Economic Consequences of the COVID-19 Pandemic: Will It Be a Barrier to Achieving Sustainability?

Abstract

:1. Introduction

2. Model and Data

2.1. GTAP Model

2.2. Data and Variables

2.3. Scenario Configuration

3. Results

3.1. Aggregated Economic Impact by COVID-19

3.2. Expenditure

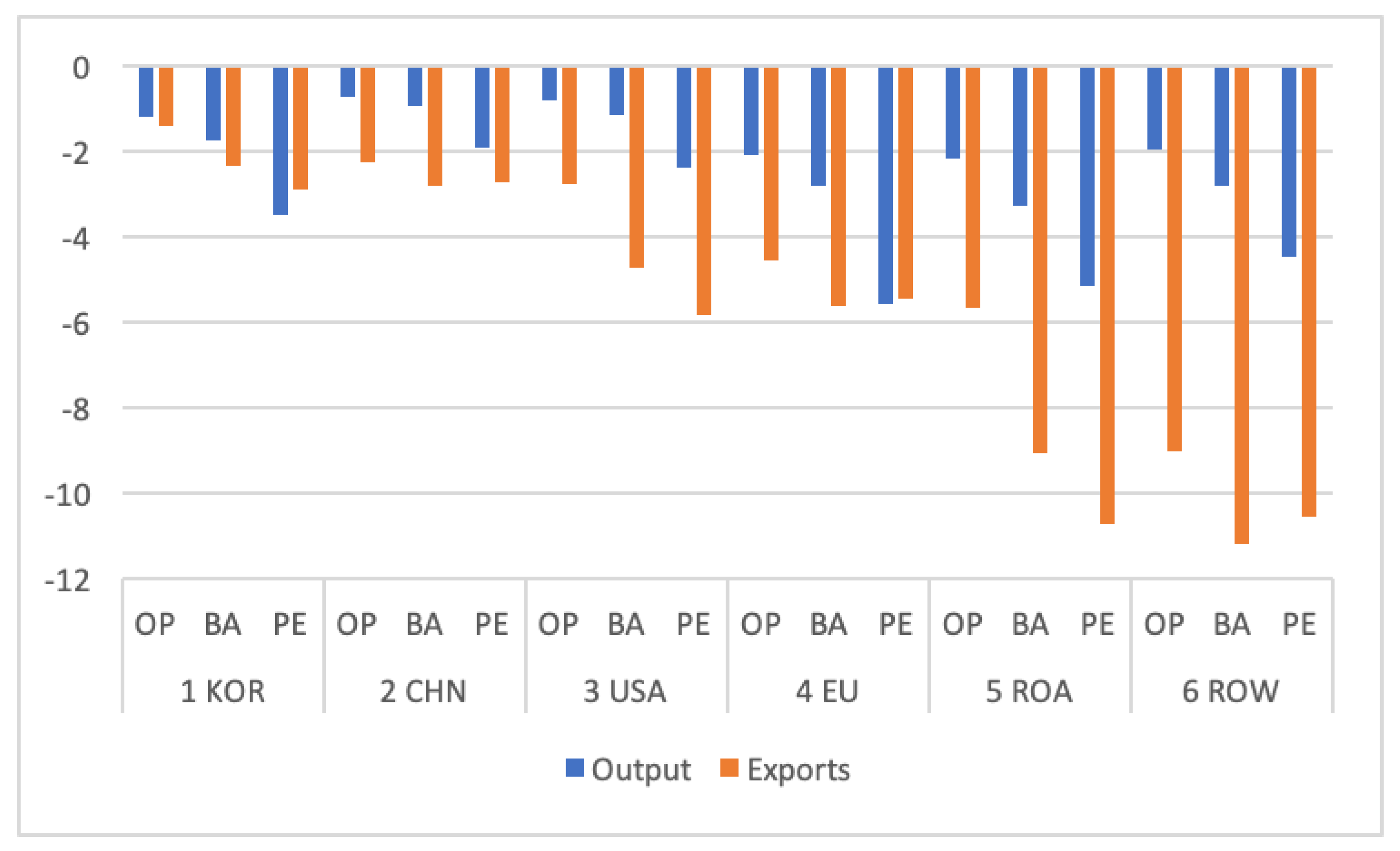

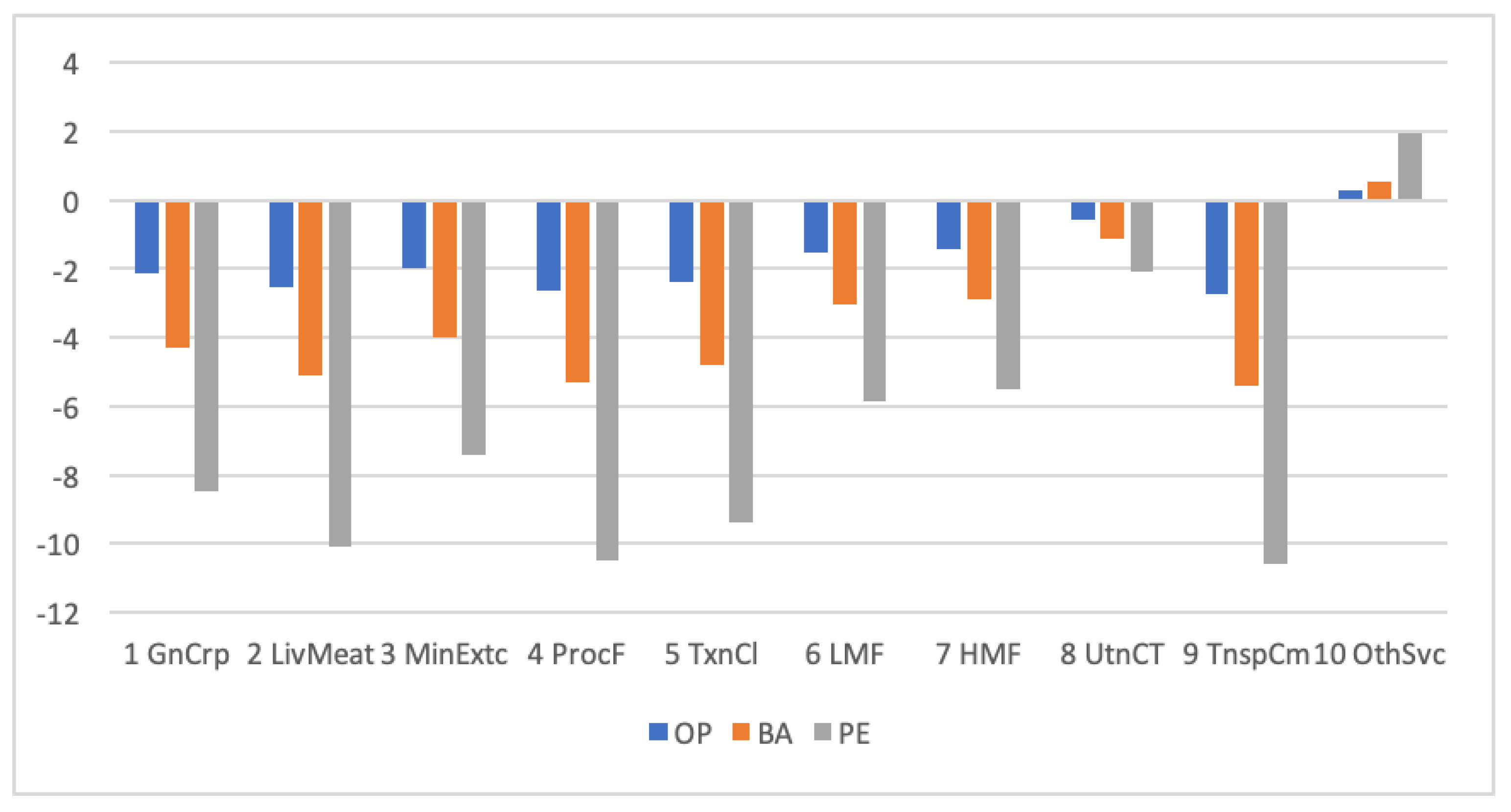

3.3. Output and Exports

3.4. Comparison of Research Results

4. Conclusions and Implications

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Disease | Ebola | MERS | SARS | |||

