Current Development Status, Policy Support and Promotion Path of China’s Green Hydrogen Industries under the Target of Carbon Emission Peaking and Carbon Neutrality

Abstract

:1. Introduction

2. The Advantages of Green Hydrogen Industry

2.1. Classifications of Hydrogen Energy

2.2. Advantages of Green Hydrogen Industry

3. Overview of the Green Hydrogen Industry in Overseas Regions

3.1. The U.S. Focuses on Building a Holistic Chain of the Green Hydrogen Industry and Frontier Technologies Development

3.2. The EU Has Laid out a Clear Roadmap for Developing a Green Hydrogen Industry

3.3. Japan Actively Guides the Coupling and Synergistic Development of the Green Hydrogen Industry with Advantageous Industries

4. China’s Green Hydrogen Industrial Policies and Its Development Advantages

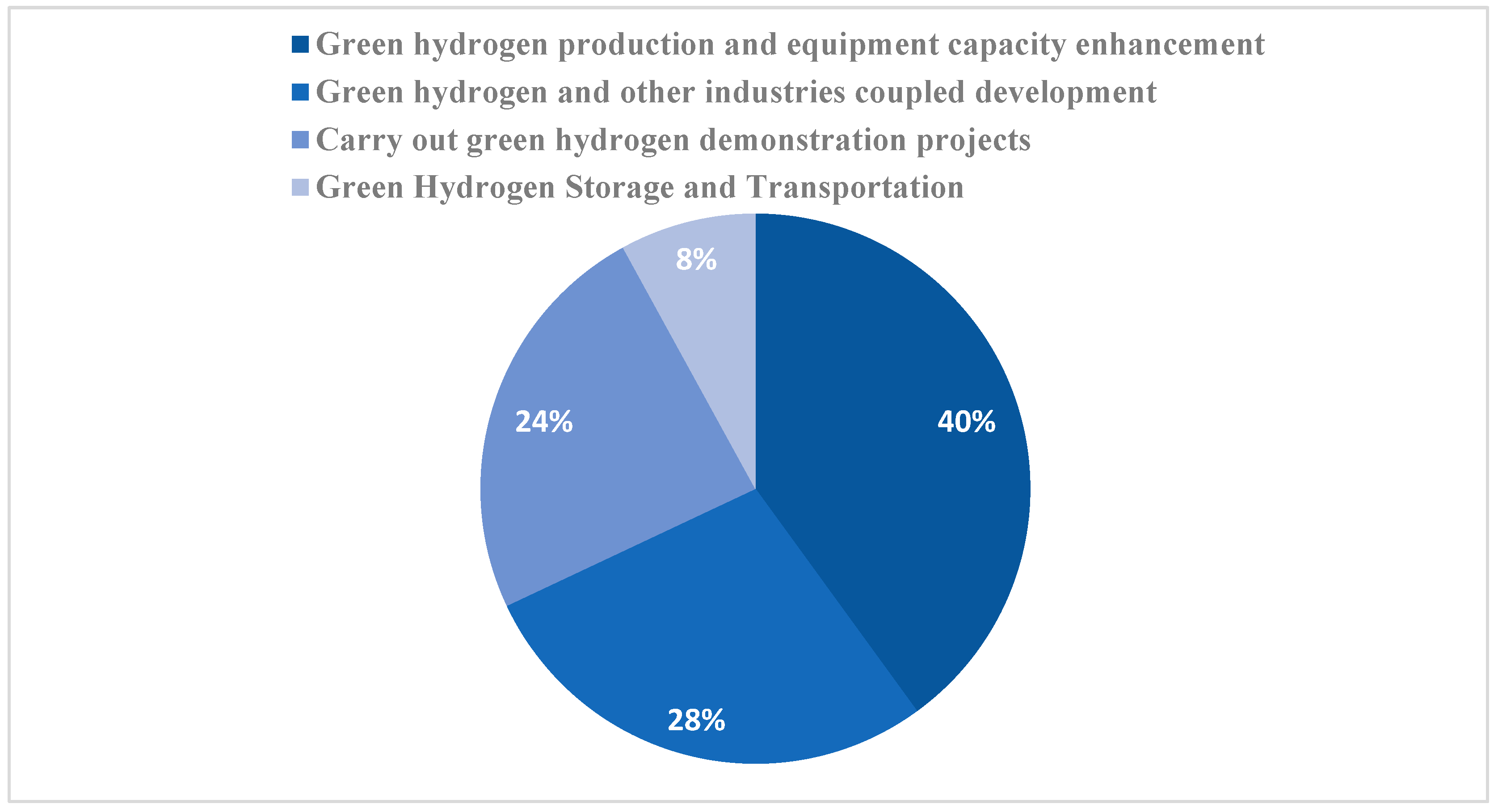

4.1. The Green Hydrogen Industry Policy Released by Central Authorities

4.2. The Green Hydrogen Industry Policy Released by Non-Central Authorities

4.3. Enormous Potential for Developing the Green Hydrogen Industry

4.4. Abundant Renewable Energy Resources and Commercialisation Experience

4.5. Robust Infrastructure and Technological Innovation Capacity

4.6. Demand for Large-Scale Applications of Green Hydrogen in Traditional Industries

5. Key Bottlenecks in the Development of China’s Green Hydrogen Industry

5.1. Lack of Clarity on the Strategic Position of the Dual Carbon Goals

5.2. Low Competitiveness in Green Hydrogen Production

5.3. Heavy Reliance on Imports of PEMs, Perfluorosulfonic Acid Resins (PFSR), Catalysts, etc.

5.4. The Development Dilemma Facing the Whole Green Hydrogen Chain

