How Does China Build Its Fintech Strategy? A Perspective of Policy Evolution

Abstract

:1. Introduction

2. Methodology

2.1. Analytical Framework

2.2. Data Acquisition and Preprocessing

2.2.1. Policy Sample Selection

2.2.2. Policy Sample Code

2.3. Model Construction and Data Analysis

2.3.1. Quantitative Analysis of Policy Tools

2.3.2. Quantitative Analysis of Policy Effectiveness

2.3.3. Social Network Analysis

2.4. Depth Analysis, Results Analysis, and Discussion

3. Quantitative Analysis of Policy Texts

3.1. Policy Tools Analysis

3.1.1. Overuse of Environmental Policy Tools and Imbalance in the Use of Secondary Policy Tools

3.1.2. Supply-Oriented Policy Tools Are Moderately Applied, While Secondary Policy Tools Are Unevenly Distributed

3.1.3. Demand-Type Policy Tools Are Not Used Enough, and the Structure of Secondary Policy Tools Is More Balanced

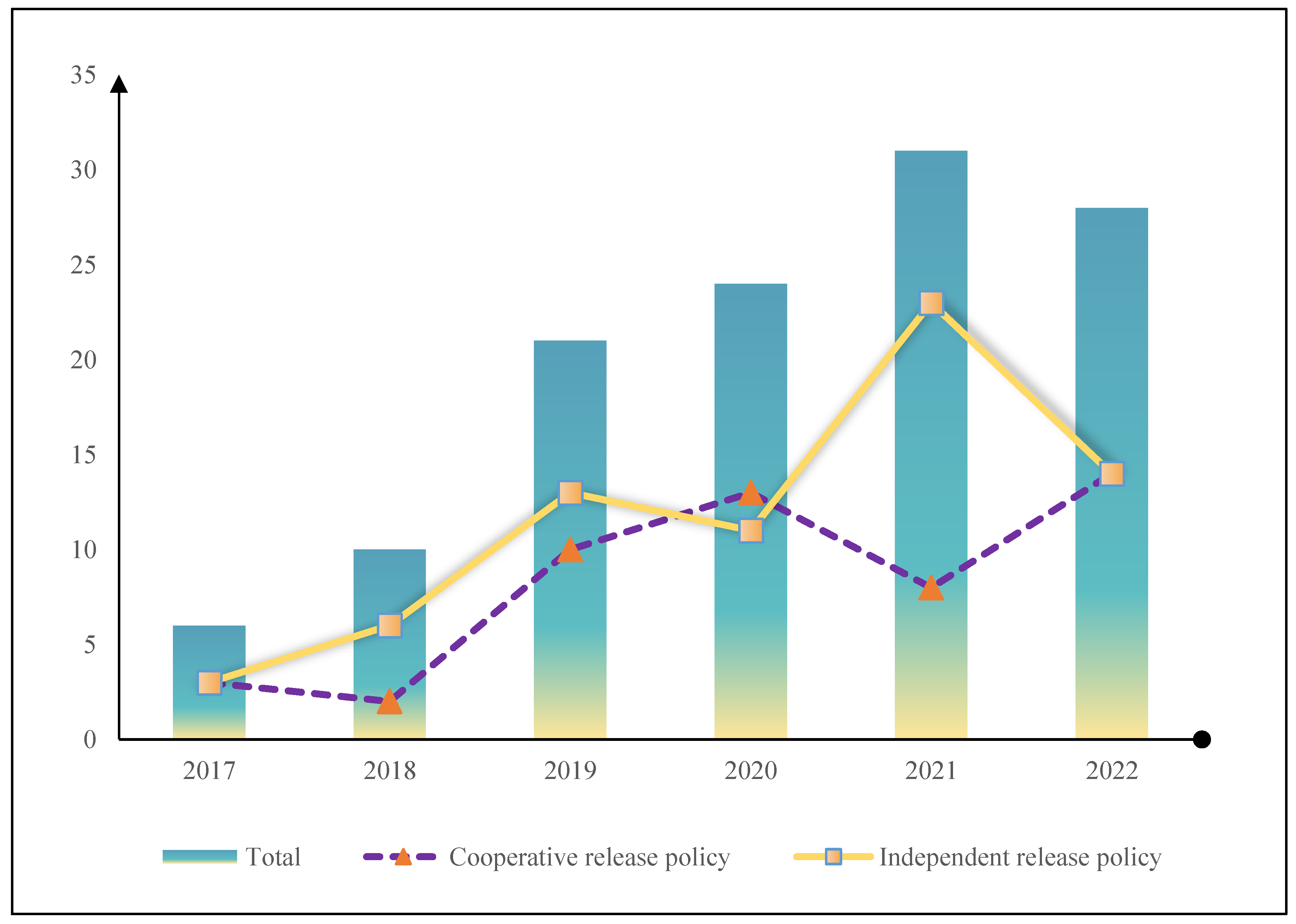

3.2. Policy Organizational Structure

3.2.1. Policy Subject

3.2.2. Type of Publication

3.2.3. Cooperation Network

3.3. Analysis of Policy Effectiveness

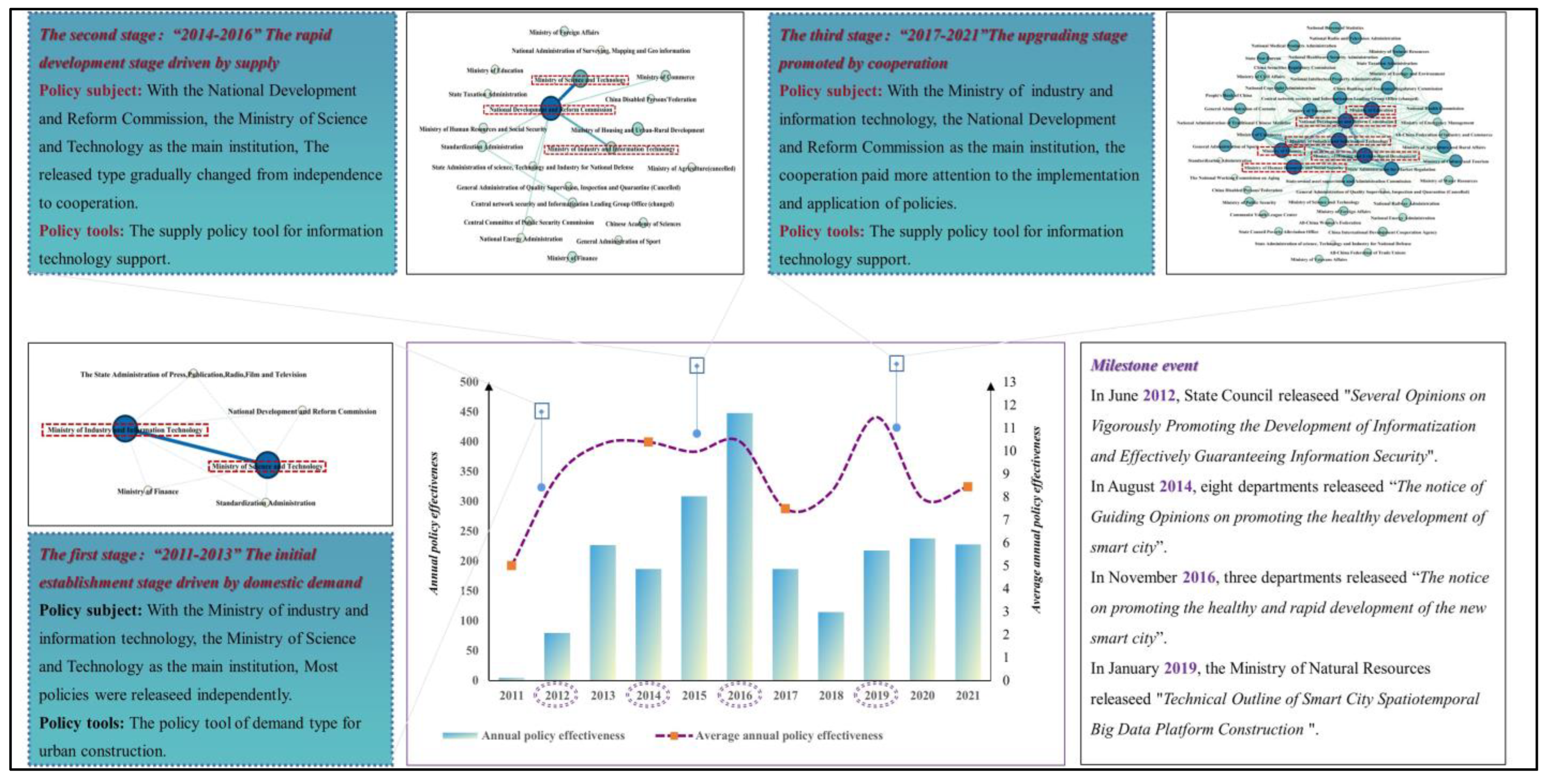

4. Analysis of Policy Evolution Stage

4.1. Initial Establishment Stage Driven by Domestic Demand

4.2. Rapid Development Stage Driven by Supply

4.3. Upgrading Stage Driven by Cooperation

5. Conclusions and Discussion

