Analysis of the Motivation behind Corporate Social Responsibility Based on the csQCA Approach

Abstract

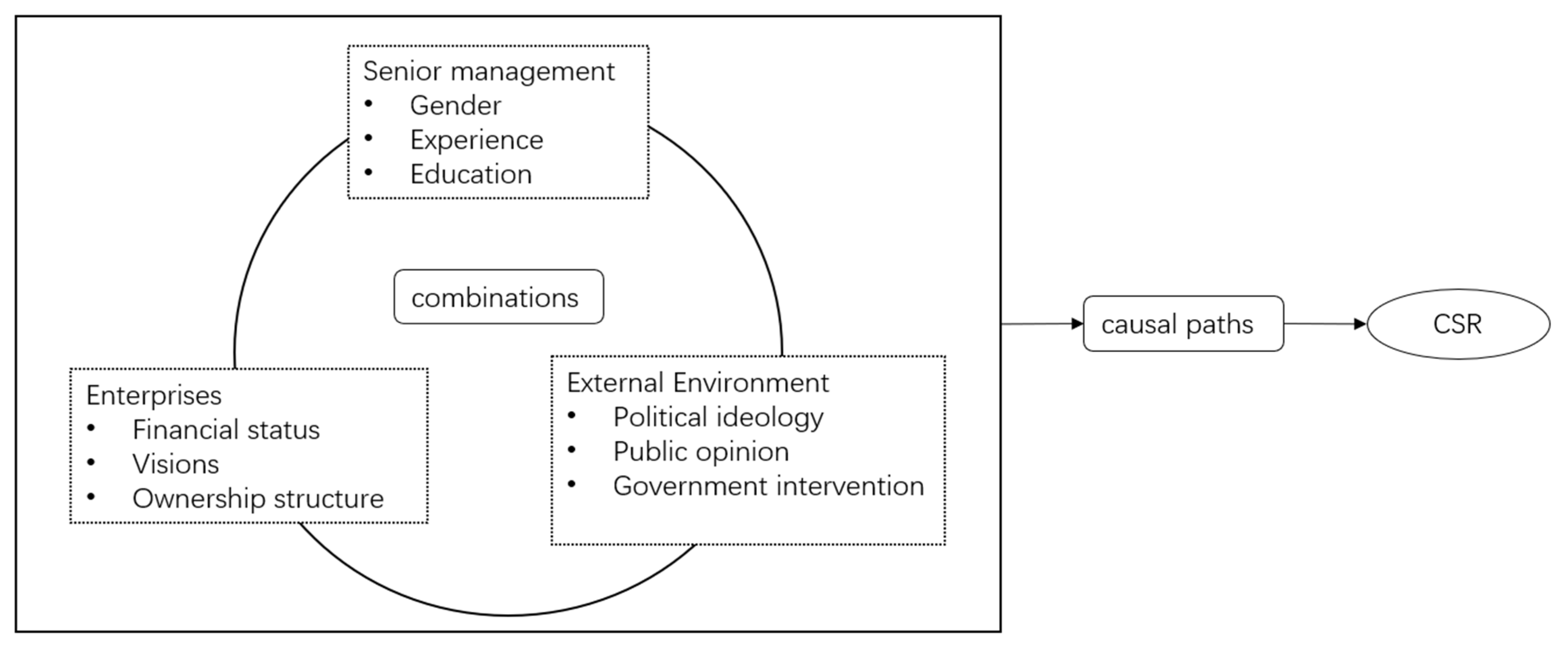

:1. Introduction

2. Literature Review

2.1. Senior Management and Environmental Impact

2.1.1. Personal Characteristics of Senior Executives

2.1.2. Senior Management Team and Corporate Governance Structure

2.1.3. Cultural Influence

2.2. Enterprise Level

2.2.1. The Ownership Structure of the Enterprise

2.2.2. Financial Status of Enterprises

2.2.3. Substantial Benefits Such as Economic Incentives

2.3. External Influences on the Enterprise

2.3.1. Public Opinion of the Enterprise

2.3.2. The Economic and Legal Environment of the Enterprise

2.3.3. Government Intervention in Enterprises

2.4. Ideological and Political Context

2.4.1. Party Membership and Political Participation

2.4.2. Party Organisations

2.5. Theory Framework and Hypothesis Development

3. Research Methods

3.1. QCA Methods

3.2. Advantages of QCA Methods

3.3. Specific QCA Method Selection

4. Data Collection and Construction

4.1. Data Collection

4.2. Data Construction

4.2.1. Outcome Variables

4.2.2. Conditional Variables

5. Data Analysis and Positive Results

5.1. Necessity Analysis of Individual Conditions

5.2. Sufficiency Analysis of the Conditional Configuration

6. Robustness Test

6.1. Methods Introduction

6.2. A Robustness Test Was Performed to Change the Consistency Threshold

6.2.1. Operation Method

6.2.2. Sufficiency Analysis of the Conditional Configuration

6.2.3. Data Results

6.3. Robustness Test with Censored Cases

6.3.1. Data Filtering

6.3.2. Necessity Analysis of Individual Conditions

6.3.3. Sufficiency Analysis of the Conditional Configuration

6.3.4. Data Results

6.4. Robustness Test Conclusion

7. Conclusions and Outlook

7.1. Review of Previous Literature

7.2. QCA Empirical Conclusions

- (1)

- “Profitability” is a necessary condition for enterprises to engage in CSR activities. That is, under general circumstances, if an enterprise wants to engage in CSR activities, it must make a profit that year. When the enterprise loses money in a given year, it will most likely not engage in CSR activities.

- (2)

- The simple solution of “women on the executive team” and “profitability” for the outcome variable of “enterprise has fulfilled its social responsibilities” plays a core role in each configuration path (intermediate solution). This view and the previous literature review suggest that having “female CEOs have a significantly enhancing effect on CSR performance” by McGuinness et al. [25] and that the “capital supply hypothesis” proposed by Preston and O’Bannon [48] are both confirmed.

- (3)

- A total of six configurations provide a path to a positive result for engagement in CSR activities. These configurations explain approximately 92% of the positive results, and approximately 83% of all the companies aligning with one of the six configurations engage in CSR activities.

- (4)

- For the first path (configuration 1), “enterprise profitable in the current year” plays a core role, while “Party member on the board” and “overseas background of leaders” play a key auxiliary role. Approximately 81.86% of all the cases with this configuration of conditions showed a positive result for “enterprise has fulfilled its social responsibilities”. Of all such positive cases, approximately 65.86% can be explained by this path, and approximately 3.10% of cases can be explained only by this path.