|---|---|---|---|---|---|---|

| Author | Evans, et al. [10] | Jung et al. [8] | Joo et al. [9] | Hanna & Huang [11] | Lee et al. [33] | Chou et al. [34] |

| Scenario | Low Ebola (low speed of transmission) High Ebola (high speed of transmission) | Using the OLS based on data about credit and debit card purchases | Calculating the difference between the “actual value” and the “projected value” | Reduced demand for service products Reduced FDI Loss of export orders Increase in government budget expenditure | Temporary SARS shock Persistent SARS shock | S1 & S2: Short-run (static) shock S3 & S4: Long-run (steady-state approach) shock |

| Results | In 2014, the loss of GDP amounted to $2.2 billion in the Low Ebola scenario, and $7.4 billion in the High Ebola scenario In 2015, the loss of GDP was $1.6 billion in Low Ebola and the loss of GDP was $25.2 billion in High Ebola | Consumer expenditure decreased by 1.24% when the number of deaths increased by a unit (5.14 per week) Expenditure on eating out, department store and leisure/cultural decreased by 8.24%, 18,01% and 6.87%, respectively. Online shopping expenditure increased by 5.24% | In 2015, about 18% of tourism revenue was lost, and 4% of total domestic and international tourism revenue was lost Reduction of $2.6 billion in tourism revenue and the number of travelers by 2.1 million GDP decreased by about 0.2% | A decrease of about 1.5% in GDP in China (no additional fiscal stimulus) A decrease of 0.9% in GDP in China with the government’s aggressive fiscal and monetary policies In 2003:Q2, China’s GDP contracted by over 5% relative to a seasonally adjusted annualized basis | Impact on GDP from temporary shock (%): China (−1.05), South Korea (−0.1), United States (−0.07) Impact on GDP from persistent shock (%): China (−2.34), South Korea (−0.08), United States (−0.07) | The changes (%) of GDP in S1 & S2: China (−0.13 & −0.2), South Korea (−0.02 & 0.03), EU (−0.01 & 0.01) The changes (%) of GDP in S3 & S4: China (−0.18 & −1.8), South Korea (0.06 & 0.44), EU (0.14 & 0.96) |

Appendix B

| Scenario | Division by Goods | Private Expenditure | Government Expenditure | Firm’s Expenditure | Firm’s Expenditure (Primary Factor) | ||

