Does Industrial Policy Reduce Corporate Investment Efficiency? Evidence from China

Abstract

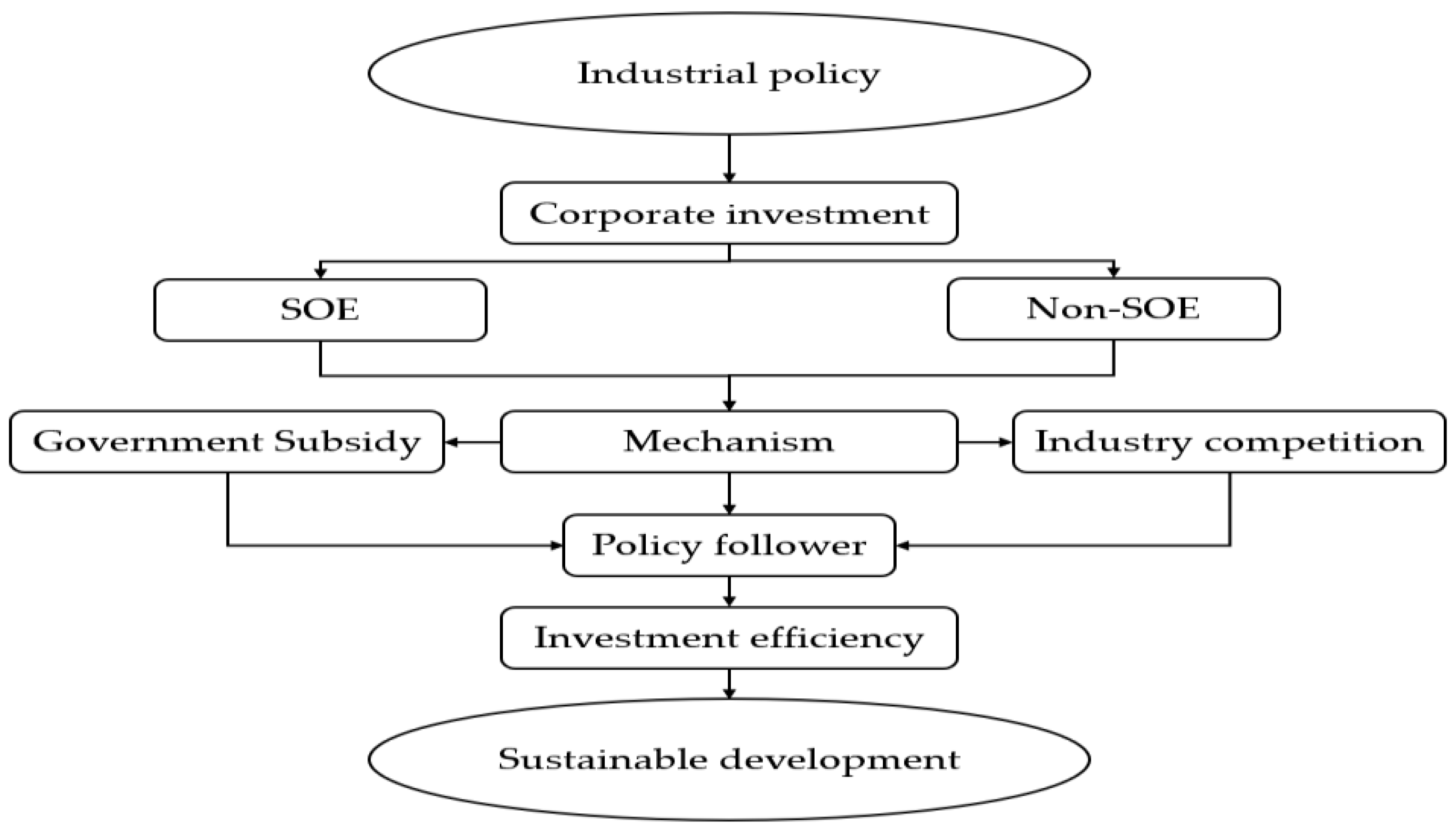

:1. Introduction

2. Literature Review and Hypothesis Development

3. Data and Variable Definitions

3.1. Data

3.2. Variable Definitions

3.2.1. Dependent Variables

3.2.2. Independent Variables

3.2.3. Control Variables

3.3. Summary Statistics

4. Empirical Results

4.1. Industrial Policy and Corporate Investment

4.2. Industrial Policy and Corporate Investment Efficiency

4.3. The Influence Mechanism of Industrial Policy on Investment Efficiency

4.3.1. Government Subsidy

4.3.2. Inter-Industry Competition

4.4. Policy Followers and Corporate Investment Efficiency

5. Robustness Checks

5.1. 2SLS for the Endogenous Problem

5.2. Change the Definition of Investment Efficiency

5.3. Change the Definition of Policy Followers

6. Discussion

7. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Nomenclature

| SOEs | State-owned enterprises |

| Non-SOEs | Non-state-owned enterprises |

| Five-Year Plan | The Five-Year Plan for National Economic and Social Development |

| National industrial policy | The Five-Year Plan for National Economic and Social Development, published by Chinese central government departments |

| Local industrial policy | The Five-Year Plan for National Economic and Social Development, published by Chinese provincial government departments |

| Policy followers | Firms in target industries that increase investment after the implement of supporting industrial policies |

| CSRC | China Securities Regulatory Commission |

| CSMAR | China Stock Market and Accounting Research |

Appendix A

{kind=link}

| Dependent Variable: Invest | Independent Variable: IPN | Independent Variable: IPL | ||||

|---|---|---|---|---|---|---|

| Total (1) | SOE (2) | Non-SOE (3) | Total (4) | SOE (5) | Non-SOE (6) | |

| IP | 0.0064 *** | 0.0024 | 0.0101 *** | 0.0017 | −0.0009 | 0.0043 ** |

| (0.0000) | (0.1902) | (0.0000) | (0.1682) | (0.6328) | (0.0109) | |

| Dummy2015 | −0.0242 *** | −0.0288 *** | −0.0207 *** | −0.0258 *** | −0.0292 *** | −0.0233 *** |

| (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | |

| Size | 0.0025 *** | 0.0006 | 0.0041 *** | 0.0024 *** | 0.0006 | 0.0039 *** |

| (0.0000) | (0.4778) | (0.0000) | (0.0001) | (0.4971) | (0.0000) | |

| Growth | 0.0071 *** | 0.0064 *** | 0.0071 *** | 0.0071 *** | 0.0064 *** | 0.0072 *** |

