Does Local Confucian Culture Affect Corporate Environmental, Social, and Governance Ratings? Evidence from China

Abstract

:1. Introduction

2. Hypotheses Development

3. Research Design

3.1. Variables Definition and Sample Construction

3.2. Model Specification

4. Empirical Results

4.1. Baseline Regression

4.2. Test of Hypotheses 2~5

4.3. Robustness Checks

4.3.1. Instrumental Variable Regression

4.3.2. Alternative Measures of Local Confucian Culture and ESG

5. Concluding Remarks

Author Contributions

Funding

Conflicts of Interest

References

- Dietzenbacher, E.; Pei, J.; Yang, C. Trade, production fragmentation, and China’s carbon dioxide emissions. J. Environ. Econ. Manag. 2012, 64, 88–101. [Google Scholar] [CrossRef]

- Narayan, P.K.; Rizvi, S.A.R.; Sakti, A. Did green debt instruments aid diversification during the COVID-19 pandemic? Financ. Innov. 2022, 8, 21. [Google Scholar] [CrossRef] [PubMed]

- Narayan, P.K.; Saboori, B.; Soleymani, A. Economic growth and carbon emissions. Econ. Model. 2016, 53, 388–397. [Google Scholar] [CrossRef]

- Wen, F.; Wu, N.; Gong, X. China’s carbon emissions trading and stock returns. Energy Econ. 2020, 86, 104627. [Google Scholar] [CrossRef]

- Xia, Y.; Yang, C.; Chen, X. Structural decomposition analysis on China’s energy intensity change for 1987–2005. J. Syst. Sci. Complex. 2012, 25, 156–166. [Google Scholar] [CrossRef]

- Brower, J.; Mahajan, V. Driven to be good: A stakeholder theory perspective on the drivers of corporate social performance. J. Bus. Ethics 2013, 117, 313–331. [Google Scholar] [CrossRef]

- Laplume, A.O.; Sonpar, K.; Litz, R.A. Stakeholder theory: Reviewing a theory that moves us. J. Manag. 2008, 34, 1152–1189. [Google Scholar] [CrossRef]

- Hart, O.; Zingales, L. Companies should maximize shareholder welfare not market value. ECGI-Financ. Work. Pap. 2017, 2, 247–274. [Google Scholar]

- Bénabou, R.; Tirole, J. Individual and corporate social responsibility. Economica 2010, 77, 1–19. [Google Scholar] [CrossRef] [Green Version]

- Eccles, R.G.; Ioannou, I.; Serafeim, G. The impact of corporate sustainability on organizational processes and performance. Manag. Sci. 2014, 60, 2835–2857. [Google Scholar] [CrossRef] [Green Version]

- Flammer, C.; Kacperczyk, A. The impact of stakeholder orientation on innovation: Evidence from a natural experiment. Manag. Sci. 2016, 62, 1982–2001. [Google Scholar] [CrossRef]

- Christensen, D.M.; Serafeim, G.; Sikochi, S. Why is corporate virtue in the eye of the beholder? The case of ESG ratings. Account. Rev. 2022, 97, 147–175. [Google Scholar] [CrossRef]

- GSIA. Global Sustainable Investment Review. 2018. Available online: http://www.gsi-alliance.org/wp-content/uploads/2019/03/GSIR_Review2018.3.28.pdf (accessed on 8 August 2021).

- Feng, J.; Goodell, J.W.; Shen, D. ESG rating and stock price crash risk: Evidence from China. Financ. Res. Lett. 2021, 46, 102476. [Google Scholar] [CrossRef]

- Friede, G.; Busch, T.; Bassen, A. ESG and financial performance: Aggregated evidence from more than 2000 empirical studies. J. Sustain. Financ. Invest. 2015, 5, 210–233. [Google Scholar] [CrossRef] [Green Version]

- Broadstock, D.C.; Chan, K.; Cheng, L.T.; Wang, X. The role of ESG performance during times of financial crisis: Evidence from COVID-19 in China. Financ. Res. Lett. 2021, 38, 101716. [Google Scholar] [CrossRef] [PubMed]

- Singh, A. COVID-19 and safer investment bets. Financ. Res. Lett. 2020, 36, 101729. [Google Scholar] [CrossRef]

- Krueger, P.; Sautner, Z.; Tang, D.Y.; Zhong, R. The Effects of Mandatory ESG Disclosure around the World. SSRN 2021, 3832745. [Google Scholar] [CrossRef]

- Bruno, M.; Lagasio, V. An overview of the European policies on ESG in the banking sector. Sustainability 2021, 13, 12641. [Google Scholar] [CrossRef]

- Chen, Y.P.V.; Zhuo, Z.; Huang, Z.; Li, W. Environmental regulation and ESG of SMEs in China: Porter hypothesis re-tested. Sci. Total Environ. 2022, 850, 157967. [Google Scholar] [CrossRef]

- Friedman, H.L.; Heinle, M.S. Taste, information, and asset prices: Implications for the valuation of CSR. Rev. Account. Stud. 2016, 21, 740–767. [Google Scholar] [CrossRef] [Green Version]