|---|---|---|---|---|---|---|---|

| KOR | OP | Total | −2.87 | 1.81 | −0.59 | Total | −1.21 |

| Domestic | −2.47 | 1.81 | −0.33 | Labor | −1.41 | ||

| Imported | −5.65 | −0.83 | −1.36 | Capital | −0.99 | ||

| BA | Total | −5.75 | 3.63 | −1.18 | Total | −2.4 | |

| Domestic | −4.93 | 3.63 | −0.66 | Labor | −2.83 | ||

| Imported | −11.3 | −1.38 | −2.73 | Capital | −1.98 | ||

| PE | Total | −11.41 | 7.99 | −2.41 | Total | −4.71 | |

| Domestic | −9.79 | 7.99 | −1.42 | Labor | −5.55 | ||

| Imported | −22.43 | −1.66 | −5.38 | Capital | −3.87 | ||

| CHN | OP | Total | −1.61 | 2.38 | −0.25 | Total | −0.48 |

| Domestic | −1.51 | 2.38 | −0.2 | Labor | −0.51 | ||

| Imported | −3.84 | 1.35 | −0.68 | Capital | −0.46 | ||

| BA | Total | −3.22 | 4.75 | −0.5 | Total | −0.97 | |

| Domestic | −3.02 | 4.77 | −0.4 | Labor | −1.01 | ||

| Imported | −7.67 | 2.71 | −1.36 | Capital | −0.91 | ||

| PE | Total | −6.44 | 9.36 | −1.07 | Total | −1.95 | |

| Domestic | −6.04 | 9.39 | −0.85 | Labor | −2.06 | ||

| Imported | −15.41 | 5.34 | −3.01 | Capital | −1.82 | ||

| USA | OP | Total | −1.93 | 5.1 | −0.37 | Total | −0.55 |

| Domestic | −1.89 | 5.1 | −0.25 | Labor | −0.59 | ||

| Imported | −2.53 | 4.76 | −1.13 | Capital | −0.45 | ||

| BA | Total | −3.86 | 10.21 | −0.73 | Total | −1.1 | |

| Domestic | −3.77 | 10.21 | −0.51 | Labor | −1.19 | ||

| Imported | −5.05 | 9.51 | −2.27 | Capital | −0.89 | ||

| PE | Total | −7.8 | 20.21 | −1.67 | Total | −2.31 | |

| Domestic | −7.62 | 20.22 | −1.2 | Labor | −2.49 | ||

| Imported | −10.3 | 18.73 | −4.88 | Capital | −1.85 | ||

| EU | OP | Total | −3.47 | 3.36 | −1.17 | Total | −1.51 |

| Domestic | −3.13 | 3.38 | −0.85 | Labor | −1.68 | ||

| Imported | −4.97 | 2.8 | −2.16 | Capital | −1.3 | ||

| BA | Total | −6.94 | 6.73 | −2.33 | Total | −3.02 | |

| Domestic | −6.25 | 6.75 | −1.71 | Labor | −3.35 | ||

| Imported | −9.94 | 5.61 | −4.32 | Capital | −2.59 | ||

| PE | Total | −13.8 | 13.72 | −4.74 | Total | −5.95 | |

| Domestic | −12.43 | 13.78 | −3.49 | Labor | −6.63 | ||

| Imported | −19.78 | 11.54 | −8.71 | Capital | −5.08 | ||

| ROA | OP | Total | −6.04 | 14.56 | −1.47 | Total | −1.41 |

| Domestic | −5.9 | 14.57 | −1.28 | Labor | −1.67 | ||

| Imported | −7.51 | 14.15 | −2.27 | Capital | −1.14 | ||

| BA | Total | −12.08 | 29.12 | −2.94 | Total | −2.82 | |

| Domestic | −11.8 | 29.13 | −2.56 | Labor | −3.33 | ||

| Imported | −15.03 | 28.3 | −4.54 | Capital | −2.27 | ||

| PE | Total | −24.12 | 67.05 | −4.61 | Total | −4.06 | |

| Domestic | −23.58 | 67.06 | −3.83 | Labor | −4.77 | ||

| Imported | −30 | 65.43 | −7.9 | Capital | −3.32 | ||

| ROW | OP | Total | −5.81 | 13.82 | −1.35 | Total | −1.13 |

| Domestic | −5.71 | 13.85 | −1.18 | Labor | −1.14 | ||

| Imported | −6.53 | 13.26 | −2.09 | Capital | −1.12 | ||

| BA | Total | −11.62 | 27.65 | −2.7 | Total | −2.25 | |

| Domestic | −11.42 | 27.7 | −2.36 | Labor | −2.27 | ||

| Imported | −13.07 | 26.52 | −4.17 | Capital | −2.23 | ||

| PE | Total | −23.45 | 62.18 | −4.35 | Total | −3.27 | |

| Domestic | −23.03 | 62.28 | −3.63 | Labor | −2.94 | ||

| Imported | −26.5 | 59.7 | −7.42 | Capital | −3.58 | ||

References

- Johns Hopkins Coronavirus Resources Center Website. Available online: https://coronavirus.jhu.edu/map.html (accessed on 11 November 2021).

- OECD. Economic Outlook, Interim Report. Available online: https://www.oecd.org/economic-outlook/september-2021/ (accessed on 1 March 2021).

