1. Introduction

In light of the latest reports on climate change impacts [

1], major economies such as the European Union and Germany have reaffirmed their commitment to attaining carbon neutrality by the mid-century. This implies transforming the energy sector, responsible for some 75% of EU greenhouse gas emissions [

2]. The European Commission estimates that EUR 260 billion will have to be invested annually in climate protection in Europe, amounting to EUR 2.6 trillion by 2030 [

2]. Turning to Germany, up to an expected EUR 3000 billion needs to be raised by 2050 to support the ongoing decarbonization of the energy system [

3]. As these large investments cannot be provided by public budgets alone, the mobilization of private finance is necessary [

4,

5,

6], but so far remains insufficient [

5,

7,

8,

9]. This is where financial institutions come into focus as finance intermediaries [

9,

10], ideally by providing a broad range of products tailored to diverse investors [

4,

11,

12].

The relationship between environmental regulation and economic performance on micro- and macroeconomic performance has been analyzed regarding triggering innovation, influencing firm value or effects of government regulation [

13,

14,

15,

16]. As the OECD notes, the definition of green finance differs significantly between jurisdictions [

17]. For the aim of this study, we will stick to the definition proposed by the EU taxonomy (see

Section 2.2). Green finance has been analyzed as regards the role of central and state co-owned banks [

7,

18,

19], the financing of large infrastructure projects [

20,

21] and regarding the different private financial institutions (see [

12,

22]). Many authors agree that private banks play a central role by either guiding investments or directly financing projects concerning the climate and energy transition [

23,

24].

In contrast to this potential role as intermediaries for the energy transition, [

25,

26,

27] affirm that the green finance of banks is still under-researched in terms of analyzing precise cases and their inner workings as regards regulatory framework, market offers and market developments. This is especially true for the segment of retail customers, where banks would have the task of bundling small deposits and channeling them into energy transition projects [

25].

The present study addresses this gap by providing case study evidence and investigating the role of banks in offering sustainability finance in Germany, which to our knowledge has not been assessed before.

Arguably, the country presents an interesting case for furthering insights into the role of banks as transition agents for several reasons:

- (1)

The ongoing energy transition in the country has seen the emergence of many small-scale projects such as local energy cooperatives (see, e.g., [

28]). These projects are based on renewable energy or energy efficiency solutions that necessitate upfront finance [

29,

30], but benefit from strong government support such as backup from public banks [

7,

31] or fixed feed-in tariffs put in place by the government [

32]. Both support measures significantly reduce the risk of investment [

8,

33,

34]. As such, they present a ‘low risk environment’ [

35] that should attract banks and their retail customers as lenders.

- (2)

Banks’ retail customers show an increasing interest in green finance. This had already been noted in 2014 by [

36], but has clearly increased since [

37].

- (3)

As [

4] underscores, a diverse financial system increases resilience and allows for the diversified funding of transition products. The German banking system can serve as an example for such a diversified market.

In sum, all pre-conditions to channel small-scale deposits from retail customers into energy transition projects seem to be present in Germany. Any barriers or solutions occurring in this market can to a certain extent provide insights for other markets as well.

These reflections raise the following three guiding questions for our research:

- Q1:

Which banks offer and promote green finance products for retail customers and which forms do these offers take? Treating public information on webpages and sustainability reports as proxy for bank offers, we screen publicly available information from 329 banks, which are representative of the overall German banking system.

- Q2:

Which factors can explain both the amount and structure of green finance offers for retail customers? We approach this question using in-depth interviews with 12 sector experts from three stakeholder groups: (1) financial intermediaries, (2) regulatory authorities and (3) non-governmental organizations. We assess the perceived status quo regarding the intermediary role of banks, available projects and retail customers’ demands.

- Q3:

Following up on our expert interviews, we investigate which (regulatory) measures could be taken to increase offers and overcome a potential mismatch between supply and demand.

By addressing these questions, we add to the literature by providing a specific yet generalizable case study on the role of banks in engaging in transition financing. From an analytical perspective, we complement studies in this field that apply a mixed methods approach by combining a literature review, quantitative analysis and qualitative expert interviews. A review of the study methodologies on sustainable finance shows that this approach has only been used so far in a minority of studies [

27].

We proceed as follows:

Section 2 outlines our conceptual background, whilst

Section 3 highlights the methodology for both external screening and in-depth interviews.

Section 4 presents our findings, which are discussed in

Section 5.

Section 6 draws policy conclusions from the insights offered by our market actors.

2. Conceptual Background

2.1. Sustainable Finance and the Role of Banks

As [

25] as well as [

35] point out, banks are one of the major sources of providing energy and climate finance. The authors of [

27] review the green finance products offered by banks based on a read-out of 46 studies. They identify green credit/loans, green long-term investment accounts, carbon finance, climate finance, green traded stocks and bonds, green bank assurance and green infrastructural finance. With this vast array of financial products, the banking sector seems to be well suited to finance a large span of energy transition projects. These range from direct loans for large transition projects to ideally channeling small-scale deposits toward large-scale projects. Especially regarding the latter aspect, several recent studies note the intermediary role in absorbing and distributing idle funds within society to ensure economic development [

23,

24,

27]. In other words, banks can perform a strategic intermediary role between retail customers’ deposits and the financing needs of transition projects.

The role of banks and the challenges that they face in providing sustainability finance have been reviewed for several countries [

38,

39,

40], underlining the difficulty of banks to find profitable business models that both work for the short- and long-term, adapting to sometimes conflicting government regulations for green finance and risk disclosure and optimizing risk-return profiles in this segment. So far, investment products focus on large private and institutional investors The term ‘institutional investor’ covers a wider range of actors, e.g., foundations, sovereign wealth funds, etc., as well, in addition to insurance, reinsurance and pension companies, with banks playing an essential role in bringing these investments into large-scale deployments of energy technology [

5,

7] and into renewable energy projects [

41,

42,

43,

44,

45,

46,

47]. However, more is needed to fund the full amount of decarbonization projects [

5,

7,

8,

25,

45,

47,

48,

49].

This shifts the focus to retail customers, who could provide additional finance resources. The role of banks’ customers has been analyzed in several studies [

50,

51,

52,

53,

54], but until recently has played only a marginal role [

44,

45]. Studies have investigated this in willingness to pay analyses for green financial products—that is, accepting lower returns on investment and general attitudes toward green finance. However, these studies are partly contradictory and do not allow drawing clear conclusions on the role of retail customers: while they demonstrate an increased willingness to engage in sustainability finance [

53], they likewise highlight a high amount of skepticism against these products [

54], limited financial literacy [

51,

52] and an overall aversion of risks [

4,

50]. This is mirrored in Germany, where sustainable investment is not common among retail customers [

40,

55]. A survey by the German Banking Association found that only 8% of retail customers in Germany hold sustainable investments [

56]. This insignificant role is in stark contrast with the potentially large role that this group could play to support the energy transition [

45,

49]. The German financial market has large amounts of private capital in search of profitable investments [

37], but the capital has not found its way into the clean energy projects of the national energy transition.

2.2. The Banking Sector in Germany

Ref. [

26] reviewed the German banking sector and found that a dense network of locally rooted banking institutions exists, which is able to provide suitable finance to renewable energy projects on all scales. In a recent study on mapping actors and discourses related to green finance, ref. [

57] presents an overview of the German banking system. The system is characterized by the coexistence of private banks and publicly (co-)owned banks such as the state support bank KfW (

Kreditanstalt für Wiederaufbau).

The German central bank (

Bundesbank) maintains a list of active banks present in Germany, listing almost 1500 institutions [

58]. Deutsche Bank is the largest privately owned commercial bank (assets of about EUR 1500 bn), with DZ Bank and Commerzbank (assets of about EUR 500 bn) following it. In addition, a large number of specialized or regionally focused banks exist [

57]. This decentralized and pluralistic structure allows the banking system to operate relatively closely to its customers and offer tailor-made financial products for their clients. The authors of [

25] as well as [

35] note that in Germany, banks are the major source of finance for clean energy projects. Despite this proximity, [

59] reports that there were only 10.3 million shareholders in Germany in 2019 active in this field. In contrast, a significant volume of retail customers have invested in treasury bonds and saving accounts, thus showing a high amount of risk aversion.

The sector is framed by both European and national regulation that will be presented in the next section.

2.3. Regulatory Framework

Several authors [

7,

32,

57] point out that the offer of climate and energy finance is largely determined by underlying regulatory frameworks. In the case of Germany, both European and national regulations apply (

Table 1).

At the European level, increased efforts are underway both to mobilize capital for green finance and to safeguard the transparency, reliability and accountability of financial products. The key EU provisions shown in

Table 1 relate to (1) mobilizing investments in climate and clean energy finance; (2) creating enhanced transparency for retail customers by means of comprehensive disclosure obligations to prevent banks from only publishing selected information on a financial product, or ‘greenwashing’ [

60], and (3) increasing market transparency and facilitating investment decisions, notably by mandating banks to investigate in customers’ sustainability preferences and by providing a positive list (‘taxonomy’) of sustainable investment areas.

The Taxonomy Regulation in particular is expected to impact strongly on individual investment decisions. It sets out an EU-wide classification system for sustainable economic activities across six major fields [

61] These are (i) climate change mitigation, (ii) climate change adaptation, (iii) circular economy, (iv) water use and marine protection, (v) biodiversity and (vi) pollution prevention. All six fields are to be further spelled out by a positive list of activities that will advance these fields by means of delegated acts. In order to qualify as an environmentally sustainable investment, economic activity must contribute substantially to one of these objectives and not harm any of the other objectives (“Do No Significant Harm Principle”). When put into practice, the Taxonomy Regulation means that financial products supporting the energy transition should be listed or labeled as such and be clearly identifiable by retail customers [

62].

Turning to the German regulatory framework, we observe that national laws mostly implement EU regulations. As such, no significant national or regional provisions augment European legislation. However, the German Federal Agency for Financial Market Supervision (

BAFin) facilitates the implementation of European/German regulations by providing guidelines for the financial sector. These guidelines are intended to support the implementation of European and national provisions. Notably, the Guidance Notice on Dealing with Sustainability Risks [

63] and a draft Guideline on Sustainable Investments [

64] stand out as being those addressed to financial institutions that might offer transition-related products, as the guidance defines the administrative practice and constitutes the framework for potential legal disputes.

