Will Green Innovation Bring about the Financial Spillover Effect? Evidence from China’s High-Carbon Listed Companies

Abstract

:1. Introduction

2. Theoretical Basis and Research Hypotheses

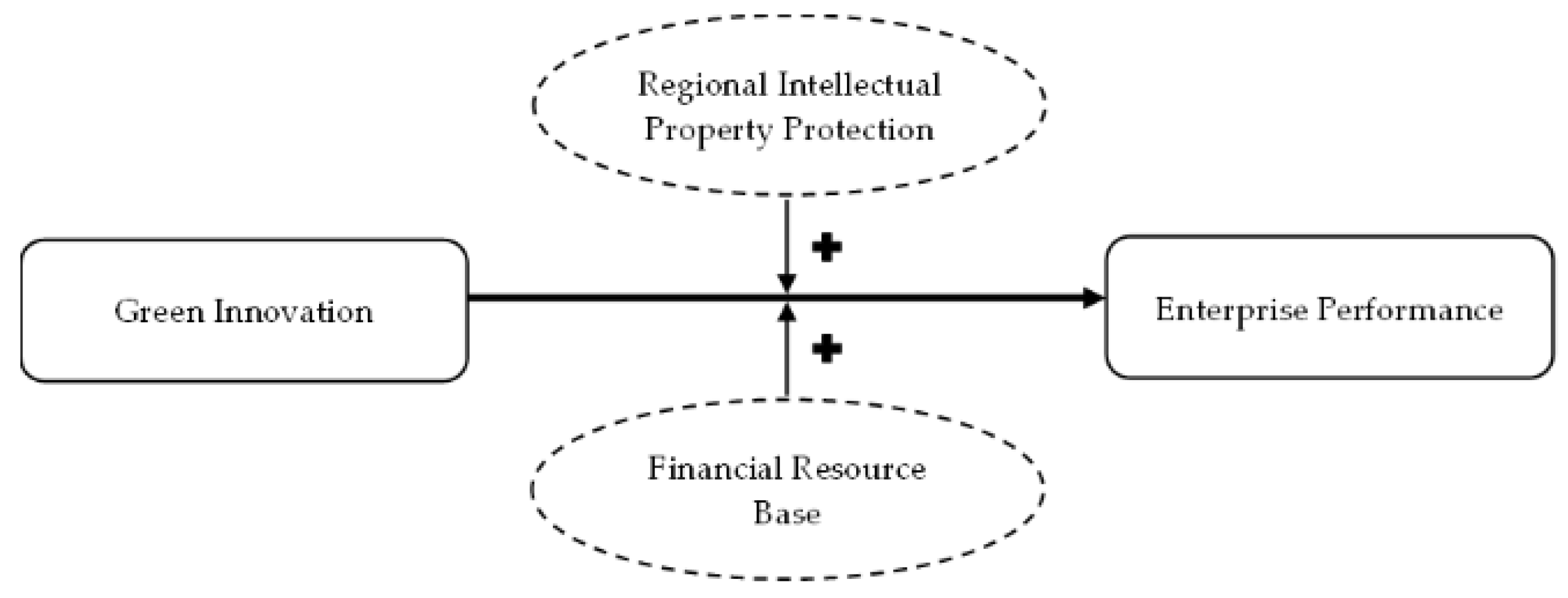

2.1. Green Innovation and Enterprise Performance

2.2. Degree of Intellectual Property Protection, Green Innovation and Enterprise Performance

2.3. Resource Base, Green Innovation and Enterprise Performance

3. Research Design

3.1. Sample Selection and Data Sources

3.2. Definition of Variables

3.2.1. Explained Variable: Enterprise Performance

3.2.2. Explanatory Variable: Green Innovation

3.2.3. Moderating Variables

- Resource base

- 2.

- Regional intellectual property protection degree

3.2.4. Control Variables

3.3. Model Establishment

4. Results

4.1. Descriptive Statistics of Variables

4.2. Hypothesis Testing

4.2.1. Direct Effect Test

4.2.2. Moderating Effect of Regional Intellectual Property Protection on the Relationship between Green Innovation and Enterprise Performance

