2. Review of the Literature

The most famous typology of competitive strategies was presented by Porter [

1], who distinguished a cost leadership strategy, a differentiation strategy (e.g., competing with high quality or level of customer service), and a focus strategy (focusing on a market niche). Competitive advantage in the concentration strategy is achieved either by differentiation consisting in adapting to the specific requirements of a given market segment, or by cost leadership in this segment [

2].

There is an ongoing discussion about these strategies in the literature. This debate concerns both the problem of choosing one of the best of these pure strategies and the problem of combining these strategies [

3,

4,

5,

6,

7,

8,

9,

10]. Many studies have shown that these strategies are contradictory [

11,

12,

13]. These strategies require different resources and organizational configurations [

8], which is an important argument for choosing one of them. Other authors point out that these strategies are not necessarily mutually exclusive [

14,

15]. According to Salavou, we can observe nowadays the shift from the pure to the hybrid competitive strategies [

16,

17]. On the basis of the Porter model [

1], Salavou identified 16 possible types of hybrid strategies [

16].

Apparel brand owners use reverse auctions, in which suppliers compete for contracts, trying to offer the lowest price, applying clauses that allow for switching from a more expensive supplier to a cheaper one without notice. The differences in the benefits achieved by different links in the supply chains are significant (distributors gain the most). These differences also apply to the size of risk and the durability of the relationship [

18].

The ongoing global economic crisis caused by the infectious disease COVID-19 resulted in shocks on both the demand and supply sides, adversely affecting the global economy [

19]. The COVID-19 pandemic has had a huge impact both on the economy and society. Research has shown that many different industries have been affected by it [

20]. It was predicted that the COVID-19 outbreak would cause the bankruptcy of many big-name brands in many industries because consumers would stay home and economies would be closed [

21]. While some branches struggled, others thrived, such as online entertainment, food delivery, online shopping, online education, remote work solutions, healthcare, drugs, herbs, and vitamins [

22]. The competitiveness of companies enables business and provide opportunities to meet customer and business environment requirements that emerged before the crisis and increased in the COVID-19 era, such as additional digital services and solutions [

23]. The economic crisis that resulted from COVID-19 was on the one hand a challenge, and on the other, marketing and IT innovations emerged that helped in surviving the crisis [

24,

25]. Negative emotions of employees (caused, e.g., by COVID-19) are an obstacle in increasing the company’s innovation, which affects product competition [

26].

Moreover, the crisis caused by the COVID-19 pandemic particularly hit sectors that are not considered essential, such as the fashion industry. The purchase of clothes by consumers is often not related to the need to buy clothes but to the personal pleasure of buying [

27]. During the pandemic, textile companies took up the challenge of creating products that helped professionals in the medical and civil industries (e.g., personal protective equipment, masks, sanitary supplies). To do this, they had to face with supply problems [

28]. Global supply chains have experienced serious problems due to a shortage of raw materials and a shortage of textiles, yarns, fabrics, and other goods. Therefore, some textile companies had to source from suppliers located closer [

29,

30,

31]. When the coronavirus pandemic broke out and, among others, production stopped in Chinese textile companies, global supply chains ran out of textiles and basic products (yarns, fabrics, and other goods) [

29]. Because of this, many companies (for example, the fashion giant Inditex) were nearly paralyzed due to a shortage of raw materials and supply problems [

30]. According to some authors, the COVID-19 pandemic accelerated the trend of deglobalization, which, however, had been observed earlier, since the outbreak of the international financial crisis in 2008 [

32]. Companies that previously recognized the risk of a single-source strategy and built a production network with factories in multiple locations could shift production from one location to another during a pandemic [

33]. Not all authors agree, however, and some believe that the COVID-19 pandemic is unlikely to have had a large impact on supply chain strategies, including location decisions [

34].

In addition to the COVID-19 pandemic, the war in Ukraine is another factor causing enormous problems in the global supply chains [

35], which has increased interest in local supply chain strategies [

36]. Due to the invasion in Ukraine, many international clothing companies that sold their clothing in Russia decided to suspend their activities in this country. On the other hand, the fashion industry is facing increasing price pressure due to the Russo–Ukrainian war. The immediate effect was a significant increase in world oil prices. This means that oil-derived textile fibers, such as polyester, may become increasingly more expensive [

37]. The fashion industry relies heavily on the use of cheap synthetic fibers, especially polyester, in order to drive the fast-fashion business model [

38]. Disruption affects to a great extent the costs, prices, and availability of clothing.

3. Materials and Methods

The author has been conducting research in Polish clothing companies since mid-2017. These were only Polish clothing companies, not branches of foreign companies operating in Poland. The subject of the research was very broad, comprehensively covering issues related to, among others, logistics, supply chains, quality management, and e-commerce. This article presents the results of only part of the research, i.e., the results of research on the elements of competitiveness and competitive strategies of clothing companies and the impact of environmental instability, such as the COVID-19 pandemic, the war in Ukraine, and the increase in fuel prices on their competitiveness. The topic of the impact of disruptions caused by the COVID-19 pandemic on the competitiveness of clothing companies was undertaken by the author in April and November 2021, while the impact of disruptions related to the war in Ukraine and the increase in fuel prices on the competitiveness of companies was from March 2022 onwards.

The research methods used by the author in clothing companies since mid-2017 included interviews with company management and observations.

An interview is a research method defined as a structured interview involving at least two people—the interviewer (researcher) and the respondent. The interview may be standardized (detailed interview questionnaires are used) or unstandardized (conducted according to a general plan, but in this case no sequence in asking individual questions is required, and additional questions can be asked here to deepen the issues), open or hidden interview (depending on whether the respondents were informed about the purpose of the interview), and individual (with one respondent) or group interview (several people participate in the interview at one time) [

39]. According to Wilson [

40], there are three types of interviews: structured interviews, semi-structured interviews, and unstructured interviews. Structured interviews involve asking the same set of questions to each research participant. Semi-structured interviews allow for more flexibility. It is possible to ask additional questions if one wants to deepen a given issue. In case of unstructured interviews, the researcher only has a general idea, and this type of interview is very flexible. When comparing these three types of interviews, the development of results is the most difficult in the case of unstructured interviews. Interviews can be conducted in person, over the telephone, or electronically using a program such as Skype. Using the telephone or Skype is cost effective, as no travel is involved, and this may provide a certain level of comfort to participants. Beck and Manuel [

41] suggest that the interview is better research method when one wants to understand shaded human issues, when questions seem best answered in prose rather than with numbers, and when one want to study a trend.