It has emerged that the offer of green finance products is limited by risk considerations as regards bank liquidity, risk protection and the information of retail customers. Only lately have considerations been encouraged to actively promote sustainable investments. As such, it remains largely with the banking sector to decide which green finance products are promoted and offered to retail customers.

3. Methodology

3.1. Overview

To determine the role of German banks in mediating investment products that support the German energy transition, we applied a mixed methods approach by combining a literature review, quantitative analysis and qualitative expert interviews. A review of the study methodologies on sustainable finance shows that this approach has only been used so far in a minority of studies [

27]. The approach was chosen to triangulate findings by applying a three-tier approach (see

Table 2).

Tier one took stock of the role of banks and their particular portrait in the case of Germany, including their regulatory environment. In tier two, we reviewed public information from a representative sample of banks on their investment products for retail customers. In tier three, we performed in-depth interviews with sector experts to build on the key findings from tier two. Specifically, we were interested in what motivates finance institutions to provide clean energy investment products for retail customers, what barriers exist against such investment products, and how favorable policies could help to mobilize private capital for the energy transition. Seeking input from all relevant supply-side perspectives, we interviewed representatives of banks, non-governmental organizations specializing in clean energy finance, and national regulatory authorities. The combined results help to establish the status quo of the offers promoted (tier 1–2) and expert feedback on how and by which means the further engagement of banks could be mobilized (tier 3).

3.2. Screening of Bank Offers

Tier two of our methodology consisted of screening websites and financial statements of a representative sample of German banks to profile the financial products offered to retail customers. Our sample was taken from the population of banking institutions given by the central registry of the German central bank (

Bundesbank), which lists 1468 banking institutions [

58]. We excluded public regional banks (

Landesbanken) that do not directly interact with retail customers. To mirror the remaining banking groups in a representative sample, we applied the standard Wald method for deriving an optimal sample size [

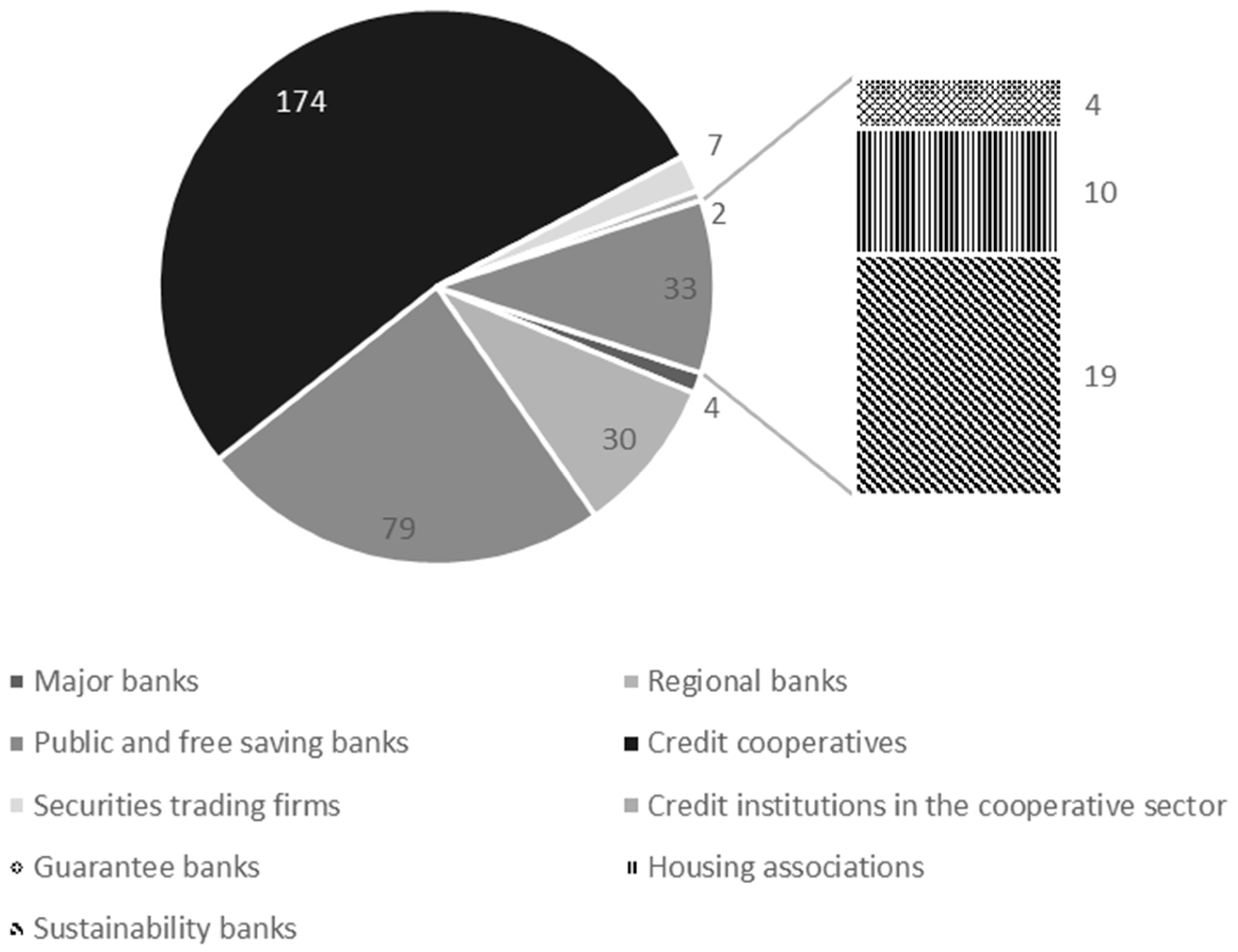

65]. For a confidence interval of 95%, this resulted in a sample size of 329. As a next step, we made sure that our sample was representative of the population by applying stratified sampling. This implies that if, e.g., sustainability banks represented 1% of all banking institutions in the population, they should also represent 1% of the sample. After establishing these subsets, we drew our sample by indexing the banks of each subset and then used a random number generator to select indices. For the subset of ‘major banks’ (n = 4), all banks were included due to their small number but large outreach capacity (see

Figure 1).

We collected publicly available information from these banks on offers for financing clean energy projects. Information came from (1) internet webpages and (2) the most recent annual and sustainability reports. To systematize the information found, we applied qualitative content analysis [

66], based on a code plan that was updated as the analysis progressed (‘in vivo’ coding). Using MAXQDA text analysis software, we performed automated screening to gain an overview of the available offers by the coded sequences. In a follow-up manual screening, we sorted the identified investment products given the coded sequences into the following categories:

- (a)

No offer to retail customers of products related to clean energy;

- (b)

Offers available, but only as a broker to third-party projects and products;

- (c)

Offers available, but not focused solely on the national energy transition;

- (d)

Investment flow focused on clean energy projects in Germany.

To safeguard intercoding and sorting reliability, we applied a ‘four-eyes-minimum’ principle to both coding and sorting.

3.3. In-Depth Interviews with Financing Experts

Our screening of bank offers allowed us to assess the clarity and transparency, based upon which retail customers are taking first decisions to invest in the clean energy transition. Its results can inform our first research question, related to the availability and form of green finance products available for retail customers. However, the screening did not allow us to investigate the possible reasons for the structure of these offers (research question 2), nor did it allow us to obtain input on (regulatory) means to increase offers or better match supply and demand (research question 3). To address these questions, we led a series of in-depth interviews with three main groups of sector experts: (1) financial institutions, including credit institutions and rating agencies; (2) government and regulatory experts; (3) financial experts from NGOs.

We first established and contacted a pool of investment managers, project finance officers, sustainability managers, relevant regulatory authorities and NGOs active in sustainable finance acting as frontline informants for sustainable investments. We contacted 107 banks to cover a broad spectrum and, in particular, to be able to draw comparisons between banks offering energy transition investment products to retail customers and banks not offering these products to this group. Furthermore, our contacts included 21 banks that distribute financial products to savings banks and cooperative banks as well as environmental organizations, government organizations, professional associations and rating agencies in Germany.

Contact was established via e-mail or an online contact form in April 2021. In total, this led to 12 interviews with sector experts from the abovementioned stakeholder groups (see

Table 3 for an overview).

We refer to interviewees by ID numbers designated with ‘I’ for ‘Interviewee’ and a distinguishing number from 1 to 12.

Interviews were conducted via phone and MS—Teams between April and August 2021. The interviews lasted between 25 and 50 min, depending on the interviewee’s availability.

Interviews were recorded and transcribed following [

67]. Based upon [

66], we performed qualitative content analysis with the help of MAXQDA, a qualitative research software, and grounded theory methodology [

68]. The analytical strategy involved a process of re-reading the transcripts and encoding the collected data. Beginning with open coding, we marked the relevant content that was connected to our research question. In subsequent steps, codes were aggregated into categories and sub-categories. The final category system used for extraction consisted of six main categories.

Table 4 presents these categories and the underlying codes. In order to avoid subjective coding—which appears to be a major disadvantage of this methodology [

69]—memos for the codes were written and the codes were discussed between the authors. Based on the coding, we applied statistical tests to assess the internal consistency of the questions (Cronbach alpha) and pertinence of the answers via a simple consistency check. Both showed good levels of 0.64 and above (see

Supplementary Material S1).

The EEG (Erneuerbare-Energien-Gesetz) or Renewable Energy Sources Act is a series of German laws providing a feed-in tariff scheme.