4.2.3. Moderating Effect of the Resource Base on the Relationship between Green Innovation and Enterprise Performance

4.3. Robustness Test

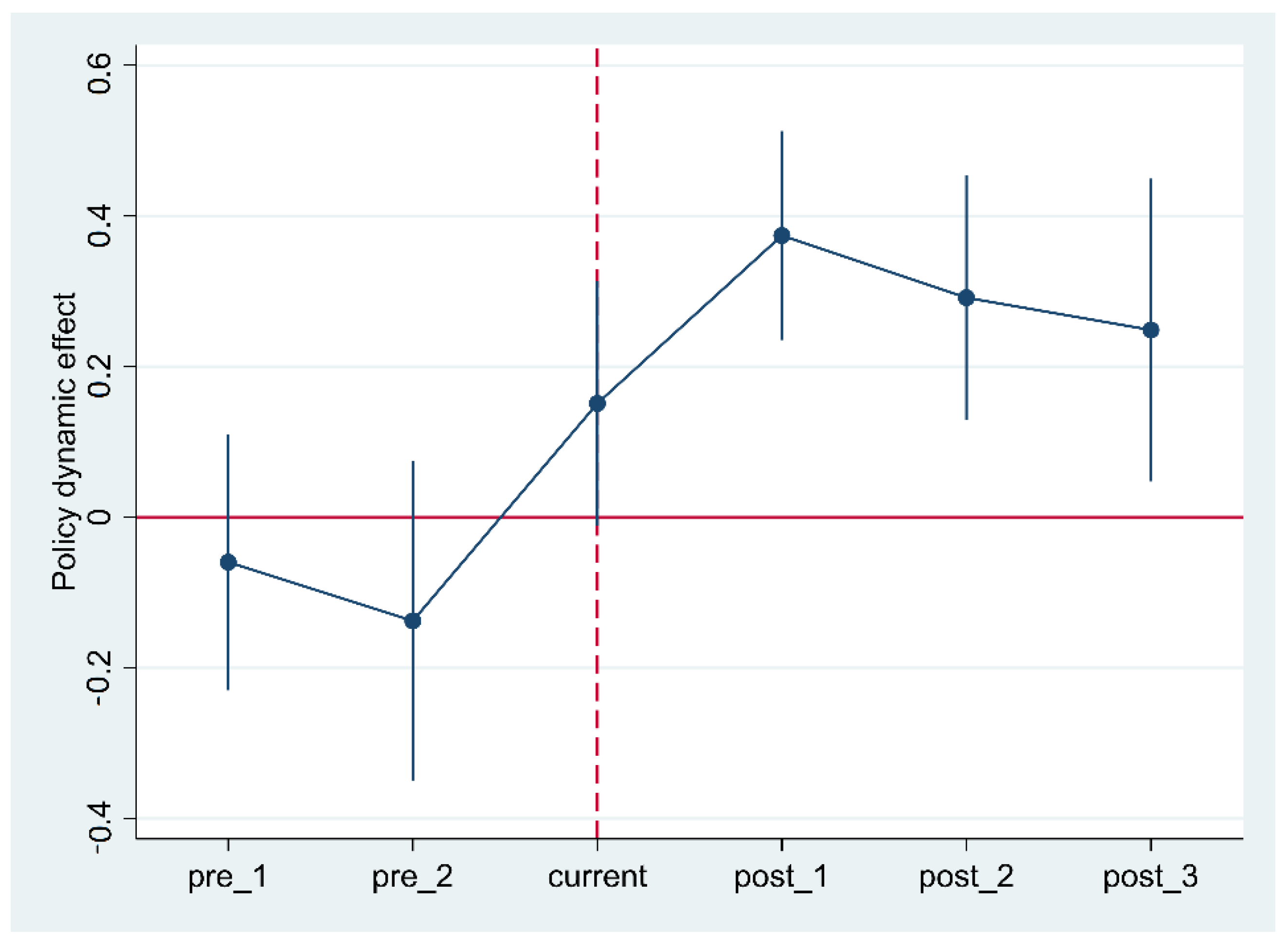

4.3.1. DID Test

4.3.2. PSM Test

4.3.3. Heckman Test

4.3.4. Change the Measurement Method of Variables

4.4. Heterogeneity Test

4.4.1. Examining the Heterogeneity of Patent Types

4.4.2. Examining the Heterogeneity of Enterprise Ownership

4.4.3. Equity Ratios

5. Research Conclusions and Implications

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Xie, X.; Huo, D.; Wang, H. A Research on the Relationship between Green Process Innovation and Financial Performance of the Manufacturing Industry. Sci. Res. Manag. 2019, 40, 63–73. [Google Scholar]

- Li, W.; Zhang, Y.; Zheng, M.; Li, X.; Cui, G.; Li, H. Research on Green Governance of Chinese Listed Companies and Its Evaluation. Manag. World 2019, 35, 126–133+160. [Google Scholar]

- Li, Q.; Xiao, Z. Hetergeneous Environmental Regulation Tools and Green Innovation Incentives: Evidence from Green Patents of Listed Companies. Econ. Res. J. 2020, 55, 199–208. [Google Scholar]

- Huang, M.; Li, M.Y.; Liao, Z.H. Do Political Connected CEOs Promote Chinese Listed Industrial Firms’ Green Innovation? The Mediating Role of External Governance Environments. J. Clean. Prod. 2021, 278, 123634. [Google Scholar] [CrossRef]

- Huang, J.W.; Li, Y.H. Green innovation and Performance: The View of Organization Capability and Social Reciprocity. J. Bus. Ethics 2017, 145, 309–324. [Google Scholar] [CrossRef]

- Hu, J.; Huang, N.; Shen, H. Can Market-Incentive Environmental Regulation Promote Corporate Innovation? A Nature Experiment Based on China’s Carbon Emissions Trading Mechanism. J. Financ. Res. 2020, 1, 171–189. [Google Scholar]

- Xu, J.; Cui, J. Low-Carbon Cities and Firms’ Green Technological Innovation. China Ind. Econ. 2020, 12, 178–196. [Google Scholar]

- Cheng, B.; Xiong, T.; Yin, J. The Stones of those Hills, Serve to Polish Gems: Spillover Effect of Green Tax System on Firm’s Innovation. Can. J. Adm. Sci. 2021, 6, 176–188. [Google Scholar]

- Tao, F.; Zhao, J.; Zhou, H. Does Environmental Regulation Improve the Quality of Green Innovation—Evidence from the Target Responsibility System of Environmental Protection. China Ind. Econ. 2021, 38, 136–154. [Google Scholar]