| (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | |

| Leverage | −0.0167 *** | −0.0035 | −0.0254 *** | −0.0171 *** | −0.0035 | −0.0258 *** |

| (0.0000) | (0.4806) | (0.0000) | (0.0000) | (0.4768) | (0.0000) | |

| CF | 0.0716 *** | 0.0952 *** | 0.0511 *** | 0.0715 *** | 0.0956 *** | 0.0502 *** |

| (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | |

| Return | 0.0056 *** | 0.0049 *** | 0.0060 *** | 0.0056 *** | 0.0049 *** | 0.0060 *** |

| (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | |

| SOE | −0.0077 *** | −0.0075 *** | ||||

| (0.0000) | (0.0000) | |||||

| Constant | 0.0614 *** | 0.0586 *** | 0.0560 *** | 0.0652 *** | 0.0605 *** | 0.0614 *** |

| (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | |

| Industry FE | Yes | Yes | Yes | Yes | Yes | Yes |

| Year FE | Yes | Yes | Yes | Yes | Yes | Yes |

| Observations | 30,795 | 14,369 | 16,426 | 30,795 | 14,369 | 16,426 |

| AdjustR2 | 0.1250 | 0.1742 | 0.1034 | 0.1239 | 0.1741 | 0.1013 |

| Dependent Variable: Inefficiency | Independent Variable: IPN | Independent Variable: IPL | ||||

|---|---|---|---|---|---|---|

| Total (1) | SOE (2) | Non-SOE (3) | Total (4) | SOE (5) | Non-SOE (6) | |

| IP | 0.0033 *** | 0.0002 | 0.0061 *** | 0.0009 | 0.0001 | 0.0017 ** |

| (0.0000) | (0.8626) | (0.0000) | (0.1208) | (0.9122) | (0.0370) | |

| Dummy2015 | −0.0062 *** | −0.0091 *** | −0.0040 *** | −0.0070 *** | −0.0092 *** | −0.0055 *** |

| (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | |

| Size | −0.0032 *** | −0.0034 *** | −0.0028 *** | −0.0032 *** | −0.0034 *** | −0.0030 *** |

| (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | |

| Growth | 0.0035 *** | 0.0025 *** | 0.0038 *** | 0.0035 *** | 0.0025 *** | 0.0039 *** |

| (0.0000) | (0.0003) | (0.0000) | (0.0000) | (0.0003) | (0.0000) | |

| Leverage | −0.0053 *** | −0.0035 | −0.0061 *** | −0.0055 *** | −0.0035 | −0.0064 *** |

| (0.0008) | (0.1291) | (0.0055) | (0.0006) | (0.1276) | (0.0038) | |

| CF | 0.0251 *** | 0.0327 *** | 0.0195 *** | 0.0250 *** | 0.0327 *** | 0.0190 *** |

| (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | |

| Return | 0.0034 *** | 0.0026 *** | 0.0041 *** | 0.0034 *** | 0.0026 *** | 0.0041 *** |

| (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | |

| SOE | −0.0035 *** | −0.0034 *** | ||||

| (0.0000) | (0.0000) | |||||

| Constant | 0.0456 *** | 0.0460 *** | 0.0413 *** | 0.0475 *** | 0.0460 *** | 0.0449 *** |

| (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | |

| Industry FE | Yes | Yes | Yes | Yes | Yes | Yes |

| Year FE | Yes | Yes | Yes | Yes | Yes | Yes |

| Observations | 30,779 | 14,365 | 16,414 | 30,779 | 14,365 | 16,414 |

| Adjust R2 | 0.0867 | 0.1191 | 0.0675 | 0.0858 | 0.1191 | 0.0645 |

Appendix B

| Dependent Variable: OverInvest | Independent Variable: FollowerN | Independent Variable: FollowerL | ||||

|---|---|---|---|---|---|---|

| Total (1) | SOE (2) | Non-SOE (3) | Total (4) | SOE (5) | Non-SOE (6) | |

| Follower | 0.5087 *** | 0.4916 *** | 0.5244 *** | 0.4909 *** | 0.4702 *** | 0.5085 *** |

| (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | |

| Size | 0.0385 *** | 0.0254 *** | 0.0515 *** | 0.0432 *** | 0.0247 *** | 0.0615 *** |

| (0.0000) | (0.0005) | (0.0000) | (0.0000) | (0.0049) | (0.0000) | |

| Growth | 0.0227 *** | 0.0283 *** | 0.0163 * | 0.0412 *** | 0.0417 *** | 0.0357 *** |

| (0.0008) | (0.0055) | (0.0756) | (0.0000) | (0.0025) | (0.0007) | |

| Leverage | 0.0977 *** | 0.1847 *** | 0.0497 | 0.0430 | 0.1071 ** | 0.0269 |

| (0.0002) | (0.0000) | (0.1550) | (0.1421) | (0.0242) | (0.4729) | |

| CF | 0.1569 *** | 0.2558 *** | 0.0475 | 0.0754 | 0.1853 ** | −0.0333 |

| (0.0008) | (0.0006) | (0.4269) | (0.1319) | (0.0269) | (0.5893) | |

| Return | −0.0510 *** | −0.0563 *** | −0.0447 *** | −0.0390 *** | −0.0461 *** | −0.0362 *** |

| (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0006) | (0.0002) | |

| SOE | −0.0316 *** | −0.0440 *** | ||||

| (0.0054) | (0.0008) | |||||

| Constant | −0.0139 | −0.0474 * | −0.0263 | −0.0010 | −0.0102 | −0.0479 * |

| (0.4309) | (0.0906) | (0.2187) | (0.9621) | (0.7697) | (0.0563) | |

| Industry FE | Yes | Yes | Yes | Yes | Yes | Yes |

| Year FE | Yes | Yes | Yes | Yes | Yes | Yes |

| Observations | 16,408 | 7939 | 8469 | 13,474 | 5860 | 7614 |

| Adjust R2 | 0.2830 | 0.2706 | 0.3100 | 0.2663 | 0.2485 | 0.2927 |

References

- Lv, P.; Spigarelli, F. The Determinants of Location Choice: Chinese Foreign Direct Investments in the European Renewable Energy Sector. Int. J. Emerg. Mark. 2016, 11, 333–356. [Google Scholar] [CrossRef]