4. Results

4.1. Availability and Structure of Finance Offers

4.1.1. Supply Structure

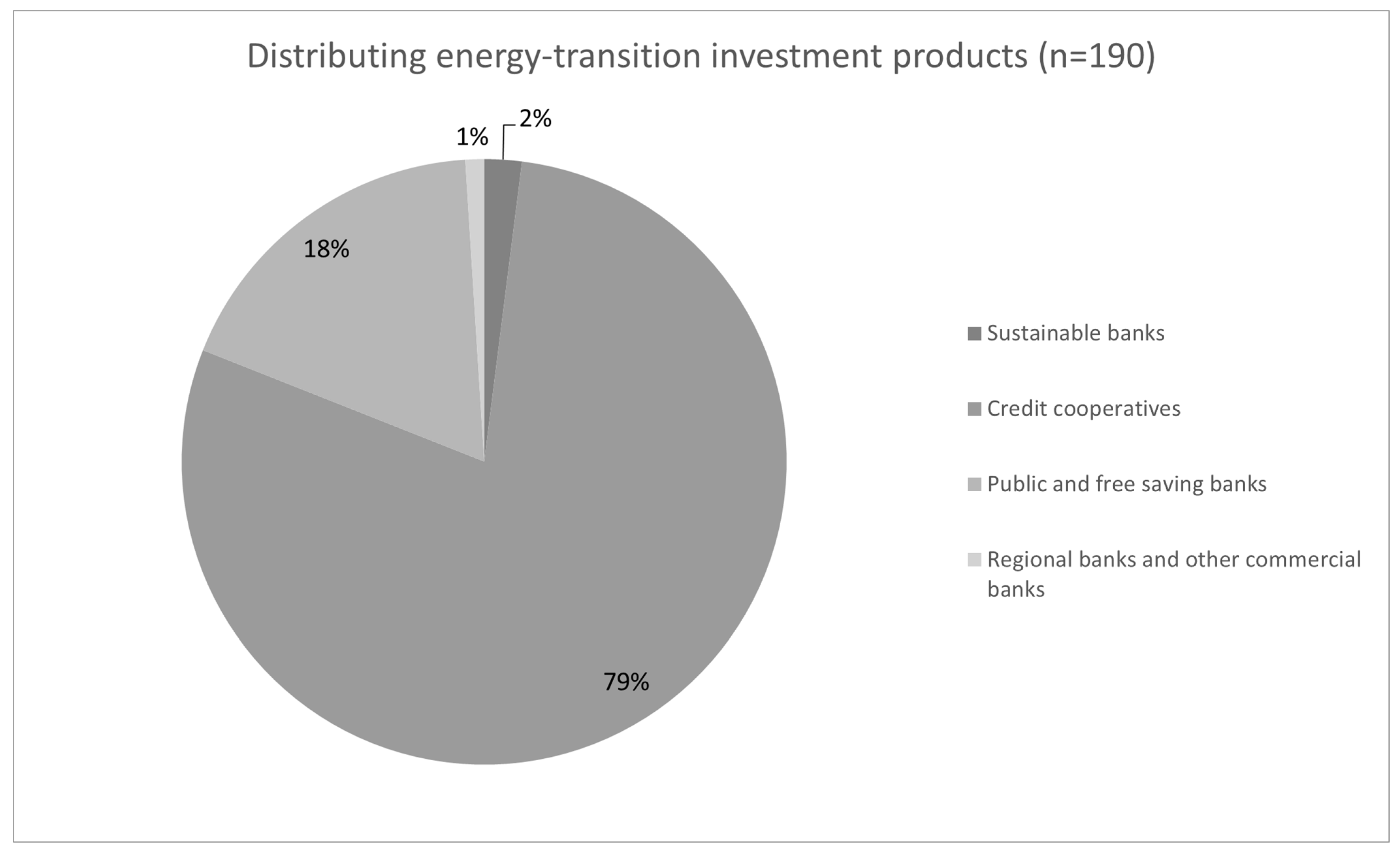

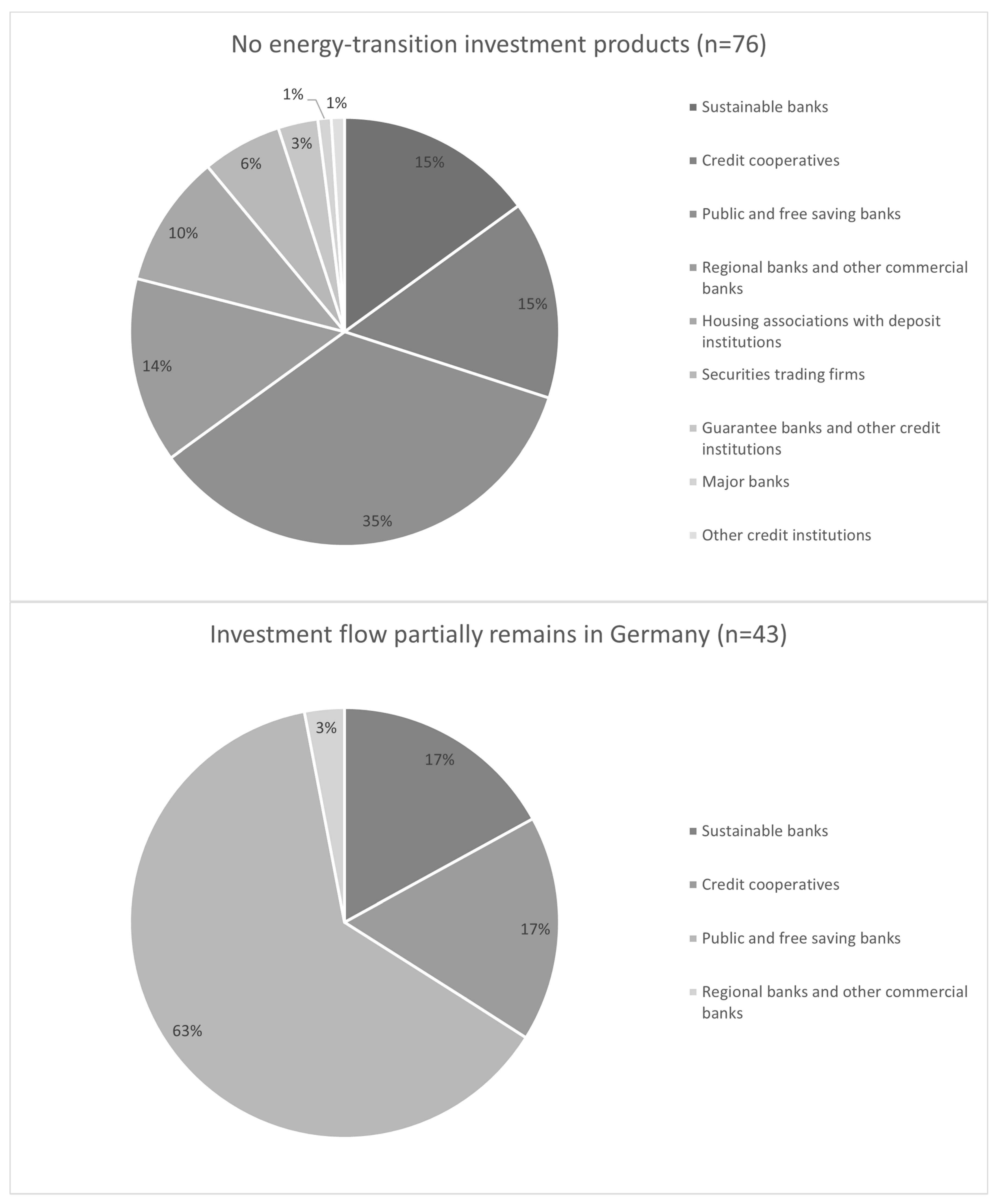

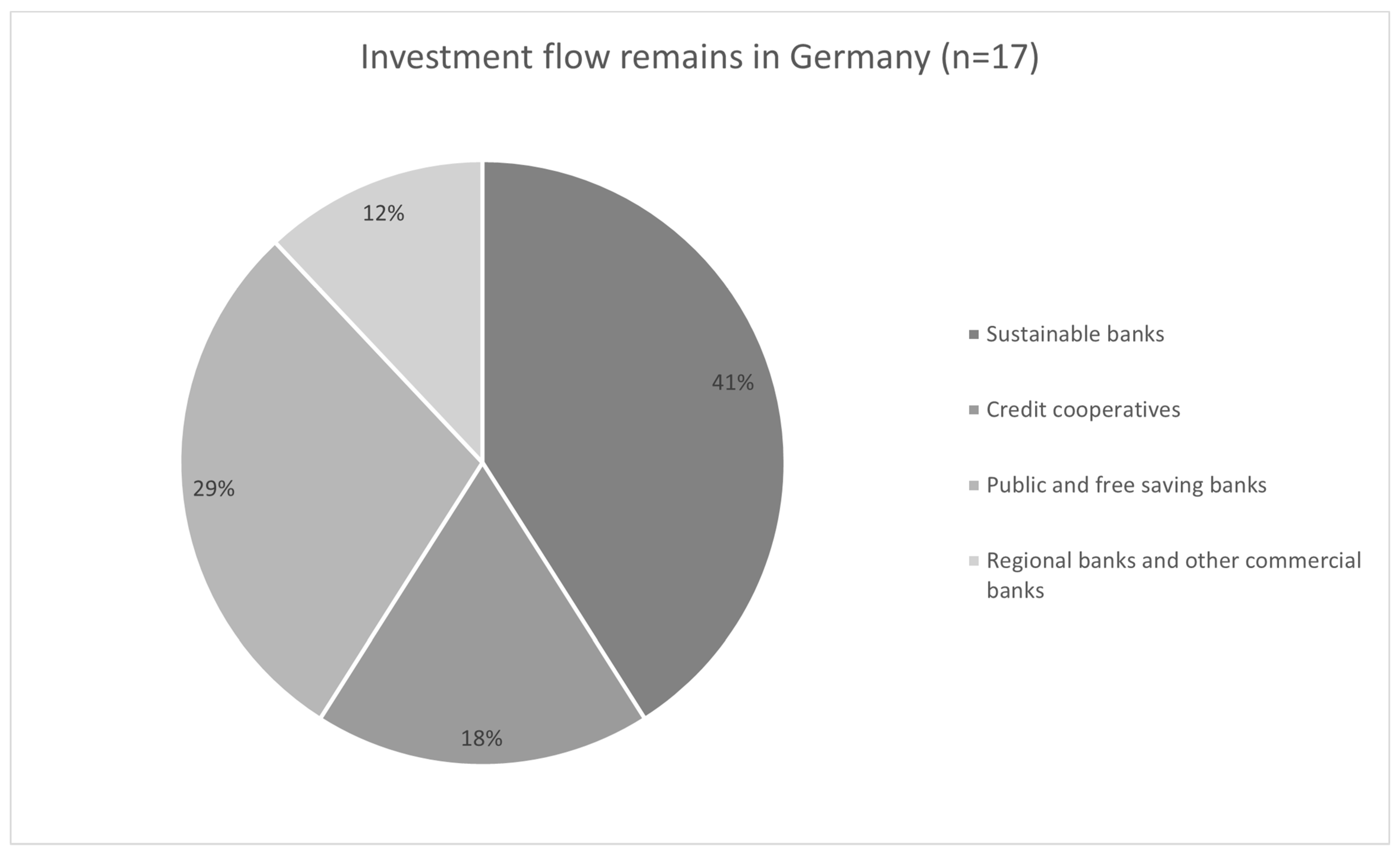

Results from the screening of publicly available information (bank websites, annual business and sustainability reports) confirm an overall lack of green investment products that focus on small- and medium-sized retail customers. Nearly one quarter (76 or 23%) of the banks sampled did not offer any energy-transition-related investment products. The majority (190 or 59%) only relay or broker energy transition investment products offered by providers of asset management. While 46 or 14% of the banks offer products whose investment flows partly remain in Germany, only 17 (5%) of the banks’ investment products focus solely on the German energy transition. That only 5% of the banks sampled provide opportunities for small and medium investors to participate directly in the national energy transition shows how niche this market remains. The niche, however, is strongly exploited by sustainability banks, with 41% of them offering dedicated investment products.

Based on this overall assessment,

Figure 2 illustrates interesting structural differences between the types of banks, highlighting the special role of sustainability banks in providing finance related to the clean energy transition.

Sustainability banks also stand out in terms of providing detailed information to customers. Generally, the information on energy transition investment opportunities for retail customers provided on the websites of banks is mostly fragmented and offers insufficient information on specific investment opportunities. Interviewees I3 and I4 confirm that this implies that retail customers