- Chan, H.K.; Yee, R.W.Y.; Dai, J.; Lim, K.M. The Moderating Effect of Environmental Dynamism on Green Product Innovation and Performance. Int. J. Prod. Econ. 2016, 181, 384–391. [Google Scholar] [CrossRef]

- Delgado-Ceballos, J.; Aragór-Correa, J.A.; Mandojana, N. The Effect of Internal Barriers on the Connection Between Stakeholder Integration and Proactive Environmental Strategies. J. Bus. Ethics 2012, 107, 181–293. [Google Scholar] [CrossRef]

- He, S.; Huang, X.; Chen, Q. Does Manager’s Environmental Cognition Improve Firms Performance? The Mediating Role of Proactive Environmental Strategy and the Moderating Role of Business Environmental Uncertainty. Nankai Bus. Rev. 2016, 19, 49–57. [Google Scholar]

- Lin, Y.H.; Chen, Y.S. Determinants of Green Competitive Advantage: The Roles of Green Knowledge Sharing, Green Dynamic Capabilities and Green Service Innovation. Qual. Quant. 2017, 51, 1663–1685. [Google Scholar] [CrossRef]

- Dangelco, R.M.; Pontrandolfo, P. Being Green and Competitive: The Impact of Environmental Actions and Collaborations on Firm Performance. Bus. Strateg. Environ. 2015, 24, 413–430. [Google Scholar] [CrossRef]

- Hojnik, J.; Ruzzier, M. The Driving Forces of Process Eco-innovation and Its Impact on Performance: Insights from Slovenia. J. Clean. Prod. 2016, 133, 6812–6825. [Google Scholar] [CrossRef]

- Xie, X.; Zhu, Q. How Can Green Innovation Solve the Dilemmas of “Harmonious Coexistence”? J. Manag. World 2021, 37, 128–149. [Google Scholar]

- Zhang, G.; Chen, X.; Xiao, H. Process and Outcome Dimensions of Environmental Governance and Corporate Financial Performance. BMJ 2020, 42, 120–139. [Google Scholar]

- Chen, Y.S. The Driver of Green Innovation and Green Image—Green Core Competence. J. Bus. Ethics 2008, 81, 531–543. [Google Scholar] [CrossRef]

- Xu, Q.; Xu, L.; Xie, Z.; Jin, M. Does Business Group Matter for the Relationship between Green Innovation and Financial Performance? Evidence from Chinese Listed Companies. Sustainability 2021, 13, 13204. [Google Scholar] [CrossRef]

- Xing, X.; Liu, T.; Shen, L.; Wang, J. Linking Environmental Regulation and Financial Performance: The Mediating Role of Green Dynamic Capability and Sustainable Innovation. Sustainability 2020, 12, 1007. [Google Scholar] [CrossRef]

- Hizarci-Payne, A.K.; İpek, I.; Gümüş, G.K. How environmental innovation influences firm performance: A meta-analytic review. Bus. Strategy Environ. 2021, 30, 1174–1190. [Google Scholar] [CrossRef]

- Al-Hakimi, M.A.; Al-Swidi, A.K.; Gelaidan, H.M.; Mohammed, A. The influence of green manufacturing practices on the corporate sustainable performance of SMEs under the effect of green organizational culture: A moderated mediation analysis. J. Clean. Prod. 2022, 376, 134346. [Google Scholar] [CrossRef]

- Xie, X.; Huo, J.; Qi, G.; Zhu, K.X. Green Process Innovation and Performance in Emerging Economies: Moderating Effects of Absorptive Capacity and Green Subsidies. IEEE Trans. Eng. Manag. 2016, 63, 101–112. [Google Scholar] [CrossRef]

- Küçükoğlu, M.T.; Pınar, R.I. Positive Influence of Green Innovation on Company Performance. Procedia Soc. Behav. Sci. 2015, 195, 1232–1237. [Google Scholar] [CrossRef] [Green Version]

- Frempong, M.F.; Mu, Y.; Adu-Yeboah, S.S.; Hossin, M.A.; Adu-Gyamfi, M. Corporate Sustainability and Firm Performance: The Role of Green Innovation Capabilities and Sustainability-Oriented Supplier–Buyer Relationship. Sustainability 2021, 13, 10414. [Google Scholar] [CrossRef]

- Wijethilake, C.; Munir, R.; Appuhami, R. Environmental Innovation Strategy and Organizational Performance: Enabling and Controlling Uses of Management Control Systems. J. Bus. Ethics 2018, 151, 1139–1160. [Google Scholar] [CrossRef]

- Hammar, H.; Löfgren, Å. Explaining Adoption of End of Pipe Solutions and Clean Technologies—Determinants of Firm’s Investments for Reducing Emissions to Air in Four Sectors in Sweden. Energy Policy 2010, 38, 3644–3651. [Google Scholar] [CrossRef]

- Chien, C.C.; Peng, C.W. Does Going Green Pay Off in the Long Run? J. Bus. Res. 2012, 65, 1636–1642. [Google Scholar] [CrossRef]

- Zhang, Q.; Ma, Y. The impact of environmental management on firm economic performance: The mediating effect of green innovation and the moderating effect of environmental leadership. J. Clean. Prod. 2021, 292, 126057. [Google Scholar] [CrossRef]

- Aftab, J.; Abid, N.; Sarwar, M.; Veneziani, M. Environmental ethics, green innovation, and sustainable performance: Exploring the role of environmental leadership and environmental strategy. J. Clean. Prod. 2022, 178, 134639. [Google Scholar] [CrossRef]