- Geczy, C.; Stambaugh, R.F.; Levin, D. Investing in socially responsible mutual funds. SSRN 2005, 416380. [Google Scholar] [CrossRef]

- Heinkel, R.; Kraus, A.; Zechner, J. The effect of green investment on corporate behavior. J. Financ. Quant. Anal. 2001, 36, 431–449. [Google Scholar] [CrossRef]

- Martins, H.C. Competition and ESG practices in emerging markets: Evidence from a difference-in-differences model. Financ. Res. Lett. 2021, 46, 102371. [Google Scholar] [CrossRef]

- Dang, R.; Houanti, L.H.; Sahut, J.-M.; Simioni, M. Do women on corporate boards influence corporate social performance? A control function approach. Financ. Res. Lett. 2021, 39, 101645. [Google Scholar] [CrossRef]

- Garcia, A.S.; Mendes-Da-Silva, W.; Orsato, R.J. Sensitive industries produce better ESG performance: Evidence from emerging markets. J. Clean. Prod. 2017, 150, 135–147. [Google Scholar] [CrossRef]

- Drempetic, S.; Klein, C.; Zwergel, B. The influence of firm size on the ESG score: Corporate sustainability ratings under review. J. Bus. Ethics 2020, 167, 333–360. [Google Scholar] [CrossRef]

- Yu, E.P.-y.; Van Luu, B. International variations in ESG disclosure–Do cross-listed companies care more? Int. Rev. Financ. Anal. 2021, 75, 101731. [Google Scholar] [CrossRef]

- Du, X.; Du, Y.; Zeng, Q.; Pei, H.; Chang, Y. Religious atmosphere, law enforcement, and corporate social responsibility: Evidence from China. Asia Pac. J. Manag. 2016, 33, 229–265. [Google Scholar] [CrossRef]

- Zaman, R.; Roudaki, J.; Nadeem, M. Religiosity and corporate social responsibility practices: Evidence from an emerging economy. Soc. Responsib. J. 2018, 14, 368–395. [Google Scholar] [CrossRef]

- Hoi, C.K.; Wu, Q.; Zhang, H. Community social capital and corporate social responsibility. J. Bus. Ethics 2018, 152, 647–665. [Google Scholar] [CrossRef]

- Peng, Y.-S.; Dashdeleg, A.-U.; Chih, H.L. National Culture and Firm’s CSR Engagement: A Cross-Nation Study. J. Mark. Manag. 2014, 5, 38–49. [Google Scholar]

- Hoi, C.K.S.; Wu, Q.; Zhang, H. Does social capital mitigate agency problems? Evidence from Chief Executive Officer (CEO) compensation. J. Financ. Econ. 2019, 133, 498–519. [Google Scholar] [CrossRef]

- Yao, X. An Introduction to Confucianism; Cambridge University Press: Cambridge, UK, 2000. [Google Scholar]

- Low, K.C.P.; Ang, S.-L. Confucian leadership and corporate social responsibility (CSR), the way forward. J. Bus. Res. 2012, 2, 85–101. [Google Scholar] [CrossRef]

- Low, K.; Ang, S.-L. Confucian ethics, governance and corporate social responsibility. Int. J. Bus. Manag. 2013, 8, 30–43. [Google Scholar]

- Hilary, G.; Hui, K.W. Does religion matter in corporate decision making in America? J. Financ. Econ. 2009, 93, 455–473. [Google Scholar] [CrossRef]

- Deng, Y. Does Culture Matter in Corporate Cash Holdings? SSRN 2021, 3891206. [Google Scholar] [CrossRef]

- Du, X. Does religion matter to owner-manager agency costs? Evidence from China. J. Bus. Ethics 2013, 118, 319–347. [Google Scholar] [CrossRef] [Green Version]

- Du, X. Does Confucianism reduce minority shareholder expropriation? Evidence from China. J. Bus. Ethics 2015, 132, 661–716. [Google Scholar] [CrossRef]

- Wang, L.; Juslin, H. The impact of Chinese culture on corporate social responsibility: The harmony approach. J. Bus. Ethics 2009, 88, 433–451. [Google Scholar] [CrossRef]

- Chen, C.; Chen, Y.; Hsu, P.-H.; Podolski, E.J. Be nice to your innovators: Employee treatment and corporate innovation performance. J. Corp. Financ. 2016, 39, 78–98. [Google Scholar] [CrossRef] [Green Version]

- Huang, M.; Li, P.; Meschke, F.; Guthrie, J.P. Family firms, employee satisfaction, and corporate performance. J. Corp. Financ. 2015, 34, 108–127. [Google Scholar] [CrossRef]

- Melo, T.; Galan, J.I. Effects of corporate social responsibility on brand value. J. Brand Manag. 2011, 18, 423–437. [Google Scholar] [CrossRef] [Green Version]

- Servaes, H.; Tamayo, A. The impact of corporate social responsibility on firm value: The role of customer awareness. Manag. Sci. 2013, 59, 1045–1061. [Google Scholar] [CrossRef]