wanting to invest in the energy transition have to actively seek out opportunities. In contrast, sustainability banks address retail customers directly and provide comprehensive information about the details and risks of investment products supporting the clean energy transition.

It appears that banks are reluctant to actively promote energy transition investment opportunities. This is likely due to general caution toward this financial segment. Ref. [

70] already found that German banks are reluctant to offer sustainable financial investments—again with the exception of the sustainability banks. Such reluctance was reflected in the limited range of financial products offered. Their screening also showed that savings banks and cooperative banks offered a smaller selection of sustainable financial products to retail customers than sustainability banks did.

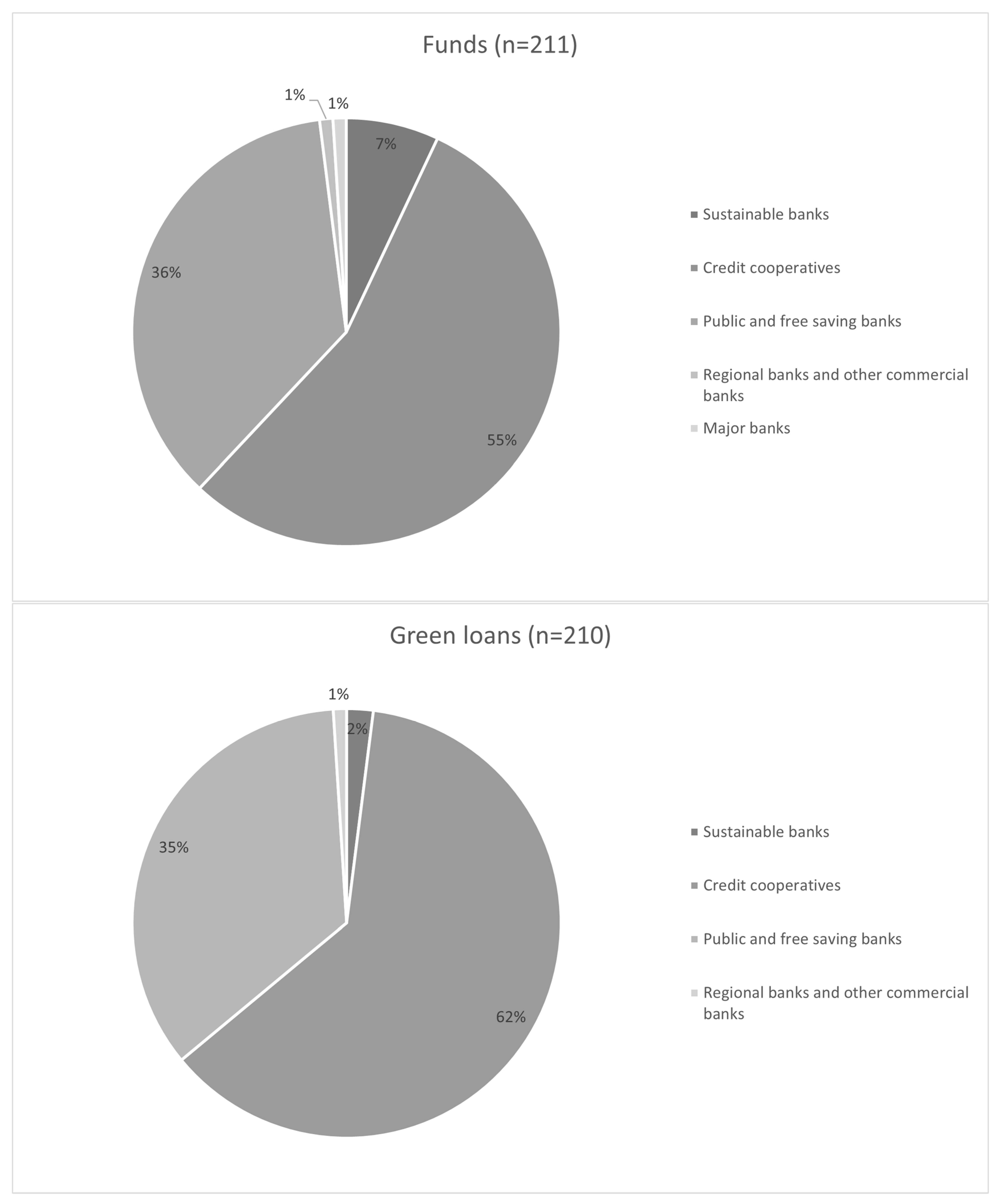

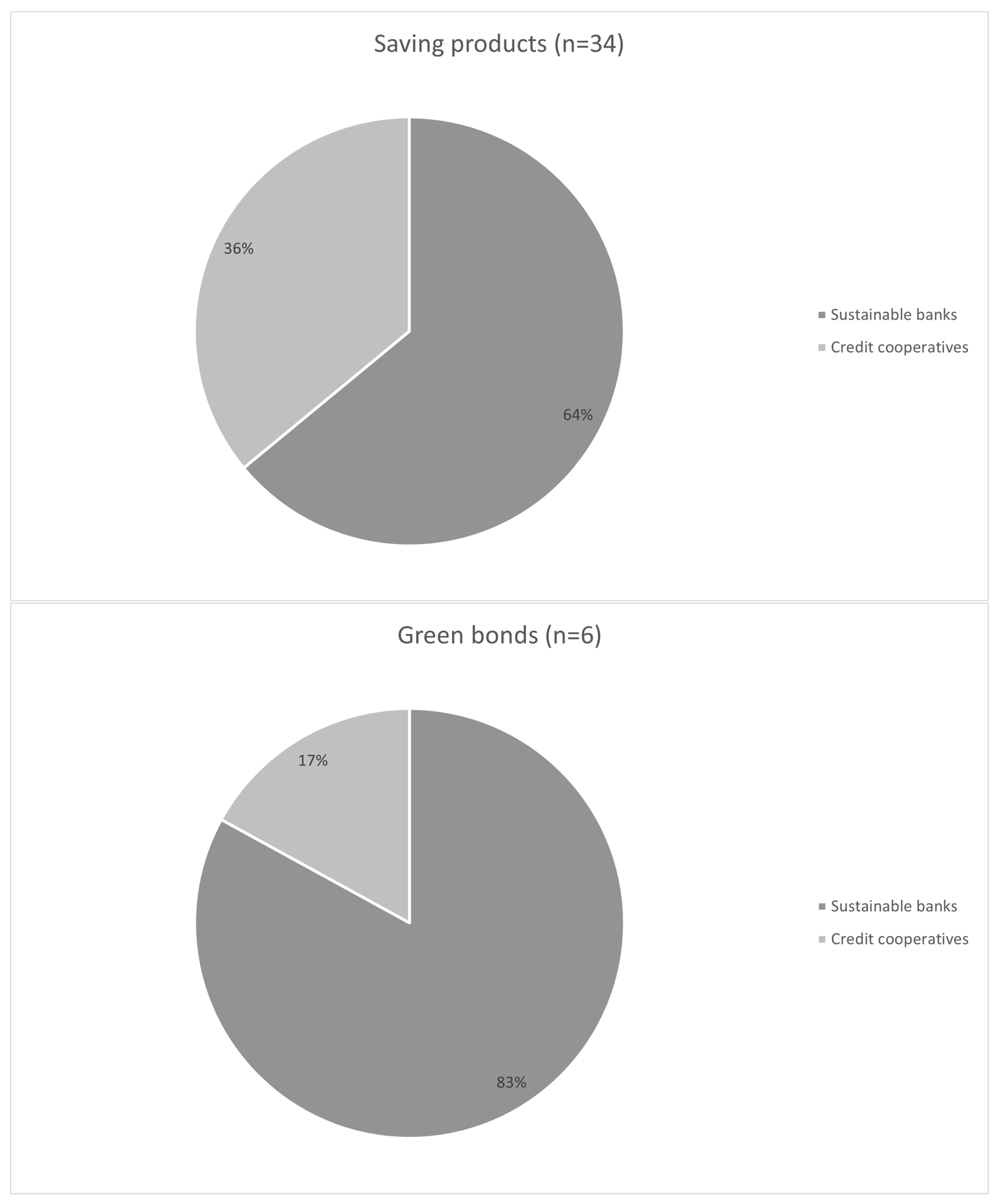

4.1.2. Products Promoted

Turning to promoted finance products that allow retail customers to invest in the clean energy transition, investment funds are the most common class of product, offered by 211 of the institutions in our sample (64%). These funds offer purpose-oriented topic-specific investments. A total of 210 banks (64% of the sample) offer ‘green loans’, allowing retail customers to invest in energy renovation projects of the real estate sector. A further 133 of the banks (40%) marketed concessionary loans from the Kreditanstalt für Wiederaufbau (KfW). Other product classes were rare: only six banks (2%) offered green bonds, while another eleven institutions (3%) offered ethical, social or environmental interest rate products. These were generally offered in the form of savings bonds, time deposits or classic savings plans.

