Research on the Impact of Economic Policy Uncertainty on Enterprises’ Green Innovation—Based on the Perspective of Corporate Investment and Financing Decisions

,

,  ,

,  and

and

Abstract

:1. Introduction

2. Literature Review

2.1. The Theoretical Basis of the Uncertainty of Economic Policy Affecting the Green Innovation of Enterprises

2.1.1. Real Options Theory

2.1.2. Growth Option Theory

2.1.3. Risk Compensation Theory

2.2. The Impact of Economic Policy Uncertainty on Corporate Green Innovation

2.3. Literature Summary

2.3.1. Inconsistent Research Conclusions

2.3.2. Few Studies on The Influencing Mechanism

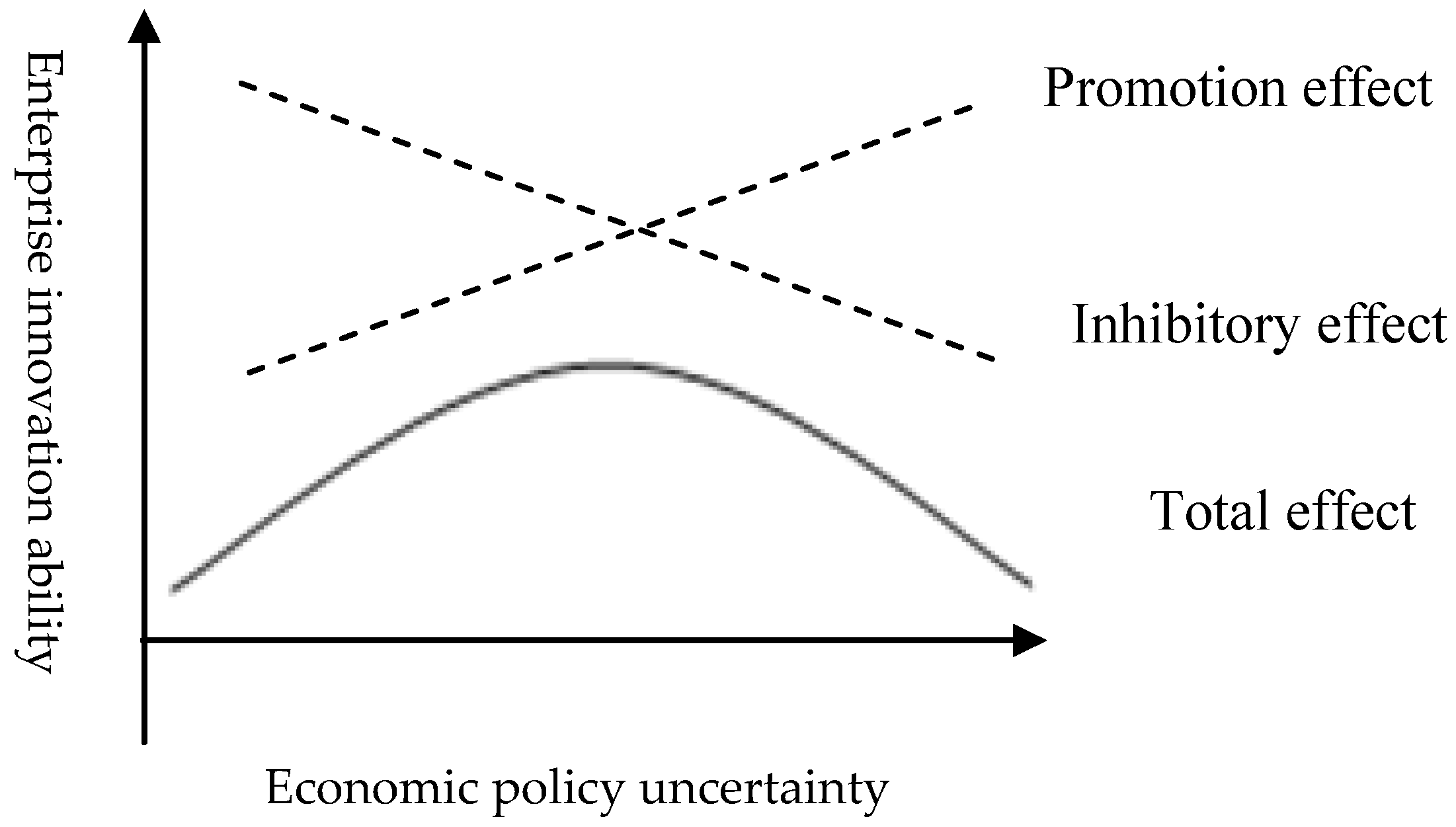

3. The Impact of Economic Policy Uncertainty on Corporate Green Innovation

4. Research Design on the Impact of Economic Policy Uncertainty on Corporate Green Innovation

4.1. Sample Selection and Data Sources

4.2. Variable Selection

4.2.1. Explained Variables

4.2.2. Explanatory Variables

- 1.