- El Ghoul, S.; Guedhami, O.; Kwok, C.C.; Mishra, D.R. Does corporate social responsibility affect the cost of capital? J. Bank. Financ. 2011, 35, 2388–2406. [Google Scholar] [CrossRef]

- Chi, W.; Chen, Y. Employee satisfaction and the cost of corporate borrowing. Financ. Res. Lett. 2021, 40, 101666. [Google Scholar] [CrossRef]

- Jiang, F.; Kim, K.A. Corporate governance in China: A survey. Rev. Financ. 2020, 24, 733–772. [Google Scholar] [CrossRef]

- Gregory, R.P. The influence of firm size on ESG score controlling for ratings agency and industrial sector. J. Sustain. Financ. Investig. 2022, 1–14. [Google Scholar] [CrossRef]

- Shakil, M.H. Environmental, social and governance performance and stock price volatility: A moderating role of firm size. J. Public Aff. 2022, 22, e2574. [Google Scholar] [CrossRef]

- Fu, P.; Ma, C.; Tian, Y. Does Confucianism mitigate informed insider trading? Evidence from China. SSRN 2021, 3953532. [Google Scholar] [CrossRef]

- Vincenty, T. Direct and inverse solutions of geodesics on the ellipsoid with application of nested equations. Surv. Rev. 1975, 23, 88–93. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Variables | Definition |

|---|---|

| ESG_Sino | ESG scores are rated by the Sino-Securities Index. ESG was rated as AAA, AA, A, BBB, BB, B, CCC, CC, and C. We assigned them as 9, 8, …, and 1 correspondingly. |

| CONFUC1 (CONFUC2, CONFUC3) | The natural logarithm of one plus the number of Confucius temples and centers within a radius of 100 (200, 300) km surrounding the headquarter of the listed firm. |

| Size | The natural logarithm of the total asset at the end of the current fiscal year. |

| BTM | The ratio of the book value of equity to the market value of equity at the end of the current fiscal year. |

| Leverage | The ratio of a firm’s total debt to its total asset at the end of the current fiscal year. |

| ROA | The return on assets, calculated as the ratio of corporate annual earnings to its total asset at the end of the current fiscal year. |

| FCF | Free cash flow, calculated as EBITDA (earnings before interest, taxes, depreciation, and amortization)—CWC (changes in working capital)—CAPEX (capital expenditure) then scaled by its total revenue at the end of the current fiscal year. |

| SOE | An indicator variable that takes the value of 1 if the firm’s final controller is a state-owned asset management agency and 0 otherwise. |

| High_Media | An indicator variable that equals 1 if the number of news pieces mentioning one firm is above the median value across the fiscal year and 0 otherwise. The data are from the Chinese Research Data Services Platform. |

| High_Analyst | A dummy variable that equals 1 if the number of analysts following the firm is above its median value in the fiscal year and 0 otherwise. |

| Panel A: Sample statistics of local Confucian culture measures | ||||||||||||

| Variables | Mean | P50 | SD | P25 | P75 | N | ||||||

| CONFUC1 | 1.883 | 2.079 | 0.711 | 1.609 | 2.398 | 29,922 | ||||||

| CONFUC2 | 2.733 | 2.833 | 0.762 | 2.708 | 3.219 | 29,922 | ||||||

| CONFUC3 | 3.307 | 3.434 | 0.749 | 3.332 | 3.638 | 29,922 | ||||||

| Panel B: Sample statistics of local Confucian culture measures in large and small-sized firms | ||||||||||||

| Large Size | Small Size | |||||||||||

| Variables | Mean | P50 | SD | P25 | P75 | N | Mean | P50 | SD | P25 | P75 | N |

| CONFUC1 | 1.887 | 2.197 | 0.713 | 1.609 | 2.398 | 14,959 | 1.879 | 2.079 | 0.709 | 1.609 | 2.398 | 14,963 |

| CONFUC2 | 2.727 | 2.833 | 0.775 | 2.639 | 3.219 | 14,959 | 2.739 | 2.833 | 0.748 | 2.708 | 3.219 | 14,963 |

| CONFUC3 | 3.309 | 3.434 | 0.768 | 3.332 | 3.664 | 14,959 | 3.304 | 3.466 | 0.731 | 3.332 | 3.638 | 14,963 |

| Panel C: Sample statistics of local Confucian culture measures in SOE and non-SOE firms | ||||||||||||

| SOE | Non-SOE | |||||||||||

| Mean | P50 | SD | P25 | P75 | N | Mean | P50 | SD | P25 | P75 | N | |

| 1.831 | 2.079 | 0.755 | 1.386 | 2.398 | 11,455 | 1.915 | 2.079 | 0.68 | 1.609 | 2.398 | 18,467 | |

| 2.671 | 2.833 | 0.836 | 2.639 | 3.219 | 11,455 | 2.771 | 2.833 | 0.709 | 2.708 | 3.219 | 18,467 | |

| 3.27 | 3.434 | 0.845 | 3.332 | 3.664 | 11,455 | 3.33 | 3.466 | 0.682 | 3.332 | 3.638 | 18,467 | |