5.1. Lessons Learned from Previous Policies

5.2. Suggestions for Future Policies

5.3. Limitations of This Work

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Puschmann, T. Fintech. Bus. Inf. Syst. Eng. 2017, 59, 69–76. [Google Scholar] [CrossRef]

- Kong, S.T.; Loubere, N. Digitally Down to the Countryside: Fintech and Rural Development in China. J. Dev. Stud. 2021, 57, 1739–1754. [Google Scholar] [CrossRef]

- Muganyi, T.; Yan, L.N.; Yin, Y.K.; Sun, H.P.; Gong, X.B.; Taghizadeh-Hesary, F. Fintech, regtech, and financial development: Evidence from China. Financ. Innov. 2022, 8, 29. [Google Scholar] [CrossRef]

- Wu, G.; Luo, J.; Tao, K. Research on the influence of FinTech development on credit supply of commercial banks: The case of China. Appl. Econ. 2023. [Google Scholar] [CrossRef]

- Song, N.; Appiah-Otoo, I. The Impact of Fintech on Economic Growth: Evidence from China. Sustainability 2022, 14, 6211. [Google Scholar] [CrossRef]

- Chorzempa, M.; Huang, Y. Chinese Fintech Innovation and Regulation. Asian Econ. Policy Rev. 2022, 17, 19. [Google Scholar] [CrossRef]

- Chen, X.H.; Zhang, H.W.; Teng, L. Technology risk management in fintech: Underlying mechanisms and challenges. J. Oper. Risk 2022, 17, 105–125. [Google Scholar] [CrossRef]