- Firth, M.; Gong, S.X.; Shan, L. Cost of Government and Firm Value. J. Corp. Financ. 2013, 21, 136–152. [Google Scholar] [CrossRef]

- Kline, P.; Moretti, E. Local Economic Development, Agglomeration Economies, and the Big Push: 100 Years of Evidence from the Tennessee Valley Authority. Q. J. Econ. 2014, 129, 275–331. [Google Scholar] [CrossRef] [Green Version]

- Chen, D.; Li, O.Z.; Xin, F. Five-Year Plans, China Finance and Their Consequences. China J. Account. Res. 2017, 10, 189–230. [Google Scholar] [CrossRef]

- Kollmann, R.; Roeger, W.; Veld, J.I. Fiscal Policy in a Financial Crisis: Standard Policy versus Bank Rescue Measures. Am. Econ. Rev. 2012, 102, 77–81. [Google Scholar] [CrossRef] [Green Version]

- Wallsten, S.J. The Effects of Government-Industry R&D Programs on Private R&D: The Case of the Small Business Innovation Research Program. RAND J. Econ. 2000, 31, 82. [Google Scholar] [CrossRef]

- Xu, R.; Shen, Y.; Liu, M.; Li, L.; Xia, X.; Luo, K. Can Government Subsidies Improve Innovation Performance? Evidence from Chinese Listed Companies. Econ. Model. 2022, 120, 106151. [Google Scholar] [CrossRef]

- Nolan, P. Globalisation and Industrial Policy: The Case of China. World Econ. 2014, 37, 747–764. [Google Scholar] [CrossRef]

- Hsieh, C.-T.; Klenow, P.J. Misallocation and Manufacturing TFP in China and India. Q. J. Econ. 2009, 124, 1403–1448. [Google Scholar] [CrossRef] [Green Version]

- Du, L.; Harrison, A.; Jefferson, G. FDI Spillovers and Industrial Policy: The Role of Tariffs and Tax Holidays. World Dev. 2014, 64, 366–383. [Google Scholar] [CrossRef]

- Chen, Y.-R.; Jiang, X.; Weng, C.-H. Can Government Industrial Policy Enhance Corporate Bidding? The Evidence of China. Pac.-Basin Financ. J. 2020, 60, 101288. [Google Scholar] [CrossRef]

- Hu, J.; Jiang, H.; Holmes, M. Government Subsidies and Corporate Investment Efficiency: Evidence from China. Emerg. Mark. Rev. 2019, 41, 100658. [Google Scholar] [CrossRef]

- Firth, M.; Malatesta, P.H.; Xin, Q.; Xu, L. Corporate Investment, Government Control, and Financing Channels: Evidence from China’s Listed Companies. J. Corp. Financ. 2012, 18, 433–450. [Google Scholar] [CrossRef]

- Claessens, S.; Feijen, E.; Laeven, L. Political Connections and Preferential Access to Finance: The Role of Campaign Contributions. J. Financ. Econ. 2008, 88, 554–580. [Google Scholar] [CrossRef] [Green Version]

- Cull, R.; Xu, L.C. Who Gets Credit? The Behavior of Bureaucrats and State Banks in Allocating Credit to Chinese State-Owned Enterprises. J. Dev. Econ. 2003, 71, 533–559. [Google Scholar] [CrossRef]

- Fama, E.F.; French, K.R. The Corporate Cost of Capital and the Return on Corporate Investment. J. Financ. 1999, 54, 1939–1967. [Google Scholar] [CrossRef]

- Duchin, R.; Ozbas, O.; Sensoy, B.A. Costly External Finance, Corporate Investment, and the Subprime Mortgage Credit Crisis. J. Financ. Econ. 2010, 97, 418–435. [Google Scholar] [CrossRef]

- Morellec, E.; Schürhoff, N. Corporate Investment and Financing under Asymmetric Information. J. Financ. Econ. 2011, 99, 262–288. [Google Scholar] [CrossRef]

- Babenko, I.; Lemmon, M.; Tserlukevich, Y. Employee Stock Options and Investment. J. Financ. 2011, 66, 981–1009. [Google Scholar] [CrossRef]

- Ozdagli, A.K. Financial Leverage, Corporate Investment, and Stock Returns. Rev. Financ. Stud. 2012, 25, 1033–1069. [Google Scholar] [CrossRef]

- Almeida, H.; Campello, M. Financial Constraints, Asset Tangibility, and Corporate Investment. Rev. Financ. Stud. 2007, 20, 1429–1460. [Google Scholar] [CrossRef] [Green Version]

- Malmendier, U.; Tate, G. CEO Overconfidence and Corporate Investment. J. Financ. 2005, 60, 2661–2700. [Google Scholar] [CrossRef] [Green Version]

- Butler, A.W.; Cornaggia, J.; Grullon, G.; Weston, J.P. Corporate Financing Decisions, Managerial Market Timing, and Real Investment. J. Financ. Econ. 2011, 101, 666–683. [Google Scholar] [CrossRef]

- Gulen, H.; Ion, M. Policy Uncertainty and Corporate Investment. Rev. Financ. Stud. 2015, 29, 523–564. [Google Scholar] [CrossRef] [Green Version]

- Alok, S.; Ayyagari, M. Politics, State Ownership, and Corporate Investments. Rev. Financ. Stud. 2020, 33, 3031–3087. [Google Scholar] [CrossRef]

- Biddle, G.C.; Hilary, G.; Verdi, R.S. How Does Financial Reporting Quality Relate to Investment Efficiency? J. Account. Econ. 2009, 48, 112–131. [Google Scholar] [CrossRef]

- Biddle, G.C.; Callahan, C.M.; Hong, H.A.; Knowles, R.L. Do Adoptions of International Financial Reporting Standards Enhance Capital Investment Efficiency? SSRN J. 2013, volume, page. [Google Scholar] [CrossRef]

- Gompers, P.; Ishii, J.; Metrick, A. Corporate Governance and Equity Prices. Q. J. Econ. 2003, 118, 107–156. [Google Scholar] [CrossRef] [Green Version]

- Li, K.-F.; Liao, Y.-P. Directors’ and Officers’ Liability Insurance and Investment Efficiency: Evidence from Taiwan. Pac.-Basin Financ. J. 2014, 29, 18–34. [Google Scholar] [CrossRef]