| Panel D: Univariate comparison of key variables. | ||||||||||||

| Full Sample | High Confucius | Low Confucius | Mean (High-Low) | T-Stat | ||||||||

| N = 29922 | N = 16226 | N = 13706 | ||||||||||

| Mean | Median | Std. Dev. | Mean | Median | Std. Dev. | Mean | Median | Std. Dev. | ||||

| ESG_Sino | 6.453 | 6 | 1.132 | 6.498 | 6 | 1.12 | 6.402 | 6 | 1.143 | 0.096 *** | 7.357 | |

| Size | 22.13 | 21.97 | 1.331 | 22.19 | 22.01 | 1.396 | 22.06 | 21.92 | 1.251 | 0.13 *** | 8.467 | |

| BTM | 0.609 | 0.607 | 0.25 | 0.608 | 0.604 | 0.25 | 0.61 | 0.61 | 0.249 | −0.002 | −0.782 | |

| Leverage | 0.442 | 0.433 | 0.219 | 0.437 | 0.428 | 0.218 | 0.448 | 0.438 | 0.22 | −0.011 *** | −4.293 | |

| ROA | 0.0326 | 0.0349 | 0.0729 | 0.0346 | 0.0367 | 0.0712 | 0.0303 | 0.0328 | 0.0747 | 0.004 *** | 5.129 | |

| FCF | −0.0254 | 0.0228 | 0.457 | −0.0232 | 0.0226 | 0.454 | −0.028 | 0.0229 | 0.46 | 0.005 | 0.905 | |

| SOE | 0.383 | 0 | 0.486 | 0.369 | 0 | 0.483 | 0.398 | 0 | 0.489 | −0.029 *** | −5.089 | |

| Dep. Var = ESG_Sino | ||||||

|---|---|---|---|---|---|---|

| Model: OLS | Model: Ordered Probit | |||||

| (1) | (2) | (3) | (4) | (5) | (6) | |

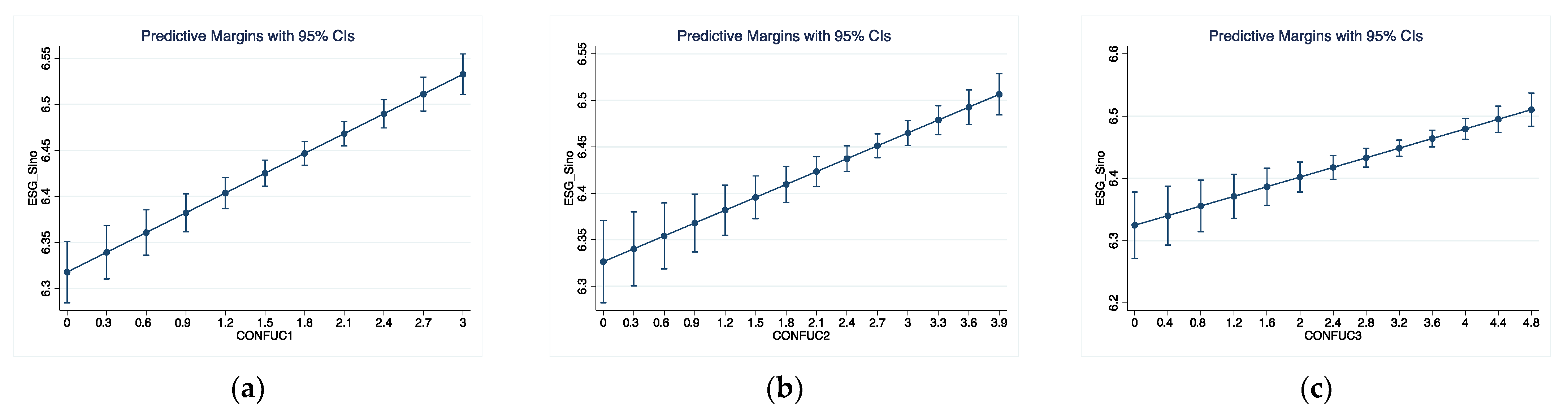

| CONFUC1 | 0.0442 *** | 0.0497 *** | ||||

| (0.0082) | (0.009) | |||||

| CONFUC2 | 0.031 *** | 0.0348 *** | ||||

| (0.0077) | (0.0084) | |||||

| CONFUC3 | 0.0239 *** | 0.0258 *** | ||||

| (0.0077) | (0.0085) | |||||

| Size | 0.3359 *** | 0.3377 *** | 0.3378 *** | 0.3731 *** | 0.3751 *** | 0.3752 *** |

| (0.0066) | (0.0066) | (0.0066) | (0.0076) | (0.0076) | (0.0076) | |

| BTM | −0.329 *** | −0.3335 *** | −0.3349 *** | −0.3652 *** | −0.3702 *** | −0.3717 *** |

| (0.0346) | (0.0346) | (0.0346) | (0.038) | (0.038) | (0.0379) | |

| Leverage | −0.6603 *** | −0.6641 *** | −0.6652 *** | −0.7226 *** | −0.7267 *** | −0.7278 *** |