- Measure Economic Policy Uncertainty by News Media and Network Information.

- 2.

- Measure Economic Policy Uncertainty by the Exchange of Local Officials

- 1.

- Degree Centrality Index

- 2.

- Betweenness Centrality Index

- 3.

- Closeness Centrality Index

- 4.

- Eigenvector Centrality Index

4.2.3. Control Variables

4.3. Model Design

5. Empirical Test and Result Analysis

5.1. Descriptive Statistical Analysis of Variables

5.2. Analysis of Regression Results

5.3. Robustness Test

5.3.1. Re-Calculation of Economic Policy Uncertainty Index

5.3.2. Re-Measurement of Enterprise Innovation Capability Index

6. The Moderating Mechanism Analysis of the Relationship between Economic Policy Uncertainty and Enterprise Green Innovation

6.1. Theoretical Analysis of the Moderating Mechanism Affecting the Relationship between Economic Policy Uncertainty and Enterprise of Green Innovation

6.1.1. Impact of Financing Constraints

6.1.2. The Impact of Corporate Investment Behavior Choices

6.2. Empirical Test Model Setting

6.2.1. Regulating Variable Definition

6.2.2. Model Construction

6.3. Analysis of Empirical Test Results

7. Conclusions and Recommendations

7.1. Suggestions for the Government to Formulate Economic Policies

7.2. Suggestions for Improving the Green Innovation Capacity of Enterprises

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Variable Types | The Variable Name | Symbol | Variable Calculation Method |

|---|---|---|---|

| Explained variable | Green innovation | GI | Ln(1 + number of green patent applications) |

| Explanatory variables | Economic policy uncertainty index | EPU1 | Baker economic policy uncertainty index |

| EPU2 | Local officials communication index based on complex network | ||

| Moderating variables | Financing constraints | SA | SA = 0.737 ∗ Size − 0.04Age + 0.043 ∗ Size2 |

| Financialization | FIN | Financial assets/total assets | |

| Control variables | The enterprise scale | Size | The natural log of total assets at year end |

| Return on equity | ROE | Net profit/total assets | |

| Asset–liability ratio | LEV | Total liabilities/total assets | |

| Tangible asset ratio | Tang | Tangible assets/total assets | |

| Cash flow ratio | Cash | (Cash flow from operating activities + cash flow from investing activities)/total assets | |

| Ownership concentration | OC | Shareholding ratio of the largest shareholder |

References

- Baker, S.; Bloom, N.; Davis, S.J. Measuring Economic Policy Uncertainty. Q. J. Econ. 2016, 131, 1593–1636. [Google Scholar] [CrossRef]

- Pastor, L.; Veronesi, P. Uncertainty about Government Policy and Stock Prices. J. Financ. 2012, 67, 1219–1264. [Google Scholar] [CrossRef]

- Chen, D.Q.; Chen, Y.S.; Dong, Z.Y. Policy uncertainty, tax collection and administration intensity and corporate tax evasion. Manag. World. 2016, 5, 151–163. [Google Scholar]

- Bhattacharya, U.; Hsu, P.H.; Tian, X. What Affects Innovation More: Policy or Policy Uncertainty? Elec. J. 2000, 1, 130–145. [Google Scholar]

- Atanassov, J.; Julio, B.; Leng, T. The Bright Side of Political Uncertainty: The Case of R&D. Prod. Oper. Manag. 2015, 9, 1517–1542. [Google Scholar]

- Meng, Q.B.; Shi, Q. The impact of macroeconomic policy uncertainty on R&D: Theory and experience. World Econ. 2017, 40, 75–98. [Google Scholar]

- Gu, X.M.; Chen, Y.M.; Pan, S.Y. Economic policy uncertainty and innovation: An empirical analysis of Listed companies in China. Econ. Res. J. 2018, 53, 109–123. [Google Scholar]