- Tang, M.; Walsh, G.; Lerner, G.; Fitza, M.A.; Li, Q. Green Innovation, Managerial Concern and Firm Performance: An Empirical Study. Bus. Strategy Environ. 2018, 27, 39–51. [Google Scholar] [CrossRef]

- Zhao, X.; Ding, X.; Li, L. Research on Environmental Regulation, Technological Innovation and Green Transformation of Manufacturing Industry in the Yangtze River Economic Belt. Sustainability 2021, 13, 10005. [Google Scholar] [CrossRef]

- Li, J.; Yan, D. Exploration on the Mechanism of the Impact of Green Supply Chain Management on Enterprise Sustainable Development Performance. Sustainability 2021, 13, 9906. [Google Scholar] [CrossRef]

- Li, F.; Xu, X.; Li, Z.; Du, P.; Ye, J. Can low-carbon technological innovation truly improve enterprise performance? The case of Chinese manufacturing companies. J. Clean. Prod. 2021, 293, 125949. [Google Scholar] [CrossRef]

- Environmental regulations, innovation and firm performance: A revisit of the Porter hypothesis. J. Clean. Prod. 2017, 155, 79–92. [CrossRef] [Green Version]

- Hermundsdottir, F.; Aspelund, A. Sustainability innovations and firm competitiveness: A review. J. Clean. Prod. 2021, 280, 124175. [Google Scholar] [CrossRef]

- Zhao, X.; Zhao, Y.; Zeng, S.; Zhang, S. Corporate Behavior and Competitiveness: Impact of Environmental Regulation on Chinese Firms. J. Clean. Prod. 2015, 86, 311–322. [Google Scholar] [CrossRef]

- Ma, Y.; Hou, G.; Yin, Q.; Xin, B.; Pan, Y. The Sources of Green Management Innovation: Does Internal Efficiency Demand Pull or External Knowledge Supply Push? J. Clean. Prod. 2018, 202, 582–590. [Google Scholar] [CrossRef]

- Rezende, L.A.; Bansi, A.C.; Alves, M.F.R.; Galina, S.V.R. Take your time: Examining when green innovation affects financial performance in multinationals. J. Clean. Prod. 2019, 233, 993–1003. [Google Scholar] [CrossRef]

- Chen, Y.S.; Lai, S.B.; Wen, C.T. The Influence of Green Innovation Performance on Corporate Advantage in Taiwan. J. Bus. Ethics 2006, 67, 331–339. [Google Scholar] [CrossRef]

- Environmental Compliance and Economic and Environmental Performance: Evidence from Handicrafts Small Businesses in Mexico. J. Bus. Ethics 2015, 126, 381–393. [CrossRef]

- Li, B.; Han, X.; Li, N. Does IPR Strength Affect the OFDI Reverse Innovation Spillover in China? Case Stud. Sport Manag. 2019, 34, 46–60. [Google Scholar]

- Wu, C.; Tang, D. Intellectual Property Rights Enforcement, Corporate Innovation and Operating Performance: Evidence from China’s Listed Companies. Econ. Res. J. 2016, 51, 125–139. [Google Scholar]

- Lee, J.M.; Joo, S.H.; Kim, Y. The complementary effect of intellectual property protection mechanisms on product innovation performance. R D Manag. 2018, 48, 320–330. [Google Scholar] [CrossRef]

- Roh, J.; Lee, K.; Yang, J.Y. How do intellectual property rights and government support drive a firm’s green innovation? The mediating role of open innovation. J. Clean. Prod. 2021, 317, 128422. [Google Scholar] [CrossRef]

- Ang, J.S.; Cheng, Y.; Wu, C. Does Enforcement of Intellectual Property Rights Matter in China? Evidence from Financing and Investment Choices in the High-Tech Industry. Rev. Econ. Stat. 2014, 96, 332–348. [Google Scholar] [CrossRef]

- Wu, W.; Zhang, T. The Asymmetric Influence of Non-R&D Subsidies and R&D Subsidies on Innovation Output of New Ventures. J. Manag. World. 2021, 37, 137–160. [Google Scholar]

- Tian, P.; Liu, B. Impact of financing constraints on firm’s environmental performance: Evidence from China with survey data. J. Clean. Prod. 2019, 217, 432–439. [Google Scholar] [CrossRef]

- Zhu, Y.; Zhang, M. Enterprise Management Team Human Capital, R & D Investment and Enterprise Performance. Can. J. Adm. Sci. 2013, 11, 45–52+96. [Google Scholar]

- Braun, E.; Wield, D. Regulation as a Means for the Social Control of Technology. Technol. Anal. Strateg. 1994, 6, 259–272. [Google Scholar] [CrossRef]

- García-Granero, E.M.; Galdeano-Gómez, E. Eco-innovation Measurement: A Review of Firm Performance Indicators. J. Clean. Prod. 2018, 191, 304–317. [Google Scholar] [CrossRef]

- Dechezleprêtre, A.; Glachant, M.; Haščič, I.; Johnstone, N.; Ménière, Y. Invention and Transfer of Climate Change-Mitigation Technologies: A Global Analysis. Rev. Env. Econ. Policy 2010, 5, 109–130. [Google Scholar] [CrossRef] [Green Version]