| (0.0355) | (0.0355) | (0.0355) | (0.0377) | (0.0377) | (0.0377) | |

| ROA | 1.759 *** | 1.7537 *** | 1.7567 *** | 1.8532 *** | 1.8469 *** | 1.8503 *** |

| (0.1067) | (0.1068) | (0.1068) | (0.1087) | (0.1088) | (0.1088) | |

| FCF | 0.0444 *** | 0.0444 *** | 0.0444 *** | 0.0455 *** | 0.0455 *** | 0.0456 *** |

| (0.0139) | (0.0139) | (0.014) | (0.0146) | (0.0146) | (0.0146) | |

| SOE | 0.3515 *** | 0.3512 *** | 0.3503 *** | 0.391 *** | 0.3905 *** | 0.3894 *** |

| (0.014) | (0.014) | (0.014) | (0.0156) | (0.0156) | (0.0156) | |

| Constant | −0.7625 *** | −0.799 *** | −0.7953 *** | - | - | - |

| (0.1284) | (0.1294) | (0.1301) | - | - | - | |

| Year FE | Yes | Yes | Yes | Yes | Yes | Yes |

| Industry FE | Yes | Yes | Yes | Yes | Yes | Yes |

| Observations | 29,922 | 29,922 | 29,922 | 29,922 | 29,922 | 29,922 |

| Adj R2 | 0.264 | 0.2637 | 0.2635 | - | - | - |

| Pseudo R2 | - | - | - | 0.1094 | 0.1092 | 0.1091 |

| Dep. Var =ESG_Sino | |||

|---|---|---|---|

| (1) | (2) | (3) | |

| Panel A: Confucianism and media | |||

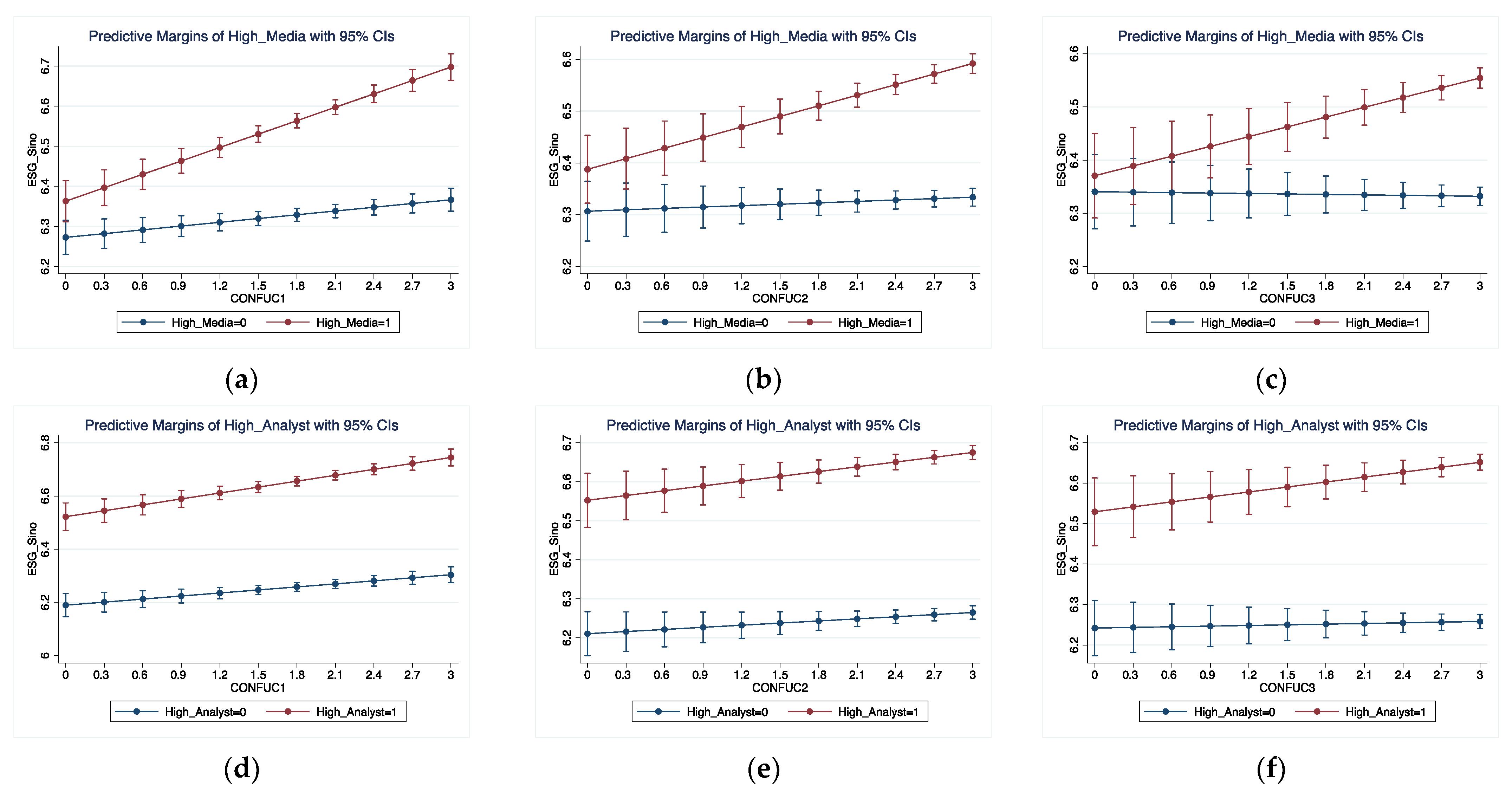

| CONFUC1 | 0.0179 * | ||

| (0.0107) | |||

| High_Media | −0.0661 ** | −0.0921 ** | −0.1274 ** |

| (0.033) | (0.0434) | (0.0523) | |

| CONFUC1 × High_Media | 0.0522 *** | ||

| (0.0161) | |||

| CONFUC2 | 0.0073 | ||

| (0.0104) | |||

| CONFUC2 × High_Media | 0.0452 *** | ||

| (0.0151) | |||

| CONFUC3 | −0.0018 | ||

| (0.0105) | |||

| CONFUC3 × High_Media | 0.0479 *** | ||

| (0.0153) | |||