The interviews used by the author were semi-structured, were open and individual, and were conducted in person and by telephone.

These interviews took place at the headquarters of the surveyed companies in the following cities and towns in Poland: Warsaw, Pruszcz Gdański, Szczecin, Stargard, Łódź, Kraków, Stryków, and Plewiska.

However, since April 2021, due to the pandemic, the main research method was telephone interviews. The supporting research method was the analysis of documents of the listed companies from the clothing industry (current and periodic reports).

The subject of the research conducted by the author in Polish clothing companies, taking into account the duration of the research and the research methods used, is presented in

Table 1. The topics presented in this article and the research methods used to collect the information presented in this article are marked in bold. Conversely, with regard to other issues, about which the author has already written in other articles, there are references to these articles.

Examples of questions that the author asked during the interviews at individual stages of the research are presented in

Table 2. However, these are not all questions, because the specificity of conducting interviews is reacting to respondents’ answers. Therefore, depending on these answers, the author asked additional questions. Thanks to this, it was possible to obtain more detailed information and make sure that the respondent understood the questions. In the opinion of the author, this is the main advantage of an interview in comparison to a questionnaire survey. On the other hand, the main disadvantage is the longer time needed to both conduct interviews and to elaborate on the results of interviews.

In two cases, the companies refused to be interviewed and replies were sent by e-mail.

Various Polish companies from the clothing industry were surveyed, both manufacturing (sewing factories) and distribution companies (e.g., networks of showrooms), but also a company producing materials for production, a subcontracting company dealing with computer embroidery, and companies dealing with the storage and transport of clothes to showrooms and online customers. They were companies of all sizes, both the largest Polish clothing company LPP S.A., which acts globally, and companies operating regionally and locally. They included both supply chain leaders (i.e., companies creating and managing a given supply chain) and participants of the supply chains.

Table 3 shows the number of surveyed companies from these particular groups. Most of the companies surveyed in 2017 were also surveyed in 2021 and 2022. The author tried to maintain continuity, and this was especially successful in the case of most of the companies that are leaders in the supply chains.

In addition to personal and telephone interviews conducted in the surveyed companies, the author used the analysis of documents (reports of listed companies) of the two largest Polish clothing companies (LPP S.A. and VRG S.A.) [

49,

50]. These reports are available on the Internet. The information obtained concerned the impact of the COVID-19 pandemic, the war in Ukraine, and the increase in fuel and energy prices on these companies.

The results of the research are presented in the following order:

the elements of the competitiveness of Polish clothing companies (

Section 4.1);

the competitiveness strategies of Polish clothing companies (

Section 4.2);

the impact of instability in the environment of clothing companies on the ability to compete with the level of logistic customer service (

Section 4.3);

the impact of instability in the environment of clothing companies on their costs and the ability to compete with price (

Section 4.4);

the comparison of the impact of COVID-19, the war in Ukraine, and the increase in fuel and energy prices on the competitiveness of Polish clothing companies (

Section 4.5).

First, the results of research on the competitiveness of Polish clothing companies, conducted before the outbreak of the COVID-19 pandemic, are presented (

Section 4.1 and

4.2). Then, the effects of environmental instability caused by the COVID-19 pandemic, the war in Ukraine, and the increase in fuel and energy prices are presented. These effects relate to two elements of competitiveness: the ability to compete with the level of logistic customer service (as presented in

Section 4.3) and costs, and related clothing prices (as presented in

Section 4.4). Following this, the impact of the COVID-19 pandemic, the war in Ukraine, and the increase in fuel and energy prices on the competitiveness of Polish clothing companies are compared (

Section 4.5)

After presenting the research results, the author presents the recommendations for companies and conclusions.

4. Results

4.1. Elements of Competitiveness in Clothing Companies

On the basis of the research (personal interviews with the management of companies), it can be concluded that the elements of competitiveness in clothing companies differ depending on their role in the supply chain. In terms of their role in the supply chain, companies can be divided into two groups:

A supply chain leader is a company that creates and manages a given chain. In the clothing industry, the leaders are very often distribution companies that outsource the sewing of their own branded clothing to selected sewing factories and then sell this clothing in their own showrooms or to online customers. The author’s research confirms that the largest Polish clothing companies, those that own the most popular Polish clothing brands, are distribution companies, not production companies. In this case, production companies (sewing factories) are only a participant in the supply chains—they sew clothes to the leader’s order and have no influence on the design, manner, place of sale, and the price for the final customer.

However, in some cases, manufacturing companies (sewing plants) are also leaders in the supply chains. In this case, they sew clothes according to their own designs and under their own brand and then sell them to various distribution companies, showrooms, or online customers—in this case, the distribution company is only a participant in the chain. The clothing manufacturing companies (sewing factories) studied by the author, which are leaders in the supply chain, are medium and small companies. In the course of the research, the author also observed the process of change related to the development of such a company—from a company sewing clothes only in its own sewing factory to a company outsourcing sewing of most of the clothes to subcontracting sewing factories (in Poland and in the region).

The competitiveness of clothing companies that are leaders in the supply chains (regardless of whether the leader is a distribution or production company) consists primarily of the following elements:

Product, e.g.,

clothing design (e.g., compliance with fashion trends);

the quality of production (whether the clothes are well sewn, the type of material used);

the width of the assortment;

standard or personalized clothing;

brand of clothing.

Logistic customer service, e.g.,

product availability (number of showrooms, availability of a given type of clothing in the showroom, product availability for the online customers);

the customer service in the showroom.

for the online customers—order processing time, lack of damages of parcels, mistakes, the possibility of returning goods;

price—depends to a large extent on operating costs, which are influenced by the possibility of achieving economies of scale (lower unit costs) and outsourcing production in countries with low production costs;

others—e.g., perception by customers of the company as ecological, caring for sustainable development.

Some of these elements depend directly on the supply chain leader, while others depend indirectly. For example, if a leader of a supply chain is a distribution company that has its own showrooms, and the sewing of clothes is outsourced to other companies, the customer service in the showroom depends directly on that company, and the quality of the garment depends indirectly by choosing a sewing factory. On the other hand, if a leader is a sewing factory that sells its products to selected clothing stores, the quality of the garment depends directly on that sewing factory, and the service in the showroom depends indirectly through the selection of sales outlets where its clothes are sold. From the point of view of the supply chain leader, regardless of whether it is a sewing factory or a distribution company, the final customers decide on the success—whether or not they buy a given item of clothing.