- Zhang, H.; Li, L.; Zhou, D.; Zhou, P. Political Connections, Government Subsidies and Firm Financial Performance: Evidence from Renewable Energy Manufacturing in China. Renew. Energy 2014, 63, 330–336. [Google Scholar] [CrossRef]

- Brandt, L.; Li, H. Bank Discrimination in Transition Economies: Ideology, Information, or Incentives? J. Comp. Econ. 2003, 31, 387–413. [Google Scholar] [CrossRef] [Green Version]

- Chen, C.J.P.; Li, Z.; Su, X.; Sun, Z. Rent-Seeking Incentives, Corporate Political Connections, and the Control Structure of Private Firms: Chinese Evidence. J. Corp. Financ. 2011, 17, 229–243. [Google Scholar] [CrossRef]

- Lin, J.Y.; Cai, F.; Zhou, L. Competition, Policy Burdens, and State-Owned Enterprise Reform. Am. Econ. Rev. 1998, 88, 422–427. [Google Scholar]

- Fazzari, S.M.; Hubbard, R.G.; Petersen, B.C.; Blinder, A.S.; Poterba, J.M. Financing Constraints and Corporate Investment. Brook. Pap. Econ. Act. 1988, 1988, 141. [Google Scholar] [CrossRef] [Green Version]

- Chen, S.; Sun, Z.; Tang, S.; Wu, D. Government Intervention and Investment Efficiency: Evidence from China. J. Corp. Financ. 2011, 17, 259–271. [Google Scholar] [CrossRef]

- Aghion, P.; Cai, J.; Dewatripont, M.; Du, L.; Harrison, A.; Legros, P. Industrial Policy and Competition. Am. Econ. J. Macroecon. 2015, 7, 1–32. [Google Scholar] [CrossRef] [Green Version]

- Liao, G.; Chen, X.; Jing, X.; Sun, J. Policy Burdens, Firm Performance, and Management Turnover. China Econ. Rev. 2009, 20, 15–28. [Google Scholar] [CrossRef]

- Chen, Q.; Goldstein, I.; Jiang, W. Price Informativeness and Investment Sensitivity to Stock Price. Rev. Financ. Stud. 2007, 20, 619–650. [Google Scholar] [CrossRef]

- Huang, Z.; Li, L.; Ma, G.; Qian, J. The Reversal of Privatization in China: A Political Economy Perspective. J. Corp. Financ. 2021, 71, 102115. [Google Scholar] [CrossRef]

- Wang, Y.; Wei, Y.; Song, F.M. Uncertainty and Corporate R&D Investment: Evidence from Chinese Listed Firms. Int. Rev. Econ. Financ. 2017, 47, 176–200. [Google Scholar] [CrossRef]

- Datta, S.; Iskandar-Datta, M.; Singh, V. Product Market Power, Industry Structure, and Corporate Earnings Management. J. Bank. Financ. 2013, 37, 3273–3285. [Google Scholar] [CrossRef]

- Piotroski, J.D.; Zhang, T. Politicians and the IPO Decision: The Impact of Impending Political Promotions on IPO Activity in China. J. Financ. Econ. 2014, 111, 111–136. [Google Scholar] [CrossRef]

- Brollo, F.; Nannicini, T.; Perotti, R.; Tabellini, G. The Political Resource Curse. Am. Econ. Rev. 2013, 103, 1759–1796. [Google Scholar] [CrossRef] [Green Version]

- Ding, Y.; Chen, G. How Do Innovation-Driven Policies Help Sports Firms Sustain Growth? The Mediating Role of R&D Investment. Sustainability 2022, 14, 15688. [Google Scholar] [CrossRef]

- Beaudry, C. Entry, Growth and Patenting in Industrial Clusters: A Study of the Aerospace Industry in the UK. Int. J. Econ. Bus. 2001, 8, 405–436. [Google Scholar] [CrossRef] [Green Version]

- Ozoguz, A.; Rebello, M.J.; Wardlaw, M. Information, Competition, and Investment Sensitivity to Peer Stock Prices. SSRN J. 2018, volume, page. [Google Scholar] [CrossRef]

- Castaño-Martínez, M.-S. Product Innovation and R&D Policy: The Case of the Transformation Industries in Developed and Developing. Int. Entrep. Manag. J. 2012, 8, 421–436. [Google Scholar] [CrossRef]

- Komlenovic, S.; Mamun, A.; Mishra, D. Business Cycle and Aggregate Industry Mergers. J. Econ. Finan. 2011, 35, 239–259. [Google Scholar] [CrossRef]

- China Securities Regulatory Commission. Guidelines on Industry Classification of Listed Companies; China Securities Regulatory Commission: Beijing, China, 2001.

- Richardson, S. Over-Investment of Free Cash Flow. Rev. Acc. Stud. 2006, 11, 159–189. [Google Scholar] [CrossRef]

- Wang, Y.; Chen, C.R.; Huang, Y.S. Economic Policy Uncertainty and Corporate Investment: Evidence from China. Pac.-Basin Financ. J. 2014, 26, 227–243. [Google Scholar] [CrossRef]

- Foucault, T.; Frésard, L. Cross-Listing, Investment Sensitivity to Stock Price, and the Learning Hypothesis. Rev. Financ. Stud. 2012, 25, 3305–3350. [Google Scholar] [CrossRef]

- Dougal, C.; Parsons, C.A.; Titman, S. Urban Vibrancy and Corporate Growth: Urban Vibrancy and Corporate Growth. J. Financ. 2015, 70, 163–210. [Google Scholar] [CrossRef]

- MacKay, P.; Phillips, G.M. How Does Industry Affect Firm Financial Structure? Rev. Financ. Stud. 2005, 18, 1433–1466. [Google Scholar] [CrossRef] [Green Version]

- Petersen, M.A. Estimating Standard Errors in Finance Panel Data Sets: Comparing Approaches. Rev. Financ. Stud. 2009, 22, 435–480. [Google Scholar] [CrossRef] [Green Version]

- Zhang, X.; Xu, L. Firm Life Cycle and Debt Maturity Structure: Evidence from China. Acc. Financ. 2021, 61, 937–976. [Google Scholar] [CrossRef]

- Heckman, J.J. Sample Selection Bias as a Specification Error. Econometrica 1979, 47, 153. [Google Scholar] [CrossRef]