- Gulen, H.; Ion, M. Policy Uncertainty and Corporate Investmen. Rev. Financ. Stud. 2016, 3, 523–564. [Google Scholar]

- Bernanke, B.S. Irreversibility, Uncertainty, and Cyclical Investment. Q. J. Econ. 1983, 98, 85–106. [Google Scholar] [CrossRef]

- Brennan, M.J.; Schwartz, E.S. Evaluating Natural Resource Investments. J. Bus. 1985, 58, 135–157. [Google Scholar] [CrossRef] [Green Version]

- McDonald, R.; Siegel, D. The Value of Waiting to Invest. Q. J. Econ. 1986, 101, 707–727. [Google Scholar] [CrossRef]

- Bloom, N. The Impact of Uncertainty Shocks. Econometrica 2009, 77, 623–685. [Google Scholar]

- Jurado, K.; Ludvigson, S.C.; Ng, S. Measuring Uncertainty. Am. Econ. Rev. 2015, 105, 1177–1216. [Google Scholar] [CrossRef]

- Zhang, Q.X.; Feng, L. Macroeconomic policy uncertainty and firm technological innovation: Empirical evidence from Listed companies in China. Contemp. Econ. Sci. 2018, 40, 48–57+126. [Google Scholar]

- Bloom, N.; Floetotto, M.; Jaimovich, N.; Saporta-Eksten, I. Really Uncertain Business Cycles. Finance 2012, 67, 1219–1264. [Google Scholar]

- Bloom, N. Fluctuations in Uncertainty. J. Econ. Perspect. 2014, 28, 153–175. [Google Scholar] [CrossRef] [Green Version]

- Bar-Ilan, A.; Strange, W.C. Investment Lags. Am. Econ. Rev. 1996, 86, 610–622. [Google Scholar]

- Kraft, H.; Schwartz, E.; Weiss, F. Growth Options and Firm Valuation. Eur. Financ. Manag. 2018, 24, 209–238. [Google Scholar] [CrossRef] [Green Version]

- Rao, P.G.; Yue, H.; Jiang, G.H. Research on economic policy uncertainty and firm investment behavior. World Econ. 2017, 2, 27–51. [Google Scholar]

- Arellano, C.; Bai, Y.; Kehoe, P.J. Financial Frictions and Fluctuations in Volatility. J. Polit. Econ. 2019, 127, 2049–2103. [Google Scholar] [CrossRef] [Green Version]

- Christiano, L.J.; Motto, R.; Rostagno, M. Risk Shocks. Am. Econ. Rev. 2014, 104, 27–65. [Google Scholar] [CrossRef]

- Ilut, C.L.; Schneider, M. Ambiguous Business Cycles. Am. Econ. Rev. 2014, 104, 2368–2399. [Google Scholar] [CrossRef] [Green Version]

- Julio, B.; Yook, Y. Political Uncertainty and Corporate Investment Cycles. J. Financ. 2012, 1, 45–83. [Google Scholar] [CrossRef]

- Li, F.Y.; Yang, M.Z. Will economic policy uncertainty discourage business investment? An empirical study based on China’s economic policy uncertainty Index. Financ. Res. 2015, 4, 115–129. [Google Scholar]

- Tan, X.F.; Zhang, W.J. Analysis of the impact of economic policy uncertainty on enterprise investment channels. World Econ. 2017, 40, 3–26. [Google Scholar]

- Liu, Z.; Huang, D.H. Economic policy uncertainty, government innovation preference and firm innovation strategy. Financ. Mon. 2020, 20, 130–138. [Google Scholar]

- Popp, A.; Zhang, F. The Macroeconomic Effects of Uncertainty Shocks: The Role of the Financial Channel. J. Econ. Dyn. Control 2016, 69, 319–349. [Google Scholar] [CrossRef]

- Arbatli, E.C.; Davis, S.J.; Ito, A.; Miake, N.; Saito, I. Policy Uncertainty in Japan; NBER Working Paper No. 23411; National Bureau of Economic Research: Cambridge, MA, USA, 2019. [Google Scholar]

- Luk, P.; Cheng, M.; Ng, P.; Wong, K. Economic Policy Uncertainty Spillovers in Small Open Economies: The Case of Hong Kong. Pac. Econ. Rev. 2020, 25, 21–46. [Google Scholar] [CrossRef]