Customer perception of a clothing company as caring for sustainable development is also important from the point of view of competitiveness, as many customers in developed countries care about the natural environment. Industries nowadays also face difficulties due to different environmental policies for the well-being of society and competitive scenarios [

51]. For example, from the environmental point of view, it is better to produce clothes locally than globally, and the production of clothes locally is also more resistant to disturbances caused by instability caused by such factors such as a pandemic.

However, the elements of competitiveness of companies that are not the supply chain leaders, but only actors, are different. The surveyed companies participating in the clothing supply chain are as follows:

sewing plants that sew clothes at the request of a chain leader;

a subcontracting company dealing with embroidery;

companies dealing with logistics services (warehousing and organization of transport to a showroom or to an online customer).

Sewing factories that sew clothes at the request of a chain leader compete with other sewing factories for their customers, i.e., the company that orders the sewing of clothes. In this case, neither the design (because they sew according to the client’s design), nor the material used (because they usually sew from materials provided by the company placing orders), nor the price that the final customer will pay, nor their service in the store depend on the sewing factory.

The factors of competitiveness that affect whether a given sewing plant will win the order or not are primarily the following:

Quality of production—i.e., whether the clothing will be well sewn, in accordance with the design;

Price of the service of sewing clothes;

Order fulfillment time—the time from accepting the order and receiving the material for sewing the ordered clothing;

Location of the sewing factory—distance from the market, which affects the response time to customer needs, but also supports sustainable development.

The surveyed sewing factories, which are not leaders of supply chains and therefore are sewing on orders of other companies, usually have several regular contractors. In addition, depending on their production capacity, they also obtain orders from new contractors. Prior to the COVID-19 pandemic, all of the sewing factories studied by the author were satisfied with the cooperation with the leaders of the supply chains. Thus, the views presented in the literature regarding the instability of relations in the supply chains of clothing and the glaring disproportions in the achievement of benefits between distributors and producers were not confirmed [

18], although of course distributors actually gain the most. It is likely that there are glaring disproportions and unsustainable relations in the case of production in countries with low production costs. It should be added, however, that at the beginning of the COVID-19 pandemic, the satisfaction of sewing factories with cooperation with partners decreased, because due to the decrease in demand for clothing, many clients suspended their cooperation or drastically reduced orders.

Polish sewing factories are of course much less cost-competitive than sewing factories from the Far East countries and are less than sewing factories from Eastern Europe. Due to the production costs, at the turn of the century, many, especially foreign contractors, moved their production from Polish sewing factories to Asian ones. As a result, some companies collapsed, and the production potential of Polish sewing factories began to decline. However, this tendency began to reverse—it turned out that Polish sewing factories can usually compete in terms of quality, and above all, due to their location, the time of order fulfillment. This allows companies ordering production to react faster to market needs and not to create large stocks.

According to the surveyed companies, the quality of production in sewing plants in Poland is high, and defects are rare, as most of the sewing factories work with experienced workers. This has a positive effect on the competitiveness of Polish sewing factories (although, on the other hand, it may cause a problem with employees in the future—in Poland, young people do not want to work as sewing workers, and there are currently no schools in Poland educating sewing workers).

Any defects in the sewn clothing may result, for example, from a defect in the fabric, which a sewing person will not notice, but it is usually picked up during the inspection in the company, before the clothing is delivered to a client. The surveyed companies also mentioned individual cases of production errors reported by clients:

too narrow elastics in the pants in the entire batch of products sewn (in this case, the fault was on the side of the sewing factory, because although the material was supplied by the company ordering the sewing of the garment, the accessories, such as rubber, were purchased by the sewing company);

packing the garments in too large cartons, the size of which did not match the devices in the client’s automated warehouse (the client charged the costs both to the company that supplied cardboard boxes other than the ones ordered and to the sewing factory that did not notice it).

Outsourcing clothing production in Poland also has an impact on sustainable development. Sewing factories located in Poland are more competitive in this respect than sewing factories in the Far East, e.g., in Bangladesh. Location of production of clothing in the so-called countries with low production costs is associated with environmental risk (transport of clothing over long distances on a mass scale, short use time of cheap clothes sewn in countries with low production costs) and, often, social risk (non-compliance with human rights, labor law, health and safety rules, etc.).

In the surveyed company, which produces fabrics (knitwear) for the needs of clothing companies, the main factors of competitiveness are the quality of the knitted fabric and the level of logistic customer service (speed of order fulfillment, the possibility of ordering small amounts of fabric). The quality of the knitted fabric depends on the quality of the raw material (yarn), the production process of the knitted fabric (because despite the good quality of the yarn, production errors may occur), and the quality of the knitted fabric finish (i.e., dyeing). The surveyed company produces high-quality knitwear. The order fulfillment time it offers is shorter than when buying materials from countries with low production costs (e.g., Bangladesh, Taiwan), where it would take about three months. When buying from the surveyed company, a small amount (e.g., 100 kg of a given color) can be ordered, whereas, in the case of import, for example, a ton would have to be ordered. On the other hand, the cost of purchasing knitted fabric in the surveyed company is much higher than in countries with low production costs, even after taking into account the costs of transport and maintaining inventories.

Among the surveyed logistics companies dealing with logistics support for the distribution of clothing, one dealt with the storage of clothing and organization of transport to showrooms, whereas the other dealt with Internet customers. The elements of competitiveness of these companies include, apart from the price, also logistic customer service, e.g., no mistakes in delivery, no damage to the clothes. The absence of mistakes regarding the goods (type, size, color, etc.) is especially important when delivering to an online customer, as well as the order processing time and handling returns.

The above-mentioned general elements influencing the competitiveness of clothing companies may be more or less important depending on the chosen competitive strategy of a given company. Later in the article, attention will be focused on companies that are leaders in supply chains.

4.2. Competitiveness Strategies of Polish Clothing Companies

The competitive strategies of supply chain leaders in the garment industry can be classified according with the three classic competitive strategies [

1]:

cost leadership strategy;

differentiation strategy—e.g., specific quality or level of customer service;

focus strategy—focusing on a market niche.

Among the surveyed companies, these were not always pure strategies.