- Baker, M.; Stein, J.C.; Wurgler, J. When Does the Market Matter? Stock Prices and the Investment of Equity-Dependent Firms. Q. J. Econ. 2003, 118, 969–1005. [Google Scholar] [CrossRef] [Green Version]

- Zhang, C.; Yang, C.; Liu, C. Economic Policy Uncertainty and Corporate Risk-Taking: Loss Aversion or Opportunity Expectations. Pac.-Basin Financ. J. 2021, 69, 101640. [Google Scholar] [CrossRef]

- Deng, Y.; Morck, R.; Wu, J.; Yeung, B. Monetary and Fiscal Stimuli, Ownership Structure, and China’s Housing Market; National Bureau of Economic Research: Cambridge, MA, USA, 2011; p. w16871. [Google Scholar] [CrossRef]

| Variable | Definition |

|---|---|

| Invest | The capital expenditures divided by total assets at the beginning period |

| Inefficiency | The absolute residual of Equation (1) |

| IP | If the firm belongs to the target national industrial policy, then IPN equals 1; otherwise, IPN equals 0 If the firm is targeted by local industrial policy, then IPL equals 1; otherwise, IPL equals 0 |

| Subsidy | The log of government subsidy |

| HHI | The HHI index of the industry |

| Follower | If the investment of the firm of target national industrial policy in year t is higher than in year t − 1, then FollowerN equals 1; otherwise, FollowerN equals 0. If the investment of the firm of target local industrial policy in year t is higher than in year t − 1, then FollowerL equals 1; otherwise, FollowerL equals 0 |

| Size | The log of total assets |

| Growth | The operating income growth rate |

| Leverage | The ratio of liabilities to assets |

| CF | The operating cash flow |

| Return | The stock return |

| SOE | The ownership status of firm (SOE) equals 1 if firm is state-owned (including central-controlled, local-controlled, city governments and state-owned assets management company); otherwise, SOE equals 0 |

| Panel A. Descriptive statistics | |||||||||

| Mean | St. Dev | Min | Median | Max | Obs. | ||||

| Invest | 0.0631 | 0.0696 | 0.0002 | 0.0405 | 0.4071 | 33,680 | |||

| Inefficiency | 0.0325 | 0.0371 | 0.0003 | 0.0215 | 0.2202 | 30,915 | |||

| IPN | 0.5439 | 0.4981 | 0.0000 | 1.0000 | 1.0000 | 33,790 | |||

| IPL | 0.4305 | 0.4952 | 0.0000 | 0.0000 | 1.0000 | 33,790 | |||

| FollowerN | 0.4320 | 0.4954 | 0.0000 | 0.0000 | 1.0000 | 16,418 | |||

| FollowerL | 0.4325 | 0.4954 | 0.0000 | 0.0000 | 1.0000 | 13,479 | |||

| Subsidy | 0.1090 | 0.5322 | −2.1179 | 0.0435 | 3.1590 | 25,203 | |||

| HHI | 0.1530 | 0.1479 | 0.0202 | 0.1088 | 1.0000 | 33,678 | |||

| Size | 3.5994 | 1.3186 | 0.8554 | 3.4356 | 8.0197 | 33,707 | |||

| Growth | 0.1834 | 0.4868 | −0.6412 | 0.1075 | 3.7009 | 33,706 | |||

| Leverage | 0.4618 | 0.2049 | 0.0530 | 0.4651 | 0.9459 | 33,707 | |||

| CF | 0.0798 | 0.1031 | −0.2427 | 0.0697 | 0.5264 | 33,703 | |||

| Return | 0.1914 | 0.7030 | −0.7216 | −0.0112 | 3.4350 | 33,702 | |||

| SOE | 0.4576 | 0.4982 | 0.0000 | 0.0000 | 1.0000 | 33,788 | |||

| Panel B. The comparison between SOEs and non-SOEs | |||||||||

| Mean of SOE | Mean of non−SOE | Difference | T value | ||||||

| Invest | 0.0473 | 0.0518 | −0.0045 *** | −5.2472 | |||||

| Inefficiency | 0.0350 | 0.0363 | −0.0013 *** | −2.6741 | |||||

| IPN | 0.5514 | 0.5154 | 0.0359 *** | 6.3251 | |||||

| IPL | 0.4077 | 0.4648 | −0.0571 *** | −10.1185 | |||||

| Panel C. Correlation matrix | |||||||||

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) | |

| Invest | 1 | ||||||||

| Inefficiency | 0.2791 *** | 1 | |||||||

| IPC | 0.0437 *** | 0.0294 *** | 1 | ||||||

| IPL | −0.0056 | −0.0105 * | 0.2383 *** | 1 | |||||

| Size | 0.0317 *** | −0.0925 *** | −0.0958 *** | 0.0272 *** | 1 | ||||

| Growth | 0.1054 *** | 0.0877 *** | 0.0292 *** | −0.0194 *** | 0.0097 * | 1 | |||

| Leverage | −0.0274 *** | −0.0503 *** | −0.0572 *** | −0.0713 *** | 0.3461 *** | 0.0409 *** | 1 | ||

| CF | 0.0702 *** | 0.0391 *** | −0.0676 *** | 0.0886 *** | 0.1024 *** | 0.0110 * | −0.2116 *** | 1 | |

| Return | 0.0411 *** | 0.0222 *** | 0.0237 *** | −0.0147 *** | −0.0609 *** | 0.1012 *** | −0.0025 | −0.0305 *** | 1 |

| Dependent Variable: Invest | Independent Variable: IPN | Independent Variable: IPL | ||||

|---|---|---|---|---|---|---|

| Total (1) | SOE (2) | Non-SOE (3) | Total (4) | SOE (5) | Non-SOE (6) | |

| IP | 0.0048 *** | 0.0005 | 0.0088 *** | 0.0024 * | 0.0006 | 0.0041 ** |

| (0.0006) | (0.7793) | (0.0000) | (0.0554) | (0.7571) | (0.0145) | |

| Size | 0.0038 *** | 0.0027 *** | 0.0047 *** | 0.0038 *** | 0.0027 *** | 0.0047 *** |

| (0.0000) | (0.0034) | (0.0000) | (0.0000) | (0.0033) | (0.0000) | |

| Growth | 0.0055 *** | 0.0048 *** | 0.0054 *** | 0.0055 *** | 0.0048 *** | 0.0055 *** |

| (0.0000) | (0.0001) | (0.0000) | (0.0000) | (0.0001) | (0.0000) | |

| Leverage | −0.0179 *** | −0.0042 | −0.0221 *** | −0.0182 *** | −0.0042 | −0.0228 *** |