- Murinde, V.; Rizopoulos, E.; Zachariadis, M. The impact of the FinTech revolution on the future of banking: Opportunities and risks. Int. Rev. Financ. Anal. 2022, 81, 102103. [Google Scholar] [CrossRef]

- Jin, L.; Pan, C.C.; Li, Y.; Liu, X.M. How Can FinTech Reduce Corporate Zombification Risk? Emerg. Mark. Financ. Trade 2022, 58, 4350–4360. [Google Scholar] [CrossRef]

- Cheng, M.Y.; Qu, Y. Does bank FinTech reduce credit risk? Evidence from China. Pac. Basin Financ. J. 2020, 63, 101398. [Google Scholar] [CrossRef]

- Xu, D.G.; Xu, D.W. Concealed Risks of FinTech and Goal-Oriented Responsive Regulation: China’s Background and Global Perspective. Asian J. Law Soc. 2020, 7, 305–324. [Google Scholar] [CrossRef]

- Kong, Y.; Feng, C.; Yang, J. How does China manage its energy market? A perspective of policy evolution. Energy Policy 2020, 147, 111898. [Google Scholar] [CrossRef]

- Liao, Z. The evolution of wind energy policies in China (1995–2014): An analysis based on policy instruments. Renew. Sustain. Energy Rev. 2016, 56, 464–472. [Google Scholar] [CrossRef]

- Chen, X.H.; Chen, W.; Lu, K.B. Does an imbalance in the population gender ratio affect FinTech innovation? Technol. Forecast. Soc. Chang. 2023, 188, 122164. [Google Scholar] [CrossRef]

- Yang, T.; Zhang, X. FinTech adoption and financial inclusion: Evidence from household consumption in China. J. Bank. Financ. 2022, 145, 106668. [Google Scholar] [CrossRef]