6. Improvement of China’s Hydrogen Production Industry

6.1. Clarify the Important Role of Green Hydrogen Production in China’s Dual Carbon Goals

6.2. Enhance the Core Technology and Equipment of Green Hydrogen

6.3. Improve the Green Hydrogen Industry Chain

6.4. Clarify the Administrative Oversight in the Green Hydrogen Chain

6.5. Improve of Financial Support Mechanism

6.6. Enhance the Safety Supervision of the Green Hydrogen Industry Chain

7. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Dong, L.; Miao, G.; Wen, W. China’s carbon neutrality policy: Objectives, impacts and paths. East Asian Policy 2021, 13, 5–18. [Google Scholar] [CrossRef]

- Hu, Y.; Chi, Y.; Zhou, W.; Wang, Z.; Yuan, Y.; Li, R. Research on energy structure optimization and carbon emission reduction path in Beijing under the Dual Carbon Target. Energies 2022, 15, 5954. [Google Scholar] [CrossRef]

- Velazquez Abad, A.; Dodds, P.E. Green hydrogen characterisation initiatives: Definitions, standards, guarantees of origin, and challenges. Energy Policy 2020, 138, 111300. [Google Scholar] [CrossRef]

- Sazali, N. Emerging technologies by hydrogen: A review. Int. J. Hydrogen Energy 2020, 45, 18753–18771. [Google Scholar] [CrossRef]

- Lee, D.H. Development and environmental impact of hydrogen supply chain in Japan: Assessment by the CGE-LCA method in Japan with a discussion of the importance of biohydrogen. Int. J. Hydrogen Energy 2014, 39, 19294–19310. [Google Scholar] [CrossRef]

- Noussan, M.; Raimondi, P.P.; Scita, R.; Hafner, M. The role of green and blue hydrogen in the energy transition—A technological and geopolitical perspective. Sustainability 2020, 13, 298. [Google Scholar] [CrossRef]