The cost leadership strategy can be successfully applied by the largest companies that operate globally and sell standard goods. These companies operate on a large scale, thanks to which they obtain the economies of scale reduction of unit costs. In the clothing industry, the largest companies are distribution companies that are leaders in supply chains, which do not sew clothing themselves but deal with distribution and sale, ordering production to sewing plants. Companies applying a cost leadership strategy outsource production to countries with low production costs, such as Bangladesh or India, thanks to which they have low unit costs of purchasing clothing. Transporting clothes from the Far East to the European market involves long-distance transport, and therefore it is more expensive than transporting clothing that is sewn in Europe. However, large-scale companies can negotiate favorable shipping rates. These companies also achieve economies of scale in warehousing, often investing in large, modern distribution centers. They also try to reduce the cost of maintaining inventories, and thus they place great emphasis on fast turnover. These kinds of companies deliver goods to stores frequently in small quantities, according to the demand in a given store, and apart from this, organize numerous promotions. Thanks to their low unit costs, such companies can offer end customers moderate or low prices while achieving financial results that allow for further development. Of course, this does not mean that these companies do not take into account the quality of products and level of customer service. Their customers usually care about the style of clothing and compliance with fashion trends, hence the great importance attached to design quality. However, since it is relatively cheap clothing, bought for one season or for the first wash, customers care less about its durability and agree to the poorer quality of the material.

The diversification strategy applies to those companies that want to distinguish themselves from competitors, e.g., with a high quality of products and/or a high level of customer service. These companies purchase good-quality materials and accessories, and thus they incur higher purchase costs than the companies competing with price. They carefully choose sewing plants, guided by the quality of workmanship and striving for permanent cooperation with sewing plants. They do not outsource production to countries with low production costs, but locally (in Poland) or regionally (in Eastern Europe), not only because of the quality, but also because of the quick response time to market needs. However, this does not mean that they may not pay attention to costs. In order to reduce costs, they sometimes outsource sewing clothes in European countries where sewing costs are lower than in Poland. Before the outbreak of the war in Ukraine, it was very often Ukraine, because of the short distances, possibility of frequent contacts, and acceptable production quality. The small distance between the place of production and the market is important not only for the response time to market needs but also for transport costs. In the case of competition with quality, the transport of certain types of clothing (jackets, suits, dresses) from the sewing plants to the distribution center and to the showrooms is carried out on hangers, being more expensive than the transport of folded clothing, but the clothing reaches the store and can be sold in better condition.

The concentration strategy is applied by small clothing companies, focusing on a market niche, e.g., products of a certain type, for a specific group of customers. It may be non-standard clothing, e.g., tailor-made suits, according to a design tailored to a given client and using materials selected by them. It may be a specific type of clothing, e.g., medical clothing for hospitals. Companies with this strategy of competitiveness are both companies that sew clothes themselves, as well as companies that outsource sewing clothes to other companies.

Sometimes one company has several brands of clothing, and some of them are more exclusive, sewn with better quality materials, produced in Europe and sold at higher prices, while others are lower quality and cheaper, sewn in Southeast Asia.

Among the surveyed companies, the cost leadership strategy, although not in its pure form, is used by the largest Polish clothing company LPP S.A. It is a distribution company with over 2000 showrooms in approximately 30 countries in Europe and the Middle East. The company is constantly entering new markets, expanding the network of showrooms, and intensively developing distribution to online customers. It orders the production of clothing according to its own designs under its own brands to various sewing factories located mainly in countries with low production costs, but also in Poland and other European countries. By operating on a large scale, the company achieves the economies of scale. Therefore, it sells its clothing either in a moderate price range or in the affordable fashion retail segment (inexpensive retail).

LPP S.A. competes not only by offering customers products at attractive prices, but also

The quality of the design—paying great attention to the design of fashionable clothing in their own design studios;

The spatial availability of products—thanks to a dense network of stores in Poland and frequent replenishment of stocks in showrooms;

Short order processing time for online customers—for this purpose, a number of investments in warehouses (fulfillment centers) were made, from which deliveries are made to online customers in various countries;

“eco-friendliness”.

The quality of sewing clothes depends on the sewing plants in which the production is outsourced. LPP controls the quality of products directly at the manufacturers because there is a LPP representative office both in Bangladesh and China. The employees working there visit producers and, apart from quality control, are responsible for sourcing suppliers; supporting individual production stages; and controlling compliance with safety rules, appropriate working conditions, and compliance with human and labor rights. The quality control department is also located in the company’s distribution center in Pruszcz Gdański in Poland. Damage to goods during transport is very rare. In the case of transport by sea, this may be due to monsoon rains off the southern and eastern shores of Asia. More serious quality deficiencies, preventing products from being shipped to stores, do not occur more often than 2–3 times a year. If the defects are the fault of the manufacturer, the goods must be shipped back to the Far East. In the case of smaller errors, a discount is obtained from the manufacturer and the goods are sold at a lower price. Moreover, this type of disadvantages is a negligible percentage of sales.

The surveyed company was also the second largest Polish clothing company, namely, VRG S.A. It is a company that distributes several clothing brands (Vistula, Bytom, Wólczanka, and Deni Cler Milano) and also distributes jewelry. The company has an extensive network of stores in Poland, and it also distributes to online customers. The company tries to compete with the quality of its products, supplying itself with high-quality fabrics and sewing accessories, increasing the cost of clothing production. In addition, most of the clothes are sewn in sewing factories in Poland, which means that the costs are much higher than in the case of companies producing clothes in countries with low production costs. The choice of a sewing factory in Poland results from the desire to care for the quality of sewing, but also due to ensuring the appropriate quality in the transport of clothing. For example, suits or jackets ordered by this company are transported by trucks on hangers to the distribution center, not by sea, being stored in containers.

Of course, in addition to competing in quality, the company also pays attention to other elements, e.g., spatial availability and short delivery times to online customers. The competitive strategy used by this company is a diversification strategy (the company wants to stand out with quality), although it is also not a pure strategy. This is because they contain some elements that are included in the cost leadership strategy, first of all acting on a large scale, and thus achieving economies of scale. Transport costs are not high, because thanks to outsourcing the production in the local sewing plants, the distances are not large. As a result, product prices are not high, despite having good quality.

Comparing the competitive strategies of the two mentioned companies, the company LPP S.A., thanks to the cost leadership strategy, has gained many customers, and despite its competitive prices, it has financial means for its expansive development. As it is a very large company, it also achieves economies of scale, especially in logistics (warehouse and transport costs). Moreover, thanks to the fact that the production of most of its clothes is located in the Far East, it has also low costs of production. Conversely, the company VRG S.A. tries to compete primarily with the quality of its products, and thus its clothing is more expensive. However, for both companies, these are not pure strategies.