- Qi, S.; Lin, S.; Cui, J. Do Environmental Rights Trading Schemes Induce Green Innovation? Evidence from Listed Firms in China. Econ. Res. J. 2018, 53, 129–143. [Google Scholar]

- Liu, S.; Liu, Y. The effect of financing constraints on firm growth—Based on the leading science and technology enterprises. J. Inf. Technol. Educ. 2015, 34, 13–19. [Google Scholar]

- Tian, H.; Hao, W. FDI, Environmental Regulation and Green Innovation Efficiency. Case. Stud. Sport Manag. 2020, 8, 174–183. [Google Scholar]

- Huang, C.; Li, S. Shareholders Link Network, Information Advantage and Firm Performance. Nankai Bus. Rev. 2019, 22, 75–88+127. [Google Scholar]

- Zhang, X.; Xu, J.; Xu, L. Can Elite Governance of Senior Executives Improve Performance? Econ. Res. J. 2015, 50, 100–114. [Google Scholar]

- Gu, L.; Ouyang, W. Corporate Philanthropy, Marketing Capability and Firm Performance. Nankai Bus. Rev. 2017, 20, 94–107. [Google Scholar]

- Liu, X.; Liu, Y. Leverage, Short-term Debt for Long-term Use and Firm Performance. Econ. Res. J. 2019, 54, 127–141. [Google Scholar]

- Qu, L.; Ren, G. The Effect of Executive Political Relations to the Performance of State-Owned Enterprises: And a Simultaneous Discussion on the De-Administration Reform of State-Owned Enterprises. BMJ 2012, 34, 50–59. [Google Scholar]

- Chen, X.; Huang, J. Split Share Structure Reform, Ownership Pyramid and Firm Performance. Can. J. Adm. Sci. 2016, 37, 56–62+96. [Google Scholar]

- Wu, J.; Wang, J.; Liu, J.; Wang, H. Marketization Reform of Loan Interest Rate and Firm Total Factor Productivity—Evidence from Cancellation of Upper and Lower Limits for Loan Interest Rate. Can. J. Adm. Sci. 2021, 42, 145–156. [Google Scholar]

- Liu, H.; Cao, T. The Economic Impacts of Rollover Restrictions on Enterprise. Econ. Res. J. 2018, 53, 108–121. [Google Scholar]

- Kaustia, M.; Rantala, V. “Social Learning and Corporate Peer Effects”. J. Financ. Econ. 2015, 117, 653–669. [Google Scholar] [CrossRef]

- Li, W.; Zheng, M. Is it substantive innovation or strategic innovation?—Impact of macroeconomic policies on micro-enterprise’ innovation. Econ. Res. J. 2016, 51, 60–73. [Google Scholar]

- Tang, Y.; Ma, W.; Xia, L. Quality of Environmental Information Disclosure, Internal Control “Level” and Enterprise Value—Empirical Evidence from Listed Companies in Heavy Polluting Industries. Can. J. Adm. Sci. 2021, 7, 69–84. [Google Scholar]

- Liu, Z.; Li, X.; Peng, X.; Lee, S. Green or nongreen innovation? Different strategic preferences among subsidized enterprises with different ownership types. J. Clean. Prod. 2020, 245, 118786. [Google Scholar] [CrossRef]

- Chen, Y.; Mao, S.; Wang, B. Dividend Stability, Equity Balance and Enterprise Value of Manufacturing Industry. Financ. Account. Manag. 2019, 13, 46–52. [Google Scholar]

- Chen, Z.; Xu, P.; Bai, G. The Relationship between Equity Balance and Performance in Listed Companies from a Perspective of Dynamic Competition. Front. Eng. Manag. 2014, 36, 3–11. [Google Scholar]

- Chen, D.; Chen, Y. Ownership Structure and Corporate Performance: Positive Study on Small and Medium Board Market in 2007~2009. Can. J. Adm. Sci. 2011, 32, 38–43. [Google Scholar]

{kind=link}

{kind=link}

| Variable Type | Variable Symbol | Variable Definition |

|---|---|---|

| Explained variable | TobinQ | The market value of the firm/the replacement cost of the firm’s assets |

| Explanatory variable | lnG | The natural log of the number of green patent applications added by 1 |

| Moderating variables | IPP | Regional technology market turnover/regional GDP |

| IPM | Interest protection multiple | |

| Control variables | Size | The natural log of total assets |

| Lev | Total liabilities/total assets | |

| Age | The natural log of firm age | |

| Growth | (Current period operating income—previous period operating income)/previous period operating income | |