Figure 3 presents an overview of the identified financial products and the repartition per type of bank that offers these products. The financial products offered to investors also varied markedly with the type of institution, confirming earlier studies [

36].

In summary, investment funds and green loans dominate the green financial market, while products with lower risk profiles such as savings books, savings bonds or time deposits remain niche products (see also [

71]). However, these products have the potential to attract further depositors in the future [

72].

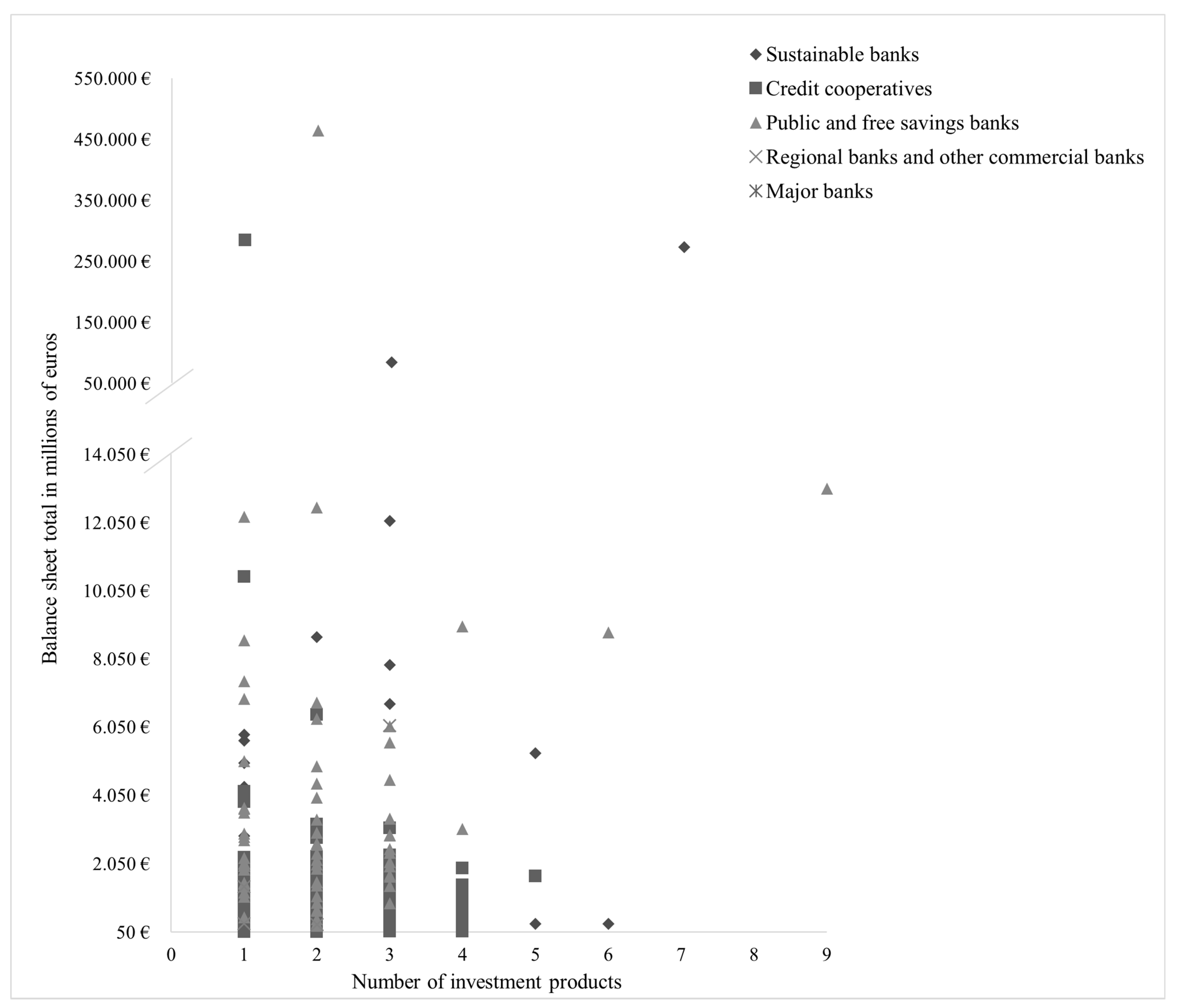

4.1.3. Offers per Bank Size

In a next step, we analyzed whether the number of financial products offered depended on the size of the banks. For this purpose, we collected the balance sheet totals for each bank in our sample as an indicator for the size of the banks.

Figure 4 shows the distribution for banks.

There is no indication that a broader range of financial products for retail customers was offered by larger banks. However, in comparison, sustainability banks offered more financial products. They provided on average three investment products (regardless of category) for retail customers.

4.2. Explanatory Factors for the Existing Offer

To answer our second research question (factors that explain the existing offer of financial products for retail customers), we provided 12 sector experts with our results and asked them to comment in structured interviews. Interestingly, the replies across all of the interviewed groups (financial institutions, NGOs, government experts) aligned strongly. For this, we decided against differentiating between the different groups and rather referred to the individual interviewees.

The experts noted that some financial institutions such as sustainability banks focusing on supporting the local energy transition served as role models (I3, I6 and I7) that raised interest with many retail customers. This could lead to increasing demand by retail customers for sustainable investment products (I1-I12) and drive other financial institutions to invest in these products (I2-I12). Our experts expected a growing number of offers to result from demand-side pressure. Interviewee I12 emphasized that ‘private investors [will] ask for sustainable financial products and this will then […] create a driving force’. Along a similar line, another interviewee affirmed that ‘an increase in offers will be pushed by demand, given that the topic of sustainable finance has raised stronger interest with retail customers’ (I3).

Against this background, we asked experts why the promotion of relevant finance products has remained such a niche market so far. Numerous studies have reported financing as being one of the major challenges to the deployment of low-carbon technologies [

4,

9] and evidence shows a significant gap in financing low-carbon projects and industries [

7]. In contrast, however, our experts (I1, I2, I3, I6, I7 and I12) see finding (attractive) projects as the most significant barrier to increasing capital flows and promoting related products. Even though German retail customers were found to be willing to invest in wind energy and ready to accept financial disadvantages for such projects [

42], there is a lack of projects to invest in (I1, I2, I3, I6, I7 and I12). As interviewee (I2) pointed out, ‘there is [no] lack of liquidity, there is a lack of assets’.

As a second factor for low offers, several interviewees (I9, I11 and I12) pointed out that sustainable investments are still little known by or at least less visible to retail customers. Banks and financiers still see institutional investors as the predominant target group when it comes to investment decisions (I3, I5, I6, I8 and I9). This is reflected in the range of products and services offered to institutional investors (I4, I5). Several experts (I1, I2, I3, I6 and I7) confirm efforts to both expand financial products and create new products for a larger customer base. However, most of our experts point out that regulatory changes are needed to support efforts of the private banking sector to expand financial products for retail customers.

4.3. Options to Further Develop the Offers for Sustainable Finance

4.3.1. Data Availability and Transparency in Assessing Financial Products

The complexity of sustainable financial products implies that the reliability of sustainable standards is especially important for investor trust [

50]. Achieving retail customers’ acceptance depends on the trustworthiness of energy transition investment details, if past failures on providing transparency [

5,

41,

50] are not to be repeated. According to our experts, the availability and visibility of information and the transparency of financial products offered are key factors in building trust (I3, I4, I8, I9, I11 and I12). Yet, the present criteria used to identify sustainable investments are open to wide interpretation, so that investors do not perceive these standards as trustworthy [

50].

Ref. [

50] argues that trust can be developed via certifications and transparent ratings of financial products. These findings are mirrored by our experts (I3, I5, I9 and I11), who point out the importance of such tools for retail customers with little financial literacy. However, stricter rating and certification procedures imply higher costs, which are then priced into the financial products (I6, I9 and I10).

Echoing calls in the literature, our interviewees call for clear regulations (I1, I2, I3, I10, I11 and I12) and clear standards for certification and labels (I3, I4, I5, I6, I9, I10 and I11). These calls are backed by studies that suggest that labels for investment products act as a nudge to generate demand [

36]. The lack of standardization (I7, I9 and I10) prevents comparisons between different ratings, which in turn highlights the need to harmonize rating methods and disclose their methodologies and underlying data (I9).

Labels that assess the transparency or quality of financial products could also make a decisive contribution to strengthening public confidence. Since labels and certifications are not yet subject to the rigor that banks impose on themselves (I2, I6), experts from both the non-governmental organizations and the financial institutions propose the development of a label for taxonomy-aligned financial products to help reach retail customers (I3, I4, I5, I6, I9, I10 and I11).

4.3.2. Strengthening Investment Advice Services

Both the literature and our expert feedback confirm that there is growing interest in sustainable investments by retail customers (I1, I3, I4, I5, I6, I7 and I11; [

31,

32]). However, both also agree that financial literacy in Germany is weak (I3, I5, I6, I8, I10 and I11; [

51,

52]). As interviewee I10 put it, ‘Adding to other barriers there is the problem of insufficient financial education of retail customers, which makes it hard to offer suitable investment products to them. Neither standardized finance monitoring nor support programs to enhance financial literacy exist’. As Refs. [

36,

44] and [

73] report, information deficits lead citizens to misjudge both monetary and non-monetary costs and benefits of the energy transition. Our experts mirror this view, underlining the fact that retail customers are not trained in finance or risk assessment (I3, I5, I6, I8, I10 and I11).