The example of the largest Polish clothing companies thus shows that it is possible to successfully incorporate elements of the differentiation strategy into the cost leadership strategy and vice versa. There are solutions that allow both for the reduction of costs and the improvement of the level of logistic customer service. For example, in the case of LPP S.A., one such solution was to change the flow of clothes from push to pull. Clothing is not being pushed from the distribution center to the showrooms, but instead, demand is pulling the flow of clothing. Consequently, garments are delivered to showrooms often in small quantities on the basis of actual demand rather than forecasts. Thanks to this, for LPP S.A., the level of inventory in the entire distribution system has decreased (lower costs), and at the same time, in the showrooms, there are products that customers look for (better logistics service). Pull flow of goods is an element of many modern concepts, such as quick response, ECR, or just-in-time. It is used in the most famous clothing companies in the world, such as Inditex or Benetton, where the pull flow is used over a longer distance (not only from the distribution center to the showrooms, but from the sewing firms to the showrooms). Such solutions allow for a reduction in total costs while improving the level of logistic customer service. In this case, there is no longer “trade-off” but “trade-up” between the costs and the level of logistics service. Therefore, one can successfully incorporate elements of a differentiation strategy into their cost leadership strategy and vice versa.

According to Porter, the third strategy is the concentration strategy. Among the surveyed companies, an example of a company that successfully applies the concentration strategy is the Macaroni Tomato company, which sells suits, sewn according to its own designs, mainly made to measure or made to order. Competitive factors in this company are as follows:

good price–quality ratio;

own brand;

own innovative projects;

the possibility of sewing a suit for a specific customer (in the case of both made-to-measure and custom-made suits, the customer can choose the fabric and accessories, and in the case of made-to-measure suits, an individual project can also be undertaken);

good fit of a tailor-made suit thanks to a two-stage system of fittings;

high-quality workmanship—thanks to cooperation with manufacturers who have the appropriate technology (e.g., laser cutting dies) and the use of high-quality sewing accessories;

high quality customer service—offering professional knowledge and advice on the selection of a suit.

The second example of a company successfully applying the concentration strategy is the small clothing company Keja, which sews specialist clothing (medical, cosmetic, and protective), mainly on orders, both for groups, e.g., for hospitals, as well as for individuals. The company operates in its market niche and competes primarily in terms of quality, both in terms of product and customer service:

designing clothes in accordance with changes and fashion trends (the company’s original clothing collection is presented at exhibitions and medical fashion shows);

the possibility of production on an individual order (the company is able to both make a customer’s design and prepare its own, being unique for people of all types of figures);

the width of the assortment (the fixed assortment is 50 products in 15 colors, in all sizes);

adjusting sizes for each customer, which is measured before the start of production, thanks to which a customer has a sense of uniqueness, the clothes fit well, and the company saves on the costs of corrections, maintaining the quality management postulate—“doing everything right the first time”;

high quality of all materials and accessories from which the garments are sewn (quality is the main criterion for selecting both suppliers and subcontractors, e.g., embroidery plants);

cooperation only with experienced sewing workers;

inspection of each sewn garment before delivering it to the customer;

timely execution of orders (orders up to 10 items are processed within 48 h);

free alterations and repairs of the clothes, e.g., in the event that, for example, the figure of a given person changes, or a zipper breaks.

Therefore, the surveyed companies use various competitive strategies—both the cost leadership strategy and differentiation (although these are not pure strategies) and concentration (focusing on a market niche).

4.3. Impact of Instability in the Environment of Clothing Companies on the Ability to Compete with the Level of Logistic Customer Service

Research conducted by the author in clothing companies indicates that disruptions caused by the COVID-19 pandemic, the war in Ukraine, and the rise of the fuel costs primarily affected two elements of competitiveness:

the level of logistics service offered to customers, primarily in terms of the availability of clothing (presented in

Section 4.3);

costs, which affect the price for the end customer (presented in

Section 4.4).

However, the disruptions in the surveyed companies did not affect the possibility of competing with the product, e.g., the quality of the clothing design, the production quality, and the width of the assortment. Therefore, this issue is omitted further in the article.

Disruptions, especially the COVID-19 pandemic, affected the availability of clothing, as lockdowns forced the closure of brick-and-mortar clothing stores. In Poland, this mainly concerned stores located in shopping malls. Most of the showrooms of the largest clothing companies are located in these centers.

There was then a sharp decline in apparel sales, around double the overall decline in sales at that time. The reasons for the sharp drop in demand for clothing at the beginning of the pandemic could have been not only the closure of clothing stores in shopping malls but also the sanitary regime in clothing stores outside shopping malls (which, due to the limitations of the number of customers in the store, meant waiting in a line in front of the store), remote work, and fear of leaving home. Later, however, the demand for clothing began to grow due to the rapid expansion of e-commerce, the end of the lockdowns, and an improvement in consumer sentiment. This increase was greater than the overall increase in sales. The dynamics of retail sales of clothing as compared to the dynamics of sales of all products are presented in

Table 4.

At the beginning of the COVID-19 pandemic, clothing was available mainly on the Internet, which is why this sales channel developed significantly during this period. Therefore, the competition was won by those companies that already developed e-commerce before the pandemic, while in companies that did not have such distribution channels, sales decreased. The following statement from 2021 of the director of a company with its own sewing factory in Poland, selling clothing in its own showroom and other stores, is typical: “During the pandemic, the company recorded a significant drop in demand—both from other stores and in its own store, although it is not a store in a mall center. The pandemic has contributed to the attempt to sell clothes over the Internet—but these are only the beginning.”

However, even companies that had well-developed delivery logistics to an online customer, experienced difficulties at the beginning of the pandemic due to the sharp increase in online orders. Initially, this contributed to the deterioration of the quality of service in this sales channel, e.g., to the extension of the order fulfillment time and to the increase in the number of errors. This resulted from the fact that deliveries to online customers began to be made from those warehouses, from which, before the pandemic, deliveries were made only to stores. However, the specificity of deliveries to stores is different than to online customers to whom individual items of clothing are delivered—there can be no mistake as to the type of clothing, size, or color, and deliveries are less regular and less predictable. Deliveries to online customers require a warehouse with appropriate equipment and prepared employees. In addition, there are more returns from customers buying online than in brick-and-mortar stores, and the returned goods must be properly prepared for resale, which also requires adequate resources. Therefore, it is not surprising that the rapid development of this distribution channel initially contributed to the deterioration of the quality of deliveries to the Internet customers.

In response to this, many companies have changed the organization of deliveries to e-commerce customers. Some of companies, anticipating that the increase in online sales would be permanent, expanded the network of warehouses to meet the needs of online customers. Usually, large companies have been better at this than small ones.