| CONSTANT | −0.6411 *** | −0.6717 *** | −0.6489 *** |

| (0.1389) | (0.1399) | (0.141) | |

| Controls | Yes | Yes | Yes |

| Year FE | Yes | Yes | Yes |

| Industry FE | Yes | Yes | Yes |

| Observations | 29,581 | 29,581 | 29,581 |

| Adj R2 | 0.2653 | 0.265 | 0.2648 |

| Panel B: Confucianism and analysts following | |||

| CONFUC1 | 0.0215 ** | ||

| (0.0109) | |||

| High_Analyst | 0.0688 ** | 0.0601 | 0.0199 |

| (0.0337) | (0.0448) | (0.0538) | |

| CONFUC1 × High_Analyst | 0.0426 *** | ||

| (0.0162) | |||

| CONFUC2 | 0.0139 | ||

| (0.0101) | |||

| CONFUC2 × High_Analyst | 0.0329 ** | ||

| (0.0155) | |||

| CONFUC3 | 0.0038 | ||

| (0.0102) | |||

| CONFUC3 × High_Analyst | 0.0396 ** | ||

| (0.0156) | |||

| CONSTANT | −0.0574 | −0.0853 | −0.0572 |

| (0.1414) | (0.1427) | (0.1441) | |

| Controls | Yes | Yes | Yes |

| Year FE | Yes | Yes | Yes |

| Industry FE | Yes | Yes | Yes |

| Observations | 29,922 | 29,922 | 29,922 |

| Adj R2 | 0.2671 | 0.2667 | 0.2666 |

| Dep. Var = ESG_Sino | ||||||

|---|---|---|---|---|---|---|

| 2009–2012 | 2013–2020 | 2009–2012 | 2013–2020 | 2009–2012 | 2013–2020 | |

| (1) | (2) | (3) | (4) | (5) | (6) | |

| CONFUC1 | 0.0217 * | 0.0516 *** | ||||

| (0.0127) | (0.01) | |||||

| CONFUC2 | 0.0165 | 0.0357 *** | ||||

| (0.0114) | (0.0095) | |||||

| CONFUC3 | 0.0141 | 0.0268 *** | ||||

| (0.0114) | (0.0096) | |||||

| Constant | 1.0622 *** | −1.5981 *** | 1.0422 *** | −1.6399 *** | 1.0395 *** | −1.6333 *** |