- Liu, W.; Wan, Y.M.; Xiong, Y.L.; Gao, P.B. Green hydrogen standard in China: Standard and evaluation of low-carbon hydrogen, clean hydrogen, and renewable hydrogen. Int. J. Hydrogen Energy 2022, 47, 24584–24591. [Google Scholar] [CrossRef]

- Eicke, L.; De Blasio, N. Green hydrogen value chains in the industrial sector—Geopolitical and market implications. Energy Res. Soc. Sci. 2022, 93, 102847. [Google Scholar] [CrossRef]

- Yu, M.; Wang, K.; Vredenburg, H. Insights into low-carbon hydrogen production methods: Green, Blue and Aqua Hydrogen. Int. J. Hydrogen Energy 2021, 46, 21261–21273. [Google Scholar] [CrossRef]

- Allied Market Research. Green Hydrogen Market Outlook 2028. Available online: https://www.Alliedmarketresearch.com/green-hydrogen-market-A11310 (accessed on 2 February 2023).

- China Hydrogen Energy Alliance. China’s Hydrogen Energy and Fuel Cell Industry White Paper 2020; People’s Daily Press: Beijing, China, 2021. (In Chinese) [Google Scholar]

- Kwok, J. Towards a hydrogen economy-a sustainable pathway for global energy transition. Trans. Hong Kong Inst. Eng. 2021, 28, 102–107. [Google Scholar] [CrossRef]

- IRENA. Green Hydrogen: A Guide to Policy Making; International Renewable Energy Agency: Abu Dhabi, United Arab Emirates, 2020; Available online: https://www.irena.org/-/media/Files/IRENA/Agency/Publication/2020/Nov/IRENA_Green_hydrogen_policy_2020.pdf (accessed on 10 February 2023).

- Liu, P.; Han, X. Comparative analysis on similarities and differences of hydrogen energy development in the World’s top 4 largest economies: A novel framework. Int. J. Hydrogen Energy 2022, 47, 9485–9503. [Google Scholar] [CrossRef]

- The White House. National Climate Task Force. Available online: https://www.whitehouse.gov/climate/ (accessed on 15 February 2023).

- Fuel Cells and Hydrogen 2 Joint Undertaking. Hydrogen Roadmap Europe: A Sustainable Pathway for the European Energy Transition. Available online: https://www.clean-hydrogen.europa.eu/media/publications/hydrogen-roadmap-europe-sustainable-pathway-european-energy-transition_en (accessed on 15 February 2023).

- European Commission. European Green Deal Climate Action. Available online: https://climate.ec.europa.eu/eu-action/european-green-deal_en (accessed on 15 February 2023).

- Wijk, A.; Chatzimarkakis, J. Green Hydrogen for a European Green Deal A 2 × 40 GW Initiative. Available online: https://itm-power-assets.s3.eu-west-2.amazonaws.com/Hydrogen_Europe_2x40_GW_Green_H2_Initative_Paper_486310ddcb.pdf (accessed on 17 February 2023).

- Pietzcker, R.C.; Osorio, S.; Rodrigues, R. Tightening EU ETS targets in line with the European Green Deal: Impacts on the ecarbonization of the EU power sector. Appl. Energy 2021, 293, 116914. [Google Scholar] [CrossRef]

- METI. Green Growth Strategy through Achieving Carbon Neutrality in 2050. Available online: https://www.meti.go.jp/english/press/2020/pdf/1225_001b.pdf (accessed on 17 February 2023).

- Wang, Y.; Guo, C.H.; Chen, X.J.; Jia, L.Q.; Guo, X.N.; Chen, R.S.; Wang, H.D. Carbon peak and carbon neutrality in China: Goals, implementation path and prospects. China Geol. 2021, 4, 720–746. [Google Scholar] [CrossRef]

- Wu, L.; Sun, L.; Qi, P.; Ren, X.; Sun, X. Energy endowment, industrial structure upgrading, and CO2 emissions in China: Revisiting resource curse in the context of carbon emissions. Resour. Policy 2021, 74, 102329. [Google Scholar] [CrossRef]

- The State Council. The Outline of the 14th Five-Year Plan (2021–2025) for National Economic and Social Development and Vision 2035. Available online: http://www.gov.cn/xinwen/2021-03/13/content_5592681.htm (accessed on 15 February 2023).