- Le, T.D.Q.; Ho, T.H.; Nguyen, D.T.; Ngo, T. Fintech Credit and Bank Efficiency: International Evidence. Int. J. Financ. Stud. 2021, 9, 44. [Google Scholar] [CrossRef]

- Li, J.; Li, N.; Cheng, X. The Impact of Fintech on Corporate Technology Innovation Based on Driving Effects, Mechanism Identification, and Heterogeneity Analysis. Discret. Dyn. Nat. Soc. 2021, 2021, 7825120. [Google Scholar] [CrossRef]

- Luo, S.; Sun, Y.; Yang, F.; Zhou, G. Does fintech innovation promote enterprise transformation? Evidence from China. Technol. Soc. 2022, 68, 101821. [Google Scholar] [CrossRef]

- Zhao, Y.; Goodell, J.W.; Dong, Q.L.; Wang, Y.; Abedin, M.Z. Overcoming spatial stratification of fintech inclusion: Inferences from across Chinese provinces to guide policy makers. Int. Rev. Financ. Anal. 2022, 84, 102411. [Google Scholar] [CrossRef]

- Gao, J.Y. Has COVID-19 hindered small business activities? The role of Fintech. Econ. Anal. Policy 2022, 74, 297–308. [Google Scholar] [CrossRef]

- Wijermars, M.; Makhortykh, M. Sociotechnical imaginaries of algorithmic governance in EU policy on online disinformation and FinTech. New Media Soc. 2022, 24, 942–963. [Google Scholar] [CrossRef]

- Peng, J.; Zhong, W.; Sun, W. Policy Measurement, Policy Coordinated Evolution and Economic Performance: An Empirical Study Based on Innovation Policy. Manag. World 2008, 09, 25–36. (In Chinese) [Google Scholar] [CrossRef]

- Walravens, N. Qualitative indicators for smart city business models: The case of mobile services and applications. Telecommun. Policy 2015, 39, 218–240. [Google Scholar] [CrossRef]

- Wright, Q.; Lerner, D.; Lasswell, H.D.J.T.A.P.S.R. The Policy Sciences; Recent Developments in Scope and Method. Am. Political Sci. Rev. 1952, 46, 234. [Google Scholar] [CrossRef]

- Abbink, K.; Jayne, T.S.; Moller, L.C. The Relevance of a Rules-based Maize Marketing Policy: An Experimental Case Study of Zambia. J. Dev. Stud. 2011, 47, 207–230. [Google Scholar] [CrossRef] [Green Version]

- Zhang, K.M.; Wen, Z.G.J. Review and challenges of policies of environmental protection and sustainable development in China. J. Environ. Manag. 2008, 88, 1249–1261. [Google Scholar] [CrossRef]

- Ye, K.; Guo, Z.; Zhang, W.; Liang, Y. Heterogeneous environmental policy tools for expressway construction projects: A crossregional analysis in China. Environmental Impact Assessment Review 2022, 97. [Google Scholar] [CrossRef]

- Yu, J.; Zhang, L. Evolution of marine ranching policies in China: Review, performance and prospects. Sci. Total Environ. 2020, 737, 139782. [Google Scholar] [CrossRef]

- Tashakkori, A.; Teddlie, C.J. Mixed Methodology: Combining Qualitative and Quantitative Approaches. Contemp. Sociol. 1999, 28, 752–753. [Google Scholar]

- Zhao, X.; Thomas, C.W.; Cai, T. The Evolution of Policy Instruments for Air Pollution Control in China: A Content Analysis of Policy Documents from 1973 to 2016. Environ. Manag. 2020, 66, 953–965. [Google Scholar] [CrossRef]

- Gibbons, C.F.J. A quantitative analysis of the science research council’s policy of “selectivity and concentration”. Res. Policy 1979, 8, 306–338. [Google Scholar]

- Yang, Q.; Huang, J. Content Analysis of Family Policy Instruments to Promote the Sustainable Development of Families in China from 1989–2019. Sustainability 2020, 12, 693. [Google Scholar] [CrossRef] [Green Version]

