0.0109 ** | |||

| (2.5600) | ||||

| MEDIA | −0.0865 * | |||

| (−1.6676) | ||||

| MEDIA × ESG | 0.0051 ** | |||

| (2.2221) | ||||

| INVEST | −0.6855 *** | |||

| (−6.1907) | ||||

| INVEST × ESG | 0.0203 *** | |||

| (4.4414) | ||||

| AGE | −0.1018 * | −0.1106 ** | −0.1079 ** | −0.1201 ** |

| (−1.8841) | (−2.0424) | (−2.0013) | (−2.2920) | |

| ROA | −0.0735 | −0.0272 | −0.1003 | 0.1721 |

| (−0.2918) | (−0.1079) | (−0.3961) | (0.7012) | |

| CAT | −0.0009 | −0.0007 | −0.0004 | 0.0006 |

| (−0.2478) | (−0.1857) | (−0.1127) | (0.1777) | |

| STATE | −0.0234 | −0.0142 | −0.0123 | 0.0240 |

| (−0.8697) | (−0.5236) | (−0.4560) | (0.8959) | |

| SIZE | −0.0159 | −0.0181 | −0.0291 * | −0.0002 |

| (−0.9976) | (−0.9544) | (−1.7602) | (−0.0138) | |

| LEV | 0.3446 *** | 0.3319 *** | 0.3513 *** | 0.4296 *** |

| (3.3890) | (3.2021) | (3.4487) | (4.3572) | |

| CD | 0.0063 | 0.0062 | 0.0078 | 0.0070 |

| (0.8176) | (0.8007) | (0.9857) | (0.9392) | |

| Constant | 1.3040 *** | 3.2068 *** | 2.0730 *** | 3.6608 *** |

| (3.7034) | (3.8761) | (4.2959) | (6.5471) | |

| Observations | 1050 | 1050 | 1050 | 1050 |

| R-squared | 0.190 | 0.195 | 0.197 | 0.248 |

| Year FE | YES | YES | YES | YES |

| Variables | First Stage ESG | Second Stage VIO |

|---|---|---|

| lESG | 0.9468 *** | |

| (42.33) | ||

| ESG | −0.0203 *** | |

| (−6.95) | ||

| AGE | 0.5129 * | −0.0818 * |

| (1.93) | (−1.80) | |

| ROA | 3.7818 * | 0.2250 |

| (2.12) | (0.91) | |

| CAT | −0.0002 | −0.0027 |

| (−0.01) | (−0.94) | |

| STATE | 0.0509 | 0.0229 |

| (0.36) | (0.93) | |

| SIZE | 0.3934 *** | 0.0049 |

| (4.17) | (−0.37) | |

| LEV | −0.5156 ** | 0.2743 ** |

| (−1.03) | (3.17) | |

| CD | −0.0428 | 0.0122 |

| (−1.42) | (1.60) | |

| Constant | −8.9435 *** | 0.8357 *** |

| (−4.25) | (3.02) | |

| Kleibergen–Paap rk LM statistic | 122.498 (Chi-sq(1) p-value = 0.0000) | |

| Weak identification test (Cragg–Donald Wald F statistic) | 2763.499 | |

| Kleibergen–Paap rk Wald F statistic 10% maximal IV size | 1791.658 16.38 | |

| Observations | 887 | 887 |

| R-squared | 0.2240 | |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Liu, D.; Jin, S. How Does Corporate ESG Performance Affect Financial Irregularities? Sustainability 2023, 15, 9999. https://doi.org/10.3390/su15139999

Liu D, Jin S. How Does Corporate ESG Performance Affect Financial Irregularities? Sustainability. 2023; 15(13):9999. https://doi.org/10.3390/su15139999

Chicago/Turabian StyleLiu, Dingru, and Shanyue Jin. 2023. "How Does Corporate ESG Performance Affect Financial Irregularities?" Sustainability 15, no. 13: 9999. https://doi.org/10.3390/su15139999