- NEA. The People’s Republic of China’s Energy Law (Draft for Comments). Available online: http://www.nea.gov.cn/2020-04/10/c_138963212.htm (accessed on 15 February 2023).

- National Development and Reform Commission National Energy Administration. The Medium and Long-Term Plan for the Development of the Hydrogen Energy Industry (2021–2035). Available online: https://www.ndrc.gov.cn/xxgk/zcfb/ghwb/202203/P020220323314396580505.pdf (accessed on 15 February 2023).

- Yu, H.M.; Shao, Z.G.; Hou, M.; Yi, B.L.; Duan, F.W.; Yang, Y. Hydrogen Production by Water Electrolysis: Progress and Suggestions. Strateg. Study CAE 2021, 23, 146–152. [Google Scholar] [CrossRef]

- Liu, Y.Y. The Installed Capacity of Renewable Energy in China has Exceeded 1.2 Billion Kilowatts. Available online: http://m.stdaily.com/index/kejixinwen/202302/bc1cd850d5f841d5b4faadb2c9f19b30.shtml (accessed on 15 February 2023).

- Seetao. Sinopec Photovoltaic Green Hydrogen Production Project Settled in Kuqa, Xinjiang. Available online: https://www.seetao.com/details/126120.html (accessed on 10 February 2023).

- Yu, J.; Shao, C.; Xue, C.; Hu, H. China’s aircraft-related CO2 emissions: Decomposition analysis, decoupling status, and future trends. Energy Policy 2020, 138, 111215. [Google Scholar] [CrossRef]

- Zhao, F.; Liu, X.; Zhang, H.; Liu, Z. Automobile industry under China’s carbon peaking and carbon neutrality goals: Challenges, opportunities, and coping strategies. J. Adv. Transp. 2022, 2022, 5834707. [Google Scholar] [CrossRef]

- Huang, R.; Zhang, S.; Wang, P. Key areas and pathways for carbon emissions reduction in Beijing for the Dual Carbon targets. Energy Policy 2022, 164, 112873. [Google Scholar] [CrossRef]

- Apostolou, D.; Xydis, G. A literature review on hydrogen refuelling tations and infrastructure. Current status and future prospects. Renew. Sustain. Energy Rev. 2019, 113, 109292. [Google Scholar] [CrossRef]

- Tanc, B.; Arat, H.T.; Baltacioglu, E.; Aydin, K. Overview of the next quarter century vision of hydrogen fuel cell electric vehicles. Int. J. Hydrogen Energy 2019, 44, 10120–10128. [Google Scholar] [CrossRef]

- Yang, L. Over 270 Hydrogen Refueling Stations Built across China, the Most in the World. Available online: https://peoplesdaily.pdnews.cn/china/over-270-hydrogen-refueling-stations-built-across-china-the-most-in-the-world-273492.html (accessed on 15 February 2023).

- Zhang, M.; Yang, X.N. The Regulatory Perspectives to China’s Emerging Hydrogen Economy: Characteristics, Challenges, and Solutions. Sustainability 2022, 14, 9700. [Google Scholar] [CrossRef]

- Fan, F.F. China Looks to Clean Hydrogen Fuel to Power Future. China Daily. Available online: http://www.Chinadaily.com.cn/a/202205/18/WS62845ee8a310fd2b29e5d76a.html (accessed on 20 February 2023).

- Shanghai Government. The Medium and Long-Term Plan for the Development of the Hydrogen Energy Industry in Shanghai. Available online: https://www.shanghai.gov.cn/cmsres/89/890a5d14a42a497993546b558f525cb0/331d8ca143e43fd6548afed86b594190.pdf (accessed on 2 February 2023).