| (0.2292) | (0.1492) | (0.2309) | (0.1505) | (0.2324) | (0.1513) | |

| Controls | Yes | Yes | Yes | Yes | Yes | Yes |

| Year FE | Yes | Yes | Yes | Yes | Yes | Yes |

| Industry FE | Yes | Yes | Yes | Yes | Yes | Yes |

| Observations | 7147 | 22,775 | 7147 | 22,775 | 7147 | 22,775 |

| Adj R2 | 0.2519 | 0.2869 | 0.2518 | 0.2865 | 0.2517 | 0.2863 |

| Dep. Var = ESG_Sino | |||

|---|---|---|---|

| (1) | (2) | (3) | |

| CONFUC1 | 0.0363 *** | ||

| (0.0105) | |||

| SOE | 0.3171 *** | 0.2458 *** | 0.1748 *** |

| (0.0338) | (0.0443) | (0.0534) | |

| CONFUC1 × SOE | 0.0186 | ||

| (0.0165) | |||

| CONFUC2 | 0.013 | ||

| (0.0103) | |||

| CONFUC2 × SOE | 0.0391 ** | ||

| (0.0154) | |||

| CONFUC3 | −0.0021 | ||

| (0.011) | |||

| CONFUC3 × SOE | 0.0536 *** | ||

| (0.0156) | |||

| CONSTANT | −0.7385 *** | −0.7355 *** | −0.6934 *** |

| (0.1296) | (0.1312) | (0.1332) | |

| Controls | Yes | Yes | Yes |

| Year FE | Yes | Yes | Yes |

| Industry FE | Yes | Yes | Yes |

| Observations | 29,922 | 29,922 | 29,922 |

| Adj R2 | 0.264 | 0.2638 | 0.2638 |

| Dep. Var = ESG_Sino | |||

|---|---|---|---|

| (1) | (2) | (3) | |

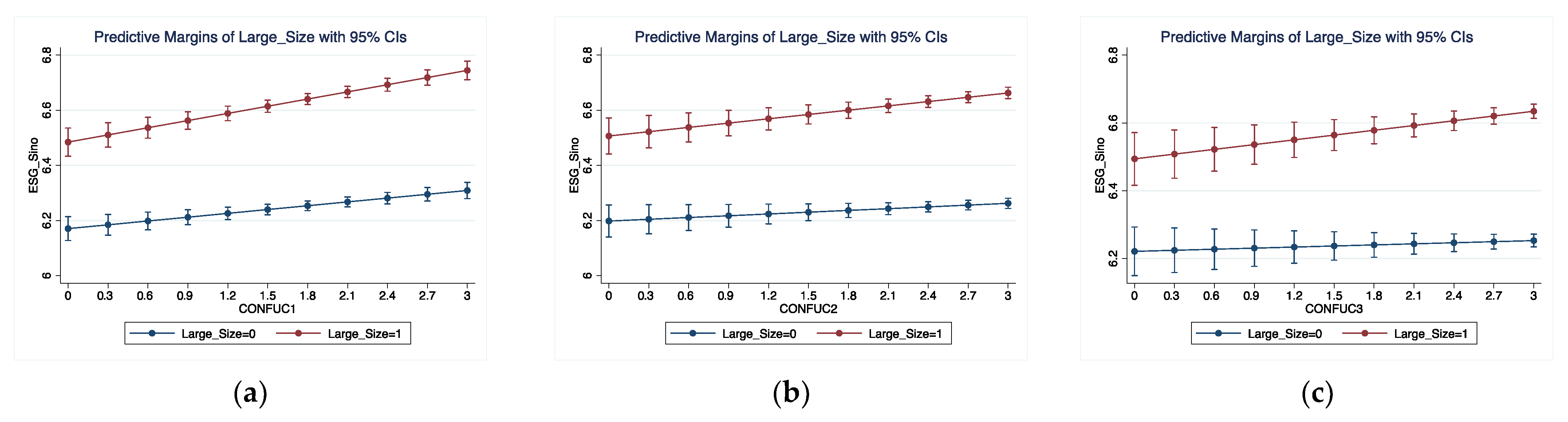

| CONFUC1 | 0.0461 *** | ||

| (0.0108) | |||

| Large_Size | 0.3137 *** | 0.3085 *** | 0.2726 *** |

| (0.0347) | (0.0453) | (0.0544) | |

| CONFUC1 × Large_Size | 0.0406 ** | ||

| (0.0165) | |||

| CONFUC2 | 0.0214 ** | ||

| (0.0104) | |||

| CONFUC2 × Large_Size | 0.0306 ** | ||

| (0.0155) | |||

| CONFUC3 | 0.0106 | ||

| (0.0107) | |||

| CONFUC3 × Large_Size | 0.0363 ** | ||

| (0.0157) | |||

| CONSTANT | 5.8871 *** | 5.9155 *** | 5.9405 *** |

| (0.0309) | (0.0367) | (0.0424) | |

| Controls | Yes | Yes | Yes |

| Year FE | Yes | Yes | Yes |

| Industry FE | Yes | Yes | Yes |

| Observations | 29,922 | 29,922 | 29,922 |

| Adj R2 | 0.2174 | 0.2163 | 0.2161 |

| Panel A: Second stage of the instrumental variable regressions | ||||||

| Dep. Var = ESG_Sino | ||||||

| Model: IV-2SLS | Model: IV-Ordered-Probit | |||||

| (1) | (2) | (3) | (4) | (5) | (6) | |

| CONFUC1 | 0.11 *** | 0.0746 *** | ||||

| (0.0259) | (0.0239) | |||||

| CONFUC2 | 0.0621 *** | 0.0452 *** | ||||

| (0.0146) | (0.0146) | |||||

| CONFUC3 | 0.0563 *** | 0.0396 *** | ||||

| (0.0133) | (0.0133) | |||||

| Constant | −1.2941 *** | −1.3538 *** | −1.3756 *** | - | - | - |

| (0.1472) | (0.1493) | (0.1503) | - | - | - | |

| Controls | Yes | Yes | Yes | Yes | Yes | Yes |

| Year FE | Yes | Yes | Yes | Yes | Yes | Yes |

| Industry FE | Yes | Yes | Yes | Yes | Yes | Yes |

| Observations | 29,420 | 29,420 | 29,420 | 29,420 | 29,420 | 29,420 |

| Adj R2 | 0.2648 | 0.2656 | 0.2654 | - | - | - |

| Panel B: First stage of the instrumental variable regressions | ||||||

| Dep. Var = | CONFUC1 | CONFUC2 | CONFUC3 | |||

| Jinshi | 0.1636 *** | 0.2888 *** | 0.3164 *** | |||

| (0.0028) | (0.003) | (0.003) | ||||

| F-statistic for joint significance of the instruments | 2507.19 | 12892.83 | 3196.32 | |||