- International Monetary Fund (IMF). World Economic Outlook: Recovery during a Pandemic-Health Concerns, Supply Disruptions, Price Pressures; International Monetary Fund (IMF): Washington, DC, USA, 2021. [Google Scholar]

- Cho, D.H.; Kim, J.J. The Impact of the COVID-19 Pandemic on the Domestic Economy and Future Challenges. J. Humanit. Soc. Sci. 2020, 11, 2597–2612. [Google Scholar]

- Choi, B.S.; Park, H.J. The Effects of COVID-19 Diffusion in the Korean Economy: Using SIR-Based Macro-Epidemiological Model. Env. Resour. Econ. 2021, 30, 27–48. [Google Scholar]

- Asian Development Bank. SARS: Economic Impacts and Implications. Economics and Research Department Policy Brief Series No. 15; Asian Development Bank: Metro Manila, Philippines, 2003. [Google Scholar]

- Siu, A.; Wong, Y.R. Economic Impact of SARS: The Case of Hong Kong. Asian Econ. Pap. 2004, 3, 62–83. [Google Scholar] [CrossRef] [Green Version]

- Jung, H.; Park, M.; Hong, K.; Hyung, E. The Impact of an Epidemic Outbreak on Consumer Expenditures: An Empirical Assessment for MERS Korea. Sustainability 2016, 8, 454. [Google Scholar] [CrossRef] [Green Version]

- Joo, H.; Maskery, B.A.; Berro, A.D.; Rotz, L.D.; Lee, Y.K.; Brown, C.M. Economic Impact of the 2015 MERS Outbreak on the Republic of Korea’s Tourism-Related Industries. Health Secur. 2019, 17, 100–108. [Google Scholar] [CrossRef] [PubMed]

- Estimating the Economic Impact of the Ebola Epidemic: Evidence from Computable General Equilibrium Models. Available online: https://www.gtap.agecon.purdue.edu/resources/res_display.asp?RecordID=4775 (accessed on 10 November 2021).

- Hanna, D.; Huang, Y. The Impact of SARS on Asian Economies. Asian Econ. Pap. 2004, 3, 102–112. [Google Scholar] [CrossRef]

- McKibbin, W.J.; Fernando, R. The Global Macroeconomic Impacts of COVID-19: Seven Scenarios. Asian Econ. Pap. 2021, 20, 1–30. [Google Scholar] [CrossRef]

- The Potential Impact of COVID-19 on GDP and Trade: A Pre-liminary Assessment. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3573211 (accessed on 11 November 2021).

- Zeshan, M. Double-hit scenario of Covid-19 and global value chains. Environ. Dev. Sustain. 2020, 23, 8559–8572. [Google Scholar] [CrossRef] [PubMed]

- Walmsley, T.; Rose, A.; Wei, D. Impacts on the US Macroeconomy of Mandatory Business Closures in Response to the COVID-19 Pandemic. Appl. Econ. Lett. 2020, 28, 1293–1300. [Google Scholar] [CrossRef]

- Lahcen, B.; Brusselaers, J.; Vrancken, K.; Dams, Y.; Paes, C.D.S.; Eyckmans, J.; Rousseau, S. Green Recovery Policies for the COVID-19 crisis: Modelling the Impact on the Economy and Greenhouse Gas Emissions. Env. Resour. Econ. 2020, 76, 731–750. [Google Scholar] [CrossRef] [PubMed]

- Malliet, P.; Frédéric, R.; Gissela, L.; Hamdi-Cherif, M.; Saussay, A. Assessing Short-Term and Long-Term Economic and Environmental Effects of the COVID-19 Crisis in France. Env. Resour. Econ. 2020, 76, 867–883. [Google Scholar] [CrossRef] [PubMed]

- Wittwer, G. The 2019–20 Australian Economic Crisis Induced by Bushfires and COVID-19 from the Perspective of Grape and Wine Sectors. Centre of Policy Studies (CoPS) Working Paper No G-299; Victoria University: Melbourne, Australia, 2020. [Google Scholar]

- Jo, H.; Shin, E.; Kim, H. Changes in Consumer Behaviour in the Post-COVID-19 Era in Seoul, South Korea. Sustainability 2021, 13, 136. [Google Scholar] [CrossRef]