This implies that sound investment advice by financial institutions is central. Regarding this advice, our experts demand transparent, comprehensible and easily accessible information for retail customers (I4, I5, I6, I8, I9, I10, I11 and I12). Clearly, there is a need for stronger regulations on providing this information; our screening shows that, at present, only sustainability banks provide complete and transparent public information to retail customers about their green finance products.

4.3.3. Reducing Investment Risks for Retail Customers

Price and risk are relevant triggers to reorient the financial sector toward a sustainable economy [

47,

74]. However, investments in renewable energy projects and energy efficiency solutions are still largely perceived as high-risk investment and involving large investment needs [

30,

35]. This again is in stark opposition to the profile of retail customers. This group is characterized by small budgets and high risk aversion (see [

4,

50], confirmed by our interview partners I1, I3, I4, I5 and I10). With long amortization periods or high risks involved, many financial products are not suitable for retail customers (I4, I5 and I9), even if investors ‘who are strongly favorable to the energy transition […] would be willing to put all their eggs in one basket’ (I6).

When asked about mitigating measures against the risk barrier, the experts cite broadening the funding base and diversifying the investment risk (I3, I6, I7 and I12). As a further option, de-risking is mentioned. In line with Refs. [

41,

75], our experts call for additional investment securities (I1, I10) to incite more private investment by retail customers. These guarantees provided by the government or the European Investment Bank (I1, I9) could reduce risk exposures for retail customers and in consequence would further boost this market segment.

4.3.4. Implementation via Strengthened Regulatory Framing

Our experts converge with findings in the literature that the growth in investments in low-carbon energy solutions depends upon long-term policy perspectives and a broad set of financial instruments (I1, I2, I3, I6, I8, I9, I10 and I11; [

5,

41,

57,

70,

76]) but also upon appropriate regulation [

22,

25,

44,

77,

78,

79]. There is wide consensus in the literature that the lack of a supportive policy framework is the main barrier for retail customers [

4,

77,

80,

81].

Our experts saw a need for relevant regulatory inventions in two fields: (i) the strengthening of the EU taxation regulation and linking it to duty disclosures on the underlying real economy assets; (ii) regulatory framing of customer advice via the revised Markets in Financial Instruments Directive (MiFID II).

Regarding (i), the strengthening of the taxation regulation, the experts suggested a broadening of the Taxonomy Regulation (I3, I8, I9 and I11) to extend it to both green and social taxonomies (I4, I6) and to increase its transparency (I3, I5, I6 and I11). This demand for transparency also strongly relates to missing data from the real economy. Experts reported that they lack energy project data that they can use for their own assessments and activities (I3, I4, I8 and I9). To this end, it is recommended that a central (European) database is established that financial market participants could access to derive assessments of financial products (I9).

Turning to (ii), a regulatory framework for customer advice, MiFID II obliges bank advisors to query retail customers’ sustainability preferences in addition to similar questions regarding financial literacy and risk preferences. On this basis, suitable investment products are then recommended. This ‘demand-side activation’ is cautiously welcomed by experts (I3, I4 and I6).

Experts expect that this additional transparency will most likely (1) increase understanding of sustainable finance as well as shift awareness of issues related to the energy transition (I6, I7, I8, I9 and I11), (2) decrease information asymmetry between retail customers and financial intermediaries and (3) facilitate access for retail customers to more climate-friendly investment products (I3, I5, I6, I8, I9 and I11). However, considering the complexity of the codes of conduct and the need for transparent policies, bank advisors will require adequate training (I5, I8), which might be a challenge at short notice (I5, I11).

5. Discussion

5.1. Similarities and Differences with Earlier Findings

Next to the presentation of our results for the German case, this raises the question of their confirmation or contrast to earlier findings in the literature.

Table 5 contrasts the results from earlier studies to our findings.

Following up on [

25,

26,

27], who confirmed a research gap regarding case analyses and motives for providing sustainable finance, especially for retail customers, our study contributes to closing this gap. While our results validate many earlier findings, they notably add to the present literature regarding the following points: First, the offer of sustainable finance products does not depend on bank size. Next, rather than missing finance, our findings suggest that the key barrier against engaging with the retail customer segment comes from a combination of (a) transaction costs to develop this market segment and (b) missing transparency on features of clean energy projects that allow for a proper risk assessment and matching to customers’ risk profiles. De-risking via government backup is however only requested by a minority of stakeholders. A larger group favors increasing market transparency via the harmonized provision of information, reporting and standards, as well as labels based on this information.

5.2. Critical Reflection of Methods

As Ref. [

27], also citing [

82], notes, it is not easy to obtain data on the green finance of banks. To overcome this hurdle, we use publicly provided information on sustainable energy finance provided by the banks themselves as proxy for the available offer. Banks are under increasing pressure from government and retail customers [

57] to provide green finance and can in turn be expected to promote their available offers. Whereas our approach will not be rigorous enough to capture all offers in practice, it can serve as an approximation of the minimum amount of offers available to retail customers.

As a next step, we complemented our findings by conducting expert interviews. While the sample of 12 respondents is not fully representative, it includes experts from banks, NGOs and public regulators that are best placed to comment on market offers and potential reasons for this offer. Given the difficulty in obtaining internal business insights due to confidentiality obligations, we sought to identify ‘information-rich cases’ that would allow in-depth analyses [

83]. We used a semi-structured interview questionnaire, pre-tested with two sector experts (representatives of a ‘sustainability-oriented’ bank), and chose an exploratory approach to support open-ended discussions with the interviewees. In doing so, our study can help to corroborate studies with a similar design, such as [

71] who based their findings on seven interviews.

As in all studies applying interviews, interviewer bias and selection bias in the coding procedure pose a challenge. We tried to minimize these by following a similar semi-structured procedure in all of the interviews and by asking open questions. Selection bias was addressed by involving peer-review in the transcription and coding process, as proposed by [

32].

Including the demand side, in our case, small retail customers, would have helped to corroborate findings and bring an additional granularity of information. Obtaining feedback from this group on their perception of green finance offers was not possible due to confidentiality restrictions prevailing in the banking sector. Yet, this is an aspect that could be addressed in follow-up research by analyzing the views of consumers on the use, availability, and challenges of availing or finding green finance and how to best use it in an effective manner.

6. Conclusions

This study analyzed the performance of German banks in offering energy transition investment opportunities to retail customers. Mobilizing private capital for the energy transition is necessary, as system-wide investments are needed that surpass government funding. The banking sector has a key role to play by offering suitable investment products to attract private capital. We investigated the barriers faced by such products, and considered how policy could help to shift private capital flows to clean energy projects. We started by screening 329 institutions, selected to represent the German banking landscape, for relevant information from websites, annual reports and sustainability reporting. We then interviewed 12 industry experts for their views on current sticking points and possible ways to mobilize private assets.

Our screening shows that retail customers seeking to invest in the energy transition will only find opportunities in a niche segment. Publicly available information on products is relatively difficult to obtain, especially for retail customers, and is often vague or ambiguous. Advising retail customers, however, is disproportionately costly compared to the capital invested, especially as this group lacks financial training and tends to be risk-averse. So, while ample private capital exists, little of it is flowing into energy transition investments.

The experts see increasing demand pressure for sustainable financial products to support the energy transition, meaning that, as one interviewee (I2) put it, a ‘revolution from below’ might be unfolding. Three options were identified for steering willing private capital toward the energy transition:

Provide financial products that mitigate risk for investors; offer themed special-purpose funds to make energy transition investments more tangible for both investors and investment advisors.

Support investors via transparent, understandable and comparable information. The transparency and clarity of information on transition investments is expected to influence decision making, so the dissemination of knowledge about renewable energies is a must. In this context, experts made strong reference to the initiatives of the EU concerning the Taxonomy Regulation, as well as the MiFID II Directive.

Undertake the creation of stronger standardization and labeling for financial products, including a transparent rating system applied according to uniform rules.

Author Contributions

Conceptualization, M.R. and S.M.; methodology, M.R. and S.M.; validation, M.R.; formal analysis, S.M.; investigation, S.M.; resources, M.R.; data curation, S.M.; writing—original draft preparation, M.R. and S.M.; writing—review and editing, M.R.; visualization, S.M.; supervision, M.R.; project administration, M.R.; funding acquisition, M.R. All authors have read and agreed to the published version of the manuscript.

Funding

This research was funded by the German Federal Ministry of Education and Research (Kopernikus—Projekt Ariadne (FKZ 03SFK5LO)). The European Chair for Sustainable Development and Climate Transition at Sciences Po is funded by the European Investment Bank, Hermès International and HSBC.

Institutional Review Board Statement

The study was conducted according to the guidelines of the Declaration of Helsinki, and approved by the Institutional Review Board (or ethics committee) of NGU (25/11/2021).

Informed Consent Statement

Informed consent was obtained from all subjects involved in the study.

Data Availability Statement

Data can by obtained from the authors due to privacy restrictions.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Intergovernmental Panel on Climate Change. Climate Change 2021: The Physical Science Basis: Contribution of Working Group I to the Sixth Assessment Report of the Intergovernmental Panel on Climate Change. 2021. Available online: https://www.ipcc.ch/report/ar6/wg1/downloads/report/IPCC_AR6_WGI_SPM_final.pdf (accessed on 22 November 2021).

- Europäische Kommission. Sustainable Europe Investment Plan: European Green Deal Investment Plan. COM (2020) 21 Final. 2020. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/HTML/?uri=CELEX:52020DC0021&from=DE (accessed on 22 November 2021).

- Leibniz Institute for Economic Research at the University of Munich. Was uns die Energiewende Wirklich Kosten Wird. Available online: https://www.ifo.de/node/43785 (accessed on 28 March 2022).