| Ocf | Cash flow from operating activities/total assets | |

| Top1 | The number one shareholder holding ratio | |

| Year | Year dummy variable | |

| Industry | Industry dummy variable | |

| Province | Province dummy variable |

| Variables | Observation | Mean | P10 | Median | P90 | Std. Dev |

|---|---|---|---|---|---|---|

| 1. TobinQ | 12,490 | 1.780 | 0.887 | 1.383 | 3.114 | 1.207 |

| 2. lnG | 12,490 | 0.261 | 0.000 | 0.000 | 1.099 | 0.628 |

| 3. Size | 12,490 | 22.128 | 20.621 | 21.934 | 23.942 | 1.288 |

| 4. Lev | 12,490 | 0.441 | 0.170 | 0.444 | 0.699 | 0.198 |

| 5. Age | 12,490 | 2.646 | 1.946 | 2.773 | 3.178 | 0.497 |

| 6. Growth | 12,490 | 0.182 | −0.147 | 0.123 | 0.516 | 0.369 |

| 7. Ocf | 12,490 | 0.060 | −0.018 | 0.058 | 0.145 | 0.067 |

| 8. Top1 | 12,490 | 37.065 | 17.690 | 35.175 | 60.000 | 15.867 |

| TobinQ | lnG | Size | Lev | Age | Growth | Ocf | Top1 | |

|---|---|---|---|---|---|---|---|---|

| 1. TobinQ | 1 | |||||||

| 2. lnG | −0.084 *** | 1 | ||||||

| 2. Size | −0.299 *** | 0.388 *** | 1 | |||||

| 3. Lev | −0.246 *** | 0.103 *** | 0.364 *** | 1 | ||||

| 4. Age | 0.135 *** | 0.143 *** | 0.286 *** | 0.033 *** | 1 | |||

| 5. Growth | 0.024 *** | −0.019 ** | 0.029 *** | −0.080 *** | 0.005 | 1 | ||

| 6. Ocf | 0.061 *** | 0.073 *** | 0.121 *** | −0.008 | −0.167 *** | 0.070 *** | 1 | |

| 7. Top1 | −0.199 *** | 0.055 *** | 0.200 *** | −0.315 *** | 0.075 *** | 0.047 *** | 0.121 *** | 1 |

| Variables | (1) Lag Phase i | (2) Lag Phase ii | (3) Lag Phase iii |

|---|---|---|---|

| TobinQ | TobinQ | TobinQ | |

| L.lnG | 0.060 *** | ||

| (2.71) | |||

| L2.lnG | 0.044 * | ||

| (1.88) | |||

| L3.lnG | 0.060 ** | ||

| (2.53) | |||

| Size | −0.353 *** | −0.377 *** | −0.369 *** |

| (−12.53) | (−12.92) | (−12.34) | |

| Lev | −0.438 *** | −0.593 *** | −0.666 *** |

| (−2.76) | (−3.57) | (−3.88) | |

| Age | 0.283 *** | 0.237 *** | 0.213 *** |

| (4.41) | (3.16) | (2.60) | |

| Growth | 0.153 *** | 0.187 *** | 0.189 *** |

| (4.46) | (5.03) | (4.92) | |

| Ocf | 2.277 *** | 2.277 *** | 2.119 *** |

| (8.32) | (8.10) | (7.28) | |

| Top1 | −0.003 ** | −0.002 | −0.003 |

| (−2.14) | (−0.94) | (−1.41) | |

| Constant | 8.603 *** | 8.883 *** | 8.674 *** |

| (13.76) | (13.45) | (12.89) | |

| Observations | 11147 | 10103 | 9141 |

| R-squared | 0.358 | 0.382 | 0.387 |

| Year FE | Yes | Yes | Yes |

| Industry FE | Yes | Yes | Yes |

| Province FE | Yes | Yes | Yes |

| Variables | (1) All | (2) High IPP | (3) Low IPP | (4) High IPM | (5) Low IPM |