- Wang, F.; Gao, C.; Zhang, W.; Huang, D. Industrial Structure Optimization and Low-Carbon Transformation of Chinese Industry Based on the Forcing Mechanism of CO2 Emission Peak Target. Sustainability 2021, 13, 4417. [Google Scholar] [CrossRef]

- Teng, Y.; Wang, Y.; Huang, Z. China Hydrogen Energy Industry Development. Available online: https://view.inews.qq.com/k/20220415A001JE00?web_channel=wap&oenApp=false (accessed on 15 February 2023).

- Dincer, I. Green methods for hydrogen production. Int. J. Hydrogen Energy 2012, 37, 1954–1971. [Google Scholar] [CrossRef]

- Marshall, A.T.; Haverkamp, R.G. Production of hydrogen by the electrochemical reforming of glycerol–water solutions in a PEM electrolysis cell. Int. J. Hydrogen Energy 2008, 33, 4649–4654. [Google Scholar] [CrossRef]

- Soochow Securities. The Economic Estimation and Cost Reduction Outlook of China’s Hydrogen Energy Industry Chain. Available online: https://www.vzkoo.com/document/202205099221911505565ffd4b5a33e6.html (accessed on 20 February 2023).

- Sadik-Zada, E.R.; Gatto, A. Energy Security Pathways in South East Europe: Diversification of the Natural Gas Supplies, Energy Transition, and Energy Futures. In From Economic to Energy Transition. Energy, Climate and the Environment; Mišík, M., Oravcová, V., Eds.; Palgrave Macmillan: Cham, Switzerland, 2020; pp. 491–514. [Google Scholar]

- Ji, M.D.; Wang, J.L. Review and comparison of various hydrogen production methods based on costs and life cycle impact assessment indicators. Int. J. Hydrogen Energy 2021, 46, 38612–38635. [Google Scholar] [CrossRef]

- Pandey, R.P.; Shahi, V.K. Sulphonated imidized graphene oxide (SIGO) based polymer electrolyte membrane for improved water retention, stability and proton conductivity. J. Power Sources 2015, 299, 104–113. [Google Scholar] [CrossRef]

- Pedicini, R.; Carbone, A.; Saccà, A.; Gatto, I.; Di Marco, G.; Passalacqua, E. Sulphonated polysulphone membranes for medium temperature in polymer electrolyte fuel cells (PEFC). Polym. Test. 2008, 27, 248–259. [Google Scholar] [CrossRef]

- Zhu, Y.; Li, H.; Tang, J.K.; Wang, L.; Yang, L.B.; Ai, F.; Wang, C.N.; Yuan, W.Z.; Zhang, Y.M. Systematic stability investigation of perfluorosulfonic acid membranes with varying ion exchange capacities for fuel cell applications. RSC Adv. 2014, 4, 6369–6374. [Google Scholar] [CrossRef]

- Jiang, B.; Pu, H.T.; Pan, H.Y.; Chang, Z.H.; Jin, M.; Wan, D.C. Proton conducting membranes based on semi-interpenetrating polymer network of fluorine-containing polyimide and perfluorosulfonic acid polymer via click chemistry. Electrochem. ACTA 2014, 132, 457–464. [Google Scholar] [CrossRef]

- Othman, R.; Dicks, A.L.; Zhu, Z. Non precious metal catalysts for the PEM fuel cell cathode. Int. J. Hydrogen Energy 2012, 37, 357–372. [Google Scholar] [CrossRef]

- Sheng, W.; Myint, M.; Chen, J.G.; Yan, Y. Correlating the hydrogen evolution reaction activity in alkaline electrolytes with the hydrogen binding energy on monometallic surfaces. Energy Environ. Sci. 2013, 6, 1509–1512. [Google Scholar] [CrossRef]