- (5)

- For the second path (configuration 2), “profitable in the current year” and “women on the senior management team” play a core role, and “overseas background of leaders” plays an auxiliary role. Approximately 83.75% of all the cases following this configuration of conditions showed a positive result for “enterprise has fulfilled its social responsibilities”. Of all such positive cases, approximately 52.03% can be explained by this path, and approximately 1.65% can be explained only by this path.

- (6)

- For the third path (configuration 3), “profitable in the current year” plays a core role, while “CSR vision of the enterprise” and “overseas background of leaders” play a supporting role. Approximately 82.56% of all the cases with this configuration of conditions showed a positive result for “enterprise has fulfilled its social responsibilities”. Of all such positive cases, approximately 70.14% can be explained by this path, and approximately 3.62% can be explained only by this path.

- (7)

- For the fourth path (configuration 4), “profitable in the current year” plays a core role, while “CSR vision of the enterprise” and “Party member on the board” play an auxiliary role. Approximately 81.07% of all the cases with this configuration of conditions showed a positive result for “enterprise has fulfilled its social responsibilities”. Of all such positive cases, approximately 63.01% can be explained by this path, and approximately 1.98% can be explained only by this path.

- (8)

- For the fifth path (configuration 5), “profitable in the current year” and “women on the senior management team” play a core role, while “CSR vision of the enterprise” plays a supporting role. Approximately 82.77% of all the cases with this configuration of conditions showed a positive result for “enterprise has fulfilled its social responsibilities”. Of all such positive cases, approximately 51.15% can be explained by this path, and approximately 2.52% of them can be explained only by this path.

- (9)

- For the sixth path (configuration 6), “women on the senior management team” plays a core role, while “Party members on the board”, “CSR vision of the enterprise” and “overseas background of leaders” play an auxiliary role. Approximately 80.94% of all the cases with this configuration of conditions showed a positive result for “enterprise has fulfilled its social responsibilities”. Of all such positive cases, approximately 37.76% can be explained by this path, and approximately 2.74% can be explained only by this path.

7.3. Theoretical and Practical Contribution

7.3.1. Theoretical Contribution

7.3.2. Practical Contribution

7.4. Study Limitations ad Future Outlook

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Shanghai Stock Exchange. Notice on Strengthening the Work of Social Responsibility of Listed Companies and Issuing the Guidelines on Environmental Information Disclosure of Listed Companies of Shanghai Stock Exchange. Available online: http://www.sse.com.cn/lawandrules/sserules/listing/stock/c/c_20150912_3985851.shtml (accessed on 13 May 2023).

- Shenzhen Stock Exchange. Guidelines on Social Responsibility of Listed Companies of Shenzhen Stock Exchange. Available online: http://www.szse.cn/disclosure/notice/general/t20060925_499697.html (accessed on 13 May 2023).

- State-Owned Assets Supervision and Administration Commission of the State Council. Guidelines on State-Owned Enterprises to Better Fulfill Their Social Responsibilities. Available online: http://www.sasac.gov.cn/n2588035/n2588320/n2588335/c20234205/content.html (accessed on 13 May 2023).

- Hollis; Edward, J.N. Rational Economic Man; Cambridge University Press: Cambridge, UK, 1975. [Google Scholar]

- Wagemann, C.; Buche, J.; Siewert, M.B. QCA and Business Research: Work in Progress or a Consolidated Agenda? J. Bus. Res. 2016, 69, 2531–2540. [Google Scholar] [CrossRef]

- Sun, M.; Wang, J.; Wen, T. Research on the Relationship between Shared Leadership and Individual Creativity-Qualitative Comparative Analysis on the Basis of Clear Set. Sustainability 2021, 13, 5445. [Google Scholar] [CrossRef]

- Carroll, A.B. A three-dimensional conceptual model of corporate performance. Acad. Manag. Rev. 1979, 4, 497–505. [Google Scholar] [CrossRef]

- McWilliams, A.; Siegel, D. Corporate social responsibility: A theory of the firm perspective. Acad. Manag. Rev. 2001, 26, 117–127. [Google Scholar] [CrossRef]

- McWilliams, A.; Siegel, D.S.; Wright, P.M. Corporate Social Responsibility: Strategic Implications. J. Manag. Stud. 2006, 43, 1–18. [Google Scholar] [CrossRef] [Green Version]

- Xu, S.; Yang, R. Indigenous Characteristics of Chinese Corporate Social Responsibility Conceptual Paradigm. J. Bus. Ethics 2010, 93, 321–333. [Google Scholar] [CrossRef]

- Campbell, D.; Moore, G.; Metzger, M. Corporate philanthropy in the U.K. 1985–2000 some empirical findings. J. Bus. Ethics 2002, 39, 29–41. [Google Scholar] [CrossRef]

- Minor, D.; Morgan, J. CSR as reputation insurance: Primum non nocere. Calif. Manag. Rev. 2011, 53, 40–59. [Google Scholar] [CrossRef] [Green Version]

- Martínez, P.; Rodríguez del Bosque, I. CSR and Customer Loyalty: The Roles of Trust, Customer Identification with the Company and Satisfaction. Int. J. Hosp. Manag. 2013, 35, 89–99. [Google Scholar] [CrossRef]

- Campbell, J.L. Why would corporations behave in socially responsible ways? An institutional theory of corporate social responsibility. Acad. Manag. Rev. 2007, 32, 946–967. [Google Scholar] [CrossRef]

- Gardberg, N.A.; Fombrun, C.J. Corporate citizenship: Creating intangible assets across institutional environments. Acad. Manag. Rev. 2006, 31, 329–346. [Google Scholar] [CrossRef] [Green Version]

- Garay, L.; Font, X. Doing Good to Do Well? Corporate Social Responsibility Reasons, Practices and Impacts in Small and Medium Accommodation Enterprises. Int. J. Hosp. Manag. 2012, 31, 329–337. [Google Scholar] [CrossRef] [Green Version]

- Groza, M.D.; Pronschinske, M.R.; Walker, M. Perceived Organizational Motives and Consumer Responses to Proactive and Reactive CSR. J. Bus. Ethics 2011, 102, 639–652. [Google Scholar] [CrossRef]