|---|---|---|---|---|---|

| TobinQ | TobinQ | TobinQ | TobinQ | TobinQ | |

| L.lnG | 0.060 *** | 0.077 ** | 0.014 | 0.091 *** | 0.032 |

| (2.71) | (2.54) | (0.44) | (3.12) | (1.64) | |

| Size | −0.353 *** | −0.367 *** | −0.340 *** | −0.313 *** | −0.382 *** |

| (-12.53) | (−8.97) | (−10.83) | (−10.90) | (−12.99) | |

| Lev | −0.438 *** | −0.217 | −0.559 *** | −0.157 | 0.295 * |

| (−2.76) | (−0.91) | (−3.26) | (−0.78) | (1.72) | |

| Age | 0.283 *** | 0.306 *** | 0.315 *** | 0.117 | 0.261 *** |

| (4.41) | (3.31) | (4.04) | (1.35) | (4.27) | |

| Growth | 0.153 *** | 0.157 *** | 0.073 * | 0.126 *** | 0.069 * |

| (4.46) | (2.92) | (1.90) | (2.60) | (1.77) | |

| Ocf | 2.277 *** | 2.470 *** | 2.125 *** | 2.724 *** | −0.208 |

| (8.32) | (5.80) | (6.44) | (7.45) | (−0.97) | |

| Top1 | −0.003 ** | −0.005 ** | −0.001 | −0.002 | −0.002 * |

| (−2.14) | (−2.25) | (−0.57) | (−1.29) | (−1.68) | |

| Constant | 8.603 *** | 9.060 *** | 8.294 *** | 7.163 *** | 9.511 *** |

| (13.76) | (11.99) | (11.05) | (11.73) | (16.06) | |

| Coefficient difference | 0.06 * | 0.06 * | |||

| Observations | 11147 | 5133 | 5059 | 4555 | 4859 |

| R-squared | 0.358 | 0.362 | 0.416 | 0.338 | 0.434 |

| Year FE | Yes | Yes | Yes | Yes | Yes |

| Industry FE | Yes | Yes | Yes | Yes | Yes |

| Province FE | Yes | Yes | Yes | Yes | Yes |

| Variable | TobinQ |

|---|---|

| Treat×After | 0.314 *** |

| (4.76) | |

| Treat | −0.009 |

| (−0.11) | |

| After | −0.863 *** |

| (−11.98) | |

| Size | −0.431 *** |

| (−11.02) | |

| Lev | −0.166 |

| (−0.70) | |

| Age | 0.398 *** |

| (3.38) | |

| Growth | 0.194 *** |

| (3.19) | |

| Ocf | 2.115 *** |

| (5.23) | |

| Top1 | −0.003 |

| (−1.24) | |

| Constant | 10.895 *** |

| (13.02) | |

| Observations | 4848 |

| R-squared | 0.352 |

| Year FE | Yes |

| Industry FE | Yes |

| Province FE | Yes |

| Variables | (1) PSM | (2) All |

|---|---|---|

| TobinQ | TobinQ | |

| L.lnG | 0.041 * | 0.060 *** |

| (1.89) | (2.71) | |

| Size | −0.257 *** | −0.353 *** |

| (−9.69) | (−12.53) | |

| Lev | −0.705 *** | −0.438 *** |

| (−4.37) | (−2.76) | |

| Age | 0.210 *** | 0.283 *** |

| (2.83) | (4.41) | |

| Growth | 0.175 *** | 0.153 *** |

| (3.70) | (4.46) | |

| Ocf | 2.209 *** | 2.277 *** |

| (7.28) | (8.32) | |

| Top1 | −0.003 * | −0.003 ** |

| (−1.84) | (−2.14) | |

| Constant | 6.636 *** | 8.603 *** |

| (10.61) | (13.76) | |

| Observations | 6747 | 11147 |

| R-squared | 0.340 | 0.358 |

| Year FE | Yes | Yes |

| Industry FE | Yes | Yes |

| Province FE | Yes | Yes |

| Variables | (1) Phase One | (2) Phase Two |

|---|---|---|

| Green_Dummy | TobinQ | |

| IV_industry | 0.723 *** | |

| (5.38) | ||

| SR | 0.281 *** | |

| (4.95) | ||

| RI | 0.025 ** | |

| (2.55) | ||

| lnG | 0.121 *** | |

| (3.39) | ||

| Size | 0.001 | −0.351 *** |

| (0.02) | (−9.71) | |

| Lev | 0.145 | −0.271 |

| (0.84) | (−1.39) | |

| Age | −0.091 | 0.367 *** |

| (−1.07) | (4.17) | |

| Growth | −0.045 | 2.742 *** |

| (−0.94) | (7.26) | |

| Ocf | 0.769 ** | 0.222 *** |

| (2.18) | (4.45) | |

| Top1 | −0.003 | −0.005 ** |

| (−1.59) | (−2.38) | |

| imr | −0.076 ** | |

| (−2.27) | ||

| Constant | −6.862 *** | 8.455 *** |

| (−10.69) | (9.72) | |

| Observations | 7188 | 7188 |

| R-squared | 0.104 | 0.304 |

| Year FE | No | Yes |

| Industry FE | No | Yes |

| Province FE | No | Yes |

| Variables | (1) | (2) | (3) |

|---|---|---|---|

| TobinQ | TobinQ | TobinQ | |

| L.lnGrant | 0.064 *** | ||

| (2.77) | |||

| L.lnPatent | 0.042 ** | ||

| (2.56) | |||

| L.Green | 0.072 * | ||

| (1.94) | |||

| Size | −0.351 *** | −0.365 *** | −0.349 *** |

| (−12.28) | (-13.16) | (−12.50) | |

| Lev | −0.439 *** | −0.424 *** | −0.441 *** |

| (−2.76) | (−2.67) | (−2.77) | |

| Age | 0.283 *** | 0.289 *** | 0.282 *** |

| (4.41) | (4.53) | (4.39) | |

| Growth | 0.152 *** | 0.153 *** | 0.151 *** |

| (4.45) | (4.48) | (4.41) | |

| Ocf | 2.280 *** | 2.286 *** | 2.278 *** |

| (8.33) | (8.35) | (8.33) | |

| Top1 | −0.003 ** | −0.003 ** | −0.003 ** |

| (−2.14) | (−2.13) | (−2.16) | |

| Constant | 8.577 *** | 8.780 *** | 8.527 *** |

| (13.54) | (14.07) | (13.76) | |

| Observations | 11,147 | 11,147 | 11,147 |

| R-squared | 0.358 | 0.359 | 0.358 |

| Year FE | Yes | Yes | Yes |

| Industry FE | Yes | Yes | Yes |

| Province FE | Yes | Yes | Yes |

| Variables | (1) | (2) | (3) |

|---|---|---|---|

| TobinQ | TobinQ | TobinQ | |

| L.lnG | 0.060 *** | ||

| (2.71) | |||

| L.lnGI | 0.083 *** | ||

| (2.66) | |||

| L.lnGU | 0.039 | ||

| (1.46) | |||

| Size | −0.353 *** | −0.353 *** | −0.347 *** |

| (−12.53) | (−12.66) | (−11.93) | |

| Lev | −0.438 *** | −0.435 *** | −0.439 *** |

| (−2.76) | (−2.75) | (-2.76) | |

| Age | 0.283 *** | 0.281 *** | 0.282 *** |

| (4.41) | (4.39) | (4.38) | |

| Growth | 0.152 *** | 0.152 *** | 0.150 *** |

| (4.46) | (4.46) | (4.40) | |

| Ocf | 2.276 *** | 2.279 *** | 2.286 *** |

| (8.32) | (8.33) | (8.34) | |

| Top1 | −0.003 ** | −0.003 ** | −0.003 ** |

| (−2.14) | (−2.14) | (−2.17) | |

| Constant | 8.603 *** | 8.603 *** | 8.482 *** |

| (13.76) | (13.87) | (13.20) | |

| Observations | 11,147 | 11,147 | 11,147 |

| R-squared | 0.358 | 0.358 | 0.357 |

| Year FE | Yes | Yes | Yes |

| Industry FE | Yes | Yes | Yes |

| Province FE | Yes | Yes | Yes |

| Variables | (1) State | (2) NonState | (3) State | (4) NonState | (5) State | (6) NonState |