| F-statistic p-value | 0.0000 | 0.0000 | 0.0000 | |||

| Observations | 29,420 | 29,420 | 29,420 | |||

| Adj R2 | 0.1692 | 0.3377 | 0.411 | |||

| Panel A: Robustness tests utilizing other Confucius variables based on different distance standards | ||||||||

| Dep. Var = ESG_Sino | ||||||||

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | |

| CONFUC120 | 0.0512 *** | |||||||

| (0.0081) | ||||||||

| CONFUC140 | 0.0483 *** | |||||||

| (0.0079) | ||||||||

| CONFUC160 | 0.0426 *** | |||||||

| (0.0078) | ||||||||

| CONFUC180 | 0.0341 *** | |||||||

| (0.0076) | ||||||||

| CONFUC220 | 0.0333 *** | |||||||

| (0.0079) | ||||||||

| CONFUC240 | 0.0305 *** | |||||||

| (0.0079) | ||||||||

| CONFUC260 | 0.0251 *** | |||||||

| (0.0077) | ||||||||

| CONFUC280 | 0.024 *** | |||||||

| (0.0077) | ||||||||

| Constant | −0.7938 *** | −0.8055 *** | −0.8084 *** | −0.8 *** | −0.8091 *** | −0.804 *** | −0.7948 *** | −0.7935 *** |

| (0.1287) | (0.1288) | (0.1291) | (0.1292) | (0.1296) | (0.1297) | (0.1298) | (0.13) | |

| Controls | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Year FE | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Industry FE | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Observations | 29,922 | 29,922 | 29,922 | 29,922 | 29,922 | 29,922 | 29,922 | 29,922 |

| Adj R2 | 0.2642 | 0.2642 | 0.264 | 0.2638 | 0.2637 | 0.2636 | 0.2635 | 0.2635 |

| Panel B: Robustness checks on province-level Confucius temples | ||||||||

| Dep. Var = ESG_Sino | ||||||||

| (1) | (2) | (3) | ||||||

| CONFUC1_prov | 0.0378 *** | |||||||

| (0.0086) | ||||||||

| CONFUC2_prov | 0.0323 *** | |||||||

| (0.0082) | ||||||||

| CONFUC3_prov | 0.0289 *** | |||||||

| (0.0081) | ||||||||

| Constant | −0.7594 *** | −0.7976 *** | −0.7981 *** | |||||

| (0.1283) | (0.1293) | (0.1296) | ||||||

| Controls | Yes | Yes | Yes | |||||

| Year FE | Yes | Yes | Yes | |||||

| Industry FE | Yes | Yes | Yes | |||||

| Observations | 29,922 | 29,922 | 29,922 | |||||

| Adj R2 | 0.2637 | 0.2637 | 0.2636 | |||||

| Panel C: Alternative measures of ESG | ||||||||

| Dep. Var = ESG_SynTao | Dep. Var = ESG_Wind | |||||||

| (1) | (2) | (3) | (4) | (5) | (6) | |||

| CONFUC1 | 0.0524 ** | 0.075 *** | ||||||

| (0.0244) | (0.0268) | |||||||

| CONFUC2 | 0.0593 *** | 0.0797 *** | ||||||

| (0.022) | (0.0238) | |||||||

| CONFUC3 | 0.049 ** | 0.0864 *** | ||||||

| (0.0233) | (0.0239) | |||||||

| Constant | 0.3347 | 0.2423 | 0.2397 | −4.1648 *** | −4.2768 *** | −4.3056 *** | ||

| (0.5021) | (0.5033) | (0.503) | (0.4932) | (0.4968) | (0.4967) | |||

| Controls | Yes | Yes | Yes | Yes | Yes | Yes | ||

| Year FE | Yes | Yes | Yes | Yes | Yes | Yes | ||

| Industry FE | Yes | Yes | Yes | Yes | Yes | Yes | ||

| Observations | 2903 | 2903 | 2903 | 2606 | 2606 | 2606 | ||

| Adj R2 | 0.179 | 0.1796 | 0.1789 | 0.3318 | 0.3324 | 0.3325 | ||

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Fu, P.; Narayan, S.W.; Weber, O.; Tian, Y.; Ren, Y.-S. Does Local Confucian Culture Affect Corporate Environmental, Social, and Governance Ratings? Evidence from China. Sustainability 2022, 14, 16374. https://doi.org/10.3390/su142416374

Fu P, Narayan SW, Weber O, Tian Y, Ren Y-S. Does Local Confucian Culture Affect Corporate Environmental, Social, and Governance Ratings? Evidence from China. Sustainability. 2022; 14(24):16374. https://doi.org/10.3390/su142416374

Chicago/Turabian StyleFu, Panpan, Seema Wati Narayan, Olaf Weber, Yonggang Tian, and Yi-Shuai Ren. 2022. "Does Local Confucian Culture Affect Corporate Environmental, Social, and Governance Ratings? Evidence from China" Sustainability 14, no. 24: 16374. https://doi.org/10.3390/su142416374