- Gold, N.O.; Taib, F.M.; Ma, Y. Firm-Level Attributes, Industry-Specific Factors, Stakeholder Pressure, and Country-Level Attributes: Global Evidence of What Inspires Corporate Sustainability Practices and Performance. Sustainability 2022, 14, 13222. [Google Scholar] [CrossRef]

- Dabic, M.; Colovic, A.; Lamotte, O.; Painter-Morland, M.; Brozovic, S. Industry-Specific CSR: Analysis of 20 Years of Research. Eur. Bus. Rev. 2016, 28, 250–273. [Google Scholar] [CrossRef] [Green Version]

- Nawrocki, T.L.; Szwajca, D. A Multidimensional Comparative Analysis of Involvement in CSR Activities of Energy Companies in the Context of Sustainable Development Challenges: Evidence from Poland. Energies 2021, 14, 4592. [Google Scholar] [CrossRef]

- Cai, Y.; Jo, H.; Pan, C. Doing Well While Doing Bad? CSR in Controversial Industry Sectors. J. Bus. Ethics 2012, 108, 467–480. [Google Scholar] [CrossRef]

- Thorisdottir, T.S.; Johannsdottir, L. Corporate Social Responsibility Influencing Sustainability within the Fashion Industry. A Systematic Review. Sustainability 2020, 12, 9167. [Google Scholar] [CrossRef]

- Shao, J.; Cherian, J.; Xu, L.; Zaheer, M.; Samad, S.; Comite, U.; Mester, L.; Badulescu, D. A CSR Perspective to Drive Employee Creativity in the Hospitality Sector: A Moderated Mediation Mechanism of Inclusive Leadership and Polychronicity. Sustainability 2022, 14, 6273. [Google Scholar] [CrossRef]

- Duarte, F. Working with Corporate Social Responsibility in Brazilian Companies: The Role of Managers’ Values in the Maintenance of CSR Cultures. J. Bus. Ethics 2010, 96, 355–368. [Google Scholar] [CrossRef]

- McGuinness, P.B.; Vieito, J.P.; Wang, M. The Role of Board Gender and Foreign Ownership in the CSR Performance of Chinese Listed Firms. J. Corp. Financ. 2017, 42, 75–99. [Google Scholar] [CrossRef] [Green Version]

- Engle, R.L. Corporate Social Responsibility in Host Countries: A Perspective from American Managers. Corp. Soc. Responsib. Environ. Manag. 2007, 14, 16–27. [Google Scholar] [CrossRef]

- Cronqvist, H.; Yu, F. Shaped by Their Daughters: Executives, Female Socialization, and Corporate Social Responsibility. J. Financ. Econ. 2017, 126, 543–562. [Google Scholar] [CrossRef]

- Chen, W.T.; Zhou, G.S.; Zhu, X.K. CEO Tenure and Corporate Social Responsibility Performance. J. Bus. Res. 2019, 95, 292–302. [Google Scholar] [CrossRef]

- McCarthy, S.; Oliver, B.; Song, S. Corporate Social Responsibility and CEO Confidence. J. Bank. Financ. 2017, 75, 280–291. [Google Scholar] [CrossRef] [Green Version]

- Hu, Y.; Zhang, Q.; Wang, X. Potentials of Top Management Team Career Development and Corporate Social Responsibility: A Study on Listed Manufacturing Companies in China. Career Dev. Int. 2019, 24, 560–579. [Google Scholar] [CrossRef]

- Huang, J.; Duan, Z.; Hu, M.; Li, Y. More Stable, More Sustainable: Does TMT Stability Affect Sustainable Corporate Social Responsibility? Emerg. Mark. Financ. Trade 2022, 58, 921–938. [Google Scholar] [CrossRef]

- El-Bassiouny, D.; Letmathe, P. The Adoption of CSR Practices in Egypt: Internal Efficiency or External Legitimation? Sustain. Account. Manag. Policy J. 2018, 9, 642–665. [Google Scholar] [CrossRef]

- Han, Y.; Chi, W.; Zhou, J. Prosocial Imprint: CEO Childhood Famine Experience and Corporate Philanthropic Donation. J. Bus. Res. 2022, 139, 1604–1618. [Google Scholar] [CrossRef]

- Liu, Y.; Quan, B.; Xu, Q.; Forrest, J.Y.-L. Corporate Social Responsibility and Decision Analysis in a Supply Chain through Government Subsidy. J. Clean. Prod. 2019, 208, 436–447. [Google Scholar] [CrossRef]

- Kong, X.; Zhang, X.; Yan, C.; Ho, K.-C. China’s Historical Imperial Examination System and Corporate Social Responsibility. Pac. -Basin Financ. J. 2022, 72, 101734. [Google Scholar] [CrossRef]

- Wang, H.; Wu, H.; Humphreys, P. Chinese Merchant Group Culture, Corporate Social Responsibility, and Cost of Debt: Evidence from Private Listed Firms in China. Sustainability 2022, 14, 2630. [Google Scholar] [CrossRef]

- Tang, L.; Li, H. Corporate Social Responsibility Communication of Chinese and Global Corporations in China. Public Relat. Rev. 2009, 35, 199–212. [Google Scholar] [CrossRef]

- Carroll, A.B. The pyramid of corporate social responsibility: Toward the moral management of organizational stakeholders. Bus. Horiz. 1991, 34, 39–48. [Google Scholar] [CrossRef]

- Hickman, L.E. Information Asymmetry in CSR Reporting: Publicly-Traded versus Privately-Held Firms. Sustain. Account. Manag. Policy J. 2020, 11, 207–232. [Google Scholar] [CrossRef]

- Zaid, M.A.A.; Abuhijleh, S.T.F.; Pucheta-Martínez, M.C. Ownership Structure, Stakeholder Engagement, and Corporate Social Responsibility Policies: The Moderating Effect of Board Independence. Corp. Soc. Responsib. Environ. Manag. 2020, 27, 1344–1360. [Google Scholar] [CrossRef]

- Garde-Sanchez, R.; López-Pérez, M.; López-Hernández, A. Current Trends in Research on Social Responsibility in State-Owned Enterprises: A Review of the Literature from 2000 to 2017. Sustainability 2018, 10, 2403. [Google Scholar] [CrossRef] [Green Version]

- Gallo, M.A. The family business and its social responsibilities. Fam. Bus. Rev. 2004, 17, 135–148. [Google Scholar] [CrossRef]