| (0.0000) | (0.3981) | (0.0000) | (0.0000) | (0.3930) | (0.0000) | |

| CF | 0.0775 *** | 0.0972 *** | 0.0612 *** | 0.0780 *** | 0.0973 *** | 0.0616 *** |

| (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | |

| Return | 0.0102 *** | 0.0080 *** | 0.0117 *** | 0.0102 *** | 0.0080 *** | 0.0117 *** |

| (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | |

| SOE | −0.0089 *** | −0.0089 *** | ||||

| (0.0000) | (0.0000) | |||||

| Constant | 0.0477 *** | 0.0413 *** | 0.0420 *** | 0.0492 *** | 0.0414 *** | 0.0449 *** |

| (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | |

| Industry FE | Yes | Yes | Yes | Yes | Yes | Yes |

| Year FE | Yes | Yes | Yes | Yes | Yes | Yes |

| Observations | 30,795 | 14,369 | 16,426 | 30,795 | 14,369 | 16,426 |

| Adjust R2 | 0.1342 | 0.1869 | 0.1154 | 0.1337 | 0.1869 | 0.1140 |

| Dependent Variable: Inefficiency | Independent Variable: IPN | Independent Variable: IPL | ||||

|---|---|---|---|---|---|---|

| Total (1) | SOE (2) | Non-SOE (3) | Total (4) | SOE (5) | Non-SOE (6) | |

| IP | 0.0027 *** | −0.0006 | 0.0058 *** | 0.0013 ** | 0.0008 | 0.0018 ** |

| (0.0001) | (0.5165) | (0.0000) | (0.0257) | (0.3488) | (0.0348) | |

| Size | −0.0024 *** | −0.0023 *** | −0.0023 *** | −0.0024 *** | −0.0023 *** | −0.0023 *** |

| (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | |

| Growth | 0.0026 *** | 0.0018 ** | 0.0029 *** | 0.0026 *** | 0.0018 ** | 0.0029 *** |

| (0.0000) | (0.0119) | (0.0000) | (0.0000) | (0.0117) | (0.0000) | |

| Leverage | −0.0068 *** | −0.0039 * | −0.0066 *** | −0.0070 *** | −0.0039 * | −0.0070 *** |

| (0.0000) | (0.0918) | (0.0054) | (0.0000) | (0.0882) | (0.0032) | |

| CF | 0.0239 *** | 0.0303 *** | 0.0198 *** | 0.0242 *** | 0.0300 *** | 0.0202 *** |

| (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | |

| Return | 0.0063 *** | 0.0047 *** | 0.0075 *** | 0.0063 *** | 0.0047 *** | 0.0075 *** |

| (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | |

| SOE | −0.0043 *** | −0.0043 *** | ||||

| (0.0000) | (0.0000) | |||||

| Constant | 0.0411 *** | 0.0389 *** | 0.0376 *** | 0.0420 *** | 0.0382 *** | 0.0399 *** |

| (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | |

| Industry FE | Yes | Yes | Yes | Yes | Yes | Yes |

| Year FE | Yes | Yes | Yes | Yes | Yes | Yes |

| Observations | 30,779 | 14,365 | 16,414 | 30,779 | 14,365 | 16,414 |

| Adjust R2 | 0.0952 | 0.1314 | 0.0750 | 0.0947 | 0.1314 | 0.0726 |

| Dependent Variable: Inefficiency | Independent Variable: IPN | Independent Variable: IPL |

|---|---|---|

| (1) | (2) | |

| IP | 0.0011 * | 0.0009 * |

| (0.0953) | (0.0881) | |

| IP*Subsidy | 0.0029 ** | 0.0018 * |

| (0.0313) | (0.0717) | |

| Subsidy | −0.0013 | −0.0006 |

| (0.1832) | (0.3853) | |

| Size | −0.0017 *** | −0.0017 *** |

| (0.0000) | (0.0000) | |

| Growth | 0.0026 *** | 0.0026 *** |

| (0.0000) | (0.0000) | |

| Leverage | −0.0092 *** | −0.0094 *** |

| (0.0000) | (0.0000) | |

| CF | 0.0241 *** | 0.0243 *** |

| (0.0000) | (0.0000) | |

| Return | 0.0064 *** | 0.0064 *** |

| (0.0000) | (0.0000) | |

| Constant | 0.0372 *** | 0.0375 *** |

| (0.0000) | (0.0000) | |

| Industry FE | Yes | Yes |

| Year FE | Yes | Yes |

| Observations | 20,590 | 20,590 |

| Adjust R2 | 0.1145 | 0.1142 |

| Dependent Variable: Inefficiency | Independent Variable: IPN | Independent Variable: IPL |

|---|---|---|

| (1) | (2) | |

| IP | 0.0020 *** | 0.0005 * |

| (0.0034) | (0.0802) | |

| IP*HHI | −0.0086 *** | −0.0071 *** |

| (0.0006) | (0.0083) | |

| HHI | −0.0025 | −0.0005 |

| (0.1912) | (0.7564) | |

| Size | −0.0016 *** | −0.0016 *** |

| (0.0000) | (0.0000) | |

| Growth | 0.0020 *** | 0.0020 *** |

| (0.0001) | (0.0001) | |

| Leverage | −0.0127 *** | −0.0124 *** |

| (0.0000) | (0.0000) | |

| CF | 0.0268 *** | 0.0269 *** |

| (0.0000) | (0.0000) | |

| Return | 0.0055 *** | 0.0055 *** |

| (0.0000) | (0.0000) | |

| Constant | −0.0016 *** | −0.0016 *** |

| (0.0000) | (0.0000) | |

| Industry FE | Yes | Yes |

| Year FE | Yes | Yes |

| Observations | 24,042 | 24,042 |

| Adjust R2 | 0.0676 | 0.0671 |

| Dependent Variable: Inefficiency | Independent Variable: FollowerN | Independent Variable: FollowerL | ||||

|---|---|---|---|---|---|---|

| Total (1) | SOE (2) | Non-SOE (3) | Total (4) | SOE (5) | Non-SOE (6) | |

| Follower | 0.0086 *** | 0.0073 *** | 0.0098 *** | 0.0084 *** | 0.0070 *** | 0.0095 *** |