For example, LPP S.A. accelerated the planned investments, as a result of which the deliveries of clothes to online customers began to be performed out from three new warehouses—in Gdańsk in Poland (for online customers from Poland), and in Slovakia and Romania (for online customers outside Poland). Selected shops of LPP S.A. were also involved in servicing online customers. Although it was not possible to buy clothes from there due to the lockdowns, it was possible to collect clothes ordered online.

The availability of clothing for the end customer was also affected by disruptions in procurement and production. The disruptions caused by the pandemic hit harder the companies outsourcing production to low-cost countries. There were periodic disruptions in the supply of clothing, caused, for example, by disruptions by the manufacturers or quarantine in the port or on the ship in which the goods were transported. Companies that manufacture in Poland experienced less disruptions, but they occurred both in the supply of materials and packaging, as well as in production in Poland (e.g., quarantine of employees).

Among the Polish sewing factories surveyed, some did not observe any greater absenteeism of employees. Some, however, experienced a periodic lack or reduction in production capacity due to COVID-19 illness or quarantine among employees. In this case, they were looking for subcontractors, both in Poland and in Eastern European countries, such as Belarus or Ukraine.

Due to its proximity and relatively low labor costs, Eastern Europe was perceived as a good location for production. Although the Polish companies were aware of the unstable political situation, many of them, being leaders in supply chains, outsourced the production of clothes to sewing factories in Eastern Europe (Ukraine, Belarus). In comparison to the Polish sewing factories, production costs in Eastern Europe are lower, while the delivery time is much a shorter than from the suppliers in the Far East. Similarly, companies from Western Europe ordered production in these countries.

After the war began, Polish companies suspended cooperation with Ukrainian sewing factories for safety reasons and tried to establish cooperation with Polish sewing factories, but this took time. This caused temporary problems with the availability of the clothing of these companies on the market, influencing their competitiveness. The companies that had previously cooperated with various sewing factories, not only in Ukraine but also with local ones, managed better in this situation.

From the point of view of Polish sewing factories that are not leaders in the supply chains, the beginning of the COVID-19 pandemic in many cases resulted in a dramatic decrease in the number of orders, even by more than one-half. As sales of clothing decreased, the supply chain leaders did not outsource their production. On the other hand, the war in Ukraine increased the competitiveness of Polish sewing factories sewing clothing to orders of other companies because they were ordered by companies that previously outsourced production to sewing factories in Ukraine (not only Polish companies, but also those from Western Europe).

The war in Ukraine also caused Polish clothing companies to withdraw from the Russian market. The largest Polish clothing company, LPP S.A., first suspended its operations in Russia and then it withdrew completely, selling its showroom network, distribution center, and fulfillment center.

Instability in the environment influenced then to a varying degree the ability to compete with the level of logistic customer service. It depended mainly on the level of e-commerce development in a given company before the COVID-19 pandemic, the possibility of developing infrastructure dedicated to e-commerce service, and the location of production (in countries with low production costs, and in Eastern Europe where disruptions were greater than in the case of the local production). The problems resulting from the instability of the environment were quickly overcome by companies that had already diversified their activities and were more flexible.

4.4. The Impact of Instability in the Environment of Clothing Companies on Their Costs and on the Ability to Compete with Price

Instability in the environment affected not only the level of logistics services offered to customers but also costs, which had an impact on the prices of clothing. Price-competing apparel companies, which outsourced production in low-cost countries, experienced an increase in the cost of purchasing not only clothing but also materials and packaging. During the COVID-19 pandemic, shipping rates also increased. Many clothing companies, which feared delays in deliveries and further price, increased the inventory levels. Because the various types of costs increased, some companies raised the prices of clothing, and thus their price competitiveness decreased.

This does not mean that the large companies that use the strategy of cost leadership failed. Although the effectiveness of the production strategy in low-cost countries decreased, it is still cheaper than outsourcing production locally, despite the increase in both logistics and production costs. During the COVID-19 pandemic, the costs of companies producing locally also increased.

The following is a statement from 2021 by the owner of a large sewing factory, a supply chain leader: “The pandemic, due to the increase in employee absenteeism (employees on layoffs, in quarantine), caused problems both in production and financial problems. As a result, competitiveness is deteriorating—companies pass these costs on to their customers.” This sewing plant started to cooperate with subcontractors before the pandemic and during the pandemic due to the costs and lack of production capacity this cooperation developed. Currently, the company sews only premium brands in its own sewing plants, while others are outsourced to other companies—local (Polish) or regional (in Belarus). This company does not exclude cooperation with subcontractors from countries with low production costs.

A similar cost increase effect was caused by the war in Ukraine. Polish companies had to suspend cooperation with sewing factories located there. Therefore, the war in Ukraine had a negative impact on the ability to compete with price for these companies, because in Poland, these companies pay more for sewing clothes. The change of suppliers from Ukrainian to Polish ones did not affect the deterioration of the quality, but when it comes to the speed of response, it even improved—the delivery time from Polish sewing factories to the Polish market is shorter. Therefore, these companies can still compete with the quality and time of order fulfillment.

Another factor that influenced costs, and thus the ability to compete with price, was the increase in transport costs. During the COVID-19 pandemic, shipping costs increased, affecting companies that outsource clothing production to the Far East. In Poland, after the start of the COVID-19 pandemic, the costs of road transport did not change rapidly, while a sharp increase occurred during the war in Ukraine that was mainly due to the sharp increase in fuel prices. Changes in the wholesale prices of EURODIESEL in Poland in 2020–2022 are presented in

Table 5. Of course, fuel prices increased not only in Poland but all over the world due to the increase in the price of crude oil.

In companies ordering production in countries with low production costs, the share of transport costs in total costs is higher than in companies operating locally. Increasing oil prices reduced the effectiveness of global supply chain strategies. However, according to the results of the calculations, despite the increase in the transport costs, the production in the Far East is still profitable [

54]. However, thus far, the sharp increase in transport costs has not changed the purchasing policy and has not significantly increased the production of clothing in Poland.

The following is a statement by the director of logistics and quality control of one of the surveyed clothing companies, who are the supply chain leaders, at the end of March 2022: “Price changes in transport are caused mainly by fuel price increases, which are caused by the war. But in logistics services there are also drastic increases in heating and electricity costs—generally following this galloping inflation. As of today, however, it has not resulted in changes of our purchasing policy and increase of production in Poland.”