- Berrone, P.; Cruz, C.; Gomez-Mejia, L.R.; Kintana, M.L. Socioemotional wealth and corporate responses to institutional pressures: Do family-controlled firms pollute less? Adm. Sci. Q. 2010, 55, 82–113. [Google Scholar] [CrossRef]

- Sahasranamam, S.; Arya, B.; Sud, M. Ownership Structure and Corporate Social Responsibility in an Emerging Market. Asia. Pac. J. Manag. 2020, 37, 1165–1192. [Google Scholar] [CrossRef] [Green Version]

- Block, J.H.; Wagner, M. The Effect of Family Ownership on Different Dimensions of Corporate Social Responsibility: Evidence from Large US Firms: Effect of Family Ownership on Corporate Social Responsibility. Bus. Strategy Environ. 2014, 23, 475–492. [Google Scholar] [CrossRef]

- Lamb, N.H.; Butler, F.C. The Influence of Family Firms and Institutional Owners on Corporate Social Responsibility Performance. Bus. Soc. 2018, 57, 1374–1406. [Google Scholar] [CrossRef]

- Li, S.; Wu, H.; Song, X. Principal–Principal Conflicts and Corporate Philanthropy: Evidence from Chinese Private Firms. J. Bus. Ethics 2017, 141, 605–620. [Google Scholar] [CrossRef]

- Preston, L.E.; O’Bannon, D.P. The corporate social-financial performance relationship: A typology an analysis. Bus. Soc. 1997, 36, 419–429. [Google Scholar] [CrossRef]

- Otero-González, L.; Durán-Santomil, P.; Rodríguez-Gil, L.-I.; Lado-Sestayo, R. Does a Company’s Profitability Influence the Level of CSR Development? Sustainability 2021, 13, 3304. [Google Scholar] [CrossRef]

- Rowley, T.; Berman, S. A brand new brand of corporate social performance. Bus. Soc. 2000, 39, 397–418. [Google Scholar] [CrossRef]

- Margolis, J.D.; Walsh, J.P. Misery loves companies: Rethinking social initiatives by business. Adm. Sci. Q. 2003, 48, 268–305. [Google Scholar] [CrossRef] [Green Version]

- McGuire, J.B.; Sundgren, A.; Schneeweis, T. Corporate social responsibility and firm financial performance. Acad. Manag. J. 1988, 31, 854–872. [Google Scholar] [CrossRef]

- Awaysheh, A.; Heron, R.A.; Perry, T.; Wilson, J.I. On the Relation between Corporate Social Responsibility and Financial Performance. Strateg. Manag. J. 2020, 41, 965–987. [Google Scholar] [CrossRef]

- Flammer, C. Corporate Social Responsibility and Shareholder Reaction: The Environmental Awareness of Investors. Acad. Manag. J. 2013, 56, 758–781. [Google Scholar] [CrossRef] [Green Version]

- Thanki, H.; Shah, S.; Rathod, H.S.; Oza, A.D.; Burduhos-Nergis, D.D. I Am Ready to Invest in Socially Responsible Investments (SRI) Options Only If the Returns Are Not Compromised: Individual Investors’ Intentions toward SRI. Sustainability 2022, 14, 11377. [Google Scholar] [CrossRef]

- Zhang, Q.; Ahmad, S. Linking Corporate Social Responsibility, Consumer Identification and Purchasing Intention. Sustainability 2022, 14, 12552. [Google Scholar] [CrossRef]

- Lin, K.J.; Tan, J.; Zhao, L.; Karim, K. In the Name of Charity: Political Connections and Strategic Corporate Social Responsibility in a Transition Economy. J. Corp. Financ. 2015, 32, 327–346. [Google Scholar] [CrossRef]

- Kong, D.; Cheng, X.; Jiang, X. Effects of Political Promotion on Local Firms’ Social Responsibility in China. Econ. Model. 2021, 95, 418–429. [Google Scholar] [CrossRef]

- Kinderman, D. “Free Us up so We Can Be Responsible!” The Co-Evolution of Corporate Social Responsibility and Neo-Liberalism in the UK, 1977–2010. Socio-Econ. Rev. 2012, 10, 29–57. [Google Scholar] [CrossRef] [Green Version]

- Chen, J.C.; Patten, D.M.; Roberts, R.W. Corporate Charitable Contributions: A Corporate Social Performance or Legitimacy Strategy? J. Bus. Ethics 2008, 82, 131–144. [Google Scholar] [CrossRef]

- Gong, G.; Huang, X.; Wu, S.; Tian, H.; Li, W. Punishment by securities regulators, corporate social responsibility and the cost of debt. J. Bus. Ethics 2020, 171, 337–356. [Google Scholar] [CrossRef]

- Vashchenko, M. An External Perspective on CSR: What Matters and What Does Not? Bus. Ethics A Eur. Rev. 2017, 26, 396–412. [Google Scholar] [CrossRef]

- Zhang, Z.; Chen, H. Media Coverage and Impression Management in Corporate Social Responsibility Reports: Evidence from China. Sustain. Account. Manag. Policy J. 2019, 11, 863–886. [Google Scholar] [CrossRef]

- Zyglidopoulos, S.C.; Georgiadis, A.P.; Carroll, C.E.; Siegel, D.S. Does Media Attention Drive Corporate Social Responsibility? J. Bus. Res. 2012, 65, 1622–1627. [Google Scholar] [CrossRef]

- Grunig, J.E. A New Measure of Public Opinion on Corporate Social Responsibility. Acad. Manag. J. 1979, 22, 738–764. [Google Scholar] [CrossRef]

- Vanhamme, J.; Grobben, B. “Too Good to Be True!”. The Effectiveness of CSR History in Countering Negative Publicity. J. Bus. Ethics 2009, 85, 273–283. [Google Scholar] [CrossRef]

- Lu, Q.; Chen, S.; Chen, P. The Relationship between Female Top Managers and Corporate Social Responsibility in China: The Moderating Role of the Marketization Level. Sustainability 2020, 12, 7730. [Google Scholar] [CrossRef]

- Zhang, C.; Liu, Q.; Ge, G.; Hao, Y.; Hao, H. The Impact of Government Intervention on Corporate Environmental Performance: Evidence from China’s National Civilized City Award. Financ. Res. Lett. 2021, 39, 101624. [Google Scholar] [CrossRef]