| (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | |

| Size | −0.0015 *** | −0.0011 * | −0.0016 *** | −0.0012 *** | −0.0012 ** | −0.0013 ** |

| (0.0004) | (0.0540) | (0.0085) | (0.0049) | (0.0470) | (0.0387) | |

| Growth | 0.0031 *** | 0.0030 *** | 0.0028 *** | 0.0034 *** | 0.0023 ** | 0.0038 *** |

| (0.0000) | (0.0010) | (0.0013) | (0.0000) | (0.0201) | (0.0001) | |

| Leverage | −0.0119 *** | −0.0057 * | −0.0141 *** | −0.0080 *** | −0.0046 | −0.0079 ** |

| (0.0000) | (0.0702) | (0.0000) | (0.0002) | (0.1381) | (0.0129) | |

| CF | 0.0189 *** | 0.0272 *** | 0.0126 ** | 0.0195 *** | 0.0306 *** | 0.0111 ** |

| (0.0000) | (0.0000) | (0.0150) | (0.0000) | (0.0000) | (0.0321) | |

| Return | 0.0048 *** | 0.0033 *** | 0.0063 *** | 0.0056 *** | 0.0033 *** | 0.0071 *** |

| (0.0000) | (0.0004) | (0.0000) | (0.0000) | (0.0016) | (0.0000) | |

| SOE | −0.0060 *** | −0.0044 *** | ||||

| (0.0000) | (0.0000) | |||||

| Constant | 0.0390 *** | 0.0321 *** | 0.0371 *** | 0.0329 *** | 0.0295 *** | 0.0312 *** |

| (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | |

| Industry FE | Yes | Yes | Yes | Yes | Yes | Yes |

| Year FE | Yes | Yes | Yes | Yes | Yes | Yes |

| Observations | 16,408 | 7939 | 8469 | 13,474 | 5860 | 7614 |

| Adjust R2 | 0.1357 | 0.1614 | 0.1207 | 0.1422 | 0.1762 | 0.1276 |

| Dependent Variable: Invest | Dependent Variable: Inefficiency | |||||

|---|---|---|---|---|---|---|

| Total (1) | SOE (2) | Non-SOE (3) | Total (4) | SOE (5) | Non-SOE (6) | |

| Fitted_IPN | 0.0041 *** | 0.0002 | 0.0078 *** | 0.0022 *** | −0.0007 | 0.0047 *** |

| (0.0023) | (0.9147) | (0.0001) | (0.0013) | (0.4092) | (0.0000) | |

| Size | 0.0045 *** | 0.0031 *** | 0.0056 *** | −0.0016 *** | −0.0017 *** | −0.0014 *** |

| (0.0000) | (0.0006) | (0.0000) | (0.0000) | (0.0000) | (0.0016) | |

| Growth | 0.0054 *** | 0.0050 *** | 0.0053 *** | 0.0026 *** | 0.0019 *** | 0.0027 *** |

| (0.0000) | (0.0001) | (0.0000) | (0.0000) | (0.0049) | (0.0000) | |

| Leverage | −0.0223 *** | −0.0073 | −0.0280 *** | −0.0100 *** | −0.0061 *** | −0.0108 *** |

| (0.0000) | (0.1400) | (0.0000) | (0.0000) | (0.0064) | (0.0000) | |

| CF | 0.0786 *** | 0.0981 *** | 0.0624 *** | 0.0230 *** | 0.0306 *** | 0.0177 *** |

| (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | |

| Return | 0.0101 *** | 0.0079 *** | 0.0117 *** | 0.0061 *** | 0.0045 *** | 0.0073 *** |

| (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | |

| SOE | −0.0079 *** | −0.0038 *** | ||||

| (0.0000) | (0.0000) | |||||

| Lambda | 0.0026 *** | 0.0008 | 0.0043 *** | −0.0000 | −0.0012 * | 0.0011 * |

| (0.0018) | (0.5206) | (0.0003) | (0.9598) | (0.0541) | (0.0939) | |

| Constant | 0.0452 *** | 0.0401 *** | 0.0392 *** | 0.0385 *** | 0.0369 *** | 0.0348 *** |

| (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | |

| Industry FE | Yes | Yes | Yes | Yes | Yes | Yes |

| Year FE | Yes | Yes | Yes | Yes | Yes | Yes |

| Observations | 30,790 | 14,367 | 16,423 | 30,776 | 14,363 | 16,413 |

| Adjust R2 | 0.1511 | 0.1984 | 0.1370 | 0.1143 | 0.1453 | 0.0984 |

| Dependent Variable: Invest | Dependent Variable: Inefficiency | |||||

|---|---|---|---|---|---|---|

| Total (1) | SOE (2) | Non-SOE (3) | Total (4) | SOE (5) | Non-SOE (6) | |

| Fitted_IPL | 0.0027 ** | 0.0008 | 0.0043 ** | 0.0014 ** | 0.0010 | 0.0017 ** |

| (0.0313) | (0.6445) | (0.0106) | (0.0129) | (0.2336) | (0.0320) | |

| Size | 0.0045 *** | 0.0032 *** | 0.0057 *** | −0.0016 *** | −0.0017 *** | −0.0013 *** |

| (0.0000) | (0.0006) | (0.0000) | (0.0000) | (0.0001) | (0.0017) | |

| Growth | 0.0054 *** | 0.0050 *** | 0.0054 *** | 0.0026 *** | 0.0019 *** | 0.0027 *** |

| (0.0000) | (0.0001) | (0.0000) | (0.0000) | (0.0048) | (0.0000) | |

| Leverage | −0.0226 *** | −0.0074 | −0.0287 *** | −0.0101 *** | −0.0061 *** | −0.0112 *** |

| (0.0000) | (0.1375) | (0.0000) | (0.0000) | (0.0060) | (0.0000) | |

| CF | 0.0790 *** | 0.0981 *** | 0.0626 *** | 0.0233 *** | 0.0304 *** | 0.0180 *** |

| (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | |

| Return | 0.0101 *** | 0.0079 *** | 0.0117 *** | 0.0061 *** | 0.0045 *** | 0.0073 *** |

| (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | |

| SOE | −0.0078 *** | −0.0038 *** | ||||

| (0.0000) | (0.0000) | |||||

| Lambda | 0.0026 *** | 0.0008 | 0.0042 *** | −0.0000 | −0.0011 * | 0.0011 |

| (0.0020) | (0.5081) | (0.0003) | (0.9199) | (0.0568) | (0.1046) | |

| Constant | 0.0463 *** | 0.0399 *** | 0.0415 *** | 0.0391 *** | 0.0361 *** | 0.0366 *** |