- Li, A.; Kong, S.; Guo, C.X.; Ooka, H.; Adachi, K.; Hashizume, D.; Jiang, Q.K.; Han, H.X.; Xiao, J.P.; Nakamura, R. Enhancing the stability of cobalt spinel oxide towards sustainable oxygen evolution in acid. Nat. Catal. 2022, 5, 109–118. [Google Scholar] [CrossRef]

- Sun, T.T.; Xu, L.B.; Wang, D.S.; Li, Y.D. Metal organic frameworks derived single atom catalysts for electrocatalytic energy conversion. Nano Res. 2019, 12, 2067–2080. [Google Scholar] [CrossRef]

- Rocky Mountain Institute (RMI); China Hydrogen Alliance. China’s Green Hydrogen New Era 2030 China’s Renewable Hydrogen 100 GW Roadmap. 2022. Available online: https://rmi.org.cn/?s=%E3%80%8A%E5%BC%80%E5%90%AF%E7%BB%BFE8%89%B2%E6%B0%A2%E8%83%BD%E6%96%B0%E6%97%B6%E4%BB%A3%E4%B9%8B%E5%8C%99%3A%E4%B8%AD%E5%9B%BD2030%E5%B9%B4%E2%80%9C%E5%8F%AF%E5%86%8D%E7%94%9F%E6%B0%A2100%E2%80%9D%E5%8F%91%E5%B1%95%E8%B7%AF%E7%BA%BF%E5%9B%BE%E3%80%8B (accessed on 20 February 2023).

- Wang, H.-R.; Feng, T.-T.; Li, Y.; Zhang, H.-M.; Kong, J.-J. What Is the Policy Effect of Coupling the Green Hydrogen Market, National Carbon Trading Market and Electricity Market? Sustainability 2022, 14, 13948. [Google Scholar] [CrossRef]

- Atilhan, S.; Park, S.; El-Halwagi, M.M.; Atilhan, M.; Moore, M.; Nielsen, R.B. Green hydrogen as an alternative fuel for the shipping industry. Curr. Opin. Chem. Eng. 2021, 31, 100668. [Google Scholar] [CrossRef]

- Yin, Y. Present Situation and Prospect of Hydrogen Energy. Ind. Chem Ind. Eng. 2021, 38, 78–83. [Google Scholar] [CrossRef]

- Saygili, Y.; Kincal, S.; Eroglu, I. Development and modeling for process control purposes in PEMs. Int. J. Hydrogen Energy 2015, 40, 7886–7894. [Google Scholar] [CrossRef]

- Cerniauskas, S.; Junco, A.J.C.; Grube, T.; Robinius, M.; Stolten, D. Options of natural gas pipeline reassignment for hydrogen: Cost assessment for a germany case study. Int. J. Hydrogen Energy 2020, 45, 12095–12107. [Google Scholar] [CrossRef] [Green Version]

- Zhu, J.; Pan, J.; Zhang, Y.; Li, Y.; Li, H.; Feng, H.; Yang, R. Leakage and diffusion behavior of a buried pipeline of hydrogen-blended natural gas. Int. J. Hydrogen Energy 2023, 48, 11592–11610. [Google Scholar] [CrossRef]

- Griffiths, S.; Sovacool, B.K.; Kim, J.; Bazilian, M.; Uratani, J.M. Industrial decarbonization via hydrogen: A critical and systematic review of developments, socio-technical systems and policy options. Energy Res. Soc. Sci. 2021, 80, 102208. [Google Scholar] [CrossRef]

- Gao, X.W.; An, R.C. Research on the coordinated development capacity of China’s hydrogen energy industry chain. J. Clean. Prod. 2022, 377, 134177. [Google Scholar] [CrossRef]

- Okolie, J.A.; Patra, B.R.; Mukherjee, A.; Nanda, S.; Dalai, A.K.; Kozinski, J.A. Futuristic applications of hydrogen in energy, biorefining, aerospace, pharmaceuticals and metallurgy. Int. J. Hydrogen Energy 2021, 46, 8885–8905. [Google Scholar] [CrossRef]