- Albareda, L.; Lozano, J.M.; Tencati, A.; Midttun, A.; Perrini, F. The Changing Role of Governments in Corporate Social Responsibility: Drivers and Responses. Bus. Ethics A Eur. Rev. 2008, 17, 347–363. [Google Scholar] [CrossRef]

- Yan, Y.; Xu, X. Does Entrepreneur Invest More in Environmental Protection When Joining the Communist Party? Evidence from Chinese Private Firms. Emerg. Mark. Financ. Trade 2022, 58, 754–775. [Google Scholar] [CrossRef]

- Liu, H.; Luo, J. Legacy of Ideology: The Enduring Effect of CEOs’ Socialist Ideological Imprint on Private Firms’ Employee-Related CSR. J. Bus. Res. 2022, 147, 491–504. [Google Scholar] [CrossRef]

- Gustafsson, B.; Yang, X.; Shuge, G.; Jianzhong, D. Charitable Donations by China’s Private Enterprises. Econ. Syst. 2017, 41, 456–469. [Google Scholar] [CrossRef] [Green Version]

- Zhou, P.; Arndt, F.; Jiang, K.; Dai, W. Looking Backward and Forward: Political Links and Environmental Corporate Social Responsibility in China. J. Bus. Ethics 2021, 169, 631–649. [Google Scholar] [CrossRef]

- Zhang, H.; Li, L.; Fan, C.; Hang, Z.; Khan, H.u.R. How Does Corporate Party Committee Governance Affect Charitable Donations? Evidence from Heavy-Pollution Industries in China. Sustainability 2021, 13, 12242. [Google Scholar] [CrossRef]

- Yan, Y.; Xu, X. The Role of Communist Party Branch in Employment Protection: Evidence from Chinese Private Firms. Asia-Pac. J. Account. Econ. 2022, 29, 1518–1539. [Google Scholar] [CrossRef]

- Dong, Z.; Luo, Z.; Wei, X. Social Insurance with Chinese Characteristics: The Role of Communist Party in Private Firms. China Econ. Rev. 2016, 37, 40–51. [Google Scholar] [CrossRef]

- Cheng, Z. Communist Party Branch and Labour Rights: Evidence from Chinese Entrepreneurs. China Econ. Rev. 2022, 71, 101730. [Google Scholar] [CrossRef]

- Scott, W.R. Organizations: Rational, Natural, and Open Systems; Prentice Hall Inc.: Englewood Cliffs, NJ, USA, 1981. [Google Scholar]

- Ragin, C. The Comparative Method: Moving Beyond Qualitative and Quantitative Strategies; University of California Press: Berkeley, CA, USA, 1987. [Google Scholar]

- Ragin, C.C.; Davey, S. Fuzzy-Set/Qualitative Comparative Analysis 4.0; Department of Sociology, University of California: Irvine, CA, USA, 2022. [Google Scholar]

- Ragin, C.C. How to Lure Analytic Social Science Out of the Doldrums: Some Lessons from Comparative Research. Int. Sociol. 2006, 21, 633–646. [Google Scholar] [CrossRef]

- Schneider, C.Q.; Wagemann, C. Set-Theoretic Methods for the Social Sciences: A Guide to Qualitative Comparative Analysis; Cambridge University Press: Cambridge, UK, 2012. [Google Scholar]

- Pappas, I.O.; Woodside, A.G. Fuzzy-Set Qualitative Comparative Analysis (FsQCA): Guidelines for Research Practice in Information Systems and Marketing. Int. J. Inf. Manag. 2021, 58, 102310. [Google Scholar] [CrossRef]

- Chin, M.K.; Hambrick, D.C.; Treviño, L.K. Political Ideologies of CEOs: The Influence of Executives’ Values on Corporate Social Responsibility. Adm. Sci. Q. 2013, 58, 197–232. [Google Scholar] [CrossRef]

- Di Giuli, A.; Kostovetsky, L. Are Red or Blue Companies More Likely to Go Green? Politics and Corporate Social Responsibility. J. Financ. Econ. 2014, 111, 158–180. [Google Scholar] [CrossRef]

- Gupta, A.; Briscoe, F.; Hambrick, D.C. Red, Blue, and Purple Firms: Organizational Political Ideology and Corporate Social Responsibility: Organizational Political Ideology and Corporate Social Responsibility. Strateg. Manag. J. 2017, 38, 1018–1040. [Google Scholar] [CrossRef]

- Nakagoshi, M.; Inamasu, K. The Role of System Justification Theory in Support of the Government under Long-Term Conservative Party Dominance in Japan. Front. Psychol. 2023, 14, 909022. [Google Scholar] [CrossRef]

- Lipscy, P.Y.; Scheiner, E. Japan Under the DPJ: The Paradox of Political Change without Policy Change. J. East Asian Stud. 2012, 12, 311–322. [Google Scholar] [CrossRef] [Green Version]

- Watanabe, R. Breaking Iron Triangles: Beliefs and Interests in Japanese Renewable Energy Policy. Soc. Sci. Jpn. J. 2021, 24, 9–44. [Google Scholar] [CrossRef]

{kind=link}

| Outcome Variable | The Portion of Donations in EBITDA | Variable Assignment |

|---|---|---|

| Enterprise has fulfilled its social responsibilities | More than one in ten thousand | 1 |

| Less than zero | 1 | |

| Enterprise has not fulfilled its social responsibilities | Simultaneously more than or equal to zero and less than one in ten thousand | 0 |

| Conditional Variable | Variable Definition | Variable Assignment |

|---|---|---|

| Party member on the board | Enterprise board includes Party members | 1 |

| Enterprise board does not include Party members | 0 | |

| Women on the senior management team (or female executives) | The corporate executive team includes women | 1 |

| The corporate executive team does not include women | 0 | |

| CSR vision of the enterprise | Company already has ideas, a vision or values regarding its economic, social and environmental responsibilities | 1 |

| Company has no ideas, vision, or values regarding its economic, social, or environmental responsibilities | 0 | |

| Overseas background among leaders | Business leaders have an overseas background | 1 |

| There is no overseas background among business leaders | 0 | |

| Enterprise profitable in current year (simple profit) | Enterprise made a profit in the current year | 1 |

| Enterprise did not make a profit in the current year | 0 |

| Fulfil CSR | Failure to Fulfil CSR | |||

|---|---|---|---|---|

| Conditional Variable | Consistency | Coverage | Consistency | Coverage |

| There is Party member on the board | 0.785950 | 0.809955 | 0.861538 | 0.190045 |