- Schneider, J.A.; Stevens, N.J.; Tornatzky, L.G.J. Policy research and analysis: An empirical profile, 1975–1980. Policy Ences 1982, 15, 99–114. [Google Scholar] [CrossRef]

- Zhang, L.; Qin, Q.; Wei, Y.-M. China’s distributed energy policies: Evolution, instruments and recommendation. Energy Policy 2019, 125, 55–64. [Google Scholar] [CrossRef]

- Libecap, G.D. Economic variables and law development: A case of western mineral property. Econ. Hist. J. 1978, 38, 338–362. [Google Scholar] [CrossRef]

- Rai, S. Policy Adoption and Policy Intensity: Emergence of Climate Adaptation Planning in U.S. States. Rev. Policy Res. 2020, 37, 444–463. [Google Scholar] [CrossRef]

- Bertoldi, P.; Mosconi, R.J. Do energy efficiency policies save energy? A new approach based on energy policy indicators (in the EU Member States). Energy Policy 2020, 139, 111320. [Google Scholar] [CrossRef]

- Levy, D.; Fergus, C.; Rudov, L.; Mccormick-Ricket, I.; Carton, T.J.P.S. Tobacco Policies in Louisiana: Recommendations for Future Tobacco Control Investment from SimSmoke, a Policy Simulation Model. Prev. Sci. 2016, 17, 199–207. [Google Scholar] [CrossRef]

- Higashiyama, H.; Kondo, M.; Kinoshita, Y.; Miyazaki, K.J. Interorganizational Relationships Within State Tobacco Control Networks: A Social Network Analysis. Prev. Chronic Dis. 2004, 1, A08. [Google Scholar]

- Drew, R.; Aggleton, P.; Chalmers, H.; Wood, K.J. Using social network analysis to evaluate a complex policy network. Evaluation 2011, 17, 383–394. [Google Scholar] [CrossRef]

- Mcgee, Z.A.; Jones, B.D.J. Reconceptualizing the Policy Subsystem: Integration with Complexity Theory and Social Network Analysis. Policy Stud. J. 2019, 47, S138–S158. [Google Scholar] [CrossRef] [Green Version]

- Kalantari, E.; Montazer, G.; Ghazinoory, S. Mapping of a science and technology policy network based on social network analysis. J. Entrep. Manag. Innov. 2021, 17, 115–147. [Google Scholar] [CrossRef]

- Zhao, Y.; Ponzini, D.; Zhang, R. The policy networks of heritage-led development in Chinese historic cities: The case of Xi’an’s Big Wild Goose Pagoda area. Habitat Int. 2020, 96, 102106. [Google Scholar] [CrossRef]

- Taeihagh, A.; Banares-Alcantara, R.; Millican, C. Development of a novel framework for the design of transport policies to achieve environmental targets. Comput. Chem. Eng. 2009, 33, 1531–1545. [Google Scholar] [CrossRef]

- Li, L.; Zheng, Y.; Zheng, S.; Ke, H.J. The new smart city programme: Evaluating the effect of the internet of energy on air quality in China. Sci. Total Environ. 2020, 714, 136380. [Google Scholar] [CrossRef]

- Li, L.; Taeihagh, A.J. An in-depth analysis of the evolution of the policy mix for the sustainable energy transition in China from 1981 to 2020. Appl. Energy 2020, 263, 114611. [Google Scholar] [CrossRef]

- Roy, R.; Walter, Z. An assessment of government innovation policies. Rev. Policy Res. 1984, 3, 9. [Google Scholar]

- Chen, R.; Xu, P.; Yao, H.; Ding, Y. How will China achieve net-zero? A policy text analysis of Chinese decarbonization policies. Energy Res. Soc. Sci. 2023, 99. [Google Scholar] [CrossRef]

- Chong, M.; Habib, A.; Evangelopoulos, N.; Park, H.W.J. Dynamic capabilities of a smart city: An innovative approach to discovering urban problems and solutions. Gov. Inf. Q. 2018, 35, 682–692. [Google Scholar] [CrossRef]

- Chatfield, A.T.; Reddick, C.G.J. Smart City Implementation Through Shared Vision of Social Innovation for Environmental Sustainability. Soc. Sci. Comput. Rev. 2016, 34, 757–773. [Google Scholar] [CrossRef]