- Sohn, J.-I.; Alakshendra, A.; Kim, H.-J.; Kim, K.-H.; Kim, H.-D. Understanding the New Characteristics and Development Strategies of Coastal Tourism for Post-COVID-19: A Case Study in Korea. Sustainability 2021, 13, 7408. [Google Scholar] [CrossRef]

- Jiang, J.; Park, E.-M.; Park, S.-T. The Impact of the COVID-19 on Economic Sustainability—A Case Study of Fluctuation in Stock Prices for China and South Korea. Sustainability 2021, 13, 6642. [Google Scholar] [CrossRef]

- Kim, M.; Lee, S. Can stimulus checks boost an economy under covid-19? evidence from South Korea. Int. Econ. J. 2021, 35, 1–12. [Google Scholar] [CrossRef]

- Aguiar, A.; Narayanan, B.; McDougall, R. An Overview of the GTAP 9 Data Base. J. Glob. Econ. Anal. 2016, 1, 181–208. [Google Scholar] [CrossRef]

- Corong, E.L.; Hertel, T.W.; McDougall, R.; Tsigas, M.E.; van der Mensbrugghe, D. The Standard GTAP Model, Version 7. J. Glob. Econ. Anal. 2017, 2, 1–119. [Google Scholar]

- McDonald, S.; Robinson, S.; Thierfelder, K.E. Globe: A SAM Based Global CGE Model Using GTAP Data; US Naval Academy Department of Economics: Annapolis, MD, USA, 2006. [Google Scholar]

- Cameron, B. The production function in Leontief models. Rev. Econ. Stud. 1952, 20, 62–69. [Google Scholar] [CrossRef]

- World Bank. Global Economic Prospects. Available online: https://www.worldbank.org/en/publication/global-economic-prospects (accessed on 15 June 2021).

- IMF. World Economic Outlook Reports. Available online: https://www.imf.org/en/Publications/WEO (accessed on 20 March 2021).

- Bank of Korea. Economic Outlook Report. Available online: https://www.bok.or.kr/eng/bbs/E0000634/view.do?nttId=10064693&menuNo=400069 (accessed on 20 August 2021).

- ILO. World Employment and Social Outlook. Available online: https://www.ilo.org/global/research/global-reports/weso/trends2021/lang-en/index.htm (accessed on 20 August 2021).

- Narayanan, B.; Villafuerte, J. Estimating the Economic Impact of COVID-19: A Supply Side Analysis. 23rd Annual Con-ference on Global Economic Analysis. 2020. Available online: https://www.gtap.agecon.purdue.edu/resources/res_display.asp?RecordID=6141 (accessed on 15 December 2021).

- UNWTO. World Tourism Barometer. Available online: https://www.e-unwto.org/loi/wtobarometereng (accessed on 5 September 2021).

- Lee, J.W.; McKibbin, W.J. Globalization and Disease: The Case of SARS. Asian Econ. Pap. 2004, 3, 113–131. [Google Scholar] [CrossRef]

- Chou, J.; Kuo, N.F.; Peng, S.L. Potential Impacts of the SARS Outbreak on Taiwan’s Economy. Asian Econ. Pap. 2004, 3, 84–99. [Google Scholar] [CrossRef]

| Region | Sector | Factor of Production |

|---|---|---|

| 1. KOR (Korea) 2. CHN (China) 3. USA (United of States) 4. EU (Europe) 5. ROA (Rest of Asia) 6. Rest of the World (ROW) | 1. GnCrp (Grains and Crops) 2. LivMeat (Livestock and Meat Products) 3. MinExtc (Mining and Extraction) 4. ProcF (Processed Food) 5. TxnCl (Textiles and Clothing) 6. LMF (Light Manufacturing) 7. HMF (Heavy Manufacturing) 8. UtnCT (Utilities and Construction) 9. TnspCm (Transport and Communication) 10. OthSvc (Other Services) | 1. Lab (Labor) 2. Capital (Capital) |

| Region and Country | Economic Situation and Outlook |

|---|---|

| CHN | There are a few additional confirmed cases In 2021, the trend of growth has continued, focusing on consumption and exports |