| There is no Party member on the board | 0.214050 | 0.878378 | 0.138462 | 0.121622 |

| There is at least one woman on the senior management team | 0.658617 | 0.835655 | 0.605128 | 0.164345 |

| There are no women on the senior management team | 0.341383 | 0.801546 | 0.394872 | 0.198454 |

| The company has a CSR vision | 0.863886 | 0.816390 | 0.907692 | 0.183610 |

| The company has no CSR vision | 0.136114 | 0.873239 | 0.092308 | 0.126761 |

| At least one board member has an overseas background | 0.128430 | 0.812500 | 0.138462 | 0.187500 |

| No board members have an overseas background | 0.871570 | 0.825364 | 0.861538 | 0.174636 |

| Company was profitable in the current year | 0.923161 | 0.829389 | 0.887179 | 0.170611 |

| The company was not profitable in the current year | 0.076839 | 0.760870 | 0.112821 | 0.239130 |

| Party Member on the Board | Women on the Senior Management Team | CSR Vision of the Enterprise | Overseas Background Among Leaders | Enterprise Profitable in the Current Year | Number | Raw Consist | PRI Consist | SYM Consist |

|---|---|---|---|---|---|---|---|---|

| 0 | 1 | 0 | 1 | 1 | 5 | 1 | 1 | 1 |

| 0 | 1 | 1 | 1 | 0 | 3 | 1 | 1 | 1 |

| 0 | 0 | 0 | 0 | 0 | 2 | 1 | 1 | 1 |

| 0 | 1 | 0 | 0 | 0 | 2 | 1 | 1 | 1 |

| 1 | 0 | 0 | 0 | 0 | 1 | 1 | 1 | 1 |

| 0 | 1 | 0 | 1 | 0 | 1 | 1 | 1 | 1 |

| 0 | 0 | 1 | 1 | 1 | 14 | 0.928571 | 0.928571 | 0.928571 |

| 0 | 1 | 1 | 0 | 1 | 96 | 0.90625 | 0.90625 | 0.90625 |

| 0 | 1 | 1 | 0 | 0 | 9 | 0.888889 | 0.888889 | 0.888889 |

| 1 | 0 | 0 | 0 | 1 | 32 | 0.875 | 0.875 | 0.875 |

| 1 | 1 | 0 | 0 | 0 | 8 | 0.875 | 0.875 | 0.875 |

| 1 | 1 | 0 | 1 | 1 | 7 | 0.857143 | 0.857143 | 0.857143 |

| 1 | 1 | 0 | 0 | 1 | 62 | 0.854839 | 0.854839 | 0.854839 |

| 0 | 0 | 1 | 0 | 1 | 39 | 0.846154 | 0.846154 | 0.846154 |

| 1 | 1 | 1 | 1 | 1 | 45 | 0.822222 | 0.822222 | 0.822222 |

| 1 | 1 | 1 | 1 | 0 | 11 | 0.818182 | 0.818182 | 0.818182 |

| 1 | 0 | 1 | 0 | 1 | 246 | 0.813008 | 0.813008 | 0.813008 |

| 1 | 1 | 1 | 0 | 1 | 393 | 0.811705 | 0.811705 | 0.811705 |

| 0 | 1 | 1 | 1 | 1 | 29 | 0.793103 | 0.793103 | 0.793103 |

| 1 | 1 | 1 | 0 | 0 | 32 | 0.78125 | 0.78125 | 0.78125 |

| 1 | 0 | 1 | 1 | 1 | 24 | 0.75 | 0.75 | 0.75 |

| 1 | 0 | 0 | 1 | 1 | 3 | 0.666667 | 0.666667 | 0.666667 |

| 1 | 0 | 1 | 0 | 0 | 18 | 0.611111 | 0.611111 | 0.611111 |

| 0 | 0 | 0 | 0 | 1 | 4 | 0.5 | 0.5 | 0.5 |

| 0 | 0 | 1 | 0 | 0 | 3 | 0.333333 | 0.333333 | 0.333333 |

| 1 | 0 | 1 | 1 | 0 | 2 | 0 | 0 | 0 |

| 0 | 0 | 0 | 1 | 0 | 0 | |||

| 1 | 1 | 0 | 1 | 0 | 0 | |||

| 0 | 0 | 1 | 1 | 0 | 0 | |||

| 0 | 0 | 0 | 1 | 1 | 0 |

| Party Member on the Board | Women on the Senior Management Team | CSR Vision of the Enterprise | Overseas Background among Leaders | Enterprise Profitable in the Current Year | Number | Result | Raw Consist | PRI Consist | SYM Consist |

|---|---|---|---|---|---|---|---|---|---|

| 0 | 1 | 1 | 0 | 1 | 96 | 1 | 0.90625 | 0.90625 | 0.90625 |

| 1 | 0 | 0 | 0 | 1 | 32 | 1 | 0.875 | 0.875 | 0.875 |

| 1 | 1 | 0 | 0 | 1 | 62 | 1 | 0.854839 | 0.854839 | 0.854839 |

| 0 | 0 | 1 | 0 | 1 | 39 | 1 | 0.846154 | 0.846154 | 0.846154 |

| 1 | 1 | 1 | 1 | 1 | 45 | 1 | 0.822222 | 0.822222 | 0.822222 |

| 1 | 0 | 1 | 0 | 1 | 246 | 1 | 0.813008 | 0.813008 | 0.813008 |

| 1 | 1 | 1 | 0 | 1 | 393 | 1 | 0.811705 | 0.811705 | 0.811705 |

| 0 | 1 | 1 | 1 | 1 | 29 | 1 | 0.793103 | 0.793103 | 0.793103 |

| 1 | 1 | 1 | 0 | 0 | 32 | 1 | 0.78125 | 0.78125 | 0.78125 |

| 1 | 0 | 1 | 1 | 1 | 24 | 1 | 0.75 | 0.75 | 0.75 |

| 1 | 0 | 1 | 0 | 0 | 18 | 0 | 0.611111 | 0.611111 | 0.611111 |

| Condition Configuration | Raw Coverage | Unique Coverage | Consistency |

|---|---|---|---|

| Female executive | 0.658617 | 0.0603732 | 0.835655 |

| Profitable | 0.923161 | 0.324918 | 0.829389 |

| Solution coverage | 0.983535 | ||

| Solution consistency | 0.82963 | ||

| Condition Configuration | Raw Coverage | Unique Coverage | Consistency |

|---|---|---|---|

| Party member on board * ~ overseas background * profitable | 0.658617 | 0.0307355 | 0.818554 |