- Pindyck, R.S.; Motamen, H. Capital Risk and Models of Investment Behaviour. In Economic Modelling in the OECD Countries; Springer: Dordrecht, The Netherlands, 1988; pp. 103–117. [Google Scholar]

- Driver, C.; Moreton, D. The Influence of Uncertainty on UK Manufacturing Investment. Econ. J. 1991, 101, 1452–1459. [Google Scholar] [CrossRef]

- Chen, G.R.; Wang, X.F.; Li, X. Introduction to Complex Network: Models, Structures and Dynamics; Higher Education Press: Beijing, China, 2012. [Google Scholar]

- Nock, D.; Yang, S. Social Network Analysis, 2nd ed.; Shanghai People’s Publishing House: Shanghai, China, 2012; pp. 103–104. [Google Scholar]

- Wang, X.F.; Li, X.; Chen, R. Introduction to Network Science; Higher Education Press: Beijing, China, 2012. [Google Scholar]

- Zhao, R.Y.; Wang, J. The Visual Analysis of Social Network Analysis (SNA). Libr. Inform. Knowl. 2011, 1, 88–94. [Google Scholar]

- Zhang, G.L.; Qian, X.H.; Xu, J. Can economic policy uncertainty affect corporate cash holding behavior? Manag Rev. 2017, 29, 15–27. [Google Scholar]

- Brown, J.R.; Petersen, B.C. Cash Holdings and R&D Smoothing. J. Corp. Fin. 2011, 17, 694–709. [Google Scholar]

- Yu, M.G.; Zhong, H.J.; Fan, R. Privatization, financing constraints and firm innovation: Evidence from Chinese industrial firms. Financ. Res. 2019, 4, 75–91. [Google Scholar]

- Hall, B.H.; Lerner, J. The Financing of R&D and Innovation. In Handbook of the Economics of Innovation; Elsevier: Amsterdam, The Netherlands, 2010; pp. 609–639. [Google Scholar]

- Hall, R.; Mishkin, F. The Sensitivity of consumption to Transitory Income: Estimate from Panel Data on Households. Econometrica 1993, 50, 461–481. [Google Scholar] [CrossRef] [Green Version]

- Savignac, F. The Impact of Financial Constraints on Innovation: Evidence from French Manufacturing Firms. Cah. Maison Des Sci. Econ. 2006, 42, 147–159. [Google Scholar]

- Liu, S.; Lin, Z.J.; Sun, F.; Chen, H.W. The impact of financing constraints and agency costs on R&D investment: Evidence from Listed companies in China. Account. Res. 2015, 11, 62–68+97. [Google Scholar]

- Zhou, K.; Lu, Y.; Yang, H. Financing constraints, innovation capacity and firm collaborative innovation. Econ. Res. J. 2017, 52, 94–108. [Google Scholar]

- Duchin, R.; Gilbert, T.; Harford, J.; Hrdlicka, C. Precautionary Savings with Risky Assets: When Cash Is Not Cash. J. Financ. 2017, 72, 793–852. [Google Scholar] [CrossRef]

- Greenwald, B.C.; Stiglitz, J.E. Macroeconomic Models with Equity and Credit Rationing; University of Chicago Press: Chicago, IL, USA, 1990; pp. 15–42. [Google Scholar]

- Gu, Y.; Zhou, Q.L. Policy uncertainty, financial flexible value and dynamic adjustment of capital structure. World Econ. 2018, 41, 102–126. [Google Scholar]

- Orhangazi, O. Financialization and Capital Accumulation in the Non-financial Corporate Sector: At Heoretical and Empirical Investigation on the US Economy:1973–2003. Camb. J. Econ. 2008, 32, 863–886. [Google Scholar] [CrossRef] [Green Version]

- Xie, J.Z.; Wang, W.T.; Jiang, Y. Manufacturing financialization, government control and technological innovation. Econ. Trends 2014, 11, 78–88. [Google Scholar]

- Wang, H.J.; Li, M.Y.; Tang, T.J. Driving factors of cross-industry arbitrage of real enterprises and its impact on innovation. China Ind. Econ. 2016, 11, 73–89. [Google Scholar]

- Palley, T.I. Financialization: What It Is and Why It Matters; Palgrave Macmillan: London, UK, 2013. [Google Scholar] [CrossRef] [Green Version]

- Tori, D.; Özlem, O. The effects of Financialisation and Financial Development on Investment: Evidence from Dirm-Level Data in Europe. Greenwich Pap. Polit Econ. 2017, 21, 65. [Google Scholar] [CrossRef]