- Polzin, F. Mobilizing private finance for low-carbon innovation—A systematic review of barriers and solutions. Renew. Sustain. Energy Rev. 2017, 77, 525–535. [Google Scholar] [CrossRef]

- Wüstenhagen, R.; Menichetti, E. Strategic choices for renewable energy investment: Conceptual framework and opportunities for further research. Energy Policy 2012, 40, 1–10. [Google Scholar] [CrossRef]

- United Nations Framework Convention on Climate Change. UNFCCC Standing Committee on Finance: 2018 Biennial Assessment and Overview of Climate Finance Flows, Bonn. 2018. Available online: https://unfccc.int/sites/default/files/resource/2018%20BA%20Technical%20Report%20Final.pdf (accessed on 12 October 2021).

- Geddes, A.; Schmidt, T.S.; Steffen, B. The multiple roles of state investment banks in low-carbon energy finance: An analysis of Australia, the UK and Germany. Energy Policy 2018, 115, 158–170. [Google Scholar] [CrossRef]

- D’Orazio, P.; Löwenstein, P. Mobilising investments in renewable energy in Germany: Which role for public investment banks? J. Sustain. Financ. Investig. 2020, 12, 451–474. [Google Scholar] [CrossRef]

- Hall, S.; Foxon, T.J.; Bolton, R. Investing in low-carbon transitions: Energy finance as an adaptive market. Clim. Policy 2017, 17, 280–298. [Google Scholar] [CrossRef]

- Pathania, R.; Bose, A. An analysis of the role of finance in energy transitions. J. Sustain. Financ. Investig. 2014, 4, 266–271. [Google Scholar] [CrossRef]

- Dikau, S.; Volz, U. Central Banking, Climate Change, and Green Finance. In Handbook of Green Finance; Sachs, J., Woo, W.T., Yoshino, N., Taghizadeh-Hesary, F., Eds.; Springer: Singapore, 2019; pp. 1–23. ISBN 978-981-10-8710-3. [Google Scholar]

- Kawabata, T. What are the determinants for financial institutions to mobilise climate finance? J. Sustain. Financ. Investig. 2019, 9, 263–281. [Google Scholar] [CrossRef]

- Li, Z.; Huang, Z.; Su, Y. New media environment, environmental regulation and corporate green technology innovation:Evidence from China. Energy Econ. 2023, 119, 106545. [Google Scholar] [CrossRef]

- Li, Z.; Liao, G.; Albitar, K. Does corporate environmental responsibility engagement affect firm value? The mediating role of corporate innovation. Bus. Strategy Environ. 2020, 29, 1045–1055. [Google Scholar] [CrossRef]

- Liao, G.; Hou, P.; Shen, X.; Albitar, K. The impact of economic policy uncertainty on stock returns: The role of corporate environmental responsibility engagement. Int. J. Financ. Econ. 2021, 26, 4386–4392. [Google Scholar] [CrossRef]

- Huang, Z.; Dong, H.; Jia, S. Equilibrium pricing for carbon emission in response to the target of carbon emission peaking. Energy Econ. 2022, 112, 106160. [Google Scholar] [CrossRef]

- OECD. Developing Sustainable Finance Definitions and Taxonomies; OECD Publishing: Paris, France, 2020; ISBN 9789264517301. [Google Scholar]

- Zhang, F. Leaders and followers in finance mobilization for renewable energy in Germany and China. Environ. Innov. Soc. Transit. 2020, 37, 203–224. [Google Scholar] [CrossRef]

- Diluiso, F.; Annicchiarico, B.; Kalkuhl, M.; Minx, J.C. Climate actions and macro-financial stability: The role of central banks. J. Environ. Econ. Manag. 2021, 110, 102548. [Google Scholar] [CrossRef]

- Buchmann, K.; Jones, A.; Zhang, Y.; Schönecker, J. Key challenges in crossborder interconnector finance. J. Sustain. Financ. Investig. 2021, 12, 1285–1307. [Google Scholar] [CrossRef]

- Schreiner, L.; Madlener, R. Investing in power grid infrastructure as a flexibility option: A DSGE assessment for Germany. Energy Econ. 2022, 107, 105843. [Google Scholar] [CrossRef]

- Polzin, F.; Sanders, M.; Serebriakova, A. Finance in global transition scenarios: Mapping investments by technology into finance needs by source. Energy Econ. 2021, 99, 105281. [Google Scholar] [CrossRef]

- Fu, J.; Ng, A.W. Green Finance Reform and Innovation for Sustainable Development of the Greater Bay Area: Towards an Ecosystem for Sustainability. In Sustainable Energy and Green Finance for a Low-Carbon Economy; Fu, J., Ng, A.W., Eds.; Springer International Publishing: Cham, Switzerland, 2020; pp. 3–23. ISBN 978-3-030-35410-7. [Google Scholar]

- Andreeva, O.V.; Vovchenko, N.G.; Ivanova, O.B.; Kostoglodova, E.D. Chapter 2 Green Finance: Trends and Financial Regulation Prospects. In Contemporary Issues in Business and Financial Management in Eastern Europe; Grima, S., Thalassinos, E., Eds.; Emerald Publishing Limited: Bingley, UK, 2018; pp. 9–17. ISBN 978-1-78756-450-3. [Google Scholar]

- Polzin, F.; Sanders, M. How to finance the transition to low-carbon energy in Europe? Energy Policy 2020, 147, 111863. [Google Scholar] [CrossRef]

- Hall, S.; Foxon, T.J.; Bolton, R. Financing the civic energy sector: How financial institutions affect ownership models in Germany and the United Kingdom. Energy Res. Soc. Sci. 2016, 12, 5–15. [Google Scholar] [CrossRef]

- Akomea-Frimpong, I.; Adeabah, D.; Ofosu, D.; Tenakwah, E.J. A review of studies on green finance of banks, research gaps and future directions. J. Sustain. Financ. Investig. 2021, 12, 1241–1264. [Google Scholar] [CrossRef]

- Brummer, V. Community energy—Benefits and barriers: A comparative literature review of Community Energy in the UK, Germany and the USA, the benefits it provides for society and the barriers it faces. Renew. Sustain. Energy Rev. 2018, 94, 187–196. [Google Scholar] [CrossRef]

- Novikova, A.; Stelmakh, K.; Klinge, A.; Stamo, I. Climate and Energy Investment Map in Germany: Status Report 2016; IKEM: Berlin, Germany, 2019. [Google Scholar]

- Egli, F.; Steffen, B.; Schmidt, T.S. A dynamic analysis of financing conditions for renewable energy technologies. Nat. Energy 2018, 3, 1084–1092. [Google Scholar] [CrossRef]

- Marois, T. How Public Banks Can Help Finance a Green and Just Energy Transformation, Amsterdam. 2017. Available online: https://eprints.soas.ac.uk/24844/1/How%20Public%20Banks%20Can%20Help%20Finance%20a%20Green%20and%20Just%20Energy%20Transformation_Marois_TNI_2017.pdf (accessed on 10 March 2023).

- Mielke, J. Signals for 2 °C: The influence of policies, market factors and civil society actions on investment decisions for green infrastructure. J. Sustain. Financ. Investig. 2019, 9, 87–115. [Google Scholar] [CrossRef]

- Gunningham, N. A Quiet Revolution: Central Banks, Financial Regulators, and Climate Finance. Sustainability 2020, 12, 9596. [Google Scholar] [CrossRef]

- Zhang, F. The policy coordinator role of national development banks in scaling climate finance: Evidence from the renewable energy sector. Clim. Policy 2022, 22, 754–769. [Google Scholar] [CrossRef]

- Steffen, B. The importance of project finance for renewable energy projects. Energy Econ. 2018, 69, 280–294. [Google Scholar] [CrossRef]

- Steiauf, T.; Schäfer, H. From integration to impact—A new investment climate for Germany’s SRI landscape. J. Sustain. Financ. Investig. 2014, 4, 38–60. [Google Scholar] [CrossRef]

- Sustainable Investment Forum. Marktbericht Nachhaltige Geldnlagen 2021: Deutschland, Österreich & die Schweiz. 2021. Available online: https://www.forum-ng.org/fileadmin/Marktbericht/2021/FNG_Marktbericht2021_Online.pdf (accessed on 1 November 2021).

- Cao, X.; Jin, C.; Ma, W. Motivation of Chinese commercial banks to issue green bonds: Financing costs or regulatory arbitrage? China Econ. Rev. 2021, 66, 101582. [Google Scholar] [CrossRef]

- Du, G. Nexus between green finance, renewable energy, and carbon intensity in selected Asian countries. J. Clean. Prod. 2023, 405, 136822. [Google Scholar] [CrossRef]

- Sunio, V.; Mendejar, J.; Nery, J.R. Does the greening of banks impact the logics of sustainable financing? The case of bank lending to merchant renewable energy projects in the Philippines. Glob. Transit. 2021, 3, 109–118. [Google Scholar] [CrossRef]

- Aguilar, F.X.; Cai, Z. Exploratory analysis of prospects for renewable energy private investment in the U.S. Energy Econ. 2010, 32, 1245–1252. [Google Scholar] [CrossRef]

- Gamel, J.; Menrad, K.; Decker, T. Is it really all about the return on investment? Exploring private wind energy investors’ preferences. Energy Res. Soc. Sci. 2016, 14, 22–32. [Google Scholar] [CrossRef]

- Gamel, J.; Menrad, K.; Decker, T. Which factors influence retail investors’ attitudes towards investments in renewable energies? Sustain. Prod. Consum. 2017, 12, 90–103. [Google Scholar] [CrossRef]

- Masini, A.; Menichetti, E. Investment decisions in the renewable energy sector: An analysis of non-financial drivers. Technol. Forecast. Soc. Chang. 2013, 80, 510–524. [Google Scholar] [CrossRef]

- Mathews, J.A.; Kidney, S.; Mallon, K.; Hughes, M. Mobilizing private finance to drive an energy industrial revolution. Energy Policy 2010, 38, 3263–3265. [Google Scholar] [CrossRef]