| Female executive * ~ overseas background * profitable | 0.520307 | 0.0164654 | 0.837456 |

| CSR vision * ~ overseas background * profitable | 0.701427 | 0.0362239 | 0.825581 |

| Party member on board * CSR vision * profitable | 0.630077 | 0.0197585 | 0.810734 |

| Female executive * CSR vision * profitable | 0.511526 | 0.025247 | 0.827709 |

| Party member on board * female executive * CSR vision * ~ overseas background | 0.377607 | 0.0274424 | 0.809412 |

| Solution coverage | 0.919868 | ||

| Solution consistency | 0.827246 | ||

| Condition Configuration | Configuration 1 | Configuration 2 | Configuration 3 | Configuration 4 | Configuration 5 | Configuration 6 |

|---|---|---|---|---|---|---|

| Party member on board | ♦ | ♦ | ♦ | |||

| Female executive | ⬤ | ⬤ | ⬤ | |||

| CSR vision | ♦ | ♦ | ♦ | ♦ | ||

| Overseas background | ⊗ | ⊗ | ⊗ | ⊗ | ||

| Profitable | ⬤ | ⬤ | ⬤ | ⬤ | ⬤ | |

| Consistency | 0.818554 | 0.837456 | 0.825581 | 0.810734 | 0.827709 | 0.809412 |

| Raw coverage | 0.658617 | 0.520307 | 0.701427 | 0.630077 | 0.511526 | 0.377607 |

| Unique coverage | 0.0307355 | 0.0164654 | 0.0362239 | 0.0197585 | 0.025247 | 0.0274424 |

| Solution coverage | 0.919868 | |||||

| Solution consistency | 0.827246 | |||||

| Party Member on Board | Female Executive | CSR Vision | Overseas Background | Profitable | Number | Result | Raw Consist | PRI Consist | SYM Consist |

|---|---|---|---|---|---|---|---|---|---|

| 0 | 1 | 0 | 0 | 1 | 15 | 1 | 1 | 1 | 1 |

| 0 | 1 | 1 | 0 | 1 | 96 | 1 | 0.90625 | 0.90625 | 0.90625 |

| 1 | 0 | 0 | 0 | 1 | 32 | 1 | 0.875 | 0.875 | 0.875 |

| 1 | 1 | 0 | 0 | 1 | 62 | 1 | 0.854839 | 0.854839 | 0.854839 |

| 0 | 0 | 1 | 0 | 1 | 39 | 1 | 0.846154 | 0.846154 | 0.846154 |

| 1 | 1 | 1 | 1 | 1 | 45 | 1 | 0.822222 | 0.822222 | 0.822222 |

| 1 | 0 | 1 | 0 | 1 | 246 | 1 | 0.813008 | 0.813008 | 0.813008 |

| 1 | 1 | 1 | 0 | 1 | 393 | 1 | 0.811705 | 0.811705 | 0.811705 |

| 0 | 1 | 1 | 1 | 1 | 29 | 0 | 0.793103 | 0.793103 | 0.793103 |

| 1 | 1 | 1 | 0 | 0 | 32 | 0 | 0.78125 | 0.78125 | 0.78125 |

| 1 | 0 | 1 | 1 | 1 | 24 | 0 | 0.75 | 0.75 | 0.75 |

| 1 | 0 | 1 | 0 | 0 | 18 | 0 | 0.611111 | 0.611111 | 0.611111 |

| Condition Configuration | Raw Coverage | Unique Coverage | Consistency |

|---|---|---|---|

| ~ Overseas background * Profitable | 0.809001 | 0.400659 | 0.830891 |

| Party member on board * female executive * ~ overseas background | 0.0570801 | 0.00987929 | 0.825397 |

| Party member on board * female executive * profitable | 0.455543 | 0 | 0.81854 |

| Solution coverage | 0.866081 | ||

| Solution consistency | 0.830526 | ||

| Condition Configuration | Raw Coverage | Unique Coverage | Consistency |

|---|---|---|---|

| Party member on board * ~ overseas background * profitable | 0.658617 | 0.0307354 | 0.818554 |

| Female executive * ~ overseas background * profitable | 0.520307 | 0.0164654 | 0.837456 |

| CSR vision * ~ overseas background * profitable | 0.701427 | 0.0362239 | 0.825581 |

| Party member on board * female executive * CSR vision * profitable | 0.390779 | 0.0406147 | 0.812785 |

| Solution coverage | 0.84742 | ||

| Solution consistency | 0.831897 | ||

| Fulfilled Its CSR | Failed to Fulfil Its CSR | |||

|---|---|---|---|---|

| Conditional Variable | Consistency | Coverage | Consistency | Coverage |

| Party member on board | 0.788079 | 0.802247 | 0.880000 | 0.197753 |

| No Party member on board | 0.211921 | 0.888889 | 0.120000 | 0.111111 |

| Female executives | 0.651214 | 0.828652 | 0.610000 | 0.171348 |

| No female executives | 0.348786 | 0.802030 | 0.390000 | 0.197970 |

| CSR vision | 0.854305 | 0.816456 | 0.870000 | 0.183544 |

| No CSR vision | 0.145695 | 0.835443 | 0.130000 | 0.164557 |

| Overseas background | 0.110375 | 0.781250 | 0.140000 | 0.218750 |

| No overseas background | 0.889625 | 0.824131 | 0.860000 | 0.175869 |

| Profitable | 0.938190 | 0.825243 | 0.900000 | 0.174757 |

| Not profitable | 0.061810 | 0.736842 | 0.100000 | 0.263158 |

| Party Member on Board | Female Executive | CSR Vision | Overseas Background | Profitable | Number | Raw Consist | PRI Consist | SYM Consist |