- Opler, T.; Pinkowitz, L.; Stulz, R. The Determinants and Implications of Corporate Cash Holdings. J. Financ. Econ. 1999, 52, 3–46. [Google Scholar] [CrossRef] [Green Version]

- Kaplan, S.N.; Zingales, L. Do Investment-Cash Flow Sensitivities Provide Useful Measures of Financing Constraints? Q. J. Econ. 1997, 112, 169. [Google Scholar] [CrossRef] [Green Version]

- Whited, T.M.; Wu, G. Financial Constraints Risk. Rev. Financ. Stud. 2006, 19, 531–539. [Google Scholar] [CrossRef]

- Hadlock, C.J.; Pierce, J.R. New Evidence on Measuring Financial Constraints: Moving Beyond the K.Z. Index. Rev. Financ. Stud. 2010, 23, 1909–1940. [Google Scholar] [CrossRef]

- Song, J.; Lu, Y. The U-shaped relationship between non-monetary financial assets and operating returns: Evidence from financialization of Listed non-financial companies in China. Financ. Res. 2015, 6, 111–127. [Google Scholar]

- Xiao, Z.H.Y.; Lin, L. Corporate finance, life cycle and sustainable innovation: An empirical study based on industry classification. Financ. Econ Res. 2019, 45, 43–57. [Google Scholar]

- Haans, R.F.J.; Pieters, C.; He, Z.L. Thinking About U: Theorizing and Testing U- and Inverted U-Shaped Relationships in Strategy Research. Strat. Manag. J. 2016, 37, 1177–1195. [Google Scholar] [CrossRef]