| (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | |

| Industry FE | Yes | Yes | Yes | Yes | Yes | Yes |

| Year FE | Yes | Yes | Yes | Yes | Yes | Yes |

| Observations | 30,790 | 14,367 | 16,423 | 30,776 | 14,363 | 16,413 |

| Adjust R2 | 0.1509 | 0.1984 | 0.1361 | 0.1141 | 0.1454 | 0.0967 |

| Dependent Variable: Invest | Independent Variable: IPN | Independent Variable: IPL | ||||

|---|---|---|---|---|---|---|

| Total (1) | SOE (2) | Non-SOE (3) | Total (4) | SOE (5) | Non-SOE (6) | |

| IP | 0.0075 *** | 0.0062 | 0.0106 *** | 0.0029 ** | 0.0036 | 0.0046 * |

| (0.0002) | (0.1350) | (0.0001) | (0.0485) | (0.2186) | (0.0806) | |

| IP*TQ | −0.0007 * | −0.0018 | −0.0006 ** | −0.0001 * | −0.0013 | −0.0002 ** |

| (0.0837) | (0.1811) | (0.0490) | (0.0902) | (0.3071) | (0.0147) | |

| TQ | −0.0010 ** | −0.0009 * | −0.0008 * | −0.0013 ** | −0.0011 ** | −0.0009 * |

| (0.0253) | (0.0599) | (0.0527) | (0.0493) | (0.0470) | (0.0945) | |

| Size | 0.0047 *** | 0.0040 *** | 0.0056 *** | 0.0048 *** | 0.0041 *** | 0.0055 *** |

| (0.0000) | (0.0001) | (0.0000) | (0.0000) | (0.0001) | (0.0000) | |

| Leverage | −0.0042 | 0.0161 *** | −0.0120 ** | −0.0048 | 0.0157 *** | −0.0127 *** |

| (0.2224) | (0.0019) | (0.0110) | (0.1709) | (0.0024) | (0.0071) | |

| MTB | −0.0332 *** | −0.0399 *** | −0.0299 *** | −0.0332 *** | −0.0399 *** | −0.0297 *** |

| (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | |

| Tangibility | 0.0559 *** | 0.0444 *** | 0.0608 *** | 0.0555 *** | 0.0441 *** | 0.0605 *** |

| (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | |

| ROA | 0.1573 *** | 0.1976 *** | 0.1323 *** | 0.1566 *** | 0.1964 *** | 0.1327 *** |

| (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | |

| SOE | −0.0097 *** | −0.0096 *** | ||||

| (0.0000) | (0.0000) | |||||

| Constant | 0.0514 *** | 0.0454 *** | 0.0449 *** | 0.0542 *** | 0.0471 *** | 0.0485 *** |

| (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | |

| Industry FE | Yes | Yes | Yes | Yes | Yes | Yes |

| Year FE | Yes | Yes | Yes | Yes | Yes | Yes |

| Observations | 30,615 | 14,314 | 16,301 | 30,615 | 14,314 | 16,301 |

| Adjust R2 | 0.1480 | 0.2004 | 0.1286 | 0.1471 | 0.2001 | 0.1269 |

| Dependent Variable: Inefficiency | Independent Variable: Follower_RN | Independent Variable: Follower_RL | ||||

|---|---|---|---|---|---|---|

| Total (1) | SOE (2) | Non-SOE (3) | Total (4) | SOE (5) | Non-SOE (6) | |

| Follower_R | 0.0118 *** | 0.0112 *** | 0.0120 *** | 0.0117 *** | 0.0108 *** | 0.0123 *** |

| (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | |

| Size | −0.0014 *** | −0.0011 ** | −0.0014 ** | −0.0010 ** | −0.0009 | −0.0012 * |

| (0.0010) | (0.0436) | (0.0287) | (0.0200) | (0.1354) | (0.0549) | |

| Growth | 0.0020 *** | 0.0021 ** | 0.0015 | 0.0022 *** | 0.0007 | 0.0027 ** |

| (0.0032) | (0.0361) | (0.1018) | (0.0022) | (0.3968) | (0.0106) | |

| Leverage | −0.0071 *** | −0.0032 | −0.0078 ** | −0.0051 ** | −0.0043 | −0.0032 |

| (0.0015) | (0.3116) | (0.0262) | (0.0170) | (0.1455) | (0.3192) | |

| CF | 0.0187 *** | 0.0247 *** | 0.0127 ** | 0.0180 *** | 0.0277 *** | 0.0105 ** |

| (0.0000) | (0.0000) | (0.0158) | (0.0000) | (0.0000) | (0.0449) | |

| Return | 0.0045 *** | 0.0031 *** | 0.0061 *** | 0.0052 *** | 0.0027 ** | 0.0067 *** |

| (0.0000) | (0.0012) | (0.0000) | (0.0000) | (0.0136) | (0.0000) | |

| SOE | −0.0054 *** | −0.0044 *** | ||||

| (0.0000) | (0.0000) | |||||

| Constant | 0.0339 *** | 0.0288 *** | 0.0313 *** | 0.0289 *** | 0.0264 *** | 0.0268 *** |

| (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | |

| Industry FE | Yes | Yes | Yes | Yes | Yes | Yes |

| Year FE | Yes | Yes | Yes | Yes | Yes | Yes |

| Observations | 14,540 | 7213 | 7327 | 12,400 | 5529 | 6871 |

| Adjust R2 | 0.1487 | 0.1756 | 0.1303 | 0.1520 | 0.1902 | 0.1336 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Wang, T.; Wang, R.; Zhang, H. Does Industrial Policy Reduce Corporate Investment Efficiency? Evidence from China. Sustainability 2023, 15, 732. https://doi.org/10.3390/su15010732

Wang T, Wang R, Zhang H. Does Industrial Policy Reduce Corporate Investment Efficiency? Evidence from China. Sustainability. 2023; 15(1):732. https://doi.org/10.3390/su15010732

Chicago/Turabian StyleWang, Ting, Rujun Wang, and Hua Zhang. 2023. "Does Industrial Policy Reduce Corporate Investment Efficiency? Evidence from China" Sustainability 15, no. 1: 732. https://doi.org/10.3390/su15010732