- Alfaro Navarro, J.L.; Lopez Ruiz, V.R.; Nevado Pena, D.J.C. The effect of ICT use and capability on knowledge-based cities. Cities 2017, 60, 272–280. [Google Scholar] [CrossRef]

- Angelidou, M. Smart cities: A conjuncture of four forces. Cities 2015, 47, 95–106. [Google Scholar] [CrossRef]

- Lin-Feng, Z.; Ni, D. Research on the Positioning of Government Functions in China under the Background of Smart City Construction. Int. J. Technol. Manag. 2013, 10, 116–118. [Google Scholar]

- Yeh, H. The effects of successful ICT-based smart city services: From citizens’ perspectives. Gov. Inf. Q. 2017, 34, 556–565. [Google Scholar] [CrossRef]

- Eugene, B. A Practical Guide for Policy Analysis: The Eightfold Path to More Effective Problem Solving; CQ Press: Washington, DC, USA, 2009. [Google Scholar]

- Tenenhaus, M.; Chatelin, Y.M.; Vinzi, V.E. State-of-Art on PLS Path Modeling through the Available Software; Les Cahiers De Recherché; HEC Paris: Jouy-en-Josas, France, 2002. [Google Scholar]

- Chen, D.; Deakin, S.; Johnston, A.; Wang, B.Y. Too Much Technology and Too Little Regulation? The Spectacular Demise of P2P Lending in China. Account. Econ. Law-A Conviv. 2021, 1–48. [Google Scholar] [CrossRef]

- Guo, L. Fintech Regulation in China: Principles, Policies and Practices. Asian J. Law Soc. 2022. [Google Scholar] [CrossRef]

- Zhao, B.; Xu, R.Y. Can technological finance cooperation pilot policy improve energy efficiency? Evidence from a quasi-experiment in China. Environ. Sci. Pollut. Res. 2023, 30, 53445–53460. [Google Scholar] [CrossRef]

- Jiang, S.; Qiu, S.; Zhou, H. Will digital financial development affect the effectiveness of monetary policy in emerging market countries? Econ. Res. Ekon. Istraz. 2022, 35, 3437–3472. [Google Scholar] [CrossRef]

- Han, M.; Xu, D.G. The sandbox approach to fintech regulation: A case study of china. Rev. Chil. Derecho 2022, 49, 193–232. [Google Scholar] [CrossRef]

- Wang, J. “The Party Must Strengthen Its Leadership in Finance!”: Digital Technologies and Financial Governance in China’s Fintech Development. China Q. 2021, 247, 773–792. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Date of Issue | Policy Name | Content Analysis Unit | APE | Types of Policy Instruments | Name of Policy Instrument | Code |

|---|---|---|---|---|---|---|

| 2017.05 | Notice of the People’s Bank of China, the Banking Regulatory Commission and the Securities Regulatory Commission on the Release of the Development Plan for the Construction of the Standardization System in the Financial Sector (2016~2020) | …Strengthen the regulation of financial technology and risk prevention and control standards development, the development of … financial technology and other areas … standards to improve the accuracy of risk prevention and control. | 5 | Environmental type | Regulations and standards | 2017-1-1 |

| … | … | … | … | … | … | |

| 2019.12 | China Banking and Insurance Regulatory Commission’s Guidance on Promoting High-Quality Development of the Banking and Insurance Industry | …Explore the application of fintech in customer credit evaluation, credit access, etc… …Study and develop a regulatory system for fintech companies to strengthen the supervision of emerging financial businesses and industries… | 14 | Environmental type Supply type Supply type | Strategic measures Infrastructure development Basic research support | 2019-24-1 2019-24-2 2019-24-3 |

| … | … | … | … | … | … | … |

| 2021.03 | Opinions of the State Council on the division of key tasks for the implementation of the Report on the Work of the Government | …Strengthen the regulation of financial holding companies and fintech to ensure that financial innovation is carried out under prudential supervision. | 16 | Environmental type | Regulations and standards | 2021-5-1 |

| Category | Policy Tools | Definition |

|---|---|---|

| Supply type | Basic research support | The government explores and researches the standard construction and application innovations of financial technology by setting up platforms, awards, or projects |