| Variable | N | Median | Mean | Standard Deviation | Minimum | Maximum |

|---|---|---|---|---|---|---|

| GI | 12,141 | 2.830 | 2.800 | 1.620 | 0 | 6.870 |

| EPU1 | 12,141 | 1.810 | 2.730 | 1.730 | 0.989 | 7.919 |

| EPU2 | 12,141 | 0.915 | 0.867 | 0.517 | 0.006 | 1.956 |

| Size | 12,141 | 21.90 | 22.09 | 1.260 | 19.99 | 26.03 |

| ROE | 12,141 | 0.070 | 0.070 | 0.090 | −0.350 | 0.330 |

| LEV | 12,141 | 0.390 | 0.400 | 0.200 | 0.0500 | 0.850 |

| OC | 12,141 | 0.330 | 0.350 | 0.150 | 0.0900 | 0.740 |

| Tang | 12,141 | 0.660 | 0.650 | 0.200 | 0.150 | 0.990 |

| Cash | 12,141 | −0.0200 | −0.0400 | 0.160 | −0.650 | 0.370 |

| Variables | (1) | (2) |

|---|---|---|

| GI | GI | |

| EPU1 | 0.940 *** | |

| (11.04) | ||

| EPU12 | −0.073 *** | |

| (−10.46) | ||

| EPU2 | 0.020 *** | |

| (3.485) | ||

| EPU22 | −0.140 *** | |

| (−14.370) | ||

| Size | −0.718 *** | −0.009 *** |

| (−5.34) | (−2.684) | |

| LEV | 0.104 | −0.087 *** |

| (0.76) | (−2.724) | |

| OC | −0.245 | −0.003 *** |

| (−1.03) | (−12.071) | |

| Tang | −0.047 | −0.002 *** |

| (−0.42) | (−4.179) | |

| Cash | 0.151 *** | −0.443 *** |

| (2.58) | (−22.379) | |

| Constant | −11.839 *** | 0.319 *** |

| (−12.75) | (4.306) | |

| Year | Yes | Yes |

| N | 12,141 | 12,141 |

| F | 53.847 | 276.921 |

| R2 | 0.295 | 0.168 |

| Variables | (1) | (2) |

|---|---|---|

| GI | GI | |

| EPU | 0.231 *** | 1.103 *** |

| (11.64) | (11.19) | |

| EPU2 | −0.092 *** | |

| (−10.81) | ||

| Size | 0.560 *** | 0.560 *** |

| (12.36) | (12.36) | |

| ROE | −0.718 *** | −0.718 *** |

| (−5.34) | (−5.34) | |

| LEV | 0.104 | 0.104 |

| (0.76) | (0.76) | |

| OC | −0.245 | −0.245 |

| (−1.03) | −1.03) | |

| Tang | −0.047 | −0.047 |

| (−0.42) | (−0.42) | |

| Cash | 0.151 *** | 0.151 *** |

| (2.58) | (2.58) | |

| Constant | −10.790 *** | −12.025 *** |

| (−11.22) | (−13.02) | |

| Year | Yes | Yes |

| N | 12,141 | 12,141 |

| R2 | 0.295 | 0.295 |

| Variables | (1) | (2) |

|---|---|---|

| GI | GI | |

| EPU | 0.003 *** | 0.009 *** |

| (10.02) | (8.11) | |

| EPU2 | −0.001 *** | |

| (−7.45) | ||

| Size | 0.009 *** | 0.009 *** |

| (5.59) | (5.59) | |

| ROE | 0.002 | 0.002 |

| (1.49) | (1.49) | |

| LEV | 0.004 | 0.004 |

| (1.28) | (1.28) | |

| OC | 0.001 *** | 0.001 *** |

| (4.34) | (4.34) | |

| Tang | −0.001 | −0.001 |

| (−0.74) | (−0.74) | |

| Cash | −0.004 *** | −0.004 *** |

| (−6.06) | (−6.06) | |

| Constant | 0.059 *** | 0.049 *** |

| (5.30) | (4.56) | |

| Year | Yes | Yes |

| N | 12,141 | 12,141 |

| R2 | 0.09 | 0.09 |

| Variables | (1) | (2) | (3) | (4) |

|---|---|---|---|---|

| High FC | Low FC | High FIN | Low FIN | |

| EPU1 | 0.819 *** | 1.033 *** | 0.742 *** | 1.000 *** |

| (7.28) | (7.74) | (4.71) | (9.63) | |

| EPU12 | −0.063 *** | −0.081 *** | −0.056 *** | −0.079 *** |

| (6.75) | (−7.43) | (−4.27) | (−9.12) | |

| Size | 0.544 *** | 0.573 *** | 0.582 *** | 0.565 *** |

| (9.75) | (7.49) | (6.23) | (11.64) | |

| ROE | −0.682 *** | −0.674 *** | −0.596 ** | −0.586 *** |

| (−3.94) | (−3.12) | (−2.38) | (−3.42) | |

| LEV | 0.158 | −0.005 | −0.034 | 0.057 |

| (0.84) | (−0.02) | (−0.13) | (0.34) | |

| OC | −0.793 ** | 0.267 | −0.430 | −0.208 |

| (−2.35) | (0.72) | (−0.81) | (−0.72) | |

| Tang | 0.080 | −0.165 | −0.153 | 0.088 |

| (0.54) | (−0.94) | (−0.77) | (0.66) | |

| Cash | 0.203 ** | 0.112 | 0.235 ** | 0.199 *** |

| (2.51) | (1.30) | (2.34) | (2.63) | |

| Constant | −11.119 *** | −12.422 *** | −11.692 *** | −12.198 *** |

| (−9.17) | (−8.17) | (−5.79) | (−12.42) | |

| Year | Yes | Yes | Yes | Yes |

| N | 6069 | 6072 | 3689 | 8452 |

| R-squared | 0.266 | 0.283 | 0.224 | 0.298 |

| F | 40.24 | 47.86 | 17.72 | 71.49 |

| r2_a | 0.263 | 0.281 | 0.220 | 0.296 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Zhou, W.; Huang, X.; Dai, H.; Xi, Y.; Wang, Z.; Chen, L. Research on the Impact of Economic Policy Uncertainty on Enterprises’ Green Innovation—Based on the Perspective of Corporate Investment and Financing Decisions. Sustainability 2022, 14, 2627. https://doi.org/10.3390/su14052627

Zhou W, Huang X, Dai H, Xi Y, Wang Z, Chen L. Research on the Impact of Economic Policy Uncertainty on Enterprises’ Green Innovation—Based on the Perspective of Corporate Investment and Financing Decisions. Sustainability. 2022; 14(5):2627. https://doi.org/10.3390/su14052627

Chicago/Turabian StyleZhou, Wenjun, Xiaorong Huang, Hao Dai, Yuanmeng Xi, Zhansheng Wang, and Long Chen. 2022. "Research on the Impact of Economic Policy Uncertainty on Enterprises’ Green Innovation—Based on the Perspective of Corporate Investment and Financing Decisions" Sustainability 14, no. 5: 2627. https://doi.org/10.3390/su14052627