- Salm, S.; Hille, S.L.; Wüstenhagen, R. What are retail investors’ risk-return preferences towards renewable energy projects? A choice experiment in Germany. Energy Policy 2016, 97, 310–320. [Google Scholar] [CrossRef]

- Jacobsson, R.; Jacobsson, S. The emerging funding gap for the European Energy Sector—Will the financial sector deliver? Environ. Innov. Soc. Transit. 2012, 5, 49–59. [Google Scholar] [CrossRef]

- McCollum, D.L.; Zhou, W.; Bertram, C.; de Boer, H.-S.; Bosetti, V.; Busch, S.; Després, J.; Drouet, L.; Emmerling, J.; Fay, M.; et al. Energy investment needs for fulfilling the Paris Agreement and achieving the Sustainable Development Goals. Nat. Energy 2018, 3, 589–599. [Google Scholar] [CrossRef]

- Mazzucato, M.; Semieniuk, G. Financing renewable energy: Who is financing what and why it matters. Technol. Forecast. Soc. Chang. 2018, 127, 8–22. [Google Scholar] [CrossRef]

- Paetzold, F.; Busch, T.; Chesney, M. More than money: Exploring the role of investment advisors for sustainable investing. Ann. Soc. Responsib. 2015, 1, 195–223. [Google Scholar] [CrossRef]

- Erner, C.; Goedde-Menke, M.; Oberste, M. Financial literacy of high school students: Evidence from Germany. J. Econ. Educ. 2016, 47, 95–105. [Google Scholar] [CrossRef]

- Ergün, K. Financial literacy among university students: A study in eight European countries. Int. J. Consum. Stud. 2018, 42, 2–15. [Google Scholar] [CrossRef]

- Sun, H.; Rabbani, M.R.; Ahmad, N.; Sial, M.S.; Cheng, G.; Zia-Ud-Din, M.; Fu, Q. CSR, Co-Creation and Green Consumer Loyalty: Are Green Banking Initiatives Important? A Moderated Mediation Approach from an Emerging Economy. Sustainability 2020, 12, 10688. [Google Scholar] [CrossRef]

- McKinsey. Consumers Care about Sustainability—And Back It up with Their Wallets. Available online: https://www.mckinsey.com/industries/consumer-packaged-goods/our-insights/consumers-care-about-sustainability-and-back-it-up-with-their-wallets#/ (accessed on 12 May 2023).

- NKI Research. Nachhaltige Kapitalanlage bei Privatanlegern: Ergebnisse einer repräsentativen Befragung von Finanzentscheidern in Privathaushalten in Deutschland. 2017. Available online: http://nk-institut.de/wp-content/uploads/2017/10/NKI-Research-06-2017-Privatanleger-Befragung.pdf (accessed on 20 January 2021).

- Kantar, T.N.S. Nachhaltige Geldanlage: Wissen und Engagement der Deutschen: Ergebnisse einer Online-Umfrage im Auftrag des Bundesverbandes Deutscher Banken, Berlin. 2021. Available online: https://bankenverband.de/media/files/2021_05_20_Charts_U_NGA_2021.pdf (accessed on 6 November 2021).

- Kuhn, B.M. Sustainable finance in Germany: Mapping discourses, stakeholders, and policy initiatives. J. Sustain. Financ. Investig. 2020, 12, 497–524. [Google Scholar] [CrossRef]

- German Federal Bank. Verzeichnis der Kreditinstitute und ihrer Verbände Sowie der Treuhänder für Kreditinstitute in der Bundesrepublik Deutschland: Bankgeschäftliche Informationen 2 2020. Available online: https://www.bundesbank.de/resource/blob/847938/c26eb8b1c483d4d1ecfb473d7e15ce64/mL/verzeichnis-der-kreditinstitute-und-ihrer-verbaende-2020-data.pdf (accessed on 1 November 2020).

- Busch, T. Industrial ecology, climate adaptation, and financial risk. J. Ind. Ecol. 2020, 24, 285–290. [Google Scholar] [CrossRef]

- Jäger, L.; Ringel, M.; Schiereck, D. Green Bonds als Instrumente der Klimaschutzfinanzierung: Eine Literaturübersicht. Z. Bankr. Bankwirtsch. 2021, 33, 209–225. [Google Scholar] [CrossRef]

- Spinaci, S. Green and Sustainable Finance: Briefing PE 679.081. 2021. Available online: https://www.europarl.europa.eu/RegData/etudes/BRIE/2021/679081/EPRS_BRI(2021)679081_EN.pdf (accessed on 22 October 2021).

- Europäische Kommission. Overview of Sustainable Finance. 2021. Available online: https://ec.europa.eu/info/business-economy-euro/banking-and-finance/sustainable-finance/overview-sustainable-finance_de (accessed on 22 October 2021).

- Federal Financial Supervisory Authority. Guidance Notice on Dealing with Sustainability Risks. 2020. Available online: https://www.bafin.de/SharedDocs/Downloads/EN/Merkblatt/dl_mb_Nachhaltigkeitsrisiken_en.html (accessed on 22 October 2021).

- Federal Financial Supervisory Authority. Konsultation 13/2021—Entwurf einer BaFin-Richtlinie für Nachhaltige Investmentvermögen. Available online: https://www.bafin.de/SharedDocs/Veroeffentlichungen/DE/Konsultation/2021/kon_13_21_WA4_Leitlinien_nachhaltige_Investmentvermoegen.html (accessed on 29 November 2021).

- Rahi, S. Research Design and Methods: A Systematic Review of Research Paradigms, Sampling Issues and Instruments Development. Int. J. Econ. Manag. Sci. 2017, 6, 1–5. [Google Scholar] [CrossRef]

- Mayring, P. Einführung in Die Qualitative Sozialforschung; 5. Auflage; Beltz: Weinheim, Germany, 2002; ISBN 9783407290939. [Google Scholar]

- Dresing, T.; Pehl, T. Praxisbuch Transkription: Regelsysteme, Software und praktische Anleitungen für qualitative ForscherInnen; 8. Aufl.; Dr. Dresing und Pehl GmbH: Marburg, PA, USA, 2018; ISBN 978-3-8185-0489-2. [Google Scholar]

- Corbin, J.M.; Strauss, A. Grounded theory research: Procedures, canons, and evaluative criteria. Qual. Sociol. 1990, 13, 3–21. [Google Scholar] [CrossRef]

- White, M.D.; Marsh, E.E. Content Analysis: A Flexible Methodology. Libr. Trends 2006, 55, 22–45. [Google Scholar] [CrossRef]

- Schäfer, H. Germany: The ‘Greenhorn’ in the Green Finance Revolution. Environ. Sci. Policy Sustain. Dev. 2018, 60, 18–27. [Google Scholar] [CrossRef]

- Heinemann, K.; Zwergel, B.; Gold, S.; Seuring, S.; Klein, C. Exploring the Supply-Demand-Discrepancy of Sustainable Financial Products in Germany from a Financial Advisor’s Point of View. Sustainability 2018, 10, 944. [Google Scholar] [CrossRef]

- Krause, K.; Battenfeld, D. Coming Out of the Niche? Social Banking in Germany: An Empirical Analysis of Consumer Characteristics and Market Size. J. Bus. Ethics 2019, 155, 889–911. [Google Scholar] [CrossRef]

- Rogers, J.C.; Simmons, E.A.; Convery, I.; Weatherall, A. Public perceptions of opportunities for community-based renewable energy projects. Energy Policy 2008, 36, 4217–4226. [Google Scholar] [CrossRef]

- Thomä, J.; Chenet, H. Transition risks and market failure: A theoretical discourse on why financial models and economic agents may misprice risk related to the transition to a low-carbon economy. J. Sustain. Financ. Investig. 2017, 7, 82–98. [Google Scholar] [CrossRef]

- Hilke, A.; Ryan, L. Mobilising Investment in Energy Efficiency: Economic Instruments for Low-energy Buildings: IEA Energy Papers, Paris. 2012. Available online: https://www.oecd-ilibrary.org/energy/mobilising-investment-in-energy-efficiency_5k3wb8h0dg7h-en (accessed on 24 October 2021).

- Hafner, S.; Jones, A.; Anger-Kraavi, A.; Pohl, J. Closing the green finance gap—A systems perspective. Environ. Innov. Soc. Transit. 2020, 34, 26–60. [Google Scholar] [CrossRef]

- Polzin, F.; Egli, F.; Steffen, B.; Schmidt, T.S. How do policies mobilize private finance for renewable energy?—A systematic review with an investor perspective. Appl. Energy 2019, 236, 1249–1268. [Google Scholar] [CrossRef]

- Egli, F. Renewable energy investment risk: An investigation of changes over time and the underlying drivers. Energy Policy 2020, 140, 111428. [Google Scholar] [CrossRef]

- Krozer, Y. Financing of the global shift to renewable energy and energy efficiency. Green Financ. 2019, 1, 264–278. [Google Scholar] [CrossRef]

- Jones, A.W. Perceived barriers and policy solutions in clean energy infrastructure investment. J. Clean. Prod. 2015, 104, 297–304. [Google Scholar] [CrossRef]

- Granoff, I.; Hogarth, J.R.; Miller, A. Nested barriers to low-carbon infrastructure investment. Nat. Clim. Chang. 2016, 6, 1065–1071. [Google Scholar] [CrossRef]

- Cui, Y.; Geobey, S.; Weber, O.; Lin, H. The Impact of Green Lending on Credit Risk in China. Sustainability 2018, 10, 2008. [Google Scholar] [CrossRef]

- Patton, M.Q. Qualitative Research & Evaluation Methods: Integrating Theory and Practice, 4th ed.; SAGE: Los Angeles, CA, USA; London, UK; New Delhi, India; Singapore; Washington DC, USA, 2015; ISBN 9781412972123. [Google Scholar]

- Sokal, R.R.; Michener, C.D. A statistical method for evaluating systematic relationshps. Univ. Kans. Sci. Bull. 1958, 38, 1409–1438. [Google Scholar]

- Taber, K.S. The Use of Cronbach’s Alpha When Developing and Reporting Research Instruments in Science Education. Res. Sci. Educ. 2018, 48, 1273–1296. [Google Scholar] [CrossRef]

| Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}