- Zhang, H.; Yuan, T.J.; Tan, J. Business model and planning approach for hydrogen energy systems at three application scenarios. J. Renew. Sustain. Energy 2021, 13, 044101. [Google Scholar] [CrossRef]

- Haslam, G.E.; Jupesta, J.; Parayil, G. Assessing fuel cell vehicle innovation and the role of policy in Japan, Korea, and China. Int. J. Hydrogen Energy 2012, 37, 14612–14623. [Google Scholar] [CrossRef]

- Kovač, A.; Paranos, M.; Marciuš, D. Hydrogen in energy transition: A review. Int. J. Hydrogen Energy 2021, 46, 10016–10035. [Google Scholar] [CrossRef]

- Zhao, X.; Ma, X.; Chen, B.; Shang, Y.; Song, M. Challenges toward carbon neutrality in China: Strategies and countermeasures. Res. Conserv. Recycl. 2022, 176, 105959. [Google Scholar] [CrossRef]

- Ho, T.; Karri, V.; Madsen, O. Prediction of hydrogen safety parameters using intelligent techniques. Int. J. Hydrogen Energy 2009, 33, 431–442. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Hydrogen Production | Raw Material Origins | Technology Line | Advantages | Disadvantages |

|---|---|---|---|---|

| Grey hydrogen | Fossil energy sources | Gas separation and reforming technologies | Technology Maturity | Limited raw material reserves high carbon emissions |

| Blue hydrogen | Chloride, alkali and other industrial by-product gases | Industrial purification combined with carbon capture and storage technology | Lower cost | Insufficient hydrogen purity and narrow application range |

| Green hydrogen | Water, renewable energy power | Electrolytic water technologies | No carbon emissions | Higher costs and technical difficulty |

| Electrolytic diaphragm | 30% KOH asbestos film | Proton Exchange Membrane | Anion exchange membrane | Solid state oxide |

| Hydrogen production purity | ≥99.8% | ≥99.99% | ≥99.99% | —— |

| Difficulty of operation | Need to control differential pressure, need to dealkalize | Fast start/stop, water vapor only | Fast start/stop, water vapor only | No change in start/stop, water vapor only |

| Maintainability | Strong alkali corrosive | Non-corrosive media | Non-corrosive media | —— |

| Environmental requirements | Asbestos air pollution | Non-polluting | Non-polluting | —— |

| Technology Maturity | Industrial Scale-up | Rapid Commercialization | Initial demonstration run | Laboratory phase |

| Hydrogen production efficiency (kWh/kg of hydrogen) | 50–70% | 50–83% | 45–55% | |

| System Cost (USD/kW) | 500–1000 | 700–1400 | 2000 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Yang, L.; Wang, S.; Zhang, Z.; Lin, K.; Zheng, M. Current Development Status, Policy Support and Promotion Path of China’s Green Hydrogen Industries under the Target of Carbon Emission Peaking and Carbon Neutrality. Sustainability 2023, 15, 10118. https://doi.org/10.3390/su151310118

Yang L, Wang S, Zhang Z, Lin K, Zheng M. Current Development Status, Policy Support and Promotion Path of China’s Green Hydrogen Industries under the Target of Carbon Emission Peaking and Carbon Neutrality. Sustainability. 2023; 15(13):10118. https://doi.org/10.3390/su151310118

Chicago/Turabian StyleYang, Lei, Shuning Wang, Zhihu Zhang, Kai Lin, and Minggang Zheng. 2023. "Current Development Status, Policy Support and Promotion Path of China’s Green Hydrogen Industries under the Target of Carbon Emission Peaking and Carbon Neutrality" Sustainability 15, no. 13: 10118. https://doi.org/10.3390/su151310118