|---|---|---|---|---|---|---|

| TobinQ | TobinQ | TobinQ | TobinQ | TobinQ | TobinQ | |

| L.lnG | 0.007 | 0.125 ** | ||||

| (0.34) | (2.39) | |||||

| L.lnGI | 0.005 | 0.214 *** | ||||

| (0.16) | (2.65) | |||||

| L.lnGU | 0.021 | 0.022 | ||||

| (0.89) | (0.40) | |||||

| Size | −0.311 *** | −0.418 *** | −0.310 *** | −0.420 *** | −0.312 *** | −0.406 *** |

| (−10.86) | (-8.04) | (−10.80) | (−8.23) | (−10.98) | (−7.42) | |

| Lev | −0.640 *** | −0.104 | −0.639 *** | −0.100 | −0.640 *** | −0.109 |

| (−3.72) | (−0.39) | (-3.70) | (−0.38) | (−3.72) | (−0.41) | |

| Age | 0.131 | 0.400 *** | 0.130 | 0.395 *** | 0.132 | 0.398 *** |

| (1.34) | (4.01) | (1.33) | (4.00) | (1.34) | (3.99) | |

| Growth | 0.146 *** | 0.166 *** | 0.146 *** | 0.164 *** | 0.147 *** | 0.165 *** |

| (3.49) | (3.17) | (3.49) | (3.15) | (3.49) | (3.14) | |

| Ocf | 1.616 *** | 3.088 *** | 1.618 *** | 3.087 *** | 1.613 *** | 3.098 *** |

| (5.60) | (7.10) | (5.62) | (7.11) | (5.59) | (7.10) | |

| Top1 | −0.001 | −0.005 * | −0.001 | −0.004 * | −0.001 | −0.005 * |

| (−0.61) | (−1.73) | (−0.62) | (−1.71) | (−0.61) | (−1.75) | |

| Constant | 8.042 *** | 9.417 *** | 8.030 *** | 9.462 *** | 8.065 *** | 9.157 *** |

| (11.90) | (8.96) | (11.86) | (9.17) | (12.00) | (8.21) | |

| Coefficient difference | −0.118 *** | −0.209 *** | −0.001 | |||

| Observations | 5236 | 5062 | 5236 | 5062 | 5236 | 5062 |

| R-squared | 0.440 | 0.335 | 0.440 | 0.336 | 0.440 | 0.333 |

| Year FE | Yes | Yes | Yes | Yes | Yes | Yes |

| Industry FE | Yes | Yes | Yes | Yes | Yes | Yes |

| Province FE | Yes | Yes | Yes | Yes | Yes | Yes |

| Variables | (1) All | (2) Low Equity Balance | (3) High Equity Balance |

|---|---|---|---|

| TobinQ | TobinQ | TobinQ | |

| L.lnG | 0.060 *** | 0.002 | 0.124 *** |

| (2.71) | (0.09) | (3.37) | |

| Size | −0.353 *** | −0.361 *** | −0.336 *** |

| (−12.53) | (−9.95) | (−8.66) | |

| Lev | −0.438 *** | −0.140 | −0.655 *** |

| (−2.76) | (−0.77) | (−2.77) | |

| Age | 0.283 *** | 0.134 * | 0.435 *** |

| (4.41) | (1.75) | (4.55) | |

| Growth | 0.153 *** | 0.162 *** | 0.143 *** |

| (4.46) | (3.16) | (2.99) | |

| Ocf | 2.277 *** | 2.251 *** | 2.337 *** |

| (8.32) | (6.94) | (6.12) | |

| Top1 | −0.003 ** | −0.002 | −0.009 *** |

| (−2.14) | (−1.04) | (−2.86) | |

| Constant | 8.603 *** | 9.181 *** | 7.937 *** |

| (13.76) | (13.31) | (9.77) | |

| Coefficient difference | 0.122 *** | ||

| Observations | 11,147 | 5658 | 5489 |

| R-squared | 0.358 | 0.401 | 0.354 |

| Year FE | Yes | Yes | Yes |

| Industry FE | Yes | Yes | Yes |

| Province FE | Yes | Yes | Yes |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Zhang, M.; Su, Y.; Zhu, P. Will Green Innovation Bring about the Financial Spillover Effect? Evidence from China’s High-Carbon Listed Companies. Sustainability 2023, 15, 89. https://doi.org/10.3390/su15010089

Zhang M, Su Y, Zhu P. Will Green Innovation Bring about the Financial Spillover Effect? Evidence from China’s High-Carbon Listed Companies. Sustainability. 2023; 15(1):89. https://doi.org/10.3390/su15010089

Chicago/Turabian StyleZhang, Min, Yu Su, and Peng Zhu. 2023. "Will Green Innovation Bring about the Financial Spillover Effect? Evidence from China’s High-Carbon Listed Companies" Sustainability 15, no. 1: 89. https://doi.org/10.3390/su15010089