|---|---|---|---|---|---|---|---|---|

| 0 | 1 | 0 | 0 | 1 | 8 | 1 | 1 | 1 |

| 0 | 0 | 1 | 1 | 1 | 5 | 1 | 1 | 1 |

| 0 | 1 | 0 | 1 | 1 | 4 | 1 | 1 | 1 |

| 1 | 1 | 0 | 0 | 0 | 2 | 1 | 1 | 1 |

| 0 | 1 | 0 | 0 | 0 | 1 | 1 | 1 | 1 |

| 0 | 1 | 0 | 1 | 0 | 1 | 1 | 1 | 1 |

| 0 | 1 | 1 | 1 | 0 | 1 | 1 | 1 | 1 |

| 0 | 1 | 1 | 0 | 1 | 49 | 0.959184 | 0.959184 | 0.959184 |

| 1 | 1 | 1 | 0 | 0 | 16 | 0.875 | 0.875 | 0.875 |

| 1 | 0 | 1 | 0 | 1 | 127 | 0.834646 | 0.834646 | 0.834646 |

| 1 | 1 | 0 | 0 | 1 | 36 | 0.833333 | 0.833333 | 0.833333 |

| 1 | 0 | 1 | 1 | 1 | 10 | 0.8 | 0.8 | 0.8 |

| 1 | 1 | 1 | 0 | 1 | 196 | 0.795918 | 0.795918 | 0.795918 |

| 1 | 0 | 0 | 0 | 1 | 19 | 0.789474 | 0.789474 | 0.789474 |

| 0 | 0 | 1 | 0 | 1 | 19 | 0.789474 | 0.789474 | 0.789474 |

| 0 | 1 | 1 | 1 | 1 | 13 | 0.769231 | 0.769231 | 0.769231 |

| 1 | 1 | 1 | 1 | 1 | 21 | 0.761905 | 0.761905 | 0.761905 |

| 0 | 1 | 1 | 0 | 0 | 3 | 0.666667 | 0.666667 | 0.666667 |

| 1 | 0 | 0 | 1 | 1 | 3 | 0.666667 | 0.666667 | 0.666667 |

| 1 | 1 | 0 | 1 | 1 | 3 | 0.666667 | 0.666667 | 0.666667 |

| 1 | 0 | 1 | 0 | 0 | 9 | 0.555556 | 0.555556 | 0.555556 |

| 0 | 0 | 1 | 0 | 0 | 2 | 0.5 | 0.5 | 0.5 |

| 1 | 1 | 1 | 1 | 0 | 2 | 0.5 | 0.5 | 0.5 |

| 0 | 0 | 0 | 0 | 1 | 2 | 0.5 | 0.5 | 0.5 |

| 1 | 0 | 1 | 1 | 0 | 1 | 0 | 0 | 0 |

| 0 | 0 | 0 | 0 | 0 | 0 | |||

| 1 | 0 | 0 | 0 | 0 | 0 | |||

| 0 | 0 | 0 | 1 | 0 | 0 | |||

| 1 | 0 | 0 | 1 | 0 | 0 | |||

| 1 | 1 | 0 | 1 | 0 | 0 | |||

| 0 | 0 | 1 | 1 | 0 | 0 | |||

| 0 | 0 | 0 | 1 | 1 | 0 |

| Party Member on Board | Female Executive | CSR Vision | Overseas Background | Profitable | Number | Result | Raw Consist | PRI Consist | SYM Consist |

|---|---|---|---|---|---|---|---|---|---|

| 0 | 1 | 0 | 0 | 1 | 8 | 1 | 1 | 1 | 1 |

| 0 | 1 | 1 | 0 | 1 | 49 | 1 | 0.959184 | 0.959184 | 0.959184 |

| 1 | 1 | 1 | 0 | 0 | 16 | 1 | 0.875 | 0.875 | 0.875 |

| 1 | 0 | 1 | 0 | 1 | 127 | 1 | 0.834646 | 0.834646 | 0.834646 |

| 1 | 1 | 0 | 0 | 1 | 36 | 1 | 0.833333 | 0.833333 | 0.833333 |

| 1 | 0 | 1 | 1 | 1 | 10 | 1 | 0.8 | 0.8 | 0.8 |

| 1 | 1 | 1 | 0 | 1 | 196 | 1 | 0.795918 | 0.795918 | 0.795918 |

| 1 | 0 | 0 | 0 | 1 | 19 | 1 | 0.789474 | 0.789474 | 0.789474 |

| 0 | 0 | 1 | 0 | 1 | 19 | 1 | 0.789474 | 0.789474 | 0.789474 |

| 0 | 1 | 1 | 1 | 1 | 13 | 1 | 0.769231 | 0.769231 | 0.769231 |

| 1 | 1 | 1 | 1 | 1 | 21 | 1 | 0.761905 | 0.761905 | 0.761905 |

| 1 | 0 | 1 | 0 | 0 | 9 | 0 | 0.555556 | 0.555556 | 0.555556 |

| Condition Configuration | Raw Coverage | Unique Coverage | Consistency |

|---|---|---|---|

| Female executive | 0.651214 | 0.0485651 | 0.828652 |

| Profitable | 0.93819 | 0.335541 | 0.825243 |

| Solution coverage | 0.986755 | ||

| Solution consistency | 0.826248 | ||

| Condition Configuration | Raw Coverage | Unique Coverage | Consistency |

|---|---|---|---|

| Party member on board * ~ overseas background * profitable | 0.677704 | 0.0331126 | 0.812169 |

| Female executive * ~ overseas background * profitable | 0.532009 | 0.0176601 | 0.83391 |

| CSR vision * ~ overseas background * profitable | 0.715232 | 0.0331126 | 0.828645 |

| Party member on board * CSR vision * profitable | 0.631347 | 0.0176601 | 0.80791 |

| Female executive * CSR vision * profitable | 0.505519 | 0.0220751 | 0.820789 |

| Party member on board * female executive * CSR vision * ~ overseas background | 0.375276 | 0.0309051 | 0.801887 |

| Solution coverage | 0.93819 | ||

| Solution consistency | 0.826848 | ||

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Xiong, F.; Shao, Y.; Fan, H.; Xie, Y. Analysis of the Motivation behind Corporate Social Responsibility Based on the csQCA Approach. Sustainability 2023, 15, 10622. https://doi.org/10.3390/su151310622

Xiong F, Shao Y, Fan H, Xie Y. Analysis of the Motivation behind Corporate Social Responsibility Based on the csQCA Approach. Sustainability. 2023; 15(13):10622. https://doi.org/10.3390/su151310622

Chicago/Turabian StyleXiong, Feng, Yaxin Shao, Haotian Fan, and Yi Xie. 2023. "Analysis of the Motivation behind Corporate Social Responsibility Based on the csQCA Approach" Sustainability 15, no. 13: 10622. https://doi.org/10.3390/su151310622