The sharp increase in fuel and energy prices also has increased the cost of transport in companies producing in Poland. Moreover, all companies have noticed an increase in heating and energy costs, e.g., in warehouses or in production. Increased fuel and energy costs translate into an increase in the prices of all goods and services, e.g., materials and additives for the production of clothing; packaging; and services, e.g., transport or logistics. Companies operating globally as well as regionally and locally were affected by this.

The following is a statement by the director of one of the surveyed clothing companies at the end of March 2022: “There is no company that has not ‘come’ with a price increase to our company—for everything from logistic services to cardboard boxes.” Due to the increase in the prices of goods and services, companies have to increase the prices of clothing (less ability to compete with the price). The following is a statement by the owner of a knitwear company in Poland at the end of March 2022: “Fuel and gas prices have definitely influenced higher production costs, which translates into higher prices of the final product.” Another possibility is to look for cheaper materials and accessories (less ability to compete with quality). With little opportunity to increase the sale prices of clothing and reduce costs, companies will have lower margins.

4.5. Comparison of the Impact of COVID-19, the War in Ukraine, and the Increase in Fuel and Energy Prices on the Competitiveness of Polish Clothing Companies

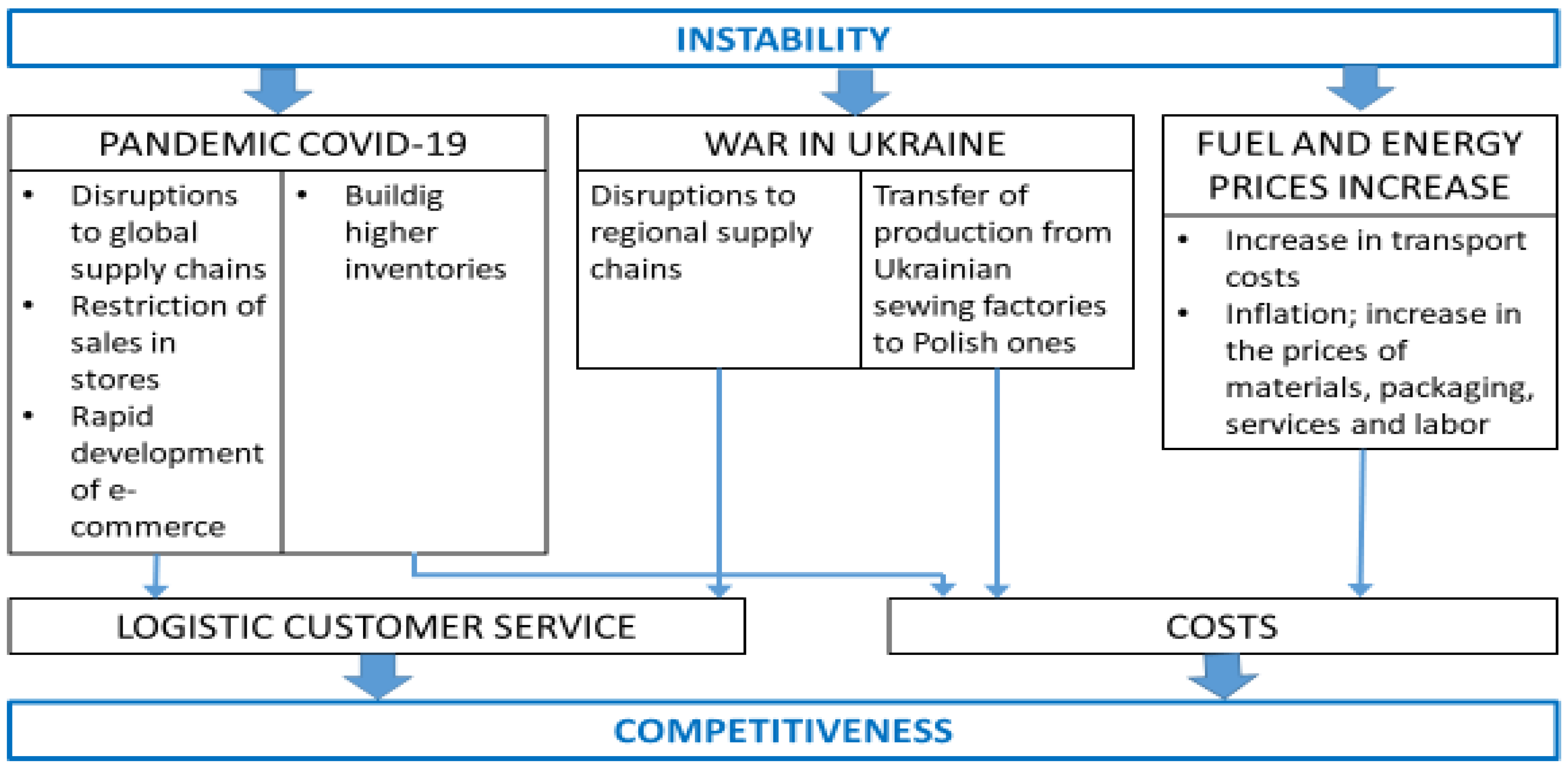

Recent instability in the business environment has been caused by three main factors: the COVID-19 pandemic, the war in Ukraine, and the sharp increase in fuel and energy prices, affecting the competitiveness of clothing companies by affecting the level of customer logistics and costs (

Figure 1).

This impact manifested itself to a varying degree in different types of clothing companies. The sharp increase in the demand for deliveries to online customers, observed at the beginning of the pandemic, affected supply chain leaders who often had to change their distribution strategy, as well as logistics companies that were to handle the increased demand for clothing from online customers. Lockdowns in shopping malls were mainly felt by the largest clothing companies that have their showrooms there. This also affected sewing factories to which these companies outsourced production. Disruptions in global supply chains affected the leaders of these chains (i.e., companies ordering sewing clothes in Bangladesh), but also companies that are only participants of global chains (e.g., Polish sewing plants sewing clothes ordered by other companies from materials supplied from countries with low production costs). In response to these disruptions, higher stocks have to be built up at these companies. The war in Ukraine meant that the leaders of regional supply chains with sewing factories in Ukraine had to start outsourcing production in Polish sewing factories. The sharp increase in fuel and energy prices contributed to a sharp increase in transport costs that was felt mainly by leaders of global supply chains, but also by other companies. However, as it entailed inflation and an increase in the prices of materials, packaging, services, and labor, all companies felt this. These dependencies are presented in

Table 6.