| Infrastructure construction | Require or encourage relevant departments, enterprises, and financial institutions to strengthen the scientific and technological support and carrier construction for the development of financial technology. | |

| Public service | The government must provide various supporting services to ensure the smooth implementation of fintech construction activities. | |

| Talent training | Provide vocational education and skills training for relevant technical personnel and management personnel. | |

| Environmental type | Goal programming | To promote the construction of fintech, make a general description and outline of the goals and prospects. |

| Regulations and standards | The formulation of a series of laws and regulations, standards, and other norms of market behaviour helps create a fair and orderly environment for the construction of fintech. | |

| Strategic measures | Encourage and provide detailed guidance to financial institutions to use financial technology to enhance the way and efficiency of financial services and promote exchanges and cooperation with multiple entities, such as rural finance, green finance, and SMEs. | |

| Tax benefits | Tax relief for companies or financial institutions engaged in key areas of financial technology or conducting innovative research and development. | |

| Demand type | Government procurement | Government directly or in coordination with other purchasers to promote innovation and adoption of fintech in the form of consumption. |

| Encourage publicity | The government has encouraged or promoted the expression in the document to guide enterprises and the public, etc., to actively learn and use financial technology. | |

| Pilot demonstration | Establishing pilot financial technology innovation to promote the landing and application of cutting-edge innovations. | |

| External contracting | Government agencies entrust R&D innovation and curriculum building to companies or research institutions to promote innovation in financial technology |

| No. | Name of Institution | Pageranks | Modularity_Class |

|---|---|---|---|

| 1 | People’s Bank of China | 0.056708 | 0 |

| 2 | China Banking and Insurance Regulatory Commission | 0.053693 | 0 |

| 3 | Ministry of Industry and Information Technology | 0.049179 | 0 |

| 4 | State Administration of Market Supervision and Administration | 0.049179 | 0 |

| 5 | Ministry of Agriculture and Rural Affairs | 0.042931 | 1 |

| 6 | Ministry of Commerce | 0.036744 | 1 |

| 7 | China Securities Regulatory Commission | 0.036232 | 0 |

| 8 | National Development and Reform Commission | 0.035838 | 0 |

| 9 | Ministry of Finance | 0.035679 | 0 |

| 10 | Ministry of Ecology and Environment | 0.031315 | 1 |

| Index | Score | Scoring Criteria |

|---|---|---|

| Policy strength P | 5 | Laws promulgated by the National People Congress and its Standing Committee |

| 4 | Joint document of the CPC Central Committee and the State Council; administrative regulations of the State Council | |

| 3 | Other documents of the State Council; rules and regulations of the ministries and commissions of the State Council | |

| 2 | Other opinions, methods, plans, and regulations of the ministries and commissions under the State Council | |

| 1 | Outside of the ministries and commissions of the State Council | |

| Policy objectives G | 5 | All policy objectives involve the construction of fintech |

| 3 | Part of the policy objectives involve the construction of fintech | |

| 1 | The goal of fintech construction has not been put forward | |

| Policy measures M | 5 | For one aspect of fintech construction, it gives the implementation content, lists the specific measures, and explains it in detail |

| 4 | For one aspect of fintech construction, the implementation content is given in detail, and the specific measures are listed | |

| 3 | For the aspects of fintech construction, this study gives the implementation content and lists specific measures | |

| 2 | Lists some basic measures and gives a brief implementation of the content | |

| 1 | Only from the macro point of view, no specific operation plan exists |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Yin, Y.; Ma, H.; Wu, Z.; Yue, A. How Does China Build Its Fintech Strategy? A Perspective of Policy Evolution. Sustainability 2023, 15, 10100. https://doi.org/10.3390/su151310100

Yin Y, Ma H, Wu Z, Yue A. How Does China Build Its Fintech Strategy? A Perspective of Policy Evolution. Sustainability. 2023; 15(13):10100. https://doi.org/10.3390/su151310100

Chicago/Turabian StyleYin, Yingkai, Hongxin Ma, Zhenni Wu, and Aobo Yue. 2023. "How Does China Build Its Fintech Strategy? A Perspective of Policy Evolution" Sustainability 15, no. 13: 10100. https://doi.org/10.3390/su151310100