| USA | Continuous implementation of large-scale financial policies Maintaining a positive recovery with rapid vaccine distribution and vaccination |

| ⇒ The unexpected spread of COVID-19 could have negative impacts on recovery, but a good trend of recovery is expected to continue, focusing on employment and demand | |

| EU | The recession in neighboring countries was caused by a mutant virus from the UK and delayed the supply of vaccines After 21Q2: augmentation of vaccination rate and relaxation of quarantine measures |

| KOR | In 2021, there was an 11.9% increase in fiscal expenditure Vaccination progressing quickly Sporadic mass infection and slow recovery in the employment sector |

| ⇒ Since the first half, the recovery is projected to expand because of consistent vaccination and implementation of fiscal stimulus | |

| ROA & ROW | Poor conditions for quick vaccination and mass storage of vaccines, unlike in advanced countries Financial difficulties in implementing immediate, large-scale reflation measures |

| ⇒ Overall, the economy is expected to recover slowly after the second half | |

| Scenario | Region | Shock | ||

|---|---|---|---|---|

| This study | Optimistic | CHN & USA | Supply of labor: −1% Demand of domestic tourism industry: −2.5% | Export tax on tourism industry: +15% |

| KOR & EU | Supply of labor: −2% Demand of domestic tourism industry: −5% | |||

| ROA & ROW | Supply of labor: −3% Demand of domestic tourism industry: −7.5% | |||

| Baseline | CHN & USA | Supply of labor: −2% Demand of domestic tourism industry: −5% | Export tax on tourism industry: +30% | |

| KOR & EU | Supply of labor: −4% Demand of domestic tourism industry: −10% | |||

| ROA & ROW | Supply of labor: −6% Demand of domestic tourism industry: −15% | |||

| Pessimistic | CHN & USA | Supply of labor: −3% Demand of domestic tourism industry: −10% | Export tax on tourism industry: +60% | |

| KOR & EU | Supply of labor: −6% Demand of domestic tourism industry: −20% | |||

| ROA & ROW | Supply of labor: −9% Demand of domestic tourism industry: −30% | |||

| Maliszewska et al. [13] | Global pandemic | China | Employment: −3% International costs of imports and exports: +25% Export tax on tourist services: +50% Demand of targeted services: −15% | |

| ROW | 1/2 of China | |||

| Amplified global pandemic | All regions | Same as China in “global pandemic” scenario | ||

| Narayanan & Villafuerte [31] | Short containment | China | Consumption: −5% Investment: −5% Tourism receipts −11.4% | Trade costs: +1% |

| ROW | Consumption: −2% Investment: −2% Tourism receipts −4.4% | |||

| Long containment | China | Consumption: −5% Investment: −6.25% Tourism receipts −22.9% | Trade costs: +2% | |

| ROW | Consumption −5% Investment: −6.25% Tourism receipts −8.9% | |||

| Scenario | World | US | China | South Korea |

|---|---|---|---|---|

| Optimistic | −1.03 | −0.45 | 0.44 | −0.96 |

| Baseline | −2.11 | −0.9 | −0.11 | −1.91 |

| Pessimistic | −3.38 | −1.92 | −0.62 | −3.92 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Choi, Y.; Kim, H.-j.; Lee, Y. Economic Consequences of the COVID-19 Pandemic: Will It Be a Barrier to Achieving Sustainability? Sustainability 2022, 14, 1629. https://doi.org/10.3390/su14031629

Choi Y, Kim H-j, Lee Y. Economic Consequences of the COVID-19 Pandemic: Will It Be a Barrier to Achieving Sustainability? Sustainability. 2022; 14(3):1629. https://doi.org/10.3390/su14031629

Chicago/Turabian StyleChoi, Yoonkyung, Hyun-ju Kim, and Yoon Lee. 2022. "Economic Consequences of the COVID-19 Pandemic: Will It Be a Barrier to Achieving Sustainability?" Sustainability 14, no. 3: 1629. https://doi.org/10.3390/su14031629