5. Conclusions

The conducted research refers to and develops Porter’s theory of competitiveness [

1]. They empirically confirm that the strategies of successful companies can be classified as one of the three classic strategies: cost leadership, diversification, or focus strategy. The surveyed largest Polish clothing companies apply either a cost leadership strategy or a diversification strategy. However, in the studied large companies, neither the cost leadership strategy nor the diversification strategy was a pure strategy, but elements of the second strategy were visible in them. The author believes then that it is possible to successfully integrate elements of the cost leadership strategy into a differentiation strategy and vice versa.

Although the research concerns Polish clothing companies, according to the author, it can be translated into other countries or industries. The possibility of successfully incorporating elements of the differentiation strategy into the cost leadership strategy and vice versa results from the fact that nowadays cost leadership does not have to be associated with lowering the quality and logistics service, and the strategy of differentiating from competitors with high quality or high level of logistics services does not have to result in the high levels of cost. The author believes that many contemporary concepts, such as TQM, quick response, ECR, or lean management, allow for the reduction of total costs without reducing the level of logistic customer service and quality, or even help to improve them. Thanks to this, there will be no “trade-off” but “trade-up” relationship between costs and quality or between costs and the level of logistics service. Thus, it is possible to successfully apply the cost leadership strategy while incorporating elements of the diversification strategy and vice versa—such as what the largest Polish clothing companies do.

Conversely, the research fully confirmed the theory, according to which the competitive advantage in the focus strategy is achieved either through diversification or through cost leadership in a market segment. The surveyed small companies that successfully applied the concentration strategy sought to diversify their offer through high quality and high level of service.

The author’s research also refers to the previously conducted research on the relationship in supply chains between a distributor and a clothing manufacturer (sewing factory). The research confirmed that the largest clothing companies that are leaders in supply chains are distribution companies. However, it was not confirmed that the disproportions between the distributor and the manufacturer are significant, and the relations are not durable—before the COVID-19 pandemic, all Polish sewing factories participating in the supply chains were satisfied with the cooperation with the leader. However, this situation was changed by the pandemic, because at that time, even long-term contractors suspended their cooperation or significantly reduced the number of orders. However, it was related to the decrease in demand on the garment market.

On the basis of the conducted research, it can be concluded that the instability in the environment has a significant impact on the competitiveness of clothing enterprises. This applies both to companies that are leaders in the supply chains, as well as the participants in these chains. The COVID-19 pandemic had a negative impact on nearly all of the apparel companies surveyed. Among the surveyed companies, only the company sewing medical clothing did not notice any negative impact. On the other hand, the war in Ukraine had a direct negative impact only on some Polish companies, namely, those that did business in Eastern Europe. On the other hand, the war in Ukraine caused in some cases the relocation of production from Ukrainian sewing firms to the Polish ones, and thus Polish sewing factories, which sew clothes on order, are now more competitive.

The impacts of instability in the environment of clothing companies on their competitiveness are as follows:

In the initial period, the COVID-19 pandemic had a negative impact on the level of logistic customer service, especially in Poland:

lower availability of clothing (closure of stores in shopping malls, where showrooms of the largest clothing companies are located; problems with deliveries from countries with low production costs, where production is mainly outsourced by companies competing with price);

lower quality of deliveries to online customers (due to the rapid development of this distribution channel).

The war in Ukraine also caused a temporary deterioration in the availability of clothing in the case of clothing companies that outsourced production to Ukraine because they had to suspend cooperation with Ukrainian sewing factories and establish with Polish companies.

Both the COVID-19 pandemic and the war in Ukraine, as well as the increase in fuel and energy costs, contributed to an increase in both logistic and production costs, which in many cases had an impact on increasing the price of clothing for the final customer.

The COVID-19 pandemic and the increase in fuel prices reduced the efficiency of outsourcing of the production of clothing in low-cost countries, but in the surveyed companies, this did not change the location of production from global to local.

Companies that previously outsourced the production of clothing in Eastern Europe now outsource their production to Polish sewing factories, which increased their costs and reduced their price competitiveness.

The war in Ukraine increased interest in Polish sewing factories, both on the part of Polish and foreign companies, which improved the competitive position of Polish sewing factories sewing clothing on demand.

Instability in the environment influenced, to varying degrees, the ability to compete with the level of logistic customer service, especially with regard to the availability of clothing and the quality of online customer service, as well as the ability to compete on price. This mainly depended on

the share of e-commerce in distribution before the COVID-19 pandemic—companies that already had a well-developed channel before the pandemic were less affected by the sudden closure of brick-and-mortar stores and a sharp increase in the number of online orders;

possibilities of developing warehouse infrastructure and increasing employment dedicated to e-commerce services;

location of production and supply—smaller problems were encountered by companies producing and sourcing in Poland, while in the case of production and supply in countries with low production costs, the problems were greater, which resulted not only from disruptions in production, but also in transport; even greater problems arose in the case of companies outsourcing the production of clothing to Ukraine in connection with the war in Ukraine.

The problems resulting from the instability of the environment were sooner overcome by those companies that were more flexible and had diversified their activities earlier. The problem of closing stores and the resulting deterioration in the availability of clothing was quickly solved by companies that had previously diversified their sales channels, selling both in stores and through e-commerce.

Similarly, companies that had previously cooperated with various sewing factories, not only in the Far East or Ukraine but also with local ones, were able to change the supplier (sewing factories) faster.

Therefore, the research confirmed the significant impact of instability in the environment on the competitiveness of enterprises in the clothing industry, primarily in terms of the ability to compete with the level of logistic customer service and price. Instability in the environment did not affect the ability to compete with the quality of clothing in the surveyed companies.

The research was conducted only in one country (Poland) and only in one industry (the clothing industry). Focusing on one area and one industry allowed for the obtaining of accurate results. On the other hand, however, this was a limitation as there was no empirical evidence that similar results could have been obtained in other industries and in other countries.

The main used method was the interview, which allows for obtaining detailed results. However, on the other hand, this is a time-consuming method, and it is difficult to develop the results. Because of this, fewer companies can be surveyed in this way.

The author has been conducting research in the clothing industry since mid-2017, i.e., for over 5 years. However, the study of the impact of environmental instability on competitiveness has been carried out by the author for about one and a half years. Thus, it is not known yet what the long-term impact will be.

The author proposes the following directions for further research in this field:

re-interviewing the surveyed companies in order to determine the long-term impact of environmental instability on their competitiveness and also in the case of further possible disruptions occurring;

also conducting similar studies in enterprises in other branches of the economy or located in other countries and providing a comparison with the studies presented in this article;

using the survey method to obtain results in more companies.

{kind=link}